41

The Current State of the Capital Markets Breakfast Forum September 2015

| Date post: | 12-Apr-2017 |

| Category: |

Business |

| Upload: | boyarmiller |

| View: | 439 times |

| Download: | 2 times |

The Current Stateof the Capital Markets

Breakfast Forum

September 2015

May 3, 2023

Drew KanalyChairman

Protect,

Perform

Preserve,

Investment Management | Financial and Estate Planning | Trustee Services

September 15, 2015

Copyright 2015 Kanaly Trust. All rights reserved.

Deeper Dive Into the DDM

Dividend Discount Model (DDM) A DCF model that states the estimated value of a stock is the discounted value of all future dividends

THE DDM EQUATION The Dividend Discount Model (DDM) states that the estimated value (per share) of a stock today is the discounted value of all future dividends:

Estimated Value of a stock today

= v — D1 + D2 + D3 + • + D. ° (1 + h) (1 + V (1+h)3 (1 + kr

= ' D N---% t

(1 + 10`

(10-2)

= Dividend discount model

where: D1, D2, .. = the dividends expected to be received in each future period h = the required rate of return for this stock, which is the discount rate applicable for an investment with this degree of riskiness (the opportunity cost of a comparable risk alternative)

Where D does not equal “The Donald”

Copyright 2015 Kanaly Trust. All rights reserved.

Exploring the Efficient Frontier

Coffee Cans to Warp Drive…

Copyright 2015 Kanaly Trust. All rights reserved.

Talk Changer

Dow Jones August 24, 2015 Opening : the first 5 minutes…gets you to thinking

Copyright 2015 Kanaly Trust. All rights reserved.

Equity Market Correction First significant market correction in 46 months (3rd longest without a 10% decline in history)

Copyright 2015 Kanaly Trust. All rights reserved.

Spike in Equity Market Volatility

Copyright 2015 Kanaly Trust. All rights reserved.

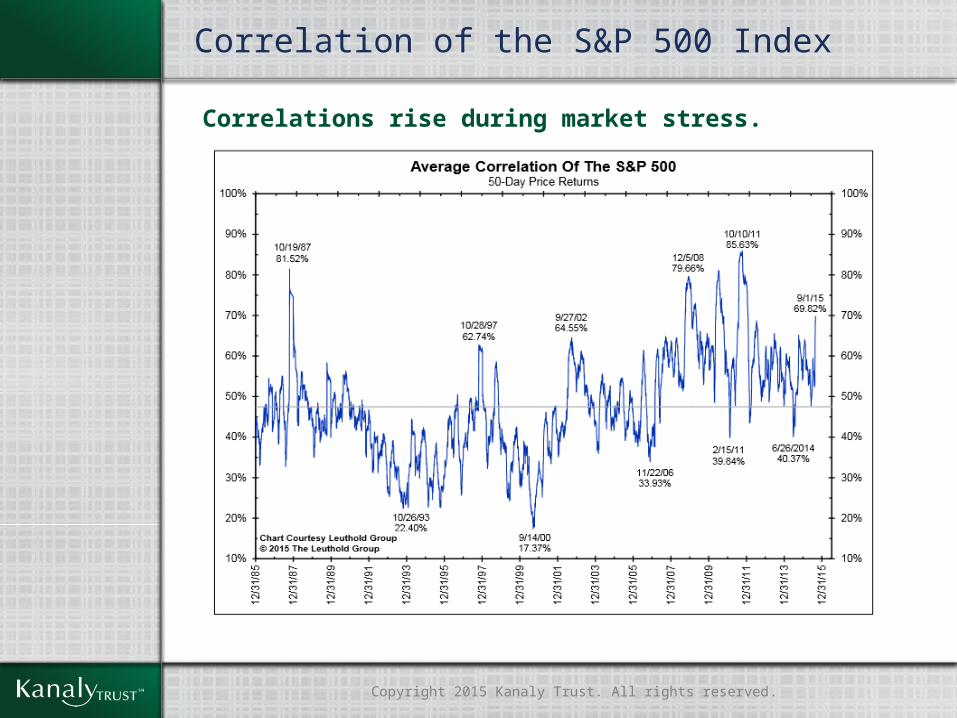

Correlation of the S&P 500 Index

Correlations rise during market stress.

Copyright 2015 Kanaly Trust. All rights reserved.

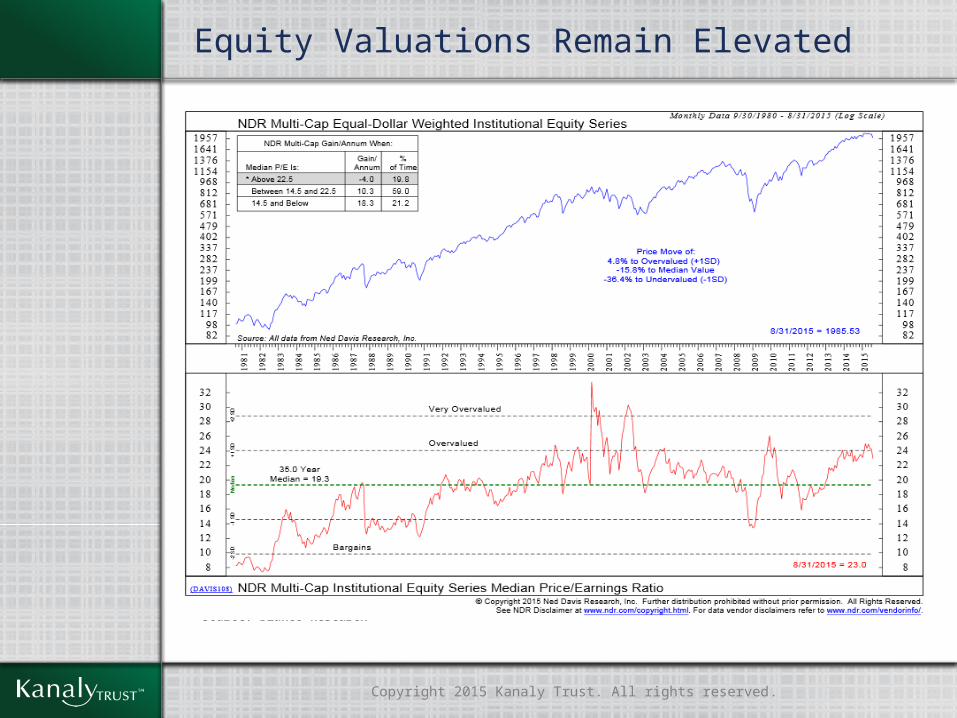

Equity Valuations Remain Elevated

Source: Bianco Research

Copyright 2015 Kanaly Trust. All rights reserved.

Little Earnings Growth in 2015One year ago, consensus called for 10% growth in S&P 500 earnings; now revised down to no growth.

Source: Bianco Research

Copyright 2015 Kanaly Trust. All rights reserved.

Credit Leads StocksCredit spread widening was a warning to equity investors.

Copyright 2015 Kanaly Trust. All rights reserved.

Commodity Super Cycle is Over

13

THE CURRENT STATE OF THE CAPITAL MARKETSMIDDLE MARKET M&A + PRIVATE EQUITY

UPDATE

COLT LUEDDE | MANAGING DIRECTOR | SEPTEMBER 2015

14

What Was Expected in 2015?Corporate Buyers Private Equity Groups

M&A Activity and Pricing Equal To or Higher than Prior Year

2015 2014

85% 84%

2015 2014

94% 89%

Source: Deloitte 2015 M&A Trend Report; KPMG 2015 M&A Outlook Survey Report

Increased Pursuit of Divestitures or Exits 2015 2014

39% 32%

2015 2014

74% 68%

Expect to Pursue Foreign Acquisitions 2015 2014

74% 59%

2015 2014

73%

85%

Expected Foreign Markets

Deloitte KPMG

29.2% 28.1%

24.7% 15.9%

20.4% 20.4%

84.0% 62.0%

36.0%

15

Less than $250 million 77%

$250 million to $499 million 12% $500 million to $999 million 5% $1 billion to $5 billion 3% Don't know 2% Greater than $5 billion 1%

Lower Middle Market Interest Continues

AVERAGE ENTERPRISE VALUE PER ACQUISITION 2014

AVERAGE ENTERPRISE VALUE PER ACQUISITION 2015

Less than $250 million 50%

$250 million to $499 million 27% $500 million to $999 million 16% $1 billion to $5 billion 6% Don't know 0% Greater than $5 billion 1%

Source: KPMG 2015 M&A Outlook Survey Report

16

2015 M&A Activity and Value Drivers

Large Cash Balances / Commitments Opportunities in Emerging Markets Robust Credit Market Consumer Confidence Improving Equity Markets Other

40%

19%

16%

13%

8%

4%

64% = Capital Availability

Source: KPMG 2015 M&A Outlook Survey Report; Golub Capital Middle Market Report

17

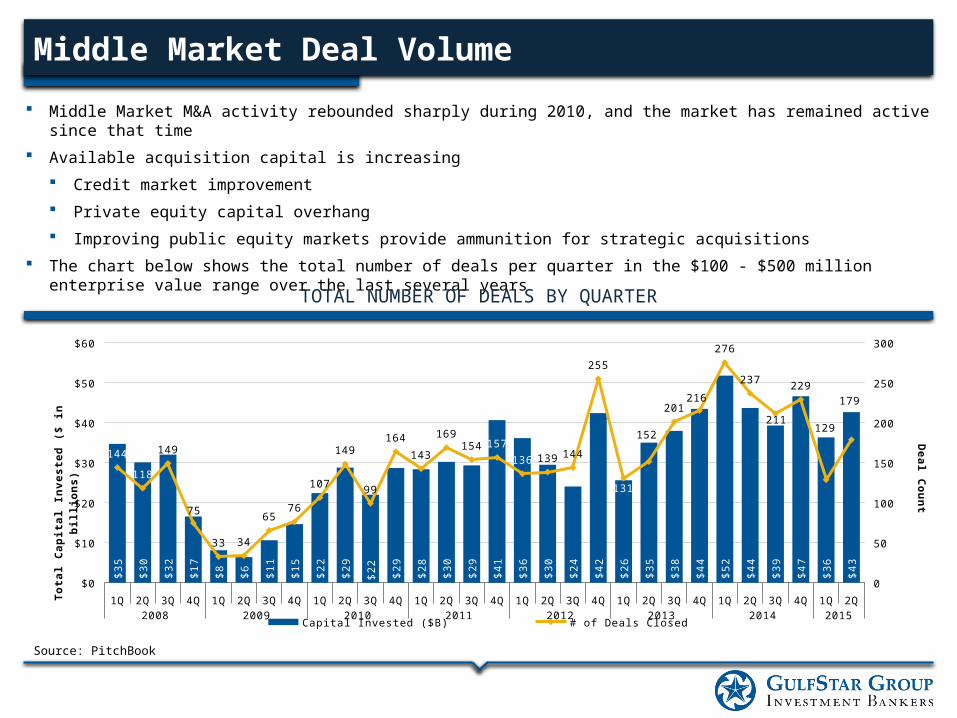

Middle Market M&A activity rebounded sharply during 2010, and the market has remained active since that time Available acquisition capital is increasing

Credit market improvement Private equity capital overhang Improving public equity markets provide ammunition for strategic acquisitions

The chart below shows the total number of deals per quarter in the $100 - $500 million enterprise value range over the last several years

Middle Market Deal Volume

TOTAL NUMBER OF DEALS BY QUARTER

Source: PitchBook

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q2008 2009 2010 2011 2012 2013 2014 2015

$0

$10

$20

$30

$40

$50

$60

0

50

100

150

200

250

300

$35

$30

$32

$17

$8 $6 $11

$15

$22

$29

$22

$29

$28

$30

$29

$41

$36

$30

$24

$42

$26

$35

$38

$44

$52

$44

$39

$47

$36

$43

144

118

149

75

33 34

6576

107

149

99

164

143

169154 157

136 139 144

255

131

152

201216

276

237

211

229

129

179

Capital Invested ($B) # of Deals Closed

Tota

l Cap

ital

Inve

sted

($ in

bill

ions

)D

eal Count

18

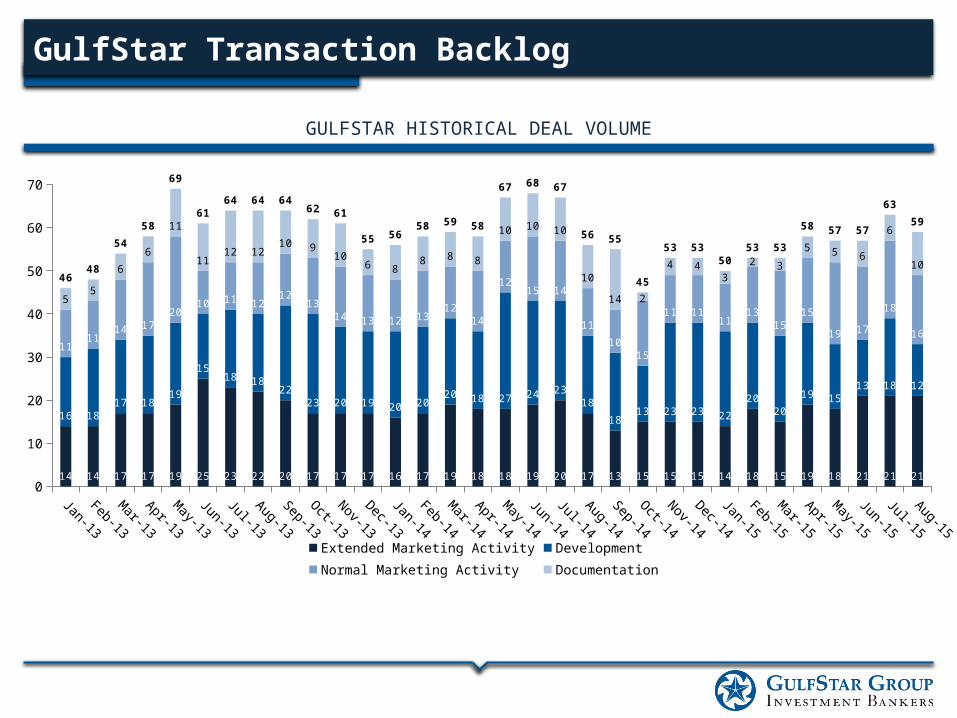

GulfStar Transaction Backlog

GULFSTAR HISTORICAL DEAL VOLUME

Jan-13Feb-13

Mar-13

Apr-13

May-13

Jun-13Jul-13

Aug-13

Sep-13Oct-13

Nov-13

Dec-13Jan-14

Feb-14Mar-14

Apr-14

May-14

Jun-14Jul-14

Aug-14

Sep-14Oct-14

Nov-14

Dec-14Jan-15

Feb-15Mar-15

Apr-15

May-15

Jun-15Jul-15

Aug-15

0

10

20

30

40

50

60

70

14 14 17 17 19 25 23 22 20 17 17 17 16 17 19 18 18 19 20 17 13 15 15 15 14 18 15 19 18 21 21 21

16 1817 18

19

1518 18

2223 20 19 20 20

20 18 27 24 2318

1813 23 23 22

2020

19 1513 18 12

1111

14 1720

10 11 1212

1314 13 12 13

1214

1215 14

11

1015

11 1111

1315

15

19 17

18

16

55

6

6

11

1112 12

10 910

6 88 8 8

10 10 10

10

14 2

4 43

2 35 5 6

6

1046

48

54

58

69

6164 64 64

62 61

55 5658 59 58

67 68 67

56 55

45

53 5350

53 53

58 57 57

63

59

Extended Marketing Activity Development Normal Marketing Activity Documentation

19

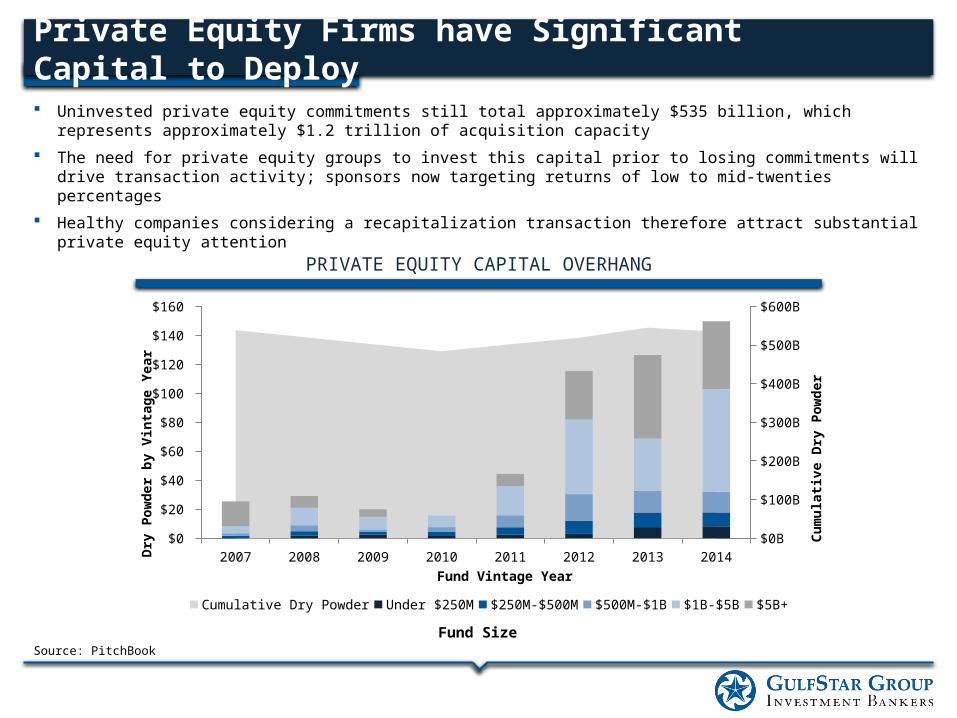

Private Equity Firms have Significant Capital to Deploy

PRIVATE EQUITY CAPITAL OVERHANG

Uninvested private equity commitments still total approximately $535 billion, which represents approximately $1.2 trillion of acquisition capacity

The need for private equity groups to invest this capital prior to losing commitments will drive transaction activity; sponsors now targeting returns of low to mid-twenties percentages

Healthy companies considering a recapitalization transaction therefore attract substantial private equity attention

Source: PitchBook

2007 2008 2009 2010 2011 2012 2013 2014$0

$20

$40

$60

$80

$100

$120

$140

$160

$0B

$100B

$200B

$300B

$400B

$500B

$600B

Cumulative Dry Powder Under $250M $250M-$500M $500M-$1B $1B-$5B $5B+

Dry

Pow

der b

y Vi

ntag

e Ye

ar

Fund Vintage Year

Cum

ulati

ve D

ry P

owde

r

Fund Size

20

S&P 500 Dry Powder Analysis

QUARTERLY CASH & SHORT-TERM INVESTMENTS S&P 500 (EX-FINANCIALS)

Source: FactSet Cash & Investment Quarterly

Aggregate Cash Grew 7%: The S&P 500 (ex-Financials) cash and marketable securities balance grew 6.6% year-over-year to a balance of $1.34 trillion at the end of Q1. However, cash declined sequentially by 4.7%, primarily as a result of Verizon Communications closing its acquisition of the remaining stake of Verizon Wireless. This marked the first sequential decline since Q2 2012.

Free Cash Flow Grew 9%: Cash flows from operations amounted to $282.0 billion in Q1, which marked an increase of 7.4% year-over-year. Free cash flow to equity increased by 8.7%.

Capital Expenditures Grew 6%: Capital expenditures (“CapEx”) accelerated growth to 6.2% in Q1. In the past four quarters, growth had not exceeded 1.5%. Analysts project that the 2014 growth rate for CapEx will be 6.7%, but also predict it will turn negative in 2015 (-1.2%)

Net Debt Issuance Positive for Fifteenth Straight Quarter: Cash inflows from net debt issuance were positive for the fifteenth straight quarter. Inflows of $74.1 billion were the second highest quarterly amount over that period.

Net Shareholder Distributions Grow 46%: Shareholder distributions in the form of dividends and net repurchase of stock ($193.8 billion) increased 45.8% year-over-year in Q1. Individually, gross share repurchases grew over 50% in Q1.

21

All $10-25 M $25-50 M $50-100 M $100-250 M0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

46.5% 41.7%47.5% 51.4%

45.8%

14.7%18.0%

15.5% 12.0%12.2%

38.4% 40.3% 37.0% 36.5%41.9%

Equity Sub Debt Senior Debt

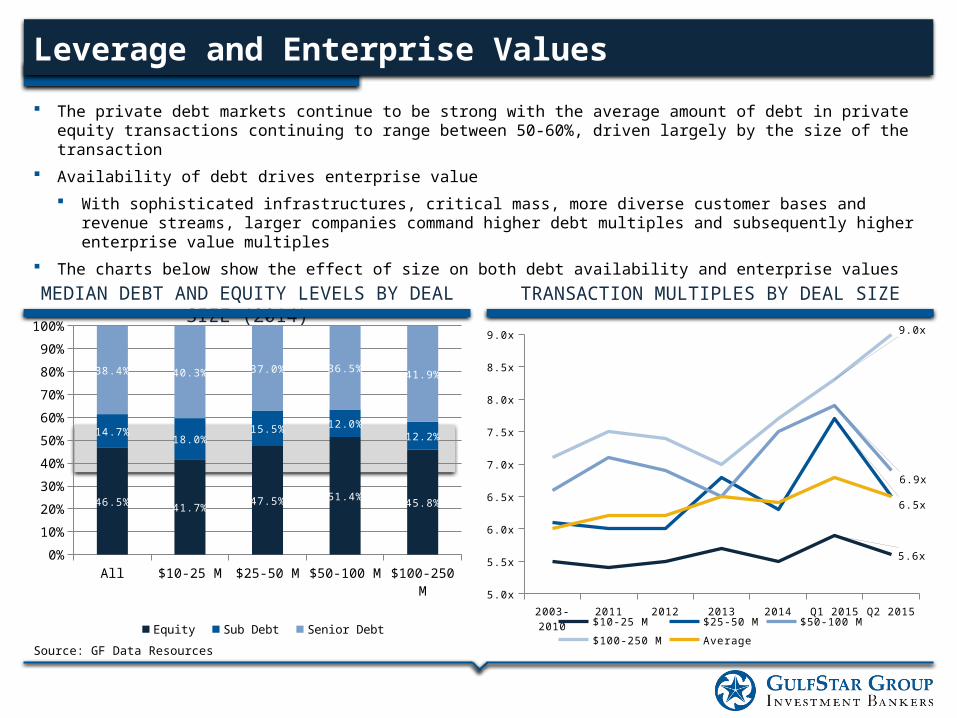

Leverage and Enterprise Values The private debt markets continue to be strong with the average amount of debt in private equity transactions continuing to range

between 50-60%, driven largely by the size of the transaction Availability of debt drives enterprise value

With sophisticated infrastructures, critical mass, more diverse customer bases and revenue streams, larger companies command higher debt multiples and subsequently higher enterprise value multiples

The charts below show the effect of size on both debt availability and enterprise values

MEDIAN DEBT AND EQUITY LEVELS BY DEAL SIZE (2014)

TRANSACTION MULTIPLES BY DEAL SIZE

Source: GF Data Resources

2003-2010 2011 2012 2013 2014 Q1 2015 Q2 20155.0x

5.5x

6.0x

6.5x

7.0x

7.5x

8.0x

8.5x

9.0x

5.6x

6.5x

6.9x

9.0x

$10-25 M $25-50 M $50-100 M$100-250 M Average

22

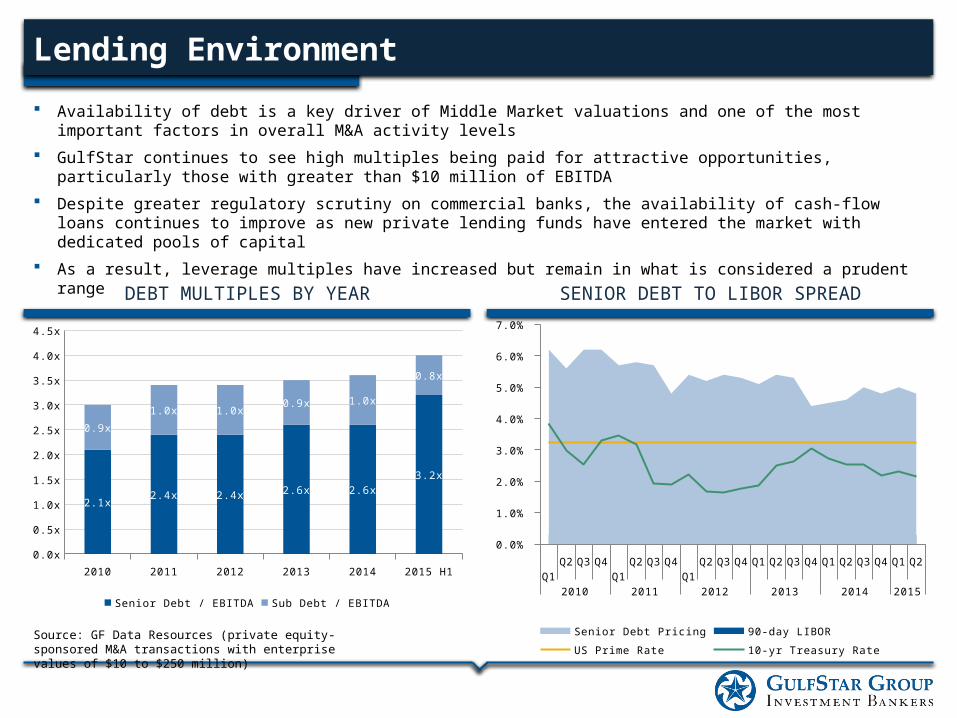

Lending Environment Availability of debt is a key driver of Middle Market valuations and one of the most important factors in overall M&A activity levels GulfStar continues to see high multiples being paid for attractive opportunities, particularly those with greater than $10 million of

EBITDA Despite greater regulatory scrutiny on commercial banks, the availability of cash-flow loans continues to improve as new private

lending funds have entered the market with dedicated pools of capital As a result, leverage multiples have increased but remain in what is considered a prudent range

DEBT MULTIPLES BY YEAR SENIOR DEBT TO LIBOR SPREAD

Source: GF Data Resources (private equity-sponsored M&A transactions with enterprise values of $10 to $250 million)

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q22010 2011 2012 2013 2014 2015

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Senior Debt Pricing 90-day LIBORUS Prime Rate 10-yr Treasury Rate

2010 2011 2012 2013 2014 2015 H10.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

2.1x 2.4x 2.4x 2.6x 2.6x3.2x

0.9x1.0x 1.0x 0.9x 1.0x

0.8x

Senior Debt / EBITDA Sub Debt / EBITDA

23

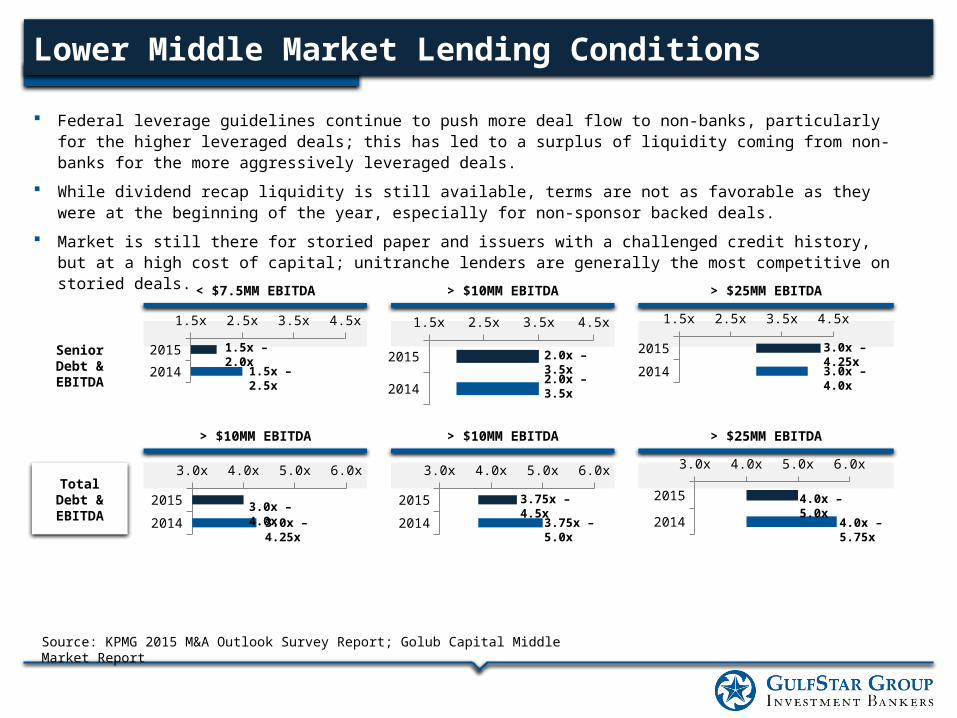

Lower Middle Market Lending Conditions

Federal leverage guidelines continue to push more deal flow to non-banks, particularly for the higher leveraged deals; this has led to a surplus of liquidity coming from non-banks for the more aggressively leveraged deals.

While dividend recap liquidity is still available, terms are not as favorable as they were at the beginning of the year, especially for non-sponsor backed deals.

Market is still there for storied paper and issuers with a challenged credit history, but at a high cost of capital; unitranche lenders are generally the most competitive on storied deals.

Source: KPMG 2015 M&A Outlook Survey Report; Golub Capital Middle Market Report

1.5x – 2.0x

1.5x – 2.5x2.0x – 3.5x

2.0x – 3.5x

3.0x – 4.25x

3.0x – 4.0x

Senior Debt & EBITDA

< $7.5MM EBITDA > $10MM EBITDA > $25MM EBITDA

2014

2015

1.5x 2.0x 2.5x 3.0x 3.5x 4.0x 4.5x

2014

2015

1.5x 2.0x 2.5x 3.0x 3.5x 4.0x 4.5x

2014

2015

1.5x 2.0x 2.5x 3.0x 3.5x 4.0x 4.5x

Total Debt & EBITDA 2014

2015

3.0x 3.5x 4.0x 4.5x 5.0x 5.5x 6.0x

3.0x – 4.0x3.0x – 4.25x 2014

2015

3.0x 3.5x 4.0x 4.5x 5.0x 5.5x 6.0x

3.75x – 4.5x

3.75x –5.0x 2014

2015

3.0x 3.5x 4.0x 4.5x 5.0x 5.5x 6.0x

4.0x – 5.0x

4.0x –5.75x

> $25MM EBITDA> $10MM EBITDA> $10MM EBITDA

24

Lower Middle Market Lending Conditions (cont’d)

Source: KPMG 2015 M&A Outlook Survey Report; Golub Capital Middle Market Report

Senior Cash Flow Pricing

No Libor Floor

L + 2.0% – 3.5%

L + 3.5% – 4.5%2014

2015

2.0% 3.0% 4.0% 5.0% 6.0% 7.0%

1.0% Libor Floor

L + 4.0% – 6.0%

L + 4.5% – 6.5%2014

2015

2.0% 3.0% 4.0% 5.0% 6.0% 7.0%

BANK NON-BANK

Unitraunch Pricing

2014

2015

6.0% 8.0% 10.0% 12.0%

2014

2015

6.0% 8.0% 10.0% 12.0%

L + 8.0% – 11.0%

L + 8.0% – 11.0%

1.0% Libor Floor 1.0% Libor Floor1.0% Libor Floor

2014

2015

6.0% 8.0% 10.0% 12.0%

L + 6.5% – 8.5%

L + 6.0% – 8.0%

L + 6.0% – 7.5%

> $25MM EBITDA< $7.5MM EBITDA > $15MM EBITDA

25

Covenant-Lite UpdateWith aggressive credit market conditions persisting, despite the recent uptick in new-issue yields, covenant-lite deals continue to be pervasive in loan structures. Covenant-lite loans with two or less covenants have grown considerably since 2010, with 88% market share. Meanwhile, covenant-lite loans with more than three covenants are virtually non-existence, only comprising 1% of the loan market.

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q1'LTM –

20%

40%

60%

80%

100%

≤ 2 3 ≥ 4

2007 2008 2009 2010 2011 2012 2013 2014 1Q14 1Q15$0B

$50B

$100B

$150B

$200B

$250B

$300B

0%

10%

20%

30%

40%

50%

60%

70%

Volume % of Institutional Volume

New-Issue First-Lien Covenant-Lite Volume Distributed by Number of Covenants

26

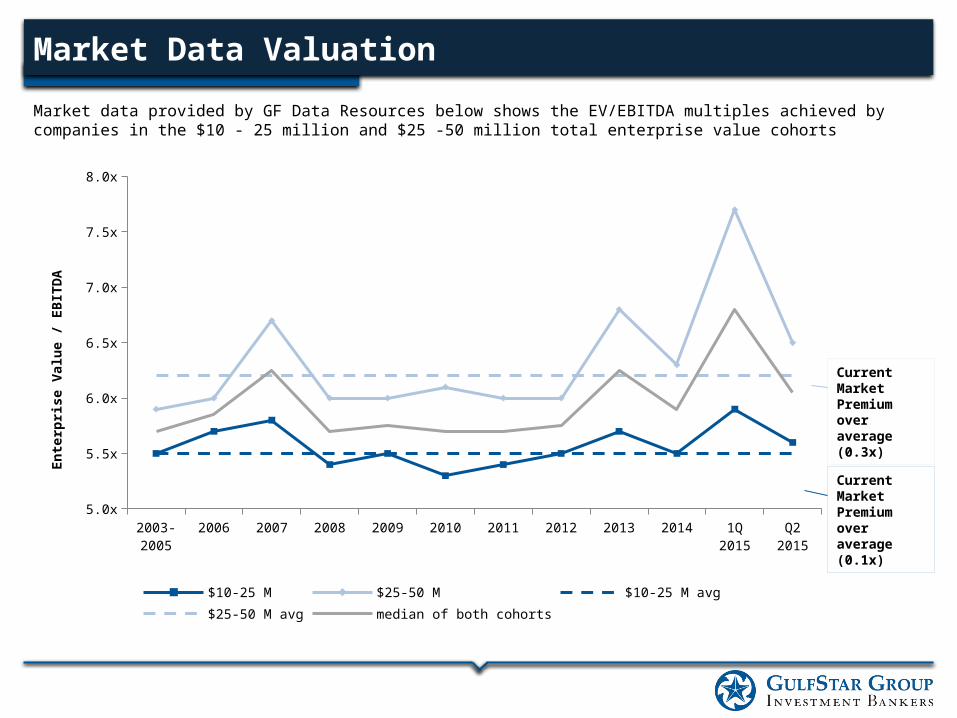

Current Market Premium over average (0.3x)

Current Market Premium over average (0.1x)

Market data provided by GF Data Resources below shows the EV/EBITDA multiples achieved by companies in the $10 - 25 million and $25 -50 million total enterprise value cohorts

Market Data Valuation

2003-2005

2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q 2015 Q2 20155.0x

5.5x

6.0x

6.5x

7.0x

7.5x

8.0x

$10-25 M $25-50 M $10-25 M avg$25-50 M avg median of both cohorts

Ente

rpris

e Va

lue

/ EB

ITDA

27

Market Data Valuation

2003-2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q 2015 Q2 20155.0x

5.5x

6.0x

6.5x

7.0x

7.5x

8.0x

5.6

6.5

6.1

7.3

$10-25 M $25-50 M $10-25 M avg$25-50 M avg median of both cohorts $100-250 M avg

Ente

rpris

e Va

lue

/ EB

ITDA

28

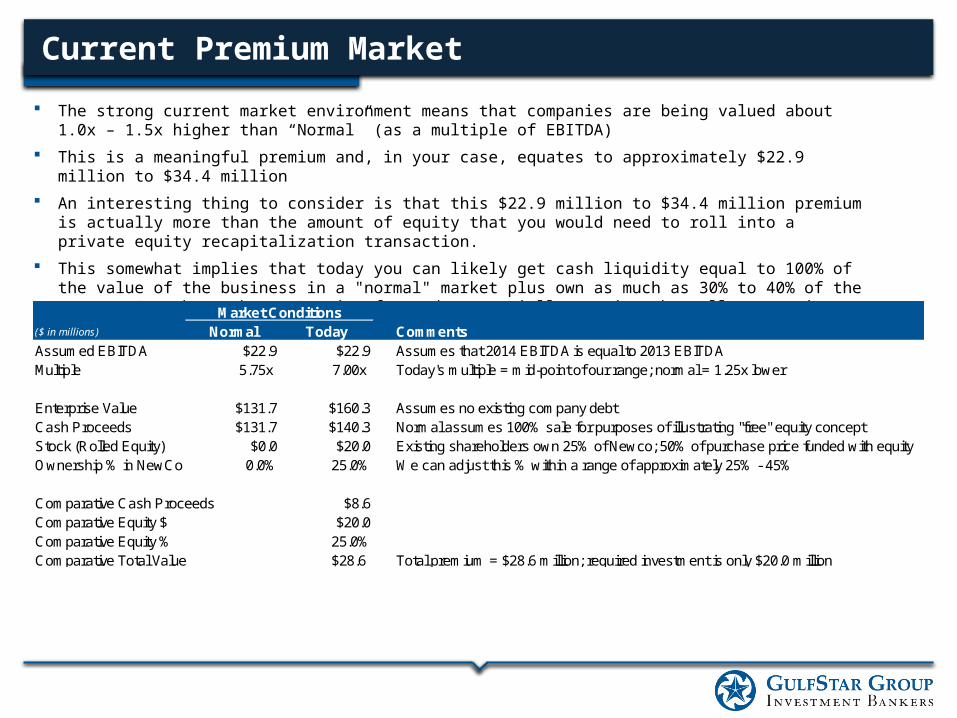

The strong current market environment means that companies are being valued about 1.0x – 1.5x higher than “Normal” (as a multiple of EBITDA)

This is a meaningful premium and, in your case, equates to approximately $22.9 million to $34.4 million An interesting thing to consider is that this $22.9 million to $34.4 million premium is actually more than the amount of

equity that you would need to roll into a private equity recapitalization transaction. This somewhat implies that today you can likely get cash liquidity equal to 100% of the value of the business in a "normal"

market plus own as much as 30% to 40% of the company (as chosen by you) going forward; essentially getting the rollover equity for free in today's market versus a "normal" market (see example calculation below).

Market Conditions($ in millions) Normal Today CommentsAssumed EBITDA $22.9 $22.9 Assumes that 2014 EBITDA is equal to 2013 EBITDAMultiple 5.75x 7.00x Today's multiple = mid-point of our range; normal = 1.25x lower

Enterprise Value $131.7 $160.3 Assumes no existing company debtCash Proceeds $131.7 $140.3 Normal assumes 100% sale for purposes of illustrating "free" equity conceptStock (Rolled Equity) $0.0 $20.0 Existing shareholders own 25% of Newco; 50% of purchase price funded with equityOwnership % in NewCo 0.0% 25.0% We can adjust this % within a range of approximately 25% - 45%

Comparative Cash Proceeds $8.6Comparative Equity $ $20.0Comparative Equity % 25.0%Comparative Total Value $28.6 Total premium = $28.6 million; required investment is only $20.0 million

Current Premium Market

29

Timing is Everything

MULTIPLE COMPARISON FOR TRANSACTIONS $100-$250 MILLION

Source: Historical Data (1988-2002) – Standard & Poors LCDSource: Historical Data (2003-2014) – GF Data Resources

Purchase Price Multiples Leverage Multiples

Theoretical Downturn &

Recovery

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

3.7x 3.4x 3.4x2.6x 2.7x 2.7x 2.8x

3.3x 3.5x 3.6x 3.5x 3.3x2.9x

2.2x 2.4x

4.2x 3.9x3.1x

4.1x4.7x

3.4x 3.7x3.3x

4.0x 4.3x3.8x 3.8x 3.8x

3.3x2.6x

3.0x3.5x

8.1x

7.1x

4.5x 4.2x

4.0x

5.5x

6.0x 6.0x

6.6x 6.7x 6.9x

6.6x 6.3x

5.8x 5.8x

6.4x 6.3x

7.4x

6.3x

7.5x 7.2x 7.2x

6.5x

7.5x 7.4x 7.1x 7.1x 7.1x

6.6x

5.2x

6.0x

7.0x

Purc

ahse

Pri

ce /

EBIT

DA D

ebt / EBITDA

30

Valuation Implications: Project Breakaway Company Overview – Project Breakaway is a provider of supply chain management services to global aerospace and defense

industries

Shareholder Objectives

Maximize value by capitalizing on strong recent performance and positive market trends

Realize substantial liquidity and diversify net worth

Manage different objectives of shareholders

Identify a proper strategic or financial partner to help achieve growth objectives

EBITDA – As calculated on financial statements; Applied to multiple for financial buyers

Synergy Adjusted EBITDA – Potential synergies are estimated and added back to EBITDA; Applied to multiple for strategic buyers

Period Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14Months 12 12 12 12 12 12 12(in $000s) A A A A A P P

Revenues $21,405 $19,816 $21,591 $24,131 $26,064 $29,563 $32,202

Gross Profit 7,863 6,715 7,358 8,308 10,137 10,991 11,972 Gross Margin 36.7% 33.9% 34.1% 34.4% 38.9% 37.2% 37.2%

EBITDA 5,613 4,393 5,210 6,276 7,717 8,007 8,807EBITDA Margin 26.2% 22.2% 24.1% 26.0% 29.6% 27.1% 27.4%

Synergy Adj. EBITDA 6,002 4,856 5,735 6,839 8,318 8,473 9,264Synergy Adj. EBITDA Margin 28.0% 24.5% 26.6% 28.3% 31.9% 28.7% 28.8%

Financial Buyers

Strategic Buyers

PROJECT BREAKAWAY SUMMARY FINANCIALS

31

Valuation Implications: Project Breakaway

$40.0

$50.0

$60.0

$70.0

$80.0

Dec-11 A Dec-12 A Dec-13 P Dec-14 P

Synergy Adjusted Value Baseline ValueDiscounted Projections Discounted MultipleDiscounted Projections & Discounted Multiple

Assumptions to GulfStar Analysis Current Projections & Multiple – EBITDA growth based on discussions with management; an 8.0x EBITDA multiple is applied Discounted Projections – A downward 10% discount was applied to EBITDA to account for a potential miss of projections Discounted Multiple – A downward market adjustment of 1.0x was utilized to represent a modest market decline Discounted Projections & Discounted Multiple – Both a 1.0x multiple reduction and a 10% discount to EBITDA to account for

potential market decline and a miss of projections

GulfStar Valuation Range: Sale based on Dec 2012 TTM

Current Multiple & Projections

Discounted Multiple

Discounted Projections& Discounted Multiple

Discounted Projections

ENTERPRISE VALUE OVER TIME ($ IN MILLIONS)

32

Valuation Implications: Project Cyclone

Assumptions to GulfStar Analysis

Current Projections & Multiple – EBITDA growth based on discussions with management; an 8.5x EBITDA multiple is applied

Discounted Projections – A downward 9.2% discount was applied to EBITDA to account for a potential miss of projections, which represents one-half of the decline experienced by the company in the 2009 downturn

Discounted Multiple – A downward market adjustment of 1.0x was utilized to represent a modest market decline

Discounted Projections & Discounted Multiple – Both a 1.0x multiple reduction and a 9.2% discount to EBITDA to account for potential market decline and a miss of projections

GulfStar Valuation Range: Sale based on Dec 2012 TTM

Current Multiple & Projections

Discounted Multiple

Discounted Projections& Discounted Multiple

Discounted Projections

$115.0

$135.0

$155.0

$175.0

$195.0

$215.0

$235.0

Dec-11 A Dec-12 A Dec-13 P Dec-14 P

Synergy Adjusted Value Baseline ValueDiscounted Projections Discounted MultipleDiscounted Projections & Discounted Multiple

ENTERPRISE VALUE OVER TIME ($ IN MILLIONS)

33

Valuation Implications: Project Wilhelm

Assumptions to GulfStar Analysis

Current Projections & Multiple – EBITDA growth based on discussions with management; an 6.0x EBITDA multiple is applied

Discounted Projections – A downward 10% discount was applied to EBITDA to account for a potential miss of projections

Discounted Multiple – A downward market adjustment of 1.0x was utilized to represent a modest market decline

Discounted Projections & Multiple – Both a 1.0x multiple reduction and a 10% discount to EBITDA to account for potential market decline and a miss of projections

GulfStar Valuation Range: Sale based on Dec 2012 TTM

Current Multiple & Projections

Discounted Multiple

Discounted Projections& Discounted Multiple

Discounted Projections

$6.0

$16.0

$26.0

$36.0

Dec-11 A Dec-12 A Dec-13 P Dec-14 P

Baseline Value Discounted Projections

Discounted Multiple Discounted Projections & Discounted Multiple

ENTERPRISE VALUE OVER TIME ($ IN MILLIONS)

34

www.gulfstargroup.com

State of Commercial Lending Markets

September 15, 2015

Texas Capital Bank

Macroeconomic Outlook

36

U.S. GDP growth rates have slowed

Domestic unemployment of 5.3%; lowest since “great recession”

The U.S. dollar gaining strength against major world currencies

Material improvement in oil prices not forecasted in the near term

Volatility in global markets related to negative economic indicators out of China

Banks have devoted substantial human and financial resources towards regulatory compliance

‒ Dodd-Frank‒ Consumer Financial Protection Bureau

Texas Capital Bank

Real Estate Lending Market

37

Low vacancy rates and an expanding economy have driven real estate activity across all sectors

Over the last three years, 22% of national banks experienced over 50% growth in total commercial real estate assets

‒ A robust pipeline of new supply is beginning to temper lender activity towards new projects

Office leasing slowing in energy-correlated markets such as Houston

The bank lending market is open to well structured transactions in favorable locations

Texas Capital Bank

State of Energy Lending

38

Oil prices remain low due to record high Saudi oil production‒ Forecasts see minimal improvement in prices through mid-2016

Top line revenue and margin declines are steepening for energy service providers

As a result of oil price declines, M&A activity has been sluggish‒ M&A opportunities are expected to increase as producers’

hedging contracts expire and require additional capital

Bank regulators have increased their focus on E&P lending

Lenders with expertise in the energy sector remain active

Texas Capital Bank

Commercial & Industrial Lending Activity

39

Competition amongst banks is fierce for higher quality loans‒ Pricing and net interest margins are under pressure

M&A activity down as purchase multiples have risen to historic levels

Dividend recapitalizations have increased in lieu of M&A

Refinancings are down approximately 25% year-over-year‒ Many issuers have already refinanced on favorable market terms

For most industry sectors, the lending market is expected to remain aggressive with abundant liquidity and competitive terms

Texas Capital Bank

Leveraged Lending Activity

40

Bank regulatory oversight has dampened risk appetite for more levered transactions

U.S. leveraged loan issuance is down 35% from same period last year

Despite liquidity and heightened competition, middle market leverage multiples are lower

‒ Bank regulatory guidance of 3x senior and 4x total leverage

Equity now a higher percentage of capital for leveraged transactions

The non-bank lending universe continues to increase