31

| Date post: | 08-Apr-2018 |

| Category: |

Documents |

| Upload: | babitabasu |

| View: | 219 times |

| Download: | 0 times |

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 1/31

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 2/31

India Social Media Survey Edition 2 3India Social Media Survey Edition 2Log on to: www.rocketalk.com or wap.rocketalk.com

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 3/31

India Social Media Survey Edition 2 5India Social Media Survey Edition 2

CONTENTS

Foreword by Rajesh Lalwani 5

Foreword by Karthik Nagarajan 7

India Social Media Report, Edition 2 9

itimes.com case studies 46

Guest article: N Madhavan 48

Guest article: Anurag Batra 50

Guest article: Ashwani Singla 52

Guest article: Rajika Talwar 55

Guest article: Hassan Mirza 57

Guest article: Mohit Gundecha 59

#24 Adchini, Lower Ground(Enter from Sarvodaya Enclave), New Delhi 110 017Landline: +91 11 41829475M: +91 9910034330Email: [email protected]

India Social Media Survey Edition 2 - December 2010Price Rs.10,000/-

Even as Blogworks India Social Media Report,Edition 2 , implemented this year in associationwith NM Incite (a Nielsen/ McKinsey company) ,draws fresh insights from your responses, itvalidates many previous assessments. You willread them in the subsequent pages.

However, let me talk about changes I have seen,over the last year, in how social media is being approached by organisations.

Reputation has never been more ckle. As

recent examples in corporate and mediacircles have shown, social media has playedan important role in amplifying importantissues - sometimes using parody, sometimes

through inane looking memes, sometimes through serious discussions that only ‘appear’disintegrated but are actually bound in threads -social media is playing the new watchdog.

Controlling the medium, or the message,is clearly out of the question. The need forpreparedness and participation in advance;

Rajesh LalwaniPrincipal and Founder, Blogworksand Principal Coordinator, IndiaSocial

to listen, identify key topics, nodes; to transparently acknowledge, participate andengage multiple stakeholders, if, forbid, anorganisation was to nd itself in midst of a crisis,are being acknowledged as the new reputationmanagement concepts.

This growing impact on reputation andmarketing has brought interest and interventionat the highest level. The number of CEOs driving

the need has seen a dramatic rise over the last6-9 months. This does three important things,a, it energizes the team into action; b, it bringsgreater rigour - the approach becomes far morestrategic; and c, the chances of departments

thinking and working together improve.

On the brand side, an important change,particularly in some of the high impactcategories (typically high involvement productssuch as automobiles, consumer electronics,mobile etc.) has been the depth of engagement.From mere presence on social media channels,marketers are beginning to map, and intervene,at all stages of the purchase cycle.

There is a much greater emphasis on trying to understand how social media is in uencing purchase, to how the customer voices feedback

post purchase. An understanding that all socialmedia channels are not the same; that blogsand forums have a different role than touchpoints like, Facebook or Twitter; or that buzz is

the mere surface, that the magic of social mediamay, in fact, lie in mapping conversations,identifying evangelists and co-creating communication and products.

As social media impact is understood, and moremarketing outlay directed in its direction, theemphasis is on scaling up, trying to gain critical

Get Set! Go!

© 2010 Blogworks.in

Design: [email protected]: +91 9810558881

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 4/31

India Social Media Survey Edition 2 7India Social Media Survey Edition 2

mass. This has brought an acknowledgement that the key to scaling social media marketing interventions could be through use of

technology and community generated content.

The understanding that creating content isgoing to be the key to success in engaging stakeholders; and that creating this content isnot easy – enter technology and the community.

Over the last 6 months, ‘lead gen’ is the wordI have heard most often in sales meetings.It’s a new word in social media circles. As B2Bmarketers jump in, lead generation has becomea key objective.

Driven by marketing leaders, B2B programmesare typically, focused and result driven, only theroute in social media interventions is through

thought leadership and content – reports,white papers, articles, expert and practicecommunities and Q&As.

Another important shift is the realization that the future of social is mobile. I have beenreading more news on my mobile device, thanon the notebook; spending more time on myphone, accessing Twitter and Facebook, thanmaking voice calls. Marketers are beginning torealize this.

Clearly organisations and brands have caughtup and the survey report corroborates that.

For me the most interesting insights from thisyear’s report include:

Market in transition, moving towards1.strategic interventions.

Sharp focus on the customer – 90 percent2. brands are using social media to engagecustomers, vis-à-vis 79 percent in theprevious edition.

Only 23 percent of the social media3.engagement is being outsourced – couldbe a sign of early usage; interestinglyprogrammes deployed by agencies showbetter width.

Notice the arrival of the sales department in4.social media programmes; and emergenceof concepts like Social CRM.

Mobile adoption for marketing likely to5.shoot up next year – 46 percent intend touse mobile social networking in the future.

Clear need and focus on deeper6.measurement and analysis.

3 out of 4 companies/ brands feel the need7.for a stated policy; and either have one inplace or are working on one.

11 percent marketers are already spending 8.more than 30 percent of their digital spendson ‘social’.

Budgets have increased in sync with last9.reports assessment, likely to go up overnext 2 years.

Sharp focus on ‘number of fans’ re ects10.attempt to gain critical mass before RoIon engagement could be achieved – it isa good sign and shows understanding of social media impact and more emphasis onit from marketers.

Next stops: E-commerce and monetisation.

2011 promises to be an exciting year forall of us.

When Blogworks approached Nielsen to partneron their India Social Media Report research,I was personally very excited about the exercise.Reason? The Indian market today is looking for empirical evidence that the ‘Social Mediaopportunity’ is real and that there is a realmomentum building up for it. This book thatyou are holding is that evidence, in my opinion.

This has been the fruit of an exciting periodof research, during which the ndings have

oscillated between pleasant surprises and

reaf rmation of our beliefs in this medium.

We believe that the world of marketing in Indiais undergoing a permanent transformationand social media is at the centre of it. Byfundamentally changing the way brandscommunicate with consumers, social media isall set to overhaul the marketing food chain.This is not a futuristic concept or something that

Karthik NagarajanDirector, Online Division, The Nielsen Company.

is happening in a distant foreign land. This ishappening in India as I write and Indian brandshave already started realising and reacting to

this.

I want to highlight two interesting stories that this research revealed to us.

Getting strategic aboutsocial mediaThe term ‘social media’ by itself is something

that seems to have multiple de nitions

within Indian marketing circles. Many brandsand sections of the media assume it to besynonymous to social networking and micro-blogging. The impact of discussion forums,message boards, review sites, video sharing sites and blogs are often overlooked, primarilybecause they are seldom talked about in

mainstream news. As a result of this, manybrands have been quite content with just

creating a Facebook page and a Twitter accountand calling it quits, with a belief that they havedone enough to have a ‘social media’ existence.This has seldom worked for them.

For this mind-set to change, social medianeeds the attention and the commitment of

the top management. There needs to be aclear understanding of the relevance of thismedium to the brand in question and a process

to leverage it. This can come about only if there

Turning a corner

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 5/31

India Social Media Survey Edition 2 9India Social Media Survey Edition 2

is a plan and resources available within theorganisation to support it. When we posed hisquestion to brands, 27 percent of them said

that they already have a stated social mediapolicy and 46 percent said that they are working on one.

Why is this important? It is not that socialmedia is a structured medium where processes

and policies de ne how you react to andleverage market situations. The truth is quite

the opposite – it is such a dynamic forum that

brands sometimes have to react in hours, if

not days. However, the fact that almost 3 out of 4 brands are serious about having a strategicsocial media policy, tells me that they recognise

the importance of this medium, right up to the top management and that is a paradigm shift inperception, compared to a year or so back.

What de nes success?When we asked brands about the top vemetrics on which they evaluate their socialmedia success, we got an interesting set of

responses. The volume of interaction (fans,followers, etc) expectedly and rightfully took the

top spot. However, the surprising element herefor me was that ‘lead generation’ featured in

the top three. This worries me a bit because itreminds me of a similar trend that has plagued

the Indian display advertising market (and

continues to do so) – over-obsessing about‘performance’.

Simply because online is a more ‘measurable’medium, Indian marketers tend to over-measure

it sometimes and bring in impractical ROI angles to their advertising decisions. This has led tolarge scale domination of performance-basedadvertising that assumes incorrectly that a

display ad (banner) is only as ef fective as thenumber of people who click on it. While thismight be actually true and even effective insome product categories, it is not by any means

the best way to leverage the digital medium. Theabove-mentioned response on ‘lead generation’makes me wonder if we will end up making asimilar mistake with social media as well.

The audience you end up having for your brandon social media is ‘earned’. It is like a party thatyou need to be invited to as a brand. You cannot

always gate-crash it by asking your customer

to click on an ad or sign up for something thatis not in his / her mind space. This medium isabout engaging and contextual advertising – orin other words, this medium is all about theconsumer. This is why historically and even inother countries, social media sites have had thelowest click-through rates for advertising. So itworries me a bit that ‘lead generation’ is one of

the key reasons brands are here.

Having said that, ‘Sentiment of the

conversations’ and ‘brand awareness’ alsofeatured in this top ve list. So I hope my worries

are unfounded and we as a market leverage this medium by playing to its stren gths. Weneed to remember that social media in India,is a relatively new trend and the Indian onlineconsumer is just about warming up to it (70% of social networking users in India started in the

last 1-2 years). So if there is inertia and teething problems, those are understandable and insome cases even inevitable.

India Social Media Survey2010 ReportInsights from Organisations and Marketers

The NeedMuch has changed since we released ourlast report in March 2009. From an emerging

tool, social media has gone on to become amainstream phenomenon, deeply impacting reputation management, marketing,communication and enterprise collaboration.

For the India Social Media Survey Edition 2,Blogworks has partnered with NM Incite(A Nielsen/McKinsey Company) to collaborateand draw the best insights from your inputs.The survey attempts to understand the nature,and level, of social media usage by businessesand brands in India; channels and impact;objectives and measurement.

Results and analysis will enable businesses andbrands in India to make educated decisionsregarding trends and spends on the medium.

MethodologyThe survey was jointly conducted by Blogworks– strategic social media solutions and NM Incite(A Nielsen/ McKinsey Company) in November2010.

A detailed questionnaire was hosted online tocollect responses from the desired audience –brands/organisations and agencies/consulting

rms.

Different, relevant, set of questionnaireswere hosted, basis categories of respondentsrelevance to participants, so as to draw themost accurate inputs.

E-mailers, advertising and word-of-mouth wereused to reach participants.

Survey forms lled in by participants who did notmeet the audience criteria were removed.

Research analysis has been done on an sampleof 499 respondents coming from 3 segments

Brands/Organisations - 236•

Agencies/Con• sultants (Agencies) - 208Others (Primarily students) - 55•

73% of the respondents from brands/organisations state that they have beendirectly involved in managing their socialmedia programme; another 18% are indirectlyinvolved.Responses from those not involvedwere not considered.

Respondents could give multiple responses insome cases and in these questions the totalnumbers won’t add up to 100.

Responses by brands/organisations, agenciesand combined results are distinguished using separate colour schemes.

Statistical analysis of each question only takesinto account valid responses to that speci cquestion and not the total number of entries,

thus allowing for a more precise evaluation.

Trends are captured graphically; comments fromparticipants are highlighted with names whereparticipants gave us explicit permission to quote

them; and without giving away identities of participants, and organisations they represent,where participants did not wish to be quoted.We have also tried to draw t rends, establishlinkages: these are highlighted.Note: Multiple terminologies associated with the space, including

social media, SMM, social technologies, digital marketing, amongstothers, can sometimes confuse participants. Hence we will stick tousing the term ‘social media’ to describe the broad phenomenon of conversational marketing and collaborative technologies.

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 6/31

India Social Media Survey Edition 20 11India Social Media Survey Edition 2

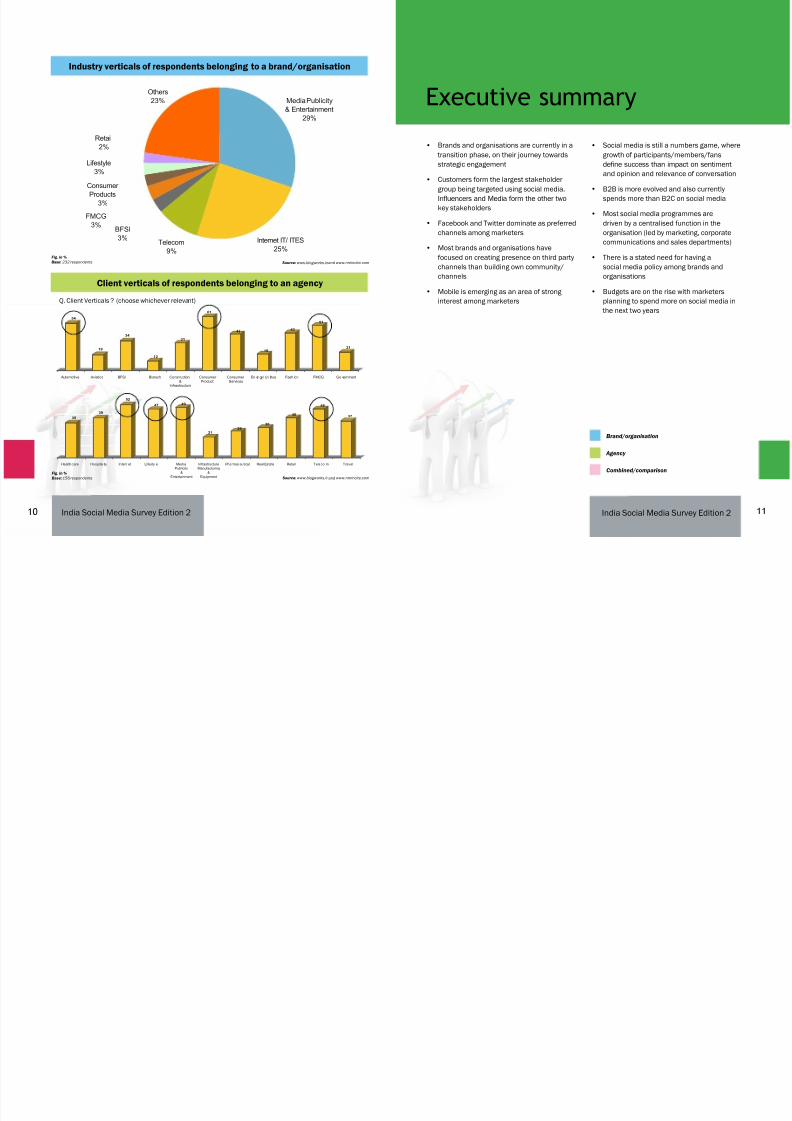

Industry verticals of respondents belonging to a brand/organisation

Media Publicity& Entertainment

29%

Internet IT/ ITES25%

Others23%

Retail2%

Lifestyle3%

Consumer

Products3%

Telecom9%

BFSI3%

FMCG3%

3539

52

47 49

2126

30

40

48

37

54

19

34

12

31

61

42

19

43

51

21

Client verticals of respondents belonging to an agency

Q. Client Verticals ? (choose whichever relevant)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 232 respondents

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 156 respondents

Brands and organisations are currently in a• transition phase, on their journey towardsstrategic engagement

Customers form the largest stakeholder•group being targeted using social media.In uencers and Media form the other twokey stakeholders

Facebook and Twitter dominate as preferred•channels among marketers

Most brands and organisations have•focused on creating presence on third partychannels than building own community/channels

Mobile is emerging as an area of strong •interest among marketers

Social media is still a numbers game, where•growth of participants/members/fansde ne success than impact on sentimentand opinion and relevance of conversation

B2B is more evolved and also currently•spends more than B2C on social media

Most social media programmes are•driven by a centralised function in theorganisation (led by marketing, corporatecommunications and sales departments)

There is a stated need for having a•social media policy among brands andorganisations

Budgets are on the rise with marketers•planning to spend more on social media in

the next two years

Automotive Aviation BFSI Biotech Construction&

Infrastructure

Consumer Product

Consumer Services

En er gy/ Uti lities Fash ion FMCG Go vernment

Healthcare Hospitality Internet Lifestyle MediaPublicity

&Entertainment

InfrastructureManufacturing

&Equipment

Pharmaceutical Real Estate Retail Teleco m Travel

Executive summary

Brand/organisation

Agency

Combined/comparison

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 7/31

India Social Media Survey Edition 22 13India Social Media Survey Edition 2

Validating socialmedia usage

90%

10%

Yes No

Q. Has your organisation engaged in any social media initiatives?

Social media adoption ismainstream

90% say• that their brands and organisationshave engaged in social media initiatives incomparison to 54% in 2009

Only 9% non social media users have also•no intention to use, in the future, as against36% in 2009

- This re ects the growing social media.impact and adoption

Don't Know,56%

SeriouslyConsidering,

35%

Not Considering,9%

Social media is becoming an importantpart of a brand’s marketing plan.

In near future?

Source: www.blogworks.in and www.nmincite.com

Fig. in %Base: 23 respondents

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 228 respondents

Nature of involvementand management

Social media adoption is a recentphenomenon; last 2 years havecontributed signi cantly

More than 70% have engaged in social•media initiatives only in past 2 years

As expected Agencies spend more time•on social media programmes with 33%agencies spending over 20 hours per week.On the other hand, only 12% clients spendmore than 20 hours per week

78% social media programmes are B2C in•orientation; B2B adoption at 41% is veryencouraging

Marketing, ORM and Lead Generation are• the top 3 purposes for which companies areusing social media in India

Nearly 80% of social media programmes are•led by the marketing department of brands/organisations; sales departments also

taking a keen interest

92% brands/ organisation are addressing •

customers using social media; othernotable stakeholders being addressed areIn uencers, Media, Current & Prospectiveemployees

57% brands/organisations have a team•of more than 3 members involved in theresocial media programme

Majority of brands manage their social•media programmes in-house; only 23% areoutsourced

Q. Since when has your brand/organisation been engaged in social media activities?

36

38

14 13

Less than ayear

1-2 Years 2-3 Years 3 Years+

74% in past 2 years

Social media adoption among brands/organisations a recent phenomenon;74% have engaged in social media initiatives only in past 2 years

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 177 respondents

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 8/31

India Social Media Survey Edition 24 15India Social Media Survey Edition 2

Q. How much time is spent by your team/organisation on its social media programme per week?

27%

31%

23%

12%

7%

Under 5 hours

5-10 hours

10-20 hours

20-40 hours

More than 40 hours

42% brands/organisations spend more than 10 hours per week on theirsocial media programmes

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 156 respondents

33% Agencies spend over 20 hours per week on social media programmes;13% spend more than 40 hours

13%

35%

19%

20%

1 %

Under 5 hours

5-10 hours

10-20 hours

20-40 hours

More than 40 hours

Strong focus on social media

16%

45%

13%

18%

8%

Time spent on social media bybrands that outsource

Agencies are spending more number of hours on socialmedia as compared to the clients. It could be becauseclients tend to spend time on supervision and direction,whereas the Agency spends time in planning and execution.

Q. How much is the average time spent by you/ your team on a client programme, per week?

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 145 respondents

Source: www.blogworks.in and www.nmincite.comBase: 38 respondents

78% social media programmes are B2C focused; B2B adoption at 41%is encouraging

Q. What’s the nature of your brand/ organisation’s social media engagement programme?

78

41

26

Business-to-Consumer

Business-to-business

Partners andemployees

Cross TabB2C B2B Partners &

employees

B2C 100% 30% 25%

B2B 58% 100% 38%

Partners &employees

74% 59% 100%

B2B focused programmes havea strong focus (58%) on B2Cengagement too

Source: www.blogworks.in and www.nmincite.com

Fig. in %Base: 174 respondents

4144

1813

4844

7871

30

2428

43

C m t i t ii n t l l i n c

C u t m rr i c

E - C m m r c E n t r r ic l l r t i n

LG n r t i n

L i t n i n nn l t i c

r k t i n n l i nr u t t i n

m n m n t /n l i n

r u c t in

l m n t

c r u i t m n t c i l C T h u h tl r h i

Marketing, ORM and Lead Generation are the top 3 purposes for whichbrands/organisations are using social media in India

Q. Which of the following purposes do you use social media for ? (Choose all that apply)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 160 respondents

Competitiveintelligence

Customer service

E-Commerce Enterprisecollaboration

LeadGeneration

Listening andanalytics

M ar ke ti ng O nli nereputation

management/Online PR

Productideasand

development

R ec ru it me nt S oc ia l CR M T ho ug htleadership

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 9/31

India Social Media Survey Edition 26 17India Social Media Survey Edition 2

8

10 10

8

43

2

4

9

11

9 9

1614 14 14

7

6

5 56

5

8

10

C m t i t ii n t l l i n c

C u t m rr i c

E - C m m r c E n t r r ic l l r t i n

LG n r t i n

L i t n i n nn l t i c

r k t i n n l i nr u t t i n

m n m n t /n l i n

r u c t in

l m n t

c r u i t m n t c i l C T h u h tl r h i

Agencies are using social media for Marketing, ORM, Listening & Analyticsand Lead Generation

Q. Which of the following purposes do you use social media for ? (Choose all that apply)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 141 respondents

Thought leadership

SocialCRM

Recruitment

Product ideasand decelopment

Online reputationmanagement/Online PR

Marketing

Listening andanalytics

LeadGeneration

Enterprise collaboration

E-Commerce

Customer service

Competitive intelligence 58

63

33

12

59

59

78

72

36

23

42

47

41

44

18

13

48

44

78

71

30

24

28

43

Brand

Agency

Agencies showcase betterwidth in terms of usage

B2B has a higher emphasis on lead generation, competitive intelligence,enterprise collaboration and thought leadership; E-commerce is gettinghigher emphasis among B2C programmes

Q. Which of the following purposes do you use social media for ? (Choose all that apply)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 160 respondents

79

49

10 9

1710 10

Nearly 80% of social media programmes are led by the marketingdepartment of brands/organisations; sales departments are also showing akeen interest

Q. Which of the following department/s is/are responsible for the planning and execution of the socialmedia programme in your organisation?

Corporate Communication is another keydepartment instrumental in social mediaplanning and execution

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 173 respondents

B2B

B2C

Competitiveintelligence

Customer service

E-Commerce Enterprisecollaboration

LeadGeneration

Listening andanalytics

Ma rke tin g O nl in ereputation

management/Online PR

Productideasand

development

Recruitment S oc ia l CR M T ho ug htleadership

Marketing CorporateCommunication

Huma nResou rces Cust om er Ser vec e Sales IT Outsourcedto anagency

43 3825 26

4 5 5 5 810

5 7 5 6

B2C B2B

Marketing & Corporate Communication departments lead in B2Cprogrammes; Sales & IT departments in B2B programmes

Q. Which of the following department/s is/are responsible for the planning and execution of the socialmedia programme in your organisation?

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 173 respondents

Marketing CorporateCommunication

Human Resour ces Customer Ser vece Sales IT Outsourcedto anagency

Emergence of lead generation isan important trend

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 10/31

India Social Media Survey Edition 28 19India Social Media Survey Edition 2

92% brands/ organisation are addressing customers using social media;other notable stakeholders being addressed are In uencers, Media, Current& prospective employees

Q. Which stakeholder groups have you addressed using social media ? (choose whichever relevant)

79

66 65

41

79

47

35

r l l c r r r i l l i c r

Notice the higher emphasis onengaging customers over anyother stakeholder group, evenwhen compared to the lastreport (March 2009)

Source: www.blogworks.in and www.nmincite.comFig. in %

Survey Report Edition 1 (2009)

Customers Employees Infuencers Partners Media Analysts Policymakers

90 92

38 31

3731

61

53

28

33

54 54

21 19

9 10

Customers ProspectiveEmployees

Employees Inf luence rs Par tner s Med ia Analyst s Pol i cy maker s

Key stakeholders that agencies address, using social media, arecustomers – 90%, in uencers – 61% and media – 54%

Q. Which stakeholder groups have you addressed using social media (choose whichever relevant)?

Survey Report Edition 2 (2010)

Source: www.blogworks.in and www.nmincite.com

Fig. in %Base: 141 respondents

Brand

Agency

44

39

7

11

1 to 2 3 to 5 6 to 9 More than 10

No social mediainitiatives at the

moment30%

In-sourced55%

Outsourced15%

Majority of brands manage their social media engagements in-house; only23% are outsourced

Over 57% brands/organisations state that their social media programme ishandled by a team of more than 3 members

Outsourcing of social media engagement has increasedfrom 15% in 2009 to 23 % in 2010. Adoption of socialmedia has likely resulted in in creation of in-sourcedpositions within the brand/ organisation

Q. Your social media engagements, are mostly in-sourced or outsourced?

In-sourced77%

Outsourced23%

Survey Report – Edition 1 (2009)

Q. How many people are deployed (including internal team and external agencies) with key responsibility to manage the social media programme for your organisation?

Strong interest is building up in the space

56% agencies deploy a team of 3+ to manage the social media programme for their clientportfolio.

57% - Team over 3+

Source: www.blogworks.in and www.nmincite.com

Fig. in %Base: 172 respondents

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 168 respondents

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 11/31

India Social Media Survey Edition 20 21India Social Media Survey Edition 2

S o m e c o m p a n i e s i n m e d i a , I T , t e l e c o m

a n d a u t o m o t i v e s e c t o r h a v e l a r g e r

t e a m s ( 1 0 p e o p l e o r m o r e ) t o m a n a g e t h e i r S o c i a l M e d i a p o r t f o l i o

A u t o m o

t i v e

A v i a t i o n a n d

A e r o s p a c e

B F S I

B i o t e c h

C o n s t r u c

t i o

n a n

d

I n f r a s t r u c t u r

e

C o n s u m e r

P r o

d u c

t s

C o n s u m e r

S e r v i c e s

E n e r g y

/ U t i l i t i

e s

F a s

h i o n

F M C G

H e a l t h

C a r e

1 - 2

-

2 %

7 %

-

2 %

3 %

2 %

-

2 %

2 %

5 %

3 - 5

-

-

2 %

2 %

-

2 %

2 %

-

2 %

3 %

-

6 - 9

-

-

9 %

-

-

9 %

-

-

-

9 %

-

M o r e

t h a n

1 0

1 2 %

-

-

-

-

-

-

-

-

-

-

H o s p

i t a l i t y

I n t e r n e

t / I T /

I T E S

L i f e s t y l e

M e d

i a ,

P u

b l i c i t y

a n

d

E n

t e r t a i n m e

n t

I n f r a s t r u c t u r

e ,

m a n u f a c

t u r i

n g a n

d

e q u

i p m e n t

P h a r m a c e u t i

c a l

R e a

l e s t a t e

R e

t a i l

T e l e c o m

T r a v e

l

1 - 2

-

3 3 %

5 %

3 1 %

-

-

-

-

7 %

-

3 - 5

-

3 2 %

-

3 3 %

2 %

-

2 %

3 %

1 3 %

3 %

6 - 9

-

2 7 %

-

3 6 %

-

-

-

-

9 %

-

M o r e

t h a n

1 0

6 %

2 4 %

-

4 1 %

-

-

-

6 %

1 2 %

-

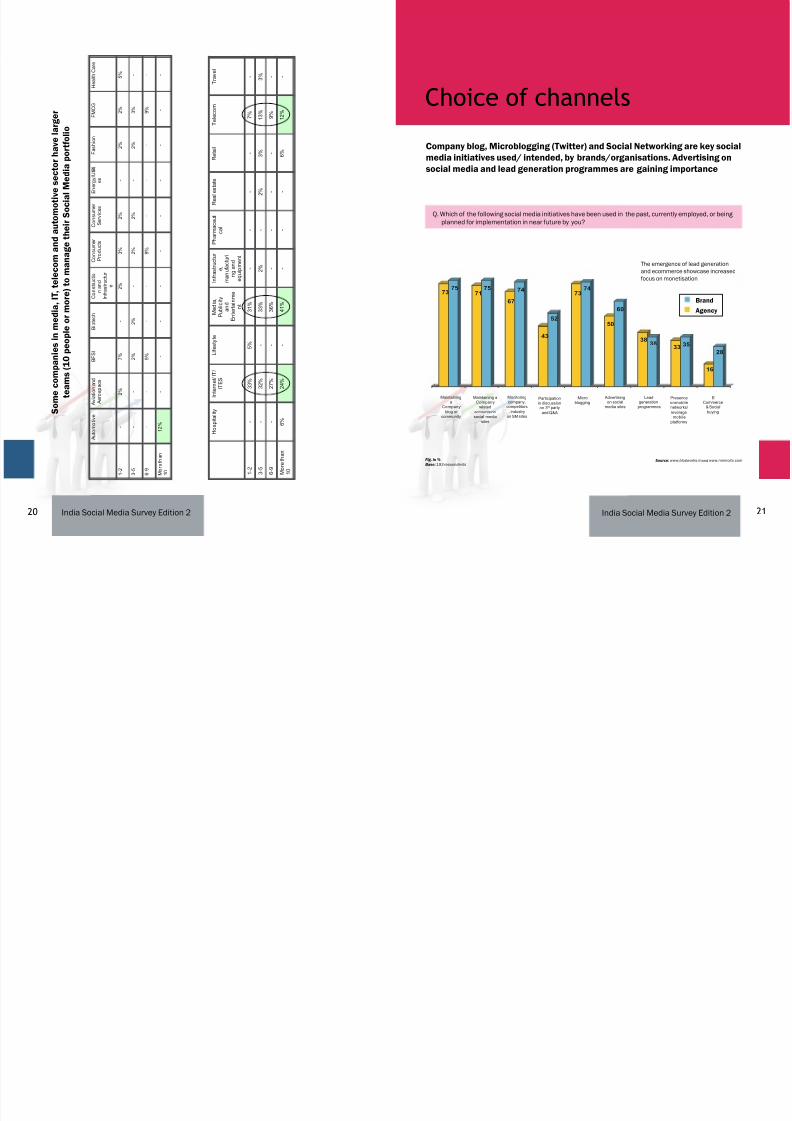

Choice of channels

Company blog, Microblogging (Twitter) and Social Networking are key socialmedia initiatives used/ intended, by brands/organisations. Advertising onsocial media and lead generation programmes are gaining importance

Q. Which of the following social media initiatives have been used in the past, currently employed, or being planned for implementation in near future by you?

Maintaininga

Companyblog or

community

Maintaining aCompany

relatedaccounts onsocial media

sites

Monitoringcompany,

competitors, industry

on SM sites

Participationin discussionon 3 rd party

and Q&A

Microblogging

Advertisingon social

media sites

Leadgeneration

programmes

Presenceon mobilenetworks/leveragemobile

platforms

ECommerce

& Socialbuying

7375

7175

67

74

43

52

7374

50

60

3835

33 35

16

28

The emergence of lead generationand ecommerce showcase increasedfocus on monetisation

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 193 respondents

Brand

Agency

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 12/31

India Social Media Survey Edition 22 23India Social Media Survey Edition 2

60

26

9083

62

17

56

16

5

1915

Companyblog

Owncommunity

Facebook Twitter LinkedIn Slideshare YouTube Flickr Yahoo Orkut Wikipedia

Facebook (90%) and Twitter (83%) are the most popular social mediachannels being used by brands/organisations

Q. On which of the following social media channels do you currently maintain one or more brand/companyaccounts/ presence ? (Choose all that apply)

A comparison between how brands and agencies are usingsocial media channels

LinkedIn, company blogs and YouTube are otherprominent channels

More attention being paid to 3rd party interfaces rather than company owned properties

Orkut appears tohave lost out in

the game

60

26

90

83

62

17

56

16

5

19

15

63

39

91

77

68

34

64

37

16

18

29

27

Companyblog

Own community

Slideshare

YouTube

Flickr

Scribd

Yahoo

Orkut

Wikipedia

Brand

Agency

Q. On which of the following social media channels do you currently maintain one or more brand/companyaccounts/presence ? (choose all that apply)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 153 respondents

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 134 respondents

‘LinkedIn Answers’ is the most preferred channel to answer brand/businessquestions in the social media space

Q. On which of the following do you/ your team/ agency ask/ answer business/related questions ?(Choose all that apply)

40

56

15

25

11 137 10

LinkedIn Answers Yahoo! Answers Wiki Answers Answers.com

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 283 respondents

26%

46%

12%

16%Present

Considering

Not Considering

Not Aware

Mobile social media networks/platforms are likely to become popular toolsamong brands/organisations

Q. Is your brand/ organisation currently present on any mobile social networking/ blogging sites/platforms?

Currently 26% brands/organisationsare present mobile social mediaplatform.

Another 46% brands/organisationsintend to use mobile socialnetworking in the future

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 148 respondents

Brands

Agency

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 13/31

India Social Media Survey Edition 24 25India Social Media Survey Edition 2

36% agencies say their clients are currently present on mobile socialnetworking platform and 34% are considering it for future use

2422

19

10

52

9

2

10

4 42

5

12

2

9

2

10

63

1214

2625

R oc ke Ta lk H iB ud dy m ig 33 M yg am ma S MS Gu pS hu p B ub bl y Wap sp el l Fr e nz o Q ee p M ob il uc k C el lu fu n

Agency Client

SMS GupShup enjoys highest awareness level among brands followed byRockeTalk and HiBuddy

Q. Which of the following mobile social networking sites/ channels/platforms are you familiar with ?(choose all that apply)

36%

34%

11%

19%Present

Considering

Not Considering

Not Aware

Q. Is your brand/ organisation currently present on any mobile social networking/ blogging sites/platforms?

Higher salience for SMS GupShupand Mobiluck among agencies

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 132 respondents

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 89 respondents

7 8.6

10

2.9

5

8.6

2

5.7

27

17.1

2

5.7

2 2.9

5

2.9

RockeTalk HiBuddy mig33 Mygamma SMS GupShup Bubbly Qeep Mobiluck

Among those ‘presently using’ mobile social networks/platform, SMSGupShup is the most popular

Q. Which of the following mobile social networking sites/ channels/platforms have you used for your client ?(choose all that apply)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 41 respondents

Brand

Agency

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 14/31

India Social Media Survey Edition 26 27India Social Media Survey Edition 2

48%

25%

12%

15%

A centralised function in theorganisation - all socialmedia deployment comesfrom a single organisedgroup

Brands/ departments/businesses/ divisions

working on independentprogrammes

Brands/ departments/businesses/ divisionsworking together oncollaborative programmes

It's all outsourced

Social Media lifecycle

29% of brands/organisations have a strategic approach to social media40% are in the transition phase

Q. In your opinion, how mature is your brand/ organisation’s social media programme?

31%

40%

29%

26%

40%

34%

Both brands/organisationsand agencies have asynchronised view onmaturity of social mediausage

Trial (an experimental approach with a series of tactical deployments)

Transition (an informal process is used and changes made as per need)

Strategic (a formal process is used and reviewed routinely)

Brands/Organisations

Agencies

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 148 respondents

32%

14%

50%

4%

A centralised function in the organisationLassez FaireCross functional teamOthers

When asked in edition 1 (2009),brands advocated a cross functional

team to best manage social mediaprogrammes. However in reality,centralised teams, lead planning andexecution as revealed in this edition

Most social media programme are being managed by a centralised functionin organisations, contrary to what was felt ‘it should be’ in edition 1 of thereport (2009)

Q. Your social media programme is managed by:

Survey Report Edition 1 (2009)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 271 respondents

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 15/31

India Social Media Survey Edition 28 29India Social Media Survey Edition 2

27%

46%

18%

5%4%

Yes, we have a social mediapolicy.

No, we do not have one butare working on one.

No, we do not have one anddon't know what our policyshould be.

No, and our 'policy' is to 'nothave' a stated policy.

Don't know.Around 46% brands/ organisations arecurrently working on a social mediapolicy showing impact and need forpreparedness

3 out of 4 brands/ organisations have felt the need for a s tated social mediapolicy and currently have one, or are in process of putting one in place

Q. Does your organisation have a stated social media policy?

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 147 respondents

22

42

48

35

1915

68

B2CB2B

Higher incidence of social media policy in B2B re ects emphasis on aplanned approach; B2C moving fast to catch up

Q. Does your organisation have a stated social media policy?

Yes, we havea SM policy

No, we areworking on

one

No, wedon't know

No, weDon’t want

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 147 respondents

8%

16%

14%

40%

18%

4%

Yes, my client (all of myclients) have a social mediapolicy.Yes, most of my clientshave a social media policy.

No, most do not have onebut are working on it.

No, most do not have oneand don't know what thepolicy should be.No, and their 'policy' is t o'not have' a stated policy.

Don't know.

Two thirds agencies say their clients have a social media policy or areworking on one

Q. Do most your clients have a stated social media policy ? (please share if you know the status)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 125 respondents

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 16/31

India Social Media Survey Edition 20 31India Social Media Survey Edition 2

43%

17%

14%

10%

11%

4%

1%

0 to 5

5 to 10

10 to 15

15 to 20

20 to 30

30 and above

Don’t know

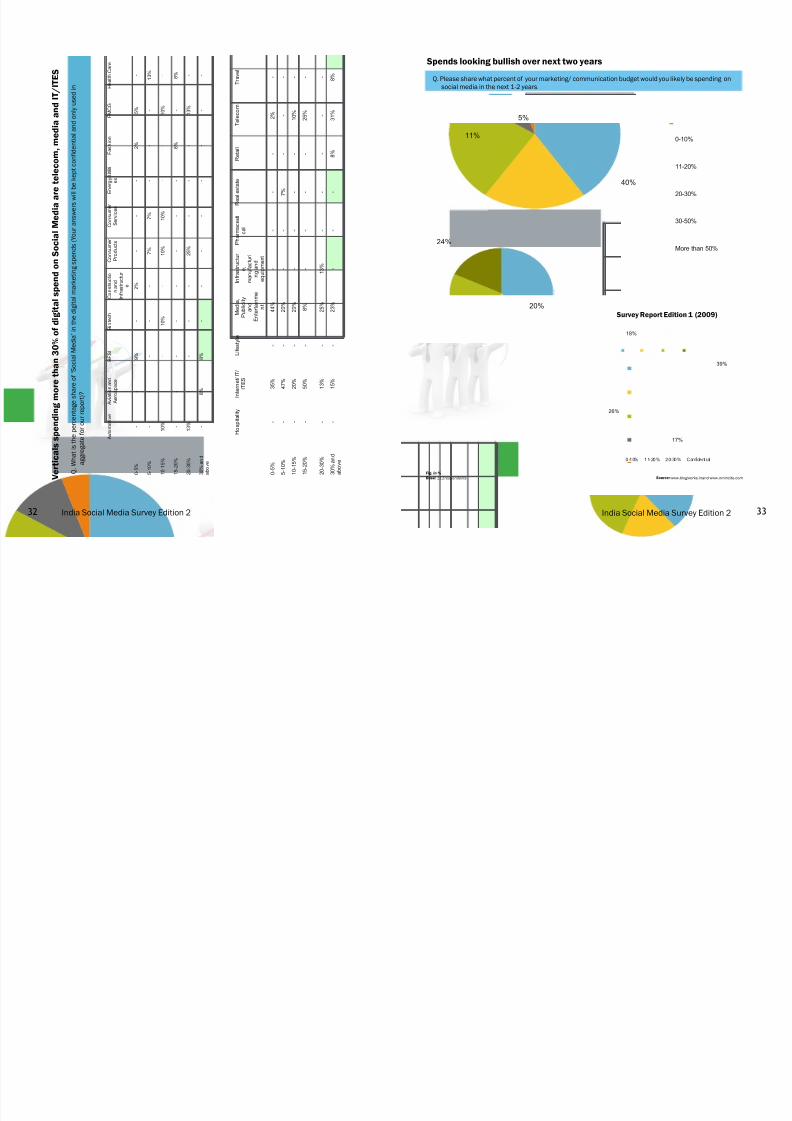

Budgets

26% brands/organisations are spending more than 10% of their marketingand communication budget on digital media

Q. What percent of your marketing and communication budget is presently spent on Digital Media ?

3 8

5 1

18

2 0

18

13

6

4

2

2

18

10

0 to 5 5 to 101 0 t o 1 5 15 t o 202 0 t o 3 0 3 0 a nd a bo ve

B2B focused programmes have higher spends on digital media

Heavy focus ondigital media

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 143 respondents

36%

11%

22%

11%

8%

8%

4%

0 to 5

5 to 10

10 to 15

15 to 20

20 to 30

30 and above

Can't say

31% marketers are spending 10% of digital spends on social media; 11% areheavy spenders with more than 30% digital budgets going to social media

Q. What is the percentage share of ‘social media’ in the digital marketing spends ?

0 to 5

5 to 10

10 to 15

15 to 20

20 to 30

30 and above

Can't say

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 141 respondents

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 17/31

India Social Media Survey Edition 22 33India Social Media Survey Edition 2

V e r t i c a l s s p e n d i n g m o r e t h a n 3 0 % o f d i g i t a l s p e n d o n S o c i a l M e d i a a r e t e l e c o m

, m e d i a a n d I T / I T E S

Q . W

h a t i s t h e p e r c e n t a g e s h a r e o f ‘ S o c i a l M e d i a ’ i n t h e d i g i t a l m a r k e t i n g s p e n d s ( Y o u r a n s w e r s w i l l b e k e p t c o n d e n t i a l a n d o n l y u

s e d i n

a g g r e g a t e

f o r o

u r r e p o r t ) ?

A u

t o m o

t i v e

A v i a t i o n a n d

A e r o s p a c e

B F S I

B i o t e c h

C o n s t r u c t i o

n a n

d

I n f r a s t r u c t u r

e

C o n s u m e r

P r o

d u c t s

C o n s u m e r

S e r v i c e s

E n e r g y / U

t i l i t i

e s

F a s h

i o n

F M C G

H e a l t h

C a r e

0 - 5 %

-

-

9 %

-

2 %

-

-

-

2 %

5 %

-

5 - 1 0 %

-

-

-

-

-

7 %

7 %

-

-

-

1 3 %

1 0 - 1 5 %

1 0 %

-

-

1 0 %

-

1 0 %

1 0 %

-

-

1 0 %

-

1 5 - 2 0 %

-

-

-

-

-

-

-

-

8 %

-

8 %

2 0 - 3 0 %

1 3 %

-

-

-

-

2 5 %

-

-

-

1 3 %

-

3 0 % a n

d

a b o v e

-

8 %

8 %

-

-

-

-

-

-

-

-

H o s p

i t a l i t y

I n t e r n e

t / I T /

I T E S

L i f e s t y l e

M e

d i a

,

P u b

l i c i t y

a n d

E n

t e r t a

i n m e

n t

I n f r a s t r u c

t u r

e ,

m a n u f a c

t u r i

n g a n

d

e q u

i p m e n t

P h a r m a c e u t i

c a l

R e a

l e s t a t e

R e t a

i l

T e

l e c o m

T r a v e

l

0 - 5

%

-

3 5 %

-

4 4 %

-

-

-

-

2 %

-

5 - 1

0 %

-

4 7 %

-

2 0 %

-

-

7 %

-

-

-

1 0 - 1 5

%

-

2 0 %

-

2 0 %

-

-

-

-

1 0 %

-

1 5 - 2 0

%

-

5 0 %

-

8 %

-

-

-

-

2 5 %

-

2 0 - 3 0

%

-

1 3 %

-

2 5 %

1 3 %

-

-

-

-

-

3 0 %

a n d

a b o v e

-

1 5 %

-

2 3 %

-

-

-

8 %

3 1 %

8 %

40%

20%

24%

11%

5%

0-10%

11-20%

20-30%

30-50%

More than 50%

Spends looking bullish over next two years

Q. Please share what percent of your marketing/ communication budget would you likely be spending onsocial media in the next 1-2 years.

39%

17%

26%

18%

0-10% 11-20% 20-30% Confident i al

Survey Report Edition 1 (2009)

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 111 respondents

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 18/31

India Social Media Survey Edition 24 35India Social Media Survey Edition 2

Brands Agencies

Very s at is f ied Very s at i sf i ed+somewhat satisfied

Very s at is f ied Very s at i sf i ed+somewhatsatisfied

Maintaining a company blog or community/ communities 20 65 23 71

Maintaining company related accounts on soci al mediasites 30 72 32 67

Monitoring company, competitors, industry relatedmentions on social media sites 22 71 29 67

Participation in discussion on 3 rd party and Q&A sites 13 43 16 44

Micro-blogging 29 57 22 62

Advertising on social media sites 17 51 28 61

Lead generation programmes 14 45 13 47

Presence on mobile networks/ leverage mobile platforms 4 21 3 18

E-commerce & social buying etc. 8 25 5 22

In terms of ROI, brand/organisation related presence on social networks,owned blogs and microblogging get a thumbs up

Q. How do the following social media activities score in terms of ROI achieved?

In terms of ROI, brands have a higher satisfaction level from micro-blogging,while agencies have better satisfaction from advertising

Q. How do the following social media activities score in terms of ROI achieved?

4 1 0 2 3 1 4 5 563 6

8 9 11 8

12 821

26 23

27 28 1625

2118

4542 49

30

28 3431

1717

2030

22 1329

17 144

8

M a i n t a i n i n g a c o m p a n y

b l o g o r

c o m m u n i t y / c o m m u n i

t i e s

M a i n t a i n i n g c o m p a n y -

r e l a t e d a c c o u n t s o n

s o c i a l m e d i a s i t e s

M o n i t o r i n g c o m p a n y ,

c o m p e t i t o r s ,

i n d u s t r y

r e l a t e d m e n t i o n s o n

s o c i a l m e d i a s i t e s

P a r t i c i p a t i o n

i n

d i s c u s s i o n o n

3 r d p a r t y

a n d Q & A s i t e s

( e . g .

f o r u m s , c o n s u m e r

r e v i e w s i t e s )

M i c r o - b l o g g i n g ( e

. g .

T w i t t e r )

A d v e r t i s i n g o n s o c

i a l

m e d i a s i t e s

L e a d g e n e r a t

i o n

p r o g r a m m e s

P r e s e n c e o n m o b

i l e

n e t w o r k s / l e v e r a g e

m o b i l e p l a t f o r m s

E - c o m m e r c e

& s o c

i a l

b u y i n g e t c .

Very Dissatisfied Somewhat Dissatisfied Neither Satisfied nor Dissatisfied Somewhat Satisfied Very Satisfied

Top 2 Box 65 72 71 43 57 51 45 21 25

Bottom 2 Box 10 4 6 10 12 12 12 17 13

Source: www.blogworks.in and www.nmincite.comBase: 120 respondents

Source: www.blogworks.in and www.nmincite.comBase: 120 respondents

Brands have a high satisfaction level from internal staff managing thesocial media programme

Q. What is your level of satisfaction on the following, basis results on the different types of investments undertaken.

According to Agencies, strategy, maintaining a company blog/ communityand monitoring competition score high in terms of ROI achieved

Q. How do the following social media activities, undertaken for your client/s, score in terms of ROI achieved?

4 2 1 4 4 3 2 2 3 3 13 6 11 5 8 3 5 5 2 1 5

19 15

2325

1821 19

21 2218 18

4237

15 19

24 33 20

18 12

13 22

1520

8 714 11

15

2 26 6

S t r a t e g y

I n t e r n a l s t a f f t o m a n a g e

s o c i a l m e d i a p r o g r a m m e

E x t e r n a l a g e n c y

f e e

d e p l o y i n g s o c i a l m e d i a

i n i t i a t i v e s

B l o g g e r e v e n t s &

i n f l u e n c e r p r o g r a m m e s

A d v e r t i s i n g o n s o c i a l

m e d i a c h a n n e l s

( F B a d s ,

L i n k e d I n a d s e t c )

A p p l i c a t i o n s / D e v e l o p m e n t

c o s t ( w e b s i t e e t c )

G i f t s a n d g i v e a w a y s

( p r o m o t i o n s , c o n t e s t s )

M o n i t o r i n g a n d

M e a s u r e m e n t ( R a d i a n 6 ,

N i e l s e n , S c o u t L a b s e t c .

)

M o b i l e

S o c i a l N e t w o r k i n g

S o c i a l C

R M

T r a i n i n g & W o r k s h o p s

Very Dis sat is fi ed Somewha t D is sat i sf ied Nei the r Sat is fi ed no r Dis sat i sf ied Somewha t Sat i sf ied Very Sat i sf ied

Top 2 Box 57 57 23 26 38 44 35 20 14 19 28

Bottom 2 Box 7 8 12 9 12 6 7 7 5 4 6

3 1 1 1 1 2 1 3 4 10 4 5 9 8 6 4 35

51319 13

1831

25 2526

29 2554

48

45

38

2840

33

34

1517

30 2332 29

16 22 2813

3 5

S t r a t e g y

M a i n t a i n i n g a c o m p a n y

b l o g o r

c o m m u n i t y / c o m m u n i t i e s

M a i n t a i n i n g c o m p a n y -

r e l a t e d a c c o u n t s o n

s o c i a l m e d i a s i t e s

M o n i t o r i n g c o m p a n y ,

c o m p e t i t o r s ,

i n d u s t r y

r e l a t e d m e n t i o n s o n

s o c i a l m e d i a s i t e s

P a r t i c i p a t i o n

i n

d i s c u s s i o n o n

3 r d p a r t y

a n d Q & A s i t e s

( e . g .

f o r u m s , c o n s u m e r

r e v i e w s i t e s )

M i c r o - b l o g g i n g ( e . g .

T w i t t e r )

A d v e r t i s i n g o n s o c i a l

m e d i a s i t e s

L e a d g e n e r a t i o n

p r o g r a m m e s

P r e s e n c e o n m o b i l e

n e t w o r k s / l e v e r a g e

m o b i l e p l a t f o r m s

E - c o m m e r c e

& s o c i a l

b u y i n g e t c .

Very Dissatisfied Somewhat Dissatisfied Neither Satisfied nor Dissatisfied Somewhat Satisfied Very Satisfied

Top 2 Box 84 71 67 67 44 62 61 47 18 22

Bottom 2Box

3 5 6 10 9 8 5 6 9 6

Source: www.blogworks.in and www.nmincite.comBase: 101 respondents

Source: www.blogworks.in and www.nmincite.comBase: 115 respondents

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 19/31

India Social Media Survey Edition 26 37India Social Media Survey Edition 2

Driving critical mass?Social media is still appears a numbers game where participants/members/fansseem more important than awareness or impact on sentiment and opinion

Growth in number of participants (users, fans, friends,followers etc on web/mobile touch points and community)

Impact on sentiment and opinion

Volume, quality and cost of leads generated/conversions

E-commerce revenues

Brand awareness

Insights – customer, competition, market

Impact on sales

Support during crisis

Share of voice vis-à-vis agreed competition

Search engine ranking/web traf c

Customer satisfaction score (including net promoter score/ recommendations)

Co-creation of products and services

Mention and prominence in relevant conversations

Increased engagement scores (retweets, likes, comments)

Q. Which of the following are the ‘top 5’ metrics that your brand/ organisation deploy to evaluate success

of your social media programme?

Measurement and analysis

39

35

35

31

30

29

29

25

22

21

16

14

13

12

Most important

Source: www.blogworks.in and www.nmincite.comFig. in %Base: 78 respondents

Q. Which of the following are the ‘top 5’ metrics that your brand/ organisation deploy to evaluate successof your social media programme?

Change in evaluation metrics (top 5)

Survey Report Edition 2 (2010)

1. Growth in number of participants

2. Impact on sentiment and opinion

3. Volume, quality and cost of leads generated

4. E-commerce revenues

5. Brand awareness

Survey Report Edition 1 (2009)

1. Impact on brand awareness

2. Volume of user generated content

3. Number of touch points with consumers

4. Better search engine ranking & increase in over all website traf c

5. Positive tone of comments, feedbacks, links etc.

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 20/31

India Social Media Survey Edition 28 39India Social Media Survey Edition 2

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 21/31

India Social Media Survey Edition 20 41India Social Media Survey Edition 2

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 22/31

India Social Media Survey Edition 22 43India Social Media Survey Edition 2

Clean & Clear TM Freshface 2010Mr. & Ms. Freshface – a talent hunt for rst year

college students across six metro cities in India.

The six month long event invited freshersfrom Delhi, Kolkata, Mumbai, Chennai, Pune,Bangalore to nominate themselves or theirfriends online and seek votes by creating aportfolio and pro le.

The social media engagement activity entailedselection and voting for contestants, inadditional to customised wall based activityand other networking utilities.

The platform also included social plugins from

Facebook and Twitter.Target Group : Young adults from Indian metrocities, undergraduate / professional degreecollege students age group 18-22

This age group of site visitors are most proactivein contributing content and interacting on thesite, inviting friends and other viral activities.

Freshface makes use of Itimes interactive tools to get users to vote for their favorite contestants.

Voting on pro les, to build online popularity of a contestant; voting widget replicated as anapplication on Facebook and activity sharedacross other leading social media sites.

Itimes groups of over 50 colleges in each cityenable users to interact amongst each otherand vote for their college contestants.

Con dence Meter – A intuitive application tomeasure visitors’ con dence score.

Teach India 2010Teach India 2010, a Times Group initiativefocuses on teaching spoken English to youthin the age group of 18-32 and through theprogram increase their employability. The

training program is held in partnership with theBritish Council in India.

The TG participating in this initiative onItimes is between 25 to 40 English speaking

Advertorial

professionals from across India, most likelyassociated with education institutes or peopleassociated with social causes.

Itimes offers interest groups on Teach India, analumni community of recent years, NGO pro lesand groups.

Itimes offers a custom created form to collectvolunteer applications.

Users registered for the initiative connect basisinterest.

Shareable rich media content like TVcommercials, celebrity pro les of stars associated with the cause,photos and videos related to theevent.

Interactive map to help sitevisitors choose a venue of choiceand convenience at the time of registering.

“Once Upon a Time….” –Networking around moviesNetworking enabled site created

to promote the movie and cast of ‘Once Upon a Time in Mumbaai’

Custom look built social media tools themed around ‘Once upon a time

in Mumbaai”.

Landing page customized to the OUATIM themewith a menu to lead the user to exclusive moviecontent.

http://itimes.com/onceuponatimeinmumbaaihosts of cal blogs and fan club pro les of alllead actors of the movie

The fan club pro les ride on the existing celebrity fan club section on itimes which hostsclose to 150 celebrity pro les with around ftycelebrities actively blogging on the platform.

Exclusive chats with the stars of the movie :Ajay Devgan, Kangna Ranaut, Prachi Desai andEmraan Hashmi

Users can personally interact with their favouritestars by posting on the celeb’s wall andcontribute to their fan albums etc.

Groups and Communities to showcase the plotof the movie, exclusive pictures, movie trailersand latest songs.

Exclusive Shobhaa De Blogs on the Movie

Fan Club pages for all the stars

Itimes also hosts the of cial movie trailers,movie synopsis, online community for sitevisitors to discuss the movie

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 23/31

India Social Media Survey Edition 24 45India Social Media Survey Edition 2

Seven lessons from the Social Mediarevolution

Fact 1: A minister called Shashi Tharoor loseshis job in India because of a tussle with acricket entrepreneur called Lalit Modi. Both of

them are on Twitter, and exchange their v iewsand facts in full public view on the Internet.Where are the editors?

Fact 2: Diplomatic missions across the worldare alerted by the government of the US, theworld’s most powerful nation, and they await adenouement: the leak of con dential cables byWikiLeaks, a Social Media entity with no realof ce or incorporation. What follows after thatis not news for day or two, or for one or twonations, but for the entire planet.

These two incidents in 2010 should be enoughfor anyone to realise that news and SocialMedia have been intermeshed in a manner that

N. Madhavan Technology Columnist/Associate Editor,

Hindustan Times

make them almost seamless extensions of eachother.

Online publications such as GigaOm.com andTechCrunch.com have converted the once-humble but spunky free Web diaries – orblogs, if you will -- into regular media entities.Huf ngton Post is now a phenomenon for“social news” while startups such as BlogAdda.com and InstaBlogs.com (which has beenventure funded already) are trying to break newpaths in journalism and media.

When 26/11 attacks were happening inMumbai, I was eagerly following one young manfrom a house close to the site describing thescene, even as mainstream television anchorscamped outside the Taj hotel in the nancialcapital of India.

It is almost routine for those who follow showbusiness, celebrity lifestyles or movie stars

to track the gures on Twitter or on Facebookfan pages. India is not there yet in terms of broadband penetration or widespread use of

the Internet, but we may be months away fromit all, as smartphones get cheaper and Indian-language content proliferates on the Net. I

tweet not just in English, but also occasionallyin Tamil, Hindi and French. It is a question of

time before the Internet, powered by growing economies of Asia, become a Tower of Babelin which conversations, news, comments andshared links ow back and forth.

A decade ago, a Website called Naked Newscreated a utter by hosting news in which the

News is naked:Are you still clothed?

newsreader does a striptease. Now, it seemsnews itself has become naked, as it faces alargely un ltered online world.

And I now call WikiLeaks the Al Qaeda of journalism.

So, what has changed in all these?

Here are my takeaway points on how newsmedia and Social Media are intersecting eachother.

Social Media is now mainstream:1.Newsbreaks are routine on Twitter orFacebook as companies, individuals andeven political parties share information on

the Net. All leading news organisations offernews on tweets, which when combined, have

the shape of a news wire.

Social Media are a countervailer:2. Newsnot just breaks on Social Media,but alsogets discussed there. This is what I call the“countervailing’ power of the Social Media onmainstream media, much like the consumermovement. Recently, when tapes of con dential conversations between lobbyistNiira Radia and journalists/industrialistswere published, the mainstream medialargely played down tapes involving themedia itself. A vir tual revolution on Twitterand Facebook gave way to prime-timeprogrammes in which TV channels turned

their oodlights on themselves.

One man’s editing is another man’s3.censorship: While mainsteam media“packages” news after “selecting” it, thereare those – especially celebrities, whoconsider that as unnecessary interference.Social Media enables them to cut through

the layer.

The Source is the News!:4. This is the21 st Century equivalent of the old saying

by Marshall McLuhan, “The mediumis the message” Celebrities, politicalspokespersons, industrialists, companies– they all have Twitter accounts or blogs

that enable them to publish directly. Formainstream media, this becomes a classiccase of “disintermediation” – somewhatlike what online commerce did to old shops.Mainstream media has to engage in the newreality.

Deal with it:5. You cannot ignore SocialMedia anymore whether you are a reader/viewer/surfer, a journalist, an advertiser, acorporate or a mainstream media publisheror broadcaster.

Don’t forget the hyperlink:6. News is not just being generated or discussed in SocialMedia. It is being shared. The intrinsicallyshared nature of online information, news,audio or video les dramatically alters socialbehaviour. This has huge implications fornearly all.

Business models will change:7. The emerging scenario is one in which mainstream andSocial Media will court each other in amanner that will change business models.How? That is the big question.

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 24/31

India Social Media Survey Edition 26 47India Social Media Survey Edition 2

Do you remember that advertisement you sawon Facebook, really liked it and fancied winning

the competition? Do you remember the numberof windows that you opened after that to nallyreach a place where it asked you to register forsomething and then claim? Are you a part of

those 760,002 people who really say “thumbsup” to a brand, like it and then forget about it?

I am sure you remember all this and are indeeda part of the Social Media revolution…in INDIA!

How many competitions did you eventuallywin? Or if I may ask, how much of shopping you recently did was inspired by the ads on thefavourite social network you visit every day?Well, I leave out the answer to you, as I am alsoone of all of you and a part of these networks,but as you would rightly guess, only to connectwith my friends who are either sitting far awayfrom me or whom I haven’t been able to get in

touch for long or share our upcoming events .

Anurag BatraChairman and Editor-in-Chief for

the exchange4media group

While doing all that does anything else attractmy attention? Well not sure about anything else,but the photographs of my friends attending parties….de nitely does!!!

The Social network(s) that you call social mediafrom the advertisers and marketer’s point of view is the buzz of the town today and everyoneseems to be trying to either teach this mediumor understand this medium or leverage thismedium or eventually making some senseout of this medium. Whatever the purpose,

the medium de nitely has caught attention of people! But how many people are these outof the total population of India? What is the

total reach of these mediums to an averageconsumer? What is the retention of the brandvalues this media creates? If I had the numbers,I would have de nitely revealed them to you, butfact is I don’t and thus my point on how effectivesocial media is as a media?

First thing that de nitely ring bells in my mindand raises a question mark to me, on theeffectiveness of social media as a tool foradvertising and marketing is the reach of thesemediums as a whole. While the numbers of

internet users as a whole is far less than othercountries in India, the social media users arede nitely quite a small lot. Now, many peoplewould counter argue my point saying that theseare the people who matter to the brands whoare advertising on these mediums and they are

their target TG’s. I agree to this point and take anote that India’s youth is quite hooked to thesemedia, but who is tracking how many of theseyouth are leaving these media after joining

Are Indian audiencesreally social?

them once? There is a signi cant fall off fromsocial media and burnout. Are we factoring theburnout numbers?

I remember the phenomenon that started3-4 years ago when not having an accounton “Orkut” was quite an unusual thing for anyurban youth. Orkut became the most popularsite with a huge member base especially inIndia. Advertising on Orkut had just star ted

owing in and the platform was just being made more viable for ads when it got a severeblow to its reputation following innumerablefake ids, misuse of its content and a gamut of other issues. While Orkut was just recovering

from the debacle, Facebook arrived, spreadand conquered. The question of “What’s yourOrkut ID soon became what’s your FB accountcalled?” Indian users still make just 3 millionof the existing 500 million plus subscribersof Facebook. And no one knows those whoare right now there, will be for how long? Whoknows how close we are to the next socialnetworking phenomenon. Twitter, as we allknow has been struggling to devise its nancialstrategies itself and a puzzle still to be solvedeven for marketers!

While social media takes you directly to your target TG, it doesn’t guarantee you attention,even though you are in front of them. Negativegoes viral but dedicated to the point campaign

takes time to even get noticed. Creativity doeshave a pull factor but there are no statistics onhow many people actually get off from these

things after getting involved at a certain point of time…..

“So… When was the last time you saw yourFriendster, Hi5, MySpace, LinkedIn, Jhoos,ibibo, apnacircle, Badoo, Xing, Mixi, Multiply,Ning…forgot amidst all…Orkut account?”

Now, what surprises me all the more is thegrowth in number of social media evangelistsavailable in this country, increasing exponentially every day. It looks like everyone

today has mastered the art of social mediaoptimization, web strategies and internetadvertising. Solutions to increase brandeffectiveness are available on zillions of websites and you have a promise to get the bestservices. In fact I would like to believe that thesocial media specialists are like the guys whoroam in your locality promising to clean your earwith archaic and dangerous tools. There are toomany promising too much and knowing it all. Iwould like to ask them what they know aboutbrand, audiences and messaging. Just because

they are 27 year old and spend a lot of timeon social media does not make them a socialmedia marketing expert. How are they using theinsights?

Talking about social media consultants I amreminded of a Scott Adams saying that seems

to mock at us all “Consultants have credibilitybecause they are not dumb enough to work atyour company”

But the question remains the same…has itreally caught the attention of the consumer inIndia? Is it turning the leads into sales? Well Ibelieve India still has a long time to go wheninternet especially social networks becomea great tool of attracting consumers towardsadvertisers. Also, the number of playersoperating in the system is unimaginable and itbecomes dif cult to nd the best.

My view is that India still needs to evolve alot in its online Social Media market to gain amomentum among its far reached, wide spreadconsumers. From a marketer point of view, untiland unless I see strong numbers as ROI, I wouldreally be wary to put my money where its worthis!

Time to “like” another brand, as my friendshas just suggested one to me…let me checkout, If I am eligible to win a Mercedes now…

8/6/2019 Blogworks India Social Media Report Edition 2 in Association With NM Incite Light Version

http://slidepdf.com/reader/full/blogworks-india-social-media-report-edition-2-in-association-with-nm-incite 25/31

India Social Media Survey Edition 28 49India Social Media Survey Edition 2

Measurement is de ned by dictionary.com as the act or process of ascertaining the extent,dimensions, or quantity of something.

Therefore, measurement of a Public Relationsprogramme would simply mean the act of ascertaining the extent, dimensions or quantityof what Public Relations programme hasachieved – the magical something.

So what is the magical something that a PublicRelations programme is expected to achieve?

Why is it considered the holy grail of PublicRelations – everyone knows about its existencebut not able to nd it? Why it is that only a fewuse it to their bene t? Is it because the role of Public Relations itself is not well understood orappreciated?

I believe that Public Relations if often seenmerely as the act of gaining favourable presscoverage and hence the measurement of its

Ashwani Singla Chief Executive Of cer, Penn Schoen Berland

impact is limited to the extent of the favourablepress coverage it was able to garner. This is

the beginning of the long journey of measuring public relations.

Given that, the measure of its successpredominantly became “Advertising ValueEquivalent” or AVE, which translates into theadvertising value of the editorial exposurereceived by a company. Many continue to use

this benchmark to measure the success of theirpublicity programme under the garb of a PublicRelations campaign.

The rst cousin of AVE is often “Number of Press Impressions” meaning the number of people who might have had the opportunity

to be exposed to a story that has appeared in the media; usually refers to the total auditedcirculation of a publication or the audiencereach of a broadcast vehicle. I call it the ‘thudfactor’ or the success of the programme being measured by whose ‘coverage dossier’ washeavier! Though, at the point of extinction, somestill continue to use this archaic methodology tobenchmark their Public Relations programmes!

Time/space measures or variations of itcontinue to be the predominant way to measureof the impact of public relations programmeand this will continue to be the case as long asPublic Relations is narrowly used for mere pressrelations.

So is there more to it than press relations?Instead of elaborating the virtues of public

Measurement – Is it the holygrail of public relations?

relations, I want to focus on the establishing a common understanding of it that helps usunderstand what and how to measure theimpact of a public relations campaign.

Public Relations is described in many ways butin the essence it remains “ the act of generating

goodwill or mutual understanding between acompany and its various publics/stakeholders.”

In the early 1900s Edward Louis Bernays ,considered the founding father of modern PublicRelations along with Ivy Lee , de ned PublicRelations as “ a management function whichtabulates public attitudes, de nes the policies,

procedures and interest of an organisationfollowed by executing a program of action toearn public understanding and acceptance ”

Robert L. Heath describes Public Relations in the Encyclopedia of Public Relations as a “ setof management, supervisory, and technicalfunctions that foster an organisation’s ability to strategically listen to, appreciate, andrespond to those persons whose mutually bene cial relationships with the organisationare necessary if it is to achieve its missions andvalues .”

Essentially it is a management function thatfocuses on two-way communication andfostering of mutually bene cial relationshipsbetween an organisation and its publics.According to the Public Relations Societyof America (PRSA), the functions of PublicRelations include research, planning,

communications dialogue and evaluation.

It would seem that Public relations isabout changing attitudes to gain public’sunderstanding and acceptance. Publicsmeaning stakeholders whose understanding and acceptance is material to the success of the company. This achieved through a two-way communication .

I had earlier described measurement as theact or process of ascertaining the extent,dimensions, or quantity of something. So, if wewere to put together Bernays, Lee and Heath’sde nition with that of measurement, what canwe conclude about measuring the impact of Public Relations?

As I understand, measuring the effectivenessof the Public Relations programme should beabout the change in attitude, understanding gained and acceptance received from

the stakeholders of a company whilst the measurement of the ef ciency of thecommunication process would be about therelevance of the medium and the message usedbetween the sender and the recipient.

Shouldn’t we use our knowledge of the true value of public relations to measureboth effectiveness and ef ciency of thecommunication process or continue to follow

the age-old practice of time and share in thepress alone?

The answer stares us in the face. Indian publicrelations professionals can learn from the

journey that their western colleagues havemade and make a leap that brings the role andimpact of public relations into the C Suite.

As Bernays and Lee explain in their de nition itis “a management function that tabulates publicattitude…”

Effectiveness of public relations has to be about