24

Equalization grants International Experience Indonesia’s Options Bert Hofman, World Bank with thanks to Jun Ma, Ehtisham Ahmad

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | clepsa-victor |

| View: | 1 times |

| Download: | 0 times |

Equalization grants

International ExperienceIndonesia’s Options

Bert Hofman, World Bank

with thanks to Jun Ma, Ehtisham Ahmad

Equalization grants

Importance of grantsRationale for grantsTypes of grantsEqualization grantsExamples of equalization grantsIssues for Indonesia

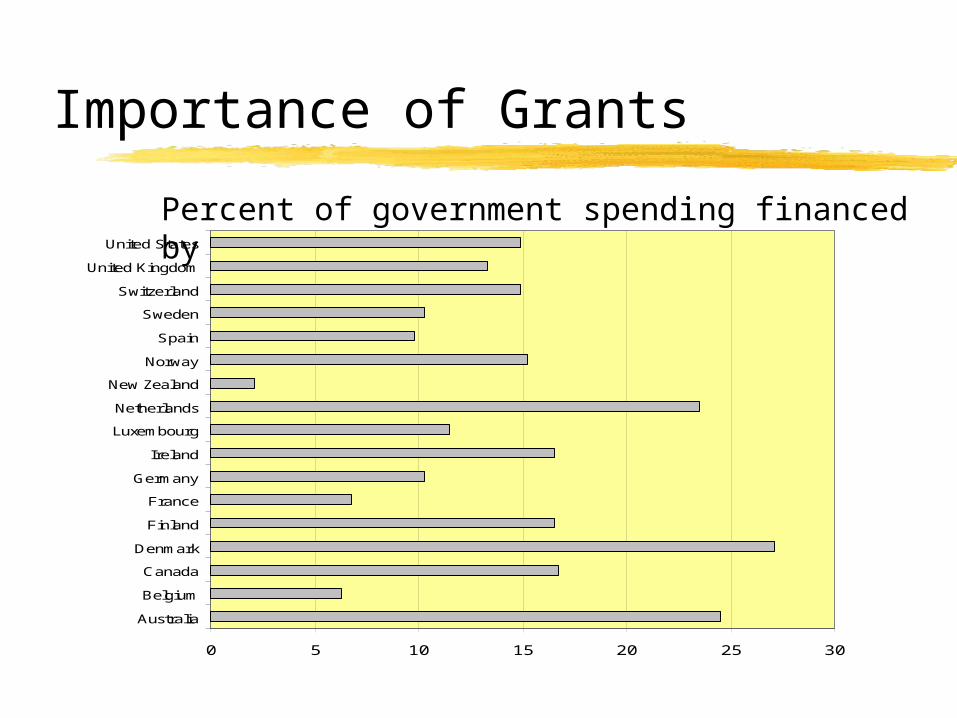

Importance of Grants

Percent of government spending financed by grants

0 5 10 15 20 25 30

Australia

Belgium

Canada

Denmark

Finland

France

Germany

Ireland

Luxembourg

Netherlands

New Zealand

Norway

Spain

Sweden

Switzerland

United Kingdom

United States

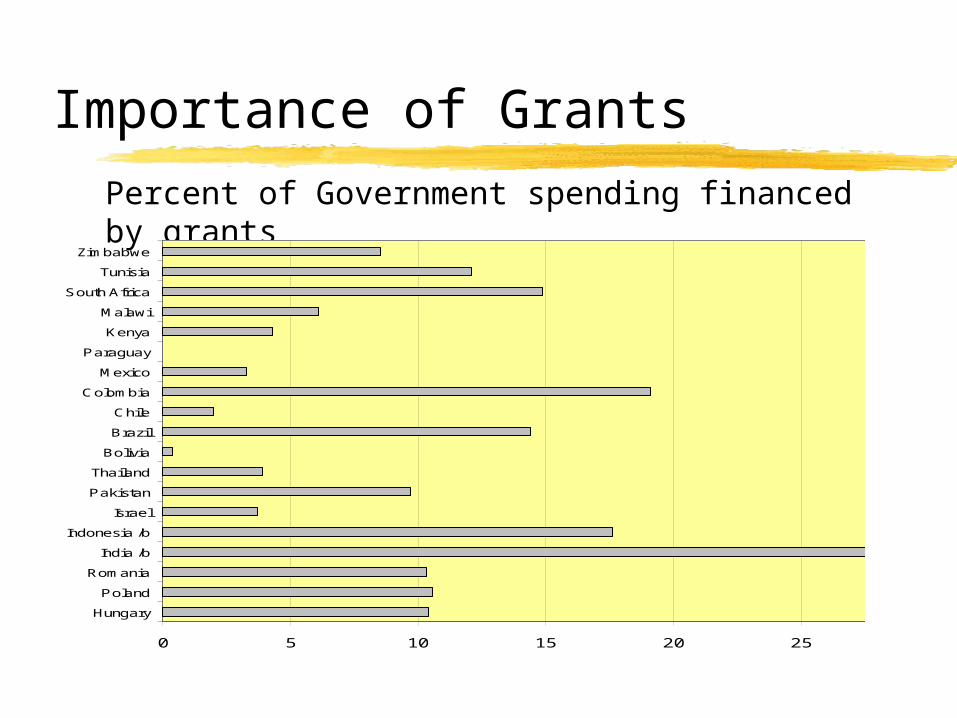

Importance of GrantsPercent of Government spending financed by grants

0 5 10 15 20 25 30

Hungary

Poland

Romania

India /b

Indonesia /b

Israel

Pakistan

Thailand

Bolivia

Brazil

Chile

Colombia

Mexico

Paraguay

Kenya

Malawi

South Africa

Tunisia

Zimbabwe

Importance of Grants

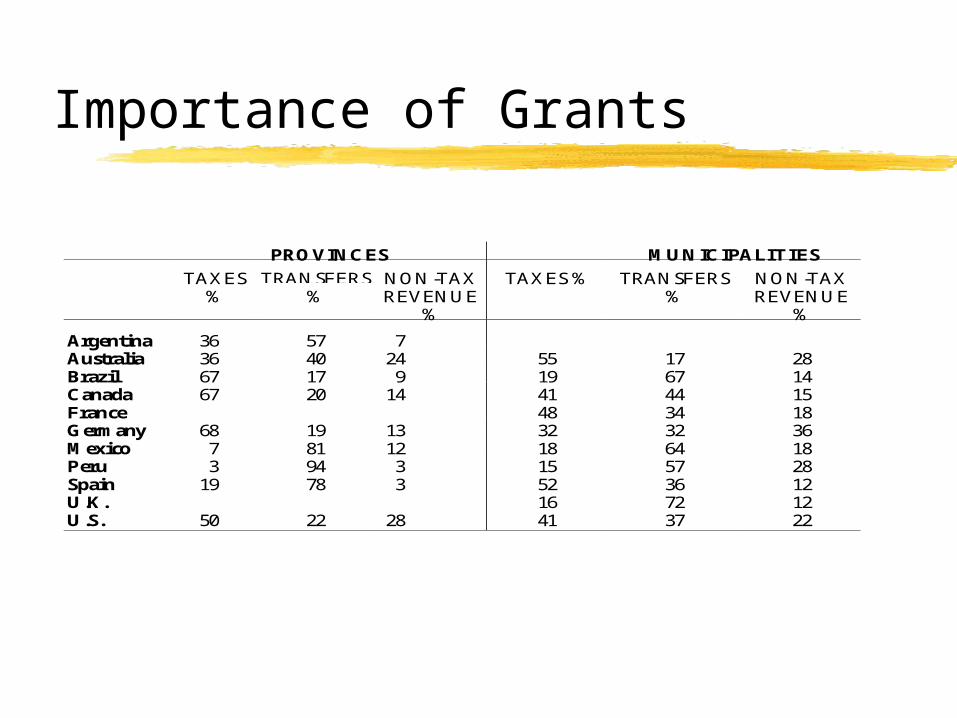

PROVINCES MUNICIPALITIES

TAXES%

TRANSFERS%

NON-TAXREVENUE

%

TAXES % TRANSFERS%

NON-TAXREVENUE

%

Argentina 36 57 7Australia 36 40 24 55 17 28Brazil 67 17 9 19 67 14Canada 67 20 14 41 44 15France 48 34 18Germany 68 19 13 32 32 36Mexico 7 81 12 18 64 18Peru 3 94 3 15 57 28Spain 19 78 3 52 36 12U.K. 16 72 12U.S. 50 22 28 41 37 22

Rational for grants

Vertical imbalanceHorizontal imbalanceSpill-oversNational prioritiesNation building

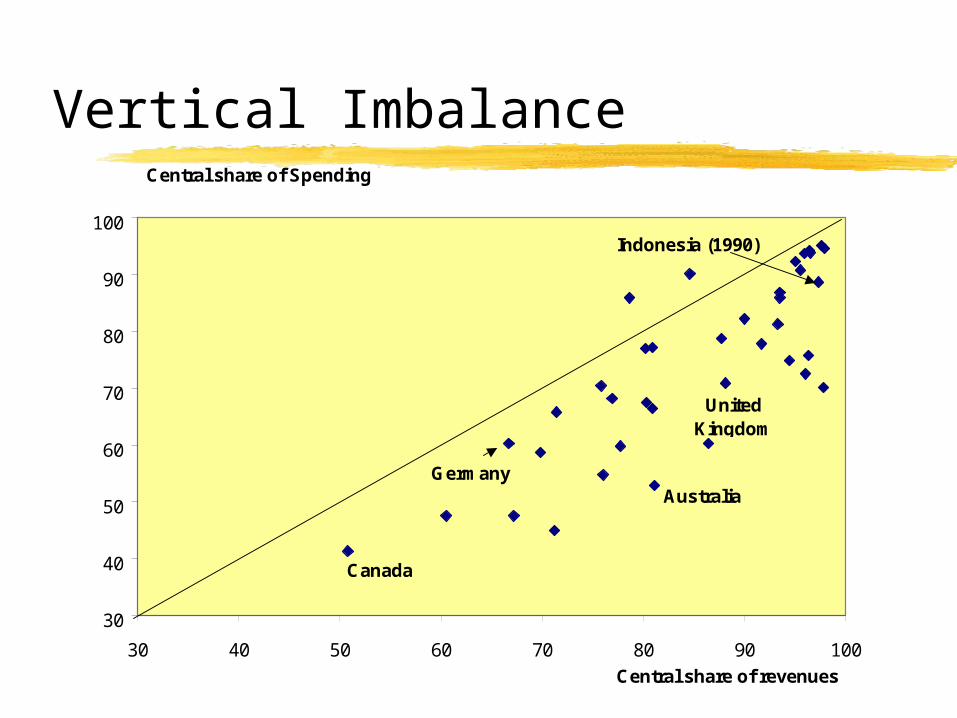

Vertical Imbalance

30

40

50

60

70

80

90

100

30 40 50 60 70 80 90 100

Australia

United Kingdom

Canada

Germany

Indonesia (1990)

Central share of Spending

Central share of revenues

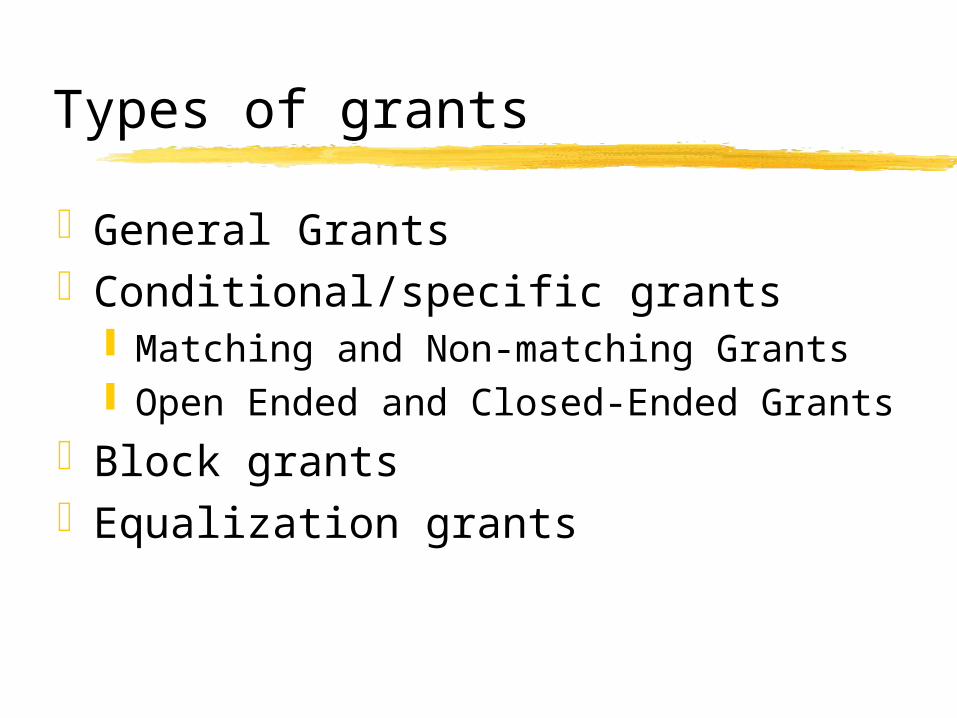

Types of grants

General GrantsConditional/specific grants

Matching and Non-matching Grants Open Ended and Closed-Ended Grants

Block grantsEqualization grants

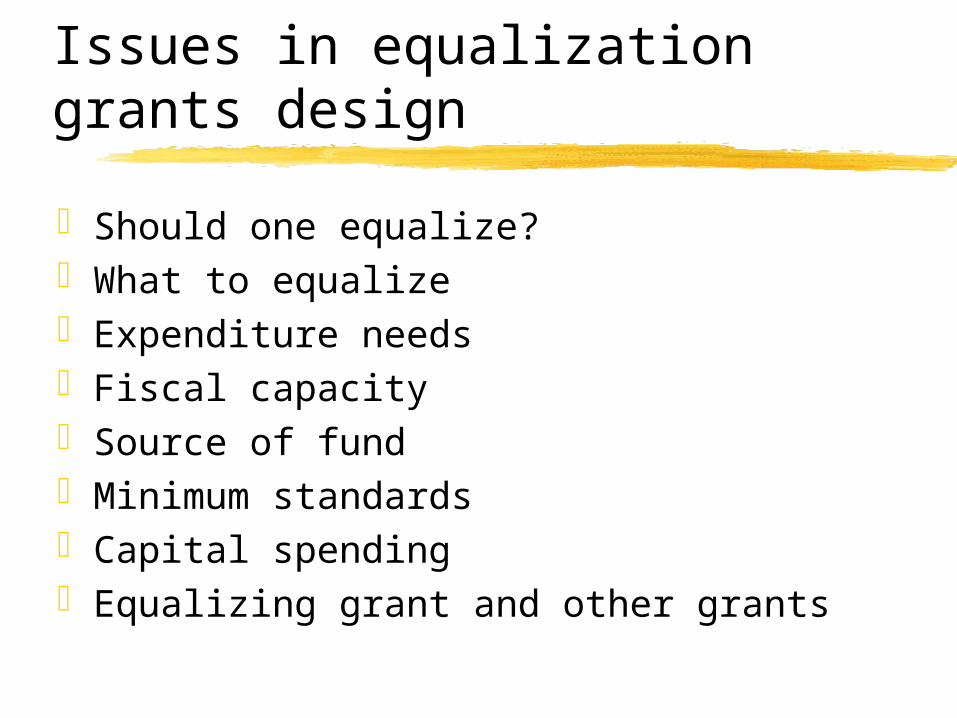

Issues in equalization grants design

Should one equalize?What to equalizeExpenditure needsFiscal capacitySource of fundMinimum standardsCapital spendingEqualizing grant and other grants

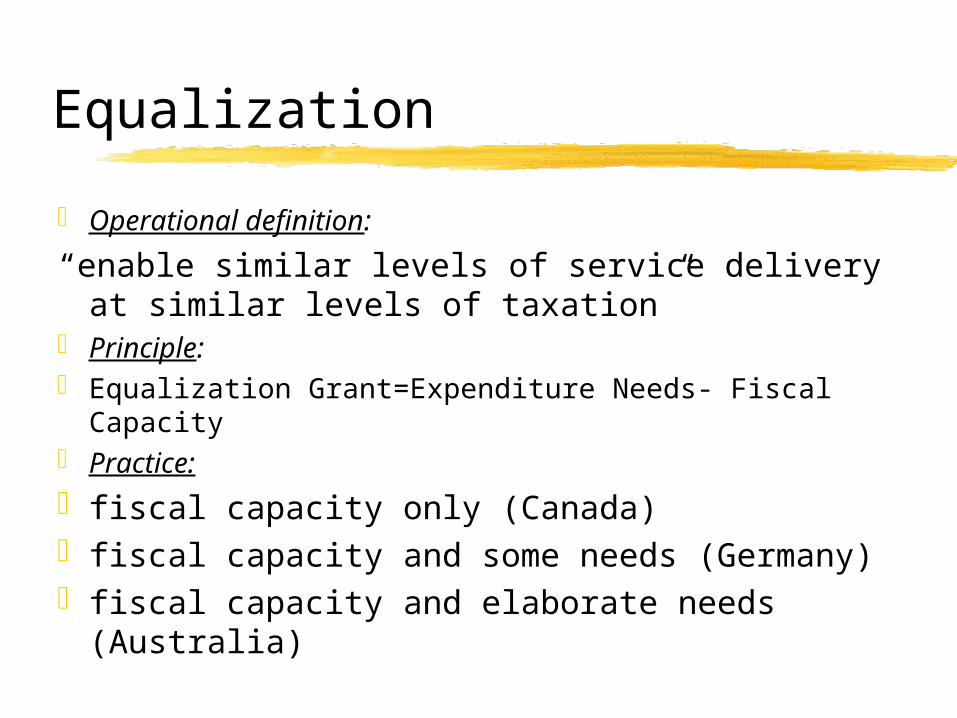

Equalization

Operational definition:

“enable similar levels of service delivery at similar levels of taxation”

Principle: Equalization Grant=Expenditure Needs- Fiscal

Capacity Practice:

fiscal capacity only (Canada)fiscal capacity and some needs (Germany)fiscal capacity and elaborate needs (Australia)

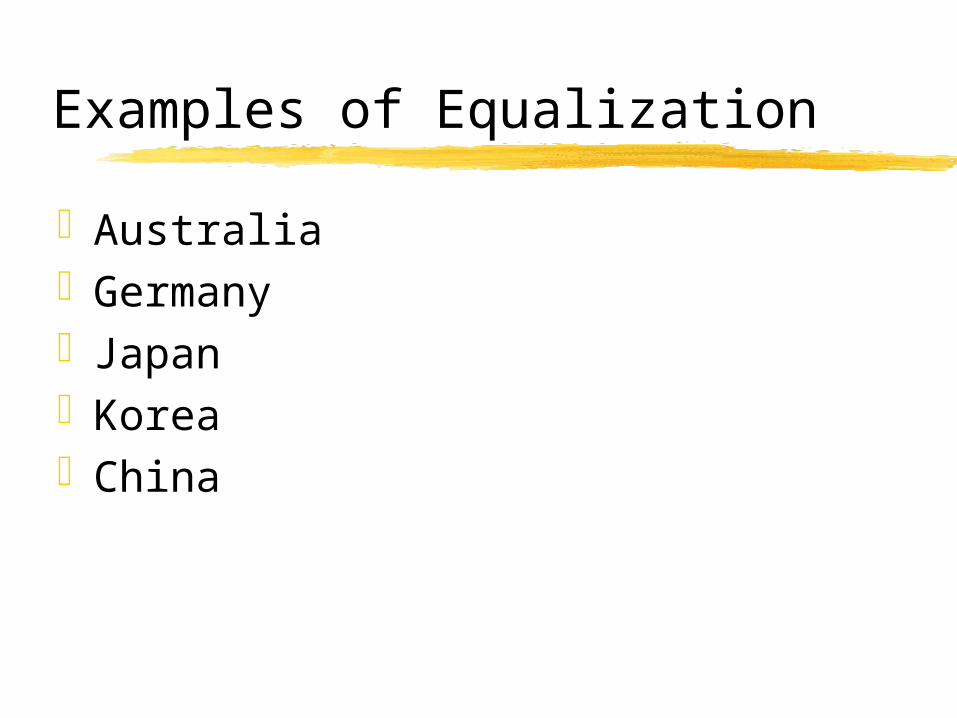

Examples of Equalization

AustraliaGermanyJapanKoreaChina

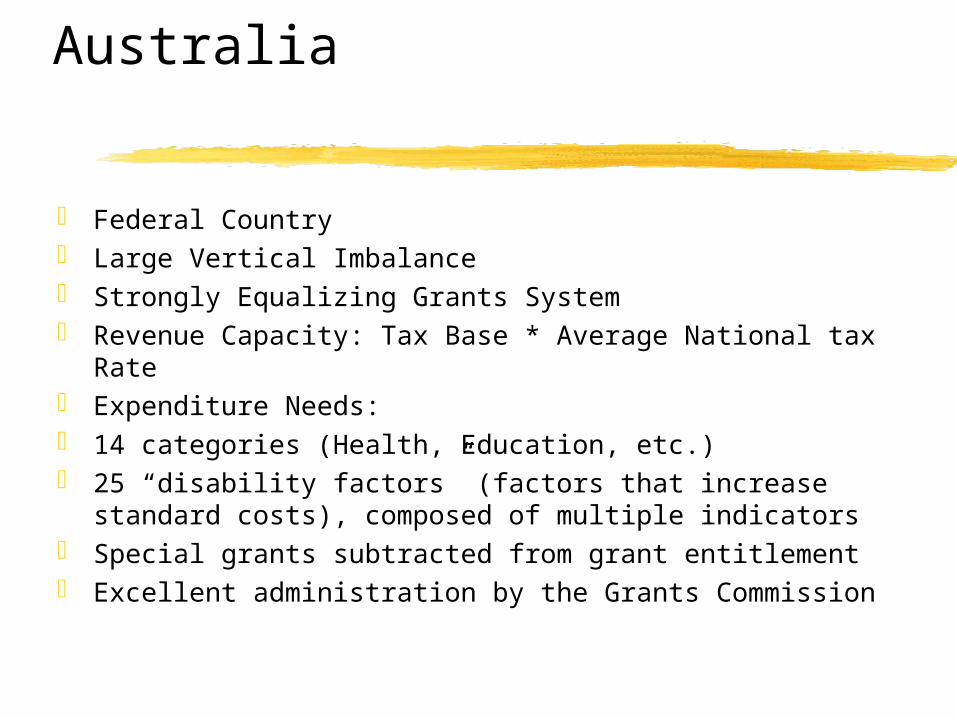

Australia

Federal Country Large Vertical Imbalance Strongly Equalizing Grants System Revenue Capacity: Tax Base * Average National tax Rate Expenditure Needs: 14 categories (Health, Education, etc.) 25 “disability factors” (factors that increase standard

costs), composed of multiple indicators Special grants subtracted from grant entitlement Excellent administration by the Grants Commission

Germany

Federal country Substantial tax sharing VAT redistributed per capita--provides most of the equalization Fiscal Equalization through Finanzausgleich (Financial Settlement) Principle: equalize needs-adjusted fiscal capacity Needs: “special burdens” for city states Every state obtains at least 95 percent of average revenues “Rich states” are taxed--discourages tax effort

Tax capacity over 110 percent of average tax with 80 percent Eastern, poor states receive additional grants from central

government

Japan

Unitary countryLarge vertical imbalanceEqualization through “Local Allocation

Tax”--both provinces and municipalitiesConsiders fiscal capacity and needsNeeds based on functions assigned to

government

Japan Cont.

Basic need = modification coefficient * unit cost

modification coefficients examples:school typessize of regionpopulation density in regioncold areaurbanization of regionMOF Administers

Korea

Unitary country Similar to Japan’s system Fiscal capacity and needs “Fiscal scarcity= standard need - standard

revenue” Needs = standard fiscal need + supplemental

need 29 standard factors Separate education transfer Ministry of Home Affairs Administers

China

See Mr. Zhang’s speech

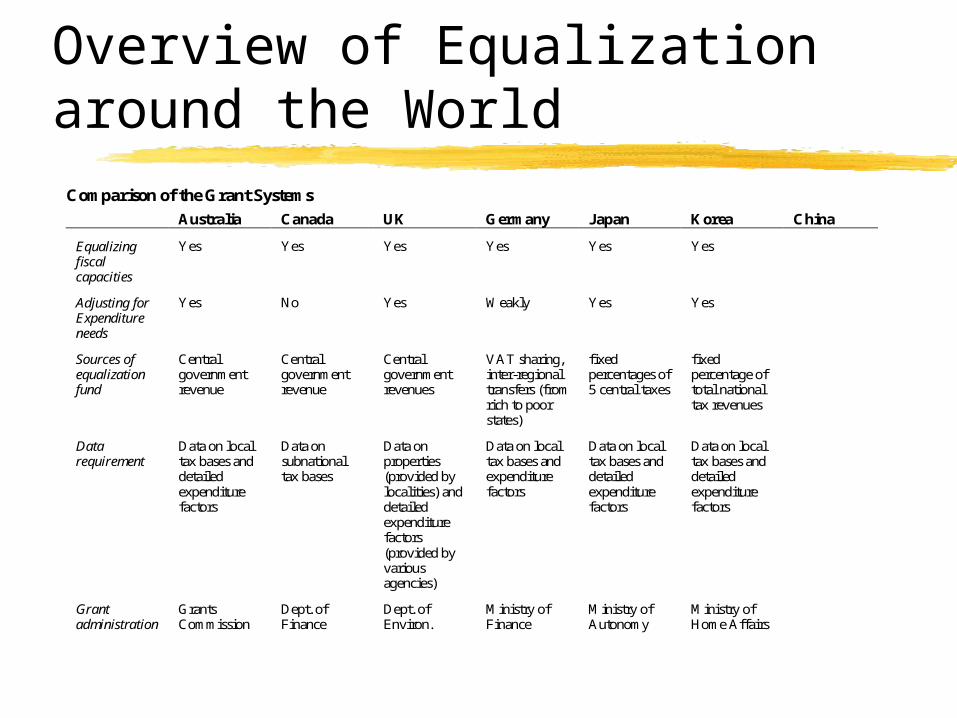

Overview of Equalization around the World

Comparison of the Grant Systems

Australia Canada UK Germany Japan Korea China

Equalizingfiscalcapacities

Yes Yes Yes Yes Yes Yes

Adjusting forExpenditureneeds

Yes No Yes Weakly Yes Yes

Sources ofequalizationfund

Centralgovernmentrevenue

Centralgovernmentrevenue

Centralgovernmentrevenues

VAT sharing,inter-regionaltransfers (fromrich to poorstates)

fixedpercentages of5 central taxes

fixedpercentage oftotal nationaltax revenues

Datarequirement

Data on localtax bases anddetailedexpenditurefactors

Data onsubnationaltax bases

Data onproperties(provided bylocalities) anddetailedexpenditurefactors(provided byvariousagencies)

Data on localtax bases andexpenditurefactors

Data on localtax bases anddetailedexpenditurefactors

Data on localtax bases anddetailedexpenditurefactors

Grantadministration

GrantsCommission

Dept. ofFinance

Dept. ofEnviron.

Ministry ofFinance

Ministry ofAutonomy

Ministry ofHome Affairs

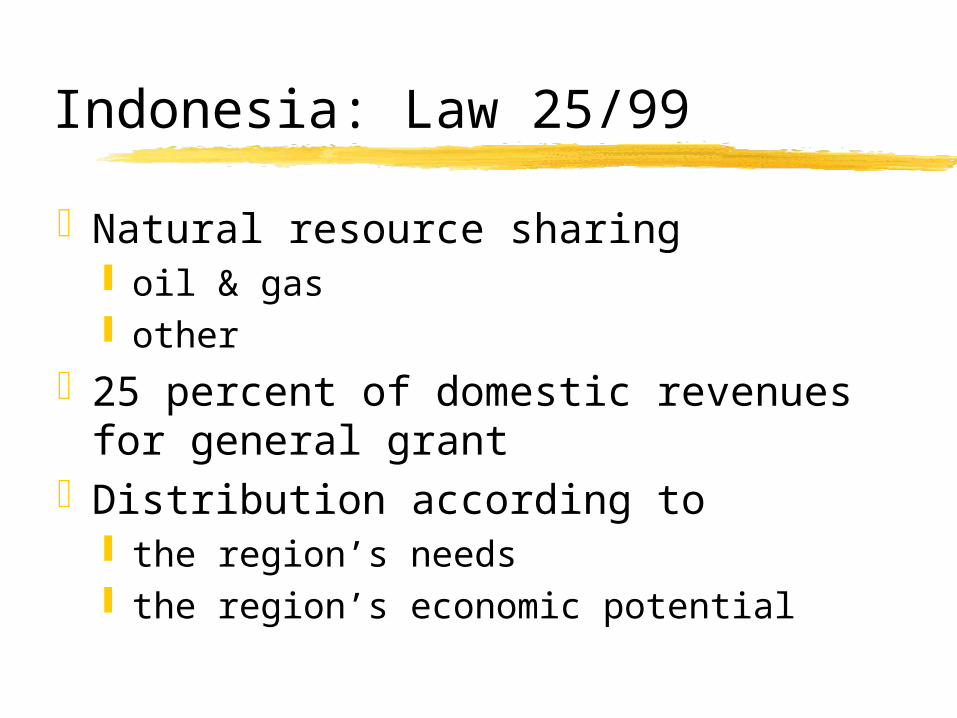

Indonesia: Law 25/99

Natural resource sharing oil & gas other

25 percent of domestic revenues for general grant

Distribution according to the region’s needs the region’s economic potential

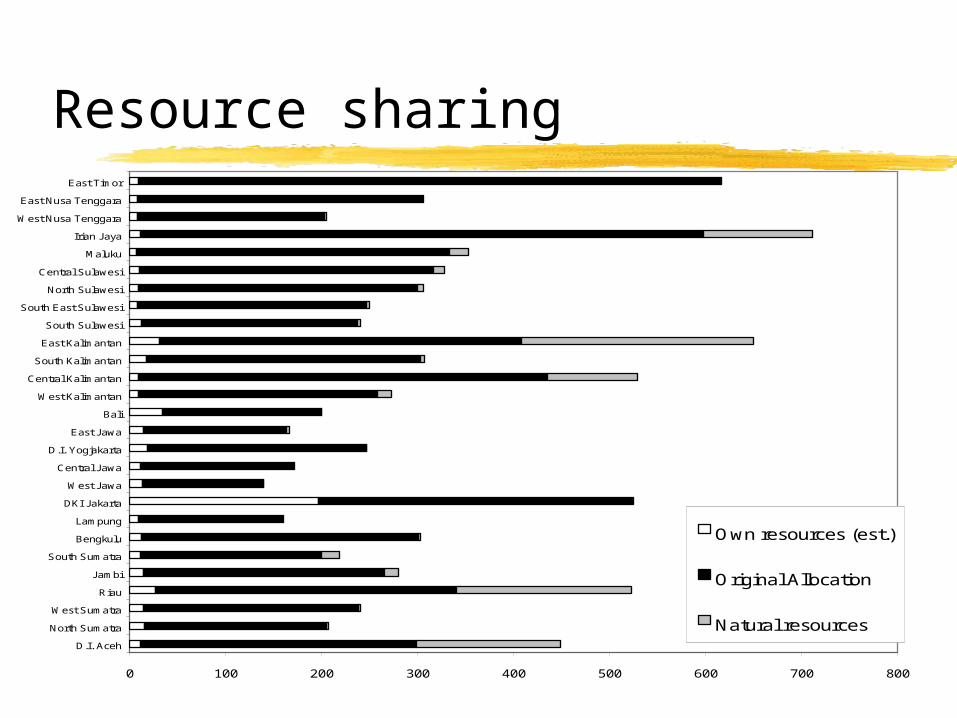

Resource sharing

0 100 200 300 400 500 600 700 800

D.I. Aceh

North Sumatra

West Sumatra

Riau

Jambi

South Sumatra

Bengkulu

Lampung

DKI Jakarta

West Jawa

Central Jawa

D.I. Yogjakarta

East Jawa

Bali

West Kalimantan

Central Kalimantan

South Kalimantan

East Kalimantan

South Sulawesi

South East Sulawesi

North Sulawesi

Central Sulawesi

Maluku

Irian Jaya

West Nusa Tenggara

East Nusa Tenggara

East Timor

Own resources (est.)

Original Allocation

Natural resources

Resource Sharing

0

100

200

300

400

500

600

700

800

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000

Transfers (000 Rupiah per capita)

Non-Oil GDP Per Capita 9Rp.'000

Before Natural Resource Sharing

After Natural Resource Sharing

De-equalizing

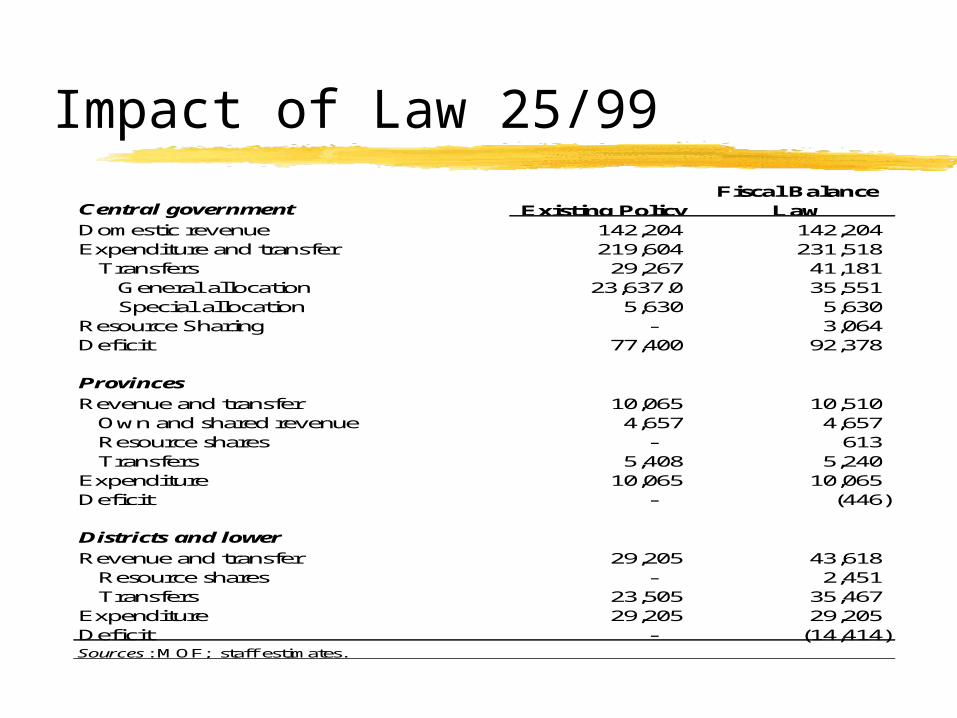

Impact of Law 25/99

Central government

Domestic revenue 142,204 142,204 Expenditure and transfer 219,604 231,518 Transfers 29,267 41,181 General allocation 23,637.0 35,551 Special allocation 5,630 5,630 Resource Sharing - 3,064 Deficit 77,400 92,378

Provinces

Revenue and transfer 10,065 10,510 Own and shared revenue 4,657 4,657 Resource shares - 613 Transfers 5,408 5,240 Expenditure 10,065 10,065 Deficit - (446)

Districts and lower

Revenue and transfer 29,205 43,618 Resource shares - 2,451 Transfers 23,505 35,467

Expenditure 29,205 29,205 Deficit - (14,414) Sources : MOF; staff estimates.

Fiscal Balance LawExisting Policy

Issues in Indonesia’s Equalization Grants Design

Defining Expenditure Needs Determine expenditure assignments

Defining Revenue Capacity Local tax base expansion?

How Much Equalization Data Requirements Consultation & Discussion Grants Administration Transition Arrangements

Goal

Not

“Make every region happy”

But

“Make Every Region Reasonably Unhappy”