30

Breaking Up is Always Hard to Do 24 April 2013 Corporate demergers and divestments Glafkos Tombolis, Michael Cashman, Paul Garland

Breaking Up is Always Hard to Do

24 April 2013

Corporate demergers and divestments

Glafkos Tombolis, Michael Cashman, Paul Garland

Dispose of non-core/low value operations

Pay down debt

Create distributable reserves

Regulatory imperative (e.g. antitrust, capital requirements for financial

institutions)

“Internal” divestment where none of the normal demerger mechanisms

are available, but tax will determine feasibility

Why divest?

1

Intermediate step to divestment, but watch tax

To facilitate tax optimal divestment

Inability to divest

Corporate group simplification

Demerged business more valuable on standalone basis

Regulatory drag

Unbundling joint acquisitions

Why demerge?

2

Divestments

Shareholders forfeit claim to future economic benefit of divested business

(unless directly/indirectly receiving purchaser paper)

Highly-negotiated definitive agreements in private M&A deals (warranties,

tax indemnity, closing accounts, working cap adjustments)

Internal due diligence and possible reorganisation - including demerger -

of group prior to sale

May give rise to a tax charge, unless losses are available to offset any

gain or relief is available (SSE if a share sale)

Key features

3

Demergers

Shareholders continue to enjoy economic benefit of demerged business

(usually on same terms as non-demerged businesses)

Demerger documentation more functional than negotiated, but beware

directors’ duties apply primarily on a per entity, not group, basis

Technical company law processes – risk of impugning transaction

Internal due diligence of group prior to sale

Important to structure demerger to avoid a current tax charge

Key features, cont’d

4

Identify assets to be demerged/sold, liabilities to be retained

Structuring in contemplation of a particular buyer, or type of buyer

Gathering financial information

Dealing with management team

Contractual issues

Threshold issues

5

Identifying the IP: registered (TM, patents) and unregistered (©,

database).

Assigning all IP “used” in business? Consider “and held for use”.

Shared IP:

who gets ownership?

licences – protecting the asset.

assigning all IP “exclusively used” – beware alternatives.

Documents and know-how. Making copies? Right to request more.

Removal of branding

Intellectual Property issues

6 Insert footer text by selecting 'Insert - Header & Footer' / page numbers may also be taken off with this function

Effect on group debt financing arrangements

Shareholder approval

Rights of pre-emption

Post-deal transition support

Consider structuring to eliminate/reduce any potential tax charges

Threshold issues, cont’d

7

Direct dividend demerger

Three cornered demerger

Dividend

Reduction of capital

Section 110 liquidation demerger

Part 26 (scheme of arrangement) demerger

Types of demerger

8

Direct dividend demerger

9

Shareholders

Parent company

Non-core

subsidiary

Dividend of

shares

The direct route involves the transfer

by a company to its shareholder of

shares in a 75% trading subsidiary

Normally only works if demerging a company, not individual assets or

whole businesses

Distributable reserves necessary: s845 CA 2006 and residual common

law

May be an “exempt distribution” and not taxable in the hands of the

shareholders

No CGT as reorganisation of share capital

No degrouping charge if exempt distribution

Transfer of the shares is a disposal for CGT purposes unless:

SSE applies

Relevant losses available

Direct dividend demerger, cont’d

10

Three-cornered demerger

11

Shareholders

Parent

Core subsidiary Non-core

subsidiary

Three-cornered demerger, cont’d

12

Distribution

agreement

Shareholders

Parent

Non-core

subsidiary

Newco

Core subsidiary

(1) Dividend satisfied by

transfer of sub/trade to Newco (2) Issue of

shares

Transfer

Three-cornered demerger, cont’d

13

Shareholders

Newco

Core subsidiary Non-core

subsidiary

Parent

Can demerge a business

Distributable reserves again

Should be treated as a tax-free share reorganisation if:

the demerger is done for the benefit of the demerging activities; and

is not done for tax avoidance purposes or to cease or sell the trade post

demerger

Three-cornered demerger, cont’d

14

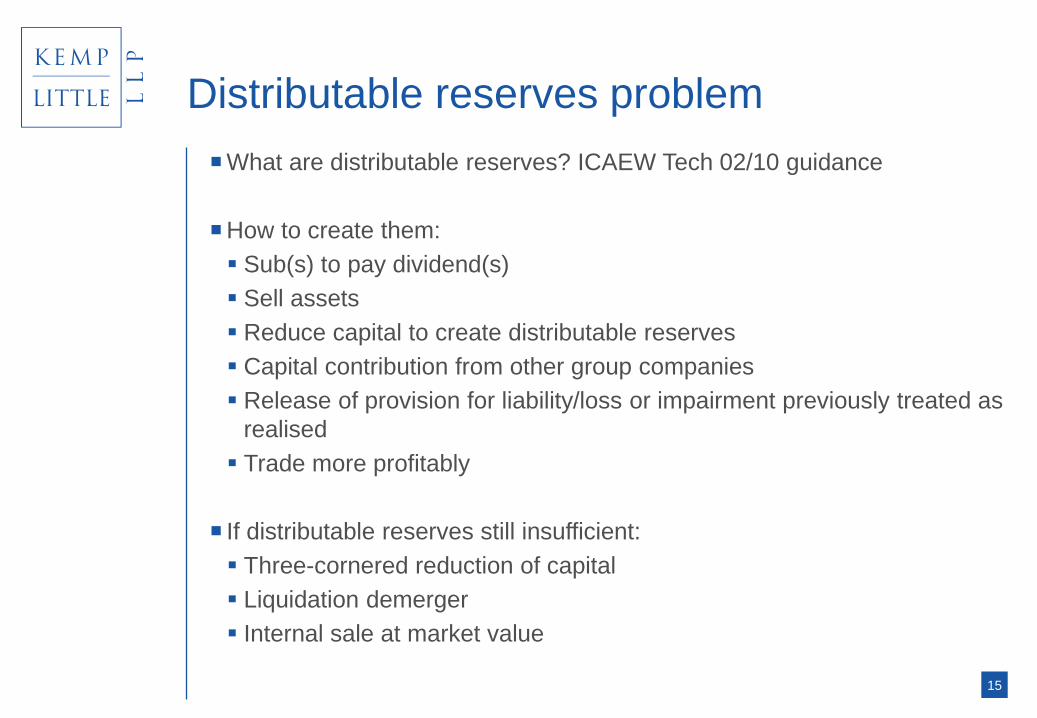

What are distributable reserves? ICAEW Tech 02/10 guidance

How to create them:

Sub(s) to pay dividend(s)

Sell assets

Reduce capital to create distributable reserves

Capital contribution from other group companies

Release of provision for liability/loss or impairment previously treated as

realised

Trade more profitably

If distributable reserves still insufficient:

Three-cornered reduction of capital

Liquidation demerger

Internal sale at market value

Distributable reserves problem

15

What is it?

When used?

When parent has insufficient or no distributable reserves or doesn’t

want to use them

When demerger purpose is to facilitate sale

When parent or demerging sub are not trading companies

When demerging subs are not 75% subs or resident in Member State

When liquidation demerger undesirable

Company law: s654(1) CA 2006, The Companies (Reduction of Share

Capital) Order 2008 and Tech 02/10 para 2.8B

Demerger mechanism explained

Three-cornered reduction of capital

16

Original structure

Three-cornered reduction of capital, cont’d

17

Shareholders

Parent

Non-core Core

Incorporation of New Parent

Three-cornered reduction of capital, cont’d

18

Shareholders

Parent

Non-core Core

New Parent

Transfer of core subsidiary

Three-cornered reduction of capital, cont’d

19

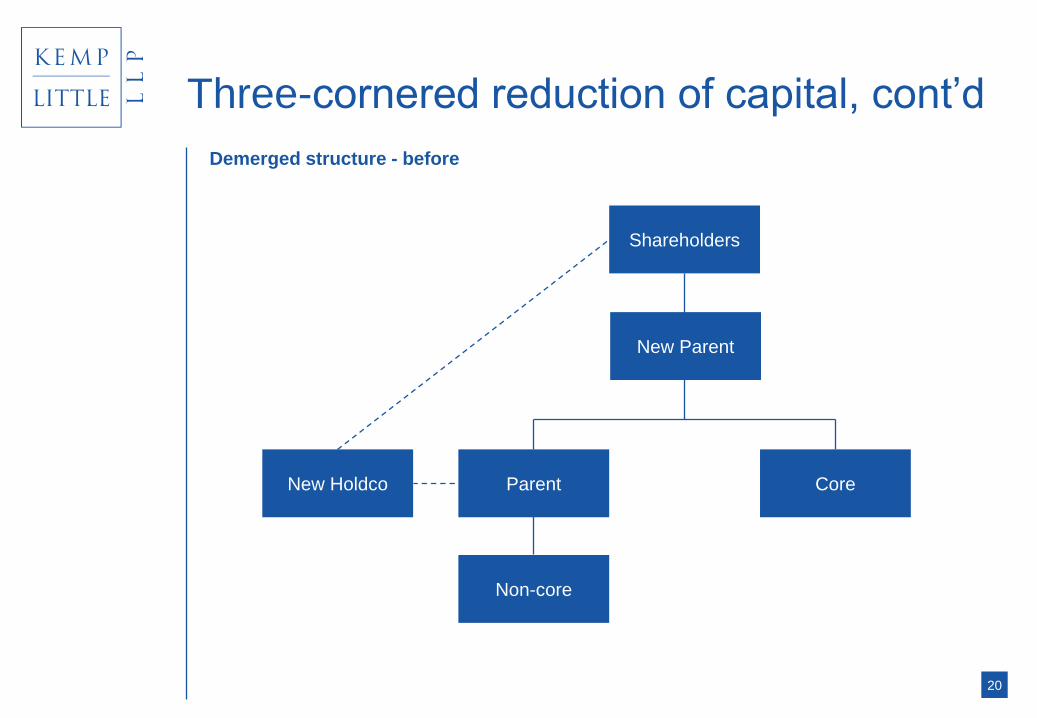

Shareholders

Parent

Non-core

Core

New Parent

Demerged structure - before

Three-cornered reduction of capital, cont’d

20

Shareholders

Parent

Non-core

Core

New Parent

New Holdco

Demerged structure - after

Three-cornered reduction of capital, cont’d

21

New Holdco

Parent

New Parent

Shareholders

Core

Non-core

Liquidation demerger

22

Shareholders

Parent company

Business 2

Newco 2 Newco 1

Issue

shares

Transfer

assets

Business 1

Issue

shares

Transfer

assets

Complex process

Costs of liquidator

Scope for shareholders and creditors to object

Directors’ statutory declaration of solvency

Effect on group contracts and debt financing arrangements

Liquidation demerger, cont’d

23

No distribution for income tax purposes

If liquidation is a scheme of reconstruction:

No gain on transfer of assets

No tax charge on shareholders

SSE may be available on a share transfer

Watch for potential degrouping charges

Liquidation demerger, cont’d

24

Used to facilitate in specie, reduction of capital and liquidation demergers;

not in and of itself a demerger route.

Examples of use:

To facilitate interposition of holdco to effect a three-cornered demerger

by reduction of capital

Interposing liquidation holdco in a s110 liquidation demerger where

existing parent has significant actual or contingent creditors

To effect partition demerger

To “cram down” dissentient creditors or shareholders in the parent

company

To effect a flip over of share options into holdco

Scheme of arrangement

25

Considerable flexibility

Costs associated with court process

Mitigation of implementation risk – 75% approval of each class

No specific tax reliefs apply, so generally structured as three-cornered

demerger or combined with liquidation

Scheme of arrangement, cont’d

26

Glafkos Tombolis

Partner, Corporate Group

dd +44 (0)20 7710 1672

27

Mike Cashman

Head of Tax Group

dd +44 (0)20 7710 1619

Kemp Little LLP

Solicitors

Cheapside House

138 Cheapside

London EC2V 6BJ

Tel: 020 7600 8080

Fax: 020 7600 7878

www.kemplittle.com

Kemp Little LLP is a limited liability partnership.

Registered number OC300242 England. Registered office as shown

The Roy Castle Lung Cancer Foundation are the only charity in the UK wholly dedicated to defeating lung cancer, the biggest cancer killer in the world.

Kemp Little is supporting the Roy Castle Lung Cancer

Foundation.