19

Meeting the Requirements for Interest Only Loans Brad Lynch Lawyer

| Date post: | 19-Mar-2017 |

| Category: |

Economy & Finance |

| Upload: | informa-australia |

| View: | 47 times |

| Download: | 1 times |

Meeting the Requirements for

Interest Only Loans

Brad Lynch

Lawyer

1. Report 445 – Review of Interest only home loans -Released August 2015

2. Report 493 – Review of Interest-only home loans: Mortgage Brokers Inquiries into consumers requirements and objectives – Released September 2016.

Useful ASIC Guidance on Interest Only Home Loans

2

ASIC expect that credit licensees would make many, if not all, of the inquiries in RG 209.33, as entering into an unsuitable home loan can have a potentially large negative financial impact on a consumer. – Report 445

Scalability Home Loans (Interest Only and P&I)

3

Pros

• Flexible repayments

• Redirect cash flow

• Temporary finance

• Tax Benefits

Cons

• Not building equity

• Higher overall interest cost

• Larger repayments when move to P&I.

Why have an interest only home loan?

4

Finding 1:

Lack of evidence of inquiries into requirements and objectives

Not keep sufficient evidence of inquiries into consumer’s requirements and objectives and not always clear how an interest-only home loan meets the requirements of an owner-occupier.

Report 445 Review of Interest only home loans

5

Action 1:

Make and document inquiries into a consumer’s requirements and objectives. For interest-only home loans, consider whether specific features, benefits and costs associated with the loan meet the consumer’s objectives.

Action 2:

Ensure that the period of interest-only repayments aligns with the particular consumer’s requirements and objectives.

Be very careful if over 5 Year IO period (particularly Owner Occupier)

Report 445 Review of Interest only home loans

6

Finding 2:

Affordability and interest-only home loans

Not ensure sufficient surplus income above their expenses and loan repayments to withstand income/ expense fluctuations or an interest rate rise.

Some lenders didn’t apply buffer to existing debts

Report 445 Review of Interest only home loans

7

Action 3

Ensure adequate policies and processes are in place to assess a consumer’s ability to meet their financial obligations, including the effect of future interest rate rises on the proposed credit contract and existing credit contracts.

Report 445Review of Interest only home loans

8

Finding 3:

Variation in treatment of volatile and irregular income

Higher income figure being used for serviceability assessments where there was a substantial difference between previous years’ incomes.

Rental income discounted by 20% to allow for property expenses and periods of non-occupancy where the property-related expenses would likely be greater than 20% of rental income.

Report 445Review of Interest only home loans

9

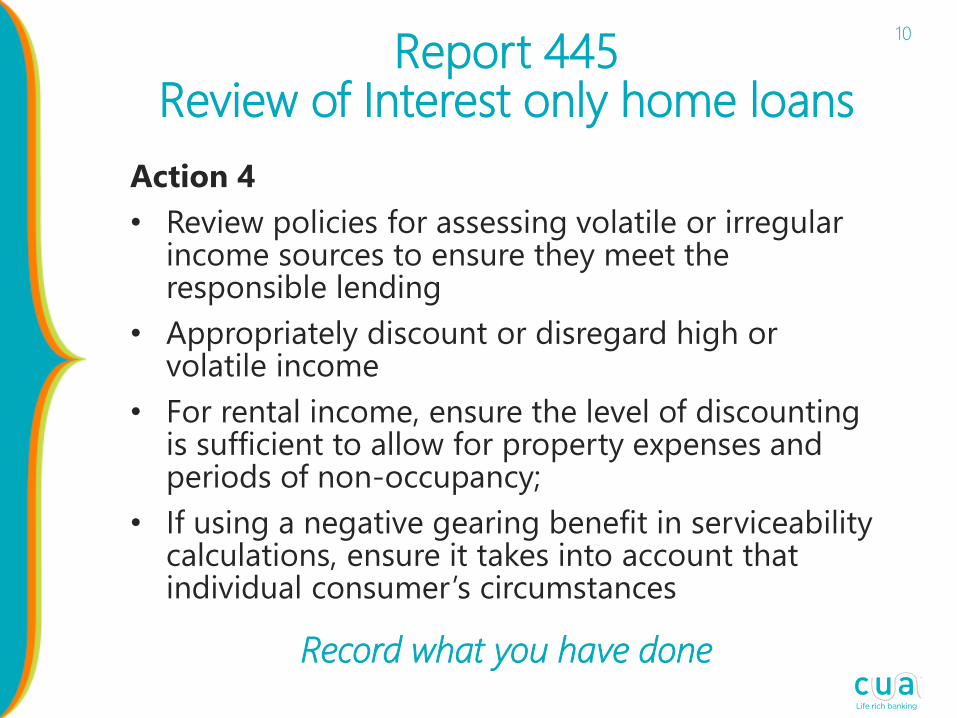

Action 4

• Review policies for assessing volatile or irregular income sources to ensure they meet the responsible lending

• Appropriately discount or disregard high or volatile income

• For rental income, ensure the level of discounting is sufficient to allow for property expenses and periods of non-occupancy;

• If using a negative gearing benefit in serviceability calculations, ensure it takes into account that individual consumer’s circumstances

Record what you have done

Report 445 Review of Interest only home loans

10

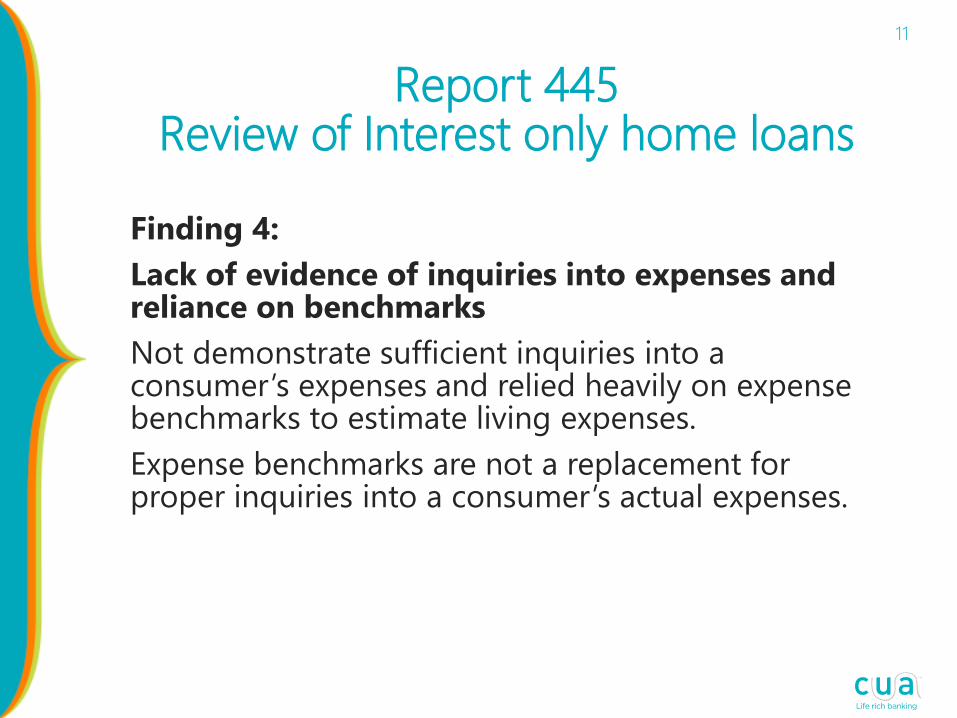

Finding 4:

Lack of evidence of inquiries into expenses and reliance on benchmarks

Not demonstrate sufficient inquiries into a consumer’s expenses and relied heavily on expense benchmarks to estimate living expenses.

Expense benchmarks are not a replacement for proper inquiries into a consumer’s actual expenses.

Report 445 Review of Interest only home loans

11

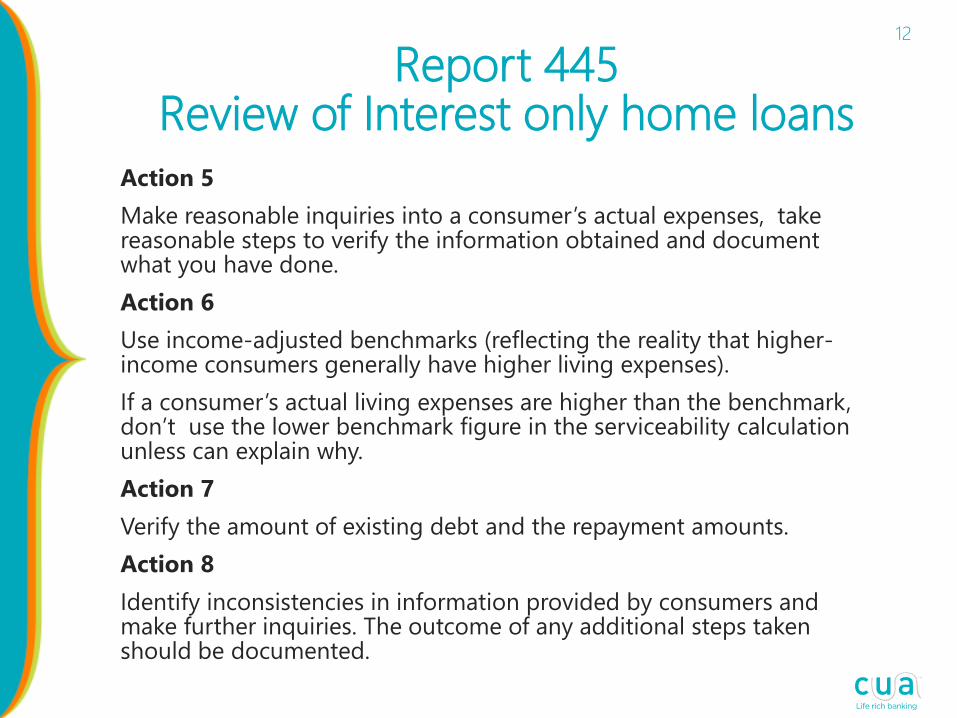

Action 5

Make reasonable inquiries into a consumer’s actual expenses, take reasonable steps to verify the information obtained and document what you have done.

Action 6

Use income-adjusted benchmarks (reflecting the reality that higher-income consumers generally have higher living expenses).

If a consumer’s actual living expenses are higher than the benchmark, don’t use the lower benchmark figure in the serviceability calculation unless can explain why.

Action 7

Verify the amount of existing debt and the repayment amounts.

Action 8

Identify inconsistencies in information provided by consumers and make further inquiries. The outcome of any additional steps taken should be documented.

Report 445 Review of Interest only home loans

12

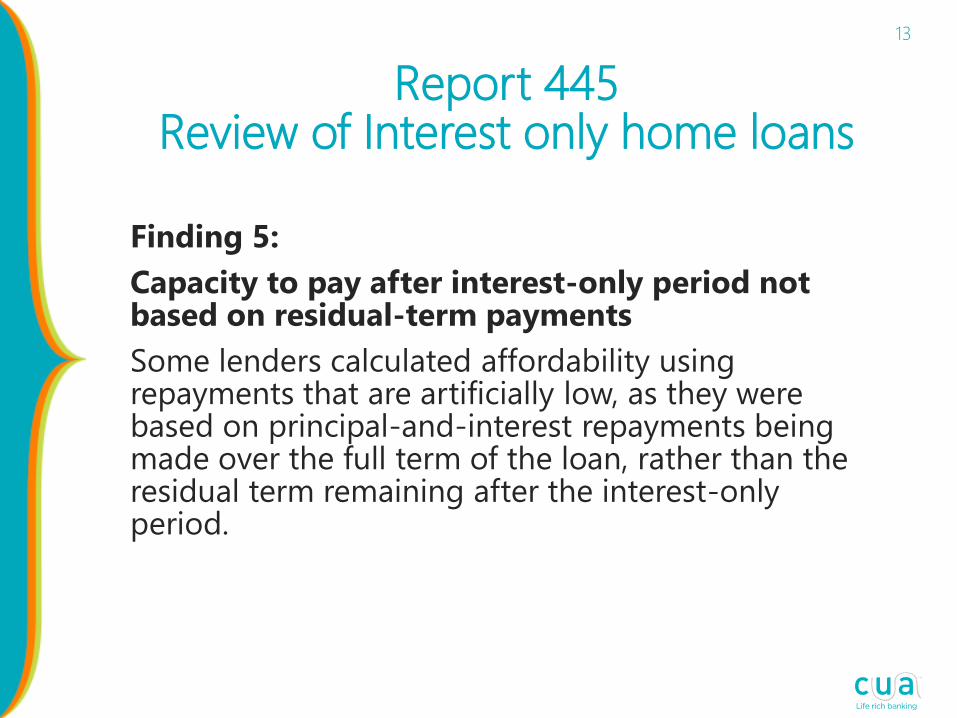

Finding 5:

Capacity to pay after interest-only period not based on residual-term payments

Some lenders calculated affordability using repayments that are artificially low, as they were based on principal-and-interest repayments being made over the full term of the loan, rather than the residual term remaining after the interest-only period.

Report 445 Review of Interest only home loans

13

Action 9

Lenders should assess a consumer’s capacity to make the principal-and-interest repayments over the residual term of the loan (after the interest-only period lapses), as this will better reflect a consumer’s ability to meet their financial obligations under an interest-only home loan.

Report 445 Review of Interest only home loans

14

Finding 6:

Lack of flexibility for hardship variations for interest-only home loans

Some lenders applied more restrictive options for borrowers seeking hardship variations under an interest-only home loan.

Report 445Review of Interest only home loans

15

Action 10

Lenders should:

• review their systems, policies and processes for hardship variations for interest-only home loans;

• have a variety of options available to consumers who are in financial hardship; and

• assess the most appropriate outcome of a hardship application on a case-by-case basis.

Report 445 Review of Interest only home loans

16

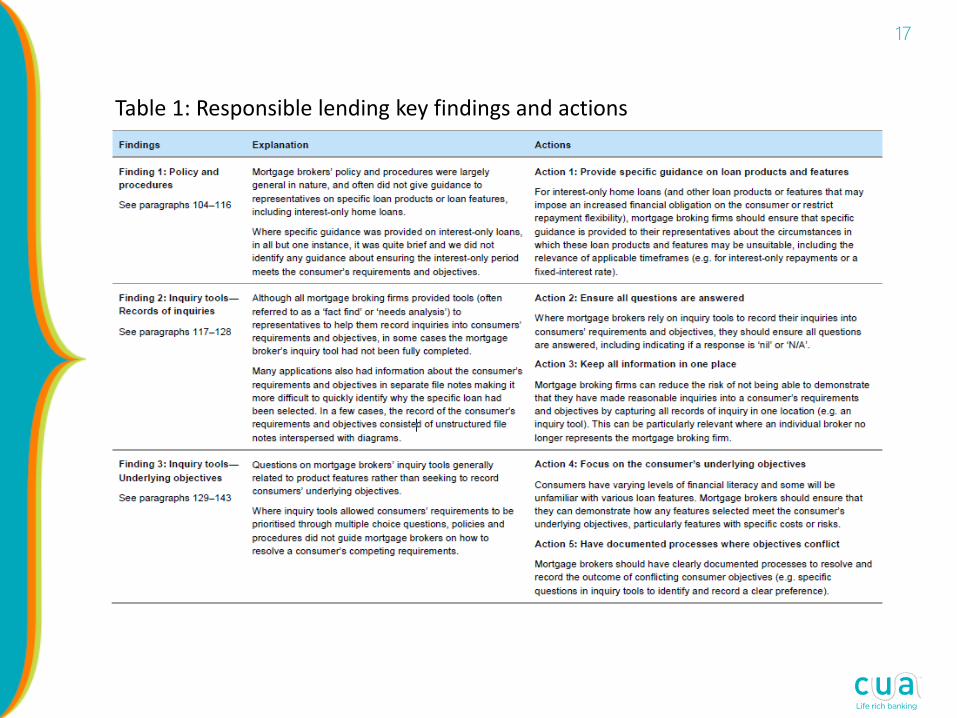

Table 1: Responsible lending key findings and actions

17

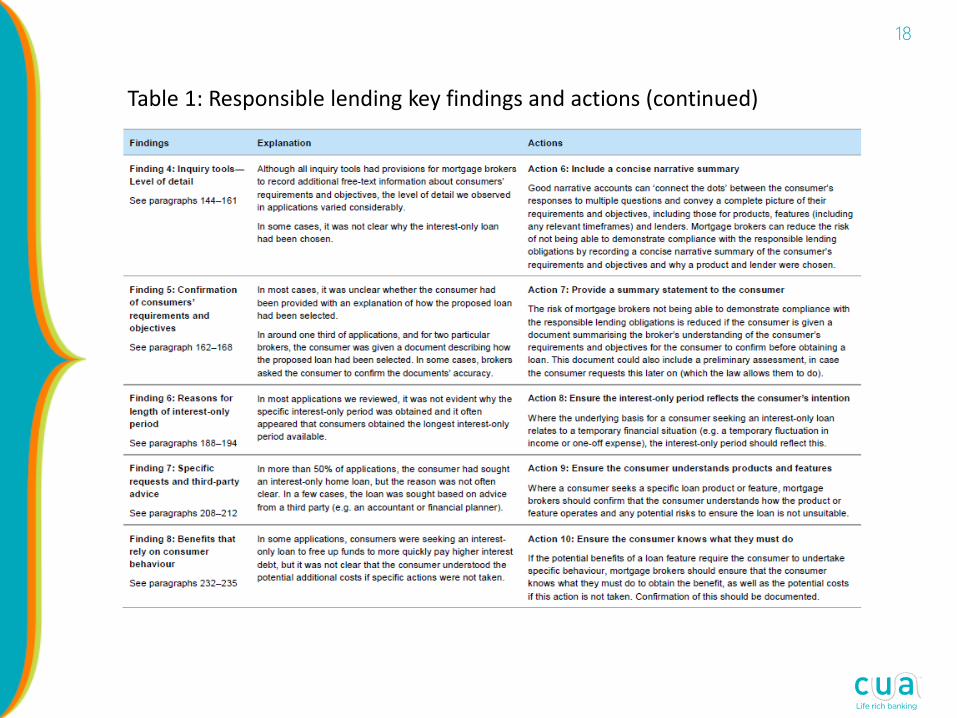

Table 1: Responsible lending key findings and actions (continued)

18

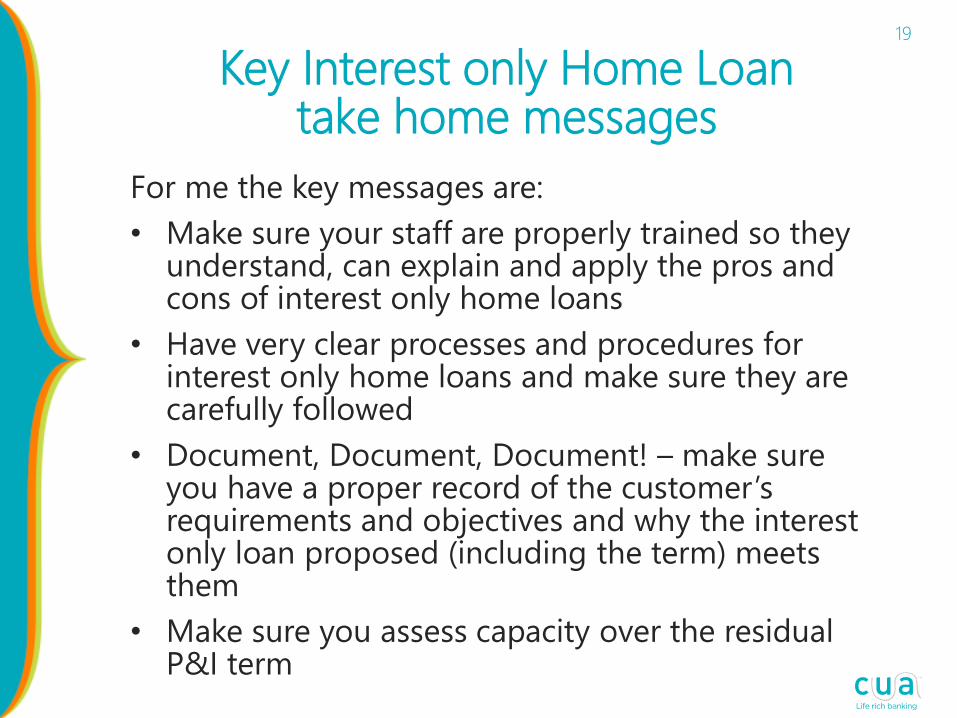

For me the key messages are:

• Make sure your staff are properly trained so they understand, can explain and apply the pros and cons of interest only home loans

• Have very clear processes and procedures for interest only home loans and make sure they are carefully followed

• Document, Document, Document! – make sure you have a proper record of the customer’s requirements and objectives and why the interest only loan proposed (including the term) meets them

• Make sure you assess capacity over the residual P&I term

Key Interest only Home Loan take home messages

19