25

Opinion Paper Broadband Everywhere ‒ Assessment of Broadband Access Strategy based on Market and Cost Modeling 2013 / 02 We make ICT strategies work

Opinion Paper

Broadband Everywhere ‒ Assessment of Broadband Access Strategy based on Market and Cost Modeling

2013 / 02

We make ICT strategies work

Broadband Everywhere

Opinion Paper 2 Detecon International GmbH

Table of Contents

1 Executive Summary ............................................................................................. 3

2 Motivation and Challenges within a Joint Venture Portfolio ................................. 4

3 Detecon Approach and Methodology .................................................................. 2

4 Project Introduction .............................................................................................. 3

4.1 Phase I –Access Strategy for 6 integrated operators .................................. 3

4.1.1 Model Design ............................................................................................... 3

4.1.2 Process ........................................................................................................ 6

4.1.3 Data and Definitions .................................................................................... 6

4.1.4 How to deal with Black Box Perception and achieve buy in? ...................... 7

4.1.5 Results ......................................................................................................... 7

4.2 Phase II – SARA for 5 integrated operators .............................................. 11

4.2.1 The re run which was more than just re fresh-run ..................................... 11

4.2.2 Improvements ............................................................................................ 12

4.2.3 Model design ............................................................................................. 12

4.2.4 Process ...................................................................................................... 15

4.2.5 Input data guidance and reconciliation ...................................................... 15

4.2.6 Results ....................................................................................................... 16

5 Lessons learned ................................................................................................ 19

5.1 Process set up ........................................................................................... 19

5.2 Alignment steps ......................................................................................... 19

5.3 Data filling Guidelines ................................................................................ 19

6 Outlook .............................................................................................................. 20

7 Authors .............................................................................................................. 21

8 The Company .................................................................................................... 22

Broadband Everywhere

Opinion Paper 3 Detecon International GmbH

1 Executive Summary

Detecon was chosen by a big European integrated network operator to execute two projects

to support resource allocation in its Joint Ventures (JV). The main focuses were to develop a

consistent generalized methodology and assess the NPV (Net Present Value) of broadband

access technologies for six integrated Joint Ventures in Europe. The existing and future local

marketing data and network infrastructure were taken into account, while supporting

strategic decision and the optimization of CAPEX allocation. The project was planned in two

main phases from 2010 to 2012 and successfully performed with a number of

comprehensive deliverables.

Detecon took advantage of a professional planning tool „NetWorks‟ and developed the

technical cost models for HSPA+, LTE, xDSL and GPON to calculate CAPEX and OPEX for

broadband access network rollout over five years. In addition, an Excel-based commercial

model was implemented to transfer the marketing input and evaluate the NPV for different

rollout areas, both for the short/middle term planning (year 1-5) and the long term planning

(year 6-20).

Although centrally (headquarters) driven, the project required international data collection

and alignment. The results had to be discussed not just with the customer but also to be

explained in front of the participating Joint Ventures – at expert level as well as at

management level.

In our opinion the project delivered value for investment transparency and efficiency within

Joint Ventures:

Due to the centralized approach the shareholder benefits from a transparent

investment within a joint venture portfolio, based on the optimized CAPEX

allocation and a subsidiary independent generalized cost model. The

deliverables from the project give a clear feedback to support network design,

cost comparisons for network elements and the centralized technology

strategy. The positive business case can be introduced to all subsidiaries.

The Joint Ventures are able to review or establish their own broadband access

strategy from marketing, technical and financial point of view. The network

modeling is based on real network dimensioning rules provided by the JV

operator. The recommendations from the project can support the local

technical and marketing development.

The technical and marketing input from all Joint Ventures provides an explicit

overview of different devices/links/locations and ARPA/ARPU/Market share,

etc., which support both, shareholder and subsidiaries to reach the similar

price level, i.e. saving costs or increase revenues.

We believe that the proposed methodologies can be applied to other network operators as

well and support the financial investment and strategic decision of broadband access

strategy.

Broadband Everywhere

Opinion Paper 4 Detecon International GmbH

2 Motivation and Challenges within a Joint Venture Portfolio

It is not a surprise that a parent company having a number of Joint Ventures in different

countries operating fix and mobile networks has some difficulties in assessing the justified

needs for investments.

Revenues and EBITDA-margins under competitive pressure are strong arguments to meet

CAPEX-Sales ratios according to international bench marks for fixed and mobile

technologies. Recent examples have demonstrated that especially Chief Financial Officers

and Invest Committees lag of detailed information about investment programs and their

earning potentials of subsidiaries often apply a ´hair cut´ while trying to optimize Cash Flow

of the group.

Beside this, subsidiaries tend to highlight their specific setup, if it comes to a comparison.

Such local constraints must be taken into account, to save investments. The global view of

the parent company has to be standardized – to support comparability – and needs to be

customized – to handle local constraints.

Since significant investments are channeled into broadband network rollout – both fixed line

and mobile – efforts for transparency are needed. Transparency is especially required in

market ambitions and correlating to this for the value of technology rollout. Furthermore the

shareholder is highly interested in the optimized mix of broadband technologies and the

profitability ranking of the different technological options.

In those cases of missing relevant information about the invest programs our method

´Strategic Access Technology Resource Allocation´ based on a standardized modeling

approach helps the parent company to perform educated discussions about invest direction

and volume with the subsidiaries when it comes to broadband rollout strategies. Those

discussions in general lead to significant investment savings in the right areas -

geographical- and technology-wise.

To be as realistic as possible in an executable project time a reasonable standardized spatial

distribution within a country has to be established in order to distinguish different demand

and competitive situations as well as different architecture and cost levels for technologies.

As a welcomed side effect, by applying equal spatial distribution the shareholder was able to

do a comparison of technology values along different countries.

Broadband Everywhere

Opinion Paper 2 Detecon International GmbH

3 Detecon Approach and Methodology

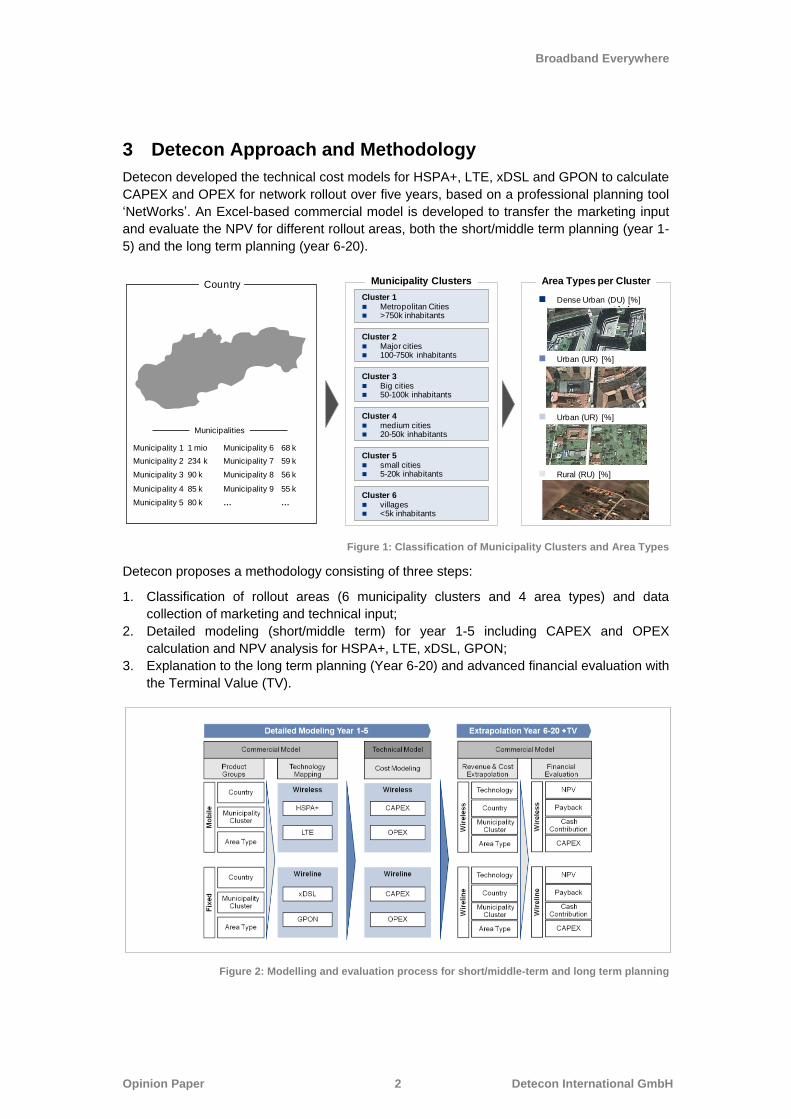

Detecon developed the technical cost models for HSPA+, LTE, xDSL and GPON to calculate

CAPEX and OPEX for network rollout over five years, based on a professional planning tool

„NetWorks‟. An Excel-based commercial model is developed to transfer the marketing input

and evaluate the NPV for different rollout areas, both the short/middle term planning (year 1-

5) and the long term planning (year 6-20).

Figure 1: Classification of Municipality Clusters and Area Types

Detecon proposes a methodology consisting of three steps:

1. Classification of rollout areas (6 municipality clusters and 4 area types) and data

collection of marketing and technical input;

2. Detailed modeling (short/middle term) for year 1-5 including CAPEX and OPEX

calculation and NPV analysis for HSPA+, LTE, xDSL, GPON;

3. Explanation to the long term planning (Year 6-20) and advanced financial evaluation with

the Terminal Value (TV).

Figure 2: Modelling and evaluation process for short/middle-term and long term planning

Municipality Clusters Area Types per Cluster

Cluster 1 Metropolitan Cities >750k inhabitants

Cluster 2 Major cities 100-750k inhabitants

Cluster 3 Big cities 50-100k inhabitants

Cluster 4 medium cities 20-50k inhabitants

Cluster 5 small cities 5-20k inhabitants

Cluster 6 villages <5k inhabitants

Dense Urban (DU) [%]

Urban (UR) [%]

Urban (UR) [%]

Rural (RU) [%]

Municipality 1 1 mio

Municipality 2 234 k

Municipality 3 90 k

Municipality 4 85 k

Municipality 5 80 k

Municipality 6 68 k

Municipality 7 59 k

Municipality 8 56 k

Municipality 9 55 k

… …

Municipalities

Country

Broadband Everywhere

Opinion Paper 3 Detecon International GmbH

4 Project Introduction

4.1 Phase I –Access Strategy for 6 integrated operators

We endorse the customer´s opinion that the modeling exercise truly unfolds its value by

making it a recurring project – building upon earlier inputs, ambitions and results and

improving the model and the process by applying lessons learned.

4.1.1 Model Design

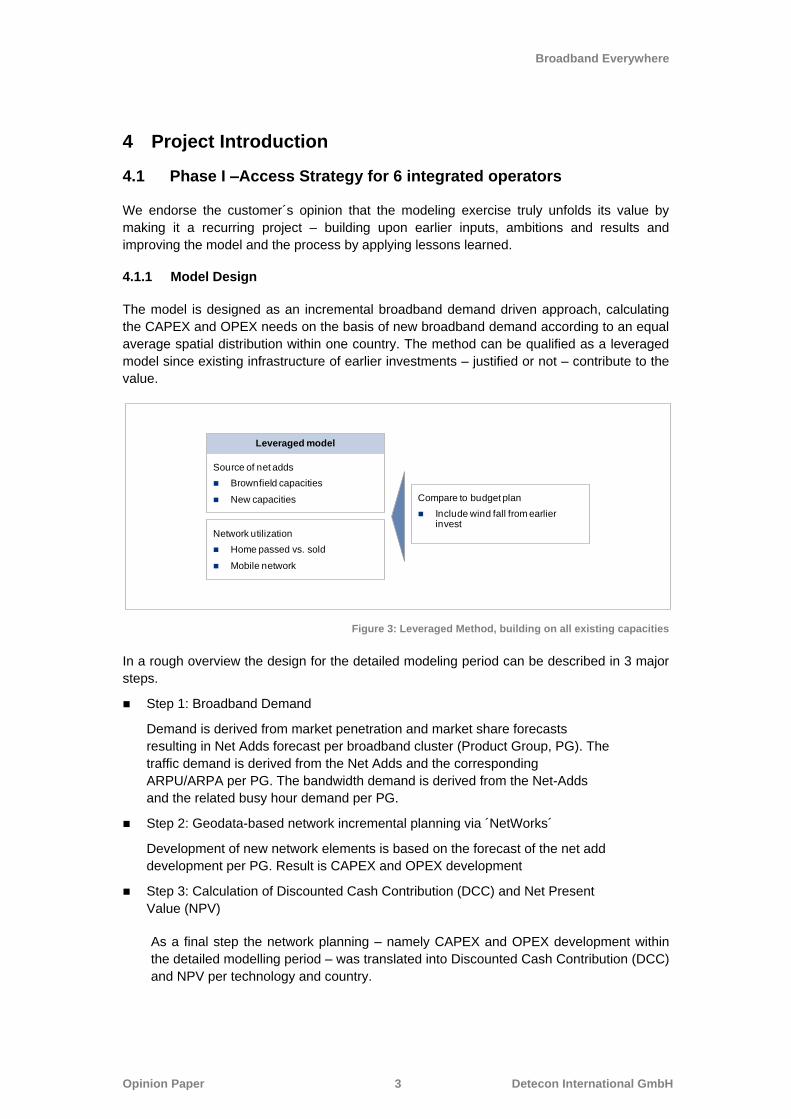

The model is designed as an incremental broadband demand driven approach, calculating

the CAPEX and OPEX needs on the basis of new broadband demand according to an equal

average spatial distribution within one country. The method can be qualified as a leveraged

model since existing infrastructure of earlier investments – justified or not – contribute to the

value.

Figure 3: Leveraged Method, building on all existing capacities

In a rough overview the design for the detailed modeling period can be described in 3 major

steps.

Step 1: Broadband Demand

Demand is derived from market penetration and market share forecasts

resulting in Net Adds forecast per broadband cluster (Product Group, PG). The

traffic demand is derived from the Net Adds and the corresponding

ARPU/ARPA per PG. The bandwidth demand is derived from the Net-Adds

and the related busy hour demand per PG.

Step 2: Geodata-based network incremental planning via ´NetWorks´

Development of new network elements is based on the forecast of the net add

development per PG. Result is CAPEX and OPEX development

Step 3: Calculation of Discounted Cash Contribution (DCC) and Net Present

Value (NPV)

As a final step the network planning – namely CAPEX and OPEX development within

the detailed modelling period – was translated into Discounted Cash Contribution (DCC)

and NPV per technology and country.

Source of net adds

Brownfield capacities

New capacities

Leveraged model

Network utilization

Home passed vs. sold

Mobile network

Compare to budget plan

Include wind fall from earlier invest

Broadband Everywhere

Opinion Paper 4 Detecon International GmbH

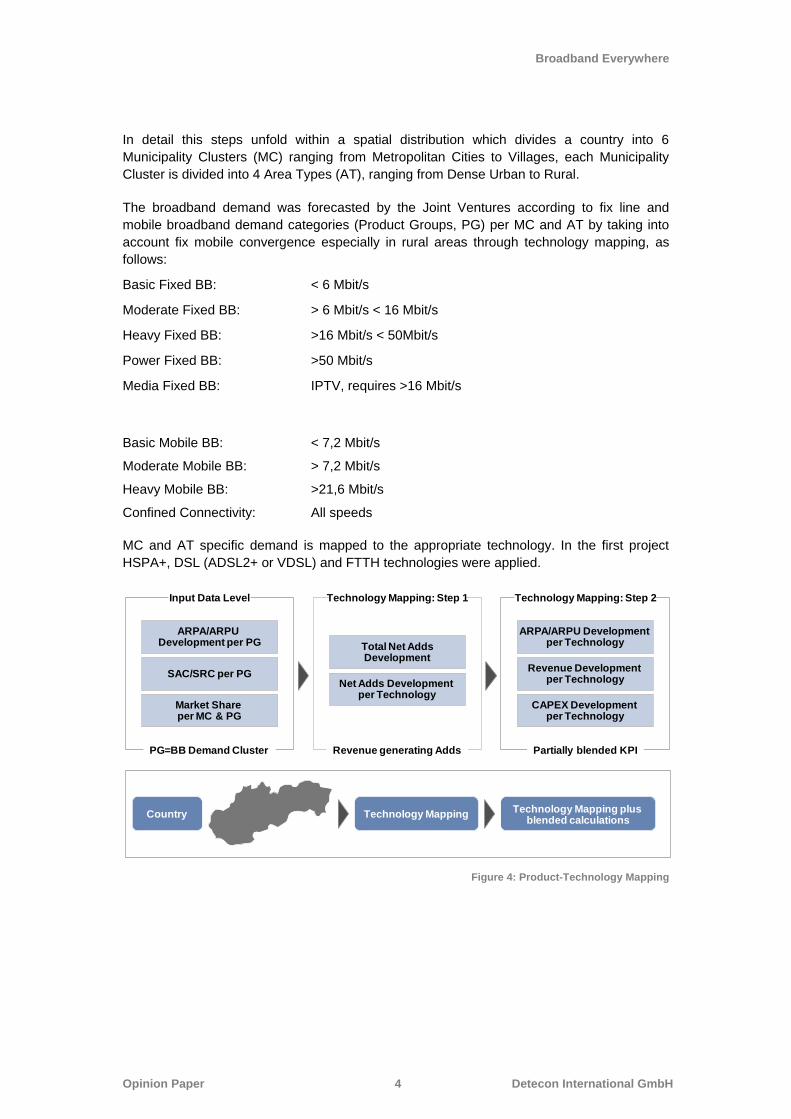

In detail this steps unfold within a spatial distribution which divides a country into 6

Municipality Clusters (MC) ranging from Metropolitan Cities to Villages, each Municipality

Cluster is divided into 4 Area Types (AT), ranging from Dense Urban to Rural.

The broadband demand was forecasted by the Joint Ventures according to fix line and

mobile broadband demand categories (Product Groups, PG) per MC and AT by taking into

account fix mobile convergence especially in rural areas through technology mapping, as

follows:

Basic Fixed BB: < 6 Mbit/s

Moderate Fixed BB: > 6 Mbit/s < 16 Mbit/s

Heavy Fixed BB: >16 Mbit/s < 50Mbit/s

Power Fixed BB: >50 Mbit/s

Media Fixed BB: IPTV, requires >16 Mbit/s

Basic Mobile BB: < 7,2 Mbit/s

Moderate Mobile BB: > 7,2 Mbit/s

Heavy Mobile BB: >21,6 Mbit/s

Confined Connectivity: All speeds

MC and AT specific demand is mapped to the appropriate technology. In the first project

HSPA+, DSL (ADSL2+ or VDSL) and FTTH technologies were applied.

Figure 4: Product-Technology Mapping

ARPA/ARPU Development per PG

SAC/SRC per PG

Market Share per MC & PG

ARPA/ARPU Development per Technology

Revenue Development per Technology

CAPEX Development per Technology

Total Net AddsDevelopment

Net Adds Development per Technology

Input Data Level Technology Mapping: Step 1 Technology Mapping: Step 2

PG=BB Demand Cluster Revenue generating Adds Partially blended KPI

Technology Mapping plus blended calculations

Technology MappingCountry

Broadband Everywhere

Opinion Paper 5 Detecon International GmbH

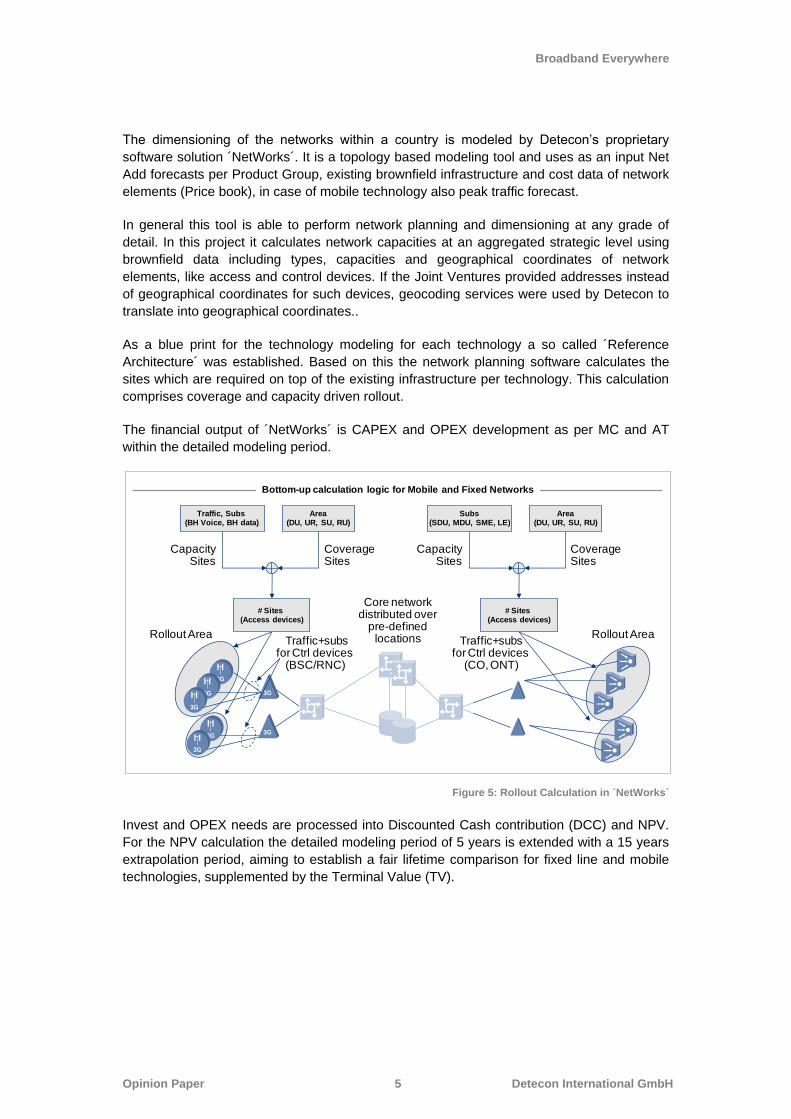

The dimensioning of the networks within a country is modeled by Detecon‟s proprietary

software solution ´NetWorks´. It is a topology based modeling tool and uses as an input Net

Add forecasts per Product Group, existing brownfield infrastructure and cost data of network

elements (Price book), in case of mobile technology also peak traffic forecast.

In general this tool is able to perform network planning and dimensioning at any grade of

detail. In this project it calculates network capacities at an aggregated strategic level using

brownfield data including types, capacities and geographical coordinates of network

elements, like access and control devices. If the Joint Ventures provided addresses instead

of geographical coordinates for such devices, geocoding services were used by Detecon to

translate into geographical coordinates..

As a blue print for the technology modeling for each technology a so called ´Reference

Architecture´ was established. Based on this the network planning software calculates the

sites which are required on top of the existing infrastructure per technology. This calculation

comprises coverage and capacity driven rollout.

The financial output of ´NetWorks´ is CAPEX and OPEX development as per MC and AT

within the detailed modeling period.

Figure 5: Rollout Calculation in ´NetWorks´

Invest and OPEX needs are processed into Discounted Cash contribution (DCC) and NPV.

For the NPV calculation the detailed modeling period of 5 years is extended with a 15 years

extrapolation period, aiming to establish a fair lifetime comparison for fixed line and mobile

technologies, supplemented by the Terminal Value (TV).

Bottom-up calculation logic for Mobile and Fixed Networks

Rollout Area

Traffic, Subs (BH Voice, BH data)

Area(DU, UR, SU, RU)

3G

3G

3G

3G

3G

3G

3G

Subs(SDU, MDU, SME, LE)

Area(DU, UR, SU, RU)

# Sites (Access devices)

CapacitySites

CoverageSites

CapacitySites

CoverageSites

Rollout Area

# Sites (Access devices)

Core network distributed over

pre-defined locations Traffic+subs

for Ctrl devices (CO, ONT)

Traffic+subsfor Ctrl devices

(BSC/RNC)

Broadband Everywhere

Opinion Paper 6 Detecon International GmbH

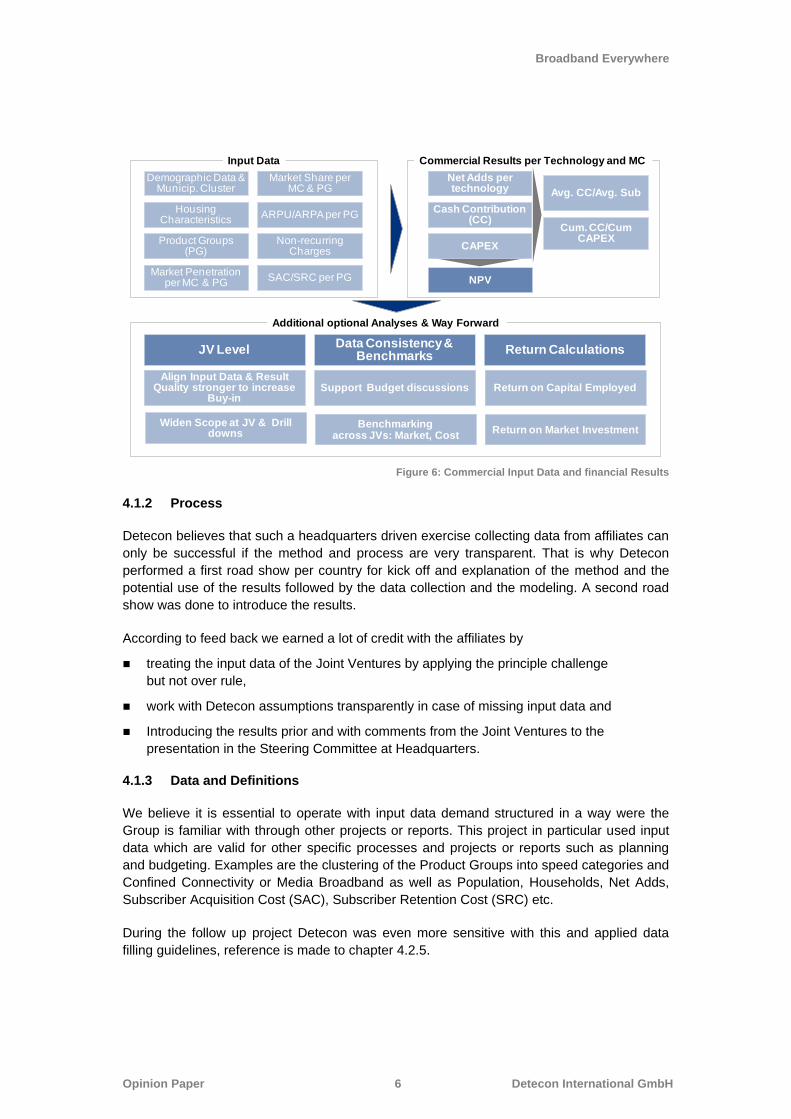

Figure 6: Commercial Input Data and financial Results

4.1.2 Process

Detecon believes that such a headquarters driven exercise collecting data from affiliates can

only be successful if the method and process are very transparent. That is why Detecon

performed a first road show per country for kick off and explanation of the method and the

potential use of the results followed by the data collection and the modeling. A second road

show was done to introduce the results.

According to feed back we earned a lot of credit with the affiliates by

treating the input data of the Joint Ventures by applying the principle challenge

but not over rule,

work with Detecon assumptions transparently in case of missing input data and

Introducing the results prior and with comments from the Joint Ventures to the

presentation in the Steering Committee at Headquarters.

4.1.3 Data and Definitions

We believe it is essential to operate with input data demand structured in a way were the

Group is familiar with through other projects or reports. This project in particular used input

data which are valid for other specific processes and projects or reports such as planning

and budgeting. Examples are the clustering of the Product Groups into speed categories and

Confined Connectivity or Media Broadband as well as Population, Households, Net Adds,

Subscriber Acquisition Cost (SAC), Subscriber Retention Cost (SRC) etc.

During the follow up project Detecon was even more sensitive with this and applied data

filling guidelines, reference is made to chapter 4.2.5.

Input Data Commercial Results per Technology and MC

Additional optional Analyses & Way Forward

Demographic Data & Municip. Cluster

Housing Characteristics

Product Groups (PG)

Market Penetration per MC & PG

Market Share per MC & PG

ARPU/ARPA per PG

Non-recurring Charges

SAC/SRC per PG

Net Adds per technology

Cash Contribution (CC)

CAPEX

Avg. CC/Avg. Sub

Cum. CC/Cum CAPEX

NPV

Align Input Data & Result Quality stronger to increase

Buy-inSupport Budget discussions

Benchmarkingacross JVs: Market, Cost

JV Level

Return on Market Investment

Return on Capital Employed

Widen Scope at JV & Drill downs

Data Consistency & Benchmarks

Return Calculations

Broadband Everywhere

Opinion Paper 7 Detecon International GmbH

4.1.4 How to deal with Black Box Perception and achieve buy in?

We should not be silent about the fact that despite a lot of efforts made to open up the

method and process the perception of a Black Box could not be eliminated totally. Especially

the mechanics within the planning software ´NetWorks´ by nature cannot be made available

to a broad audience. First as a result of a two decade development it is simply too complex,

second it belongs to the intellectual property of Detecon.

To meet remaining concerns we believe there is one promising route.

Be honest with the method, the data and with the communication towards

Headquarters and Joint Ventures especially when it comes to strength and

weaknesses of the model and the potential utilization of the results.

Address what can and should be done with the results and what not. Be aware

that any model only can serve as a proxy of the reality. In our case it means

that calculated investment cannot substitute detailed rollout planning but rather

establish a detailed country technology and investment pattern.

Perform ´NetWorks´ workshops with the client with detailed demonstrations of

model mechanics.

Take up improvement proposals and try to implement them in the coming

release.

In a subsequent phase of the project we established another effective method to increase

buy in by performing sensitivity analysis, reference is made to chapter 4.2.6.2.

4.1.5 Results

The results prepared numeric as well as graphical reflect the necessary network rollout by

showing existing and new network elements and NPV per technology and MC and AT on a

country level. This provides sufficient granularity for detailed decisions.

On cross country level an NPV ranking per technology and MC and AT was established,

showing were the highest NPV can be realized with which technology.

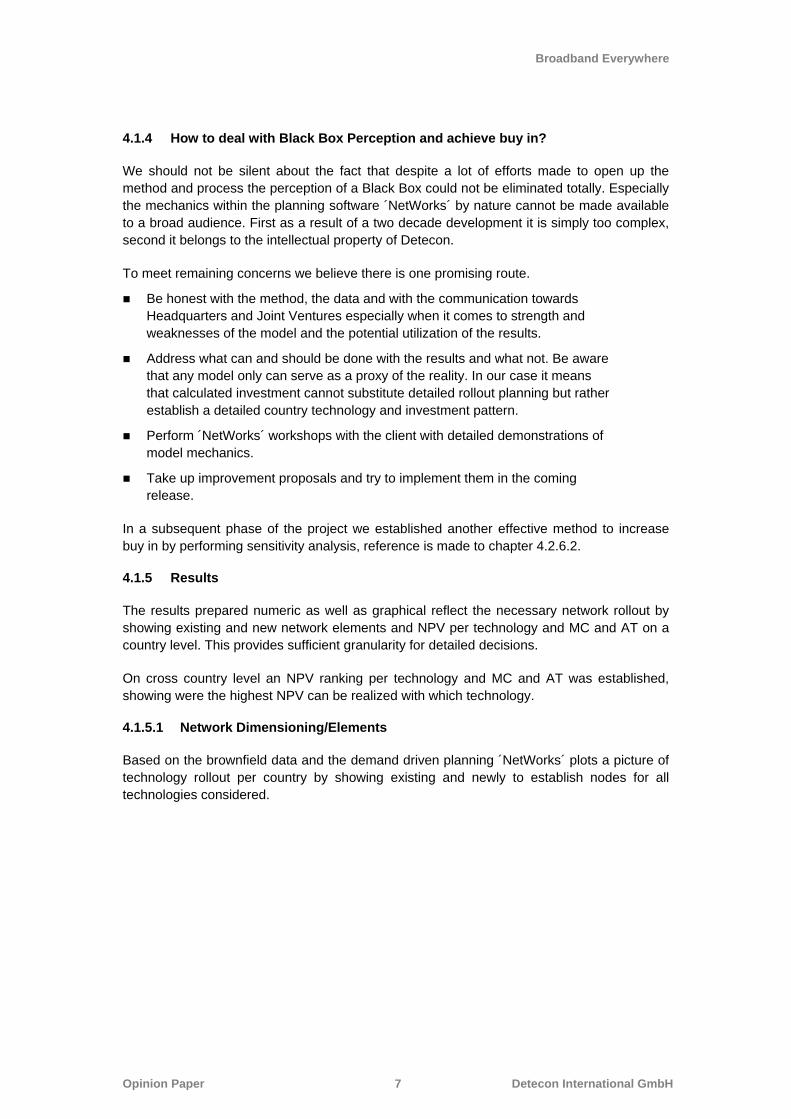

4.1.5.1 Network Dimensioning/Elements

Based on the brownfield data and the demand driven planning ´NetWorks´ plots a picture of

technology rollout per country by showing existing and newly to establish nodes for all

technologies considered.

Broadband Everywhere

Opinion Paper 8 Detecon International GmbH

Figure 7: Existing and new Network Nodes per Technology (Example)

4.1.5.2 Financial KPI

Building upon the output of topology based cost modeling the financial results can be edited

and processed into a short or mid- term view, supported by the detailed modeling period.

Those short term results comprise of the

Net Adds

Revenues, ARPA/ARPU and

DCC or related KPI such as Average CC/Average Net Adds or Cum.

CC/CAPEX

This short term view in general is equal to the budgeting and planning process of the client

and thus helps to understand and argue the planning numbers.

A second major result is the Net Present Value (NPV) calculation per technology, MC and

AT. The NPV calculation includes the short term period, the extrapolation period and the

Terminal Value (TV).

Optical network is mainly present in the major cities

Other cities have installed limited optical network infrastructure

FTTB/H

The DSL network is based on ADSL and ADSL2+ technologies

xDSL

Three technologies are present in the wireless network GSM 900/1800

UMTS

F-OFDM

The complete nation-wide network is based on defined number of sites providing coverage and capacity

HSPA+

Broadband Everywhere

Opinion Paper 9 Detecon International GmbH

Figure 8: Development of financial KPI

The NPV view allows to determine

a so called „Demand Case‟ which shows the CAPEX needs if all market

demand would be served and

the ´NPV Case´ displays where only the demand in positive clusters would be

served.

The combination of both values shows the range, where the actual invest can be expected,

since they refer to worst and best case, respectively.

Figure 9: Example of a VDSL NPV Case (Cash in/out development over time is shown)

Development of financial KPM

id-T

erm

20

10

-2

01

4

Country

KPI

Net Adds

ARPU/ARPA

Revenue

CAPEX

OPEX

Disc. Cash Contrib.

Technology

HSPA+

Municipality Cluster

VDSL

Area Type FTTH

Lo

ng

-Te

rm

Country HSPA+

Municipality Cluster VDSL

Area Type FTTH

Segments

Revenue

CAPEX

OPEX

Disc. Cash Contribution

NPV

Relevant KPIs

10

5

0

-5

-10

-15

-20

15

10

5

0

-5

-10

-15

-20

2928272625

15

242322212019181716151413121110

CAPEXRevenuesCash Contribution OPEX

Total CAPEX 2010-2014 = mEUR 31,4Total CAPEX 2010-2029 = mEUR 45,2

TV = mEUR 3,7; NPV = mEUR 30,5

Broadband Everywhere

Opinion Paper 10 Detecon International GmbH

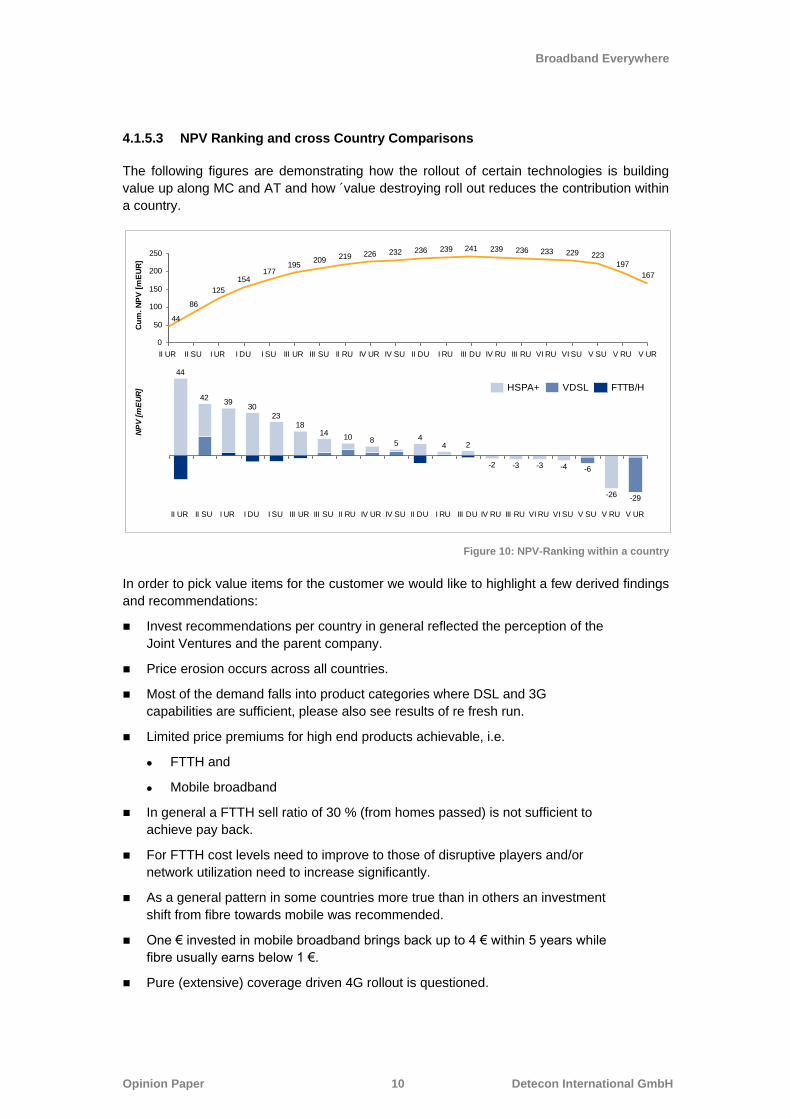

4.1.5.3 NPV Ranking and cross Country Comparisons

The following figures are demonstrating how the rollout of certain technologies is building

value up along MC and AT and how ´value destroying roll out reduces the contribution within

a country.

Figure 10: NPV-Ranking within a country

In order to pick value items for the customer we would like to highlight a few derived findings

and recommendations:

Invest recommendations per country in general reflected the perception of the

Joint Ventures and the parent company.

Price erosion occurs across all countries.

Most of the demand falls into product categories where DSL and 3G

capabilities are sufficient, please also see results of re fresh run.

Limited price premiums for high end products achievable, i.e.

FTTH and

Mobile broadband

In general a FTTH sell ratio of 30 % (from homes passed) is not sufficient to

achieve pay back.

For FTTH cost levels need to improve to those of disruptive players and/or

network utilization need to increase significantly.

As a general pattern in some countries more true than in others an investment

shift from fibre towards mobile was recommended.

One € invested in mobile broadband brings back up to 4 € within 5 years while

fibre usually earns below 1 €.

Pure (extensive) coverage driven 4G rollout is questioned.

V UR

-29

V RU

-26

V SU

-6

VI SU

-4

VI RU

-3

III RU

-3

IV RU

-2

III DU

2

I RU

4

II DU

4

IV SU

5

IV UR

8

II RU

10

III SU

14

III UR

18

I SU

23

I DU

30

I UR

39

II SU

42

II UR

44

200

150

100

50

250

0

V UR

167

V RU

197

V SU

223

VI SU

229

VI RU

233

III RU

236

IV RU

239

III DU

241

I RU

239

II DU

236

IV SU

232

IV UR

226

II RU

219

III SU

209

III UR

195

I SU

177

I DU

154

I UR

125

II SU

86

II UR

44

FTTB/HVDSLHSPA+

Cu

m. N

PV

[m

EU

R]

NP

V [m

EU

R]

Broadband Everywhere

Opinion Paper 11 Detecon International GmbH

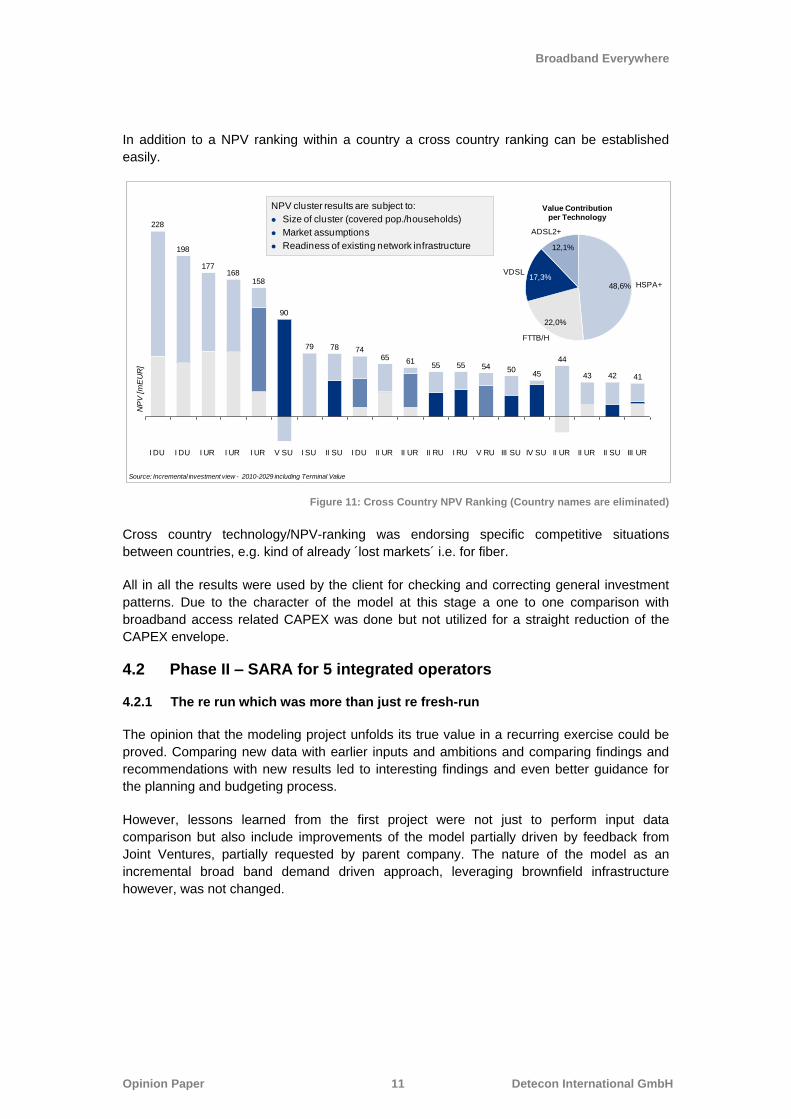

In addition to a NPV ranking within a country a cross country ranking can be established

easily.

Figure 11: Cross Country NPV Ranking (Country names are eliminated)

Cross country technology/NPV-ranking was endorsing specific competitive situations

between countries, e.g. kind of already ´lost markets´ i.e. for fiber.

All in all the results were used by the client for checking and correcting general investment

patterns. Due to the character of the model at this stage a one to one comparison with

broadband access related CAPEX was done but not utilized for a straight reduction of the

CAPEX envelope.

4.2 Phase II – SARA for 5 integrated operators

4.2.1 The re run which was more than just re fresh-run

The opinion that the modeling project unfolds its true value in a recurring exercise could be

proved. Comparing new data with earlier inputs and ambitions and comparing findings and

recommendations with new results led to interesting findings and even better guidance for

the planning and budgeting process.

However, lessons learned from the first project were not just to perform input data

comparison but also include improvements of the model partially driven by feedback from

Joint Ventures, partially requested by parent company. The nature of the model as an

incremental broad band demand driven approach, leveraging brownfield infrastructure

however, was not changed.

43

II UR

44

III UR

41

II SU

42

II URII UR

65

I DU

74

II SU

78

I SU

79

V SU

90

I UR

158

I UR

168

I UR

177

I DU

198

I DU

228

IV SU

45

III SU

50

V RU

54

I RU

55

II RU

55

II UR

61

ADSL2+

12,1%

VDSL17,3%

FTTB/H

22,0%

HSPA+48,6%

Value Contributionper Technology

NP

V [m

EU

R]

NPV cluster results are subject to:

Size of cluster (covered pop./households)

Market assumptions

Readiness of existing network infrastructure

Source: Incremental investment view - 2010-2029 including Terminal Value

Broadband Everywhere

Opinion Paper 12 Detecon International GmbH

4.2.2 Improvements

The detailed modeling period remained to be 5 years - now two years ahead. Also the

extrapolation period and the structure of Product Groups were not changed. However, some

improvements reflecting feedback and requests were implemented. The most important ones

are listed below.

Considering fix mobile substitution in the technology mapping according to

judgement of the Joint Ventures.

Inclusion of wholesale as it contributes to the efficient utilization of investments

as time-variant portion of retail-subscriber and revenue at MC-level.

Support time-variant utilization ratios homes-passed to homes-connected for

the detailed modelling period.

Time-variant Wifi off-load at MC-level of mobile traffic

Taking into account fix-network Next Generation Access Regulation by

additional capacity/investment requirements.

Inclusion of mobile spectrum one time and annual fee in addition.

TV channel license fee for IPTV services.

CATV ED3 proxy modelling ED3

Output and reports were improved also.

In order to meet the increased demand for output additional reports were created and all

results were handed over as Excel files as well. Examples

Coverage numbers

New and co-location site number 3G and LTE respectively

Existing and new Street cabinets

Homes passed, homes connected FTTH respectively (FTTC is applicable for

VDSL)

Traffic volume (TB per year or busy hour network traffic GB/s or busy hour

traffic per customer 3G and LTE respectively),

The major portion of further development however, lies in the adjusted design of the model,

i.e. ´NetWorks´.

4.2.3 Model design

Taken into account technology evolution and the new requirements the model was developed further.

Broadband Everywhere

Opinion Paper 13 Detecon International GmbH

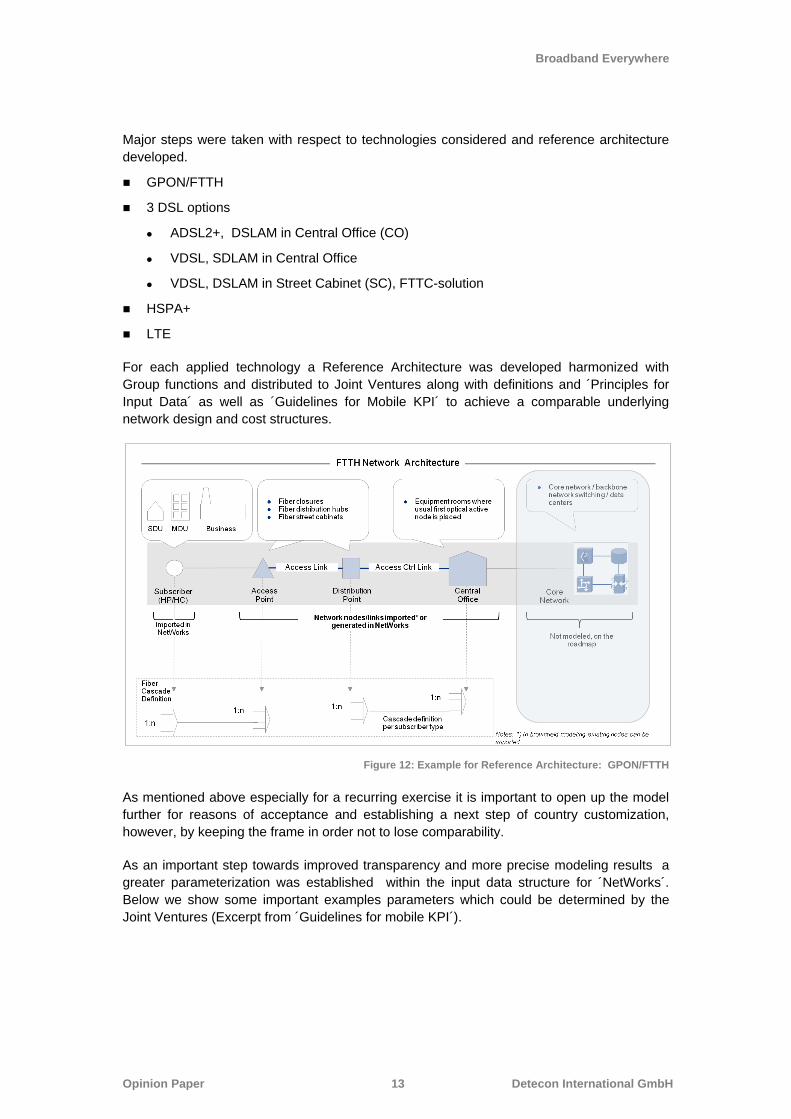

Major steps were taken with respect to technologies considered and reference architecture

developed.

GPON/FTTH

3 DSL options

ADSL2+, DSLAM in Central Office (CO)

VDSL, SDLAM in Central Office

VDSL, DSLAM in Street Cabinet (SC), FTTC-solution

HSPA+

LTE

For each applied technology a Reference Architecture was developed harmonized with

Group functions and distributed to Joint Ventures along with definitions and ´Principles for

Input Data´ as well as ´Guidelines for Mobile KPI´ to achieve a comparable underlying

network design and cost structures.

Figure 12: Example for Reference Architecture: GPON/FTTH

As mentioned above especially for a recurring exercise it is important to open up the model

further for reasons of acceptance and establishing a next step of country customization,

however, by keeping the frame in order not to lose comparability.

As an important step towards improved transparency and more precise modeling results a

greater parameterization was established within the input data structure for ´NetWorks´.

Below we show some important examples parameters which could be determined by the

Joint Ventures (Excerpt from ´Guidelines for mobile KPI´).

Broadband Everywhere

Opinion Paper 14 Detecon International GmbH

Site Area and Scaling Factor

The site area and the site area scaling factors can be used to calculate a maximum area per

site so that the minimum number of sites needed to cover a certain area can be determined.

By applying specific factors for HSPA+ and LTE frequencies in most of the case the

combined value of the site area and site area scaling factor is representative of the network

being modelled.

Since the scaling factors for area are defined per municipality cluster and area type, a

detailed modelling is possible. The combination of site area and scaling factor is used to

model frequency plans like shown in the following table. Frequency plans strongly depend on

available frequencies and obligations.

Table 1: Frequencies and bands used for different municipality clusters and environments

Site Capacity and Scaling Factor

The site capacity parameters are used for calculation the minimum number of sites needed

to support a certain traffic level in a particular area. It changes similar to the site area over

municipality cluster and area type and is mainly reflected by the bandwidth value (5 or 10

MHz) given in the previous table.

Maximum Utilization Factor

The ´NetWorks´ tool calculates the number of sites needed to support a certain traffic level in

a given area by dividing the total area traffic by the product of the utilization and carrier

capacity, considering also the number of carriers and number of sectors per site.

As an example a 100% utilized cell capacity cannot be filled in all sites for a number of

reasons.

At 100% utilization the user experience in a given sector is very poor. Usually,

it is recommended an individual carrier should not typically be utilized at more

than 70% during the busy hour.

The traffic distribution over the sectors of a given site is uneven. Typically in a

three sectored site there might be one sector that carries 50% of the site traffic,

so that when that sector is fully loaded, that average site capacity utilization is

67%.

Dense urban Urban Suburban Rural

Cluster 1:

Metropolitan Cities

2600 MHz

10 Mhz

2600 MHz

10 Mhz

2600 MHz

10 Mhz

1800 MHz

10 Mhz

Cluster 2:

Major Cities

2600 MHz

10 Mhz

2600 MHz

10 Mhz

2600 MHz

10 Mhz

1800 MHz

10 Mhz

Cluster 3:

Big Cities

2600 MHz

10 Mhz

2600 MHz

10 Mhz

1800 MHz

10 Mhz

1800 MHz

10 Mhz

Cluster 4: Medium

Cities

1800 MHz

10 Mhz

1800 MHz

10 Mhz

800 MHz

10 Mhz

800 MHz

10 Mhz

Cluster 5:

Small Cities

1800 MHz

10 Mhz

800 MHz

10 Mhz

800 MHz

5 Mhz

800 MHz

5 Mhz

Cluster 6:

Villages

800 MHz

10 Mhz

800 MHz

10 Mhz

800 MHz

5 Mhz

800 MHz

5 Mhz

Broadband Everywhere

Opinion Paper 15 Detecon International GmbH

The traffic distribution over the sites in a given area is uneven. Some site

maybe approaching their capacity limit, while other sites might have reached

their capacity limit recently, and cell splits or carrier expansions might have

been deployed. To account for this variability from site to site, a further

utilization factor of 75% can be considered.

Individual sectors have different busy hours to the overall network busy hour so

that the summed cell BH traffic exceeds the core network BH traffic.

The Maximum Utilization Factor should consider the combination of the above effects. As a

result an utilization value exceeding 50% was not recommended by experts. However, it is

advisable to give these numbers only as a guidance and leave it to the Joint Ventures to fill it

with their own planning assumptions. During the modeling we found utilization assumptions

ranging from 25 % to 50%.

On the NPV judgment side we believe it was important to take into account that the results of

a model always will be a proxy of the reality. Therefore we calculated the results for an

´Optimized Scenario´ instead of a sharp separation of NPV=0 per area type, by developing a

sound ratio of a negative NPV to the investment volume. A NPV to CAPEX ratio (NPV

divided by total cumulative CAPEX) of above -10 percentage was applied as hurdle for the

NPV case.

4.2.4 Process

In such a recurring project it is important to always aim for improvement of the data collection

and harmonization process as well. This time Detecon conducted one ´ramp up´ and

alignment visit per Joint Venture prior to commercial and technical input data fill. Fitting to

the central model but allowing more customization the tasks listed below were performed:

Communication of central modelling parameter to all participants ,

Find out country specific specifications and

Develop and discuss and data filling guidelines

4.2.5 Input data guidance and reconciliation

Next to the definitions in the input sheets ´Principles for Input Data´ and ´Guidelines for

mobile KPI´ were designed to give guidance for the input data. Typical examples from the

input principles are

Source of commercial input data, i.e. Forecast 2012

Comparison with Planning data 2011 and 2012

Handling of CPE expenses

Utilization definitions for fixed network architecture

More choice usually opens up for more interpretations and even misunderstandings which

only partially could be offset by definitions and guidelines provided. Therefore the input data

reconciliation, including reconciliation with relevant group functions resulted in numerous

teleconferences and required significant more time than expected.

Broadband Everywhere

Opinion Paper 16 Detecon International GmbH

4.2.6 Results

Due to the fact that the technology portfolio was more up to date, 3 DSL options were

offered, LTE technology was in scope and more modeling parameters were offered the

results improved compared to the first project significantly. The results were accepted by the

Steering Committee and the next phase was envisaged.

In a subsequent work Detecon prepared the comparison of technical and marketing input

parameters. Price information for network elements and value drivers such as ARPU/ARPA

puts the shareholder into the position to compare the effectiveness and the value of the

operations. The JVs are able to compare themselves with other operations.

In particular the following results were acknowledged by the Steering Committee:

NPV improvement throughout

Re-visited cost levels and revenue forecasts in some JVs

Re-modelling with updated inputs based on the results created transparent

way of iteration

Risk and opportunity review

The model showed exposure due to volatility, regulatory environment

(including license fee, unbundling) and operational risks

The model showed opportunities like Fixed Mobile Substitution (FMS), cost

benchmark, project profitability ranking including mobile spectrum costs and

wholesale, NPV improvement and advantages of vectoring in a strong copper

environment

CAPEX driven by business demand

Better aligned projects to maximize broadband customer reach and profitability

Improved cost levels and incremental revenue enabled more NPV positive

CAPEX

4.2.6.1 Financials

Similar to the first project the financial results can be edited and processed into a short or

mid- term view by technology applied, supported by the detailed modeling period. Those

short term results comprise of the

Net Adds

Revenues, ARPA/ARPU and

DCC or related KPI such as Average Cash Contribution (CC)/Average Net

Adds or Cum. CC/CAPEX

This view in general is equal to the budgeting and planning process of the client and thus helps to understand and argue the planning numbers. The long term view - the NPV calculation was done per technology, MC and AT. As mentioned above the deciding NPV-trigger is not zero anymore but following a ratio of a negative NPV to related revenue. As examples we refer to results of mobile technology.

Broadband Everywhere

Opinion Paper 17 Detecon International GmbH

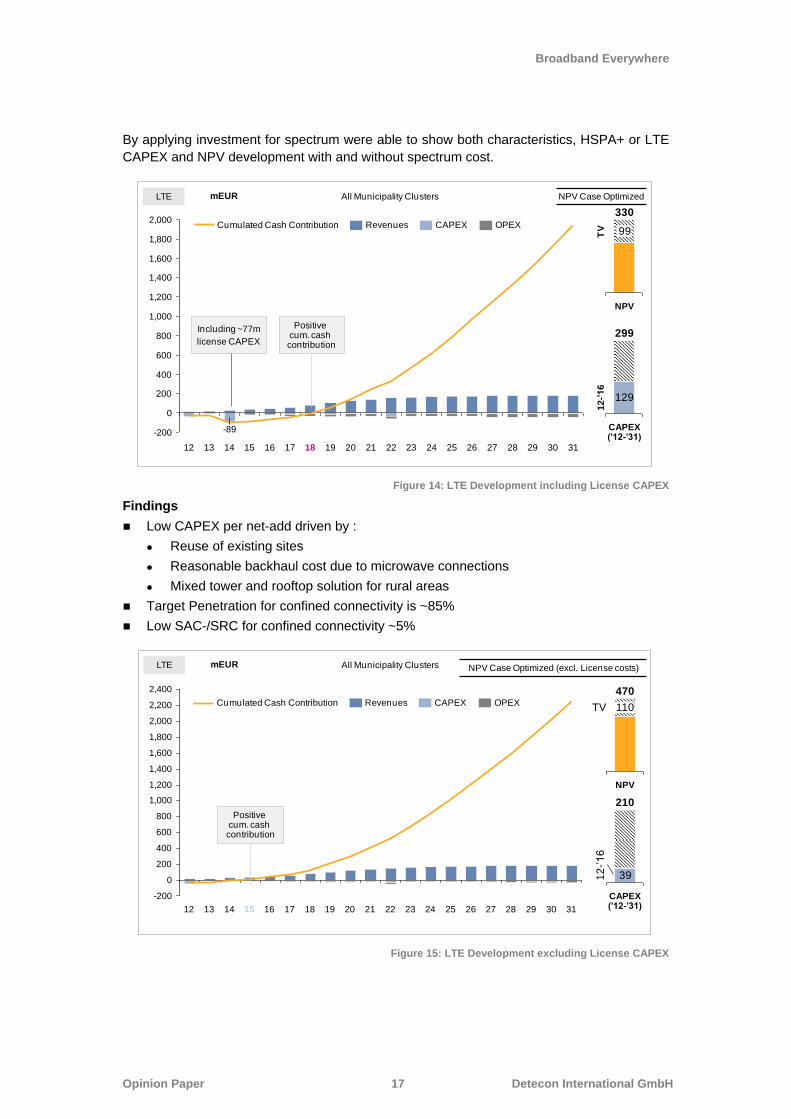

By applying investment for spectrum were able to show both characteristics, HSPA+ or LTE

CAPEX and NPV development with and without spectrum cost.

Figure 14: LTE Development including License CAPEX

Findings

Low CAPEX per net-add driven by :

Reuse of existing sites

Reasonable backhaul cost due to microwave connections

Mixed tower and rooftop solution for rural areas

Target Penetration for confined connectivity is ~85%

Low SAC-/SRC for confined connectivity ~5%

Figure 15: LTE Development excluding License CAPEX

NPV Case Optimized

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

-200

31302928272625

2,000

2423222120191817161514

-89

1312

OPEXCAPEXRevenuesCumulated Cash Contribution

All Municipality ClustersmEUR

TV

NPV

330

99

12

-’16

CAPEX (’12-’31)

299

129

Including ~77m

license CAPEX

Positive cum. cash contribution

LTE

NPV Case Optimized (excl. License costs)

2,400

2,200

2,000

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

-200

3130292827262524232221201918171615141312

OPEXCAPEXRevenuesCumulated Cash ContributionTV

NPV

470

110

12

-‟1

6

CAPEX (’12-’31)

210

39

Positive cum. cash contribution

All Municipality ClustersmEURLTE

Broadband Everywhere

Opinion Paper 18 Detecon International GmbH

The ´old truth´ applies here as well. CAPEX not spent for spectrum can be allocated for the

coverage of areas.

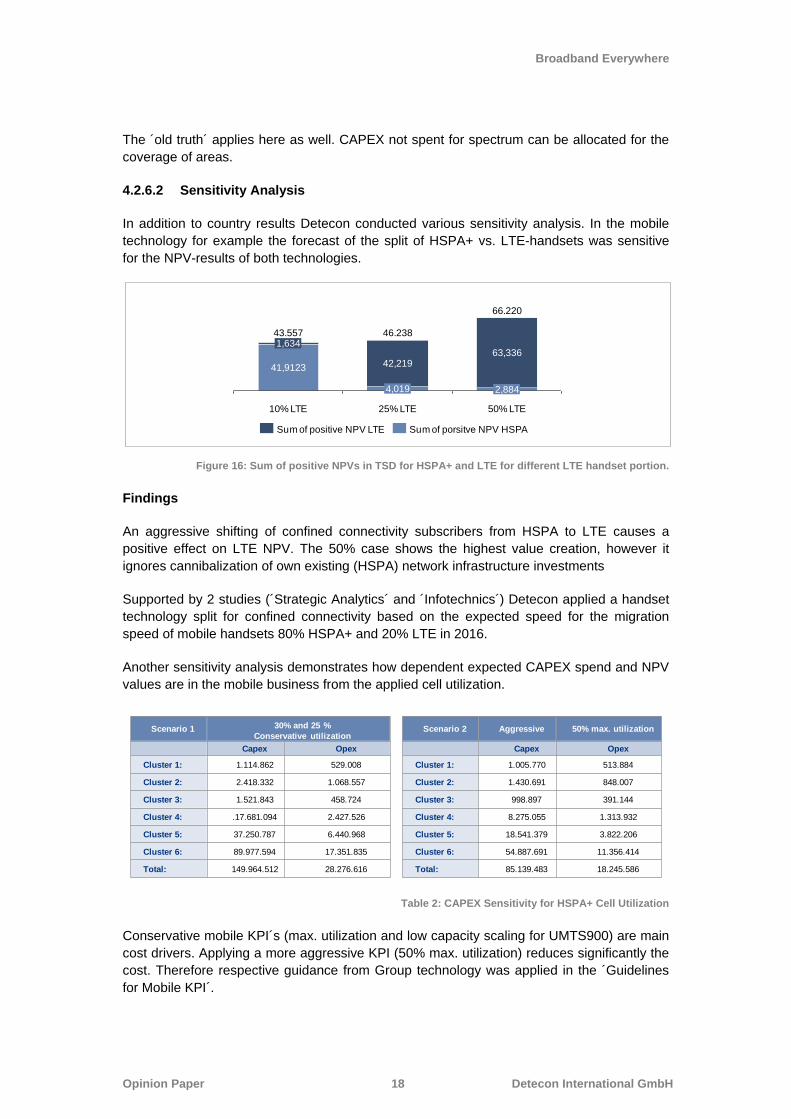

4.2.6.2 Sensitivity Analysis

In addition to country results Detecon conducted various sensitivity analysis. In the mobile

technology for example the forecast of the split of HSPA+ vs. LTE-handsets was sensitive

for the NPV-results of both technologies.

Figure 16: Sum of positive NPVs in TSD for HSPA+ and LTE for different LTE handset portion.

Findings

An aggressive shifting of confined connectivity subscribers from HSPA to LTE causes a

positive effect on LTE NPV. The 50% case shows the highest value creation, however it

ignores cannibalization of own existing (HSPA) network infrastructure investments

Supported by 2 studies (´Strategic Analytics´ and ´Infotechnics´) Detecon applied a handset

technology split for confined connectivity based on the expected speed for the migration

speed of mobile handsets 80% HSPA+ and 20% LTE in 2016.

Another sensitivity analysis demonstrates how dependent expected CAPEX spend and NPV

values are in the mobile business from the applied cell utilization.

Table 2: CAPEX Sensitivity for HSPA+ Cell Utilization

Conservative mobile KPI´s (max. utilization and low capacity scaling for UMTS900) are main

cost drivers. Applying a more aggressive KPI (50% max. utilization) reduces significantly the

cost. Therefore respective guidance from Group technology was applied in the ´Guidelines

for Mobile KPI´.

41,9123

2,884

25% LTE

63,336

4,019

50% LTE10% LTE

1,634

42,219

46.238

66.220

43.557

Sum of positive NPV LTE Sum of porsitve NPV HSPA

Scenario 2 Aggressive 50% max. utilization

Capex Opex

Cluster 1: 1.005.770 513.884

Cluster 2: 1.430.691 848.007

Cluster 3: 998.897 391.144

Cluster 4: 8.275.055 1.313.932

Cluster 5: 18.541.379 3.822.206

Cluster 6: 54.887.691 11.356.414

Total: 85.139.483 18.245.586

Scenario 1 30% and 25 %

Conservative utilization

Capex Opex

Cluster 1: 1.114.862 529.008

Cluster 2: 2.418.332 1.068.557

Cluster 3: 1.521.843 458.724

Cluster 4: .17.681.094 2.427.526

Cluster 5: 37.250.787 6.440.968

Cluster 6: 89.977.594 17.351.835

Total: 149.964.512 28.276.616

Broadband Everywhere

Opinion Paper 19 Detecon International GmbH

5 Lessons learned

5.1 Process set up

This project was initiated by financial department, but requires input from marketing and

technology. A clear definition of process and responsibilities will improve the project

performance. An earlier alignment with central marketing and technology functions will

speed up preparation of the data filling guidelines.

5.2 Alignment steps

It was proven that the opening of the modeling parameter was beneficial, however, at the

same time it became clear that this phase is essential for the success of the project.

Therefore more time must be considered for data collection and alignment.

An effective cooperation and alignment with marketing and technology departments supports

to save the data collection time and increase the input quality, while avoiding additional

discussions or reruns after the result presentation.

5.3 Data filling Guidelines

To avoid the misunderstanding with the input data template, it is proven that a guideline for

data filling is very helpful. It is even better if the head-quarter (shareholder) prepares a

centralized guideline especially for technical parameters by giving space for parameters

reflecting the local situation.

Broadband Everywhere

Opinion Paper 20 Detecon International GmbH

6 Outlook

Since SARA is established as a recurring tool for investments pattern, CAPEX allocation and

efficiency in JVs operations related to broadband roll out it is important to further develop the

model and improve the data mining and modeling process mainly along the lessons learned

so far without increasing complexity too much.

In our opinion the already discussed stronger involvement of central and technology

functions of the HQ will further increase the benefits through better guidelines for critical

parameters. With respect to the clustering of the countries into 6 MCs an addition of

additional 3 Clusters for Metropolitan, Major and Big Cities with intense CATV competition

need to be checked in order to respond to specific competitive challenges on the fixed line

side.

At the marketing side in particular an improvement of the market modeling and a stronger

coupling with SARA would decrease the effort at the JV side.

At the technology side we consider it as an ideal solution if central technology group would

take ownership for the technical data filling guidelines.

Model design

Based on project feed backs some further model adjustments seem to be justified. Next to

some minor adjustments and prior to the next run a few options need to be evaluated such

as.

For polygon instead of radial planning, especially for fixed line a switch to geo

based clutter seems to be necessary to reflect density specifics of cities. If

input data can be made available for the respective countries, Detecon

considers the use of the ArcGIS tool to improve the regionalization.

Enter into a multi technology modeling per area; consider a second technology

for non profitable first technology choices.

Improve CATV modeling while shifting it from a proxy calculation towards a

´NetWorks´ modeling.

Integrated aggregation network planning, if the benefit is tangible.

Check the possibility of devise driven input on the mobile side such as new add numbers for Confined Connectivity/Smart phone penetration.

Broadband Everywhere

Opinion Paper 21 Detecon International GmbH

7 Authors

Horst Hermann, now independent telecommunications expert, used to work as Principal

with Detecon in Cologne. His background ranges from Telecommunications Strategies,

Regulatory, Finance, M&A, Post Merger Integration and Corporate Governance. Within

Detecon his main focus was acquisition and broadband access modeling. Horst Hermann

continues to stay in close contact with Detecon.

He can be reached +49 151 14805360 or [email protected]

Dr. Rong Zhao joined in Detecon International GmbH in Germany in 2008, with focus on

fixed access, transport networks and cost modeling. His expertise covers FTTx strategic

planning and optimization, migration to FTTH, fixed and mobile cost modeling, and network

rollout. He is involved in a number of projects in Europe, MENA and Asia. Since 2012, he

has been the Vice Chair of Deployment & Operations Committee by FTTH Council Europe.

He is also the member of VDE/ITG Expert Group 5.2.5 – “Access and Home Networks” in

Germany.

He can be reached +49 170 2276103 or [email protected]

Dr. Mathias Schweigel works as a managing consultant in the group Network Optimization

and Tools and joined Detecon after finishing his PhD in telecommunications in 2004. In

addition to the specification of functions and the training of users in Detecon‟s network

planning and optimization software ´NetWorks´, he supported many Detecon projects that

required the application of planning software for operational as well as strategic questions.

He can be reached at: +49 351 8734 1508 or [email protected].

Broadband Everywhere

Opinion Paper 22 Detecon International GmbH

8 The Company

We make ICT strategies work

Detecon is a consulting company which unites classic management consulting with a high

level of technology expertise.

Our company's history is proof of this: Detecon International is the product of the merger of

the management and IT consulting company Diebold, founded in 1954, and the

telecommunications consultancy Detecon, founded in 1977. Our services focus on

consulting and implementation solutions which are derived from the use of information and

communications technology (ICT). All around the globe, clients from virtually all industries

profit from our holistic know-how in questions of strategy and organizational design and in

the use of state-of-the-art technologies.

Detecon‟s know-how bundles the knowledge from the successful conclusion of management

and ICT projects in more than 160 countries. We are represented globally by subsidiaries,

affiliates, and project offices. Detecon is a subsidiary of T-Systems International, the

business customer brand of Deutsche Telekom. In our capacity as consultants, we are able

to benefit from the infrastructure of a global player spanning our planet.

Know-how and hands-on expertise

The rapid development of information and telecommunications technologies has an

increasingly significant influence on the strategies of companies as well as on the processes

within an organization. The subsequent complex adaptations affect business models and

corporate structures, not only technological applications.

Our services for ICT management encompass classic strategy and organization consulting

as well as the planning and implementation of highly complex, technological ICT

architectures and applications. We are independent of manufacturers and obligated solely to

our client's success.

Detecon International GmbH

Sternengasse 14 - 16

50676 Cologne

Phone: +49 221 9161 0

E-Mail: [email protected]

Internet: www.detecon.com