12

www.accelirate.com © 2018 Accelirate, Inc., All Rights Reserved. AUTOMATING MORTGAGE BREACH LETTERS Default Management/Pre-Foreclosure: CASE STUDY Accelerating Automation & AI

www.accelirate.com

© 2018 Accelirate, Inc., All Rights Reserved.

AUTOMATING MORTGAGE BREACH LETTERS

Default Management/Pre-Foreclosure:

CASESTUDY

Accelerating Automation & AI

2

Automating Mortgage Breach Letters

The purpose of this Case Study is to shed light on how to improve throughput and reduce cycle time in the Default Management function by automating the production of Mortgage Breach Letters.

The client is a Mortgage Investment firm that currently has over $10 billion in assets under management, along with loan servicing and origination affiliates. In 2017, the client embarked on a journey to transform the organization’s approach to Enterprise Optimization by utilizing a multitude of technologies including Robotic Process Automation (RPA), Optical Character Recognition (OCR), and Process Re-engineering methodologies.

After establishing our knowledge in automation and performing a Proof of Concept, the client chose to partner with Accelirate Inc. to establish their RPA capabilities within their organization.

Executive Summary

3

SCENARIO

The client’s Default Management Function was broken into four separate business units: Pre-Foreclosure, Foreclosure, Bankruptcy, and Loss Mitigation. Within the Pre-Foreclosure business unit lies an important activity called ‘Breach’ that involves the servicer aggregating all loan data that warrants a Mortgage Breach Letter and compiling that data into a State-specific format that accommodates for requirements by individual U.S. States. Due to the vast number of loans being serviced, the servicing provider had broken this ‘Breach’ activity into three separate processes: Automated, Hybrid, and Manual. By doing this, the client was able to better accommodate for volume increases in cases of mortgage portfolio acquisition. However, even with this added functionality, the client was still facing resource constraints causing Service Level Agreements (SLAs) not to be met and employees having to work overtime to accommodate for volume.

CLIENT ISSUES AND CHALLENGES

The client’s process required an initial validation that identifies which of the three Breach Processes (Automated, Hybrid, or Manual) the loan would fall under; the validation requires filtering a ‘Pending Breach Report’ that contains all loans that are currently in the Pre-Foreclosure business unit. Each of the three Breach Processes have their own separate filtering criteria that excludes any loans that would not require a Breach Letter to be sent. Once filtering has been applied, the Managing Foreclosure Coordinator would take the three datasets and place them in their corresponding Breach queues for other FCs (Foreclosure Coordinators) to work on.

4

Automating Mortgage Breach Letters

BREACH – AUTOMATED

Automated was the least time-consuming Breach process. After the Managing Foreclosure Coordinator filtered out the Pending Breach Report, they would take the loan dataset and run an automated script that would trigger a request from their Mainframe Application. The batch of loans would be sent to a third-party vendor who would prepare the Breach Letters for the Managing FC to review the next day. Once the batch was approved, the letters would be sent out to notify the respective borrowers.

BREACH – HYBRID AND MANUAL

The differentiation between these two processes, at first glance, was minimal and mainly centered around the method in which the actual letter was being sent out, either via the client’s mailroom or another differentiator. However, after further analysis, we determined that certain States’ depending on whether it was Hybrid or Manual, required separate data points that needed to be included in the Breach Letter. Additionally, certain States required registration via their State website, which required more data points than the Breach Letter. As mentioned before, the Managing FC would assign specific States to different coordinators that would be represented by ‘tasks’ in their Mainframe Application. Once the task was assigned, Coordinators would:

- Gather all Borrower/Company information from their system of records including all figures related to the loan (i.e. Suspense Balance, Uncollected Fees, etc.) payment information (i.e. Due Date, Payment

Breakdown), calculate the ‘Cure Period’ (i.e. timeframe in which the borrower has to bring the loan current), and input into State-specific Breach Letter templates.

- Certain States (both in the Hybrid and Manual processes) required State registration, thus the coordinators would have to gather additional data points that were not required for the Breach Letter (i.e. Current Interest Rates, etc.) and input them into the State website before submitting the loan for registration.

- Certain States (both in the Hybrid and Manual processes) required a figures breakdown of the loan, outlining pertinent mortgage loan information (i.e. Escrow Advances, Accumulated Late Charges, etc.) that was not required in the State Breach letter, however, they would be stored in their Document Management System for future reference.

- After all the State-specific required documentation had been prepared, the coordinators would save them into their Document Management System, then, dependent upon the Breach process type (Hybrid or Manual), the mailing of the letter would either be manually fulfilled by the Coordinator, for Breach Manual, or the mailroom for Breach Hybrid.

- Lastly, once all documentation had been sent out correctly and uploaded to the repository, the Coordinators would close out the task in their Mainframe Application, indicating a successfully processed loan.

5

Keep in mind, each State has its own set of requirements in terms of required data for the Breach Letter, in addition to States that require registration on their website and a figures breakdown. The manual effort to accommodate each of these differing scenarios whilst maintaining data integrity and meeting the agreed upon SLAs was unsustainable, requiring the employees to work overtime to meet their deadlines. Fortunately, due to Accelirate’s approach to both Process Analysis and Solution Design, we were able to provide multiple automations that accommodate for the handling criteria for each of the three Breach Processes, providing significant time savings to the business while increasing data integrity.

The Breach Letter cycle time breakdown is as follows:

BREACH MANUAL

State Cycle Time State Registration Required?

Massachusetts 15 Minutes

New York 27 Minutes Yes

Maryland 15 Minutes Yes

West Virginia 5 Minutes

Arkansas 15 Minutes

BREACH HYBRID

State Cycle Time State Registration Required?

Figures Breakdown Required?

Pennsylvania 12 Minutes Yes

North Carolina 12 Minutes Yes Yes

New Jersey 5 Minutes

Mississippi 3 Minutes

Rhode Island 5 Minutes

Utah 3 Minutes

Nevada 4 Minutes

6

Automating Mortgage Breach Letters

Accelirate Solution

Accelirate took a holistic approach to automating the ‘Breach’ activity, rather than trying to exactly replicate what the human was doing, we looked at the overall goal of this process and the necessary requirements to reach that goal. Instead of jumping straight into solution design, we spent an extensive amount of time working alongside the business in the ‘Analysis’ phase to determine what would be included in our automation scope and then began building our modules while utilizing an Agile ‘phased-UAT’ approach to ensure the effectiveness and reusability.

UNDERSTANDING THE INPUT

The first challenge we decided to focus on was automating the filtration of the ‘Pending Breach Report’ as it would provide immediate lift to the Managing FC and provide the filtered datasets that were required for each of the three Breach Processes. By taking this approach, we were able to ‘modularize’ our initial input, validate its efficacy so it could be utilized for the later User Acceptance Testing (UAT) phases, and provide an immediate lift to the business as the dev turn around time was minimal.

7

DETERMINING SCOPE

The initial difficulty in determining scope was gathering the volume data relating to the two individual processes. We needed to have a clear understanding of where the majority of effort was being spent so we could efficiently scope the solution. By following the Pareto Principle, we were able to identify that over 91% of all volume in Breach Manual and 87% of all volume in Breach Hybrid came from just six States. The complete loan volume-by-State breakdown is as follows:

Breach Manual

State Annual Loans

Massachusetts 7,003

New York 6,025

Maryland 4,520

West Virginia 836

Arkansas 703

Breach Hybrid

State Annual Loans

Pennsylvania 10,200

North Carolina 7,006

New Jersey 4,520

Mississippi 1,000

Rhode Island 702

Utah 702

Nevada 636

8

Automating Mortgage Breach Letters

The volume breakdown made it clear that by focusing on six out of twelve States we could account for the majority of use cases in both the Breach Hybrid and Breach Manual processes. However, we needed to consider the States that required State registration, as not only did they have completely separate handling criteria, some States required different information than others.

BREACH AUTOMATED

The overall volume of the Breach Automated process was significantly higher than both the Breach Manual and Breach Hybrid as the Breach Automated process had 1,000 Loans Weekly. However, because the process was already being outsourced to a third-party vendor, we determined that the cost-benefit of bringing that responsibility in-house was too low to accommodate. Thus, we decided that replicating the user actions was more efficient than trying to re-engineer the process. Though the cycle time was only two hours per week,

we were able to quickly develop a solution, thus providing immediate lift to the Managing Foreclosure Coordinator.

DATA POINT CONSOLIDATION

After establishing the solution scope, consolidation of all necessary data points was key. By doing this, we could more efficiently approach the solution from a modular perspective. We also created a ‘data map’ for all the States. We were then able to identify any shared data points that could be leveraged for reusability, as well as used to outline any data points that were State-specific. Additionally, since two States in the Breach Manual process required State registration and one State in the Breach Hybrid process required it along with two of them requiring a ‘Figures’ breakdown, the data mapping practice helped us immensely in our solution approach.

The data point breakdown is as follows:

Breach Manual

Massachusetts

Breach Letter 19 Data Points

New York

Breach Letter 15 Data Points

State Registration 27 Data Points 9 Unique

Maryland

Breach Letter 18 Data Points

State Registration 19 Data Points 6 Unique

9

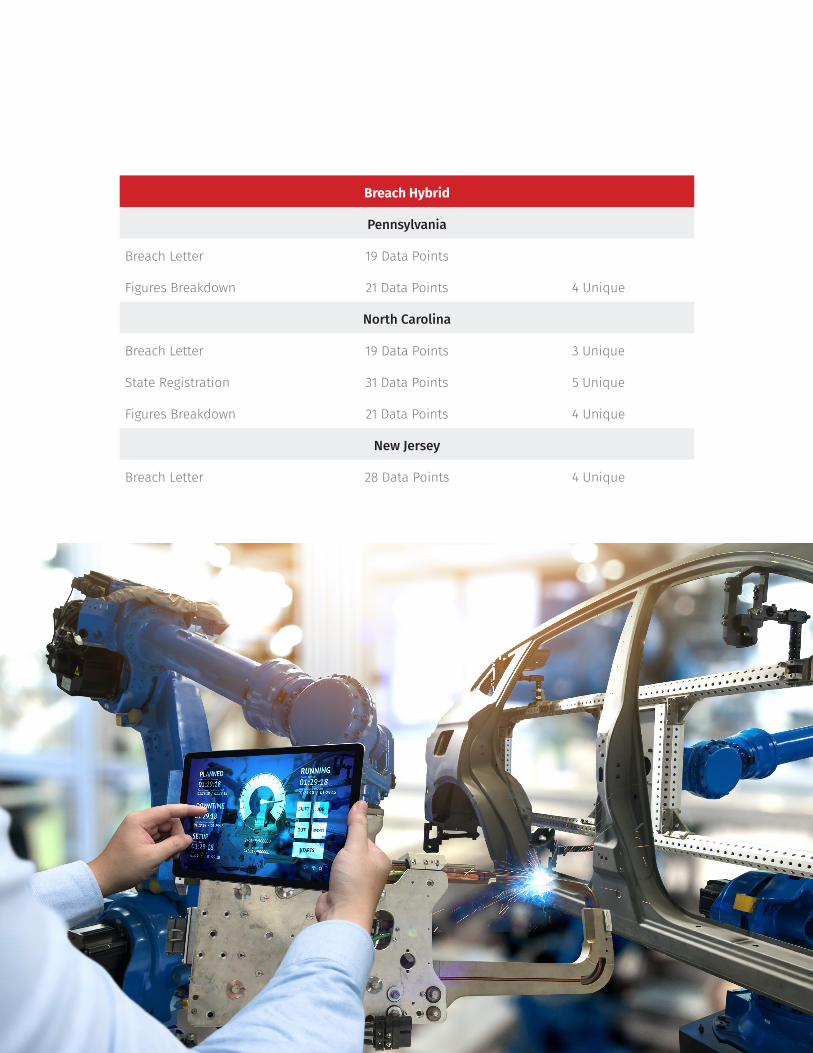

Breach Hybrid

Pennsylvania

Breach Letter 19 Data Points

Figures Breakdown 21 Data Points 4 Unique

North Carolina

Breach Letter 19 Data Points 3 Unique

State Registration 31 Data Points 5 Unique

Figures Breakdown 21 Data Points 4 Unique

New Jersey

Breach Letter 28 Data Points 4 Unique

10

Automating Mortgage Breach Letters

As you can see from the charts on the previous page, many of the data points among the six States in scope were shared and the outlying unique values could be more easily accommodated when presented in a data map that clearly indicated the source location information. Now that all data points had been outlined, our next concern was the method in which we were going to extract them, either by replicating the users’ actions or via back-end integration.

SOURCE DATA LOCATION

All data points that needed to be extracted were held in the client’s system of record, which was a Mainframe application. However, instead of solely relying on this application, we worked with the analytics team to understand which data points could be accessed via back-end integration and worked with the business to understand which data points needed to be ‘live’ as the data held in the database was reflective of the previous days information. By doing this we were able to provide additional cost savings to the business by not having to pay the third-party Mainframe provider, who charged our client on a ‘per click’ basis for a majority of data points.

PHASED SOLUTION INTEGRATION

Accelirate’s automation framework encompassed a Waterfall Matrix approach for analysis with an agile methodology for development, providing all the benefits of the Waterfall in the ‘requirements gathering’ phase while having it still be adaptable to change during development. By utilizing the data map created in analysis, we were able to strategically develop modules that would be used by each States’ variation and implement them in a phased approach where benefits would be compounded as their integration to production increased. Our approach allowed us to both empathize with the business in terms of data integrity and provide the most efficient solution possible given the circumstances.

11

- Provided 2,286 Annualized Man Hour Savings on Breach Manual (Phase 1)

- Provided 1,011 Annualized Man Hour Savings on Breach Hybrid (Phase 1)

- Provided 479 Annualized Man Hour Savings on Breach Automated (Phase 1)

- Provided $145,000 Annualized ROI Savings (Phase 1)

- Customization: The automation was configured to allow for the easy integration of additional State requirements for future phases

- Increased Throughput: Because the automation decreased process cycle time, the business was able to decrease their backlog and meet agreed upon business SLA’s

- Greater Employee Satisfaction: The automation was able to decrease the amount of manual effort required, negating the need for the employees to work overtime to meet deadlines

- Greater Audit Capabilities: Software bots were able to provide audit reports of every loan that was processed and give a ‘snapshot’ of each States’ breach letter for later review

Business Value of Accelirate Solution

Accelirate Inc1580 Sawgrass Corporate ExpresswaySuite 110Sunrise, FL [email protected]