23

Institutional Presentation March 2012

Institutional Presentation

March 2012

The Sector

3

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Sales Performance in the Brazilian Pharmacy Retail Sector from 1996-2011 (R$ Billion)

Pharmacy Retail: A Growth History…

Sources: IBGE, Farmácia Popular, Health, OMS IMS, Brazil Central Bank

Micro Drivers Timing

Regional

Brands

Fragmented

Market Formalization

Macro Drivers

Income Growth Population Aging Generic Drugs

1997 – 2000

1997: Asian Crisis

1998: Russian Crisis

1999: Real Depreciation

2000: Internet Bubble burst

2001 - 2002

2002: Crisis pre-Lula election

2001: Argentine Default

2003 – 2005

2003-04: First years of

Lula´s election

2004: Mensalão scandal

2006 – 2007

2006: Second Lula election

2008 – 2011

2008: Subprime Crisis

2010: Greece Debt Crisis

CAGR 03-11 Generics: 37%

4

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159 Market Share and Players Footprint

Source: IMS Health, Companies web site, Brazil Pharma

Brazil Pharma is located in strategic regions with low competition, high growth perspectives and large

complementarities to top players.

Revenues

Breakdown per

State

Raia +

Drogasil

Drogaria

S. Paulo +

Pacheco

Brazil

Pharma

São Paulo 31%

Rio de Janeiro 14%

Minas Gerais 10%

Rio Grande do Sul 8%

Paraná 6%

Goiás + DF 5%

Bahia 4%

Santa Catarina 4%

Pernambuco 3%

Ceará 3%

Pará 2%

Others 11%

Pharmacy Retail: ... With Consolidation Opportunity

South

East

Region

Other

Regions

Brazil Pharma Focus

Peers Focus

The Company

6

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159 Geographic Location Strong Organic Growth Capacity (# Stores)¹

TOTAL: 986

627 own stores e

359 franchise stores

Brazil Pharma: Ready to Grow

Largest Pharmacy Retail Company in Brazil outside the Southeast

Profitable Mix (4Q11 Sales Mix)¹

Brazil Pharma Abrafarma

Branded

Generics

Non-Medicines

¹Excluded Big Ben and Sant´ana’s Stores

104 own stores

1st

228 own stores

1st

359 franchise stores

1st

194 own stores

2nd

5

1

95 20

14

89 7

8

187

7

1

7

85

98

52

150

71

221

71

292

378

2007 2008 2009 2010 2011

86

101 own stores

101

1st

32,9%

47,7%

19,4%

7

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

(1) Including Sant’ana and Big Ben acquisition that is still pending shares incorporation

Brazil Pharma: The Shareholders

BTG is our main Shareholder

Farmais Rosário

Distrital

Mais

Econômica

100% 100% 100%

Big Ben

100%

Sant’ana

100%

Operating

Partners

23%

Free Float

39%

BTG

Pactual(2)

38%

8

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

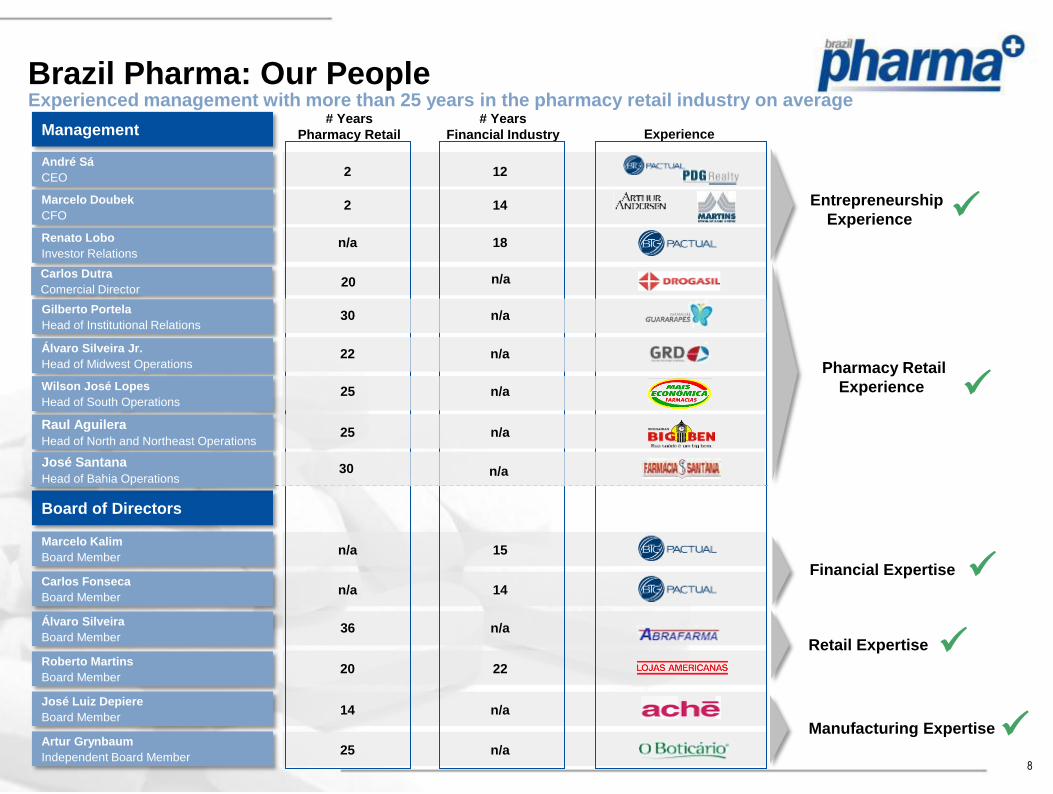

Experienced management with more than 25 years in the pharmacy retail industry on average

Brazil Pharma: Our People

André Sá

CEO

Marcelo Doubek

CFO

Renato Lobo

Investor Relations

Management

Board of Directors

Marcelo Kalim

Board Member

Carlos Fonseca

Board Member

Roberto Martins

Board Member

José Luiz Depiere

Board Member

2

2

n/a

36

# Years

Pharmacy Retail

n/a

n/a

20

14

25

# Years

Financial Industry

12

14

18

n/a

15

14

22

n/a

n/a Artur Grynbaum

Independent Board Member

Experience

Álvaro Silveira

Board Member

Carlos Dutra

Comercial Director 20 n/a

Financial Expertise

Retail Expertise

Manufacturing Expertise

Pharmacy Retail

Experience

Entrepreneurship

Experience

Gilberto Portela

Head of Institutional Relations 30 n/a

Álvaro Silveira Jr.

Head of Midwest Operations

Wilson José Lopes

Head of South Operations

22

25

n/a

n/a

Raul Aguilera

Head of North and Northeast Operations 25 n/a

José Santana

Head of Bahia Operations 30 n/a

9

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

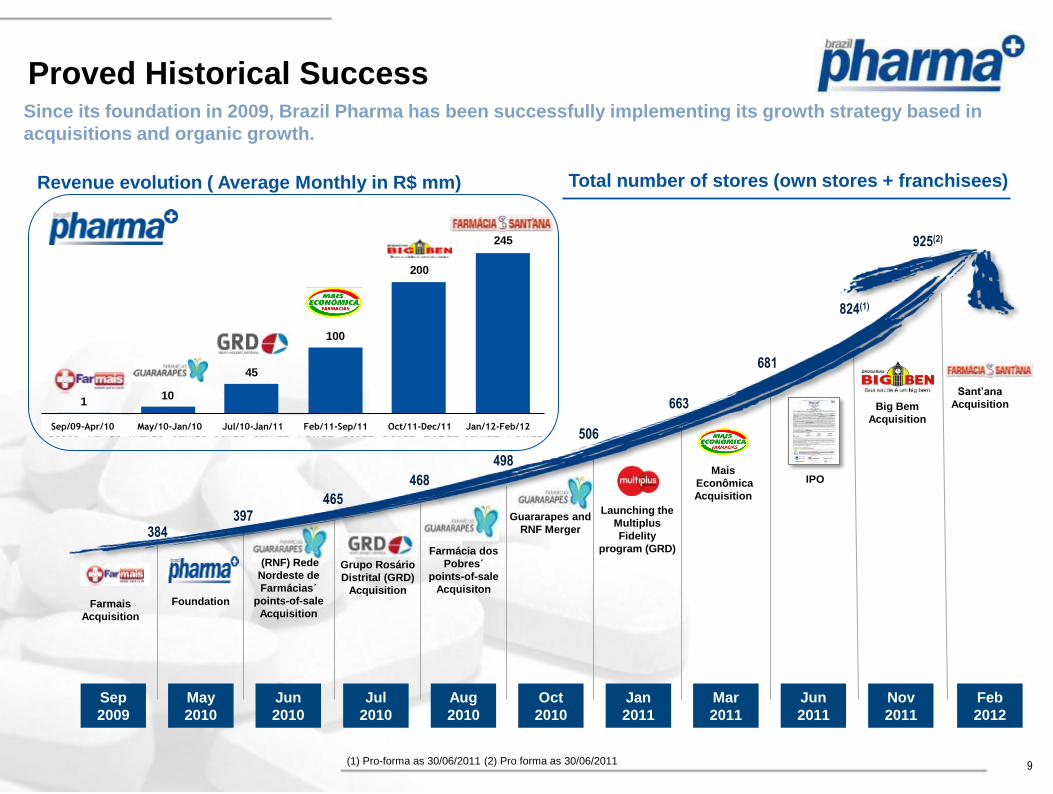

110

45

100

200

245

Set/09 - Abr/10 Mai/10 - Jan/10 Jul/10 - Jan/11 Fev/11 - Set/11 Out/11 - Dez/11 Jan/12 - Fev/12

Proved Historical Success Since its foundation in 2009, Brazil Pharma has been successfully implementing its growth strategy based in

acquisitions and organic growth.

Revenue evolution ( Average Monthly in R$ mm)

Foundation

Farmácia dos

Pobres´

points-of-sale

Acquisiton

Guararapes and

RNF Merger

(RNF) Rede

Nordeste de

Farmácias´

points-of-sale

Acquisition

Launching the

Multiplus

Fidelity

program (GRD)

Mais

Econômica

Acquisition

Grupo Rosário

Distrital (GRD)

Acquisition

384 397

465

468

506

663

Sep

2009

Aug

2010

Oct

2010

May

2010

Jun

2010

Jan

2011

Mar

2011

Nov

2011

681

IPO

Jul

2010

Jun

2011

498

Big Bem

Acquisition

824(1)

(1) Pro-forma as 30/06/2011 (2) Pro forma as 30/06/2011

Total number of stores (own stores + franchisees)

Feb

2012

Farmais

Acquisition

Sant’ana

Acquisition

925(2)

Sep/09-Apr/10 May/10-Jan/10 Jul/10-Jan/11 Feb/11-Sep/11 Oct/11-Dec/11 Jan/12-Feb/12

10

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

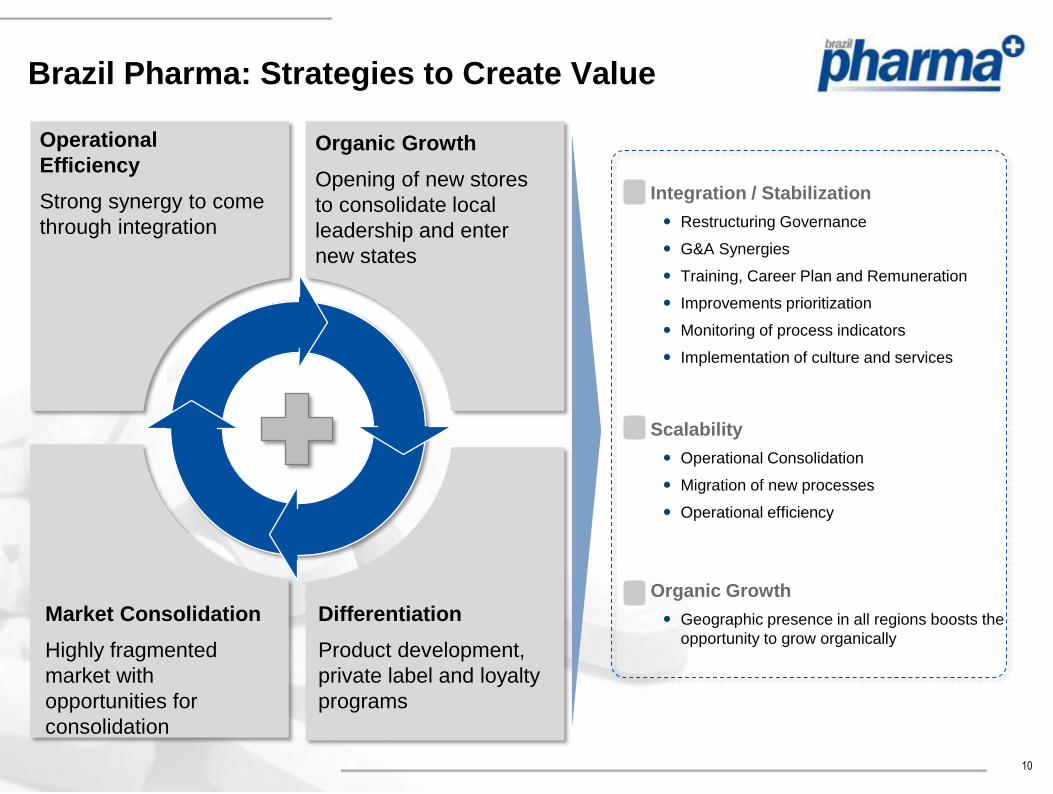

Brazil Pharma: Strategies to Create Value

Organic Growth

Opening of new stores

to consolidate local

leadership and enter

new states

Operational

Efficiency

Strong synergy to come

through integration

Market Consolidation

Highly fragmented

market with

opportunities for

consolidation

Differentiation

Product development,

private label and loyalty

programs

Integration / Stabilization

Restructuring Governance

G&A Synergies

Training, Career Plan and Remuneration

Improvements prioritization

Monitoring of process indicators

Implementation of culture and services

Scalability

Operational Consolidation

Migration of new processes

Operational efficiency

Organic Growth

Geographic presence in all regions boosts the

opportunity to grow organically

11

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159 16.5%

83.5%

Competitive Geographic Position with Differenced Mix

Brazil Pharma Focus / Competitors Drugstores per region

Brazil

Pharma Focus

Competitors Focus

More dense

Less dense

Located in strategic regions

Lower competition, giving higher gross margin

High growth with higher Real Estate opportunity

Complementarity with Large Networks

Favorable Mix to capture the potential of generics in Brazil

Higher HPC participation gives higher profitability per m2

Brazil Pharma Abrafarma

Branded Generics

Medicines Sales Mix: 4T11%

Total Sales Mix: 4T11%

Branded

Generics

Non-Medicines

71,1%

28,9%

32,9%

47,7%

19,4%

12

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Brazil

4o

2o

1o

3o

North

n/a (2)

n/a (2)

Northeast

n/a (2)

Mid-West

n/a (2)

Southeast

n/a (2)

South

n/a (2)

(1). Number of Stores Number of Stores Revenue

2011 Abrafarma Ranking

1

The New Brazil Pharma Brazil Pharma consolidates its leadership position in four of the five regions of Brazil, becoming the

largest retail pharmacy, excluding Southeast. (1)

986 points of sale 627 own stores

359 Franchise stores

359 franchise stores

228 own stores

104 own stores

101 lown stores

5

1

95 20

14

89 7

8

187

7

1

7

85

101

194 own stores

(1)Ranking by number of own stores as on September 30, 2011, considering the four largest drugstore chains in Brazil; and

(2)n/a: other chains do not have operations in the region.

13

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Results Consistency with Margin Stability

Gross Revenue

(R$ million; Pro-forma)

Gross Profit and Gross Margin

(R$ million)

EBITDA and EBITDA Margin

Number of own Stores and Organic Growth

Stores Maturation¹

221 292

378

627 71

86

148

101

2009 2010 2011 - 2011

¹ Pro-forma to include Big Ben and Sant’ana

192 279 396

802 267

138

29,1% 30,2% 34,7%

30,1% 26,2% 31,3%

2009 2010 2011 2011 PF

14

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

627

743

Brazil Pharma: Comparing With The Peers

Solid track record in sales, Gross Margin and EBITDA

LTM 3Q11 EBITDA and EBITDA Margin

(R$ million, % of Gross Revenues

LTM 3Q11 Selling, General, Administrative and Other

Expenses and % of Gross Revenue

(R$ million, % of Gross Revenues)

¹ Pro-forma to include Big Ben and Sant’ana 2 As of 30-sep-2011

LTM 3Q11 Gross Profit and Gross Margin

(R$ million, % of Gross Revenues)

Stores (as of December 31, 2011)¹

1

1 1

1

Integration Process

16

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Operations Administrative

(SSC) Procurement

Corporate

Finance

Accounts Payable

Human Resource

Accounting

IT

Legal department

Sales (pricing, mix,

location

New stores

Logistics

Purchase process

Relationship with

manufactures

Service Level

Working Capital

G&A Reduction Sales increase

Operational efficience

Gross margin Benefits

We have three operations areas:

(i) Procurement

(ii) Sales and Operations

(iii) Back Office

Brazil Pharma: Integration Process

17

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Em 5 de março de 2012 inauguramos nosso Centro de Serviços Compartilhados,

que integrará as áreas de back office das operações da Companhia, permitindo a

integração e otimização de suas atividades e processos e a implementação de um

sistema de gestão unificado

CSC Brazil Pharma

Operational and Financial Highlights 4Q2011/2011

19

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Sales and SSS

Solid track record in sales and SSS growth

Gross Revenues

(R$ million)

SSS (Same Store Growth Sales)

SSS SSS mature stores (36 months)

192.4

219.6

249.4 259.8

240.0

274.1

305.2

323.2

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11

20

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Sales Mix and Average Ticket

Increase in average ticket even with the growing relevance of generics in our sales mix

Sales Mix

(% of sales)

Average Ticket

(R$)

21

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Gross Profit and Expenses

Gross margin expansion, given better mix and inventory management

Gross Profit and Gross Margin

(R$ million, % of gross revenues)

Selling, General, Administrative and Other

Expenses1 and % of Gross Revenue

(R$ million, % of gross revenue)

(1) The figures disregard each period’s SOP expenses and “non-recurring expenses”. In 4Q11, our non-

recurring expenses came to R$3.4 million, relating to M&As.

22

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

EBITDA and Net Income

Positive EBITDA evolution since the creation of Brazil Pharma

EBITDA and EBITDA Margin

(R$ million, % of gross revenue)

44.4

70.9

4.8%

6.2%

2010 2011

Net Income and Net Margin1

(R$ million, % of gross revenue)

(1) Net income before minority interest and adjusted to exclude non-recurring expenses in the period.

29.6

16.2 20.1

45.8

2.6% 2.2%

4.0%

2010 2011

23

126 / 161 / 199

65 / 163 / 99

144 / 199 / 163

166 / 166 / 166

217 / 217 / 217

2 / 79 / 159

Contact Details

Investor Relations

Renato Lobo IR Officer

Mara Boaventura

IR Manager

(55 11) 2117 -5200

www.brazilpharma.com.br/ri

Brazil Pharma S.A.

Rua Gomes de Carvalho, 1629

6th and 7th floors

CEP 04547-006

São Paulo, SP, Brazil