29

Brazil Economic Outlook FIRST QUARTER 2018

Brazil Economic OutlookFIRST QUARTER 2018

Brazil Economic Outlook 1Q18

Brazil: recovery gains momentum,

but risks do not recede

1. The growth of the Brazilian economy has surprised upwards

during 2017. That and the improvements in the global

environment, especially the acceleration of global growth,

reinforce the prospects for a (cyclical) recovery of the activity. We

have thus revised upwards our growth forecasts Brazil. We now

estimate growth to have reached 1.0% in 2017 and expect it to

increase to 2.1% in 2018 and 3.0% in 2019

2. Inflation has already bottomed out, but its acceleration from

now on will be gradual, allowing the Central Bank to keep

SELIC interest rates at historically low levels. Specifically,

inflation should reach 4.3% in 2018 and 4.7% in 2019, after having

closed 2017 at 2.9%, while SELIC rates should soon reach 6.75%

and remain at this level for a long time

3. Although in our baseline scenario the economy will continue to

recover and the fiscal problem will be addressed with a reform of

the social security and other measures at the beginning of the next

government to be elected in Oct-18, we can not rule out an

alternative scenario where political and fiscal risks

materialize, bringing the recovery to and end and perhaps

even generating a new economic crisis

Brazil Economic Outlook 1Q18

3

GLOBALGlobal growth confirmed and

short-terms risks moderated

Brazil Economic Outlook 1Q18

Global growth confirmed

01 Improved forecasts for the US,

China and the Eurozone

There is less short-term

uncertainty

02 More positive perspectives for

emerging countries

Greater global demand and

increase in commodity prices

03 More caution in the financial

markets

Expectations of lower liquidity

may reduce flows to emerging

markets

04 Contained core inflation

Although the downward pressure

factors are disappearing

05 Central banks continue their paths

towards normalization

The reasons for withdrawing stimuli

are materializing

06 Global risks

Lesser in the short term; no

changes in the medium and long

term

4

Brazil Economic Outlook 1Q18

Reasons for optimism in large areas, although with caution

Growth revised upwards

Improvement in the labor market

Approval of the tax reform

Continuistic changes in the Fed

UNITED STATES

Moderate deceleration

Some reforms already underway

Positive conclusions at

the XIX Congress of the CPC

Greater potential growth

CHINA

Greater growth than expected

More robust domestic demand

Lower political uncertainty

Plans for greater integration

EUROZONE

5

Brazil Economic Outlook 1Q18

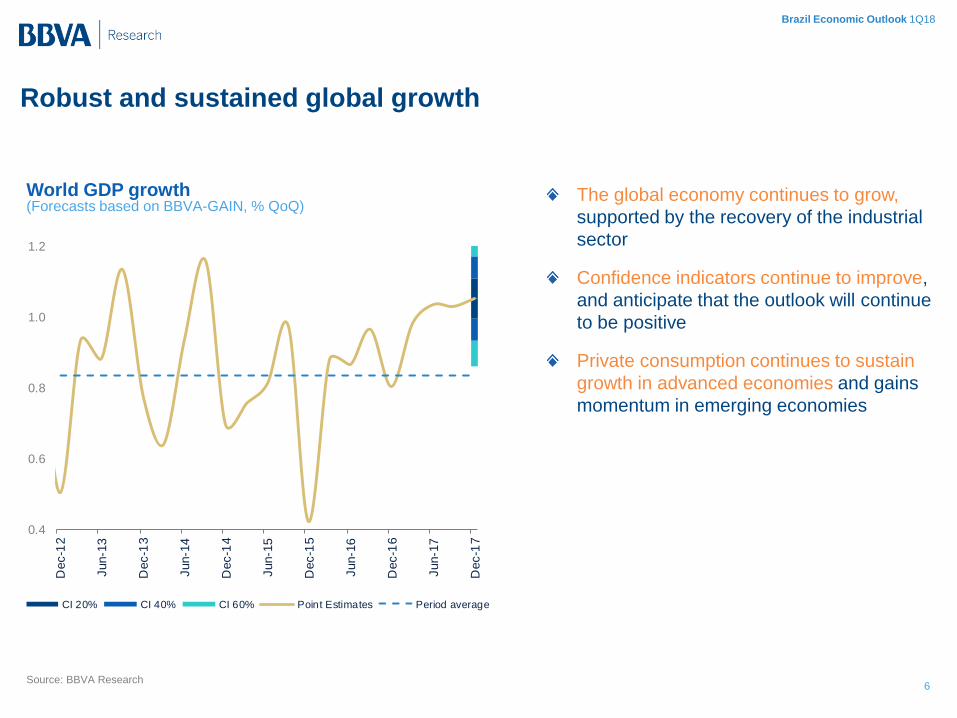

Robust and sustained global growth

Source: BBVA Research6

World GDP growth(Forecasts based on BBVA-GAIN, % QoQ)

The global economy continues to grow,

supported by the recovery of the industrial

sector

Confidence indicators continue to improve,

and anticipate that the outlook will continue

to be positive

Private consumption continues to sustain

growth in advanced economies and gains

momentum in emerging economies

0.4

0.6

0.8

1.0

1.2

Dec-1

2

Jun-1

3

Dec-1

3

Jun-1

4

Dec-1

4

Jun-1

5

Dec-1

5

Jun-1

6

Dec-1

6

Jun-1

7

Dec-1

7

CI 20% CI 40% CI 60% Point Estimates Period average

6

Brazil Economic Outlook 1Q18

The outlook for emerging economies improves

7

The increase in oil prices reflects a greater

global demand, which would account for

60% of such increase

But this is also due to supply factors, linked

to geopolitical risks and the correction of

inventories

Positive and significant impact on emerging

economies that produce raw materials

However,we still expect prices to converge

to $ 60 per barrel in the medium term, due

to increased competition and structural

changes in the energy sector

Price of oil(Dollars per barrel,%)

Source: BBVA Research

Variation over previous period Dollars per barrel

4Q17 2018 2019

18%

21.8%

-2.8%

61.5

65.9

64.1

7

Brazil Economic Outlook 1Q18

88

-1.3

-1.0

-0.8

-0.5

-0.3

0.0

0.3

0.5

0.8

1.0

1.3

ma

r.-1

3

sep.-

13

ma

r.-1

4

sep.-

14

ma

r.-1

5

sep.-

15

ma

r.-1

6

sep.-

16

ma

r.-1

7

sep.-

17

China

Trump

Taper tamtrun

Brexit

Preferencefor EM

Preference for DM

Caution in financial markets, with moderation of flows to emerging markets

Source: BBVA Research, EPFR

Risk appetite indicator(Factor 1 (global), EPFR flow analysis)

Investors appetite for emerging (EM) vs developed (DM)(Inflows in EM vs. DM in % of assets under management)

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

Dec-1

3

Jun-1

4

Dec-1

4

Jun-1

5

Dec-1

5

Jun-1

6

Dec-1

6

Jun-1

7

Dec-1

7

Greater appetite for risk

Less appetite for risk

8

Brazil Economic Outlook 1Q18

Contained core inflation

Source: BBVA Research and the OCDE

Production gap and core inflation(% GDP potential, % YoY)

Reduction of the idle capacity of the

economy, but with room to grow without

strong inflationary pressures

Less reaction of prices to the increase in

activity, for several reasons:

Globalization

Increased flexibility of the labor market

Low inflationary expectations

Reduced productivity growth

The increase in the price of oil will push up

inflation in the short term, facilitating the

normalization of central banks in developed

economies -4

-3

-2

-1

0

1

2

3

4

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

US output gap US core inflation

EA output gap EA core inflation

9

Brazil Economic Outlook 1Q18

Fed

ECBBoJ

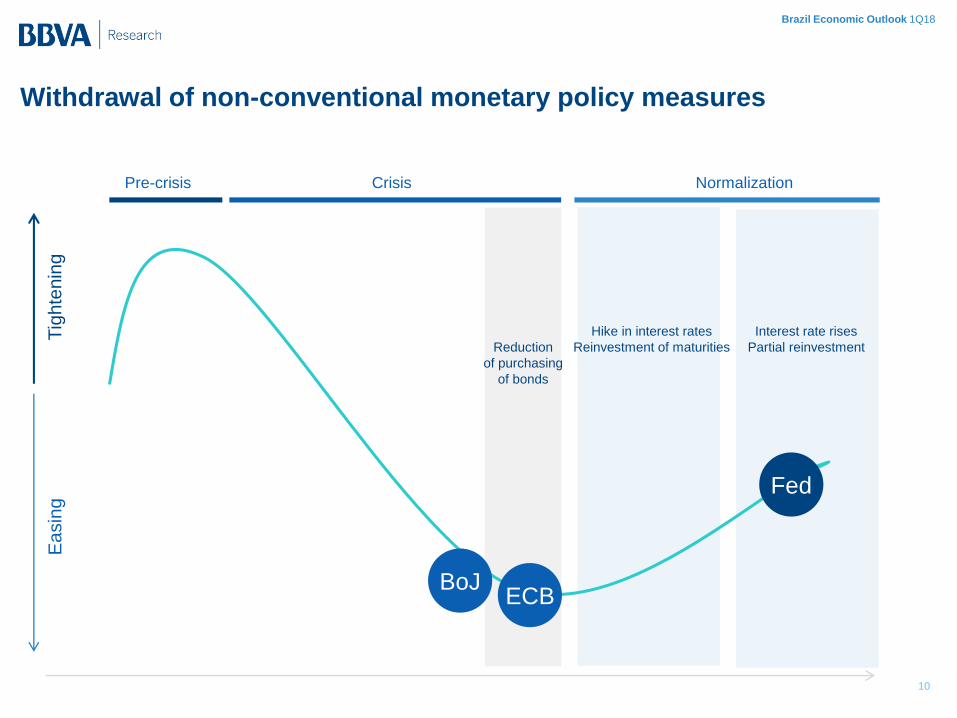

Withdrawal of non-conventional monetary policy measures

Tig

hte

nin

gE

asin

g

Pre-crisis Crisis Normalization

Hike in interest rates

Reinvestment of maturities

Interest rate rises

Partial reinvestmentReduction

of purchasing

of bonds

10

Brazil Economic Outlook 1Q18

FED ECB

Tightening cycle and reduction of

the balance in progress

Estimated rise of 75pbs in 2018 to

2.25% and reduction of the balance

by 500,000 million dollars

QE reduction, but extension until

September 2018

No rate hikes are expected until

2019

• Macro : possible surprises

in inflation

Elements of uncertainty:

• Politics: changes in government

ministries (Fed, ECB)

• Markets: Long-term rates and

slope of the curve

Monetary policy normalization: accelerated in the case of the Fed,

gradual in the case of the ECB

Focus: avoid sudden acceleration

of long-term rates Focus:

gain room for manoeuvre

11

Brazil Economic Outlook 1Q18

Down

Up

Unchanged

Generalized revision of the upward growth

Source: BBVA Research

UNITED STATES

2018

2.62019

2.5

SOUTH AMERICA

2019

2.6

EURO ZONE

CHINA2018

2.2

2019

6.0

WORLD

2018

3.82017

3.8

2019

1.8

2018

1.6

2018

6.3MEXICO2019

2.22018

2.02019

4.32018

4.5

TURKEY

12

Brazil Economic Outlook 1Q18

Global risks: Fewer in the short term

13* US: United States; EX: Eurozone; CHN: China. Source. BBVA Research

-P

rob

ab

ilit

y i

n t

he

sh

ort

te

rm+

- Severity+

CHN

US

EZ

• Containment of risks associated with high leverage in

the short term

• Potential negative effect of increased protectionism

• Political tensions still high, but more contained

• Negotiation of trading relations (NAFTA)

• Signs of over-valuation of certain assets

• Reduced risk of rapid normalization by the Fed, but

uncertainty persists

• Reduced political uncertainty, but significant question

marks remain in several countries:

• Brexit: fewer doubts about future trading

relations

• Germany: functioning of the “grand coalition”

• Italy (elections in March 2018): risk of a

government opposed to the European project

• Management of the normalization of monetary policy

Brazil Economic Outlook 1Q18

14

BRAZILRecovery gains momentum,

but risks do not recede

JGA / 14

Brazil Economic Outlook 1Q18

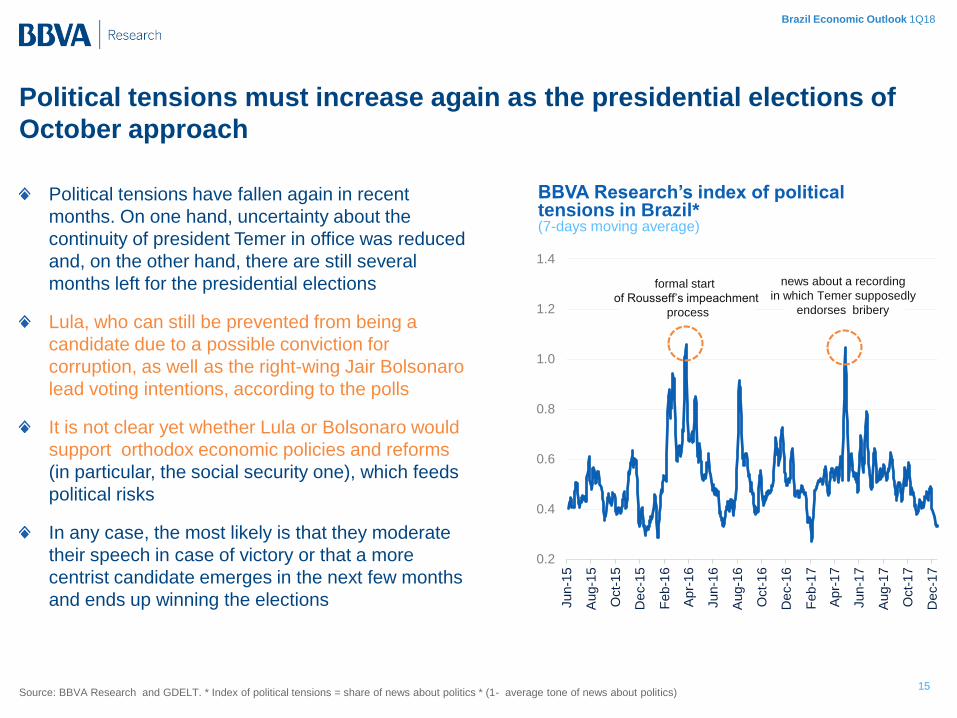

Political tensions must increase again as the presidential elections of

October approach

Political tensions have fallen again in recent

months. On one hand, uncertainty about the

continuity of president Temer in office was reduced

and, on the other hand, there are still several

months left for the presidential elections

Lula, who can still be prevented from being a

candidate due to a possible conviction for

corruption, as well as the right-wing Jair Bolsonaro

lead voting intentions, according to the polls

It is not clear yet whether Lula or Bolsonaro would

support orthodox economic policies and reforms

(in particular, the social security one), which feeds

political risks

In any case, the most likely is that they moderate

their speech in case of victory or that a more

centrist candidate emerges in the next few months

and ends up winning the elections

BBVA Research’s index of political tensions in Brazil*(7-days moving average)

Source: BBVA Research and GDELT. * Index of political tensions = share of news about politics * (1- average tone of news about politics)

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Jun-1

5

Aug-1

5

Oct-

15

De

c-1

5

Feb

-16

Apr-

16

Jun-1

6

Aug-1

6

Oct-

16

De

c-1

6

Feb

-17

Apr-

17

Jun-1

7

Aug-1

7

Oct-

17

De

c-1

7

formal start

of Rousseff’s impeachment

process

news about a recording

in which Temer supposedly

endorses bribery

1515

Brazil Economic Outlook 1Q18

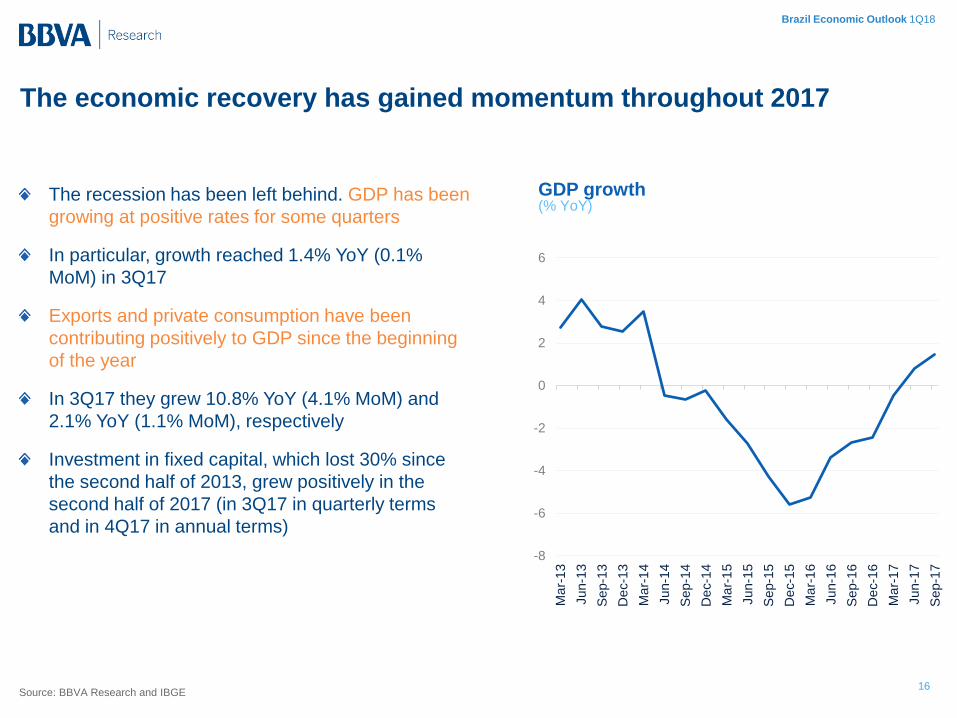

The economic recovery has gained momentum throughout 2017

The recession has been left behind. GDP has been

growing at positive rates for some quarters

In particular, growth reached 1.4% YoY (0.1%

MoM) in 3Q17

Exports and private consumption have been

contributing positively to GDP since the beginning

of the year

In 3Q17 they grew 10.8% YoY (4.1% MoM) and

2.1% YoY (1.1% MoM), respectively

Investment in fixed capital, which lost 30% since

the second half of 2013, grew positively in the

second half of 2017 (in 3Q17 in quarterly terms

and in 4Q17 in annual terms)

GDP growth(% YoY)

16Source: BBVA Research and IBGE

-8

-6

-4

-2

0

2

4

6

Ma

r-1

3

Jun-1

3

Sep-1

3

De

c-1

3

Ma

r-1

4

Jun-1

4

Sep-1

4

De

c-1

4

Ma

r-1

5

Jun-1

5

Sep-1

5

De

c-1

5

Ma

r-1

6

Jun-1

6

Sep-1

6

De

c-1

6

Ma

r-1

7

Jun-1

7

Sep-1

7

16

Brazil Economic Outlook 1Q18

Robustness of exports and recovery of private consumption and

investment sustain the cyclical recovery of the economy

Exports are supported by the global environment, as

well as by favorable terms of trade and exchange

rate

Private consumption, which represents two thirds of

GDP, has been accelerating due to the moderation

of inflation and improvements in the labor market,

and despite the weakness of the credit market

Unemployment reached 12.0% in Nov-17 (13.70% in

Mar-17) helping the real wage bill to grow over 4% in

recent months

With respect to investment, it has been stimulated

by the recovery of consumption, expansive

monetary policy and the reduction of political

uncertainty

Both public consumption and expansion of imports

continue to contribute negatively to GDP

Exports, private consumption and investment(% YoY)

17Source: BBVA Research and IBGE

-20

-15

-10

-5

0

5

10

15

Ma

r-1

3

Jun-1

3

Sep

-13

Dec-1

3

Ma

r-1

4

Jun-1

4

Sep

-14

Dec-1

4

Ma

r-1

5

Jun-1

5

Sep

-15

Dec-1

5

Ma

r-1

6

Jun-1

6

Sep

-16

Dec-1

6

Ma

r-1

7

Jun-1

7

Sep

-17

Exports Private consumprion Investment in Fixed Capital

17

Brazil Economic Outlook 1Q18

Growth prospects for Brazil improve, mainly due to a more positive

global environment

18

The greater strength of the recovery of activity in Brazil since

the beginning of 2017 and, mainly, the better perspectives for

global growth (particularly in China) have caused an upward

adjustment in our forecast for the country

The approval of an ambitious social security reform during the

final year of the Temer government is unlikely. Unaddressed

fiscal problems and the political noise that the October elections

must generate should together prevent a more robust

economic recovery

2017 20192018

3.0%

(now)

1.5%(before)

2.1%(now)

2.7%(before)

0.6%(before)

1.0%(now)

18

Brazil Economic Outlook 1Q18

In 2017 private consumption has started to grown positively again and in

2018-19 investment must do so; net exports will contribute less to GDP

19

Consumption and investment forecasts have been

revised upwards, in line with the improved tone

exhibited by recent data and improvement in the

global environment

Exports must also grow more than previously expected,

stimulated by further growth in the global economy. The

expansion of domestic demand will support imports, reducing the

net contribution of external demand to GDP

GDP growth, by demand components*(%)

* (f) = forecasts. Source: BBVA Research and IBGE

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

GDP Investment Private consumption Public consumption Exports Imports

2017 (f) 2018 (f) 2019 (f)

19

Brazil Economic Outlook 1Q18

Inflation has already hit bottom

Inflation closed 2017 at 2.95%, slightly below the

target range and in line with our forecast

We maintain our forecast that inflation will close

2018 at 4.3% and 2019 at 4.7%

The acceleration of domestic demand, the

expected (moderate) depreciation of the exchange

rate and the view that food prices will exert ahead

more pressure than in 2017, when they fell 1.9%,

will all contribute for an acceleration of inflation

throughout 2018 and 2019

Inflation(IPCA; % YoY; forecast from Jan-18 onwards)

20Source: BBVA Research and IBGE.

0

2

4

6

8

10

12

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

Apr-

17

Jul-1

7

Oct-

17

Jan-1

8

Apr-

18

Jul-1

8

Oct-

18

Jan-1

9

Apr-

19

Jul-1

9

Oct-

19

Target range

20

Brazil Economic Outlook 1Q18

Monetary policy will remain exceptionally loose in 2018

The Monetary policy easing cycle, started on Sep-

16 when the SELIC interest rates was at 14.25%,

is about to come to an end

Specifically, we anticipate that the BCB will

announce a 25 bp cut of the SELIC rate, bringing it

to 6.75%, at its next monetary policy meeting in

February, and that from then onwards it will keep it

stable at this historically low level until the end of

2018

In 2019, as inflationary pressures increase and

interest rates in the developed economies are

hiked, the SELIC rate would be adjusted upwards

to 9.50%

Interest rates: SELIC(% end of period; forecasts from 2018 onwards)

21(f) = forecasts Source: BBVA Research and BCB.

7,25

10,00

11,75

14,2513,75

7,00 6,75

9,50

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

20

12

20

13

20

14

20

15

20

16

20

17

20

18 (

f)

20

19 (

f)

21

Brazil Economic Outlook 1Q18

Fiscal situation: there is still no light at the end of the tunnel

The economic recovery will drive tax collection up,

benefitting public accounts. In particular, the recent

recovery in public revenue will allow the

government to meet the 2017 fiscal target (primary

deficit of -2.5% of GDP)

Anyway, even if activity growth surprises upwards,

a strong additional fiscal adjustment will be needed

so that - in the medium term - the spending ceiling

rule will be met and - in the long term - the

unsustainability of public debt will be avoided.

In this sense, a reform of the social security and

other complementary measures are needed

One of the biggest problems is that the current

government will hardly manage to pass an

ambitious social security reform and, while we

continue to wait for the next president to do so at

the beginning of his government, it is still not clear

whether he will be willing or able to do so

22Source: BBVA Research and BCB.

Public sector’s primary result and gross debt(% of GDP; forecasts from 2017 onwards)

-90

-70

-50

-30

-10

10

30

50

70

90

-5

-4

-3

-2

-1

0

1

2

3

4

5

2010 2012 2014 2016 2018

Gross public debt (right axis) Primary balance (left axis)

22

Brazil Economic Outlook 1Q18

The current account will deteriorate moderately, but the deficit will

remain at low levels

The trade balance has been exceptionally high in

2017. On one hand, exports have grown robustly

due to the global environment and a relatively

depreciated exchange rate. On the other hand,

imports remained relatively low, due to weak

domestic demand

Thus, the commercial balance of 2017, of around

3.3% of GDP, will contribute for driving down the

current account deficit to historically low levels

(close to 0.3% of GDP)

The strengthening of domestic demand and the

stability of the terms of trade should generate an

increase in the current account deficit to around

0.6% of GDP in 2018 and 1.9% of GDP in 2019

23

Current account(% GDP; forecasts from 2017 onwards)

(f) = forecasts Source: BBVA Research and BCB.

-4.5

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

(f)

20

18

(f)

20

19

(f)

23

Brazil Economic Outlook 1Q18

Financial markets continue to display a very positive tone, stimulated by

the global environment and, in a certain way, downplaying local risks

24

At the start of Jan-18, the Sao Paulo Stock Exchange reached

historical maximum levels (in nominal terms), while the risk

premium was around 220 bp, close to the values observed

before the crisis, when the country still exhibited an investment

grade

The exchange rate has appreciated 1% in real terms in 2017 (a

nominal depreciation of 2%). The normalization of monetary

policy in the US and the stability of the terms of trade will

contribute for the Brazilian real to depreciate from 3.30 in Dec-

17 to 3.35 in Dec-18 and 3.45 in Dec-19

Nominal exchange rate(BRL / USD)

Stock exchange and risk premium(% variation in 2017 and in the last three months*)

* Variations in the last three months: from October 10, 2017 to January 10, 2018

Source: Datastream and BBVA Research. Source: Datastream and BBVA Research.

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

Sao Paulo Stock Exchange Risk premium

2017 Last three months

1.5

2.0

2.5

3.0

3.5

4.0

4.5

en

e.-

11

sep.-

11

ma

y.-1

2

en

e.-

13

sep.-

13

ma

y.-1

4

en

e.-

15

sep.-

15

ma

y.-1

6

en

e.-

17

sep.-

17

ma

y.-1

8

en

e.-

19

sep.-

19

24

Brazil Economic Outlook 1Q18

Political and fiscal risks remain high, feeding each other

25

In our baseline scenario, the economy will continue to recover

and the fiscal problem will be addressed with a reform of

social security and other measures at the beginning of the

next government, to be elected in October

However, it can not be ruled out that political and fiscal risks

materialize, slowing down the recovery and even generating a new

economic crisis, especially if the global environment stops being so

positive

Political risks

(turbulence in the presidential race,

heterodox policies, populist

government, political polarization,

government without sufficient

support in the congress, etc.)

Fiscal risks

(no approval of the social security

reform, breach of the spending

ceiling rule, unsustainability of

public debt, inflation, etc.)

25

Brazil Economic Outlook 1Q18

Brazil: recovery gains momentum,

but risks do not recede

1. The growth of the Brazilian economy has surprised upwards

during 2017. That and the improvements in the global

environment, especially the acceleration of global growth,

reinforce the prospects for a (cyclical) recovery of the activity. We

have thus revised upwards our growth forecasts Brazil. We now

estimate growth to have reached 1.0% in 2017 and expect it to

increase to 2.1% in 2018 and 3.0% in 2019

2. Inflation has already bottomed out, but its acceleration from

now on will be gradual, allowing the Central Bank to keep

SELIC interest rates at historically low levels. Specifically,

inflation should reach 4.3% in 2018 and 4.7% in 2019, after having

closed 2017 at 2.9%, while SELIC rates should soon reach 6.75%

and remain at this level for a long time

3. Although in our baseline scenario the economy will continue to

recover and the fiscal problem will be addressed with a reform of

the social security and other measures at the beginning of the next

government to be elected in Oct-18, we can not rule out an

alternative scenario where political and fiscal risks

materialize, bringing the recovery to and end and perhaps

even generating a new economic crisis

Brazil Economic Outlook 1Q18

27

FORECASTS

Brazil Economic Outlook 1Q18

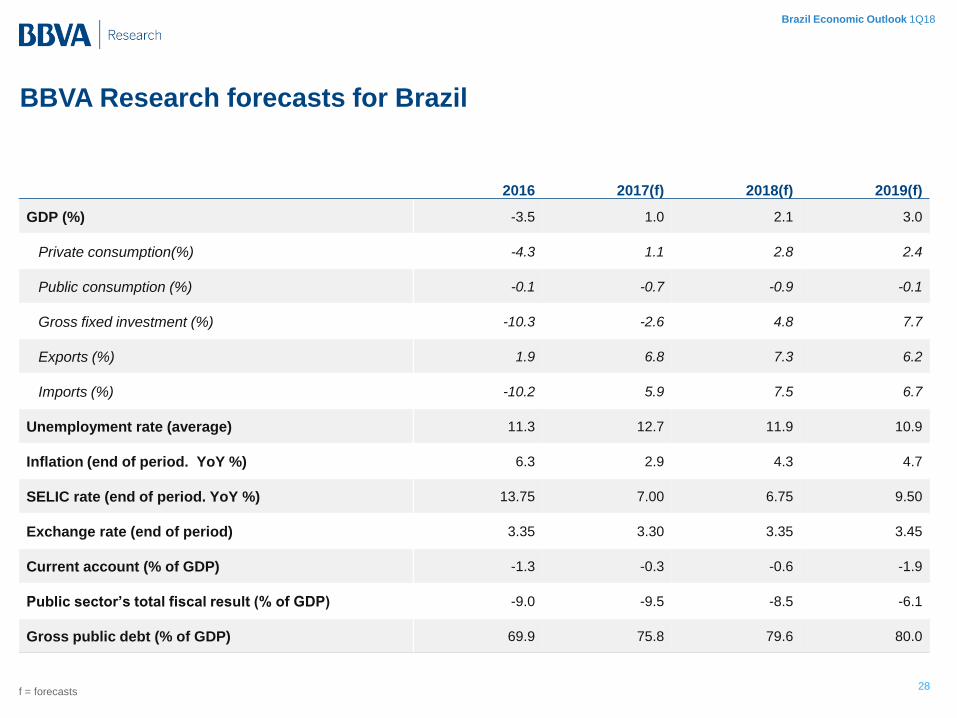

BBVA Research forecasts for Brazil

28f = forecasts

2016 2017(f) 2018(f) 2019(f)

GDP (%) -3.5 1.0 2.1 3.0

Private consumption(%) -4.3 1.1 2.8 2.4

Public consumption (%) -0.1 -0.7 -0.9 -0.1

Gross fixed investment (%) -10.3 -2.6 4.8 7.7

Exports (%) 1.9 6.8 7.3 6.2

Imports (%) -10.2 5.9 7.5 6.7

Unemployment rate (average) 11.3 12.7 11.9 10.9

Inflation (end of period. YoY %) 6.3 2.9 4.3 4.7

SELIC rate (end of period. YoY %) 13.75 7.00 6.75 9.50

Exchange rate (end of period) 3.35 3.30 3.35 3.45

Current account (% of GDP) -1.3 -0.3 -0.6 -1.9

Public sector’s total fiscal result (% of GDP) -9.0 -9.5 -8.5 -6.1

Gross public debt (% of GDP) 69.9 75.8 79.6 80.0

28

Brazil Economic Outlook 1Q18

This report has been produced by the Latin America unit

Chief Economist for Latin AmericaJuan Manuel Ruiz

BBVA-ResearchJorge Sicilia Serrano

Enestor Dos Santos

Cecilia Posadas

With the collaboration of:Global Economic Situations

Miguel Jiménez

Macroeconomic analysis

Rafael Doménech

Global Economic Situations

Miguel Jiménez

Global Financial Markets

Sonsoles Castillo

Long-Term Global Modelling and Analysis

Julián Cubero

Innovation and Processes

Oscar de las Peñas

Financial Systems and Regulation

Santiago Fernández de Lis

International Coordination

Olga Cerqueira

Digital Regulation

Álvaro Martín

Regulation

Financial Systems

Ana Rubio

Financial Inclusion

Spain and Portugal

Miguel Cardoso

United States

Nathaniel Karp

Mexico

Carlos Serrano

Middle East, Asia and

Geopolitical

Álvaro Ortiz

Turkey

Álvaro Ortiz

Asia

Le Xia

South America

Juan Manuel Ruiz

Argentina

Gloria Sorensen

Chile

Jorge Selaive

Colombia

Juana Téllez

Peru

Hugo Perea

Venezuela

Julio Pineda