51

Dr. Ian Giddy New York University WilmerHale Bond Market Essentials

Dr. Ian Giddy

New York University

WilmerHale

Bond Market Essentials

4Copyright ©2008 Ian H Giddy

What Are The Bond Markets?What Are The Bond Markets?

� The bond markets, as part of the global capital markets, are corporate, bank or government obligations with fixed contractual payments of interest and principal.

� Bonds are financing tools issued by different entities –but they have many comparable characteristics, including interest rates, maturity, and credit risk.

� Today’s world of structured finance and leveraged lending have given bonds a new role as catalysts for corporate recapitalizations, acquisitions, and buyouts.

5Copyright ©2008 Ian H Giddy

Bond Market EssentialsBond Market Essentials

� The Capital Markets: Investments and Financing

� Instruments of the Bond Markets

� Issuing a Corporate Bond

� Risk and Pricing of Bonds

� Bonds and the Credit Crunch

6Copyright ©2008 Ian H Giddy

Key SecuritiesKey Securities

�� Money market instrumentsMoney market instruments - Short-term debt instruments, like deposits and bills

�� BondsBonds - used by businesses and governments to raise money

�� Common StockCommon Stock - Units of ownership, interest, or equity

� Also:

�� Mezzanine, Preferred Stock, ConvertiblesMezzanine, Preferred Stock, Convertibles - Forms of investment with features of both debt and common stock

�� DerivativesDerivatives – contracts based on bonds, stocks, etc

7Copyright ©2008 Ian H Giddy

A Picture of the Global Financial MarketsA Picture of the Global Financial Markets

Source: Bank for International Settlements, 2006 AR

8Copyright ©2008 Ian H Giddy

The Players, such as Institutional Investors and Money The Players, such as Institutional Investors and Money

ManagersManagers

Institutional Investors Money Managers

Mutual Funds

Insurance Companies

Pension Funds

Hedge funds,

Central banks, etc.

Stocks

and

bonds

Money managersMoney managers

9Copyright ©2008 Ian H Giddy

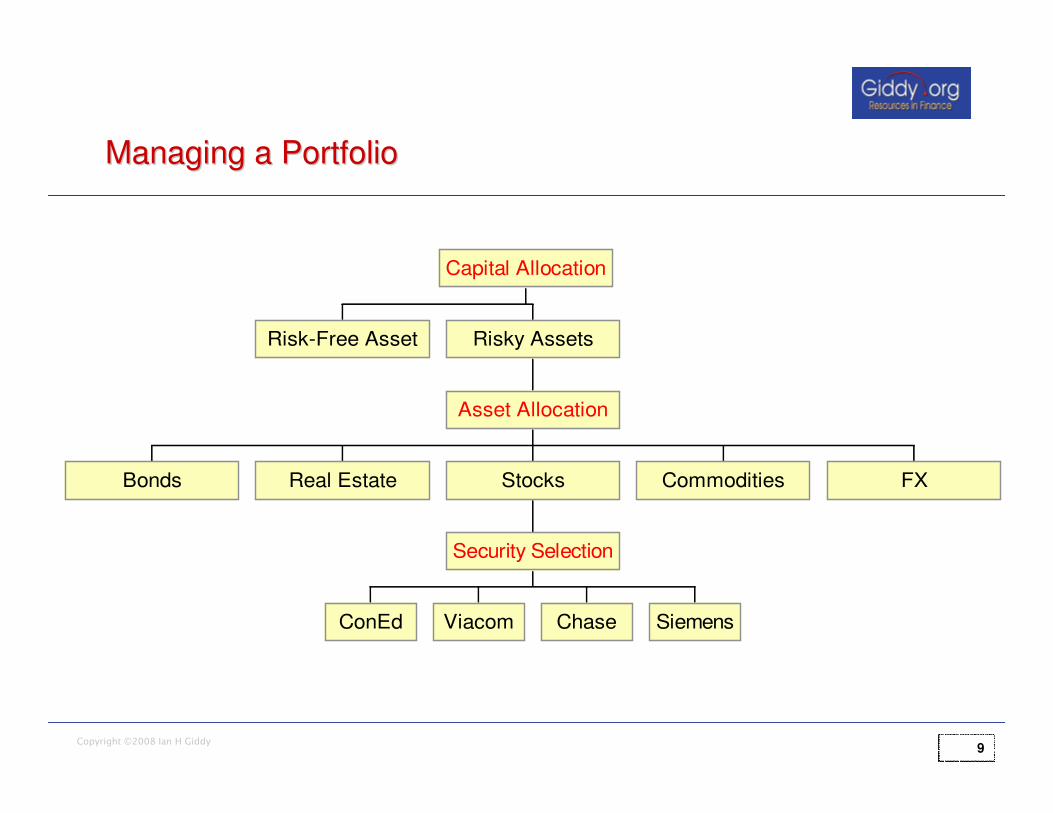

Risk-Free Asset

Bonds Real Estate

ConEd Viacom Chase Siemens

Security Selection

Stocks Commodities FX

Asset Allocation

Risky Assets

Capital Allocation

Managing a PortfolioManaging a Portfolio

10Copyright ©2008 Ian H Giddy

The InstrumentsThe Instruments

What Investments?What Investments?

Treasury Bills?

(risk-free)

Treasury Bills?

(risk-free)

Stocks and Bonds?

(risky)

Stocks and Bonds?

(risky)

11Copyright ©2008 Ian H Giddy

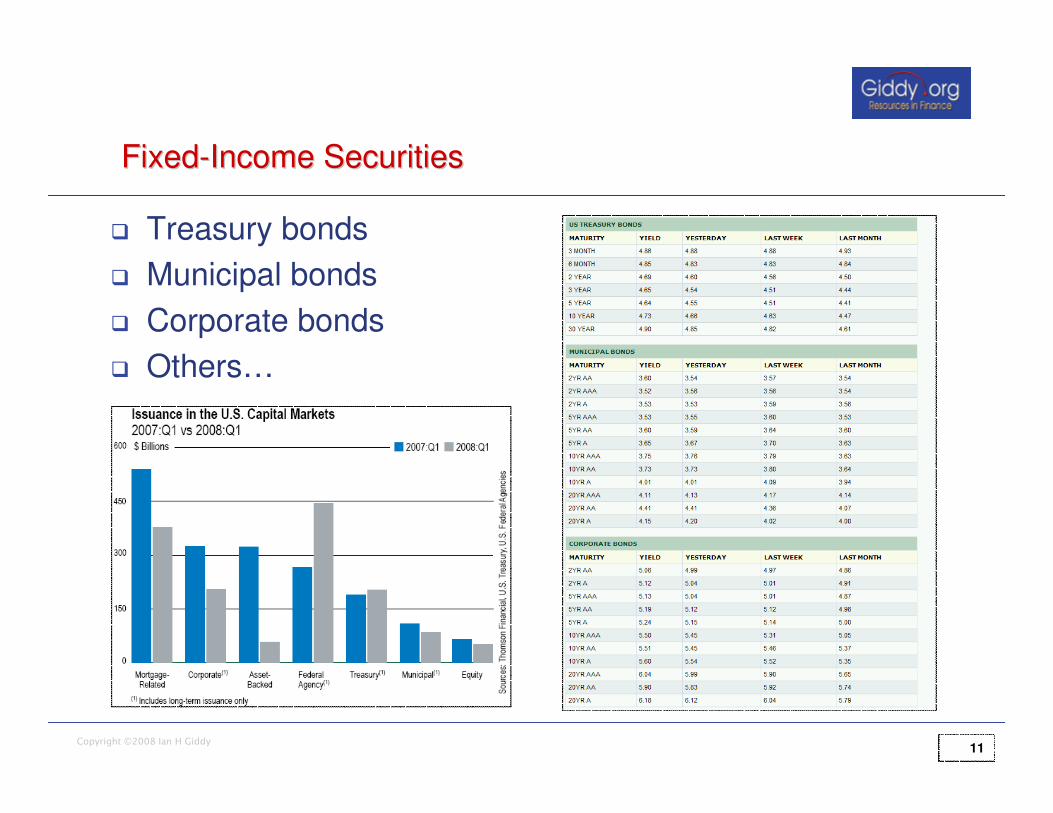

FixedFixed--Income SecuritiesIncome Securities

� Treasury bonds

� Municipal bonds

� Corporate bonds

� Others…

12Copyright ©2008 Ian H Giddy

The Bond MarketThe Bond Market

Municipal Bonds Mortgage-Backed Securities

Foreign Bonds

Euroyen Bonds, etc.

Euro$bonds

Corporate Bonds

US Treasury Bonds

Private Placements

13Copyright ©2008 Ian H Giddy

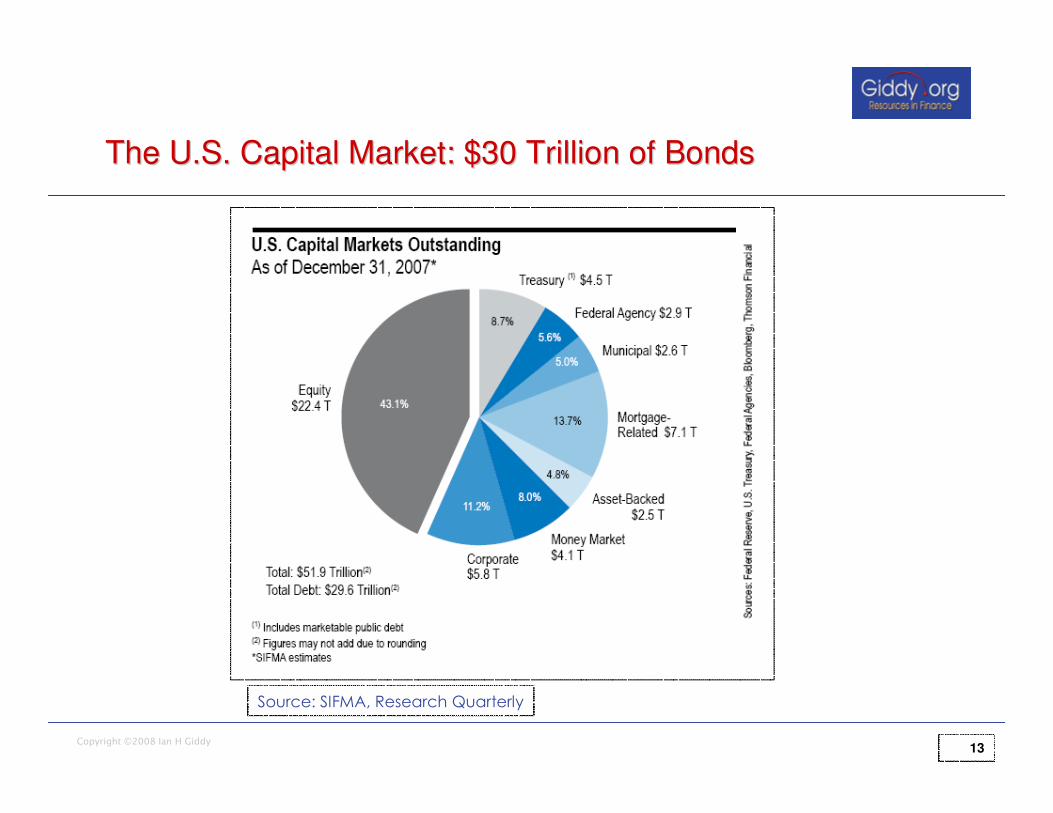

The U.S. Capital Market: $30 Trillion of BondsThe U.S. Capital Market: $30 Trillion of Bonds

Source: SIFMA, Research Quarterly

15Copyright ©2008 Ian H Giddy

TreasurysTreasurys

� Treasurys pay a semi-annual coupon and are (usually) non-callable.

16Copyright ©2008 Ian H Giddy

Agency BondsAgency Bonds

� Federal agency debt is issued by various government-sponsored enterprises (GSEs) which were created by Congress to fund loans to borrowers such as homeowners, farmers and students. Through the creation of GSEs, the government addressed various public policy concerns about the ability of members of these groups to borrow sufficient funds at affordable rates.

� Most GSEs rely primarily on debt financing for their day-to-day operations. Among the most active issuers of agency debt securities are: Federal Farm Credit System Banks, Federal Home Loan Banks, Federal Home Loan Mortgage Corporation (Freddie Mac), Federal National Mortgage Association (Fannie Mae), Student Loan Marketing Association (Sallie Mae) and Tennessee Valley Authority (TVA).

� There is an estimated $2.3 trillion in agency debt currently outstanding (April 2007).

17Copyright ©2008 Ian H Giddy

MortgageMortgage--Backed SecuritiesBacked Securities

� Mortgage securities represent an ownership interest in mortgage loans made by financial institutions (savings and loans, commercial banks, or mortgage companies) to finance the borrower's purchase of a home or other real estate.

� Mortgage-Backed Securities are created when these loans are packaged, or "pooled", by issuers or servicers for sale to investors. As the underlying mortgage loans are paid off by the homeowners, the investors receive payments of interest and principal.

� The majority of mortgage securities are issued and/or guaranteed by an agency of the U.S. Government, the Government National Mortgage Association (Ginnie Mae), or by government-sponsored enterprises such as the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac).

� Some private institutions, such as subsidiaries of investment banks, financial institutions, and home builders, also package various types of mortgage loans and mortgage pools. The securities they issue are known as "private-label" mortgage securities, in contrast to "agency" mortgage securities.

� Because most US mortgage loans are government backed, they bear little credit risk. However because fixed-rate, long-term mortgages are prepayable, they bear substantial prepayment risk.

18Copyright ©2008 Ian H Giddy

AssetAsset--Backed SecuritiesBacked Securities

� Asset-backed securities (ABS) are certificates which represent an interest in a pool of assets such as credit card receivables, auto loans and leases, or home equity loans.

� The pool of assets is sold to a Special Purpose Vehicle, which issues high-rated ABS bonds to the public – typically institutional investors.

� The SPV passes interest and principal payments on the pool of assets through to the investors.

� One form of ABS is Collateralized Debt Obligations (CDOs) – pools of corporate loans or bonds.

Source: SIFMA Quarterly

19Copyright ©2008 Ian H Giddy

Corporate BondsCorporate Bonds

� Corporate debt securities are obligations issued by corporations for capital and operating cash flow purposes.

� Corporate debt is issued by a wide variety of corporations involved in the financial, industrial, and service-related industries.

� There is approximately $4.0 trillion in corporate debt currently outstanding.

20Copyright ©2008 Ian H Giddy

Corporate Bonds and RatingsCorporate Bonds and Ratings

Why bother with a rating?

� Compare equivalent credit risks across different kinds of debt: corporate, sovereign, ABS

� Compare alternatives across different ratings levels

� Obtain a relative as well as an absolute measure of credit risk

� Be reasonably sure of a market to sell the security.

21Copyright ©2008 Ian H Giddy

What Do Ratings Mean?What Do Ratings Mean?

M o o d y’sS ta n d a rd &P o o r’s In te rp re ta tio n

A a aA a

A A AA A

H igh -qu a lity d e b t in s tru m e n ts

AB a a

AB B B

S tro n g to a d e qu a te a b ility top a y p rin c ip a l a n d in te re s t

B aBC a aC aC

B BBC C CC CC

A b ility to pa y in te re s t a ndp rin c ip a l sp e cu la tive

D In d e fa u lt

22Copyright ©2008 Ian H Giddy

What Do Ratings Tell Us About Default Rates?What Do Ratings Tell Us About Default Rates?

23Copyright ©2008 Ian H Giddy

Ratings: Contrast with AssetRatings: Contrast with Asset--Backed SecuritiesBacked Securities

24Copyright ©2008 Ian H Giddy

Corporate Bonds Corporate Bonds –– ExamplesExamples

Source: bonds.yahoo.com

25Copyright ©2008 Ian H Giddy

Instruments and MarketsInstruments and Markets

Corporate BondsCorporate Bonds

DomesticDomestic InternationalInternational

26Copyright ©2008 Ian H Giddy

� The Eurobond Market is the market for bonds issued outside the country of the currency

� The Foreign Bond Market is one in which a foreign corporation or government issues bonds in a domestic market in the local currency

� An International Equity Market has emerged that allows corporations to sell large blocks of shares simultaneously to investors in several different countries

Major International Capital MarketsMajor International Capital Markets

27Copyright ©2008 Ian H Giddy

International Bonds: GovernmentsInternational Bonds: Governments

Source: ft.com

28Copyright ©2008 Ian H Giddy

International Bonds: Emerging Markets & High YieldInternational Bonds: Emerging Markets & High Yield

Source: ft.com

� Foreign companies and government entities can issue bonds denominated in US dollars, outside of the USA

� Or they can use the 144A market, selling the bonds within the USA to institutional investors.

Dr. Ian Giddy

New York University

WilmerHale

Issuing a Corporate Bond

30Copyright ©2008 Ian H Giddy

Issuing a Corporate BondIssuing a Corporate Bond

� During 2006, Xerox’s financial condition improved, and its ratings were upgraded.

� In August 2006, the company decided that now was the time to issue a bond. Said Lawrence Zimmerman, chief financial officer: "Xerox's financial strength allows us to access the markets on an opportunistic basis, taking advantage of favorable conditions to lock in attractive interest rates."

31Copyright ©2008 Ian H Giddy

Corporate BorrowingCorporate Borrowing

� Working capital revolvers

� Bank term loans

� Leasing and other secured debt

� Bonds and other unsecuredunsecured debt

32Copyright ©2008 Ian H Giddy

Issuance of a BondIssuance of a Bond

Issuance need oropportunity identified

Announcement ofEurobond issue

Offering day:Eurobond issued

Closing day:Eurobonds delivered,

Issuer gets money

Issuerdiscussesdeal withleadmanager

Syndicateformed,bonds"presold"prior tofinal terms

Finalterms,bonds soldby sellinggroup toinvestors

33Copyright ©2008 Ian H Giddy

Bonds in Action: Bonds in Action: Issuing Corporate DebtIssuing Corporate Debt

� STAMFORD, Conn., Aug. 15, 2006 -- Xerox Bond Offering

� Xerox Corporation expects to raise $400 million through a seniorunsecured note offering announced today.

� Proceeds from the offering will be used to support the company'scustomer financing activities through unsecured debt and for general corporate purposes. The notes, which are due in 2017 andwill be issued in U.S. dollars by Xerox, will be sold under the company's effective shelf registration statement. The offering is subject to market and other conditions.

� Goldman, Sachs & Co., and Bear, Stearns & Co. Inc. are acting asjoint book-running managers for the offering.

34Copyright ©2008 Ian H Giddy

Issuing a Bond:Issuing a Bond:

Key Players in the Issuance of a BondKey Players in the Issuance of a Bond

MANAGERSUNDER-

WRITERS

SELLING

GROUP

35Copyright ©2008 Ian H Giddy

OfferingOffering

36Copyright ©2008 Ian H Giddy

SummarySummary

37Copyright ©2008 Ian H Giddy

SummarySummary

38Copyright ©2008 Ian H Giddy

Underwriting EconomicsUnderwriting Economics

Selling

Concession

60%

Underwriting

Fee

20%

Management

Fee

20%

Management Fee: Normally shared equally among managers (may be subject to a praecipium for Global Coordinator or Lead Manager)

Selling Concession: Payable as a percentage of allocation (determined by book-runner)

Underwriting Fee: Based on underwriting commitment (often less expenses of offering)

39Copyright ©2008 Ian H Giddy

Pricing and FeesPricing and Fees

The Business

� Telecoms

� Dot-Coms

� Avons(How much volatility?)

Debt

Equity

Fees

0.15%

to

1.5%

4% to

7%

Pricing

T+Spread

L+Spread

Comparables/Ratios

The market

Future cash flow valuation

The Issuer

40Copyright ©2008 Ian H Giddy

The OfferingThe Offering

� STAMFORD, Conn., Aug. 18, 2006 -- Xerox Corporation (NYSE: XRX) closed today on a $500 million offering of senior unsecured notessenior unsecured notes due in 2017 and bearing a coupon of 6.75 percent. In addition, the company closed on a $150 million offering of floating rate senior unsecured notes due in 2009. "These successful transactions give us flexibility to fund our customer financing activities with more unsecured debt than secured debt - an important step in returning Xerox to investment grade," said CFO Zimmerman, noting that the funding was "upsized" from the initial $400 million offering announced earlier this week.

� Fitch Ratings earlier this month raised its rating on Xerox to investment grade, citing the company's solid balance sheet, strengthened credit metrics, ample liquidity and improving post-sale revenue trends.

� In the second quarter of this year, Xerox generated operating cash flow of $220 million after contributing $226 million to its U.S. pension plans. The company closed the second quarter with $1.2 billion in cash and short-term investments. Debt declined $1 billion year over year and about $600 million from the first quarter of this year.

41Copyright ©2008 Ian H Giddy

The YieldThe Yield

� Yield to maturity combines coupons and capital gains - all cash flows.

� The yield to maturity on any bond, is the rate that will make the present value of the cash flows from the investment equal to the price of the investment.

� Also known as the internal rate of return or IRR.

42Copyright ©2008 Ian H Giddy

How Are Bonds Priced?How Are Bonds Priced?

Time

$1,000

?$100 $100 $100 $100

INTEREST

PRINCIPAL

The formula for a bond’s price is

BI

k

I

k

M

k n0 1 21 1 1

=

+

+

+

+ +

+( ) ( )...

( )

43Copyright ©2008 Ian H Giddy

� The yield curve shows the relationship between the interest rate, or rate of return, and the time to maturity of securities with similar issuer characteristics

� Yield curves can be downward-sloping, flat, or upward sloping

� The three theories of term structure are the expectations hypothesis, liquidity preference theory, and market segmentation theory

� A normal yield curve is upward-sloping

InterestInterest Rates and TimeRates and Time

Source: ft.com

44Copyright ©2008 Ian H Giddy

Determining a CompanyDetermining a Company‘‘s Yield: Level and Credit Factors Yield: Level and Credit Factor

� Level of rates… …and credit spreads

Source: ft.com Source: fitchratings.com

45Copyright ©2008 Ian H Giddy

Determining a CompanyDetermining a Company‘‘s Yield: Level and Credit Factors Yield: Level and Credit Factor

� Level of rates… …or credit default swaps

Source: ft.com Source: fitchratings.com

46Copyright ©2008 Ian H Giddy

The Crunch: Major BanksThe Crunch: Major Banks’’ Credit Default Swap Credit Default Swap PremiaPremia

Sources: Markit Group Limited, Thomson Datastream, published accounts and Bank of England calculations.

(a) Data to close of business on 22 April 2008.(b) Asset-weighted average five-year premia.(c) October 2007 Report.

47Copyright ©2008 Ian H Giddy

Sources: Bank of England, Bloomberg, Chicago Board Options Exchange, Debt Management Office, London Stock Exchange, Merrill Lynch, Thomson Datastream and Bank calculations.

The liquidity index shows the number of standard deviations from the mean. It is a simple unweighted average of nine liquidity measures, normalised on the period 1999–2004. The series shown is an exponentially weighted moving average. The indicator is more reliable after 1997 as it is based on a greater number of underlying measures.

The Result: Financial Market IlliquidityThe Result: Financial Market Illiquidity

48Copyright ©2008 Ian H Giddy

Sudden DebtSudden Debt

Source: International Monetary Fund, Global Financial Stability Report, April 2008

49Copyright ©2008 Ian H Giddy

Banks Exposed to Banks Exposed to ““ABSABS”” CDOsCDOs are Worst Hurtare Worst Hurt

Source: International Monetary Fund, Global Financial Stability Report, April 2008

50Copyright ©2008 Ian H Giddy

Worst Problems Arose from Nested Worst Problems Arose from Nested ““ABSABS”” CDOsCDOs

51Copyright ©2008 Ian H Giddy

The Domino Effect?The Domino Effect?Sub

prim

e

Res

iden

tial M

BS

Com

merc

ial M

BS

Leve

raged L

oans

Securitizations

CD

Os

of S

ecuritizations

Cre

dit D

eriva

tive

s

Asset-

Backed C

P &

SIV

s

Hedge F

unds

Banks

Monolin

es

Sove

reig

n &

Sub-S

ov

52Copyright ©2008 Ian H Giddy

The Bad NewsThe Bad News……and the Goodand the Good

53Copyright ©2008 Ian H Giddy

Bond Market Essentials: SummaryBond Market Essentials: Summary

� The Capital Markets: Investments and Financing

� Instruments of the Bond Markets

� Issuing a Corporate Bond

� Risk and Pricing of Bonds

� Bonds and the Credit Crunch

54Copyright ©2008 Ian H Giddy

Ian H. Giddy

NYU Stern School of Business

Tel +1.646-8080-746; Fax +1.866-369-9350

www.giddy.org

Contact InformationContact Information