15

Borsa Italiana market for open-end funds Borsa Italiana Page 1

Borsa Italiana market for open-end funds

Borsa ItalianaPage 1

A new market for open-end fund trading

Objective: creating a new electronic market where investors can buy and sell open-end funds

�New segment of Borsa Italiana’s ETFplus market dedicated to open-end funds

Intermediaries already admitted to ETFplus market will have access to open-end funds brought to the market

by issuers.

�NAV of the relevant trading day is the trading price

No arbitrage between buy or sell on the market and to be created or redeemed directly with the issuer.

�Order imbalance (buy or sell) will be executed by the Appointed Intermediary (A.I.)

The presence of the A.I. is mandatory in order execute the buy or sell order imbalance.

�Straight through processing from listing to settlement of dematerialized open-end funds

Dematerialized shares/units will be settled in Monte Titoli at T+3, as for all other financial instruments listed in

Borsa Italiana

The Italian market model is developed with focus on the following points:

Fund’s issuer is the leading actor, it:

�submits the listing application;

�calculates and sends the NAV to Borsa Italiana;

�appoints the Appointed Intermediary;

� processes daily creation/redemption.

Maximum investor’s safeguard:

�Trading at NAV;

�Regulated and supervised official market;

�Borsa Italiana is the main Italian HUB for financial information and data.

The new market for open-end funds - pros

Main features:

�New market segment of ETFplus market

�Trading model: auction call from 8:00 a.m. to 3:00 p.m.

�Not cleared market segment (no central counterparty)

�Orders must display the quantity only (no price to be inserted, i.e. market orders)*

�Minimum trading lot is 1 share/unit (no decimals available)

�The NAV of the relevant trading day is the trading price

�Order imbalance will be executed by the Appointed Intermediary

�All the intermediaries already admitted to ETFplus market will be able to trade on this new segment

* The trading platform shows a «conventional price» of 1€

The new market for open-end funds - details

• A segment of the ETFplus market, the open-end CIU segment, will be devoted to these instruments.

• There will be admission requirements for open-end CIUs and ongoing disclosure obligations, includingthe obligation to notify the net asset value (NAV) of the share/unit.

• The open-end CIUs will be traded through entry on the book of market orders. Buy and sell orders willbe matched taking account of the time priorities of the individual orders until the quantities availableare filled.

• For each trading day an intermediary appointed for the purpose will undertake to enter bids and offersfor a quantity equal to the difference between the buy and sell quantities on the book.

• In the last five minutes of trading market, intermediaries other than the one appointed must refrainfrom entering, cancelling and modifying orders.

• Contracts will be concluded on the basis of the NAV of the share/unit of the open-end CIU on thetrading day of reference and notified by the issuer.

• Contracts will be sent for settlement via X-TRM on the day following their conclusion and in any casein time for settlement on the third day following their conclusion.

• Trading will not take place on days when the net asset value (NAV) of the share/unit is not calculated.

• The transparency of the trading for intermediaries and the public will be ensured by the usualchannels. Disclosures will include the conventional price while the data on the contracts concluded,updated with the prices at which they were concluded (NAV), will be provided in the Official List on theday following their conclusion.

The new market for open-end funds - details

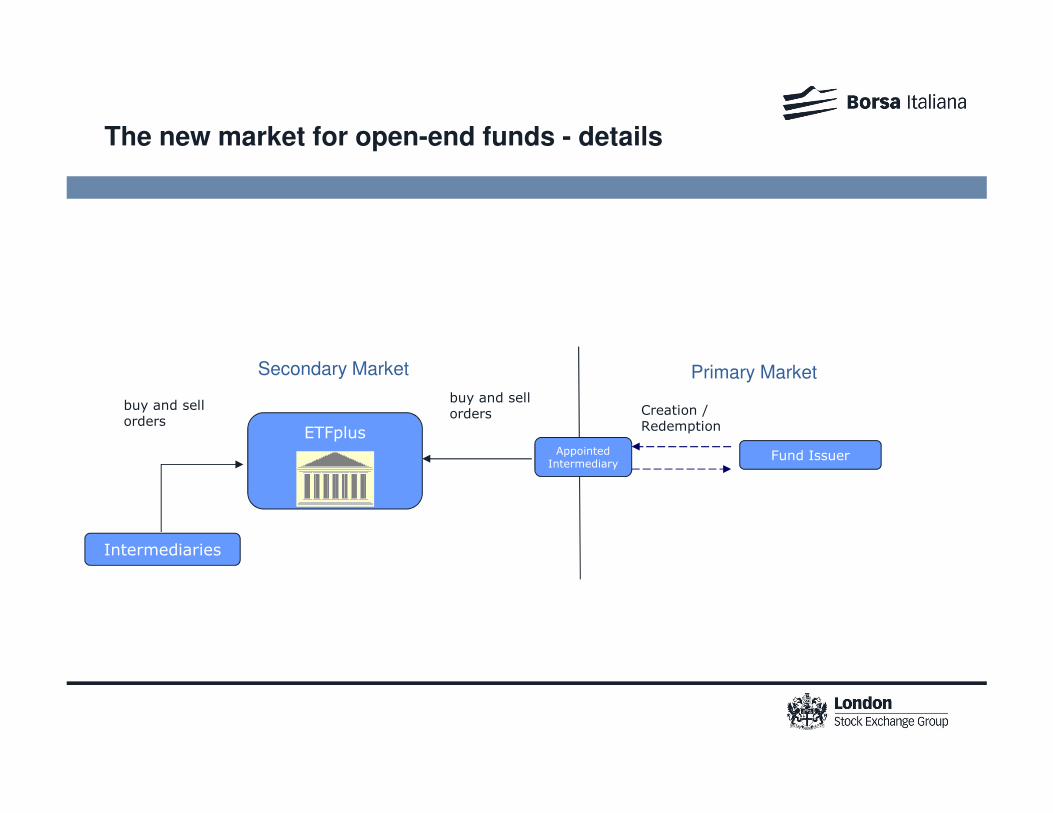

ETFplus

Fund IssuerAppointed Intermediary

Intermediaries

buy and sell orders

Creation / Redemption

Secondary Market Primary Market

buy and sell orders

The new market for open-end funds - details

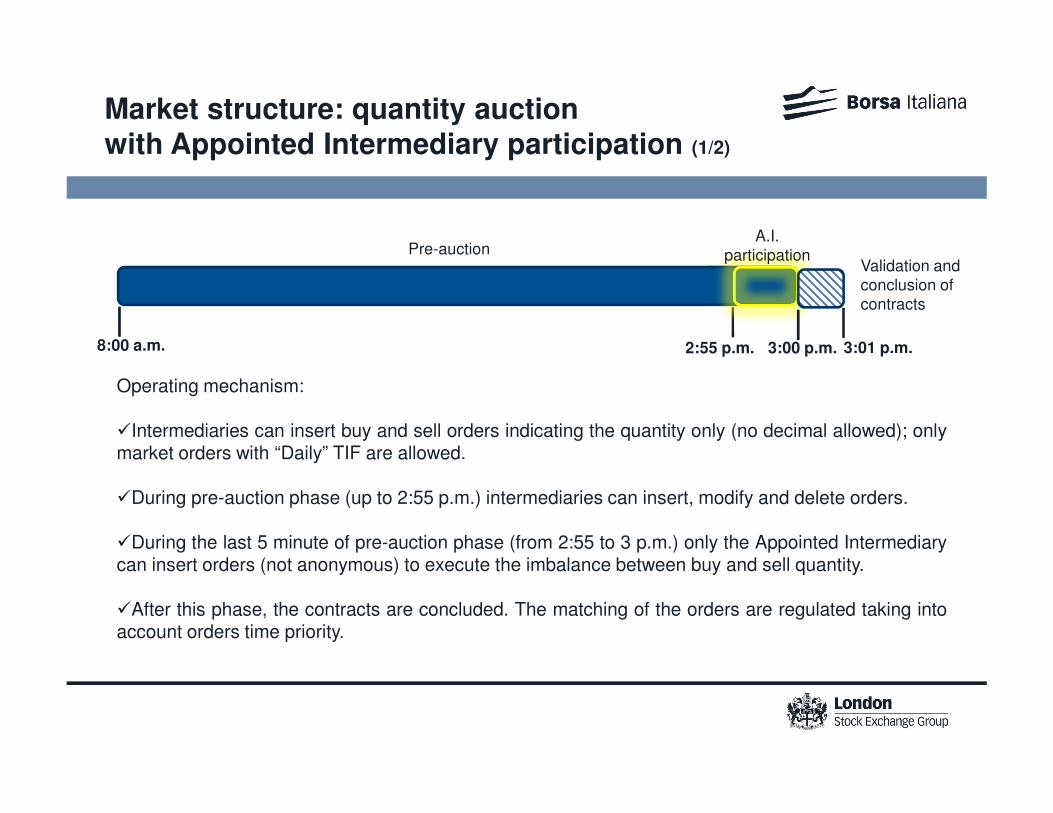

Market structure: quantity auction

with Appointed Intermediary participation (1/2)

Operating mechanism:

�Intermediaries can insert buy and sell orders indicating the quantity only (no decimal allowed); onlymarket orders with “Daily” TIF are allowed.

�During pre-auction phase (up to 2:55 p.m.) intermediaries can insert, modify and delete orders.

�During the last 5 minute of pre-auction phase (from 2:55 to 3 p.m.) only the Appointed Intermediarycan insert orders (not anonymous) to execute the imbalance between buy and sell quantity.

�After this phase, the contracts are concluded. The matching of the orders are regulated taking intoaccount orders time priority.

8:00 a.m. 2:55 p.m.

Pre-auctionA.I.

participation Validation and conclusion of contracts

3:00 p.m. 3:01 p.m.

Bid Ask10000

1000

500

5000

1000

Pre-auction phase: all intermediaries can insert, modify and delete orders for quantity.

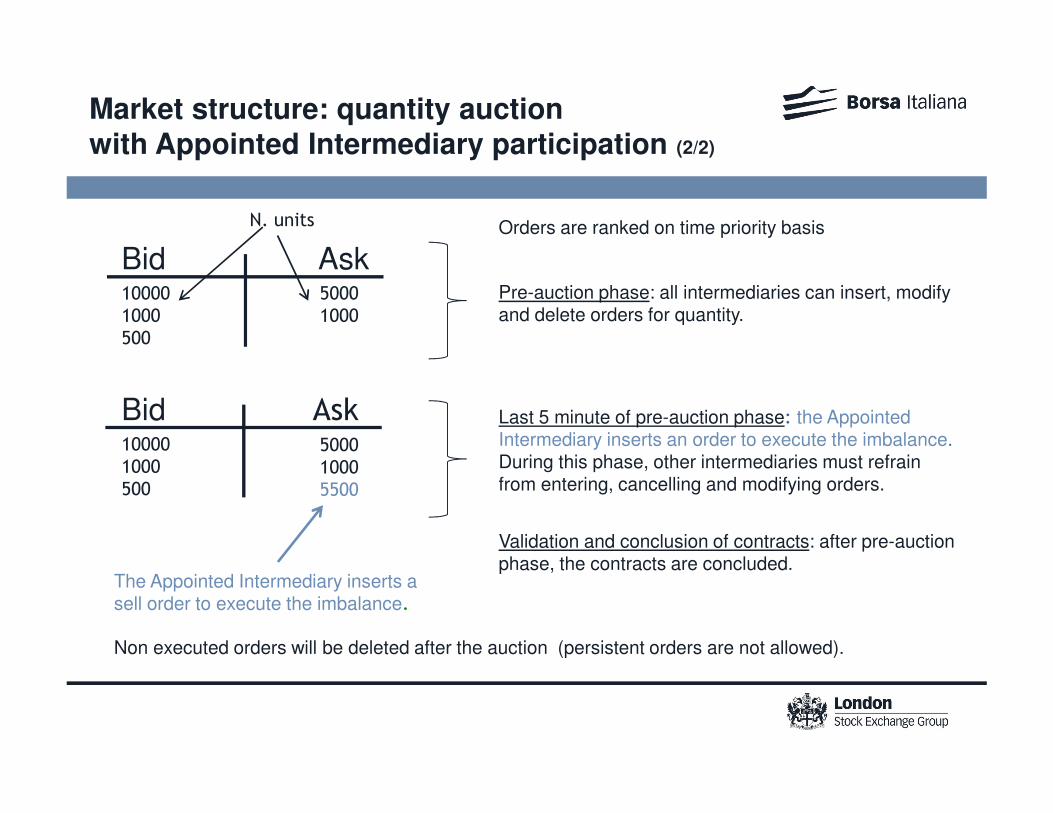

Bid Ask

10000

1000

500

5000

1000

5500

Last 5 minute of pre-auction phase: the Appointed Intermediary inserts an order to execute the imbalance.During this phase, other intermediaries must refrain from entering, cancelling and modifying orders.

Validation and conclusion of contracts: after pre-auction phase, the contracts are concluded.

The Appointed Intermediary inserts a sell order to execute the imbalance.

N. units

Non executed orders will be deleted after the auction (persistent orders are not allowed).

Market structure: quantity auction

with Appointed Intermediary participation (2/2)

Orders are ranked on time priority basis

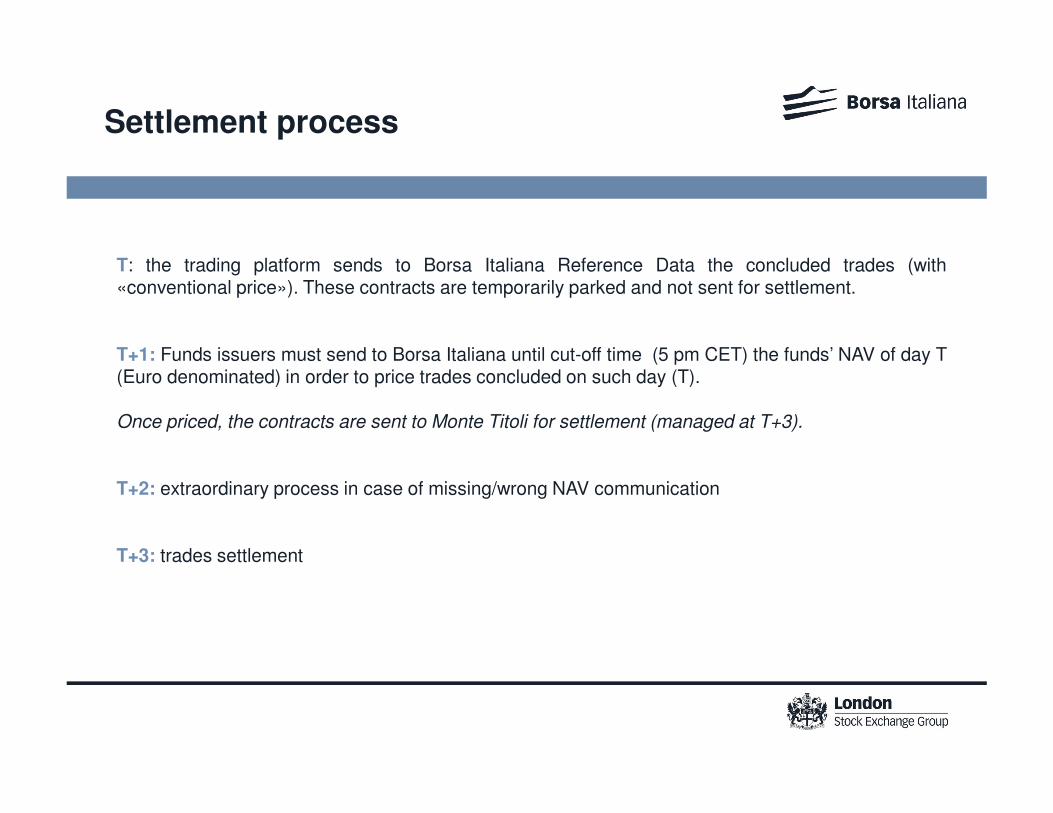

T: the trading platform sends to Borsa Italiana Reference Data the concluded trades (with«conventional price»). These contracts are temporarily parked and not sent for settlement.

T+1: Funds issuers must send to Borsa Italiana until cut-off time (5 pm CET) the funds’ NAV of day T(Euro denominated) in order to price trades concluded on such day (T).

Once priced, the contracts are sent to Monte Titoli for settlement (managed at T+3).

T+2: extraordinary process in case of missing/wrong NAV communication

T+3: trades settlement

Settlement process

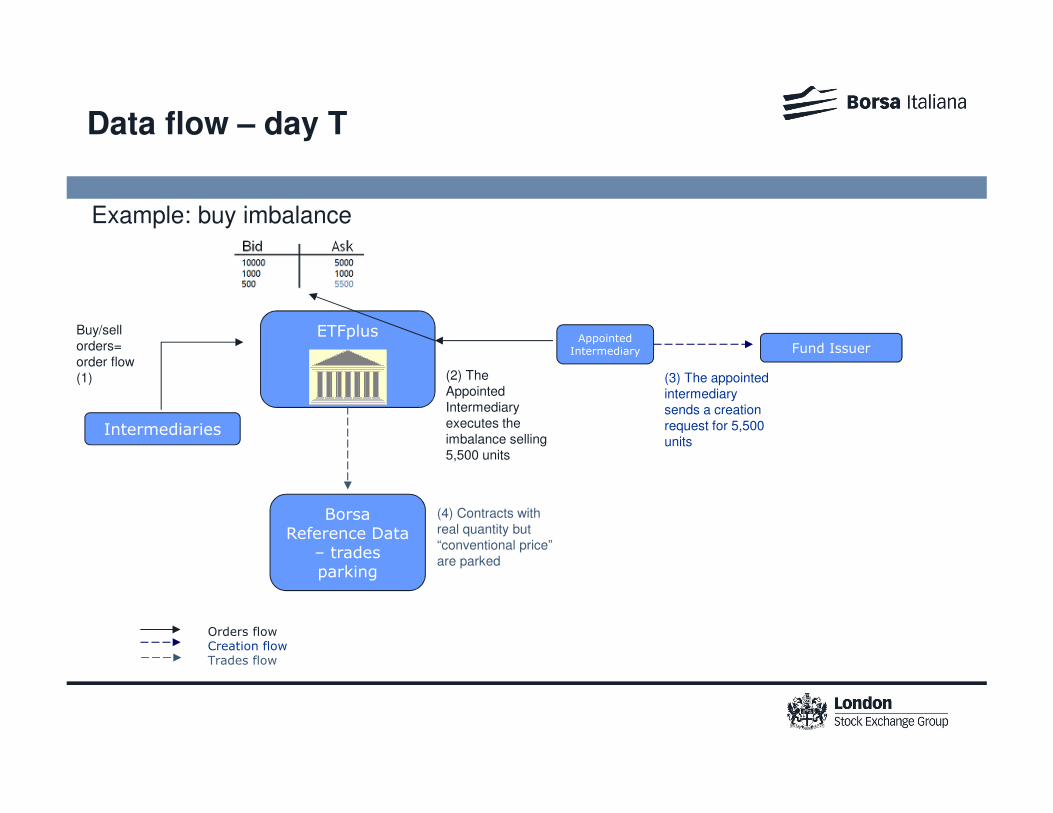

Buy/sell

orders=

order flow

(1) (2) The

Appointed

Intermediary

executes the

imbalance selling

5,500 units

ETFplusFund Issuer

Appointed Intermediary

(3) The appointed

intermediary

sends a creation

request for 5,500

units

Orders flowCreation flowTrades flow

Intermediaries

Data flow – day T

Borsa Reference Data

– trades parking

(4) Contracts with

real quantity but

“conventional price”

are parked

Example: buy imbalance

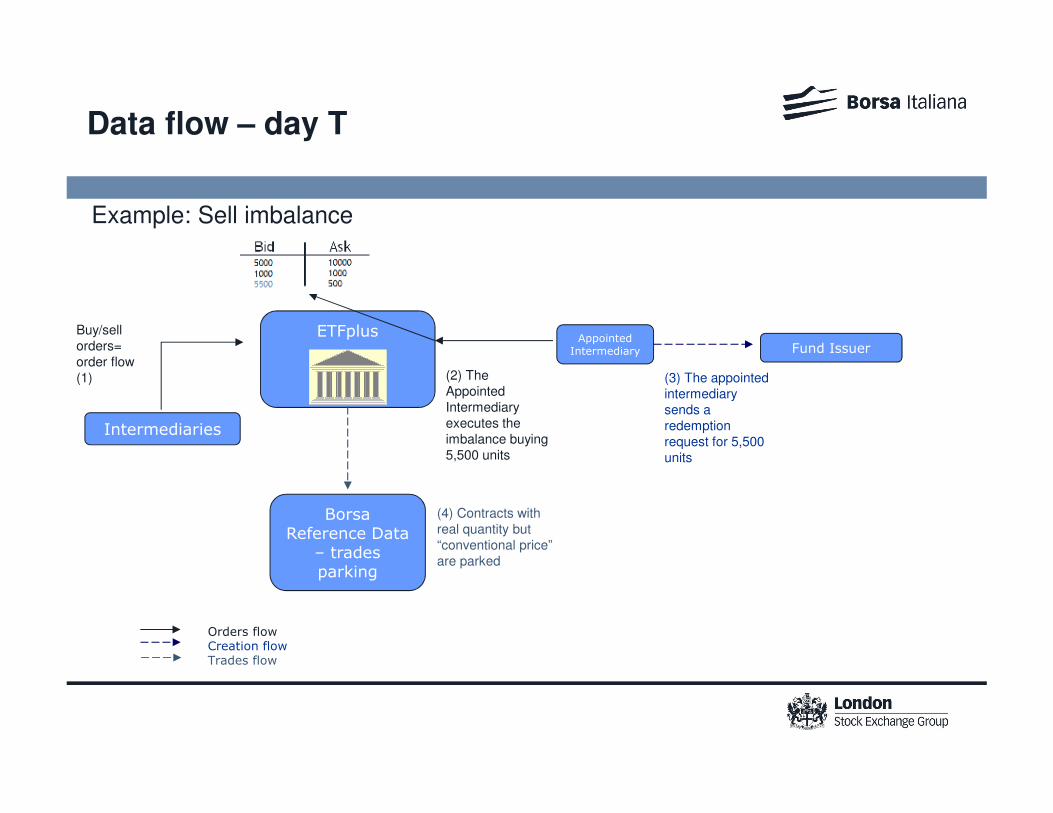

ETFplus

Intermediaries

Orders flowCreation flowTrades flow

(4) Contracts with

real quantity but

“conventional price”

are parked

Borsa Reference Data

– trades parking

Buy/sell

orders=

order flow

(1) (2) The

Appointed

Intermediary

executes the

imbalance buying

5,500 units

(3) The appointed

intermediary

sends a

redemption

request for 5,500

units

Fund IssuerAppointed

Intermediary

Data flow – day T

Example: Sell imbalance

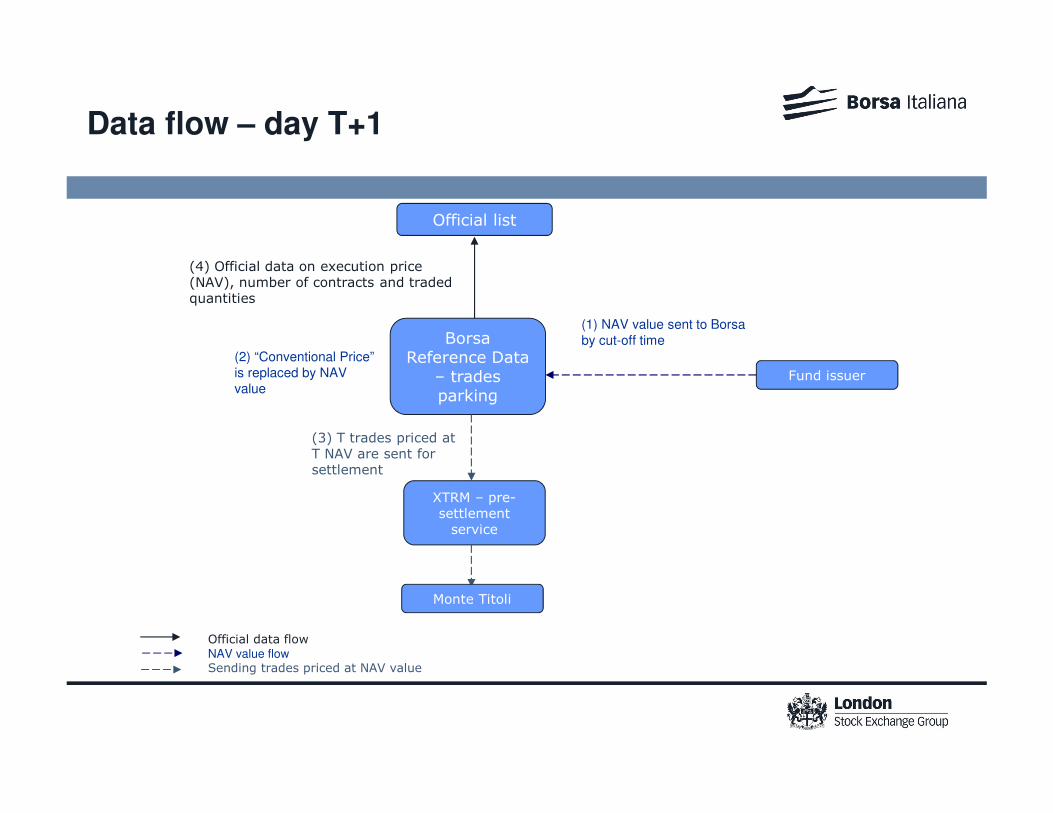

(4) Official data on execution price (NAV), number of contracts and traded quantities

Fund issuer

Official data flowNAV value flow

Sending trades priced at NAV value

Official list

Borsa Reference Data

– trades parking

(1) NAV value sent to Borsa

by cut-off time

XTRM – pre-settlement service

(3) T trades priced at T NAV are sent for settlement

Monte Titoli

(2) “Conventional Price”

is replaced by NAV

value

Data flow – day T+1

Appointed Intermediary

account

Intermediaries account

Paying bank

account

Fund Issuer

Custodian account

Fund Issuer account

MTX

Instruction to increase outstanding units

U

N

I

T

S

€ €

U

N

I

T

S

€

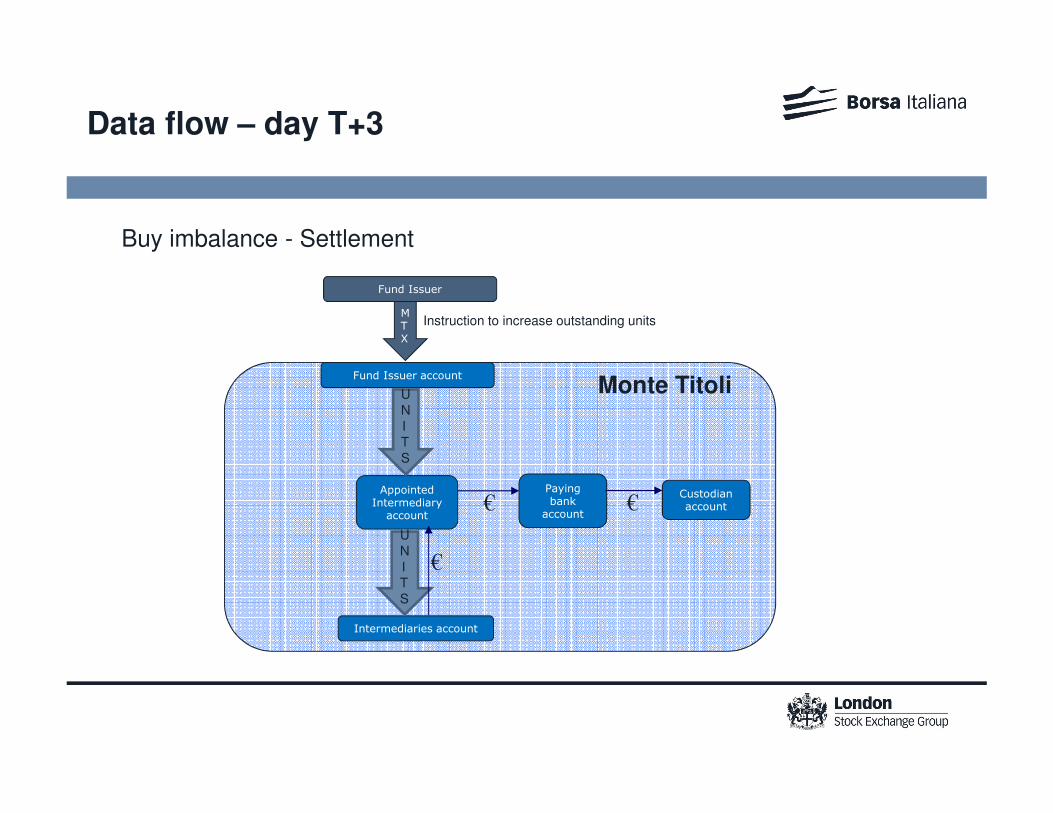

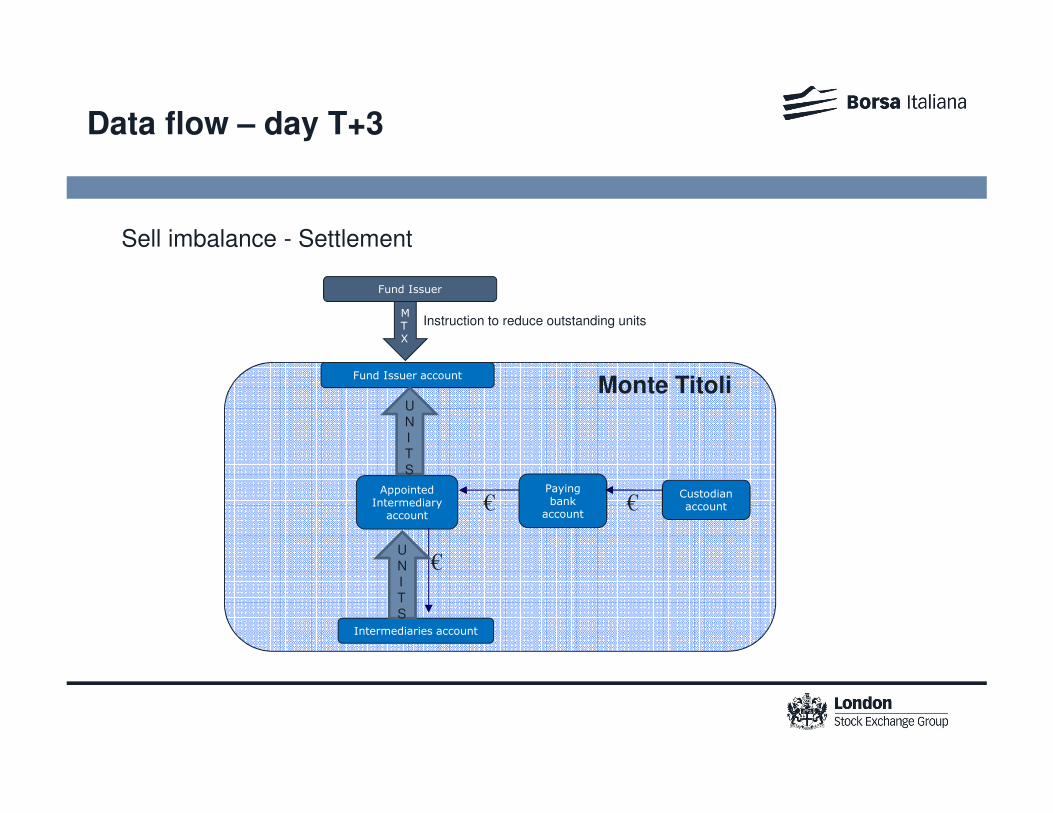

Data flow – day T+3

Buy imbalance - Settlement

Monte Titoli

Appointed Intermediary

account

Intermediaries account

Paying bank

account

Custodian account

Fund Issuer account

€ €

€

U

N

I

T

S

Data flow – day T+3

Sell imbalance - Settlement

Monte Titoli

Instruction to reduce outstanding units

Fund Issuer

MTX

U

N

I

T

S

The publication of this document does not represent solicitation, by Borsa Italiana S.p.A., of public saving and is not to be considered

as a recommendation by Borsa Italiana as to the suitability of the investment, if any, herein described. This document has not to be

considered complete and it is meant for information and discussion purposes only. Borsa Italiana accepts no liability, arising, without

limitation to the generality of the foregoing, from inaccuracies and/or mistakes, for decisions and/or actions taken by any party based

on this documents. Trademarks Borsa Italiana and Borsa Italiana's logo, ETFplus, IDEM, MOT, MTA, STAR, SeDeX, MIB, IDEX, BIt

Club, Academy, MiniFIB, DDM, EuroMOT, Market Connect, NIS, Borsa Virtuale, ExtraMOT, MIV BIt Systems Piazza Affari Gestione

e Servizi, Palazzo Mezzanotte Congress and Training Centre and PAGS are owned by Borsa Italiana S.p.A. FTSE is a registered

trademark of London Stock Exchange plc and The Financial Times Limited and is used by FTSE International Limited under licence.

London Stock Exchange, the coat of arms device and AIM are a registered trade mark of London Stock Exchange plc. The above

trademarks and any other trademark owned by the London Stock Exchange Group cannot be used without express written consent

by the Company having the ownership of the same. Borsa Italiana S.p.A. and its subsidiaries are subject to direction and

coordination of London Stock Exchange Group Holdings (Italy) Ltd – Italian branch. The Group promotes and offers the post-trading

services of Cassa di Compensazione e Garanzia S.p.A. and Monte Titoli S.p.A. in an equitable, transparent and non-discriminatory

manner and on the basis of criteria and procedure aimed at assuring interoperability, security and equal treatment among market

infrastructures, to all subjects who so request and are qualified in accordance with national and community legislation, applicable

rules and decisions of the competent Authorities.

© November 2013 London Stock Exchange Group plc

All rights reserved.

No part of this book may be reproduced or transmitted in any form or by any means, electronic or mechanical, including

photocopying, recording, or any information storage or retrieve system without prior permission from the copyright owners.