24

INVESTOR INVESTOR INVESTOR INVESTOR BRIEFING BRIEFING BRIEFING BRIEFING December 2013

| Date post: | 17-Feb-2017 |

| Category: |

Investor Relations |

| Upload: | company-spotlight |

| View: | 4,333 times |

| Download: | 0 times |

INVESTORINVESTORINVESTORINVESTORBRIEFINGBRIEFINGBRIEFINGBRIEFING

December 2013

Safe Harbor StatementSafe Harbor Statement

This presentation includes forward‐looking statements within the meaning of the Safe Harbor provisions of the Securities Litigation Reform Act of 1995. Such statements include, but are not limited to, statements relating to the expected future performance of the company and its objectives, expectations and intentions for the future. These forward‐looking statements are based on the current beliefs and expectations of Bemis Company’s management and are subject to risks and uncertainties. The forward‐looking statements speak only as of the date of this presentation, and Bemis Company does not undertake to update such statements to reflect changes that occur after that date. There are a number of factors that could cause actual results to differ from those set forth in the forward‐looking statements. These factors include, but are not limited to: general economic conditions, competitive conditions in our markets, regional governmental regulations, the cost and availability of raw materials, and our ability to pass these price changes on to our customers or otherwise manage commodity price fluctuation risks. These and other risks, uncertainties, and assumptions are identified from time to time in our filings with the Securities and Exchange Commission including our most recent Annual Report on form 10‐K and our quarterly reports on Form 10‐Q. Such reports are available on the website of the Securities and Exchange Commission (www.sec.gov).

Page 2

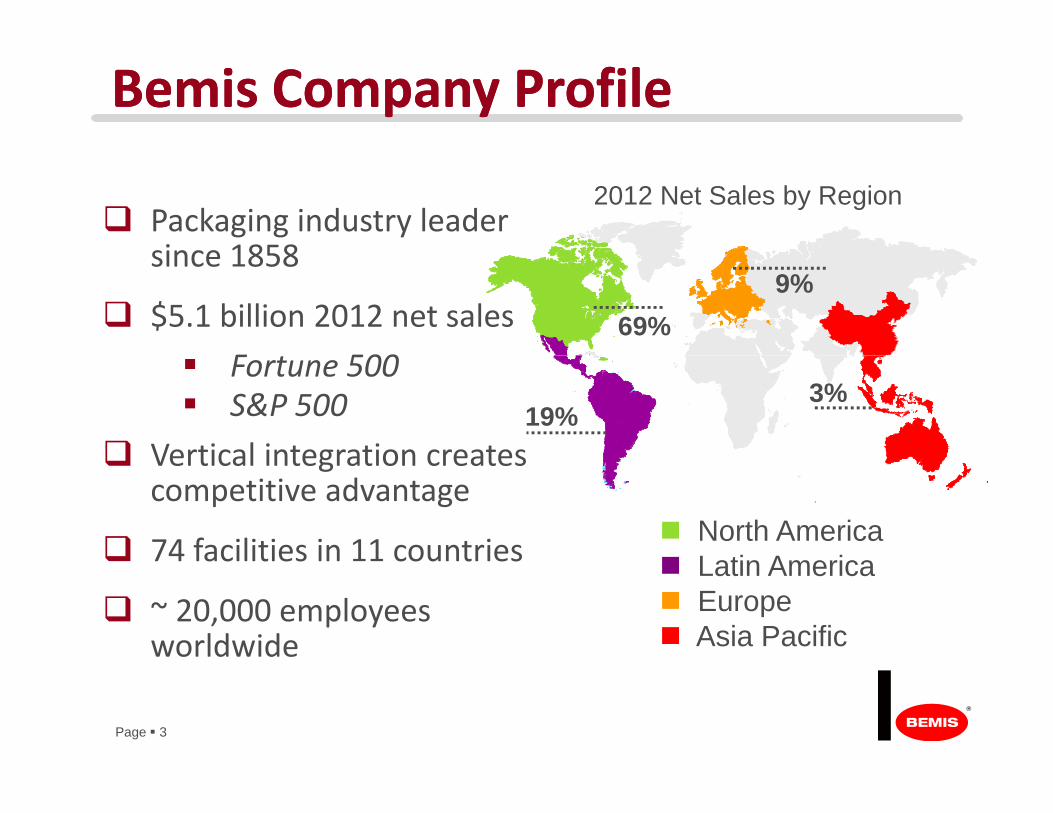

Bemis Company ProfileBemis Company Profile

2012 Net Sales by Region Packaging industry leader

since 1858

69%9%

since 1858

$5.1 billion 2012 net sales

F 50019%

3% Fortune 500 S&P 500

Vertical integration creates

North America Latin America

Vertical integration creates competitive advantage

74 facilities in 11 countries Latin America Europe Asia Pacific

74 facilities in 11 countries

~ 20,000 employees worldwide

Page 3

2012 Highlights2012 Highlights

Record adjusted EPS of $2.15

Increased dividend payable to shareholders Increased dividend payable to shareholders

Announced new reportable segment structure: U S PackagingU.S. Packaging Global Packaging Pressure Sensitive Materials

Substantially completed facility consolidation program to close 9 manufacturing locations

Increased footprint in Asia‐Pacific

Page 4

Net Sales & Adjusted Op ProfitNet Sales & Adjusted Op Profit** % by Segment% by Segment($ i illi )($ in millions)

U.S. Packaging

Pressure SensitiveMaterials

Global Packaging

$3 04043%

$556

16%

8%

$1 544

100%

$3,04057%

$55612%

64%

$1,544

15.0% $3,000

12.8%11.0%

13.0%

10 0%

15.0% $3,000 15.0%

$3,000

North America Latin AmericaEurope Asia Pacific

$1,451 $1,637 $1,543

8.8%7.4% 7.0%

5.0%

10.0%

$1,000

$2,000

$2,822 $3,111 $3,040

5.0%

10.0%

$1,000

$2,000

5.9% 6.3% 6.6%

5.0%

10.0%

$1,000

$2,0008.8%

Page 5

$ ,

0.0% $‐2010 2011 2012

0.0% $‐2010 2011 2012

$563 $574 $556 0.0% $‐

2010 2011 2012

* See appendix for reconciliation from GAAP to Adjusted Operating Profit excluding certain items.Page 5

U.S. Packaging ProfileU.S. Packaging ProfilePercent of 2012 Net Sales

20%

30%Percent of 2012 Net Sales

0%

10%

Meat & Dairy & Specialty Dry Foods Beverage Candy, Health & OtherCheese Liquids Food &

MealsWraps Snacks &

BakeryHygiene Non‐food

Extends shelf life of perishable foods (meat, cheese dairy produce)cheese, dairy, produce)

Proprietary and patented film structures

Premium manufacturing Premium manufacturing scale and printing capabilities support both national and regional brands

Page 6

U.S. U.S. Packaging Growth DriversPackaging Growth Drivers Conversion from jars and

cans to pouches

Single serving / Single serving / convenience sizes

Material content and

Glass jar Pouch

weight reduction for sustainability and cost management

Convenient cook‐in packages

Eli i ti f PVdC

Paper envelope Stand up pouch w/window

Elimination of PVdCcontent from plastic cups

Page 7

Can Cook-in Pouch

Global Packaging ProfileGlobal Packaging Profile

20%

Percent of 2012 Net Sales

0%

10%

Medical & Dairy & Meat & Health & Specialty Beverage Candy, Other

Expanding consumer

ed ca &Pharma

a y &Liquids

eat &Cheese

ea t &Hygiene

Spec a tyFood

e e ageWraps

Ca dy,Snacks &Bakery

Ot eNon‐food

markets in Latin America and Asia

Sterility and quality areSterility and quality are paramount for medical applications

Page 8

Global Packaging Global Packaging Growth DriversGrowth Drivers Food safety regulations in

emerging marketsWal-Mart located in China

New generation of consumers looking for convenience features

Need for shelf stable foods due to lack of available refrigeration spacerefrigeration space

Retort

Page 9

Pressure Sensitive Materials ProfilePressure Sensitive Materials Profile

40%

60%

Percent of 2012 Net Sales

0%

20%

40%

Technical Graphic Label

Page 10

DisciplinedDisciplined CapitalCapital StewardshipStewardshipPriorities:

1) 30 consecutive years $400

$500Cash Flow from Operations ($ in millions)

of increasing dividend payments

2) Fund organic growth $100

$200

$300

$400

2) Fund organic growth to enhance revenues and returns

) d$1.20

Cash Di idends

$0

$100

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

3) Fund acquisitions

4) Balance share repurchases and $0 40

$0.60

$0.80

$1.00Cash Dividends

repurchases and deleveraging

$0.00

$0.20

$0.40

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Page 11

Share Repurchase HistoryShare Repurchase History

$154 $161

$50 $18 $27

$46

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Deleveraging

M&A Transactio

n

M&A Transactio

n

M&A Transactio

n

($203)

M M M

Page 12

World Class Customer BaseWorld Class Customer Base

Why customers choose Bemis:

U i h l i l d i i Unique technological and engineering resources

Reduced waste in production and pdistribution system

Flexible capacity to accommodate new product launchesnew product launches

Reliable supply; Quality product

Investment grade supplier Investment grade supplier

Global supply capabilities

Page 13

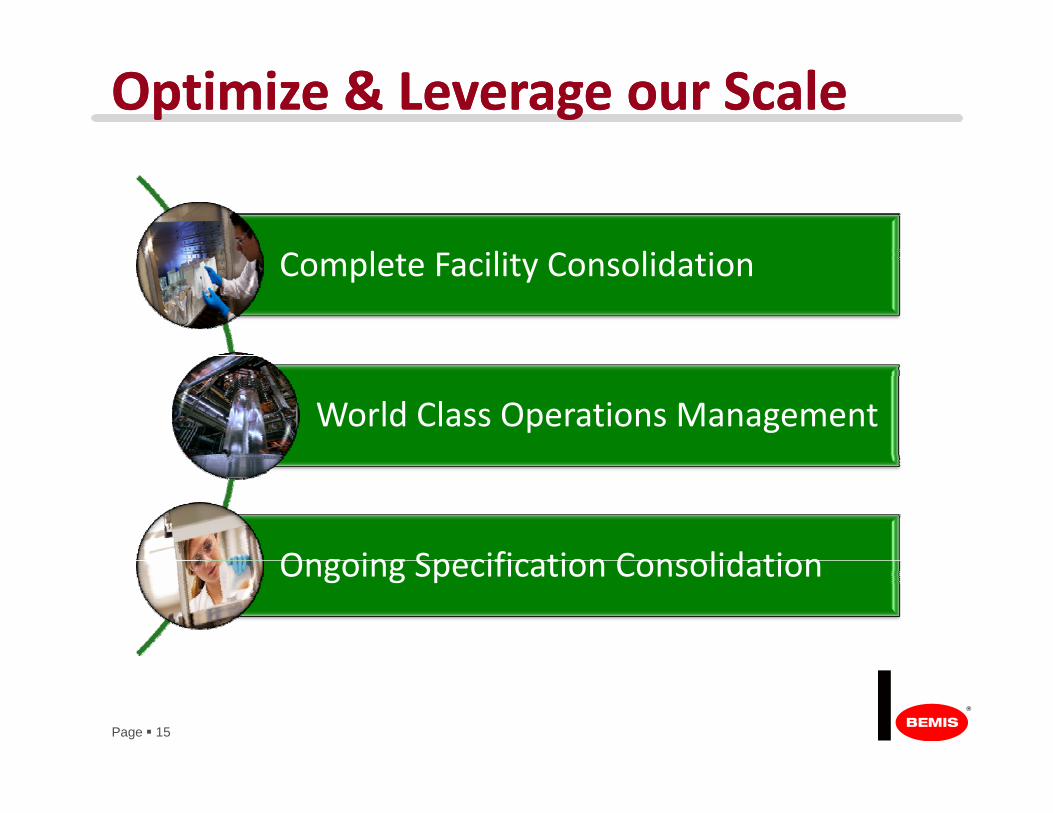

Strategic PrioritiesStrategic Priorities

Optimize & Leverage p gOur Scale

Grow in Target Areas

Accelerate InnovationAccelerate Innovation

Page 14

Optimize & Leverage our ScaleOptimize & Leverage our Scale

C l F ili C lid iComplete Facility Consolidation

World Class Operations Management

Ongoing Specification ConsolidationOngoing Specification Consolidation

Page 15

Grow in Target AreasGrow in Target Areas

Packaging demand from Medical and pharmaceutical High barrier packaging

developing countries

• Emerging economies demanding/regulating

pharmaceutical industries

• Demographics continue to drive

opportunities

• New products continue to win business in g g g

food safety and convenience features

• Lack of refrigeration creates need for shelf

growth• Modern bio‐technology requires more complex packaging

established U.S. food applications

• Expanding opportunities for high

stable packaging• Increasing consumer populations

p g g• Opportunities for smart packaging to solve emerging market needs

pp gbarrier film in Latin America and Asia

Page 16

Accelerate InnovationAccelerate Innovation

Unique Polymer

Polyethylene

Polyester

NylonPolymer Technologies

Nylon

Polypropylene

Barrier resins

Consumer Convenience Features

EZ Peel/Reseal

IntegraCut / IntegraScore

Microwaveable/self venting

Weight reduction

Reduced transportationFood

Proprietary sealantsSustainability Reduced packaging material

Less food and material waste

Lower carbon footprint

Food Safety

Antimicrobial coatingsRetort technologies

Page 17

Our Sustainability CommitmentOur Sustainability Commitment

E i t i bilitEconomic sustainability

Transparency and good governance are

Environmental Sustainabilitygood governance are fundamental tools for delivering long‐term value to shareholders

2020 Targets: Social Sustainability

We are a responsible b f th

Reduce electricity and fuel use by 10%

Reduce use of solvents member of the communities in which we operate and make safety our number one

Reduce use of solvents by 20%

Zero waste to landfills Zero process water discharged sa ety ou u be o e

priority in each of our global operations

discharged

Page 18

2013 2013 GuidanceGuidance

Adjusted EPS guidance of $2.24 to $2.30

Cash flow from operations ~ $400 million

• Reflects ~$40 million of pension contributions• Includes ~$50 million of cash payments for facility consolidation activities

• Cash flow from operations expected to be $500 million beginning in 2014

Capital expenditures of ~$130 to 140 million

Page 19

Note: Guidance as of October 25, 2013

An Attractive InvestmentAn Attractive Investment

Strong balance sheet and cash

flow

Disciplined capital allocation

World‐class customer base allocation

Strong market position

Expanding global market reach

Patented and proprietary

Page 20

p p yproducts

APPENDIXAPPENDIX

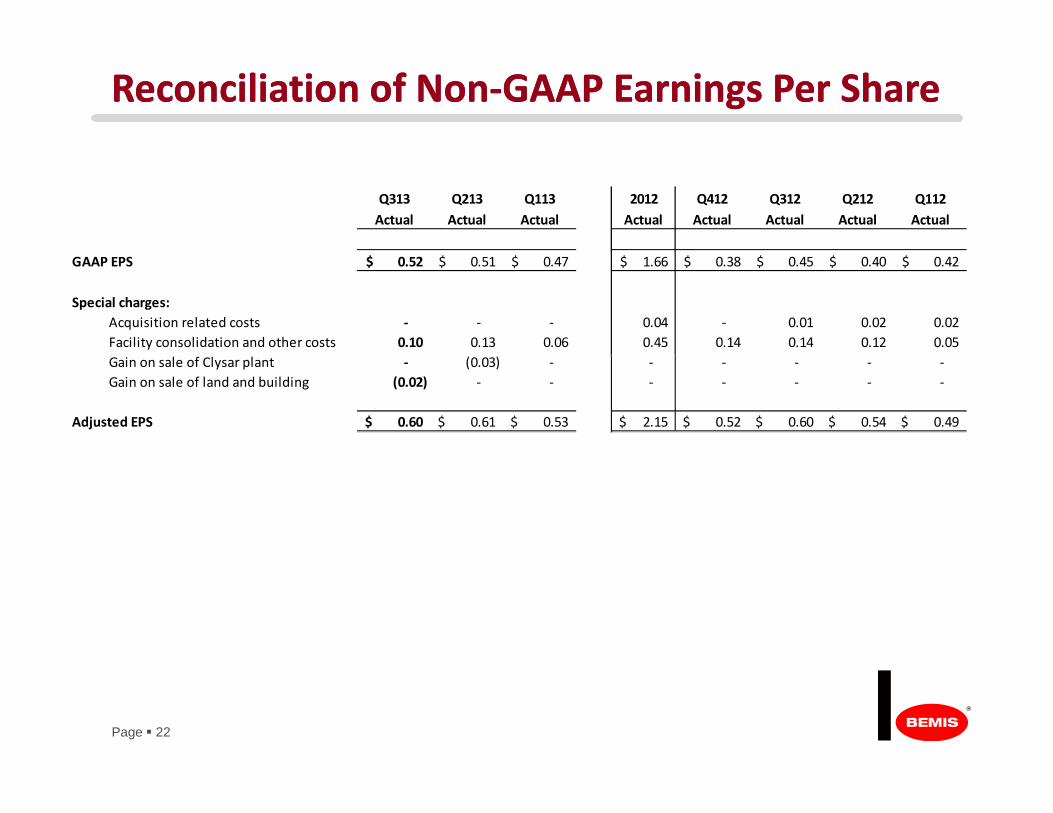

Reconciliation of NonReconciliation of Non‐‐GAAP Earnings Per ShareGAAP Earnings Per Share

Q313 Q213 Q113 2012 Q412 Q312 Q212 Q112Actual Actual Actual Actual Actual Actual Actual Actual

GAAP EPS 0.52$ 0.51$ 0.47$ 1.66$ 0.38$ 0.45$ 0.40$ 0.42$

Special charges:Acquisition related costs ‐ ‐ ‐ 0.04 ‐ 0.01 0.02 0.02 Facility consolidation and other costs 0.10 0.13 0.06 0.45 0.14 0.14 0.12 0.05 Gain on sale of Clysar plant ‐ (0.03) ‐ ‐ ‐ ‐ ‐ ‐ Gain on sale of land and building (0.02) ‐ ‐ ‐ ‐ ‐ ‐ ‐

Adjusted EPS 0.60$ 0.61$ 0.53$ 2.15$ 0.52$ 0.60$ 0.54$ 0.49$

Page 22

Facility Consolidation Program Financial SummaryFacility Consolidation Program Financial Summary

Cash Net CostCash Net CostExpense Paid Savings*

Q411 38.4$ 3.3$ 2011 38.4 3.3

Q112 8.3 8.0 Q212 19.7 4.5 Q312 21.4 11.2 5.0 Q412 19 3 11 5 3 0Q412 19.3 11.5 3.0 2012 68.7 35.2 8.0

Q113 9.3 10.8 7.5 Q213 20 9 11 7 12 5Q213 20.9 11.7 12.5 Q313 15.8 10.2 6.0 Q413 Estimate ‐ 24.2 6.0 2013 Estimate 46.0 56.9 32.0

Total Facility Consolidation Impact 153.1$ 95.4$

Expected Annual Savings Run‐Rate 50.0$

Page 23

*Savings net of increased costs associated with consolidation activities.

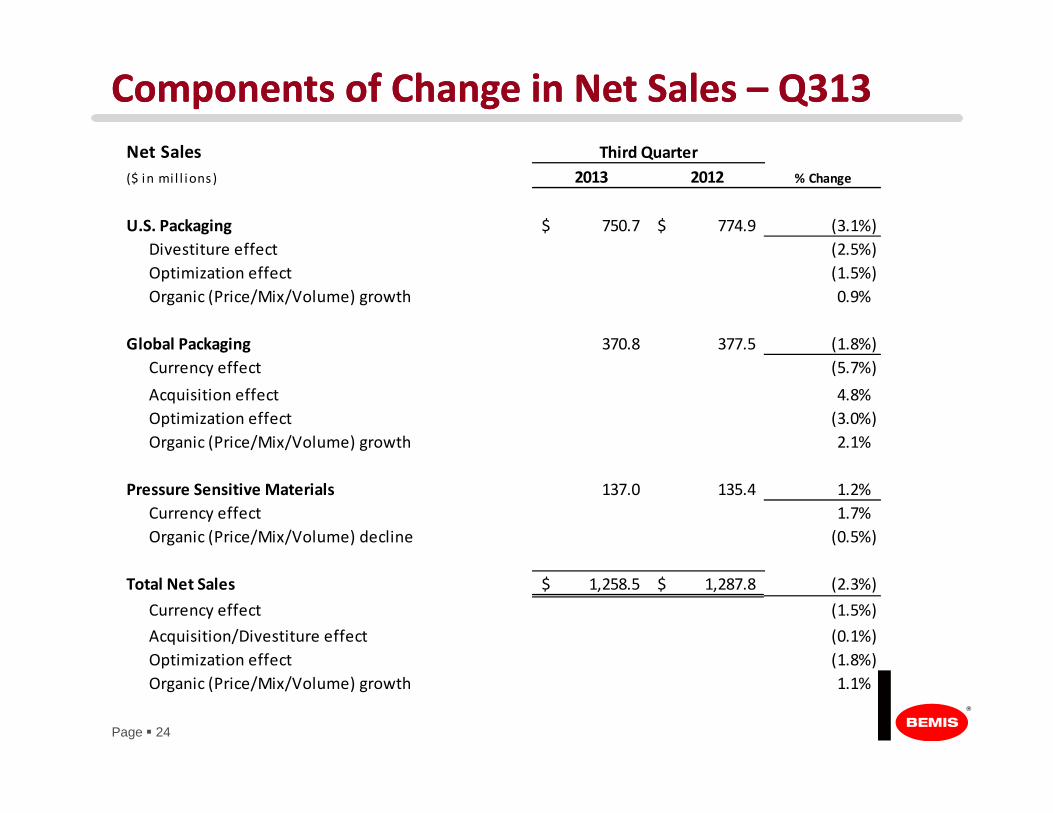

Components of Change in Net Sales Components of Change in Net Sales –– Q313Q313Net Sales Third QuarterNet Sales($ in mil l ions ) 2013 2012 % Change

U.S. Packaging 750.7$ 774.9$ (3.1%)Divestiture effect (2.5%)

Third Quarter

Divestiture effect (2.5%)Optimization effect (1.5%)Organic (Price/Mix/Volume) growth 0.9%

Global Packaging 370.8 377.5 (1.8%)Currency effect (5.7%)

Acquisition effect 4.8%Optimization effect (3.0%)Organic (Price/Mix/Volume) growth 2.1%

Pressure Sensitive Materials 137.0 135.4 1.2%Currency effect 1.7%Organic (Price/Mix/Volume) decline (0.5%)

Total Net Sales 1,258.5$ 1,287.8$ (2.3%)

Currency effect (1.5%)

Acquisition/Divestiture effect (0.1%)Optimization effect (1 8%)

Page 24

Optimization effect (1.8%)Organic (Price/Mix/Volume) growth 1.1%