12

BNP Seminar on Italian Banking Sector & NPLs Resolution of NPL credits Amb. Pasquale Terracciano London, 8 September 2016 Italian Embassy – London

BNP Seminar on

Italian Banking Sector & NPLs

Resolution of NPL credits Amb. Pasquale Terracciano London, 8 September 2016

Italian Embassy – London

Macroeconomic Scenario: growth to be consolidated

2

Macroeconomic Drivers in Italy European GVD vs Italian GDP

Source: Pwc

Macroeconomic Scenario: the good picture (1)

3 Source: MEF

Primary Surplus of the Five Largest European Countries: 1995-2016

Macroeconomic Scenario: the good picture (2)

4 Source: MEF

Public debt as % of GDP: 2008-2014

Economic Cycles & NPLs

5

• Loan performance is tightly linked to the economic cycle

• A mildly worse than usual phase of the economic cycle due to the recession post-2008

• We are now about to enter the growth phase of the

economic cycle

The Overall Plan

6

Structural Reforms

Constitutional & Institutional Reforms

Interventions in the banks

Reforming the judicial system

7

Patto Marciano

Non-possessory lien

Provides for the extra-judicial allocation of the properties given as guarantee of a loan

Allows companies to keep and use the guaranteed asset to generate revenues and repay the loan

Use of electronic tools

Put in place to safeguard parties from dilatory tactics and reduce the time of proceedings

NPL Register Enables both parties, entrepreneurs and banks, to consult quickly and easily information on one another

Source: ABI, MEF

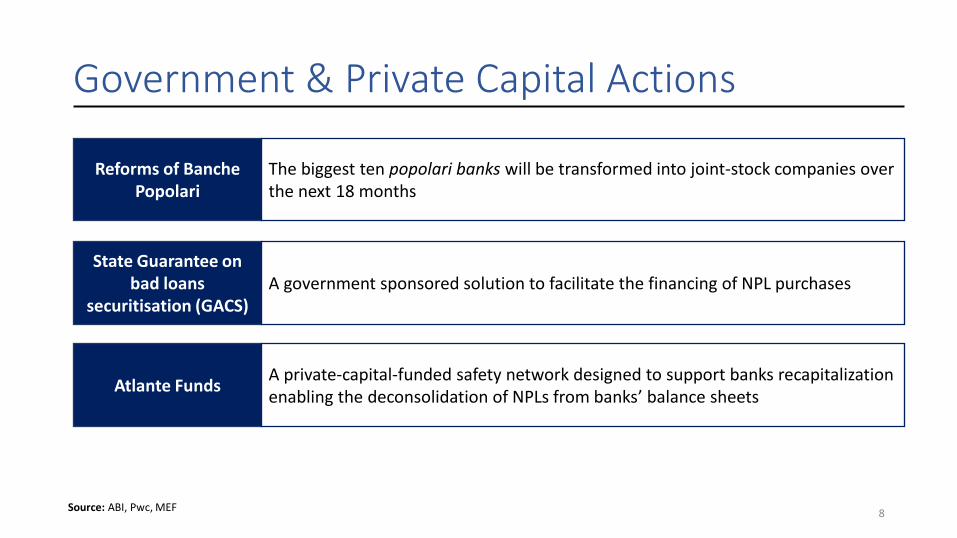

Government & Private Capital Actions

8 Source: ABI, Pwc, MEF

State Guarantee on bad loans

securitisation (GACS)

Atlante Funds

A government sponsored solution to facilitate the financing of NPL purchases

A private-capital-funded safety network designed to support banks recapitalization enabling the deconsolidation of NPLs from banks’ balance sheets

Reforms of Banche Popolari

The biggest ten popolari banks will be transformed into joint-stock companies over the next 18 months

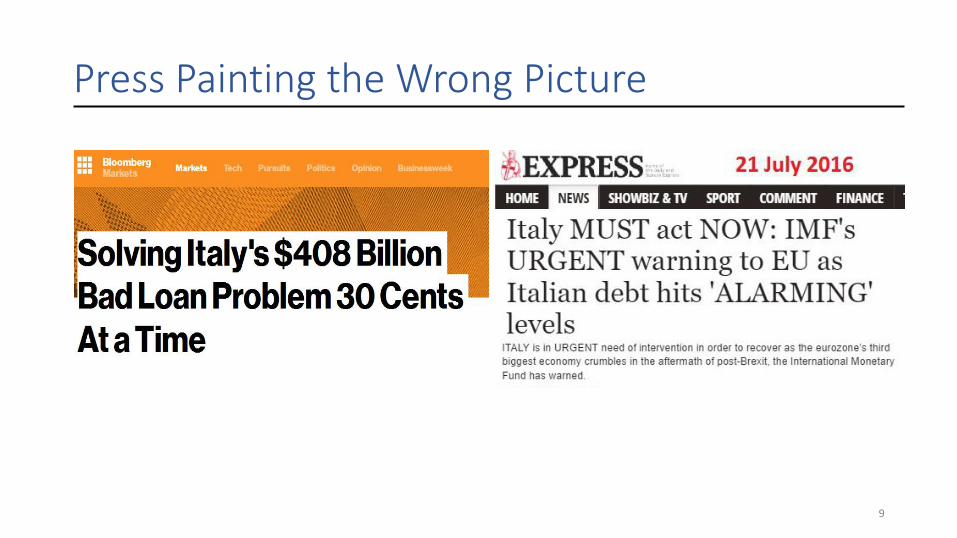

Press Painting the Wrong Picture

9

The real numbers

10 Source: MEF

Non Performing and Bad Loans – Gross and Net Values Net Loans and Relevant Collaterals

Moving Forward

11

• NPLs resolution + recapitalizations + changes in business model will be a turning point for the Italian banking sector

• Remodeling of banks’ business model

• Tackling technology disruption and changing consumer preferences

Far-more-ism vs a collective effort

12

• “Far-more-ism” syndrome: nothing but a misleading attitude

• Better check the unprecedented consistency and commonality of intent by government, industry and regulator as THE effective way for long-term solutions