40

| Date post: | 25-Oct-2015 |

| Category: |

Documents |

| Upload: | vaibhav-garg |

| View: | 13 times |

| Download: | 1 times |

Dear Reader,

Welcome to the special issue of Blue Chip!

At a time when few of us have joined our dream col-

leges while others complete a year of MBA, Blue Chip

proudly celebrates its first anniversary and presents its

special issue from a new editorial team. Taking the ba-

ton forward from the progenitors of Blue Chip, we look

forward to the coming year with hope and optimism.

To make the anniversary issue of Blue Chip special, we

introduce a new section wherein our team members

share their summer internship experiences across vari-

ous companies and functions in finance and economics.

This issue’s cover article is about the current situation

of the insurance sector in India, and prescribes a dosage

of bancassurance, increased FDI and micro-insurance

to help this sector pick up speed and reach the next

stage of growth.

Retaining popular sections from the last issue, this time

we talk about Current Account Deficit in the Beginners’

Section and present a review of the movie Too Big To

Fail. For the inquisitive minds, a tutorial on Inflation

Indexed Bonds is included, and to exercise your grey

cells, we offer you a crossword.

From the entire Blue Chip team, here’s wishing all our

readers all the best for their new phase of life.

Be happy. Do good. Stay sane.

And most importantly, Keep reading.

~ Editors for Blue Chip

BLUE CHIP

ISSUE 4

All images, artwork and design

are copyright of Monetrix,

The Finance and

Economics Club of

MDI, Gurgaon

The Team

Cover Page photo

Source: ibnlive.in.com

For any information or feedback,

please feel free to write in to us at

OR visit our Facebook page

www.facebook.com/

From the Editor’s Desk

Editorial Team

Ashish Gupta

Nidhi Soni

Content Creators

Amit Agarwalla

Daman Aggarwal

Karan Jaidka

Radhika Bhattar

Rishabh Gupta

Rishi Maheshwari

Rohit Agarwal

Sankalp Raghuvanshi

Saurabh Saxena

Saurav Singh

Shaunak Laad

Swapnil Sheth

Vibhav Srivastava

Tutorial ( 12

Inflation Indexed bonds

Capital Account Convertibility ( 27

Capital Account Converti-

bility of China by 2015

Business Quiz ( 33

Crossword

P.E. in India 8

A perspective on P.E. in India

Market Update ( 36

Stock Market Update

In the News

Beginners’ Corner ( 20

Current Account Deficit

A radical solution to a

rational problem ( 4

Through the eyes of

finance students

Wipro Limited | Goldman Sachs

Axis Bank | HSBC Bank

Summer Internship Ex-periences ( 23

Cover Article ( 14

Insuring India

The way forward

Movie Review ( 35

Too Big To Fail Rupee ( 30

Rupee on a Wheel Chair

Contents

4

© Monetrix, Finance & Economics Club of MDI, Gurgaon

The Indian Banking Sector that was considered

sufficiently robust to cushion the challenges

posted by the global meltdown has been wit-

nessing some problems of its own lately. The

rising NPA’s and Cost of Funds/Deposits are a

matter of concern. This shifts focus on how to

reduce the two. Here, I am concerned with the

latter.

Banks accept deposits in form of Demand De-

posits and Term Deposits. Current Account and

Savings Account Deposits (CASA) are a part of

Demand Deposits.

CASA deposits, also known as low cost deposits

are considered to be the cheapest source of

funds available to banks. They refer to deposits

made in Savings (SB) and Current (CD) Ac-

counts. In CASA deposits, the banks pay interest

on Savings Accounts but not on funds main-

tained with Current Accounts (So ideally they

should try to have more and more funds in the

Current Accounts).

Banks borrow money from various sources at

some interest and lend that money at higher

rates to book profits. The sources of funds being

- RBI (borrowed at prevalent repo rates), short

term call money market, CASA deposits and

term deposits among others. CASA deposits are

the traditional source of income for the banks.

These Deposits help bank to generate low cost

funds which are then used for advances/

investments or to maintain liquidity for day-to-

day operations.

Also, absence of these low-cost funds in consid-

erable amounts will not allow the banks to lower

interest rates for the end-user because if a bank

starts with a high cost deposit base then to earn

a profit you have to lend at high rates, effectively

taking on more risks. High cost of deposits

reduces the profit margins for the bank and

increases reliance on short term borrowings.

The banks which have been performing rela-

tively better have a larger share of CASA de-

posits in total deposits and within CASA also,

the share of Current Account deposits is of

considerable percentage. For example, for the

Fiscal Year 2012-13 HDFC Bank had a CA

Deposits share of 37.23% of the total CASA

deposits, while Central Bank of India has a CA

Deposits share of only 20.37% which is among

the lowest in the industry, hence, it is of no

surprise that the cost of deposits for it is

among the highest in the Indian Banking sector

(7.42%).

For Central Bank of India the Cost of Deposits

have been rising steadily over the past few

years while the CASA share of Total Deposits

has been decreasing. By analyzing and plotting

some graphs for past few years we can arrive at

some conclusions. Firstly, it points to an in-

verse relationship between the CASA share of

Total Deposits and Cost of Deposits. Also the

share of Term Deposits in total deposits has

been increasing over the years.

As bank pays more interest on Term deposits

than CASA deposits, it leads to considerable

expenditure. Hence, there is a direct relation-

ship between the Term Deposits share of total

deposits and cost of Deposits.

So the aim is to find out ways by which the

cost of deposits and funds can be reduced. Af-

ter RBI de-regulated interest rate payment on

Savings Accounts many banks like Kotak

Mahindra, Yes Bank etc. started offering higher

interest rates on Savings Accounts with an aim

A RADICAL SOLUTION TO A RATIONAL PROBLEM

A Radical Solution to a Rational Problem

PGDM (2012-14)-2nd Year

IMI, New Delhi Soumya Sharma

5

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

of increasing their CASA deposits as they recog-

nize the cost benefits associated with it. The

schemes have helped these banks gain a lot of

mileage and they are still gaining traction from

them. As a matter of fact Yes Bank registered a

growth rate of 206.4% in its savings account port-

folio in the Fiscal Year 2011-12 (the scheme offer-

ing higher interest rates was launched in October,

2011). These banks could offer the differentiated

rates because their Savings Bank Balance as of to-

day is low as compared to older, more estab-

lished banks. The older banks have a very

large Savings Account base so the cost of

offering higher interest rates is huge for

them. The increment required in the savings

account balance to offset the increased ex-

penditure if the higher rates were to be of-

fered will be very unrealistic. (Banks will gain

interest by investing or lending out addi-

tional funds which will help in negating the

Figure 2: Growth Rate of Term deposits and Cost of deposits, Cost of Funds over the past four

years for Central Bank of India

Figure 1: Growth Rate of CASA Deposits and Cost of Deposits over the past four years for

Central Bank of India.

The CASA

share of total

Deposits is

decreasing.

Cost of Funds

as well as

Cost of De-

posits has

been increas-

ing.

The Term De-

posit share of

total Deposits

has been in-

creasing.

Cost of Depos-

its and Cost of

Funds has been

increasing.

A RADICAL SOLUTION TO A RATIONAL PROBLEM

6

© Monetrix, Finance & Economics Club of MDI, Gurgaon

Money from these mutual funds can be re-

deemed within 24 hours. The mutual funds

lend this money to the short term Call Money

Market, from where the banks borrow to

maintain their liquidity requirements at very

high interest rates. Hence, the money which

could have been deposited in the Current Ac-

counts if they were to offer even a customary

rate has come back to the bank but at a much

higher cost.

The impact that this proposal might have on

the bottom-line of the bank can be offset by

interest income that the bank will receive

once it invests or lends out the additional

money that is attracted through the scheme at

higher rates. Also, banks should be allowed to

decide the interest rates that they want to of-

fer, on the basis of, the perceived impact on

their financials, and the estimated growth

prospects by launching of the scheme.

For certain banks like Central Bank of India

which have a low Current Account Balance,

the proposal to offer interest rates on these

accounts means maximum benefit. In fact

their situation can well be termed as a bless-

ing in disguise.

The fact that it has only 20% of its CASA

funds as Current Account Balances means

that it will have considerable advantage with

respect to other banks if we assume all were

to offer interest on Current Accounts.

As mentioned above, the expenditure in-

curred due to this scheme can be offset by

deploying the additional funds generated in

form of advances. Also the bank does not

have to pay interest on whole of its Current

Account Portfolio, some riders like the mini-

mum monthly balance requirement to be eli-

gible for the scheme will lower the number of

expenditure)

The problem is more pronounced in case of Pub-

lic Sector Banks-CASA as a share of Total De-

posits has been decreasing and so is the share of

Current Accounts in CASA. These banks are

mostly left with the customers who are very loyal

to them while others(savings and current account

customers) are being poached by private sector

banks by providing better services and in some

cases higher interest rates.

So the solution. RBI should allow banks to offer

interest on Current Accounts as well. Currently

no interest is paid on Current Account deposits

which has not only deprived banks of deposits at

cheaper rates but has also resulted in money from

current accounts flowing into other markets and

mutual funds. Banks like State Bank of India are

in talks with RBI for de-regulation of interest

rates on Current Accounts.

Infact, Mr Pradip Chaudhuri (Chairman, State

Bank of India) has advocated for a 2% interest on

Current Accounts to attract cash lying in the

hands of businesses.

As of now, Banks cannot accept term deposits

for periods that are less than seven days, hence

the corporates instead of depositing their excess

money in the current accounts which bear them

no interest, prefer investing with mutual funds.

A RADICAL SOLUTION TO A RATIONAL PROBLEM

Figure 3: Current & Savings Account as a Share

of Total Deposits for select commercial banks

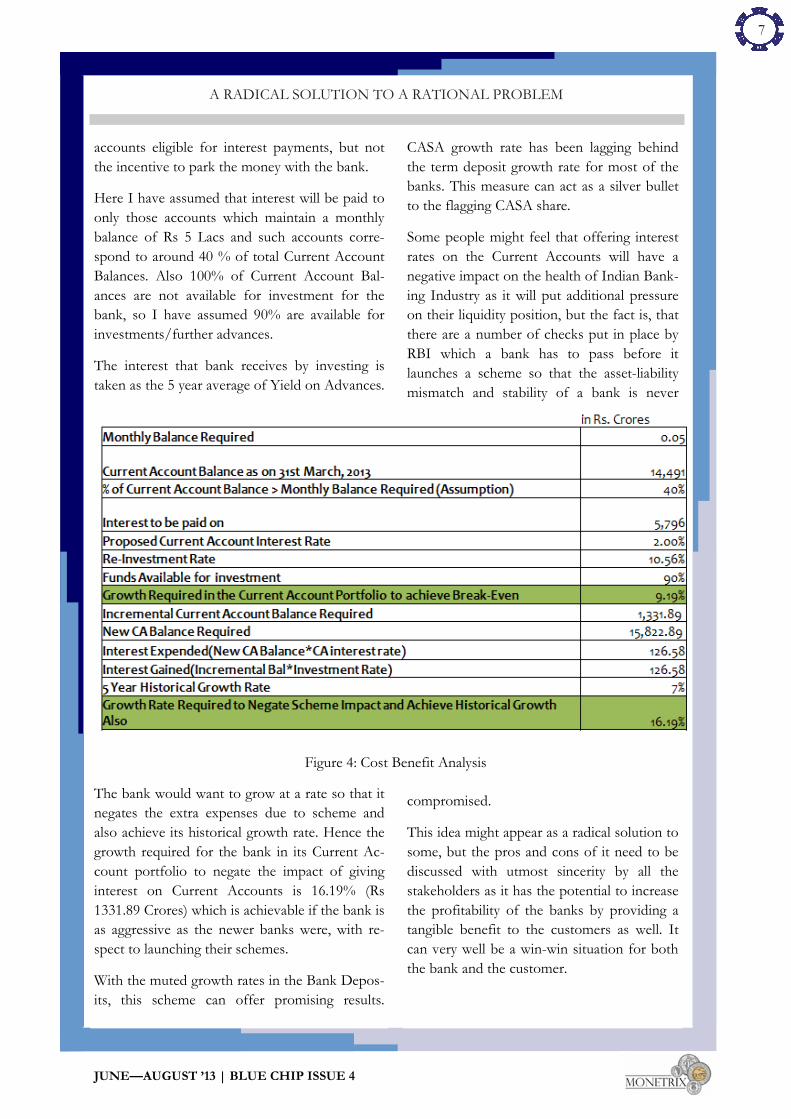

Cost Benefit Analysis for a PSU bank

if 2% Interest Rate were to be offered

7

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

accounts eligible for interest payments, but not

the incentive to park the money with the bank.

Here I have assumed that interest will be paid to

only those accounts which maintain a monthly

balance of Rs 5 Lacs and such accounts corre-

spond to around 40 % of total Current Account

Balances. Also 100% of Current Account Bal-

ances are not available for investment for the

bank, so I have assumed 90% are available for

investments/further advances.

The interest that bank receives by investing is

taken as the 5 year average of Yield on Advances.

The bank would want to grow at a rate so that it

negates the extra expenses due to scheme and

also achieve its historical growth rate. Hence the

growth required for the bank in its Current Ac-

count portfolio to negate the impact of giving

interest on Current Accounts is 16.19% (Rs

1331.89 Crores) which is achievable if the bank is

as aggressive as the newer banks were, with re-

spect to launching their schemes.

With the muted growth rates in the Bank Depos-

its, this scheme can offer promising results.

CASA growth rate has been lagging behind

the term deposit growth rate for most of the

banks. This measure can act as a silver bullet

to the flagging CASA share.

Some people might feel that offering interest

rates on the Current Accounts will have a

negative impact on the health of Indian Bank-

ing Industry as it will put additional pressure

on their liquidity position, but the fact is, that

there are a number of checks put in place by

RBI which a bank has to pass before it

launches a scheme so that the asset-liability

mismatch and stability of a bank is never

compromised.

This idea might appear as a radical solution to

some, but the pros and cons of it need to be

discussed with utmost sincerity by all the

stakeholders as it has the potential to increase

the profitability of the banks by providing a

tangible benefit to the customers as well. It

can very well be a win-win situation for both

the bank and the customer.

A RADICAL SOLUTION TO A RATIONAL PROBLEM

Figure 4: Cost Benefit Analysis

8

© Monetrix, Finance & Economics Club of MDI, Gurgaon

The Indian corporate scene has witnessed a dra-

matic transformation in the past decade. Private

equity was a niche domain in India, a relatively

unheard term till 2004. But there has been a

complete overhaul in the story ever since 2007,

with the emergence of companies owned and

supported by Private Equity and a number of

global Private Equity firms flush with funds set

up business in India.

Lerner (1999) defined Private Equity organiza-

tions as partnerships specializing in venture capi-

tal, leveraged buyouts (LBOs), mezzanine invest-

ments, build-ups, distressed debt and other re-

lated investments. Today, the Indian industry

covers the entire spectrum of private equity

products including seed funding, expansion capi-

tal, buyout financing, financing restructuring of

companies and providing mezzanine capital

across a variety of sectors.

Cumming and Walz (2007) analysed the drivers

behind institutional investors investment in pri-

vate equity firms. They conclude that institu-

tional investors are inclined to invest in PE firms

in economies which have strong disclosure stan-

dards, congenial legal environment, stable econ-

omy and robust financial markets.

Private equity funds attract huge amounts of

capital from investors, including pension funds,

insurance funds, universities, foundations and

individuals who are looking for new investment

avenues. The allure of rapid growth has attracted

more and more foreign investors to India. This

has been strengthened by liberalisation of For-

eign Direct Investment norms. This segment has

now reached significant scale. Till date there are

2000 companies in which Private Equity firms

have invested and this amount ranges in ex-

cess of $ 65 billion over the past eight years.

Private Equity has proved to be beneficial for

small and medium enterprises (SMEs) in India

looking for alternative methods of fundraising.

They get much needed resources for opera-

tional expansion and are enabled to access

global markets. Entrepreneurs also get a boost

and private equity funding in their businesses

adds to India Inc’s growth story.

E-commerce emerged as an attractive sector

for Private Equity investment in 2012 owing

to the ever increasing internet accessibility and

percolation in Tier II and Tier III cities in In-

dia. Investment in sectors such as healthcare,

FMCG, food, agriculture, dairy products and

other consumer focused businesses are also

being viewed as attractive.

In this article we take stock of the state of pri-

vate equity in India including the prospects

and implications and what the future holds for

PE investments in India Inc.

Top Deals of 2012

While the PE boom witnessed in 2007 and

2008 is yet to be seen again, the private equity

scenario in India showed sustained momen-

tum and clocked a total of 400 deals in 2012

amounting to USD 7.35 billion. The top sec-

tors that attracted the most amount of PE

investment in 2012 were IT and ITes, Pharma,

Healthcare and Biotech, Banking and Finan-

cial Services Industries, Real Estate and Power

and Energy.

A PERSPECTIVE ON P.E. IN INDIA

A Perspective on P.E. in India

PGDM, 2013-15 XIMB

Tanvi Randhar Soveet Gupta

9

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

The top private equity investments of 2012 were

seen in the BPO sector with Bain investing in

Genpact and Morgan Stanley investing in the Sin-

gapore based Continuum which is developing

wind assets in Kutch, Gujarat. E-commerce and

healthcare industries also attracted major invest-

ments. This was seen in

the case of Accel’s $50 million investment in Flip-

kart as well as a combined total of $ 100 million

in the four deals that took place in the hospital

segment as well as a total of $1,225 million across

48 deals in the healthcare and life sciences indus-

try. Banking and Financial services industry ac-

counted for $ 890 million across 43 deals fol-

lowed by energy companies that attracted invest-

ments worth $478 million across 20 investments.

Thus it was observed that the trend that was seen

in 2011 with respect to investment in the IT sec-

tor continued in 2012 as well with the sector ac-

counting for 28% and 35% in terms of value and

volume respectively, thereby becoming the most

preferred sector for private equity investment.

Demographically speaking, companies in

South India attracted the most number of

investments by way of 162 deals amounting

to $2,460 million while companies in Western

India attracted the maximum capital amount-

ing to $3,799 million across 126 deals.

Impact of various Governmental Policies

2012 has been a volatile year for markets

worldwide. With Europe reeling under the

Eurozone crisis and the countries unable to

come up with a consensus with respect to

developing a coherent fiscal policy and the

US averting the fiscal cliff, Asia still showed a

positive growth story especially with respect

to Indian and Chinese markets vis a vis

Europe and America but this does not dis-

count the fact that China reported only a 7%

increase in GDP and India saw a drop to ap-

proximately 5% GDP growth.

It has been a tough year for the PE sector in

India. Unrest on the political and economic

fronts has contributed to the woes. Several

A PERSPECTIVE ON P.E. IN INDIA

Acquirer Target Company Sector Stake

Valuation

( US $ mn)

Bain Capital Genpact Ltd IT and ITes 30% 1000

Morgan Stanley Continuum Wind

Energy

Power and

energy 210

Blackstone Embassy Property

Developments Real estate 50% 200

Accel Partners and Global

Management LLC

Flipkart Online

Services IT and ITes 150

Macquarie SBI Infrastruc-

ture Fund, SBI Macquarie

Infrastructure Trust

Ashoka Conces-

sions Ltd.

Infrastructure

Management 150

Figure 1: Top PE Deals in 2012

10

© Monetrix, Finance & Economics Club of MDI, Gurgaon

controversies ranging from protests against cor-

ruption and the various scandals as well as the

the debate over Foreign Direct Investment (FDI)

in the retail and aviation sectors hampered the

market sentiments at the outset of the year.

Furthermore, the Vodafone controversy brought

a lot of uncertainty in the minds of the investors

and they became wary with respect to the Indian

government’s tough stance with respect to retro-

spective taxation policies. This was harmful for

the investment climate in the country.

The union budget for the year 2013-2014 was a

cause for disappointment for the PE industry

since it did not accord the pass through status to

all funds registered under the Alternative Invest-

ment Fund (AIF) regulations ignoring SME

funds, social venture funds and infrastructure

funds.

One of the major amendments in the budget was

the change of taxability in relation to buyback of

shares. The liability to pay tax at the rate of 20%

on the consideration paid for buy-back of

unlisted shares in excess of the issue price of

such shares will now be of the company. This

amendment was introduced so that unlisted

companies that had been resorting to buyback of

shares instead of payment of dividend in order to

avoid incidence of dividend distribution tax, es-

pecially wherein capital gains to shareholders on

account of such buyback were either not charge-

able to tax such as in case of investments routed

from DTAA territories such as Mauritius or

were taxable at a lower rate.

Furthermore, there was a deferment in imple-

mentation of GAAR to 2016-17, thereby giving

enough time to investors to adapt to the new

regulations. It is also hoped that by then there

will be clarity on what certain ambiguous terms

in the provisions imply.

In addition to this the government also im-

posed a higher tax surcharge of 10% on indi-

viduals whose income exceeded INR 10 million

and corporates whose taxable income exceeded

INR 100 million. Overall, there were concerns

in the minds of investors with respect to India’s

feasibility as an investment destination.

Trends

The Indian private equity sector witnessed a

downfall in investment during 2012. One of the

primary reasons for this decline was that the

LPs have been getting increasingly cautious

with fund allocation, doing their due diligence

with tremendous care before committing funds.

A total of $7.4 billion were allocated, represent-

ing a 16% decline as compared to the $8.8 bil-

lion invested in 2011.

Deal flow was restrained by high inflation that

spilled over from 2011 and continued for most

of the year, ending at an average of 7.5%.

Weakening rupee and low Index of Industrial

Production growth, which was negative in some

months (0.1% in April, -1.8% in June, -0.2% in

July), also affected investor confidence.

On the brighter side, the number of deals actu-

ally rose from 373 deals in 2011 to 400 deals in

2012. The shrinking size of the deals meant that

the value of funds put to work over the year

dropped.

Overall, 2012 could be viewed as a year of cau-

tion for the Indian PE industry. The market

seems to be moving towards maturity, with PE

A PERSPECTIVE ON P.E. IN INDIA

Figure 2: Total PE investments (value, 2005-12)

11

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

being favourably viewed as a credible source of

capital by promoters and PE firms growing in-

creasingly careful about the deals they make.

Exits

On a brighter note, 2012 turned out to be a good

year in terms of exits. Their number rose consid-

erably - 115 (valued at about $7 billion) vs. 88 in

2011 (valued at about $4.1 billion). PE firms con-

tinued to prefer public market sales, including

IPOs, as the exit route. Additionally, the financial

sector accounted for 35% of the total number of

exits, including the major ones as listed in

Figure 3.

Going Forward

The year 2012 has been one of turbulence for the

PE sector. But there is much to look forward to

in 2013. Despite a slower growth of the econ-

omy, GDP continues to rise, paving way for an

increased trade flow, industrial production and

consumer spending. And with the economy

opening up to FDI in the retail sector, invest-

ments are expected to get a boost. Sectors which

support retail back end, including logistics and

warehousing, food processing and more, will

become more attractive.

Further, Indian promoters are adopting a more

pragmatic viewpoint, which creates an oppor-

tunity for PE funds to target companies with a

healthy operating model, but have been the

victim of unrealistic expansion plans or medio-

cre capital structures. Investing aside, PE firms

will also be looking forward to raising more

funds from the global community, which will

serve as a good indicator of India Inc.’s image

as an investment ground.

However, concerns about returns, especially

the ones made during the boom years of 2004

to 2007 remain. There is a mounting pressure

on exits since a number of investments have

exceeded their 5 year holding period. PE firms

will have to devise appropriate strategies to

overcome these challenges and more in the

coming years.

But we should not forget that India today has

amplitude of entrepreneurial talent, the largest

English speaking population with a high num-

ber of university graduates and a rising middle

class that is rapidly developing an appetite for

western lifestyle. Private Equity is just the cata-

lyst that such a potentially explosive combina-

tion needs for a frantic span of economic

activity.

A PERSPECTIVE ON P.E. IN INDIA

Target Seller Exit Type of Exit Value (US $

mn)

HDFC Carlyle Asia Partners II Open Market 841

Genpact Ltd. General Atlantic, Oak Hill

Capital Partners Secondary Sale 1000

Kotak Mahindra Bank

Ltd. Warburg Pincus India Open Market 272

ICICI Bank Ltd. Temasek Holdings Advisors

India Open Market 298

HDFC Carlyle Asia Partners II Open Market 270

Figure 3: Top PE Exits in 2012

12

© Monetrix, Finance & Economics Club of MDI, Gurgaon

have historically shown low correlations with commodities, equities and other assets and hence help in diversifying a portfolio and in turn improve risk-adjusted returns.

One main disadvantage of IIBs is the liquidity concern as not all the countries have deep and liquid IIB market.

Key terms

Real yield: The real yield of an inflation-linked bond represents the annualized growth rate of purchasing power earned by holding the secu-rity to maturity.

Nominal Yield: The nominal yield realized by holding an inflation linked bond to maturity depends on the average level and trajectory of inflation over the bond’s lifetime. The realized nominal yield can be approximated, by ignoring the trajectory of the inflation rate.

Break-Even Inflation Rate: It is the rate that results in the holder of an IIB bond to break even with the holder of a nominal bond. Inves-tors would earn a higher return holding IIBs with lower inflation risk if the actual inflation rate over the term of the bond is higher than the break-even inflation rate.

Break-Even Inflation Rate tells us about the market participants’ average inflation expecta-tions over the rest of the term of the bonds used in calculating BIER. However, since infla-tion-indexed bond markets are not as liquid as nominal bond market it may lead to a higher liquidity premium in the yields of IIBs which, probably, will tend to bias the BIER downwards.

Inflation is the key driver of investment per-formance. It can erode common man’s purchas-ing power. Inflation reduces the real return gen-erated by any asset. Inflation Indexed Bonds (IIBs) are financial instrument to protect inves-tors from inflation. The principal and interest payments of IIBs rise and fall with inflation as these payments are based on Consumer Price Index (CPI), Wholesale Price Index (WPI) or any other inflation index.

IIBs popularity amongst investors has been ris-ing over the years as investments in money mar-ket, savings account or nominal bonds expose investors to inflation risk and may lead to lower or even negative real return.

IIBs can be of various types depending on the fact if only the principal or both principal and coupon payments are linked to inflation. IIBs’ prices are inversely related to real yield. There-fore, in deflationary scenario, the principal amount could decline below the par value. How-ever, many governments pay the greater of the initial par value or the inflation adjusted princi-pal. This provision provided to the investors is known as deflation floor at maturity.

Potential advantages of IIBs

IIBs are a good hedge against inflation. Apart from protecting against inflation risk, IIBs are less volatile and enhance diversification. IIBs

TUTORIAL

Inflation Indexed Bonds

Figure 1: Barclays Universal Government In-

flation-Linked All Maturities Bond Index as

of December 2011

13

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

will take some time to stabilize and monetary policy has been targeting WPI for achieving price stability.

IIBs issued by RBI will not have any special tax treatment. FIIs are allowed to invest in IIBs but subject to the overall cap for their investment in G-Secs, which is currently $25 billion. IIBs are G-Sec and therefore would be eligible for short-sale and repo transactions.

Illustration

A 10 year IIB with coupon of 2% was issued on Mar 15, 2010, with the first coupon payment due on Sep 15, 2010. The reference WPI on issue date was 125 and the reference WPI on coupon due date was 140. For a face amount of Rs 1,000 the inflation adjusted principal on Sep 15, 2010 would be:

Rs 1,000 * (140/120) = Rs 1,166.67

The coupon payment on Sep 15, 2010, would be calculated using adjusted principal amount and the applicable coupon rate as follows

Rs 1,166.67 * (0.02/2) = Rs 11.67

Moral Hazard

Some economists argue that, generally, govern-ment is both the issuer of IIBs and publisher of the inflation index. This creates a moral hazard because the government can directly influence the value of its liability. However, some econo-mists believe that such an act of distorting infla-tion index might lead to erosion of govern-ment’s credibility with long-term repercussions on future government promises. Therefore, no government would dare to do so as the long term repercussions would greatly outweigh the short term benefits.

IIBs help issuers reduce their cost of financing because investors are ready to pay a premium for protection against inflation and this pre-mium reflects in a lower yield paid by the issuer. It is also argued that issuance of IIBs have a fa-vourable impact on the issuer’s cost of financing by reducing the desired inflation risk premium from the rest of the nominal bond. However, IIBs expose issuers to the inflation risk.

IIBs in Indian context

Inflation has been consistently high in the past few years in India. Interest rate offered by banks’ products and other financial instruments were not meeting the expected return of Indians which led to a shift from financial assets to physical asset. Indians started increasing their gold holdings which to an extent deteriorated India’s CAD. The government tried various measures to curb gold import without any con-siderable success.

Ultimately in June 2013, RBI issued 10 years IIB to offer better real returns to investors. The first issuance was worth Rs 1000 crore at a real yield of 1.44% and was oversubscribed with a bid to cover ratio greater than four. The coupon rate of 1.44% will be a fixed real rate. This rate is determined through auction and remains con-stant for the bond’s tenor. The first issuance of IIB was open to institutional investors, however, exclusive series for retail investors is scheduled to launch around October 2013.

IIBs are not new to the Indian market. Capital Indexed Bonds (CIBs) were issued in 1997 but CIBs provided protection only to principal and not to the coupon payments. However, this time around RBI filled the void by providing protec-tion to both coupon payments and the principal. IIBs have a deflation floor or capital protection scheme which means that at the time of re-demption higher of the adjusted principal and face value will be paid to the investors.

RBI has linked IIBs to WPI rather than CPI which is a concern for the investors as they are primarily exposed to CPI and not WPI. As per RBI, out of WPI, CPI and GDP Deflator, WPI was most suitable for indexing. The argument given by RBI for picking WPI is that CPI, in India, is being released since January 2011 and it

TUTORIAL

RBI criteria for selecting the index to which IIBs should

be linked

The index should:

● Fulfill hedging require-

ments

● Closely track inflation

● Be a widely accepted indi-

cator of inflation

● Be available to the public

● Have a high frequency of

14

© Monetrix, Finance & Economics Club of MDI, Gurgaon

companies got merged to form LIC. It enjoyed

a monopoly for 38 long years till the former

Governor of RBI Mr R N Malhotra submitted

a Report in 1994 recommending opening of

insurance sector. Eventually, the4 Insurance

Regulatory and Development Authority was

formed in 1999 which is the main regulator for

Insurance in India. It is the main authority in

India with responsibility to protect the rights of

policyholders, make modifications, cancella-

tions renewals of all the insurance companies

registered under it. Recently, IRDA has made it

better for the companies to raise capital by al-

lowing life insurance companies which have

completed 10 years to come out with IPOs.

The empowerment and flexibility to frame

regulations will help IRD promote sustainable

growth of the insurance sector.

If we see the current situation, Insurance Pene-

tration in India is rather low. It is measured as

Ratio of Total Premium Underwritten to the

Insurance in general works on the principle that

if we collectively pool our money, we can safe-

guard ourselves in circumstances which are rare

and damaging. In simple terms, if everybody

pays a portion of the threat faced by them, the

collective pool may help them in the times of

need. For a country with a 1.2 billion population

like India, it is very critical to have such institu-

tions and markets as people face constant

threats from getting run over by a careless driver

to a fraud to natural calamities. Insurance is

mainly classified as Life Insurance and Non-Life

Insurance or General Insurance (Health, Prop-

erty & Casualty, Disability and Long-Term

Care).

Need of Insurance for an Economy

Insurance decreases the total Savings of the

Economy - It has been observed that as more

and more people get insured, they tend to save

less with themselves for precautionary measures

and hence the individual savings of the economy

reduce. This money is instead transferred to the

insurance companies which through various

channels can be utilised for investments and

other potential development projects thus in-

creasing the GDP for a country. It is worthwhile

to note that while the insurance companies have

steady, regular cash inflow in the form of pre-

mium, the cash outflow is generally deferred for

a long time. So the investment horizon is gener-

ally long term, which benefits the long term

markets and lengthy infrastructure projects.

Insurance in India

The origin of insurance in India dates as back as

1818 when Oriental Life Insurance Company

was set up in Calcutta. Over the years many

laws, policies and acts got passed and after inde-

pendence, in 1956, a total of 245 insurance

COVER ARTICLE

Insuring India - The Way Forward

In May 2013, Raghuram Rajan, the soon

to be RBI governor, pitched for the ap-

proval of increasing the FDI in insurance

limit to 49%. With this tenure set to be-

gin next month, this brings insurance

sector, the under-nourished child of the

financial services industry, in the fore-

front. This article looks at status quo of

insurance in India and ways to make this

under-nourished child a healthy one with

a prescription of bancassurance, in-

creased FDI and micro-insurance.

15

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

15

necessary product in majority of the segments.

Hence spending on insurance tend to be dis-

cretionary.

4. Complexity involved in Settlement - Al-

though increased

competition has

forced the companies

to be quick and sim-

ple in modes of set-

tlement, it is still per-

ceived by the masses

that insurance, spe-

cially general insur-

ance has complex

terms of contract and

settlement involves

lot of hassles.

5. Macroscopically, If

we see the age of India, it is reaping its demo-

graphic dividend. It is young and comparing

GDP of a country. India stands at a meagre

3.4% compared to other Asian Countries like

Taiwan, Hong Kong which have Insurance

Penetration of more than 10%. However during

the last decade the insurance Market has grown

at a staggering 25% year on year.

Challenges in Insurance Penetra-

tion

in India

1. Lack of Transparency in Insur-

ance Policies - Indian mindset is

fearful. There is a constant fear of

being cheated by Insurance Compa-

nies. Insurance is a push product

rather than a pull product. Compa-

nies have to call people, regularly

advertise, spend a lot of money to

make people aware of the risks they

face in order to get customers.

2. Perceived Lack of Short Term

benefits - The benefits of insurance

will always be felt at times of a ca-

lamity. Paying regular premium is

always seen as a burden in the eyes

of an Indian earning a meager sum.

3. Insurance is not yet deemed as

COVER ARTICLE

Figure 1: Indian Insurance Market, 2004-2015

Figure 2: Percentage of Population above 60 years for a few

countries

16

© Monetrix, Finance & Economics Club of MDI, Gurgaon

● To improve the current level of services of-

fered in the insurance sector through in-

creased competition among the existing

companies ensuring better standards

Bancassurance in the World

Banks have been in existence since as early as

1472 (Monte dei Paschi di Siena of Italy) and

the first life insurance company was Amicable

Society for a Perpetual Assurance Office which

started in 1706. In those terms, even for the

world, Bancassurance is relatively new. France

has had Bancassurance only since past 30 years.

Benefits of Bancassurance

For the Banks

Because of increasing competition, banks have

found their Net Interest Margins reducing

which is an indicator of their margins thinning

out. Not only that, but bancassurance can also

What is Bancassurance?

Bancassurance is a Portmanteau of Bank and

Insurance. In simple words, Bancassurance

means selling insurance products through banks

existing distribution channels. However it does-

n't only mean distribution through agents, but an

overall integral approach towards legal, cultural,

behavioural, fiscal aspects of Banking and

Insurance.

Referral Model

In this model the bank parts only the client data-

base to the insurance company and the insurance

company sells the insurance to the prospective

customer by itself. The bank in return gets a re-

ferral fee

Corporate Agency

In the corporate agency model, the bank staff is

trained to sell the insurance products and

charges an appropriate fee from the insurance

company

Insurance as Fully Integrated Financial

Services/Joint Ventures

Apart from the above two, a fully integrated

model is when the two entities behave as if it is

just a function of the bank, which fully under-

stands the insurance products, and customises

the products to its customers just as it would do

to its own banking products.

The development of Bancassurance in India be-

gan for the following reasons:

● To improve the channels through which insur-

ance can reach the common man in a widen-

ing Middle Class of India

● To create a wider base for the marginally

penetrated banking sector, utilizing the base of

insurance companies

COVER ARTICLE

Figure 3: Country-wise market share of

Bancassurers in Life and Non-life segment

Country Bancassurers’

Life Share

Bancassurers’

Nonlife Share

Australia 43 Very small

Belgium 48 6

Brazil 55 13

Chile 13 19

France 64 9

Italy 59 2

Malaysia 45 10

Portugal 88 10

Spain 72 7

Source: World Bank

17

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

panies. Banks are made for daily transactions

where as insurance are made for long term in-

cidents. Also, as banks do take term deposits

which are similar products as insurance pre-

mium, banks sometimes feel integrating the

two would cause a substitution effect, i.e. cus-

tomers would reduce consuming one product

for the sake of other. Another issue is that the

insurance products themselves have become

complicated over the years. Banks would have

to thoroughly understand implications and

risks involved before selling them. A possible

“Conflict of Interest” is also a threat to bancas-

surance penetration in India as Banks have a

lot of detailed information about its customers

through “KYC” norms set in place, which the

insurance company might take advantage of.

Hence regulatory policies need to be set just

right.

FDI in Insurance

India opened the insurance sector to foreign

players in 2000 with FDI limit of 26% through

automatic route. The couple of years that fol-

lowed saw an influx of many foreign players

partnering with domestic players.

13 years on, although insurance has

seen good growth, a lot of it is largely

because of domestic players. However,

the potential for growth is still tremen-

dous. However, after the initial excite-

ment, foreign players have not really

been attracted to Indian Insurance sec-

tor. On the contrary, some of them

have started pulling out of India.

The Insurance Laws Amendment Bill

seeks to raise FDI cap in the insurance

sector from 26 percent to 49 percent,

but has been pending in the Rajya Sabha since

2008. There have been recent calls from

P.Chidambaram and Raghuman Rajan for clear

the pending Parliament approval of this bill. It

has been a long wait for the Bill to get passed

help them reduce the NPA ratio of banks

through diversifying channels like insurance.

For the Insurance Companies

For the insurer, the banks customer base is a

gold mine of sorts. It not only gives them the

large pool of customers to target but also gives

them their financial profiles, their buying be-

haviour, purchasing habits an insight into their

personality. They can then target which product

to sell to which customer, customise and tailor

make their insurance according to their needs

For the Customers

For a customer to the insurance industry, trust

plays a major role in making decisions. Custom-

ers for long have had to keep trusting the gov-

ernment controlled monopolised insurance

companies for long term commitment towards

their insurance needs. The incoming plethora of

private players both in insurance and banking

sector, which a common man doesn't know

much about, from this consolidation in the

form of bancassurance he can keep the faith he

has had for a long time and avail the other ser-

vice without a heavy heart.

Challenges for Bancassurance

One of the big challenges for Bancassurance is

merging of two seemingly different working

styles and cultures of banks and insurance com-

COVER ARTICLE

Figure 4: Bancassurance Model

18

© Monetrix, Finance & Economics Club of MDI, Gurgaon

ers contributed around Rs. 21000 crore. IRDA

estimates the sector will need further invest-

ment of around Rs. 50,000 crore over the next

5 years. Considering the capital crunch faced

by domestic companies, increased FDI will go

a long way in addressing this need. The new

funds will help increase the penetration. In-

creased FDI in the sector would help more

foreign players enter the market, making the

market more competitive. It will help challenge

the monopoly of the government owned Life

Insurance Corporation. It will make insurance

and the sooner it gets passed, the better it will

be everyone involved. FDI hike in the sector

will prove beneficial for all stakeholders: do-

mestic players, foreign players, government and

customers, and boost the overall sentiment

about Indian economy.

The most obvious benefit of FDI will be the

increased investment in insurance, which is

capital intensive. Over the last decade, insur-

ance sector has seen a capital investment of

over Rs. 32,000 crores, of which domestic play-

COVER ARTICLE

Top Insurance Cos. Foreign Partner Domestic Partner Year

Bajaj Allianz Life In-

surance

Allianz AG

(26%)

Bajaj Finserv Ltd

(74%) 2001

SBI Life BNP Paribas Assurance (26%) SBI

(74%) 2001

HDFC Standard Life Standard Life

(26%)

HDFC Bank

(72.4%) 2000

Birla Sun Life Sun Life Financial Inc (26%) Aditya Birla Group

(74%) 2000

Max New York Life New York Life International

(26%)

Max India

(74%) 2000

ICICI Lombard Fairfax Financial Holdings Ltd

(26%)

ICICI Bank Ltd

(74%)

2001

Bajaj Allianz General

Insurance

Allianz AG

(26%)

Bajaj Finserv Ltd

(74%)

2001

IFFCO-Tokio General

Insurance

Tokio Marine & Nichido Fire

Iznsurance Group

(26%)

IFFCO

(74%)

2000

Reliance Life Insur-

ance

Nippon Life Insurance

(26%)

Reliance Capital

(74%)

2011

Source: Insurance Sector Report, March 2013, IBEF

Figure 5: Major Private Insurance Players in India and their Foreign Partners

19

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

But, micro-insurance is not simply offering low

premium insurance products.

It involves different distribution channels than

urban insurance to reach out to rural areas

where the people generally are illiterate, un-

known to the concept and need of insurance.

These people are more prone to risks, say ill-

ness, calamities, etc. and hence offering insur-

ance at low premiums is a challenge. And

hence, micro-insurance market is governed by

supply, not demand. Keeping distribution and

customer acquisitions costs low is key.

IRDA specifies the rural obligations to be met

by each insurance provider. However, it needs

to develop more supportive regulations to in-

crease the micro-insurance market in India.

Tata-AIG is a prime example of successful im-

plementation of micro-insurance. In the Tata-

AIG model, 4 or 5 women belonging to self-

help groups become informal brokers for mi-

cro-insurance and earn some income by selling

insurance.

Looking Ahead

Undoubtedly, the potential as well as the need

for growth of insurance in India is tremendous.

But, to fulfill this promise, all the stakeholders

- the Government, the insurance companies,

both domestic and foreign, the regulators, and

the non-insurance providing partners - all of

them need to go ahead hand in hand. Increased

FDI limit, regulations to attract the foreign

players, successful implementation of various

bancassurance models, and increased penetra-

tion of micro-insurance by more companies

will go a long way in achieving the desired in-

surance penetration in India and pave the way

for further economic growth.

policies available at lower premiums leading to

more number of people opting for insurance.

The foreign players will bring in more innova-

tive insurance products available in the devel-

oped countries. Even if these products may or

may not be foremost requirement of the Indian

insurance sector, these will be lucrative in the

urban areas. New technological capabilities

brought by the foreign players will add im-

proved efficiency throughout the value chain.

Also, with the proposed increased limit, risk-

sharing business models can be developed with

foreign and domestic players.

Thus because of all these advantages, it is im-

perative that the proposal for hiking FDI in

insurance to 49% is approved and implemented

as soon as possible.

Micro-insurance

Another key way of achieving better insurance

penetration is micro-insurance, which is spe-

cially designed for insuring low-income people

by offering them affordable insurance products.

The premium is low but regular and propor-

tionate to the risks involved.

COVER ARTICLE

Micro-insurance operates through

three regulated distribution mecha-

nisms:

1) Partnership model

2) Agency model, and

3) Micro-agent model.

Partnership model is more found and

mostly the partners are NGOs, Micro-

finance institutes and banks.

20

© Monetrix, Finance & Economics Club of MDI, Gurgaon

scope for investment and relatively lesser do-

mestic savings. In such a case, a deficit in the

current account is, to some extent, preferable

to foster swifter economic growth in a less de-

veloped economy.

Causes of a Current Account Deficit

A desire to purchase imported goods espe-

cially in times of high economic growth will

lead to depletion in the current account bal-

ance. Higher consumer spending will result in a

higher spending on imports. For instance, dur-

ing the late 1980s, the UK economy was ex-

periencing a high growth phase and a simulta-

neously widening current account deficit. On

the other hand, a recession led to an improve-

ment in the current account.

An appreciation in the exchange rate would

make the domestic currency more expensive in

terms of the foreign currency. The impact of

this would be seen in a fall in demand for ex-

ports and a rise in demand for imports given

that imports and exports are price sensitive.

This situation would deteriorate the current

The Balance of Payments of an economy is an

accounting record of all transactions of a coun-

try with the rest of the world. It has two com-

ponents: current account and capital account.

The current account is further subdivided into

three components:

1. Balance of trade which is the difference

between the value of goods and services

exported from the country and the value

of goods and services imported into the

country.

2. Transfer payments

3. Net income such as interests and divi-

dends

Of these three parts, the second and third are a

small fraction of the total.

The current account balance is one of the two

indicators of a country’s foreign trade balance.

The largest component of current account be-

ing the trade balance, a surplus in the current

account implies that the country is earning

more foreign exchange from exporting goods

and services than it is spending on importing

goods and services. Therefore, this positive net

sales abroad leads to creation of foreign assets

in the domestic economy. A current account

deficit, on the other hand, depletes the coun-

try’s foreign resource base by extracting more

foreign exchange than it injects.

The current account deficit can also be meas-

ured in terms of the difference between invest-

ments in an economy and its national savings

(both public and private). This implies that the

savings are insufficient to finance all investment

opportunities which is generally true in case of

developing countries on account of their huge

BEGINNERS’ CORNER

Current Account Deficit

Figure 1: INR vs USD

21

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

is a positive sign indicating a growing econ-

omy. If savings are lower it could be pointing

towards conspicuous consumerism or impact

of fiscal policy or a temporary shock in the

economy. However, if investments are higher it

shows that the domestic markets are prosper-

ing and hence, are attractive to foreign inves-

tors.

India: A case study

India’s current account deficit or CAD is a hot

topic of discussion in any economic or finance

related circles and rightly so since it impacts

the economy by posing risks to macroeco-

nomic stability. India has been experiencing a

consistently high CAD which is unsustainable

and unhealthy for the progress of the econ-

omy. The Finance ministry along with the apex

bank, Reserve bank of India has taken several

measures to bring down the CAD.

India’s CAD which was around 1% of the

GDP in the early 2000s, grew sharply to nearly

5% of GDP in September 2012. This was

mainly seen as a consequence of imports of

gold and crude oil in large quantities on the

one hand, and moderating exports on the

other.

India’s growth story has been majorly driven

by oil of which over two thirds are imported. It

is also the largest component of India’s import

bill followed by gold. Since oil has a variety of

uses both as an industrial input as well as a do-

mestic commodity, the only way to reduce oil

imports is to discover indigenous methods of

oil exploration and extraction to fulfil the

needs of the country. This would also protect

India from the external oil supply shocks that

can have a huge impact on foreign exchange

reserves. The government is considering op-

tions for shale gas exploration but this will take

time and till then the oil import bill will con-

tinue to be a major contributor to the deficit in

the current account.

account whereas depreciation in the exchange

rate would improve the current account bal-

ance.

Relative competitiveness of industrial pro-

duction is an important determinant of the

demand for exports of the domestic country. If

a country lags behind in terms of technological

or other efficiencies, its products become less

attractive in the international market thereby

reducing the current account balance.

A current account deficit sometimes balances

itself out. A deficit implies greater demand for

foreign currency to purchase imports and lesser

supply due to relatively lesser exports. This

makes the foreign currency more expensive in

terms of the domestic currency, in other words,

the exchange rate falls. Thus, domestic consum-

ers will start purchasing less of imported goods

and more of domestically produced goods be-

cause of the presence of a cheaper currency, as

a consequence of which the current account

deficit will reduce.

Consequences of a Current Account Deficit

A deficit in the current account is not always

bad unless it constitutes a high percentage of

GDP. In that case also it becomes imperative to

analyse the factors responsible for the deficit to

judge whether it is good or bad.

If the deficit is a result of excess of imports

over exports, it may be an indicator of the do-

mestic economy being less competitive in the

international market or a case of high economic

growth leading to consumer spending being

biased towards imports. In such a scenario, the

economy must focus on improving demand for

domestic products both internally and exter-

nally by ensuring that production technology is

more efficient and comparable to international

standards.

If, on the other hand, the deficit is a conse-

quence of excess of investment over savings, it

BEGINNERS’ CORNER

22

© Monetrix, Finance & Economics Club of MDI, Gurgaon

fibres and simultaneously improve its competi-

tiveness in manufacturing goods. This should

be backed by the government policy of

strengthening ties with global partners and im-

proving infrastructure of existing Export Proc-

essing Zones.

Implications of a large deficit

The deficit implies an excess demand for for-

eign exchange which is financed by attracting

capital inflows in terms of foreign direct invest-

ments (FDI) or foreign institutional invest-

ments (FII). If capital inflows are insufficient,

limited foreign exchange reserves of the coun-

try are used which causes a depreciation in the

exchange rate of currency. In case of India, a

large part of the current account deficit has

been financed by external debt. Coupled with a

weak currency, it can pose a huge threat to

India’s external liquidity position and credit

rating. As no major change is expected in the

current global growth or commodity price

trends in the near term, India must introduce

policy changes like further liberalization of the

economy towards foreign investments, curbing

import demand and increasing export competi-

tiveness to rein in its burgeoning current ac-

count deficit.

High demand for gold comes as a result of In-

dians’ strong affinity for the “yellow metal” as a

safe investment in a volatile market. After the

recession in the U.S. in 2008 and the EU in

2009-10, the world markets have lost investor

confidence and the only asset providing large

returns is gold. Hence, it becomes difficult to

curb gold imports. In March 2013, the Finance

Minister made an appeal to people to reduce

gold imports. The government has been taking

measures to reduce imports by increasing gold

import duty by 2% to 6% in January 2013 and

by another 2% to 8% in June 2013. In May

2013, RBI restricted the import of gold on a

consignment basis by banks.

Other imports include capital goods, transport

equipment, machinery etc which are significant

investments for building the infrastructure in

India. Domestic production to a certain extent

has reduced dependence on imports, but in ar-

eas like telecom and mining, imports still play a

crucial role. Thus it is evident that an effort to

reduce imports alone is not a sustainable solu-

tion to correct the deficit situation. Instead

there should be more focus towards increasing

demand for exports in the world markets. India

must leverage areas where it has a stronghold

like IT, pharmaceuticals, garments and natural

BEGINNERS’ CORNER

Figure 1: India’s Current Account Deficit as percentage of GDP

23

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

numerous meetings and interviews with Busi-

ness Unit heads, project owners and other

team-members associated with these projects

in order to gather first-hand information. I also

had meetings with Business Finance Mangers

(BFMs) of various BUs to gather financial data

of these projects. I was in regular contact with

Mr. Rishad Premji, Chief Strategy Officer at

Wipro, who took a key interest in my project

and its analysis.

Were there any events organized just for

interns? Were there any ice-breaking or

networking activities?

We had an exhaustive induction program, in

which many business leaders addressed us and

introduced us to the culture at Wipro. There

was a one-day training program on data analy-

sis and effective presentation techniques. There

were also two fun-filled experiential learning

sessions, in which we got to know and interact

with many fellow interns from different B-

schools. The last day witnessed a grand closing

ceremony and felicitation for the best interns.

How was the overall experience? Would

you like to work in the organization (same

profile) as a full-time employee?

I had a good two-month stint at Wipro and

had a great learning experience. I got to meet,

interview and work with many top leaders in

the industry. My work was also well appreci-

ated by my team members and the HR person-

nel. Hence, if given an opportunity, I would

gladly work with the same team in Wipro.

Title of Project:

Strategic Investment Effectiveness and Road-

map for the Future

Brief Description about the Project:

The Central Strategy Office (CSO) at Wipro

critically analyzes and subsequently funds (if

found suitable) for a period of two years, vari-

ous new initiatives and seed projects which dif-

ferent BUs across Wipro have identified as po-

tential new projects and offerings. Once the

funding ceases after two years, the initiative is

‘rolled-back’ to the respective Business Unit

(BU) and the BU takes the project forward. I

had to analyze (strategically and financially) 51

past ‘rolled-back’ projects, identify the current

state of these projects, have they grown or have

they ceased to exist, and finally provide recom-

mendations for improving the success ratio of

these CSO approved-and-funded projects and

the investment program as a whole.

How was the Internship structured?

It was a 9-week internship. The first few days

were sent in Induction activities. This was fol-

lowed by a detailed project scoping, commence-

ment of the project, a mid-term progress review

after Week 5, the final presentation during

Week 9 and a closing and felicitation ceremony

on the last day. There were regular weekly re-

views with my mentor during the entire course.

What were the roles and responsibilities you

had to take up as part of your project?

As I had to study 51 projects, I had to conduct

ISSUE SPECIAL

Summer Internship Experiences

Company: Wipro Limited

Team: Strategy and M&A

Location: Bangalore India Karan Jaidka

24

© Monetrix, Finance & Economics Club of MDI, Gurgaon

standing of the various facets of credit risk. Do

the literature survey of the existing models

which have been developed for credit risk

measurement. The based on the secondary re-

search and the best practices followed in indus-

try, develop a model for credit risk measure-

ment of different types of counterparty banks.

Were there any events organized just for

interns? Were there any ice-breaking or

networking activities?

The culture in Axis Bank is really one in which

amicable and everyone is very approachable.

So there was really no need for any such activ-

ity.

How was the overall experience? Would

you like to work in the organization (same

profile) as a full-time employee?

The overall experience was very enriching and

eye – opening. The organization helps you in

building up a holistic understanding of the

banking and is very friendly and amicable at

the same time.

I would love to go back and work in the same

profile which was offered to me as a full time

employee.

Title of Project:

Developing a Credit Risk Model for counter-

party banks

Brief Description about the Project:

Measuring the credit risk a counterpart plays an

important ole in a bank. For a counterparty

bank with a lower risk, the interest rates

charged would be low and a higher credit expo-

sure can be undertaken as a percentage of

bank’s capital and vice versa is true for a bank

with a higher counterparty risk. Here at Axis,

my internship project was to develop the credit

risk rating model for different types of banks.

How was the Internship structured?

We had induction on the first day which was

followed with our meeting with our project

guides and buddies. We had leadership talks

within the entire span of our internship in

which leaders from the different verticals of the

bank would share their rich experiences and

learning’s with us.

We also had branch visit to give us exposure to

the daily work life in a branch and understand

the various facets of it.

What were the roles and responsibilities you

had to take up as part of your project?

My job was to understand the banking industry

as a whole and alongside develop a deep under-

ISSUE SPECIAL

Summer Internship Experiences

Company: Axis Bank Ltd.

Team: GFID, Treasury

Location: Mumbai, India

Saurabh Saxena

25

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

During the internship, I had the chance to

work on the sector report which was later

released by Goldman Sachs.

Apart from this, I worked on the financial

models of the companies in the sector, up-

dating and modifying them according to re-

quirement.

Were there any events organized just for

interns? Were there any ice-breaking or

networking activities?

The guest lecture series in which several emi-

nent personalities from Goldman Sachs of-

fices worldwide came to deliver lecture and

share their experiences and career growth

opportunities was designed specifically for

intern class.

How was the overall experience? Would

you like to work in the organization

(same profile) as a full-time employee?

Overall, it was a great learning experience

which helped me to develop both financial

expertise and soft-skills.

I look forward to returning to the company

as a full-time employee.

Title of Project:

Stock Pitch and Coverage of Earnings Season

Brief Description about the Project:

It involved studying and analyzing the sector

allocated during the internship period. Based

on that, a stock was selected to ascertain pos-

sibility of investment and accordingly BUY/

SELL recommendation was given for the

stock.

Apart from this, I followed the release of

quarterly results by companies in the sector

and accordingly updated the earnings esti-

mates in the Goldman Sachs model for the

company.

How was the Internship structured?

It was an eight-week internship where the

first week involved induction into the GS

culture and imparting financial and excel

skills to be needed during the internship pe-

riod.

After this, interns were allotted different

teams spread over several geographies and

sectors for rest of the internship.

What were the roles and responsibilities

you had to take up as part of your pro-

ject?

ISSUE SPECIAL

Summer Internship Experiences

Company: Goldman Sachs

Team: Global Investment Research

Location: Bangalore, India Rishabh Gupta

26

© Monetrix, Finance & Economics Club of MDI, Gurgaon

fronts and seeks opportunities for their reduc-

tion or elimination wherever feasible.

Were there any events organized just for

interns? Were there any ice-breaking or

networking activities?

Yes, the internship started with a 3 day orienta-

tion program wherein I got to meet various

business leaders and understand the values and

processes being followed at HSBC.

It also included many ice breaking activities

and team games which gave all the interns

from schools across the country an opportu-

nity to know each other. Also, at the end of the

internship, we had a closing ceremony and a

big party.

How was the overall experience? Would

you like to work in the organization (same

profile) as a full-time employee?

Working with HSBC was a very enriching ex-

perience. I understood the corporate culture

and how a multinational bank operates. I got to

learn a lot from the experiences of senior peo-

ple in the company. Also, I got an opportunity

to meet and network with fellow interns.

Yes, I would love to join HSBC as a full time

employee in the same profile I interned for.

Title of Project:

Identification of potential initiatives for Strate-

gic Cost Management

Brief Description about the Project:

The objective of the project was to understand

various costs and expenses incurred by the

company, specifically in managing the Informa-

tion Technology (IT) infrastructure, forecast

the cost for the next three business quarters and

identify the potential initiatives that can be

taken to manage and reduce cost incurred on

the same.

How was the Internship structured?

The internship was for a period of 9 months,

which began with various orientation activities

followed by team introduction, detailing of the

project, midterm review after 4 weeks and a

final presentation in the last week.

There was a regular interaction with the project

mentor who helped a lot in understanding and

completing the project.

What were the roles and responsibilities you

had to take up as part of your project?

The most important part for me was that I was

independently working on this project, under

the aegis of my mentor. This gave me a better

sense of responsibility and accountability to-

wards the deliverables. I was responsible for

understanding and analyzing various opera-

tional costs incurred by the company on various

ISSUE SPECIAL

Summer Internship Experiences

Company: HSBC Bank

Team: Retail Banking and Wealth Management

Location: Mumbai, India Ashish Gupta

JUNE—AUGUST ’13 | BLUE CHIP ISSUE 4

phenomenon called as ‘Capital Flight’ caused

major Asian crisis in 1990s following which

many countries imposed capital controls.

Why China is aiming towards CAC?

The recent global slowdown has led to de-

cline in China’s GDP growth rate to 7 % in

year 2013 from 9.2 % recorded in FY

2011.This is due to significant fall in exports by

3 % as compared to previous year. This has

made clear that China’s economy can no longer

sustain on export oriented growth model.

China’s economists had known this for long

and therefore came up with 12th Five Year Plan

which talked about new development models.

The 12th Five Year Plan which, came into ef-

fect in 2011, strengthens the commitment to

promote the “going global” policy. For a dec-

ade China has advanced mainly because of ex-

ports and high investment in production ca-

pacities. This has led to imbalance in demand

and supply. Now, resort to outward foreign

direct investment is needed to absorb excessive

production capacities. According to official

figures, China’s outward direct investment

(ODI) exceeded $77 billion in 2012, an in-

crease of 12.6% on the previous year, even as

inflows of FDI fell for the first time since the

height of the global financial crisis. This indi-

cates that many Chinese investors are looking

for opportunities outside their home country .

A recent report from the think tank Global

Financial Integrity (GFI) identifies China as the

largest source of illicit financial flows in the

developing world. $ 3.1 trillion of reserves

were illegally moved out of China into real es-

What is Full Capital Account Convertibility?

CAC was first coined as a theory by the Reserve

Bank of India in 1997 by the Tarapore Com-

mittee, in an effort to find fiscal and economic

policies that would enable Third World coun-

tries transition to globalized market econo-

mies However, it had been practiced, although

without formal thought or organization of pol-

icy or restriction, since the very early 90's..

Capital Account Convertibility means freedom

of currency conversion in relation to capital

transactions in terms of inflows and outflows.

In layman’s term CAC would mean easing of

norms in transactions which leads to creation of

an asset or liability in any foreign country or

freedom in converting local financial asset into

foreign financial asset and vice versa.

Till 20th century there were no restrictions on

movement of capital across transnational

boundaries. But later on many countries started

imposing capital controls to retain their domes-

tic reserves. Following the end of Second

World War; US, Switzerland and Canada were

the only countries to have open regimes. In

1980s and early 1990s when these economies

started booming, this trend of open regime was

adopted by several developed economies. Free

capital flows enabled financiers to invest in

other nations as well. It helped them diversify

their portfolio and share risk.

Many Asian economies imitated the trend and

opened their borders to free capital flows .But

absence of adequate safeguards and proper

structure led to diminished local reserves. This

CAPITAL ACCOUNT CONVERTIBILITY OF CHINA BY 2015

Capital Account Convertibility of

China by 2015 PGDM 2012-14

Fore School of Management Prachi Aggarwal

28

© Monetrix, Finance & Economics Club of MDI, Gurgaon

ily tradable across different nations and will

reduce dollar hegemony that China has been

aiming for years. At a time when factory costs

are rising and manufacturing growth has

slowed China believes that more capital inflows

will help in domestic financing and spur the

growth. It will help China to come out of

shackles of economic downturn

that all emerging nations are facing

in current fiscal.

Also, it will enable financiers to

invest in different nations and di-

versify their portfolio. This will

lead to risk sharing and will expand

capital markets of China.

Risks that China may face due

to Full CAC

Dutch Disease

Dutch Disease is a term that was

coined after Netherland crisis

erupted in year 1959.The discovery

of large reserves of natural gas field

shifted the focus from manufactur-

ing sector to mining sector. This

caused downfall of Netherland’s

manufacturing sector and led to

economic crisis. China is seen as

the most favorable destination of trade by

WTO. Several top notch companies have es-