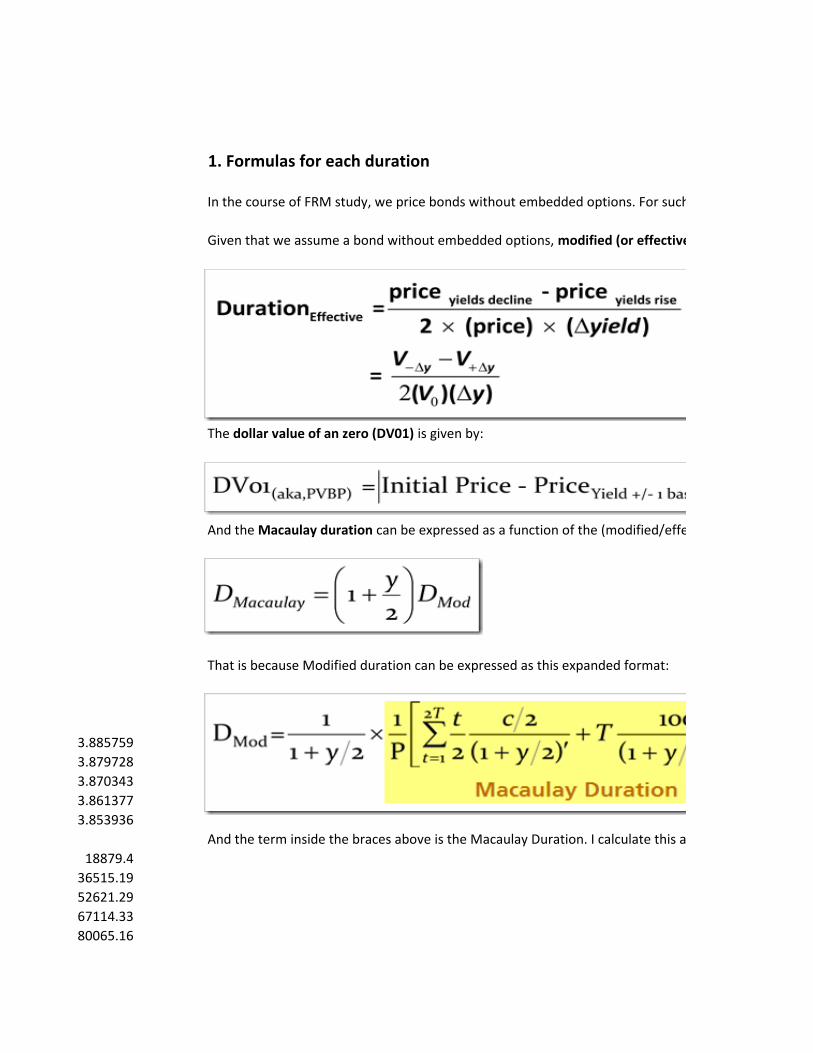

In the course of FRM study, we price bonds without embedded options. For such plain-vanilla bonds, the distinction between modified and effective duration does not matter. (see Fabozzi for the difference: effective duration recognizes that cash flows dynamically change with the yield. An unnecessary nuance in our case).

Given that we assume a bond without embedded options, modified (or effective) duration is given by:

The dollar value of an zero (DV01) is given by:

And the Macaulay duration can be expressed as a function of the (modified/effective) duration above:

That is because Modified duration can be expressed as this expanded format:

3.885759

3.879728

3.870343

3.861377

3.853936

And the term inside the braces above is the Macaulay Duration. I calculate this above formula in the spreadsheet below (see the blue section, which solves for the Macaulay)

In the course of FRM study, we price bonds without embedded options. For such plain-vanilla bonds, the distinction between modified and effective duration does not matter. (see Fabozzi for the difference: effective duration recognizes that cash flows dynamically change with the yield. An unnecessary nuance in our case).

Given that we assume a bond without embedded options, modified (or effective) duration is given by:

And the Macaulay duration can be expressed as a function of the (modified/effective) duration above:

And the term inside the braces above is the Macaulay Duration. I calculate this above formula in the spreadsheet below (see the blue section, which solves for the Macaulay)

In the course of FRM study, we price bonds without embedded options. For such plain-vanilla bonds, the distinction between modified and effective duration does not matter. (see Fabozzi for the difference: effective duration recognizes that cash flows dynamically change with the yield. An unnecessary nuance in our case).

In the course of FRM study, we price bonds without embedded options. For such plain-vanilla bonds, the distinction between modified and effective duration does not matter. (see Fabozzi for the difference: effective duration recognizes that cash flows dynamically change with the yield. An unnecessary nuance in our case).

Basel 2.5 Tripled Year-End 2011 Regulatory Capital Disclosures For Large Banks

Potential Overlaps, Gaps, And Inconsistencies In Basel 2.5

Basel 2.5 Should Improve Public Disclosure

Further Ahead, Basel III Will Add Further Market Risk Capital Charges

Related Criteria And Research

Standard & Poor's Ratings Services broadly welcomes Basel 2.5, the Basel Committee on Banking Supervision's regulations requiring banks to hold greater capital against the market risks they run in their trading operations. These new regulations, which are now live in most major trading centers globally except the U.S., were responsible for a threefold increase in the year-end 2011 capital charge on traded market risk among 11 European banks that we have reviewed. We believe that this adds to the pressure on investment banking returns and will encourage derisking and deleveraging of trading book activities.

We don't anticipate that the new regulations will have a systematic impact on our ratings on banks because our risk-adjusted capital (RAC) framework--our primary capital analysis tool--already applied far higher charges to banks' trading positions than the Basel II Accord required. Nevertheless, the disclosure of new information that Basel 2.5 requires could lead us to revise downward our capital and earnings assessment, which could result in rating downgrades in some isolated cases. We have today published an advance notice of a proposed criteria change explaining how we propose to adapt the RAC charges to Basel 2.5 disclosures. (Watch the related CreditMatters TV segment titled, "Basel 2.5's Impact On Investment Banking Returns," dated May 14, 2012.)

OverviewBasel 2.5 in our view raises regulatory capital requirements on traded market risk to a more appropriate level.

We are in favor of these tougher rules because they are consistent with the direction of Standard & Poor's approach in its risk-adjusted capital framework.

Nevertheless, we believe the Basel 2.5 measures are complex and there could be overlaps and gaps between them, as well as inconsistencies in implementation between individual banks.

In an analysis of 11 banks, we found that Basel 2.5 regulations were responsible for an average threefold increase in their capital charge on traded market risk.

Basel 2.5 is one of several factors squeezing investment banks' returns, and staggered implementation across the world has added to the sector's uneven playing field.

We consider the enhanced regulations as directionally consistent with the approach we take in our RAC framework and a significant step forward in addressing the deficiencies of the original Basel II framework in light of lessons learned from the financial market crisis. Building on the Basel II value-at-risk (VaR) capital charge, Basel 2.5 introduces extra charges to bolster what regulators viewed as an undercapitalized trading book. A new stressed value at risk charge uses a 12-month period of market turmoil to assess potential losses above the 99% confidence level used in the VaR model. Basel 2.5 also imposes an incremental risk charge that captures default and credit migration risk, a standardized charge for securitizations and resecuritizations, and a comprehensive risk measure for correlation trading.

Yet, although an improvement, we believe the new measures are complex, and that they open up potential for overlaps (double-counting of risks) and gaps (inadequate assessment of certain risks). We also see scope for inconsistencies in their implementation among individual banks.

The higher regulatory capital requirement under Basel 2.5, as well as further regulations in the forthcoming Basel III regime, in our view represent the main challenges to investment banks' ability to generate sustainable returns in excess of their cost of capital. It adds to pressures they are already facing, such as tighter conditions in wholesale funding markets, a structural shift away from higher return products following the financial crisis, and market uncertainties that have dampened client activity. The industry is responding by adapting its balance-sheet usage, funding model, expense base, and risk profile to the new regulatory and market context. Accordingly, we expect further restructuring and deleveraging as banks seek to optimize inventory positions, increase balance-sheet turnover, and refocus allocated capital on their competitive strengths.

Furthermore, the staggered implementation of Basel 2.5 across the world has added to the uneven playing field for global investment banks. It was introduced in Switzerland on Jan. 1, 2011, although the Bank for International Settlements (BIS) capital ratios published during 2011 by Swiss banks were still computed using Basel II rules. It came into force in the EU and other major trading centers except the U.S. on Dec. 31, 2011. We understand that Basel 2.5 implementation in the U.S. has been delayed, probably until later this year, while authorities adapt it to satisfy a Dodd-Frank Act requirement concerning the use of external credit ratings.

We believe the European banks' preparations for Basel 2.5 contributed to their trading book derisking and deleveraging in the second half of 2011 and perhaps put them at a competitive disadvantage relative to their U.S. peers. In our view, it is possible that the delayed implementation of Basel 2.5 in the U.S. might also have contributed to specific transactions, such as sales of correlation trading portfolios by some European banks to U.S. competitors. On the other hand, we see other differences and inconsistencies in national regulations that might penalize U.S. banks more than their international peers.

What Is Basel 2.5?Basel 2.5 is a complex package of international rules that imposes higher capital charges on banks for the market risks they run in their trading books, particularly credit-related products. The Basel Committee on Banking Supervision began the process of enhancing the Basel II market risk framework in 2005, and widened the scope materially in response to the subsequent financial crisis.

The four main elements of Basel 2.5 are:A stressed value-at-risk (SVaR) model, which adds to the VaR-based capital requirements in Basel II. SVaR is intended to capture more adequately the potential consequences of more volatile market conditions than those encountered in the historical prices on which their VaR models are based.

The incremental risk charge (IRC), which aims to capture default and credit migration risk.

New standardized charges for securitization and resecuritization positions.

The comprehensive risk measure (CRM) for correlation trading positions, which assesses default and migration risk of the underlying exposures.

The capital requirement generated by each of these measures adds to those of Basel II, with no possibility of reductions for risk offsets or for possible double counting.

Stressed value-at-risk (SVaR) model

The original Basel II market risk framework calculated banks' capital requirement according to standardized charges or the output of VaR models. These VaR models are validated by national regulators for either general risk only or both general and specific risk. They mostly estimate the probability of portfolio losses based on the statistical analysis of historical price trends and volatilities over the prior one-year period. Some banks, however, incorporate a longer time frame, such as UBS AG (A/Negative/A-1). Regulatory VaR models use a 99% confidence interval and assume a 10-day holding period.

In order to capture the potential consequences of more volatile market conditions than those encountered in the historical prices on which their VaR models are based, Basel 2.5 additionally requires banks to calculate the stressed VaR on their portfolios. These SVaR models have the same confidence interval and holding period as the VaR models, but must be based on a one-year historic dataset that would produce significant losses for the total portfolio. The volatile market conditions of 2007-2009 are an obvious starting point for banks looking to find stressed market data, although their choices will depend on the composition and positioning of their aggregate portfolio.

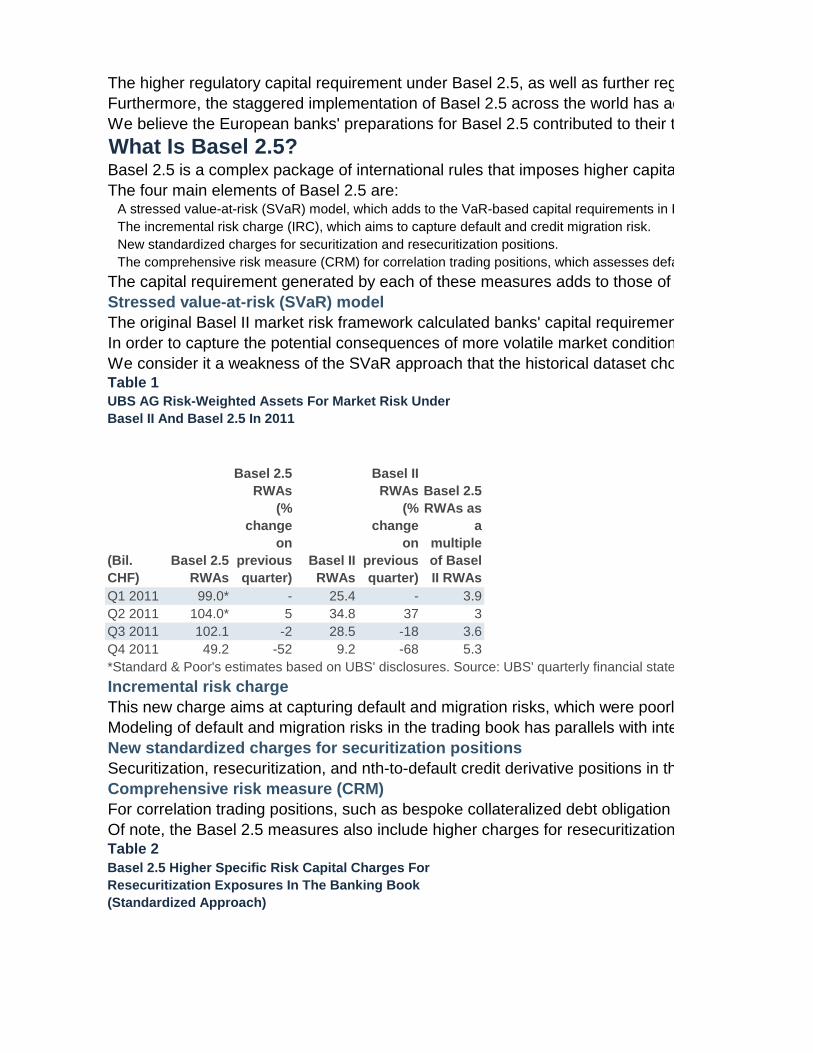

We consider it a weakness of the SVaR approach that the historical dataset chosen for the portfolio as a whole may not represent the most significant stress for some individual asset classes, such as commodities or sovereign bonds, especially those from the European Economic and Monetary Union (EMU or eurozone). We also consider that SVaR model results can be sensitive to the choice of proxies. For example, banks need to use proxies to model historical prices for securities that did not exist during the 2007-2009 crisis. The introduction of SVaR under Basel 2.5 should nevertheless make the regulatory market risk charge less volatile than it was under Basel II. Quarterly Basel II and Basel 2.5 risk-weighted asset (RWA) data published in 2011 by UBS supports this view (see table 1). The bank managed its market risk appetite relatively actively in this period.Table 1

(Bil.

CHF)

Basel 2.5

RWAs

Basel 2.5

RWAs

(%

change

on

previous

quarter)

Basel II

RWAs

Basel II

RWAs

(%

change

on

previous

quarter)

Basel 2.5

RWAs as

a

multiple

of Basel

II RWAs

Q1 2011 99.0* - 25.4 - 3.9

Q2 2011 104.0* 5 34.8 37 3

Q3 2011 102.1 -2 28.5 -18 3.6

Q4 2011 49.2 -52 9.2 -68 5.3

Incremental risk charge

This new charge aims at capturing default and migration risks, which were poorly captured, in our view, in specific risk VaR models. VaR models better capture potential losses due to credit spread variations at unchanged credit rating levels. Typical positions included in the scope of the incremental risk charge (IRC) model are bonds, credit default swaps, and traded loans. The scope excludes securitization positions. The IRC is measured with a one-year holding period and 99.9% confidence interval. We see these parameters as a clear improvement over the 10-day holding period and 99% confidence interval of regulatory VaR models.

Modeling of default and migration risks in the trading book has parallels with internal rating-based modeling of credit risk in the banking book and therefore presents similar challenges, such as how to analyze highly rated securities with little or no history of losses. In theory, banks could differentiate between the liquidity horizon (the time to liquidate the positions, if needed, with a regulatory "floor" of three months) and the capital horizon (which is one year). For positions with a liquidity horizon lower than one year, the IRC assumes that, when liquidated, each position is replaced with a position bearing the same level of risk as the initial one. In practice, however, we note that a majority of banks have chosen to use a liquidity horizon of one year for all positions. We observe that about 70%-80% of the IRC charge reflects the modeling of default whereas the residual stems from credit migration risk: the downgrade of a bond, for example, being associated in general with higher credit spreads an

New standardized charges for securitization positions

Securitization, resecuritization, and nth-to-default credit derivative positions in the trading book are excluded from the IRC and subjected instead to different approaches. With the exception of positions held in correlation trading portfolios, which are the subject of the CRM charge described below, securitization tranches receive banking book capital charges and there are higher risk weights for resecuritizations. Lower rated positions must be deducted from regulatory capital, 50% from Core Tier 1 capital and 50% from Tier 2. We observe that the Basel II VaR charge on these positions was generally low and the effect of these changes is to increase the capital requirement for securitizations and resecuritizations substantially. As an example, because of the new Basel 2.5 rules, Credit Suisse deducted an additional CHF2.37 billion ($2.5 billion) of lower rated securitization positions from regulatory capital at year-end 2011. This compares with total capital requirements for market risk of Swiss franc (CHF)

Comprehensive risk measure (CRM)

For correlation trading positions, such as bespoke collateralized debt obligation (CDO) tranches sold to customers and their hedges, the CRM assesses default and migration risk of the underlying exposures. It incorporates basis risk--that is, the risk that a hedge becomes less effective--and the potential costs of resetting a hedge following a change in the underlying position, such as an amendment to the composition of an index. The CRM is subject to a floor of at least 8% of the capital charge for specific risk according to the standardized approach. This floor is generally binding, or close to binding, for the banks with the largest correlation trading portfolios. We understand that the Basel Committee carved out correlation portfolios from the IRC because assessing trading positions and their hedges separately might have overstated the underlying risks.

Of note, the Basel 2.5 measures also include higher charges for resecuritization in the banking book as well as higher charges for the specific risk on equity holdings in the trading book under the standardized approach for market risk (see table 2).Table 2

UBS AG Risk-Weighted Assets For Market Risk Under

Basel II And Basel 2.5 In 2011

*Standard & Poor's estimates based on UBS' disclosures. Source: UBS' quarterly financial statements.

Basel 2.5 Higher Specific Risk Capital Charges For

Resecuritization Exposures In The Banking Book

(Standardized Approach)

External

credit

Assessm

ent

AAA to

AA-

A+ to A- BBB+ to

BBB-

BB+ to

BB-

Below BB-

Charge

under

Basel II

1.60% 4% 8% 28% Deductio

n from

regulator

y capital

Charge

under

Basel 2.5

3.20% 8% 18% 52% Deductio

n from

regulator

y capital

Basel 2.5 Tripled Year-End 2011 Regulatory Capital Disclosures For Large BanksThe new regulatory measures are already significantly increasing capital charges on traded risks, particularly for large international banks. The introduction of the new Basel 2.5 measures translated into a 5.2% increase in total regulatory risk-weighted assets (RWA) as of June 30, 2011, for Group 1 banks--that is, banks with Tier 1 capital above €3 billion and which are internationally active--according to a recent study by the Bank for International Settlements based on 102 banks which had already implemented Basel 2.5. The introduction of the SVaR charge accounted for more than one-third of this increase, the IRC for just less than one-quarter.

The impact on RWA will be higher for banks with large investment banking activities. We estimate that, for these banks, regulatory capital charges for market risk increased threefold with the introduction of Basel 2.5. This figure includes the impact of the additional deductions from regulatory capital, owing to lower rated securitization in the trading book.

In general, banks that included most of their trading positions in their Basel II regulatory VaR model, such as UBS, face the greatest increase in regulatory market risk RWAs. On the contrary, banks for which the scope of the VaR model was limited, and which therefore use the more stringent standardized approach for a significant part of the trading portfolio, are less affected. For example, we observe that the impact of Basel 2.5 for U.K. banks is probably more limited than for their main competitors. This is mainly because the scope of U.K. banks' regulatory VaR models reflects the U.K. Financial Services Authority's relatively cautious approach to granting model approval. Furthermore, U.K. banks' capital requirements for market risk under Basel II generally included a charge for incremental default risk, which anticipated the IRC charge. This charge, for example, was £751 million for Royal Bank of Scotland in 2010.

Our survey of 11 large international banks shows that SVaR accounted for the largest component of the Basel 2.5 charges as of year-end 2011, with close to 30% of the total (see chart 1).Chart 1

It is worth noting that the VaR charge under Basel 2.5 is not directly comparable with the VaR charge under the former Basel II rules for the following reasons:Regulators have removed the specific risk surcharge;

The scope of the specific risk VaR model under Basel 2.5 is not always comparable with the scope of the model under Basel II. For example, some securitization positions and their hedges may be excluded from the Basel II.5 model since specific risk is now captured by other charges; and

Some banks, including those in the U.K., already included an Incremental Default Risk (IDR) charge in the Basel II VaR model. This IDR charge has now been replaced (and complemented) by the IRC.

For several banks, the year-end 2011 impact of Basel 2.5 was lower than their guidance earlier in the year. This resulted from trading book deleveraging and derisking undertaken in the second half of 2011 in preparation for the new regulations and in response to the adverse market conditions. For example, incremental RWA resulting from Basel 2.5 was €52 billion for Deutsche Bank AG (A+/Negative/A-1) as of Dec. 31, 2011. Based on its September 2011 positions, the incremental RWA would have been 46% higher (€76 billion).

Potential Overlaps, Gaps, And Inconsistencies In Basel 2.5We support the higher capital charges introduced by Basel 2.5 because we consider that the capital requirement on market risk was too low under the Basel II regime, therefore providing an incentive for banks to hold securities in the trading book rather than the banking book. Nonetheless, we view the Basel 2.5 measures as complex and difficult to implement. Even under the Basel II VaR regime, we believe banks found it time-consuming and challenging to assess the marginal impact of a new trading position. Under Basel 2.5 this is even more so the case.

We see potential for the following overlaps and gaps in the Basel 2.5 risk measures, as well as the possibility for inconsistencies in their implementation.

Overlaps

In our view, the Basel 2.5 framework gives rise to potential double-counting of the same risks. This is most evident by the inclusion of both VaR and SVaR measures, which will likely generate similar results in times of high market volatility. There is also potentially some double-counting between SVaR and the IRC in the case of speculative-grade bonds or higher risk tradable loans, for which the SVaR would be akin to a default charge. Taking the example of a straightforward trading exposure, such as a long speculative-grade bond position, it appears possible that the aggregate size of the VaR, SVaR, and IRC charges might in some cases overstate the risk inherent in that particular position. In theory, the aggregate charges on the bond might even exceed its fair value, although it is questionable whether such a scenario would arise in practice. Overlaps might also arise from correlation trading positions, which in many instances are still included in the scope of the VaR model. This is because the hedges on b

Gaps

While we consider that Basel 2.5 captures a broader range of market risks than the previous regulatory regime, certain risks are still not adequately assessed, in our view. In particular, this includes interest rate risk in the banking book, which is not specifically considered in Basel 2.5 or Basel III and therefore still does not attract Pillar 1 regulatory capital charges. The likely reason for this is the complexity in quantifying this risk in a consistent and meaningful way. For similar reasons, in our RAC framework we do not assign capital charges to market risk in the banking book, but instead consider it qualitatively.

Within the trading book, an example of a gap in the coverage of Basel 2.5 is the absence of a capital charge on the risk of severe adverse changes in counterparties' creditworthiness. We note, however, that this will be introduced in Basel III.

A further gap arises from the risk associated with a sudden contraction in market liquidity, which in our view is only partly captured by the one-year time horizon of the IRC. Market risk models assume that positions are constant over the holding period and can then be closed or hedged without cost. In reality, however, trading positions tend to be managed dynamically and the financial crisis illustrated that close-out and hedging costs can be significant. This risk was amplified by Lehman Brothers' default in 2008, when counterparties had to rehedge exposures at a time of severe price volatility. Furthermore, significant jumps in, or the unavailability of, market prices due to illiquidity, known as gap risk, can make valuing and hedging positions difficult. The regulatory models do not fully take this into account, in our view. As part of the consultative document, "Fundamental review of trading book," which the BIS published on May, 3. 2012, regulators suggest classifying banks' exposures into different liq

Inconsistencies

The extensive use of internal models under both the Basel II and Basel 2.5 market risk frameworks means that individual institutions might treat the same risks in different ways. The requirement for models to be validated by national regulators reduces the scope for material inconsistencies, but is unlikely to eliminate them, in our view. Under Basel 2.5, in addition to the overall characteristics of individual models--such as whether certain risks are captured within a VaR model or through specific add-ons--discrepancies might occur in the choice of the historical window for the SVaR model, in the treatment of highly rated securities in the IRC, in the use of proxies in SVaR, or in the modeling of the recovery rate for the IRC.

These overlaps, gaps, and inconsistencies emphasize to us that effective market risk management requires more tools and metrics than just regulatory-driven measures. Stress testing and scenario modeling would be prime additions, in our view. For example, two types of stress tests that have become more common since the financial crisis are liquidity-adjusted stress tests, which take into account the expected liquidity in stress conditions of different products and different sizes of trading positions, and reverse stress tests, which assess the circumstances in which a portfolio might incur a certain level of losses.

Nevertheless, although we see some drawbacks and inconsistencies within the Basel 2.5 regime, we consider that it is the best starting point for our RAC charges since it will be applied by all major investment banks once it is adopted in the U.S., and because public disclosure of market risk exposures is largely based on regulatory measures.

Basel 2.5 Should Improve Public DisclosureWe welcome the elements of Basel 2.5 that call for improved reporting of market risk exposures in banks' Pillar 3 reports (which cover capital adequacy and risk management). In particular, whenever relevant, we would expect banks to disclose not only the total amount of market risk RWA under Basel 2.5, but also the regulatory RWA due to each component--that is, the VaR-based charge, SVaR charge, IRC, CRM, and regulatory charge according to the standardized approach. We would also expect banks to identify specifically the proportion of total RWAs derived from the standardized approach that is actually imputable to securitization exposures in the trading book. Some granularity regarding the external ratings of securitization exposures in the trading book (including exposures that are deducted from regulatory capital) would also be an improvement. Finally, we would consider as best practice that banks disclose the breakdown of positions included in the IRC (such as bonds and traded loans) by internal ratings ran

Further Ahead, Basel III Will Add Further Market Risk Capital ChargesBasel 2.5 will not be the last word on regulatory capital charges for traded market risk. The Basel III regime, due to come into effect from 2013, will require banks to hold more and better quality capital. It also includes new additive capital charges for credit valuation adjustment risk (CVA; an adjustment to the valuation of trades based on the creditworthiness of the counterparty), and for wrong-way risk (where the exposure to a counterparty increases while the counterparty's creditworthiness worsens). We believe that the CVA charge will have a material impact on RWAs and, in some instances, an even greater impact than the entire Basel 2.5 package. For example, Deutsche Bank quantifies incremental RWA due to Basel III at €105 billion, most of it arising from the new CVA charge, compared with additional RWA of €52 billion for the entire Basel II.5 set of measures. UBS estimated that the CVA charge itself would have added about CHF50 billion to its Basel 2.5 RWAs as of year-end 2011, but it believed that mi

The Basel Committee has recently conducted a trading book review to assess the effectiveness of the market risk framework in light of the Basel 2.5 and Basel III measures. In its consultative document, published on May, 3. 2012, the Basel Committee considers fundamental questions regarding the design of the regulatory market risk framework, such as the boundary between the trading and banking books and the relationship between internal models-based and standardized approaches, with the goal of better aligning the treatment of hedging and diversification between the two approaches. It also considers the comprehensive incorporation of the risk of market illiquidity and the possibility of replacing VaR with expected-shortfall measures to better capture tail risk.

In our view, banks may hope that future changes would also consider simplifying the complex measures introduced by Basel 2.5 and Basel III. The current framework seems more like a patchwork of additive charges, with double-counting issues and gaps not yet fully addressed, in our view. Yet history suggests that it will take several years to implement any changes that result from the review and may perhaps form part of a future Basel 3.5 or a Basel IV accord.

Standard & Poor's Ratings Services broadly welcomes Basel 2.5, the Basel Committee on Banking Supervision's regulations requiring banks to hold greater capital against the market risks they run in their trading operations. These new regulations, which are now live in most major trading centers globally except the U.S., were responsible for a threefold increase in the year-end 2011 capital charge on traded market risk among 11 European banks that we have reviewed. We believe that this adds to the pressure on investment banking returns and will encourage derisking and deleveraging of trading book activities.

We don't anticipate that the new regulations will have a systematic impact on our ratings on banks because our risk-adjusted capital (RAC) framework--our primary capital analysis tool--already applied far higher charges to banks' trading positions than the Basel II Accord required. Nevertheless, the disclosure of new information that Basel 2.5 requires could lead us to revise downward our capital and earnings assessment, which could result in rating downgrades in some isolated cases. We have today published an advance notice of a proposed criteria change explaining how we propose to adapt the RAC charges to Basel 2.5 disclosures. (Watch the related CreditMatters TV segment titled, "Basel 2.5's Impact On Investment Banking Returns," dated May 14, 2012.)

Basel 2.5 in our view raises regulatory capital requirements on traded market risk to a more appropriate level.

We are in favor of these tougher rules because they are consistent with the direction of Standard & Poor's approach in its risk-adjusted capital framework.

Nevertheless, we believe the Basel 2.5 measures are complex and there could be overlaps and gaps between them, as well as inconsistencies in implementation between individual banks.

In an analysis of 11 banks, we found that Basel 2.5 regulations were responsible for an average threefold increase in their capital charge on traded market risk.

Basel 2.5 is one of several factors squeezing investment banks' returns, and staggered implementation across the world has added to the sector's uneven playing field.

We consider the enhanced regulations as directionally consistent with the approach we take in our RAC framework and a significant step forward in addressing the deficiencies of the original Basel II framework in light of lessons learned from the financial market crisis. Building on the Basel II value-at-risk (VaR) capital charge, Basel 2.5 introduces extra charges to bolster what regulators viewed as an undercapitalized trading book. A new stressed value at risk charge uses a 12-month period of market turmoil to assess potential losses above the 99% confidence level used in the VaR model. Basel 2.5 also imposes an incremental risk charge that captures default and credit migration risk, a standardized charge for securitizations and resecuritizations, and a comprehensive risk measure for correlation trading.

Yet, although an improvement, we believe the new measures are complex, and that they open up potential for overlaps (double-counting of risks) and gaps (inadequate assessment of certain risks). We also see scope for inconsistencies in their implementation among individual banks.

The higher regulatory capital requirement under Basel 2.5, as well as further regulations in the forthcoming Basel III regime, in our view represent the main challenges to investment banks' ability to generate sustainable returns in excess of their cost of capital. It adds to pressures they are already facing, such as tighter conditions in wholesale funding markets, a structural shift away from higher return products following the financial crisis, and market uncertainties that have dampened client activity. The industry is responding by adapting its balance-sheet usage, funding model, expense base, and risk profile to the new regulatory and market context. Accordingly, we expect further restructuring and deleveraging as banks seek to optimize inventory positions, increase balance-sheet turnover, and refocus allocated capital on their competitive strengths.

Furthermore, the staggered implementation of Basel 2.5 across the world has added to the uneven playing field for global investment banks. It was introduced in Switzerland on Jan. 1, 2011, although the Bank for International Settlements (BIS) capital ratios published during 2011 by Swiss banks were still computed using Basel II rules. It came into force in the EU and other major trading centers except the U.S. on Dec. 31, 2011. We understand that Basel 2.5 implementation in the U.S. has been delayed, probably until later this year, while authorities adapt it to satisfy a Dodd-Frank Act requirement concerning the use of external credit ratings.

We believe the European banks' preparations for Basel 2.5 contributed to their trading book derisking and deleveraging in the second half of 2011 and perhaps put them at a competitive disadvantage relative to their U.S. peers. In our view, it is possible that the delayed implementation of Basel 2.5 in the U.S. might also have contributed to specific transactions, such as sales of correlation trading portfolios by some European banks to U.S. competitors. On the other hand, we see other differences and inconsistencies in national regulations that might penalize U.S. banks more than their international peers.

Basel 2.5 is a complex package of international rules that imposes higher capital charges on banks for the market risks they run in their trading books, particularly credit-related products. The Basel Committee on Banking Supervision began the process of enhancing the Basel II market risk framework in 2005, and widened the scope materially in response to the subsequent financial crisis.

A stressed value-at-risk (SVaR) model, which adds to the VaR-based capital requirements in Basel II. SVaR is intended to capture more adequately the potential consequences of more volatile market conditions than those encountered in the historical prices on which their VaR models are based.

The comprehensive risk measure (CRM) for correlation trading positions, which assesses default and migration risk of the underlying exposures.

The capital requirement generated by each of these measures adds to those of Basel II, with no possibility of reductions for risk offsets or for possible double counting.

The original Basel II market risk framework calculated banks' capital requirement according to standardized charges or the output of VaR models. These VaR models are validated by national regulators for either general risk only or both general and specific risk. They mostly estimate the probability of portfolio losses based on the statistical analysis of historical price trends and volatilities over the prior one-year period. Some banks, however, incorporate a longer time frame, such as UBS AG (A/Negative/A-1). Regulatory VaR models use a 99% confidence interval and assume a 10-day holding period.

In order to capture the potential consequences of more volatile market conditions than those encountered in the historical prices on which their VaR models are based, Basel 2.5 additionally requires banks to calculate the stressed VaR on their portfolios. These SVaR models have the same confidence interval and holding period as the VaR models, but must be based on a one-year historic dataset that would produce significant losses for the total portfolio. The volatile market conditions of 2007-2009 are an obvious starting point for banks looking to find stressed market data, although their choices will depend on the composition and positioning of their aggregate portfolio.

We consider it a weakness of the SVaR approach that the historical dataset chosen for the portfolio as a whole may not represent the most significant stress for some individual asset classes, such as commodities or sovereign bonds, especially those from the European Economic and Monetary Union (EMU or eurozone). We also consider that SVaR model results can be sensitive to the choice of proxies. For example, banks need to use proxies to model historical prices for securities that did not exist during the 2007-2009 crisis. The introduction of SVaR under Basel 2.5 should nevertheless make the regulatory market risk charge less volatile than it was under Basel II. Quarterly Basel II and Basel 2.5 risk-weighted asset (RWA) data published in 2011 by UBS supports this view (see table 1). The bank managed its market risk appetite relatively actively in this period.

This new charge aims at capturing default and migration risks, which were poorly captured, in our view, in specific risk VaR models. VaR models better capture potential losses due to credit spread variations at unchanged credit rating levels. Typical positions included in the scope of the incremental risk charge (IRC) model are bonds, credit default swaps, and traded loans. The scope excludes securitization positions. The IRC is measured with a one-year holding period and 99.9% confidence interval. We see these parameters as a clear improvement over the 10-day holding period and 99% confidence interval of regulatory VaR models.

Modeling of default and migration risks in the trading book has parallels with internal rating-based modeling of credit risk in the banking book and therefore presents similar challenges, such as how to analyze highly rated securities with little or no history of losses. In theory, banks could differentiate between the liquidity horizon (the time to liquidate the positions, if needed, with a regulatory "floor" of three months) and the capital horizon (which is one year). For positions with a liquidity horizon lower than one year, the IRC assumes that, when liquidated, each position is replaced with a position bearing the same level of risk as the initial one. In practice, however, we note that a majority of banks have chosen to use a liquidity horizon of one year for all positions. We observe that about 70%-80% of the IRC charge reflects the modeling of default whereas the residual stems from credit migration risk: the downgrade of a bond, for example, being associated in general with higher credit spreads an

Securitization, resecuritization, and nth-to-default credit derivative positions in the trading book are excluded from the IRC and subjected instead to different approaches. With the exception of positions held in correlation trading portfolios, which are the subject of the CRM charge described below, securitization tranches receive banking book capital charges and there are higher risk weights for resecuritizations. Lower rated positions must be deducted from regulatory capital, 50% from Core Tier 1 capital and 50% from Tier 2. We observe that the Basel II VaR charge on these positions was generally low and the effect of these changes is to increase the capital requirement for securitizations and resecuritizations substantially. As an example, because of the new Basel 2.5 rules, Credit Suisse deducted an additional CHF2.37 billion ($2.5 billion) of lower rated securitization positions from regulatory capital at year-end 2011. This compares with total capital requirements for market risk of Swiss franc (CHF)

For correlation trading positions, such as bespoke collateralized debt obligation (CDO) tranches sold to customers and their hedges, the CRM assesses default and migration risk of the underlying exposures. It incorporates basis risk--that is, the risk that a hedge becomes less effective--and the potential costs of resetting a hedge following a change in the underlying position, such as an amendment to the composition of an index. The CRM is subject to a floor of at least 8% of the capital charge for specific risk according to the standardized approach. This floor is generally binding, or close to binding, for the banks with the largest correlation trading portfolios. We understand that the Basel Committee carved out correlation portfolios from the IRC because assessing trading positions and their hedges separately might have overstated the underlying risks.

Of note, the Basel 2.5 measures also include higher charges for resecuritization in the banking book as well as higher charges for the specific risk on equity holdings in the trading book under the standardized approach for market risk (see table 2).

*Standard & Poor's estimates based on UBS' disclosures. Source: UBS' quarterly financial statements.

Basel 2.5 Tripled Year-End 2011 Regulatory Capital Disclosures For Large BanksThe new regulatory measures are already significantly increasing capital charges on traded risks, particularly for large international banks. The introduction of the new Basel 2.5 measures translated into a 5.2% increase in total regulatory risk-weighted assets (RWA) as of June 30, 2011, for Group 1 banks--that is, banks with Tier 1 capital above €3 billion and which are internationally active--according to a recent study by the Bank for International Settlements based on 102 banks which had already implemented Basel 2.5. The introduction of the SVaR charge accounted for more than one-third of this increase, the IRC for just less than one-quarter.

The impact on RWA will be higher for banks with large investment banking activities. We estimate that, for these banks, regulatory capital charges for market risk increased threefold with the introduction of Basel 2.5. This figure includes the impact of the additional deductions from regulatory capital, owing to lower rated securitization in the trading book.

In general, banks that included most of their trading positions in their Basel II regulatory VaR model, such as UBS, face the greatest increase in regulatory market risk RWAs. On the contrary, banks for which the scope of the VaR model was limited, and which therefore use the more stringent standardized approach for a significant part of the trading portfolio, are less affected. For example, we observe that the impact of Basel 2.5 for U.K. banks is probably more limited than for their main competitors. This is mainly because the scope of U.K. banks' regulatory VaR models reflects the U.K. Financial Services Authority's relatively cautious approach to granting model approval. Furthermore, U.K. banks' capital requirements for market risk under Basel II generally included a charge for incremental default risk, which anticipated the IRC charge. This charge, for example, was £751 million for Royal Bank of Scotland in 2010.

Our survey of 11 large international banks shows that SVaR accounted for the largest component of the Basel 2.5 charges as of year-end 2011, with close to 30% of the total (see chart 1).

It is worth noting that the VaR charge under Basel 2.5 is not directly comparable with the VaR charge under the former Basel II rules for the following reasons:

The scope of the specific risk VaR model under Basel 2.5 is not always comparable with the scope of the model under Basel II. For example, some securitization positions and their hedges may be excluded from the Basel II.5 model since specific risk is now captured by other charges; and

Some banks, including those in the U.K., already included an Incremental Default Risk (IDR) charge in the Basel II VaR model. This IDR charge has now been replaced (and complemented) by the IRC.

For several banks, the year-end 2011 impact of Basel 2.5 was lower than their guidance earlier in the year. This resulted from trading book deleveraging and derisking undertaken in the second half of 2011 in preparation for the new regulations and in response to the adverse market conditions. For example, incremental RWA resulting from Basel 2.5 was €52 billion for Deutsche Bank AG (A+/Negative/A-1) as of Dec. 31, 2011. Based on its September 2011 positions, the incremental RWA would have been 46% higher (€76 billion).

Potential Overlaps, Gaps, And Inconsistencies In Basel 2.5We support the higher capital charges introduced by Basel 2.5 because we consider that the capital requirement on market risk was too low under the Basel II regime, therefore providing an incentive for banks to hold securities in the trading book rather than the banking book. Nonetheless, we view the Basel 2.5 measures as complex and difficult to implement. Even under the Basel II VaR regime, we believe banks found it time-consuming and challenging to assess the marginal impact of a new trading position. Under Basel 2.5 this is even more so the case.

We see potential for the following overlaps and gaps in the Basel 2.5 risk measures, as well as the possibility for inconsistencies in their implementation.

In our view, the Basel 2.5 framework gives rise to potential double-counting of the same risks. This is most evident by the inclusion of both VaR and SVaR measures, which will likely generate similar results in times of high market volatility. There is also potentially some double-counting between SVaR and the IRC in the case of speculative-grade bonds or higher risk tradable loans, for which the SVaR would be akin to a default charge. Taking the example of a straightforward trading exposure, such as a long speculative-grade bond position, it appears possible that the aggregate size of the VaR, SVaR, and IRC charges might in some cases overstate the risk inherent in that particular position. In theory, the aggregate charges on the bond might even exceed its fair value, although it is questionable whether such a scenario would arise in practice. Overlaps might also arise from correlation trading positions, which in many instances are still included in the scope of the VaR model. This is because the hedges on b

While we consider that Basel 2.5 captures a broader range of market risks than the previous regulatory regime, certain risks are still not adequately assessed, in our view. In particular, this includes interest rate risk in the banking book, which is not specifically considered in Basel 2.5 or Basel III and therefore still does not attract Pillar 1 regulatory capital charges. The likely reason for this is the complexity in quantifying this risk in a consistent and meaningful way. For similar reasons, in our RAC framework we do not assign capital charges to market risk in the banking book, but instead consider it qualitatively.

Within the trading book, an example of a gap in the coverage of Basel 2.5 is the absence of a capital charge on the risk of severe adverse changes in counterparties' creditworthiness. We note, however, that this will be introduced in Basel III.

A further gap arises from the risk associated with a sudden contraction in market liquidity, which in our view is only partly captured by the one-year time horizon of the IRC. Market risk models assume that positions are constant over the holding period and can then be closed or hedged without cost. In reality, however, trading positions tend to be managed dynamically and the financial crisis illustrated that close-out and hedging costs can be significant. This risk was amplified by Lehman Brothers' default in 2008, when counterparties had to rehedge exposures at a time of severe price volatility. Furthermore, significant jumps in, or the unavailability of, market prices due to illiquidity, known as gap risk, can make valuing and hedging positions difficult. The regulatory models do not fully take this into account, in our view. As part of the consultative document, "Fundamental review of trading book," which the BIS published on May, 3. 2012, regulators suggest classifying banks' exposures into different liq

The extensive use of internal models under both the Basel II and Basel 2.5 market risk frameworks means that individual institutions might treat the same risks in different ways. The requirement for models to be validated by national regulators reduces the scope for material inconsistencies, but is unlikely to eliminate them, in our view. Under Basel 2.5, in addition to the overall characteristics of individual models--such as whether certain risks are captured within a VaR model or through specific add-ons--discrepancies might occur in the choice of the historical window for the SVaR model, in the treatment of highly rated securities in the IRC, in the use of proxies in SVaR, or in the modeling of the recovery rate for the IRC.

These overlaps, gaps, and inconsistencies emphasize to us that effective market risk management requires more tools and metrics than just regulatory-driven measures. Stress testing and scenario modeling would be prime additions, in our view. For example, two types of stress tests that have become more common since the financial crisis are liquidity-adjusted stress tests, which take into account the expected liquidity in stress conditions of different products and different sizes of trading positions, and reverse stress tests, which assess the circumstances in which a portfolio might incur a certain level of losses.

Nevertheless, although we see some drawbacks and inconsistencies within the Basel 2.5 regime, we consider that it is the best starting point for our RAC charges since it will be applied by all major investment banks once it is adopted in the U.S., and because public disclosure of market risk exposures is largely based on regulatory measures.

We welcome the elements of Basel 2.5 that call for improved reporting of market risk exposures in banks' Pillar 3 reports (which cover capital adequacy and risk management). In particular, whenever relevant, we would expect banks to disclose not only the total amount of market risk RWA under Basel 2.5, but also the regulatory RWA due to each component--that is, the VaR-based charge, SVaR charge, IRC, CRM, and regulatory charge according to the standardized approach. We would also expect banks to identify specifically the proportion of total RWAs derived from the standardized approach that is actually imputable to securitization exposures in the trading book. Some granularity regarding the external ratings of securitization exposures in the trading book (including exposures that are deducted from regulatory capital) would also be an improvement. Finally, we would consider as best practice that banks disclose the breakdown of positions included in the IRC (such as bonds and traded loans) by internal ratings ran

Further Ahead, Basel III Will Add Further Market Risk Capital ChargesBasel 2.5 will not be the last word on regulatory capital charges for traded market risk. The Basel III regime, due to come into effect from 2013, will require banks to hold more and better quality capital. It also includes new additive capital charges for credit valuation adjustment risk (CVA; an adjustment to the valuation of trades based on the creditworthiness of the counterparty), and for wrong-way risk (where the exposure to a counterparty increases while the counterparty's creditworthiness worsens). We believe that the CVA charge will have a material impact on RWAs and, in some instances, an even greater impact than the entire Basel 2.5 package. For example, Deutsche Bank quantifies incremental RWA due to Basel III at €105 billion, most of it arising from the new CVA charge, compared with additional RWA of €52 billion for the entire Basel II.5 set of measures. UBS estimated that the CVA charge itself would have added about CHF50 billion to its Basel 2.5 RWAs as of year-end 2011, but it believed that mi

The Basel Committee has recently conducted a trading book review to assess the effectiveness of the market risk framework in light of the Basel 2.5 and Basel III measures. In its consultative document, published on May, 3. 2012, the Basel Committee considers fundamental questions regarding the design of the regulatory market risk framework, such as the boundary between the trading and banking books and the relationship between internal models-based and standardized approaches, with the goal of better aligning the treatment of hedging and diversification between the two approaches. It also considers the comprehensive incorporation of the risk of market illiquidity and the possibility of replacing VaR with expected-shortfall measures to better capture tail risk.

In our view, banks may hope that future changes would also consider simplifying the complex measures introduced by Basel 2.5 and Basel III. The current framework seems more like a patchwork of additive charges, with double-counting issues and gaps not yet fully addressed, in our view. Yet history suggests that it will take several years to implement any changes that result from the review and may perhaps form part of a future Basel 3.5 or a Basel IV accord.

Standard & Poor's Ratings Services broadly welcomes Basel 2.5, the Basel Committee on Banking Supervision's regulations requiring banks to hold greater capital against the market risks they run in their trading operations. These new regulations, which are now live in most major trading centers globally except the U.S., were responsible for a threefold increase in the year-end 2011 capital charge on traded market risk among 11 European banks that we have reviewed. We believe that this adds to the pressure on investment banking returns and will encourage derisking and deleveraging of trading book activities.

We don't anticipate that the new regulations will have a systematic impact on our ratings on banks because our risk-adjusted capital (RAC) framework--our primary capital analysis tool--already applied far higher charges to banks' trading positions than the Basel II Accord required. Nevertheless, the disclosure of new information that Basel 2.5 requires could lead us to revise downward our capital and earnings assessment, which could result in rating downgrades in some isolated cases. We have today published an advance notice of a proposed criteria change explaining how we propose to adapt the RAC charges to Basel 2.5 disclosures. (Watch the related CreditMatters TV segment titled, "Basel 2.5's Impact On Investment Banking Returns," dated May 14, 2012.)

We consider the enhanced regulations as directionally consistent with the approach we take in our RAC framework and a significant step forward in addressing the deficiencies of the original Basel II framework in light of lessons learned from the financial market crisis. Building on the Basel II value-at-risk (VaR) capital charge, Basel 2.5 introduces extra charges to bolster what regulators viewed as an undercapitalized trading book. A new stressed value at risk charge uses a 12-month period of market turmoil to assess potential losses above the 99% confidence level used in the VaR model. Basel 2.5 also imposes an incremental risk charge that captures default and credit migration risk, a standardized charge for securitizations and resecuritizations, and a comprehensive risk measure for correlation trading.

Yet, although an improvement, we believe the new measures are complex, and that they open up potential for overlaps (double-counting of risks) and gaps (inadequate assessment of certain risks). We also see scope for inconsistencies in their implementation among individual banks.

The higher regulatory capital requirement under Basel 2.5, as well as further regulations in the forthcoming Basel III regime, in our view represent the main challenges to investment banks' ability to generate sustainable returns in excess of their cost of capital. It adds to pressures they are already facing, such as tighter conditions in wholesale funding markets, a structural shift away from higher return products following the financial crisis, and market uncertainties that have dampened client activity. The industry is responding by adapting its balance-sheet usage, funding model, expense base, and risk profile to the new regulatory and market context. Accordingly, we expect further restructuring and deleveraging as banks seek to optimize inventory positions, increase balance-sheet turnover, and refocus allocated capital on their competitive strengths.

Furthermore, the staggered implementation of Basel 2.5 across the world has added to the uneven playing field for global investment banks. It was introduced in Switzerland on Jan. 1, 2011, although the Bank for International Settlements (BIS) capital ratios published during 2011 by Swiss banks were still computed using Basel II rules. It came into force in the EU and other major trading centers except the U.S. on Dec. 31, 2011. We understand that Basel 2.5 implementation in the U.S. has been delayed, probably until later this year, while authorities adapt it to satisfy a Dodd-Frank Act requirement concerning the use of external credit ratings.

We believe the European banks' preparations for Basel 2.5 contributed to their trading book derisking and deleveraging in the second half of 2011 and perhaps put them at a competitive disadvantage relative to their U.S. peers. In our view, it is possible that the delayed implementation of Basel 2.5 in the U.S. might also have contributed to specific transactions, such as sales of correlation trading portfolios by some European banks to U.S. competitors. On the other hand, we see other differences and inconsistencies in national regulations that might penalize U.S. banks more than their international peers.

Basel 2.5 is a complex package of international rules that imposes higher capital charges on banks for the market risks they run in their trading books, particularly credit-related products. The Basel Committee on Banking Supervision began the process of enhancing the Basel II market risk framework in 2005, and widened the scope materially in response to the subsequent financial crisis.

A stressed value-at-risk (SVaR) model, which adds to the VaR-based capital requirements in Basel II. SVaR is intended to capture more adequately the potential consequences of more volatile market conditions than those encountered in the historical prices on which their VaR models are based.

The capital requirement generated by each of these measures adds to those of Basel II, with no possibility of reductions for risk offsets or for possible double counting.

The original Basel II market risk framework calculated banks' capital requirement according to standardized charges or the output of VaR models. These VaR models are validated by national regulators for either general risk only or both general and specific risk. They mostly estimate the probability of portfolio losses based on the statistical analysis of historical price trends and volatilities over the prior one-year period. Some banks, however, incorporate a longer time frame, such as UBS AG (A/Negative/A-1). Regulatory VaR models use a 99% confidence interval and assume a 10-day holding period.

In order to capture the potential consequences of more volatile market conditions than those encountered in the historical prices on which their VaR models are based, Basel 2.5 additionally requires banks to calculate the stressed VaR on their portfolios. These SVaR models have the same confidence interval and holding period as the VaR models, but must be based on a one-year historic dataset that would produce significant losses for the total portfolio. The volatile market conditions of 2007-2009 are an obvious starting point for banks looking to find stressed market data, although their choices will depend on the composition and positioning of their aggregate portfolio.

We consider it a weakness of the SVaR approach that the historical dataset chosen for the portfolio as a whole may not represent the most significant stress for some individual asset classes, such as commodities or sovereign bonds, especially those from the European Economic and Monetary Union (EMU or eurozone). We also consider that SVaR model results can be sensitive to the choice of proxies. For example, banks need to use proxies to model historical prices for securities that did not exist during the 2007-2009 crisis. The introduction of SVaR under Basel 2.5 should nevertheless make the regulatory market risk charge less volatile than it was under Basel II. Quarterly Basel II and Basel 2.5 risk-weighted asset (RWA) data published in 2011 by UBS supports this view (see table 1). The bank managed its market risk appetite relatively actively in this period.

This new charge aims at capturing default and migration risks, which were poorly captured, in our view, in specific risk VaR models. VaR models better capture potential losses due to credit spread variations at unchanged credit rating levels. Typical positions included in the scope of the incremental risk charge (IRC) model are bonds, credit default swaps, and traded loans. The scope excludes securitization positions. The IRC is measured with a one-year holding period and 99.9% confidence interval. We see these parameters as a clear improvement over the 10-day holding period and 99% confidence interval of regulatory VaR models.

Modeling of default and migration risks in the trading book has parallels with internal rating-based modeling of credit risk in the banking book and therefore presents similar challenges, such as how to analyze highly rated securities with little or no history of losses. In theory, banks could differentiate between the liquidity horizon (the time to liquidate the positions, if needed, with a regulatory "floor" of three months) and the capital horizon (which is one year). For positions with a liquidity horizon lower than one year, the IRC assumes that, when liquidated, each position is replaced with a position bearing the same level of risk as the initial one. In practice, however, we note that a majority of banks have chosen to use a liquidity horizon of one year for all positions. We observe that about 70%-80% of the IRC charge reflects the modeling of default whereas the residual stems from credit migration risk: the downgrade of a bond, for example, being associated in general with higher credit spreads an

Securitization, resecuritization, and nth-to-default credit derivative positions in the trading book are excluded from the IRC and subjected instead to different approaches. With the exception of positions held in correlation trading portfolios, which are the subject of the CRM charge described below, securitization tranches receive banking book capital charges and there are higher risk weights for resecuritizations. Lower rated positions must be deducted from regulatory capital, 50% from Core Tier 1 capital and 50% from Tier 2. We observe that the Basel II VaR charge on these positions was generally low and the effect of these changes is to increase the capital requirement for securitizations and resecuritizations substantially. As an example, because of the new Basel 2.5 rules, Credit Suisse deducted an additional CHF2.37 billion ($2.5 billion) of lower rated securitization positions from regulatory capital at year-end 2011. This compares with total capital requirements for market risk of Swiss franc (CHF)

For correlation trading positions, such as bespoke collateralized debt obligation (CDO) tranches sold to customers and their hedges, the CRM assesses default and migration risk of the underlying exposures. It incorporates basis risk--that is, the risk that a hedge becomes less effective--and the potential costs of resetting a hedge following a change in the underlying position, such as an amendment to the composition of an index. The CRM is subject to a floor of at least 8% of the capital charge for specific risk according to the standardized approach. This floor is generally binding, or close to binding, for the banks with the largest correlation trading portfolios. We understand that the Basel Committee carved out correlation portfolios from the IRC because assessing trading positions and their hedges separately might have overstated the underlying risks.

Of note, the Basel 2.5 measures also include higher charges for resecuritization in the banking book as well as higher charges for the specific risk on equity holdings in the trading book under the standardized approach for market risk (see table 2).

The new regulatory measures are already significantly increasing capital charges on traded risks, particularly for large international banks. The introduction of the new Basel 2.5 measures translated into a 5.2% increase in total regulatory risk-weighted assets (RWA) as of June 30, 2011, for Group 1 banks--that is, banks with Tier 1 capital above €3 billion and which are internationally active--according to a recent study by the Bank for International Settlements based on 102 banks which had already implemented Basel 2.5. The introduction of the SVaR charge accounted for more than one-third of this increase, the IRC for just less than one-quarter.

The impact on RWA will be higher for banks with large investment banking activities. We estimate that, for these banks, regulatory capital charges for market risk increased threefold with the introduction of Basel 2.5. This figure includes the impact of the additional deductions from regulatory capital, owing to lower rated securitization in the trading book.

In general, banks that included most of their trading positions in their Basel II regulatory VaR model, such as UBS, face the greatest increase in regulatory market risk RWAs. On the contrary, banks for which the scope of the VaR model was limited, and which therefore use the more stringent standardized approach for a significant part of the trading portfolio, are less affected. For example, we observe that the impact of Basel 2.5 for U.K. banks is probably more limited than for their main competitors. This is mainly because the scope of U.K. banks' regulatory VaR models reflects the U.K. Financial Services Authority's relatively cautious approach to granting model approval. Furthermore, U.K. banks' capital requirements for market risk under Basel II generally included a charge for incremental default risk, which anticipated the IRC charge. This charge, for example, was £751 million for Royal Bank of Scotland in 2010.

Our survey of 11 large international banks shows that SVaR accounted for the largest component of the Basel 2.5 charges as of year-end 2011, with close to 30% of the total (see chart 1).

The scope of the specific risk VaR model under Basel 2.5 is not always comparable with the scope of the model under Basel II. For example, some securitization positions and their hedges may be excluded from the Basel II.5 model since specific risk is now captured by other charges; and

Some banks, including those in the U.K., already included an Incremental Default Risk (IDR) charge in the Basel II VaR model. This IDR charge has now been replaced (and complemented) by the IRC.

For several banks, the year-end 2011 impact of Basel 2.5 was lower than their guidance earlier in the year. This resulted from trading book deleveraging and derisking undertaken in the second half of 2011 in preparation for the new regulations and in response to the adverse market conditions. For example, incremental RWA resulting from Basel 2.5 was €52 billion for Deutsche Bank AG (A+/Negative/A-1) as of Dec. 31, 2011. Based on its September 2011 positions, the incremental RWA would have been 46% higher (€76 billion).

We support the higher capital charges introduced by Basel 2.5 because we consider that the capital requirement on market risk was too low under the Basel II regime, therefore providing an incentive for banks to hold securities in the trading book rather than the banking book. Nonetheless, we view the Basel 2.5 measures as complex and difficult to implement. Even under the Basel II VaR regime, we believe banks found it time-consuming and challenging to assess the marginal impact of a new trading position. Under Basel 2.5 this is even more so the case.

In our view, the Basel 2.5 framework gives rise to potential double-counting of the same risks. This is most evident by the inclusion of both VaR and SVaR measures, which will likely generate similar results in times of high market volatility. There is also potentially some double-counting between SVaR and the IRC in the case of speculative-grade bonds or higher risk tradable loans, for which the SVaR would be akin to a default charge. Taking the example of a straightforward trading exposure, such as a long speculative-grade bond position, it appears possible that the aggregate size of the VaR, SVaR, and IRC charges might in some cases overstate the risk inherent in that particular position. In theory, the aggregate charges on the bond might even exceed its fair value, although it is questionable whether such a scenario would arise in practice. Overlaps might also arise from correlation trading positions, which in many instances are still included in the scope of the VaR model. This is because the hedges on b

While we consider that Basel 2.5 captures a broader range of market risks than the previous regulatory regime, certain risks are still not adequately assessed, in our view. In particular, this includes interest rate risk in the banking book, which is not specifically considered in Basel 2.5 or Basel III and therefore still does not attract Pillar 1 regulatory capital charges. The likely reason for this is the complexity in quantifying this risk in a consistent and meaningful way. For similar reasons, in our RAC framework we do not assign capital charges to market risk in the banking book, but instead consider it qualitatively.

Within the trading book, an example of a gap in the coverage of Basel 2.5 is the absence of a capital charge on the risk of severe adverse changes in counterparties' creditworthiness. We note, however, that this will be introduced in Basel III.

A further gap arises from the risk associated with a sudden contraction in market liquidity, which in our view is only partly captured by the one-year time horizon of the IRC. Market risk models assume that positions are constant over the holding period and can then be closed or hedged without cost. In reality, however, trading positions tend to be managed dynamically and the financial crisis illustrated that close-out and hedging costs can be significant. This risk was amplified by Lehman Brothers' default in 2008, when counterparties had to rehedge exposures at a time of severe price volatility. Furthermore, significant jumps in, or the unavailability of, market prices due to illiquidity, known as gap risk, can make valuing and hedging positions difficult. The regulatory models do not fully take this into account, in our view. As part of the consultative document, "Fundamental review of trading book," which the BIS published on May, 3. 2012, regulators suggest classifying banks' exposures into different liq

The extensive use of internal models under both the Basel II and Basel 2.5 market risk frameworks means that individual institutions might treat the same risks in different ways. The requirement for models to be validated by national regulators reduces the scope for material inconsistencies, but is unlikely to eliminate them, in our view. Under Basel 2.5, in addition to the overall characteristics of individual models--such as whether certain risks are captured within a VaR model or through specific add-ons--discrepancies might occur in the choice of the historical window for the SVaR model, in the treatment of highly rated securities in the IRC, in the use of proxies in SVaR, or in the modeling of the recovery rate for the IRC.

These overlaps, gaps, and inconsistencies emphasize to us that effective market risk management requires more tools and metrics than just regulatory-driven measures. Stress testing and scenario modeling would be prime additions, in our view. For example, two types of stress tests that have become more common since the financial crisis are liquidity-adjusted stress tests, which take into account the expected liquidity in stress conditions of different products and different sizes of trading positions, and reverse stress tests, which assess the circumstances in which a portfolio might incur a certain level of losses.

Nevertheless, although we see some drawbacks and inconsistencies within the Basel 2.5 regime, we consider that it is the best starting point for our RAC charges since it will be applied by all major investment banks once it is adopted in the U.S., and because public disclosure of market risk exposures is largely based on regulatory measures.

We welcome the elements of Basel 2.5 that call for improved reporting of market risk exposures in banks' Pillar 3 reports (which cover capital adequacy and risk management). In particular, whenever relevant, we would expect banks to disclose not only the total amount of market risk RWA under Basel 2.5, but also the regulatory RWA due to each component--that is, the VaR-based charge, SVaR charge, IRC, CRM, and regulatory charge according to the standardized approach. We would also expect banks to identify specifically the proportion of total RWAs derived from the standardized approach that is actually imputable to securitization exposures in the trading book. Some granularity regarding the external ratings of securitization exposures in the trading book (including exposures that are deducted from regulatory capital) would also be an improvement. Finally, we would consider as best practice that banks disclose the breakdown of positions included in the IRC (such as bonds and traded loans) by internal ratings ran

Basel 2.5 will not be the last word on regulatory capital charges for traded market risk. The Basel III regime, due to come into effect from 2013, will require banks to hold more and better quality capital. It also includes new additive capital charges for credit valuation adjustment risk (CVA; an adjustment to the valuation of trades based on the creditworthiness of the counterparty), and for wrong-way risk (where the exposure to a counterparty increases while the counterparty's creditworthiness worsens). We believe that the CVA charge will have a material impact on RWAs and, in some instances, an even greater impact than the entire Basel 2.5 package. For example, Deutsche Bank quantifies incremental RWA due to Basel III at €105 billion, most of it arising from the new CVA charge, compared with additional RWA of €52 billion for the entire Basel II.5 set of measures. UBS estimated that the CVA charge itself would have added about CHF50 billion to its Basel 2.5 RWAs as of year-end 2011, but it believed that mi

The Basel Committee has recently conducted a trading book review to assess the effectiveness of the market risk framework in light of the Basel 2.5 and Basel III measures. In its consultative document, published on May, 3. 2012, the Basel Committee considers fundamental questions regarding the design of the regulatory market risk framework, such as the boundary between the trading and banking books and the relationship between internal models-based and standardized approaches, with the goal of better aligning the treatment of hedging and diversification between the two approaches. It also considers the comprehensive incorporation of the risk of market illiquidity and the possibility of replacing VaR with expected-shortfall measures to better capture tail risk.

In our view, banks may hope that future changes would also consider simplifying the complex measures introduced by Basel 2.5 and Basel III. The current framework seems more like a patchwork of additive charges, with double-counting issues and gaps not yet fully addressed, in our view. Yet history suggests that it will take several years to implement any changes that result from the review and may perhaps form part of a future Basel 3.5 or a Basel IV accord.

Standard & Poor's Ratings Services broadly welcomes Basel 2.5, the Basel Committee on Banking Supervision's regulations requiring banks to hold greater capital against the market risks they run in their trading operations. These new regulations, which are now live in most major trading centers globally except the U.S., were responsible for a threefold increase in the year-end 2011 capital charge on traded market risk among 11 European banks that we have reviewed. We believe that this adds to the pressure on investment banking returns and will encourage derisking and deleveraging of trading book activities.

We don't anticipate that the new regulations will have a systematic impact on our ratings on banks because our risk-adjusted capital (RAC) framework--our primary capital analysis tool--already applied far higher charges to banks' trading positions than the Basel II Accord required. Nevertheless, the disclosure of new information that Basel 2.5 requires could lead us to revise downward our capital and earnings assessment, which could result in rating downgrades in some isolated cases. We have today published an advance notice of a proposed criteria change explaining how we propose to adapt the RAC charges to Basel 2.5 disclosures. (Watch the related CreditMatters TV segment titled, "Basel 2.5's Impact On Investment Banking Returns," dated May 14, 2012.)

We consider the enhanced regulations as directionally consistent with the approach we take in our RAC framework and a significant step forward in addressing the deficiencies of the original Basel II framework in light of lessons learned from the financial market crisis. Building on the Basel II value-at-risk (VaR) capital charge, Basel 2.5 introduces extra charges to bolster what regulators viewed as an undercapitalized trading book. A new stressed value at risk charge uses a 12-month period of market turmoil to assess potential losses above the 99% confidence level used in the VaR model. Basel 2.5 also imposes an incremental risk charge that captures default and credit migration risk, a standardized charge for securitizations and resecuritizations, and a comprehensive risk measure for correlation trading.

Yet, although an improvement, we believe the new measures are complex, and that they open up potential for overlaps (double-counting of risks) and gaps (inadequate assessment of certain risks). We also see scope for inconsistencies in their implementation among individual banks.