17

Border adjustment regulations in the Danish Gravel tax Senior manager Tor Christensen The Danish Ministry of Taxation (Skatteministeriet)

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | neil-james-moore |

| View: | 217 times |

| Download: | 0 times |

Border adjustment regulations in the Danish Gravel tax

Senior manager Tor ChristensenThe Danish Ministry of Taxation (Skatteministeriet)

18-04-23Side 2

The purpose of border adjustment regulations

• In order to ensure that domestically and imported raw materials are treated equally, so that competition is undisturbed.

• In order to ensure that exported resources are untaxed, to ensure that exports are unaffected.

• But also to take account for the EU-treaty and other international treaties, which ensure the free movement of goods.

18-04-23Side 3

Registered enterprises – Extraction and import

• All raw materials found in Denmark are taxed – see law annex 1. All similar imported raw materials are also taxed – see law annex 2.

• Companies which extract or import taxed raw materials have to be registered according to the law. The tax has to be paid of the amount of raw materials, which has been handed out from the company in the tax period.

• Registered enterprises are entitled to receive taxable raw materials from other registered enterprises without the tax being paid. The same applies to import.

18-04-23Side 4

Export – registered enterprises

• In the statement of the taxable quantity of raw materials the registered enterprises can deduct the quantity of taxable raw materials that is exported.

• As documentation for the export the registered company has to present:

a) A copy of the invoice regarding the exported raw materials, and

b) Written purchase order, correspondence with the buyer, bank statement etc.

18-04-23Side 5

Export – non registered enterprises

• Suppose a Danish enterprise produce tiles and use taxable raw materials, e.g. clay, from a registered enterprise in Denmark. The clay will be taxed when it is used for the production of tiles. If the tiles afterwards are exported there is a need for the possibility of reimbursement.

• Therefore in the case of commercial export of raw materials which have undergone simple or more extensive processing the customs and tax administration shall reimburse the tax paid if the annual reimbursement is at least DKK 500. The statement shall be carried out in the aggregate once a year to keep the administrative costs down.

• The exporting company have to present documentation regarding the amount of raw materials used form the production enterprise, e.g. the tile producer if the exporting company is different from the producer.

18-04-23Side 6

Special regulations regarding cement

• The tax on Danish-produced cement manufactured from raw materials listed in Annex 1 is DKK 5 per m3 of the raw material, if the producer can document the quantity of raw materials used in the manufacturing process. If no such documentation exists, tax shall be paid in accordance with the conversion factors quoted in Annex 2.

• The tax on imported cement referred to in Annex 2 is also DKK 5 per m3 and is paid in accordance with the conversion factors quoted in Annex 1, if the importer can document the quantity of raw materials used in the manufacturing process. If no such documentation exists, tax shall be paid in accordance with the conversion factors quoted in Annex 2.

18-04-23Side 7

Example 1 – import of 1000 t. of cement

Case 1: Suppose the importer can document that there has been used 571.4 tonnes of chalk and 1000 tonnes of sand to produce the 1000 tonnes of cement. Then he can use the conversion factors in annex 1, which is 0,7 and 0.6, so that 400 m3 of chalk and 600 m3 sand has been used to produce the cement and the total tax payment will thereby be 5000 DKK.

Case 2: Suppose that the importer cannot document the amount of raw materials used to produce the cement. Then annex 2 apply and the version factor will be 1,1 so that the 1000 tonnes correspond to 1100 m3 and the total tax payment will be

5.500 DKK.

18-04-23Side 8

Example 2 – export of 1000 t. of cement

Case 1: Suppose the producer can document that there has been used 571.4 tonnes of chalk and 1000 tonnes of sand to produce the 1000 tonnes of cement.

Then he can use the conversion factors in annex 1 which 0,7 and 0.6, so that 400 m3 of chalk and 600 m3 sand has been used to produce the cement and the total amount he have exported is 1000 m3 which he can deduct in the taxable

quantity.

Case 2: Suppose that the producer cannot document the amount of raw materials used to produce the cement. Then annex 2 apply and the conversion factor will be 1,1 so that the 1000 tonnes correspond to 1100 m3 and this he can deduct in the

taxable quantity.

18-04-23Side 9

Example 3 – export of tiles

Suppose that there has been used 5000 tonnes of clay to produce the exported amount of tiles. Then the taxable amount of clay will be 3000 m3 (5000x0.6) and the tax paid on the clay will amount to 15000 DKK, so that the exporter will get this amount reimbursed.

18-04-23Side 10

Use of border adjustment regulations in general

• As in the case with the gravel tax but in addition there will also be a so calledcover tax “dækningsafgift” on imports. Such a tax is not present in the gravel tax, so e.g. imported tiles are untaxed. However, in this case the distortion is minor as imports of this kind of products are small in Denmark.

• But it is used in other excise taxes e.g. the tax on fertilizer.

Annex 1

18-04-23Side 11

List of taxable raw materials with associated conversion factors Bentonite 1 t = 0.6 m3 Lignite 1 t = 1.4 m3 Expanding clay 1 t = 0.6 m3 Flint 1 t = 0.6 m3 Granite (crushed and broken) 1 t = 0.6 m3 Granite (paving stones, kerbstones, blocks and the like) 1 t = 0.4 m3 Gravel 1 t = 0.6 m3 Fireclay 1 t = 0.6 m3 Soil (filling soil, raw soil) 1 t = 0.6 m3 Lime 1 t = 0.7 m3 Lime filler and feed clay 1 t = 1.0 m3 Limestone 1 t = 0.6 m3 Kaolin 1 t = 0.6 m3 Source lime, bog lime and sea lime 1 t = 0.8 m3 Kieselguhr (diatomaceous earth), finished products 1 t = 2.5 m3 Adhesive clay 1 t = 1.0 m3 Chalk 1 t = 0.7 m3

Annex 1 - continued

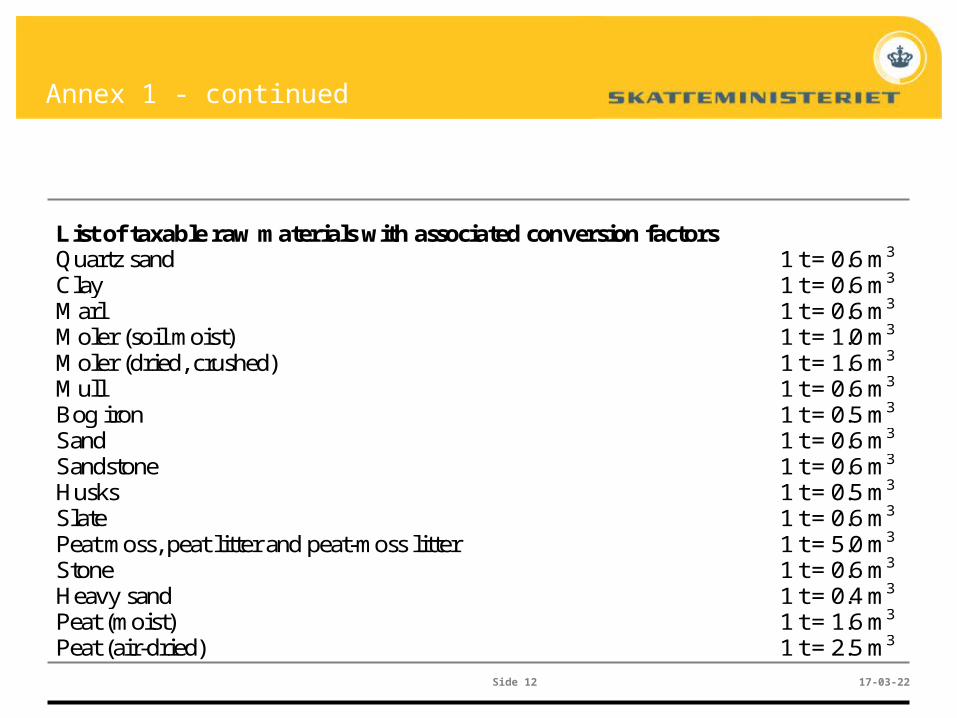

18-04-23Side 12

List of taxable raw materials with associated conversion factors Quartz sand 1 t = 0.6 m3 Clay 1 t = 0.6 m3 Marl 1 t = 0.6 m3 Moler (soil moist) 1 t = 1.0 m3 Moler (dried, crushed) 1 t = 1.6 m3 Mull 1 t = 0.6 m3 Bog iron 1 t = 0.5 m3 Sand 1 t = 0.6 m3 Sandstone 1 t = 0.6 m3 Husks 1 t = 0.5 m3 Slate 1 t = 0.6 m3 Peat moss, peat litter and peat-moss litter 1 t = 5.0 m3 Stone 1 t = 0.6 m3 Heavy sand 1 t = 0.4 m3 Peat (moist) 1 t = 1.6 m3 Peat (air-dried) 1 t = 2.5 m3

Annex 2

18-04-23Side 13

List of imported raw materials covered by the raw material tax, with associated conversion factors

25.05 Natural sand of any kind, including coloured, with the exception of metal-containing sand belonging under Chapter 26 (ores, slag and ash):

-2505.10.00 Quartz sand 1 t = 0.6 m3 -2505.90.00 Other natural sand types (e.g. sea sand, pit sand, etc.) 1 t = 0.6 m3 25.08 Clay types (with the exception of expanded clay belonging under item 6806), andalusite, cyanite

and sillimanite, including where baked; mullite; chamotte and dinasles: Bentonite -2508.10.00 Bentonite 1 t = 0.6 m3 Other clay types (e.g. brick clays and similar clay types), apart from

kaolin, bentonite, bleaching earth and fuller’s earth, fireclay:

-2508.40.00 All products 1 t = 0.6 m3 25.09 Chalk -2509.00.00 All products 1 t = 0.7 m3 25.21

Annex 2 - continued

18-04-23Side 14

List of imported raw materials covered by the raw material tax, with associated conversion factors

25.12 Fossil siliceous meal (e.g. kieselguhr, tripoli powder and diatomaceous earth) and similar siliceous soil types, with an apparent density of 1000 kg/m3 or less, also baked:

E.g. 2512.00.00: – moler (soil moist) 1 t = 1.0 m3 – moler (dried, crushed) 1 t = 1.6 m3 25.16 Granite, porphyry, basalt, sandstone and other monument or building stone, including coarse-

shaped or only cut, by sawing or in some other way, into blocks or slabs of square or rectangular form:

Granite: -2516.11.00 Raw or coarse-shaped 1 t = 0.4 m3 -2516.12.10 Only cut, by sawing or in some other way, into

blocks or slabs of square or rectangular form – with a thickness of 25 cm and less 1 t = 0.4 m3

-2516.12.90 Shaped in some other way 1 t = 0.4 m3 Sandstone: -2516.21.00 Raw or coarse-shaped 1 t = 0.4 m3 -2516.22.10 Only cut, by sawing or in some other way, into

blocks or slabs of square or rectangular form – with a thickness of 25 cm and less 1 t = 0.4 m3

-2516.22.90 Shaped in some other way 1 t = 0.4 m3

Annex 2 - continued

18-04-23Side 15

List of imported raw materials covered by the raw material tax, with associated conversion factors

25.17 Broken stone, gravel and crushed stone, of the type generally used in concrete, for road and railway building and the like, and shingle and flint, including heat-treated; tar macadam; granules, chips and powder of stone types belonging under item 2515 (travertine, ecaussine and other monument or building limestone with an apparent density of 2,500 kg/m3 or more and alabaster) or 2516 (sandstone), including heat-treated (aggregates, etc.):

-2517.10.10 Broken stone, gravel, shingle and flint 1 t = 0.6 m3 -2517.10.20 Crushed dolomite and crushed limestone 1 t = 0.6 m3 -2517.10.80 Other products of a similar nature (e.g. crushed

granite) 1 t = 0.6 m3 -2517.30.00 Tar macadam 1 t = 0.6 m3 -2517.49.00 Granules, chips and powder of stone types belonging

under item 2515 or 2516, also heat-treated: (apart from marble) 1 t = 0.6 m3

25.18 Dolomite, also baked or sintered, including dolomite, coarse-shaped or only cut, by sawing or in

some other way, into blocks or slabs of square or rectangular form; tamped mixture of dolomite: -2518.10.00 Dolomite; not baked or sintered 1 t = 0.7 m3 -2518.20.00 Baked or sintered dolomite 1 t = 0.7 m3 -2518.30.00 Tamped mixture of dolomite 1 t = 0.7 m3

Annex 2 - continued

18-04-23Side 16

List of imported raw materials covered by the raw material tax, with associated conversion factors

25.23 Portland cement, aluminate cement, slag cement and similar hydraulic cement, also coloured or in the form of clinker:

-2523.10.00 Cement clinker 1 t = 1.1 m3 -2523.21.00 Portland cement: white or artificially coloured 1 t = 1.1 m3 -2523.29.00 Portland cement, other products 1 t = 1.1 m3 -2523.30.00 Aluminate cement 1 t = 1.1 m3 -2523.90.10 Slag cement 1 t = 1.1 m3 -2523.90.30 Puzzolan cement 1 t = 1.1 m3 -2523.90.90 Other hydraulic cement 1 t = 1.1 m3 27.03 Peat and peat briquettes and also peat litter and peat-moss litter, also agglomerated: -2703.00.00 All products 1 t = 5.0 m3 68.01 Cobblestones, kerb stone and flagstones of natural stone types (with the exception of slate) -6801.00.00 All products 1 t = 0.4 m

Annex 2 - continued

18-04-23Side 17

List of imported raw materials covered by the raw material tax, with associated conversion factors

25.19 Natural magnesium carbonate (magnesite); melted magnesia; dead-burnt (sintered) magnesia, including with a content of small quantities of other oxides added before the sintering process; other magnesium oxide, including pure:

-2519.10.00 Natural magnesium carbonate (magnesite) 1 t = 0.7 m3 -2519.90 Other products: -2519.90.10 Magnesium oxide, with the exception of burnt natural

magnesium carbonate 1 t = 0.7 m3 -2519.90.30 Dead-burnt (sintered) magnesia 1 t = 0.7 m3 -2519.90.90 Other products 1 t = 0.7 m3 25.21 Limestone, of the type used in the manufacture of lime or cement or in metallurgy as fluxing agent

(lime, cement or metal manufacture): -2521.00.00 All products 1 t = 0.6 m3 25.22 Baked lime, slaked lime and hydraulic lime, with the exception of calcium dioxide and calcium

hydroxide belonging under item 2825: -2522.10.00 Baked lime 1 t = 1.6 m3 -2522.20.00 Slaked lime 1 t = 1.3 m3 -2522.30.00 Hydraulic lime 1 t = 1.2 m3