Emerging Markets Insight BRAZILIAN INDUSTRY Petrobras: How to Crush a Company SPECIAL INTERVIEW Moshe A. Milevsky INDONESIAN AIR Garuda Flies High BY MIRAE ASSET FINANCIAL GROUP Q2 2013 COSMETICS, ASIAN RUSH THE ASIAN MARKET IS THE DECISIVE BATTLEGROUND FOR GLOBAL COSMETICS BRANDS. WHO WILL WIN THE BATTLE FOR BEAUTY? ❶ ASIANS DRIVE THE PREMIUM SKIN CARE MARKET ❷ ESTÉE LAUDER : ON TOP IN PRESTIGE BEAUTY MARKET ❸ L´ORÉAL DREAMS OF ONE BILLION NEW CONSUMERS

Transcript

Great Consumer!

Emerging Markets InsightBrazilian industryPetrobras: How to Crush a Company

special interviewMoshe A. Milevsky

indonesian air Garuda Flies High

by MirAe Asset FinAnCiAl GrouPQ2 2013

CosmetiCs, AsiAn Rushthe AsiAn mARket is the deCisive bAttlegRound foR globAl CosmetiCs bRAnds. Who Will Win the bAttle foR beAuty?❶ AsiAns Drive tHe PreMiuM skin CAre MArket❷ estée lAuDer : on toP in PrestiGe beAuty MArket❸ l´oréAl DreAMs oF one billion new ConsuMers

EmErging markEts insight 2

Duncan ParkLee Sang Wonkim kuk hWa marc SicheL

Yang Young heeLee hoo Shimchae Yun bYoung

kim gYung rok

Lee Sang geon

Yoon chi Sun

oh eun mi, Lee Seung a

Peter graham

hYeon-Joo Park

Editor-in-ChiEfEditors

art

PrEsidEnt

ExECutivE dirECtor

rEsEarCh fEllow

rEsEarChErs

hEad of MarkEting division

PublishEr & ChairMan

Mirae asset retireMeNt research iNstitUte

Mirae asset Global iNvestMeNts (Usa) llc

PUblished by Mirae asset FiNaNcial GroUP

The views and information discussed in this publication are as of the date of publication, are subject to change and may not reflect the current views of the writers or of Mirae Asset Global Investments (USA) LLC. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the portfolios or any securities or any sectors mentioned herein. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Mirae Asset Global Investments (USA) LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

Emerging Markets Insight is a quarterly, on-line publication of Mirae Asset Financial Group. Our editorial mission is to provide timely and actionable information about economics, finance, and business opportunity to key stakeholders in emerging market investing, particularly financial professionals, strategists and academics.

Contact us for further information on subscriptions:[email protected]

3 Briefing4 Chart & Graph5 Special Interview

Moshe A. Milevsky9 Great Consumer

Cosmetics, Asian Rush

① Asians Drive the Premium Skin Care

Market

②Estée Lauder : On Top in Prestige

Beauty Market

③L’Oréal Dreams of One Billion New

Consumers

16 New Volvo

After Volvo’s Honeymoon22 Indian Export

The Devil in the Details27 Indonesian Air

Garuda Flies High31 Brazilian Industry

Petrobras: How to Crush a Company

Q2 2013 contents

checkPoINT

Briefing

EmErging markEts insight 3

By

Jos

eph

ha

n

Positive

Improvement in US economic data- With the Us unemployment rate down to 7.7% in February, retail sales

in the Us continued to rise in excess of the forecasted numbers.- In February, Us IsM manufacturing data rose to 54.2 and the service

sector rose to 56, both above expectations. - housing Index data in the Us also showed improvement; home price,

home sales and housing starts all showed an upward trend. Expectation on Chinese new leadership - Chinese government expressed its willingness to accelerate the ‘urban-

ization’ process and boost ‘consumption,’ offsetting the lingering wor-ries on its economic hard-landing.

- expectations for a pick-up in spending across the country following spring Festival season and the annual session of the national people’s Congress held in March boosted the market over the first quarter.

Negative

US sequester officially starts on March 1st- according to the Congress’ Budget department, the sequester will

slow down the growth of economy by 0.5% and cost 750,000 jobs. The general election polls in Italy: Prolonged instability- Italy’s political deadlock after the general election is making europe

much more difficult to manage its crisis. - Would Italy continue to bow to the requested austerity demands or

would it continue with the pro-growth structural reforms? Two oppos-ing views have garnered the same amount of votes in the lower house of Italy’s parliament and in senate.

(2013.01.01 ~ 2013.03.31)

The ocean is vast because it admits hundreds of rivers.At the opening ceremony of the Boao Forum for Asia (BFA) Annual Conference 2013 held in Boao, Chinese President Xi Jinping called on countries around the world to show more openness and respect for diversity to facilitate common development.

BRICs Overview (2013.01.01 ~ 2013.03.31)

During 1Q 2013, there was a positive sentiment across the globe generally, yet there were different results by markets.

SHCOMP Index (China)

Index revised at 100

2013-01-01 2013-02-01 2013-03-01 2013-04-01

125

120

115

110

105

100

95

90

85

80

IBOV Index (Brazil)

HSCeI Index(China-H)

SPX Index (USA)

nky Index(Japan)

SX5e Index (europe)

Debt-ceiling increase issue - The debt ceiling issue (temporarily suspended) will be raised again on

May 18th.- While the national debt of the Us is currently more than 16.4 trillion

dollars, exceeding its debt limit, failure to raise the debt ceiling would have catastrophic consequences for the Us economy.

Country Highlights

China (China Shanghai composite -1.43%, H share -4.72%, Yuan FX

0.44% appreciated) - The stock market of main-land China was fueled by high expectations

about what the new government can achieve and the economy’s favorable statistics.

- China’s GDp growth rebounded in the fourth quarter of 2012 to 7.9%, after more than two years of slow down.

- premier Wen Jiabao’s comment at the national people’s Congress meeting that the country will not slacken its efforts in regulating hous-ing prices overshadowed the market.

India (Sensex composite -3.80%, FX 0.74% appreciated )- India’s 4th quarter GDp grew by 4.5%, lower than expectation of 5.5%. - Wholesale price Index (WpI) stood at 6.62% for the month of January

2013 compared to 7.18% for the previous month and 7.23% for January 2012.

- There is a low possibility of a decrease in interest rates given the con-siderable current account deficit.

Brazil (Bovespa Index -7.55%, FX 1.46% appreciated)- Worries that iron ore exports to China will decrease as China contin-

ues to regulate the real estate market had a negative effect on the Brazilian equity market.

- Brazil’s consumer price index reached a higher-than-expected level of 6.31% in March, continuing the worries over inflation. The key interest rate remains unchanged.

Russia (RTS Index -4.38%, FX 1.63% depreciated)- Both internal and external environments for Russia are still challeng-

ing: with high vulnerability to global uncertainty, considerable drops were seen in Industrial output and retail sales.

- Consumer prices accelerated to 7.3%.

EmErging markEts insight 4

Venezuela is World #1 in terms of oil reserVes

HealtH care & consumer staples are leading

global market

cHina’s goVernment to promote oVerseas

inVestment

Chart and Graph

Looking For

PatternsNumbers worth remembering.

You can find more at “Chart of the day” in an iPhone app, EM Experts, that provides unique info-graphics

about emerging markets or follow us on twitter (@emexperts).

Consumers, financials, and industrials have led the US stock markets in early 2013. Due to the rebound of the US housing market, both the financial and consumer sectors posted a rate of return higher than the market index (i.e. S&P500).

Venezuela, a nation well-known for its abundance of oil, has proved to be holding the world’s largest oil reserves. As of the end of 2011, the total value of proved oil reserves in Venezuela was 296.5 billion barrels. Saudi Arabia was close behind with 265.4 billion barrels, and Canada ranked third.

In terms of global market performance by sector, health care & consumer staples have led the entire market since the beginning of 2013. Consumer discretionary and industrials were close behind, falling short by only a small margin.

Recently, China has observed strong fund inflows to the nation’s capital markets through the QFII (Qualified Foreign Institutional Investor) system. This is highly likely to get the Chinese government to raise the quota of the QDII (Qualified Domestic Institutional Investor).

decoupling stock markets promotes diVersity

in portfolios

The correlation between the Korean stock market and the rest of the world decreased to a historic low since Aug 2012. This indicates that the Korean market may be decoupling from the global markets.

WHo is moVing tHe s&p 500?

EmErging markEts insight 5

Even in retirement, you are the engine of your financial future.

Moshe A. Milevsky

Special Interview

InvestIng In Yourself

EmErging markEts insight 6

Moshe Milevsky is a world-renowned expert on the economics of retirement.

He is an associate professor of finance at the Schulich School of Business at York University in Toronto, Ontario, Canada, and a member of the university’s graduate faculty in the department of mathematics and sta-tistics.

He has written 10 books and numerous articles on retirement planning. In addition to being a popular speaker on retirement and longevity investment issues, Milevsky is the CEO and president of the QWeMA Group, a software company that develops proprietary retirement income analysis tools.

He graduated from Yeshiva University in 1990 and received a master’s degree in Mathematics and Statistics from Nipissing University in 1992 and a Ph.D. in Business Finance from York University in 1996.

Milevsky’s 2008 book, Are You a Stock or a Bond?: Identify Your Own Human Capital for a Secure Financial Future was updated

and revised in 2012. He recently met with us to talk about the many issues the book rais-es and how these issues relate to many retir-ees.

the title of your recently updated 2008 book is Are you a Stock or a Bond? We guess that the title refers to the main theme that you try to deliver through the book. Would you say that this is accurate?

Yes. The main idea of the book is getting

investors to think about their human capital, which is their most valuable asset for most of their life. Specifically I was hoping to elicit the notion that human capital can have risk and return characteristics like financial capital. It can be risky, it can be safe or it can be bal-anced.

That is why I called the book “Are You a Stock or a Bond?” In fact, I was thinking of calling the book “Are You Cash, Stock, Bond, Real-Estate or Commodity,” which are the five major asset classes, but my publisher felt the title was too long!

In chapter 1, “You, Inc.,” unlike the tradi-tional accounting measures (the value of assets minus the value of liability), you said human capital is also an important contrib-utor in retirement strategy. regarding human capital, please explain the concept of “nest embryo” which will eventually become “nest egg.” How can we increase our human capital?

I was hoping to elicit the notion that human capital can have risk and return

characteristics like financial capital.

Special Interview

EmErging markEts insight 7

When you are young you have much potential to earn income. You may have a very small or minor nest egg (savings for retirement). But, you own a very valuable gold mine, or oil well, which is the present value of all the wages and salary you will earn for the rest of your life.

As you get within 10 to 15 years of retire-ment, you have start thinking about how the remainder of your human capital can be used to secure a safe retirement. If you want to increase the value and quantity of human capital, then you might go back to school, perhaps gain more experience or even eat healthy and sleep well! This will make you work better, more productive and increases human capital.

It is very difficult to judge the merits of debt without knowing what the debt is being used for. So, if you are 20, young and want to borrow money at a low interest rate to go to school and increase your human capital—this is good debt! On the other hand, if you are older, have existing debts and want to borrow money to buy another house or per-haps take a vacation—that is not the best debt. Also, if the interest rate is high, that makes debt worse as well. So, the answer to your question is, “What is the debt being used for?”

regarding retirement planning, what kinds of lessons were learned from the financial crisis?

We have learned about the importance of diversification, making sure that we have multiple sources of income and that we invest our financial capital (money) in a way that reflects the riskiness of our human capi-tal (job, career.) Also, you might have the desire to take risk, but you might not have the capacity to take risk. The two are quite different. Also, we have learned to be much more skeptical, cautious and “legal” when selecting investments. If it sounds too good to be true, then you are not listening carefully!

“strong desires to leave a bequest to their children” can be mentioned as one of gener-al features of retirees in some emerging Asian countries. What kind of advice can you give the retirees of these Asian coun-tries such as China, Korea?

I think that retirees that have strong pref-erences to leave large bequests to their chil-dren should ensure that they have set aside enough to take care of themselves. People will be living a very long time—much longer than they anticipated—and sometimes I worry that they are placing their bequest and legacy preferences ahead of them-selves. They must understand that retire-ment will be more costly than they think and should ensure they have enough resources to do so. I conclude by asking, “Can you afford your desires”?

Special Interview

You might start thinking about how the

remainder of your human capital

can be used to secure a safe retirement.

recently the total household debt of south Koreans has peaked. Korea experi-enced the calamitous IMf bailout in 1997, and for most Koreans “debt” is considered evil or a thing to avoid rather than a financial strategy.

But you have showed that when properly utilized and managed, debt can be a very effective component of a comprehensive financial strategy. Could you give us more detail or specific examples?

EmErging markEts insight 8

Special Interview

of the baby boom generation? And are there any industry/sectors or global com-panies which are expected to benefit from potential growth of retirement markets in emerging markets?

I am “bullishly” optimistic about the finan-cial services, insurance and pharmaceutical and health-care industries to help with the bulge of people moving into retirement. As far as countries are concerned, aging is a recent phenomenon. It is too early to tell.

As well as inflation and market volatility risks, longevity risk (outliving the income needed to support you) is mentioned as one of the biggest retirement risks in your book. Is there any risk management instru-ment you can recommend to hedge this longevity risk?

I am a very big fan of longevity insurance, pensions and lifetime income products because they enable people to hedge against the various risks they face in retirement and also provide them with the psychological ben-efits and the comfort of a secure income stream that they can’t outlive.

I am a very big fan of longevity insurance,

pensions and lifetime income products to hedge against the

various retirement risks.

fact, retirees may be consuming items—like health care or pharmaceuticals or services—that increase at a rate greater than inflation. In general, I find that the very wealthy and very poor or unfortunate tend to experience inflation rates that are higher than the aver-age, which is the middle of the income distri-bution group.

the rapid growth in emerging markets will be followed by an accelerated expan-sion of elderly people at some point. Are there any good examples of Western coun-tries which have coped well with the aging

You said the sequence of returns does matter when we withdraw retirement money. In retirement timing, does the mar-ket situation have a considerable impact on the sequence of returns for retirees? Are there any study cases to prove this?

Another way to appreciate to the impact of the sequence of returns is to examine a hypothetical situation of someone who retires and invests in a fund that earns the same average return, but one that cycles around different values. The following figure provides some examples. Notice how the amount of time the money last will depend completely on when you join the merry-go-round

You also pointed out that the most widely used Consumer Price Index cannot reflect each retiree’s personal lifestyle and experi-ence. Is there any measure to reflect one’s personal inflation rate specifically, espe-cially for the elderly (as one ages, his/her inflation rate is likely higher)?

This is a problem when inflation indices around the world tend to average many dif-ferent goods and services across many dif-ferent ages and sectors of the economy. In

100$ InItIal nest egg and spendIng

*This chart shows the number of years in which your original $100 investment lasts when you spend 6, 7 or 8 dollars each year. The more you spend, the shorter it becomes. By the way, It also depends on the market situation. If you start your retirement when it's a bull market, your investment lasts much longer than a bear market.(1) Rate of returns in first 4 years and it repeats again afterward. source: M. Milevsky “The Trigonometry of Retirement Income” Research Magazine, February 2007.

All roads lead to China. What's happening in the new frontier?

By Ahn Sol (Reserch Analyst at Mirae Asset Global Investments(HK))

ASIANS DRIVE THE PREMIUM SKIN CARE MARKET

Worldwide cosmetics sales have never declined in the past 18 years, and their annual growth rate was 4.4% between 1993 and 2011. From 2001 to 2011, the Chinese skin/cosmetics market has shown a 17.0% growth rate, and premium skin/cosmetics market has grown by an even faster rate of 22.3%. This is why China is often cited by cosmetics companies as a key market for growth. Estée Lauder, L’Oréal, Shiseido, Proctor &Gamble, etc. have been making substantial invest-ments in the country over the past decade.

Cosmetics market growth rates in China are expected to decelerate compared to the past 10 years, but we believe the industry can

EmErging markEts insight 10

Cosmetics, Asian Rush

still continue to grow by double digits and even faster for

premium cosmetics in the next five years. In addi-

tion to nominal GDP growth and popu-lation growth, urbanization will be the strong growth driver of cosmetics indus-try. Urbanization

is the top priority of the new govern-

ment in China. This is impor tant because

urbanization will not only stimulate consumer adoption of

skin care and color cosmetics but, also, urban households tend to earn higher incomes than rural households which enable consumers to trade up to more discretionary items such as premium cosmetics products.

China's AttractionEmerging market consumers need to reach

a certain level of income or GDP per capita before adoption of consumer products begin. This adoption wave typically starts with household products like detergents and soaps, extends to packaged foods such as instant noodles and then moves up to rela-tively discretionary categories, which include most personal care products. Skin care and color cosmetics are one of the later adoption categories, and deceleration occurs here gen-erally more slowly than other consumer prod-ucts. Thus, cosmetics maintain faster growth rates for a longer period. China has grown to become the largest Asian market for two gigantic beauty players, namely L’Oréal and Estée Lauder. China accounts for 7% and 5% of L’Oréal’s and Estée Lauder’s total sales respectively. And this is purely sales from mainland China. We assume Estée Lauder’s real sales from Chinese consumers to be around 15% of total company sales, as Chinese consumers will be buying Estée Lauder products in other places

like Hong Kong, New York, and Paris. Accordi-ng to Estée Lauder, every $1 spent in China implies an extra $2 in sales from Chinese out-side of China.

The Chinese cosmetics industry trend favors foreign luxury cosmetics players not only because of its faster organic growth but also because China (and Asia overall) is a more profitable market. The Asian cosmetics market is over-indexed to premium markets. In China, the premium skin care market has grown to 26% of the total skin-care market from 17% in 2001. Still, the premium market share is under-indexed to other Asian mar-kets, thus we expect China’s premium mar-ket to continue to outgrow the overall indus-try. Premium skin care has a 72% market share in Hong Kong, 59% in Taiwan, 57% in

South Korea, and 55% in Japan, whereas it is only 20% in Germany, 30% in the US, 44% in Canada and 48% in France. We believe China will follow the same path as other Asian coun-tries. This is definitely a tailwind for global cos-metics players who are well-positioned in the prestige and premium market.

Asian markets including China tend to offer higher returns for many global cosmetics players. This is because Asians spend more on skin care products that tend to have higher price points. Also, it is easier for companies to premiumize skin care products with added functions. There are more opportunities to add values on skin care products with whiten-ing, anti-aging, brightening, etc., compared to color cosmetics or fragrances. Skin care accounts for roughly 70% of the Chinese beauty market whereas it is only 35% in North America, 32% in Brazil, or 37% in Russia. This is again an Asian phenomenon as skin care accounts for 62% of the beauty market in Japan, 64% in South Korea and 62% in India. For Estée Lauder, skin care accounts for 60% in the Asia Pacific market

compared to that of 43% for the group. In China, specifically, 82% of sales were incurred from premium facial care and the rest from premium color cosmetics. Asian consumers tend to spend or invest more on skin care because of the increased cultural importance of having well-maintained skin. A significant

Asian markets including China tend to offer higher returns

for many global cosmetics players.

2006

20152011

Source : TrefisUnit : %

US

EUROPE

JAPAN

ASiA PAcific (Ex JAPAN)

middlE EASt, etc.

26.8 22.4 20.6

37.3 36.1 33.4

15.7 9.5 7.1

15.8 26.8 33.1

4.4 5.1 5.8

GlObAl SAlES Of PREStiGE cOSmEticS PROdUctS

(forecast)

EmErging markEts insight 11

Cosmetics, Asian Rush

number of women are buying LV bags in China, and we assume that these same women would be more than happy to pay a premium for their beauty.

The Men's Market Another emerging trend in cosmetics is the

fast-growing men’s grooming segment. In the past, it was almost taboo for European men to use skin care products, but this now is changing. In fact, the popularity of the men’s segment actually started in China. According to the president of L’Oréal Asia, the company saw a boom in men’s skin care in China and realized the potential for the segment globally. It has become a larger market earlier in Asia because there is no such taboo for Asian men and partly due to Asian climates, as skin care products are more of a necessity in some regions. Still, cosmetics is largely women’s category globally, but if it can be extended to men, there will be another strong demand pull for the whole industry.

Local players in Asia are generally very strong compared to those in other emerging markets. This is because many Asian coun-tries have solid competitiveness in manufac-turing, and local companies usually have bet-ter distribution networks. This is especially true for food companies. Food is an indige-nous product and locals better understand

massive advantage to MNCs as they can easi-ly leverage their global heritage brands into emerging markets. Local companies in emerging markets may somehow—albeit this is also a challenge—make a breakthrough to manufacture a good quality product, but even if they do so, they cannot build a brand story in one day. Also, MNCs tend to have stronger muscles for heavy advertisement and R&D. Particularly for cosmetics, since brand is so important, it can also be seen as an advertise-ment and marketing battle. L’Oréal and Estée Lauder spend around 30% of their sales on advertising and promotions.

The “Lipstick Effect”The cosmetics market is about aspirational

brands which provide natural moats to MNCs with many global brands. As emerging mar-ket consumers acquire higher pricing power with double-digit wage growth in China, con-sumption trade-up will increasingly benefit global cosmetics companies. Such character-istics are evidenced by the top 12 Beauty and Personal Care (B&PC) companies having a more-than 50% global market share com-pared to that of only a 17% share for the top 15 global food and beverage (F&B) compa-nies. The prestige and premium cosmetics market will continue to be a game between only a handful of global companies, just like other luxury goods.

Cosmetics is a unique category, having both staples and discretionary characteristics, and even luxury characteristics for prestige/premium cosmetics. It is a consumer staple because women (soon perhaps men as well) have to use cosmetics every day once they start using them. At the same time, consum-ers trade up to premium brands along with an increase in discretionary income. In a reces-sion, women tend to satisfy their luxury demand with lower-ticket-price items and typically they buy prestige cosmetics. This is the so-called “lipstick effect.” Thus, cosmetics category growth is usually faster than other consumer staples goods in a good economy and it also tends to be more defensive than luxury goods growth in slow economy.

their region’s tastes. We believe, however, that multinational corporations (MNCs) have stronger moats in the household beauty and personal care (HPC) business especially when it comes to luxury or high-end consumer goods because then it becomes more of a brand game. Global cosmetics players well understand such phenomena and thus invest significantly in emerging markets.

HPC is a purely brand business as a product itself is homogeneous and does not require much localization unlike food. This provides a

MNCs have stronger moats in the household beauty and personal care (HPC) business.

GlObAl HPc ExPENditURE by cAtEGORy, 2011

Sources : Euromonitor, Bernstein analysis

total HPc: $925bn

beauty &Personal care

$414bn

45%

Home care$142bn 15%

consumer Health$198bn

21%

Hygiene$171bn

19%

EmErging markEts insight 12

Cosmetics, Asian Rush

Estée Lauder is the second-largest cos-metics company in the world, but the only multinational corporation offering pure-play exposure to the prestige beauty market. This $160 billion industry is projected to grow at an annual rate of 4-5% through 2015, while Estée projects its sales will grow twice as fast over the same period . The company stands to benefit from long-term

structural trends in the global marketplace, such as emerging market consumption growth and the expansion and premiumiza-tion of the personal care industry.

Wide exposure to a fast-growing and highly profitable segment of the global per-sonal care market differentiates Estée from its peers. Whereas the company’s main competitor, L’Oréal, receives 60% of its sales

from the mass beauty market, Estée oper-ates solely in the premium prestige beauty realm. As prestige beauty sales continue to outpace mass beauty spending on a global basis, the company is benefiting from the secular growth of the industry.

Competitive StrategyOne of the company’s long-term strategic

priorities is to focus its resources on markets with the greatest growth potential and most attractive consumer demographics. China has been one of the world’s fastest-growing

on Top in preSTige BeauTy MarkeT

EstéE LaudErEstéE LaudErEstéE LaudEr

Its sales are expected to grow twice as fast as the rest of the beauty industry. By Mirae Asset US research team, Photos by SHUTTERSTOCK

China5.3%

Japan5.2%

Korea3%

Hong Kong2%

Taiwan2%

Others4%

US 43%Asia Pacific 21%

Europe,Etc. 37%

2013 Estée Lauder Global Sales Forecast

Source : Estée Lauder, Bernstein estimates

EmErging markEts insight 13

Cosmetics, Asian Rush

personal-care markets over the past decade, and Estée Lauder CEO Fabrizio Freda has declared his intent to make it the company’s “second home market .” While the global beauty market has grown by 5% annually over the past 10 years, the Chinese beauty market has expanded by 12% per annum over the same period. Prestige beauty has proven to be a particularly dynamic segment of the industry in China, growing in excess of 20% each year.

Skincare has been a key catalyst for pres-tige beauty growth in China. Asian consum-ers tend to have more sophisticated skincare regimes compared to their global counter-parts. An Asian woman, on average, will use eight different skincare products each day, including special products like whitening creams . A recent survey by China Reality Research found that middle-class Chinese women are much more likely to trade up in their beauty regimen, rather than trade down in order to save money. The Chinese consumer is most aspirational in terms of skincare, as an overwhelming 68% surveyed said they would trade up compared to only 2% planning to trade down.

Fast-growing Skincare MarketSkincare is a major strength for Estée

Lauder, as it is the company’s most profitable and fastest-growing product segment. As such, the company has largely focused its innovation and advertising efforts in this area. In the fall of 2012, Estée launched a luxury skincare line specifically targeting the local preferences of Chinese consumers, in hopes to further penetrate the most impor-tant market for the category globally. Osiao, as the brand is known, was developed over a five-year period with dedicated R&D special-ists in Shanghai who extensively studied dif-ferent types of Asian skin and téd the prod-uct on several thousand women across the region. The company has ambitions for Osiao to become one of the major brands of its Asian portfolio.

A booming travel trend among emerging

market consumers is yet another growth driver for the prestige cosmetics industry. Estée Lauder has been able to capitalize on the trend by shifting some of the focus away from its traditional department store busi-ness model toward faster-growing, more profitable channels, like travel retail.

The company’s travel retail business has become an especially important driver of earnings growth in recent years, as it has emerged as a key beneficiary of increased travel rates in Asia. Over the past decade, Chinese outbound travel activity has grown by more than 20% each year and is antici-pated to rise by 15% annually over the next decade to more than 100 million people . While traveling, consumers have an increased proclivity to shop, whether in air-port retail or downtown stores. And brands

with strong recognition in their home market are more likely to be purchased by consum-ers when traveling abroad. Because of this, increased travel trends largely benefit multi-national cosmetics companies with strong brand equity, like Estée Lauder. The compa-ny recently cited that for every $1 worth of cosmetics sold in China, it is able to generate $2 abroad from Chinese consumers . As travel retail trends continue to grow, Estée Lauder’s sales figures should follow closely in line.

Estée Lauder offers a sustainable competi-tive advantage over its peers operating in the personal care industry due to its pure-play exposure to the prestige beauty mar-ket, strong geographic footprint in emerging economies, and increased focus on high-growth, high-margin product categories and retail channels. The company is well-posi-tioned to benefit from the secular tailwinds of the rising emerging market consumer, and it continues to invest more heavily in the busi-ness to gain market share globally.

We believe this is one of the strongest global growth stories taking place in the market today and will be following the com-pany closely in years to come.

Estée Lauder is well-positioned to benefit from the secular

tailwinds of the rising emerging market consumer.

Skin Care: Best Performing in Chinese Premium Category

Source : Euromonitor, UBS Reasearch Skincare Makeup Fragrances Hair etc.

2001

3,500

3,000

2,500

2,000

1,500

1,000

500

02011

63% of Total53% of Total

Sales (Euro Million)

EmErging markEts insight 14

Cosmetics, Asian Rush

enable L’Oréal to reach this goal. Home and personal care is an $820 billion global indus-try with a projected annual growth rate of 6.4% through 2020, up from 5.1% from 2001-2011. Emerging economies of Asia and the Middle East/Africa are expected to drive 60% and 27% of this growth, respectively. As these countries develop and their con-sumption levels converge with those of more mature markets, it is estimated the industry could be six times as large—nearly $5 trillion globally. Personal care currently accounts for nearly half of the industry’s sales and has the highest expected growth rate among all sub-segments, with beauty products emerging

as a clear winner . L’Oréal is expected to benefit from the

global growth of the home and personal care industry. Revenue growth of personal care companies correlates highly to increasing income and consumption levels in emerging markets.

Global ReachTherefore, exposure to growth is largely

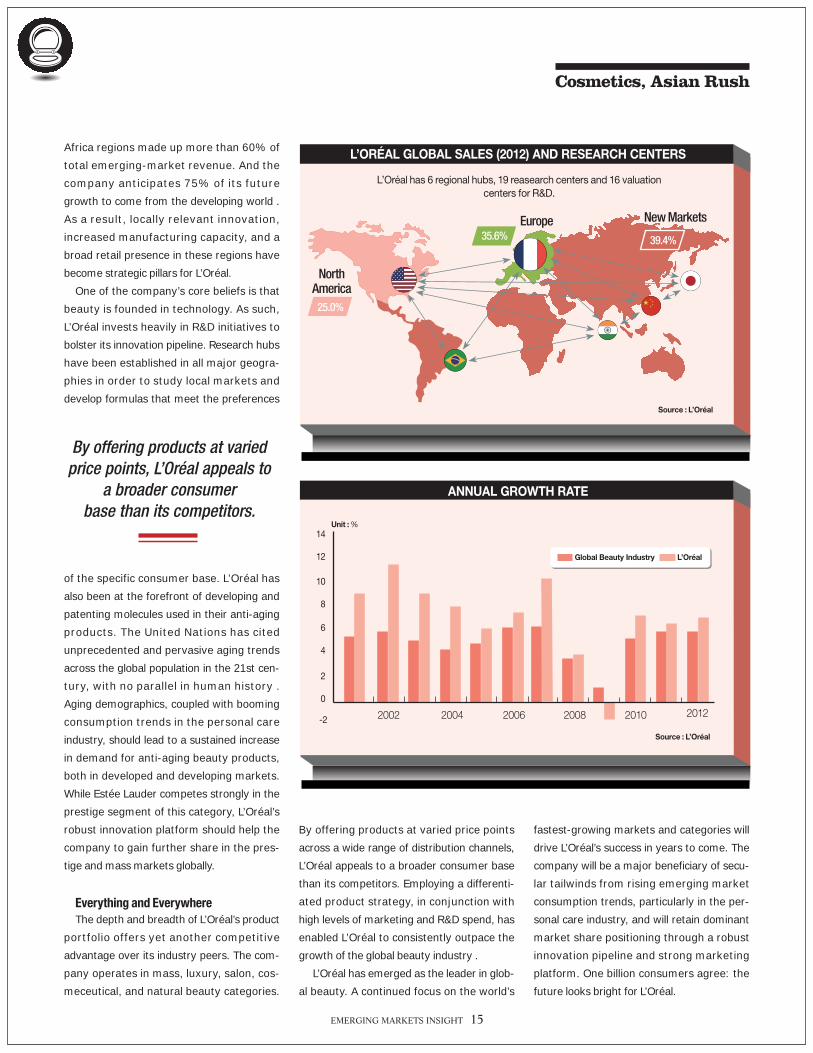

determined by a company’s geographic foot-print. In 2012, emerging markets accounted for almost 40% of L’Oréal’s total sales, with a growth rate of nearly 10% on a year-over-year basis. Asia Pacific and Middle East/

DReams of one Billion new ConsumeRs

L´ORÉALL´ORÉAL

As L’Oréal operates in categories across the beauty spectrum, the company is able to reach more consumers relative to its competitors and retain dominant market-share positioning.By Mirae Asset US research team

L’Oréal is a global beauty powerhouse. With $26 billion in annual sales last year, the company enjoys a commanding market share advantage over its competitors in the home and personal care industry, such as Proctor & Gamble, Unilever, and Estée Lauder. The company boasts a broad pres-ence globally, with operations in 130 coun-tries across 27 international brands.

Over the next decade, the company is tar-geting one billion new customers. Secular growth trends in the global personal care industry, increased investments in innova-tion and marketing efforts and a focus on growth markets and categories should

EmErging markEts insight 15

Cosmetics, Asian Rush

Africa regions made up more than 60% of total emerging-market revenue. And the company anticipates 75% of its future growth to come from the developing world . As a result, locally relevant innovation, increased manufacturing capacity, and a broad retail presence in these regions have become strategic pillars for L’Oréal.

One of the company’s core beliefs is that beauty is founded in technology. As such, L’Oréal invests heavily in R&D initiatives to bolster its innovation pipeline. Research hubs have been established in all major geogra-phies in order to study local markets and develop formulas that meet the preferences

of the specific consumer base. L’Oréal has also been at the forefront of developing and patenting molecules used in their anti-aging products. The United Nations has cited unprecedented and pervasive aging trends across the global population in the 21st cen-tury, with no parallel in human history . Aging demographics, coupled with booming consumption trends in the personal care industry, should lead to a sustained increase in demand for anti-aging beauty products, both in developed and developing markets. While Estée Lauder competes strongly in the prestige segment of this category, L’Oréal’s robust innovation platform should help the company to gain further share in the pres-tige and mass markets globally.

everything and everywhereThe depth and breadth of L’Oréal’s product

portfolio offers yet another competitive advantage over its industry peers. The com-pany operates in mass, luxury, salon, cos-meceutical, and natural beauty categories.

By offering products at varied price points across a wide range of distribution channels, L’Oréal appeals to a broader consumer base than its competitors. Employing a differenti-ated product strategy, in conjunction with high levels of marketing and R&D spend, has enabled L’Oréal to consistently outpace the growth of the global beauty industry .

L’Oréal has emerged as the leader in glob-al beauty. A continued focus on the world’s

By offering products at varied price points, L’Oréal appeals to

a broader consumer base than its competitors.

fastest-growing markets and categories will drive L’Oréal’s success in years to come. The company will be a major beneficiary of secu-lar tailwinds from rising emerging market consumption trends, particularly in the per-sonal care industry, and will retain dominant market share positioning through a robust innovation pipeline and strong marketing platform. One billion consumers agree: the future looks bright for L’Oréal.

L’OréaL gLObaL saLes (2012) and research centers

L’Oréal has 6 regional hubs, 19 reasearch centers and 16 valuation centers for R&D.

North America25.0%

39.4%35.6%Europe New Markets

source : L’Oréal

global beauty Industry L’Oréal

2002 2004 2006 2008 2010 2012

14

12

10

8

6

4

2

0

-2

annuaL grOwth rate

source : L’Oréal

unit : %

New Volvo

SYN

DIC

ATIO

N/C

hIN

A e

NTr

epr

eNeu

r, p

hO

TO/G

eTTY

IMA

GeS

, CFpAfter

Volvo’s HoneymoonIt’s been more than two years since Geely, the Chinese carmaker, took over Volvo. Now the company feels that it is on firm footing to meet new challenges. By Yang Jing

EmErging markEts insight 17

On a weekend morning, we sat in a coffee shop with some Swedish friends. The shop is located on the famous Kungsportsavenyn in Gothenburg. It is a bit like some of the streets in Hong Kong; it has trams running down the middle of the road with cars going by on either side. At 10 a.m., the shops had just opened for business and there were a few people on the street. A friend said: “I bet that more than 90 percent of the people reading the newspapers are supporting the acquisi-tion of Volvo by the Chinese company Geely. Do you believe it or not?”

We didn’t’ take the bet. Since our arrival in Sweden, we had posed the question many times, learning that a large proportion of the people considered the acquisition in April 2010 as a “success.”

Even the board of directors of Volvo Cars

(hereafter referred to as Volvo) has felt the same affirmative support. At the end of 2011, the board decided to close a joint-venture fac-tory. At that time, a director joked that some

media would soon report that Geely had shut down a factory after purchasing Volvo. The board was worried that its business decision would cause a public scandal. Gothenburg has a population of 500,000 people, with 70% of them related to Volvo directly or indirectly.

Even the slightest change in the company would be easily noticed by the Swedish peo-ple.

Unexpectedly, nothing bad happened. “It reflects to some extent that the Swedes believe that this is a management team solv-ing problems using commercial common sense,” said Yuan Xiaolin, head of the Office of Chairman at the Volvo Group headquarters. In 2009, he joined Geely Group as M&A Director, targeting the acquisition of Volvo, and has since stayed in Sweden for almost three years now.

It was cold in Gothenburg in early November 2012. After several rounds of rain, the sky was gloomy. Volvo was not as calm as it may have appeared, as it had just experi-enced the first major change in management since Geely’s acquisition of the company.

We had posed the question many times, learning that

a lot of people considered the acquisition as a “success.”

New Volvo

President and CEO Hakan Samuelsson: “China is our most important sales market, and we must help Volvo’s growth plans in China return to the right track.”

New Volvo

EmErging markEts insight 18

Local and global media had divergent views on the deal. But more noticeably, compared to its profits in 2010 and 2011 when it had just been acquired, Volvo’s performance in 2012 was not ideal—its earnings had fallen sharply. More than two years after the acqui-sition, Volvo’s China plan is still teetering.

“It seems nothing happened after the acquisition. Nothing happened in China either.” Yuan Xiaolin has often heard worries and remarks like these.

But in his eyes, Volvo has experienced mul-tiple twists and turns over the past two-plus years, changes that Volvo had not experi-enced for many years. Some of the changes were quite radical. Volvo has found success over these same two years, a fact overlooked by outsiders. Yuan compared this to a half glass of water: we see it half full, while others see it half empty, when in fact both state-ments are accurate.

At present, the Volvo board has set a goal for the company’s future growth: global sales volume is set to increase to 800,000 vehicles from 500,000 vehicles. Geely Chairman Li Shufu has set 2020 as the deadline for this goal. The individual responsible for reaching this goal is new President and CEO Hakan Samuelsson. Yuan Xiaolin admitted that for Volvo’s future, either Li Shufu or Samuelsson will be facing huge challenges and that chang-es in the external environment increased the risks for Volvo in adjusting for any such changes.

“We need to choose what to do and what not to do to be at par with competitors. We do not only live for today’s performance results. Every auto company is facing enormous chal-lenges, and there are times that you have to make your choice: A or B,” said Yuan in explaining the difficult situation Volvo is in.

As was expected by Li Shufu, the acquisi-tion was only the first step on a long path, and the rescue is far from over. A few years from now, the most prominent aspect of Li’s record overseeing this acquisition may be that he successfully persuaded the Swedish employ-ees to accept a Chinese company without destroying their team morale. Well, can the

larly in its IT systems. In his opinion, the old Volvo, whether con-

sidered as a part of AB Volvo or later as a part of Ford, was only a small section of a giant company. AB Volvo is Sweden’s largest public company, while Ford is one of the world’s leading auto companies. Volvo was only a small part of the bigger company and received a very limited level of attention and support compared to the situation now. Although acquired by Geely, Volvo in fact is a much bigger company than Geely. Volvo Car, as an independent company, first had to be separated from Ford in order to continue on, which was not an easy task. “A lot of people do not realize how complicated it can be.”

According to a press release from Volvo, the handover after the acquisition was real-ized on Aug. 2, 2010, meaning most of the work was declared to be complete, but in fact Volvo was not fully separated from Ford until almost 10 months later, in June 2011.

During those 10 months, the top manage-ment team took great pains in separating the companies. “In brief, when a couple gets divorced, they will sign an agreement on the divorce and division of property. However, the devil is in the details. It is hard to tell exactly what inside the house belongs to me and what to you,” said Yuan Xiaolin, drawing an analogy. He tried to explain that Volvo had developed a deep Ford imprint during its 10 years of administration under Ford, and its systems were tightly linked to Ford’s.

story continue? Can Volvo really thrive again in the hands of this company coming from the Orient?

Separation Volvo headquarters, about 12 km from the

city center, are located on Hisingen Island, northwest of Gothenburg. It is known as

Volvo Town. The AB Volvo headquarters nests in a low three-story building on a hill. One can walk down to the Geely Volvo facili-ties along a narrow path.

Volvo belonged to the AB Volvo company located on that hill until 1998. At the begin-ning of 1999, Ford acquired Volvo Car at a cost of $6.4 billion. Ten years later, the com-pany again changed hands as the Geely Group took over Volvo from Ford in March 2010 at a price of $1.8 billion.

What are Volvo’s biggest changes during the past two-plus years? Yuan Xiaolin believes one is that Volvo has successfully separated itself from the original Ford system, particu-

Yuan Xiaolin believes that Volvo has successfully separated

itself from the original Ford system, particularly

in its IT systems.

volvo’s Global sales and operatinG profit 2010-2012

373.4449.3

221.3

2010 2011 2012

113 125 65

source : Volvo

Unit : 1,000

Unit : billion krona

EmErging markEts insight 19

A variety of problems were waiting to be solved. One arose out of a certain software system. Before the acquisition, in the Ford family, Volvo had been using the Microsoft Windows operating system and related soft-ware. Every time Microsoft updated the oper-ating system, Ford would pay for the new version to keep the entire IT system running smoothly. After its separation from Ford, Microsoft raised the price for new Windows updates. In the past, Volvo had only about 20,000 employees among the roughly 400,000 in the Ford family. How much should Volvo pay for Microsoft’s new software sys-tem? What service range should be covered? All of these agreements needed to be renego-tiated between Microsoft and Volvo.

Li Shufu’s team had done substantial homework for the M&A. Almost everyone on

Volvo had been integrated in the Ford system for nearly 10 years. Now, the Volvo board had to rebuild operational processes more suited to its needs, which involved a number of third-party suppliers. For an auto company, the R&D division is the top commercial secret in the entire IT system. According to an expert familiar with M&As in the automotive industry, Tata in India bought Ford’s Jaguar and Land Rover in 2008. Switching IT sys-tems was also an issue for integrating those companies. Tata hired technical and legal con-sultants, but failed to solve the issue despite six months of efforts. As of November 2012, Jaguar and Land Rover were still using Ford’s IT system.

Learning from the past, as the former larg-est shareholder of Volvo, Ford played an important role in Volvo’s separation from

the team has experience in mergers and acquisitions. They are all veterans, knowing that any M&A case consists of five core areas: finance, legal, auditing, environmental protec-tion and the IT system. All of these areas are

in need of independent negotiations, with the IT system being a particular challenge.

The IT system is almost equivalent in func-tion to the nervous system of a company.

As the former largest shareholder of Volvo, Ford played an important role

in Volvo’s separation from Ford’s IT systems.

Geely Chairman, Li Shufu attended the 2011 National People’s Congress in Beijing with his new Volvo cars.

New Volvo

New Volvo

EmErging markEts insight 20

expert who has observed Volvo over the long term commented that before Volvo’s acquisi-tion by Geely, the Volvo board was a name on paper only. In fact, all resolutions affecting Volvo could be made in the absence of the Volvo board. No resolutions were produced as the results of Volvo board meetings. “We must re-establish the governance framework, board of shareholders, board of directors and management,” Yuan Xiaolin expressed. “Then, we can really entrust the governance framework with responsibilities and roles.”

The members of the board are the key. When Li Shufu decided to acquire Volvo, he sent a signal that he had no preconceived ideas regarding the origins of new board

members. He hoped that the board members as a body would possess the capacity to be a business generalist that could manage change and turn the tide for the company.

On Aug. 3, 2010, after a global screening and recruitment process, the new Volvo board made its debut appearance at the han-dover. Li Shufu took the post of Volvo Chairman, Stefan Jacoby, former CEO of Volkswagen North America, became the new Volvo President and Global CEO. 70-year-old Hans-Olov Olsson, former President and CEO of Volvo and CMO of Ford Motor Company, was hired as Vice Chairman of Volvo to hold the line. Volvo board members also included 59-year-old Hakan Samuelsson, former Chairman and CEO of the commercial vehicle giant MAN Group; 56-year-old Dr. Herbert H. Demel, former Audi Chairman and Fiat CEO;

and Shen Hui, former VP of Fiat China. Learning from the lessons of the board dur-

ing the Ford period, the new board took a dis-ciplined approach, holding six meetings a year, or a meeting every two months on average. Each meeting generally lasted for two days, allowing preparatory meetings on the first day, attended by all board members and members of subcommittees, such as the Remuneration Committee and Audit Committee. The Formal board meeting was held on the second day to discuss the compa-ny’s major strategic and business decisions, aiming at a collective discussion on major decisions.

But the reality was different. Rumor had it that the Volvo board members had been fighting with each other from the day the board was re-established. Swedish tabloids often reported that Stefan Jacoby and Vice Chairman Hans-Olov Olsson got into a fight. Then, a tabloid claimed that the fight contin-ued. Another rumor was that Hans-Olov Olsson took personal interest and rights from Volvo in favoring his son-in-law (though Olsson’s son-in-law did work in Volvo). These ungrounded messages sent a signal to Volvo employees that Volvo was still struggling, and search of a new direction.

“[Olsson] has spent his life with Volvo. If he wants to fight for his self-interest, there would have been a variety of evidence. But no signs indicate that he is not a man of integrity.” Yuan said, “We work together, so I know what could happen and what could not. These are rumors.” During a nearly three-hour interview, Yuan Xiaolin rarely discussed his emotions. However, when it came to the topic of the rumors, he said: “I really feel helpless and quite angry.”

Jacoby’s departure at the end of 2012 is a major event in Li Shufu’s exploration of the Volvo governance structure. In the interview, Yuan Xiaolin did not comment on Jacoby’s departure, said to be due to his health, as it was put in the company’s official statements.

Yuan added that Volkswagen is a bench-mark for Geely Group, and Geely had its eye on Jacoby when selecting the Volvo manage-

Ford’s IT systems. Yuan Xiaolin commented: “They have performed very detailed work.”

Ford, Volvo and software service providers quickly built a small team. On the one hand, they extracted each module of Volvo’s; on the other hand, they had to ensure that Volvo’s R&D system, production system and sales system could run as usual in the process of each module separation and at the point of disconnection from the Ford IT system. Fortunately, Volvo was able to complete this separation successfully.

Governance Besides separating from Ford and gradually

adapting to its new owner, the most impor-tant job for Volvo over the past two years has been reviving its fortunes in global business. These efforts, however, have not gone as well.

First, Volvo reorganized its board which had been weakened under the Ford regime. Its new owners recognized that Volvo, being larger in size than Geely, would need to have the chance to examine what it wants to be and how to fill the gap in reaching its future goals. However, there was also a practical problem: What is final course after the strate-gies have been mapped out? The core issue was how to govern the company.

Even Geely admitted that, in today’s auto industry and global market, basically no one dares claim that they know exactly what they should do, especially ill-fated Volvo. According to Li Shufu’s understanding, confronting these issues requires a governance structure. This structure can help answer these questions by forming a consensus and making joint deci-sions rather than permitting a dictatorship of shareholders to guarantee the “right” direc-tion.

Previously, the Volvo board was hard put to exercise influence in the decision making over the fate of the company. Ford set up a sales company in China only after it decided to sell off Volvo in 2009. Moreover, the Ford board seldom discussed Volvo issues independently. “Let’s devote 15 minutes to Volvo,” was the kind attitude it had. What wishful thinking! An

Swedish tabloids often reported that Stefan Jacoby and

Vice Chairman Hans-Olov Olsson got into a fight.

New Volvo

EmErging markEts insight 21

ment. Later, it was shown that Jacoby did fulfill his capacity in the reorganization pro-cess. Soon after the acquisition, someone was needed to lead the enterprise and rouse the spirit of Volvo staff so that they were aware of the company’s future direction. “But two years later, what we need is a lead-er of powerful executive ability and experi-ence to ensure the implementation of the strategy and planning that we have worked out,” Yuan Xiaolin said. He added that the board discussed and agreed that Samuelsson would be the best fit in this regard.

After the acquisition and once Geely was in posses-sion of the well-known, yet crisis-ridden auto compa-ny, Li Shufu, as a busi-nessman, clearly hoped to adopt Western rules on governance and has made his greatest efforts to follow that course of action. But he needed more exploration and wis-dom, as well as rebuilding the delicate rela-tionship between shareholders and profes-sional managers in the West to manage the company and achieve his intentions follow-ing the Western governance structure.

For example, at present, of the 11 mem-bers of the Volvo board, other than Li Shufu, Huo Jianhua and the CEO, three directors are from the labor union and five are inde-pendent directors. These eight directors are not involved in company management and operations, which means for day-to-day management, the CEO plays a pivotal role and actually controls the entire company.

According to Li Shufu, two years ago, Jacoby was determined to be the most suit-able CEO candidate during a 30-minute meeting, and was fully trusted. But as it stands now, the Volvo board is not satisfied with Jacoby’s implementation of the estab-lished strategy. There were even rumors that Jacoby had defined Geely as strictly a financial investor, and thought he alone should be the one making decisions on the

company’s operations. It is common to see conflicts between

Chinese and Western management ideas after an acquisition made for the internation-alization of Chinese enterprises. Lenovo has replaced two CEOs in succession due to per-ceived egotism and arbitrariness after acquir-ing IBM’s PC business.

Most likely, the “outsider” Jacoby was asked to leave. His successor Samuelsson and Li Shufu share common thoughts on strategy and execution. “China is our most

important sales market, and we must help Volvo’s growth plans in China return to the right track,” Samuelson announced after assuming his current position.

Challenges AheadIn the eyes of Yuan Xiaolin, the biggest

risk for Volvo’s in the future is the surround-ing economic environment. He explained: “Volvo’s qualitative change ties in with its greater development. It will be easier if the economic environment permits.” If the envi-ronment continues to deteriorate, it will undoubtedly have a great impact on Volvo.

In his view, after more than two years of implementation, the governance structure, as established by Volvo, has gained energy

and been able to respond to external and internal events.

During our interviews, many people who were familiar with Volvo expressed that Volvo, after being under the wings of a large company for many years, has to tackle many issues and is now facing a test of its own survival as a going business concern. A top manager of Geely Group remarked: “No company has unlimited resources to invest regardless of profit or not. Some companies can do so, but we can’t afford it. Volvo is not

such a company, nor is Geely.” Volvo would like to survive in a truly competitive market.

In fact, the board well knew the reasons for the improved earnings seen in 2010 and 2011. First, it is a general trend; second, Ford had fully prepared for the

divestment, including the establishment of a dedicated

sales company in China. In other words, Volvo has a complete system

to ensure its survival; and third, the board has trusted the right people with developing its corporate goals.

Yuan Xiaolin met sometimes with Li Shufu when participating in the board meetings. “My impression of Li Shufu is completely dif-ferent from what I see in the media. He always has a clear mind on what he wants and what goals to achieve. In other words, you can anticipate something from him and you will not be surprised, which is why the Swedes respect him.” In the eyes of the for-mer diplomat, Li is an entrepreneur that can do great things.

After signing the M&A contract, Yuan Xiaolin has been stationed in Gothenburg. In the nearly three years there, he has become one of those individuals who know Volvo best. Once, Yuan Xiaolin told his friends that this is historically significant in the develop-ment of China’s auto industry. “We are happy to be part of it. In the future, we can tell our children and grandchildren just this. Do you know that we participated in it?”

Li Shufu hoped to adopt Western rules on governance and has made his greatest efforts to follow that course of action.

The Devil in The DeTailsIndia must learn to deal with an ever-growing number of visible and invisible non-tariff barriers if its exports are to thrive. By Joe C. Mathew

SYN

DIC

ATIO

N/B

US

INES

SW

OR

LD, p

hO

TOS

/Sh

UTT

ERS

TOC

k

Indian Export

So many new regulations are

impacting India’s export.

EmErging markEts insight 22

EmErging markEts insight 23

Indian Export

Seven months ago, over 100,000 families engaged in fish farming in West Bengal and Orissa were dealt a rude shock when ship-ments of their most valuable export—black tiger shrimp—were rejected by Japan, the biggest market for the product. Japan’s food safety commission had decided to lower the permissible level of ethoxyquin in fish prod-ucts. A key ingredient in shrimp feed, etho-xyquin is a preservative that enhances the shelf life of shrimp by weeks.

In 2011-12, India exported marine prod-ucts worth $456 million to Japan. However, since August 2012, more than 100 Indian shrimp cargoes to Japan have been rejected and dozens of orders cancelled as a result of the lowering of permissible ethoxyquin levels in fish products to 0.01 parts per billion (ppb), causing a 16% fall in shrimp exports. The resultant glut in the domestic market has led to a 25-30% dip in shrimp prices.

The farmers’ woes have not ended there. Alternative shrimp feeds have added to their costs as well as reducing the shelf life of shrimp and making their produce less com-petitive in the price-sensitive global market.

On Dec. 28, the US International Trade Commission initiated a probe against shrimp exporters from India and six other countries following complaints that the products they were selling in the US had been subsidized by their governments, giving them a cost advantage. According to the Seafood Exporters Association of India (SEAI), if the charges are proved, Indian shrimp exporters may have to cough up as much as 21% of the value of exports as countervailing duties in the US. “An adverse verdict will hit us hard, as the payment can be as high as $1.5 million,” said Sandu Joseph, SEAI’s secretary.

These developments can cause a huge setback to India’s export of marine products. Shrimp is a major component of India’s marine exports to Japan and accounts for one-fourth of the country’s $1.7 billion marine exports to the US.

Such problems are not confined to marine exports alone. Hundreds of similar mea-sures, in the garb of health safety, environ-

address environment and human safety issues, has increased the cost of compliance by 85,000 Euros to 325,000 Euros per chemical. According to the Chemicals Export Promotion Council (Chemexcil), the law has made registration very expensive and, as a result, Indian firms could register only 35 substances out of 312 chemical products covered under REACH in the first phase.

The second phase of registration for 1,084 chemicals is due this year. About 6,000 sub-stances will be covered in the last phase in 2018. Measures such as these are known as technical barriers to trade (TBT).

“Industry has no choice but to go for re-registration of products. But a large number of firms did not go for registration in the first phase due to high costs and many may not go for registration during the second and third phases, which will impact our exports to the EU,” said SatishWagh, chairman of Chemexcil. Indian exports of chemical and related products were worth over $240,000 during April-October 2012.

In May 2012, when then-US Secretary of State Hillary Clinton visited New Delhi, then-Foreign Minister S.M. Krishna conveyed to her India’s IT companies’ concerns over mobility of professionals and protectionist sentiments in the US. Krishna may not have called those as NTBs, but he did express India’s concern over the business lost due to a barrier that discouraged short-term job visas for professionals in the services sector in the US.

Again, if the EU declares India a “data-se-cure” country, it is estimated that outsourc-ing to the region could zoom to $50 billion from $20 billion now. Under EU laws, firms that outsource jobs to countries that are not “data secure” have to sign stringent con-tracts with clients. The measures increase operating costs of companies, rendering such places unattractive.

Roadblocks for automomakersOver the past six years, the Society of

Indian Automobile Manufacturers (SIAM) and its counterparts in Brazil, Canada, EU,

The [government's] efforts may not prove fruitful unless hidden trade barriers... are

dealt with effectively.

10 products account for 97% of India’s exports

leading the charge

Commodity apr~nov 2011 apr~nov 2012* Growth(%)

Engineering 32,429 35,730 10%

Petroleum 31,659 34,442 9%

Gems, jewellery

26,828 28,431 6%

Chemicals & others

21,598 27,002 25%

Agri & others 13,415 21,162 58%

Textiles 14,928 16,362 10%

Electronic 4,999 5,544 11%

Unclassified exports

10,956 4,001 -63%

Ores, minerals

4,389 3,583 -18%

Leather products

2,715 3,094 14%

Unit: million USD *Provisional estimates Source: DGCIS Kolkata

mental protection and the adoption of ethical standards, among others, are affecting the growth of exports in dozens of areas, includ-ing agriculture, automobiles, pharmaceuti-cals, chemicals, textiles, information technol-ogy (IT), etc. The loss—though no official statistics quantifies it—is expected to be sev-eral billion dollars a year.

Already, India is making efforts to halt the decline in its export growth (export revenues fell 4.17% to $22.3 billion in November 2012, falling seven months in a row).

In December, the commerce ministry announced measures to spur growth in exports. But trade experts say these efforts may not prove fruitful unless hidden trade barriers, broadly termed as non-tariff barri-ers (NTB), are dealt with effectively.

Recent European Union legislation called Registration, Evaluation and Authorisation of Chemicals (REACH), which is meant to

EmErging markEts insight 24

Indian Export

Japan, Korea and the US have time and again requested the intervention of the World Trade Organization (WTO) to end trade disruptions caused by NTBs. According to a working group of these associations, which represent 85% of global motor vehicle production, removal of NTBs will give devel-oping countries better access to global mar-kets and secure new investment in product and technology.

“SIAM, along with others, approached the WTO and various groups to underline the importance of addressing NTBs. But nothing

has happened till now,” said a senior SIAM official. Inconsistency in customs valuations, discriminatory licensing and quota practices, auto standards and technical regulations, intellectual property issues—NTBs cited by the automotive industry are plenty. Perhaps this is why vehicles manufactured in India are not seen on the US and European roads.

Most non-tariff measures (NTMs) target agricultural and related products. The com-merce ministry lists about 70 specific instances in the form of sanitary and phyto-sanitary or SPS measures (broadly, food

safety and animal and plant health mea-sures). They include high standards that pre-vent milk exports to the EU, impractical plant quarantine procedures for flowers in Columbia, biosecurity issues connected with pomegranate exports to New Zealand, and documentation, certification and other issues that restrict tea exports to Iran, Iraq and Libya.

Indian rice exporters regularly face phyto-sanitary hurdles in the EU, the US, Japan, Russia, and several West Asian countries. In the US, Indian basmati rice faces more hur-dles than any other category, giving rise to suspicion that SPS measures are used to “protect domestic producers of high-cost rice, which are often passed-off as basmati,” according to a report by the Centre of WTO Studies at the Indian Institute of Foreign Trade.

The First victimThe Indian textile sector was the first to be

subjected to NTBs. In fact, NTBs began to be introduced only from 1993 onward, after the WTO founding members decided to end all bilateral quotas within 10 years of the WTO coming into force. Bilateral quotas had been in existence since 1961, and referred to a system whereby developed countries such

as the US and Canada had fixed quotas for the import of textile products from each developing country.

The decades-old “azo dye” controversy, in which the dye’s use was prohibited by importers on grounds of health concerns was an early example. Today, NTBs in tex-tiles is an old story. Importing nations have introduced ever more sophisticated trade barriers that cannot be challenged even under the WTO system, said D.K. Nair, sec-retary general of the Confederation of Indian Textile Industry. “You can only challenge a

trade barrier enforced by a government under the WTO system. You are defenseless if the barrier is imposed through individual contracts that an importer signs with his sourcing firm.”

Increasingly, importers are making suppli-ers sign a code of ethics. If it were uniform for all exporters, it would be reasonable, but problems arise when it is not uniform across exporters. “If there are 10 buyers and 10 codes of ethics, all can be different, and even be contradictory, requiring a large body of regulations to be followed by the exporter, which, in turn, make his produce more expensive and less competitive in the global market,” said Nair. To make matters worse, “some norms are not being followed or enforced across countries by the same com-panies,” he added.

Global scenario According to the WTO, NTMs contribute

much more than tariffs to overall trade restrictiveness. Any country can announce NTMs for genuine health or environment safety goals. The WTO allows such restric-tions. But the reasons behind such barriers are not always backed by scientific evidence, according to Indian seafood exporters. “They reflect public policy goals, but they

satish WaghChairman, Chemexcil

“Our industry has no choice but to go for re-registration of the products we export.”

D. K. nairSecretary General, Confederation of Indian Textile Industry

“You are defenseless if the barrier is imposed through individual contracts an inporter signs with his sourcing company.”

“If there are 10 buyers and 10 codes of ethics, all can be different, and even be contradictory.”

EmErging markEts insight 25

Indian Export

may also be designed and applied in a way that unnecessarily frustrates trade,” noted the World Trade Report 2012 by the WTO.

Though there is no single estimate of the financial loss from NTMs to Indian exports, the WTO report dropped sufficient hints. For the apparel sector, it said that prices in the US, EU and Canada were higher by 15%, 66% and 25%, respectively, owing to NTMs. Similarly, in Southeast Asia, South Asia and Japan, paper products cost 67%, 119% and 199 %more, respectively.

The impact of such measures on exports from countries such as India is apparent. Stricter rules mean costlier compliance, turning products more expensive and less competitive in the global market. The TBT and SPS measures have proven to be a huge burden for exporters from developing coun-tries. In 2010, almost half of the NTMs per-ceived as burdensome by exporting firms were TBT or SPS measures.

The invisible OnesWTO rules stipulate that every member

country has to announce NTMs. The idea is

to provide an opportunity for others to see if these measures have been suggested in the right spirit. Countries can raise objections, and the member that introduces such mea-sures can defend it. An analysis carried out by the Centre for WTO Studies has revealed that such notifications hide more than they reveal. The center has a unique system to track such notifications. It says 90% of such notifications listed at the WTO forum do not provide accurate details of the products they actually target.

According to MuraliKallummal, the brain behind the database analysis system at the Centre for WTO Studies, of the nearly 31,000 NTMs which covered about 212,000 products until March 2012 (from January 1995), only 10% provide meaningful details

about the exact target. For the remaining NTMs, it takes special skills and time-con-suming research to figure out the targets. The center now scans each such notification to suggest the possible product it might be targeting. “It will be useful to understand issues related to market access. It will help exporters, importers, academics, apex industrial bodies and trade policymakers,” Kallummalsaid.

He said keeping things vague and unclear is not limited to NTMs alone; it also happens in the case of tariffs, as there are several ways to keep them within WTO compliant levels and still provide higher tariffs for spe-cific products. “Higher product distinction allows a country to apply varying levels of tariffs, while keeping the average tariff at the harmonized level, closer to its WTO-committed level,” he said. The strategy, he explains, is clearly visible in the EU’s product distinction for wine and spirits (based on a 2005 study done by the center for the UB Group).

In the EU (266 products), the distinction of products for tariff application in the wine and

The increasing incidence of NTBs signals the need for more diplomatic, political and legal

steps to help its exporters.

Sectors such as agriculture and automobiles are more easily targeted by NTMs than others.

Indian Textile

EmErging markEts insight 26

spirits industry was eight times more sophis-ticated than the Indian classification (33 products). Product distinction in wine cate-gory is 27 times more sophisticated than India’s. “The expansion in the product list has provided the EU with substantial flexibili-ties by way of application of varying tariff levels, even when the average tariff remains low,” Kallummal said.

Fight Your Way in In the globalized world of trade, countries

that fight such clauses successfully can mini-mize NTBs, at least the visible ones. A couple of years ago, Indian drug export consign-ments to Africa and Latin America were being confiscated regularly in Dutch ports on grounds that the drugs violated the EU’s intellectual property laws. These seizures forced Indian drug exporters to ship medi-cines through longer routes, which raised the cost of shipment and made the drugs costli-

er. Only after the matter was taken to WTO forums, and the exporting countries, includ-ing India, Brazil, South Africa, threatened to take it to WTO’s dispute settlement forum, that the EU agreed to review its rules and the member countries agreed to amend their intellectual property laws.

Today, India may have to take the same action against Japan’s notification on shrimp exports. Such NTBs are being discussed, sorted out and minimized, as countries are entering bilateral and multilateral trade agreements. For instance, the India-EU bilat-eral trade and investment agreement (BTIA) deals with issues related to services, agricul-tural market access and disciplining of quali-ty requirements under SPS and TBT.

The commerce ministry says that prob-lems arising due to NTBs are duly taken up with the authorities of the country con-cerned. This is done either bilaterally with a view to their early and mutually satisfactory

resolution or presented for resolution by the WTO’s Dispute Settlement Mechanism.

That said, the increasing incidence of NTBs signals the need for more diplomatic, political and legal steps that India should take to help its exporters fight the bigger challenge. Perhaps it should begin closer home. CUTS International—a think tank on trade, regula-tions and governance issues—estimates that if the existing potential (which considers both tariff and non-tariff barriers) of India-Pakistan trade is harnessed, India will gain about $80 million.

The gain for Pakistan could be much more, about $1.4 billion. “Aviation spirit, light petro-leum distillates, gold and silver jewelry and iron ore are some of the prominent items from India that have significant potential for export to Pakistan,” said Bipul Chatterjee, deputy executive director, CUTS. Benefits, thus, can be mutual, and therein lies the hope.

Stringent visa rules and protectionist sentiments in countries like the US hurt India's IT industry.

SYN

DIC

ATIO

N/G

LOB

E A

SIA

Garuda Flies HiGHState-owned airlines are not in great shape. But Garuda in Indonesia is an exception. Let’s take a look at how its CEO, Emirsyah Satar, has changed it to be a promising airline business.By Shoeb K Zainuddin

Indonesian Air

Profile

Emirsyah Satarhas been the CEO and President Director at PT Garuda Indonesia since 2005. He began his career in the field of a banking including Citibank NA in Indonesia from 1985 to 1990. He first joined PT Garuda Indonesia in 1998 as an Executive Vice President of Finance. He left Garuda Indonesia in 2003 and came

back as CEO in 2005.

EmErging markEts insight 27

EmErging markEts insight 28

Indonesian Air

Execution. This one word encapsulates the success of

Emirsyah Satar, CEO and president of national carrier Garuda Indonesia. Over the past eight years, Emirsyah has not only transformed the once-struggling airline, he has made it the pride of the nation.

In 2012 alone, Garuda Indonesia won 60 international and domestic awards. “That’s more than one a week,” Emirsyah told GlobeAsia in a recent interview. The awards range from corporate governance and stan-dard of service to world-class information technology.

Perhaps his proudest moment came last July when UK-based airline service reviewer Skytrax named Garuda the World’s Best Regional Airline. The carrier was also named the Best Regional Airline in Asia, beating the likes of Dragon Air, Bangkok Airways and SilkAir.

Emirsyah has also taken the company public, listing it on the Indonesia Stock Exchange (IDX) in February 2011. These accomplishments have not only elevated his status as one of the most talented corporate leaders in the country, they have also proved that state-owned enterprises (SOEs), with the right leadership, can succeed in a tough market environment.

“We have proven that SOEs can be strong companies provided the management has the liberty to run them as private companies and everybody respects corporate gover-nance,” said Emirsyah.

“Nobody in the past thought Garuda could be where it is today,” he reflected. “When I told my friends in banking that I was joining Garuda and that I was going to list on the

stock exchange, they said I better close down the company,” noted the former Citibank staffer.