Year end 30 June Sales (US$m) Pre-tax (US$m) Normalised net (US$m) EPS (US¢) PER (x) DPS (US¢) Yield (%) EV/Sales (x) EV/EBITDA (x) 2006A 431.5 192.1 85.6 100.9 26.9 24.0 0.9 5.1 9.5 2007E 648.6 349.1 143.0 169.0 16.1 59.1 2.2 3.4 5.6 2008E 751.0 437.3 186.0 219.7 12.4 109.9 4.0 2.9 4.6 Source: Seymour Pierce Limited full year forecasts C o m p a n y N o t e 8 M a r c h 2 0 0 7 M e t a l s & M i n i n g Aquarius Platinum Going platinum Aquarius Platinum has grown quickly to become the fifth largest platinum producer in the world. The company has four operations in South Africa and one in Zimbabwe and expects attributable production to grow by over 50% in the next three years. With metal prices expected to remain above long-term historic averages, Aquarius should generate substantial cash flows enabling the company to make acquisitions, or become a significant dividend payer. As we believe that the group’s expansion prospects are not fully reflected in the current share price, we initiate coverage with a Buy recommendation. Thanks to record platinum group metal output of 277,156oz and strong metal prices, Aquarius has seen half-year profits to December 2006 triple to US$85.4m, all but equalling the profit for the full financial year 2006. We expect the strong financial performance to continue through the second halfof FY2007 and for FY2008 to bring further record earnings as production increases. Aquarius is well underway with its aggressive growth strategy at its existing operations. This will see attributable production rise by 57% to just over 700,000oz of platinum, palladium, rhodium and gold in the next three years. The company has reiterated its ongoing efforts to identify a suitable acquisition target, but opportunities within the South African platinum sector are limited and expensive. However, ongoing strong metal prices are changing the perspective on the value of these opportunities. If a suitable target can not be identified, the company has pledged to return excess cash to shareholde rs. We believe that the shares still have considerable upside potential despite the marked rise in recent months , coinciding with strong half-yearnumbers. We have valued the company using both our long-term forecasts for metal prices and the current spot prices. Overall, our valuations range between £14.29 and £21.17/share. From this range, we take £17.86/share as our target price. BUY. BUY 1465p LSE AQP.L No of shares (m) 84.57 Market cap (£m) 1,239.0 Net cash (£m) 54.13 Enterprise value (£m) 1,184.87 (%) 1m 3m 12m FTA relative +6.4 +28.5 +102.7 12 month high/low (p) 1585.0/602.0 Next news Q3 FY2007 production results Business Platinum mining in Southern Africa www.aquariusplatinum.com Price and price relative (2y) AQUARIUS PL AT INUM 8/3/07 M A M J J A S O N D J F M A M J J A S O N D J F 200 400 600 800 1000 1200 1400 1600 PRICE PRICE REL. TO FTSE ALL SHARE - PRICE INDEX Source: DATASTREAM Source : Datastream Contacts Charles Kernot Research Analyst 020 7107 8069 [email protected]Asa BridleResearch Analyst 020 7107 8034 [email protected]

Source: Seymour Pierce Limited full year forecasts

C o m p a n y N o t e

8 M a r c h 2 0 0 7

M e t a l s & M i n i n

g

Aquarius PlatinumGoing platinum

Aquarius Platinum has grown quickly to become the fifth largest

platinum producer in the world. The company has four operations in

South Africa and one in Zimbabwe and expects attributable production

to grow by over 50% in the next three years. With metal prices

expected to remain above long-term historic averages, Aquarius

should generate substantial cash flows enabling the company to make

acquisitions, or become a significant dividend payer. As we believethat the group’s expansion prospects are not fully reflected in the

current share price, we initiate coverage with a Buy recommendation.

Thanks to record platinum group metal output of 277,156oz and strong

metal prices, Aquarius has seen half-year profits to December 2006 triple to

US$85.4m, all but equalling the profit for the full financial year 2006. We

expect the strong financial performance to continue through the second half

of FY2007 and for FY2008 to bring further record earnings as production

increases.

Aquarius is well underway with its aggressive growth strategy at its

existing operations. This will see attributable production rise by 57% to justover 700,000oz of platinum, palladium, rhodium and gold in the next three

years.

The company has reiterated its ongoing efforts to identify a suitable

acquisition target, but opportunities within the South African platinum

sector are limited and expensive. However, ongoing strong metal prices are

changing the perspective on the value of these opportunities. If a suitable

target can not be identified, the company has pledged to return excess cash

to shareholders.

We believe that the shares still have considerable upside potential

despite the marked rise in recent months, coinciding with strong half-year numbers. We have valued the company using both our long-term forecasts

for metal prices and the current spot prices. Overall, our valuations range

between £14.29 and £21.17/share. From this range, we take £17.86/share

as our target price. BUY.

BUY

1465p

LSE AQP.L

No of shares (m) 84.57

Market cap (£m) 1,239.0

Net cash (£m) 54.13

Enterprise value (£m) 1,184.87

(%) 1m 3m 12m

FTA relative +6.4 +28.5 +102.7

12 month high/low (p) 1585.0/602.0

Next news

Q3 FY2007 production results

Business

Platinum mining in Southern Africa

www.aquariusplatinum.com

Price and price relative (2y)

AQUARIUS PL ATINUM 8/3/07

M A M J J A S O N D J F M A M J J A S O N D J F

200

400

600

800

1000

1200

1400

1600

PRICE

PRICE REL. TO FTSE ALL SHARE - PRICE INDEXSource: DATASTREAM

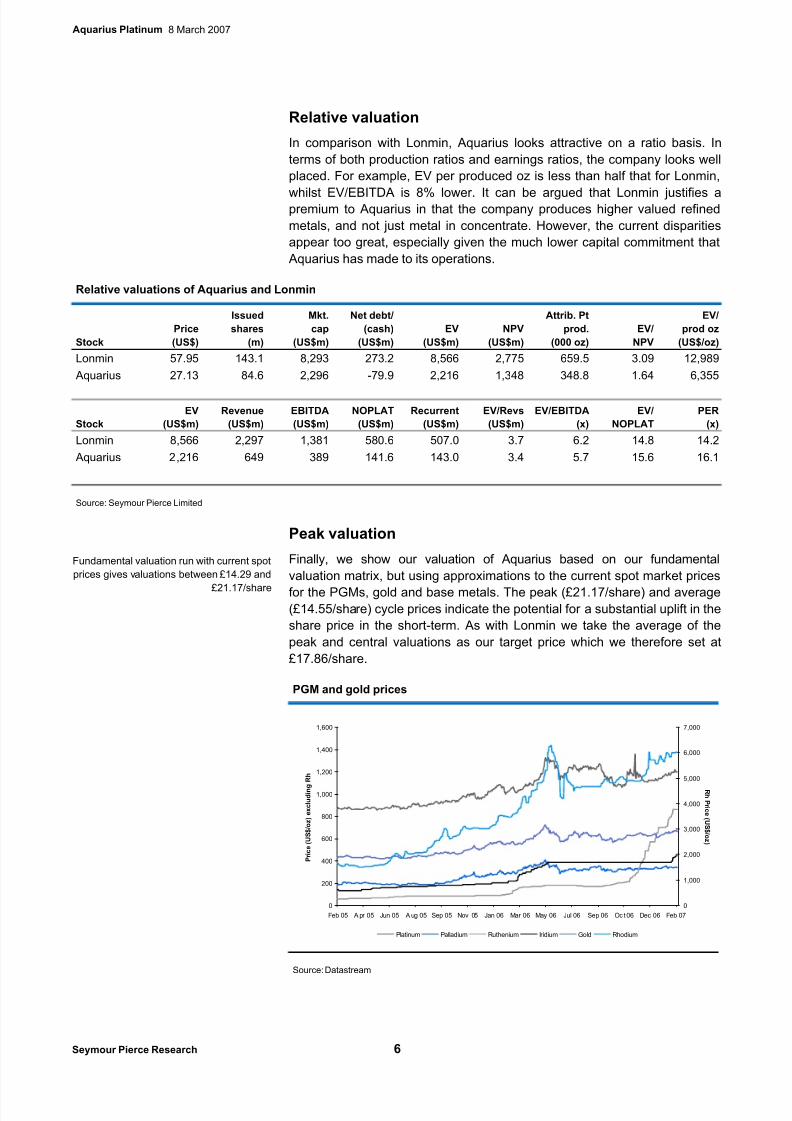

Aquarius is now a well established and significant PGM producer. The

company’s share price has increased substantially in the past twelve

months matching developments at its operations and strengthening

metal prices. We have applied three methodologies to valuing the

company, which involve both fundamental and relative valuation of the

producing assets. We have also attempted to highlight the variation in

valuation that might be expected during a PGM price cycle. Overall, our

valuations for the peak of the cycle range between £14.29/share and

£21.17/share. We take the mid-point as our target price at £17.86/share.

Summary

Assuming that 2007 will represent the peak of the current cycle, our

fundamental valuation implies a target price of £14.28p per share, which

represents a premium to the current price. Our relative valuation also implies

some upside, whilst our peak valuation, using current spot prices extended

over the longer term, gives a cycle peak value of £21.17.

Fundamental valuation

Our fundamental valuation of Aquarius looks at the value of the company

based on long term metrics. PGM prices are a key factor, and in general

terms, we expect the major PGM prices to peak in 2007 before easing to the

bottom of the current cycle in 2010. Prices should then climb steadily for theremainder of the forecast period as the next cycle begins. More detail of our

PGM and base metal price forecasts can be found later in the note, but we

regard these estimates as reasonably conservative.

Foreign exchange must be regarded as the other key factor for Aquarius,

with the majority of costs in South African Rand and Zimbabwean dollars

and metal sales in US dollars. South African producers have benefited from

a weakening of the rand in recent times, which has lowered costs in relative

terms. Our forecasts assume a continuation of this trend over the forecast

period. The hyperinflationary environment in Zimbabwe has led to a series of

devaluations against the US dollar in recent years. Future, relative

movements in the currency are hard to forecast, but we believe costs at thecompany’s Zimbabwean operations in US dollar terms should be

manageable.

The matrix below calculates the valuation of Aquarius on a number of

different bases – in order to generate indications of its peak, trough and

average share prices over the course of a platinum cycle. The multiples are

set in line with those exhibited historically. The discounted cash flow and

price/book valuations also reflect minimum levels for the shares, in order to

reflect takeover potential of the stock. It should be noted that the cash flow

model only includes those funds due to Aquarius from its South African

subsidiary as governed by its stake in the subsidiary. This is set to changeassuming the group’s BEE transaction is completed but, even though

ownership of the subsidiary is set to increase, there are likely to be more

shares in issue, reducing per share valuations back to current levels.

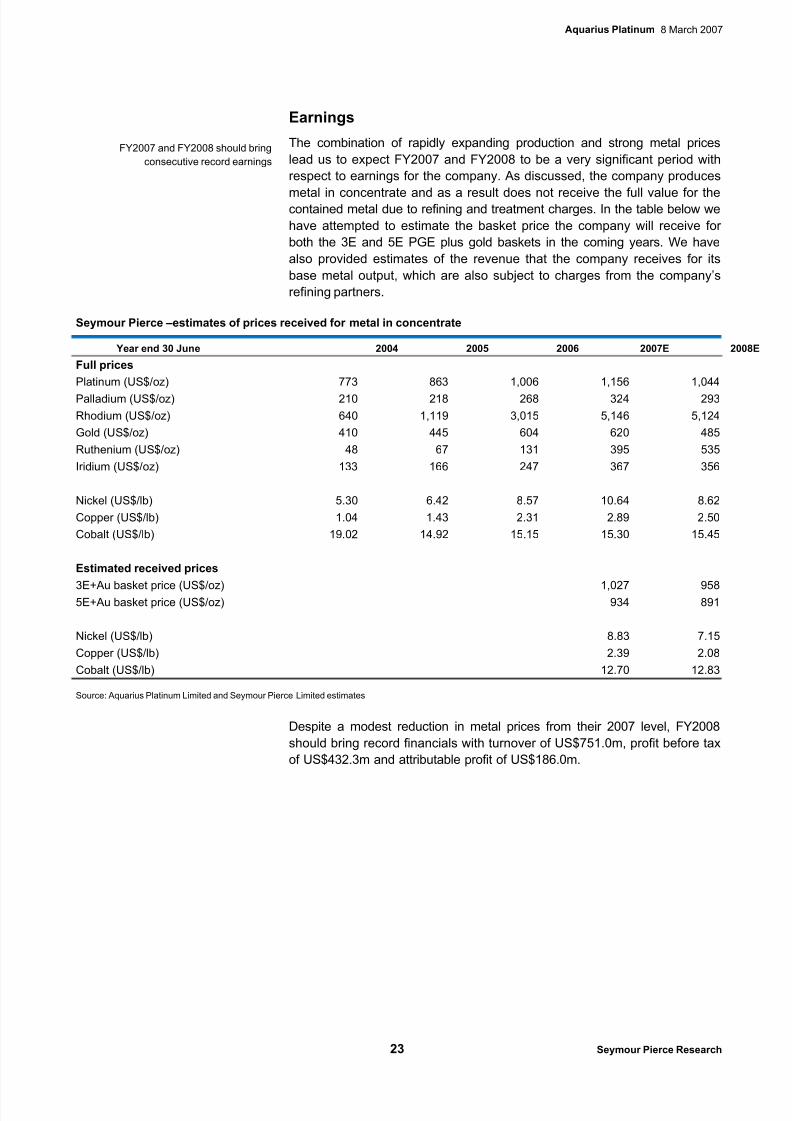

The combination of rapidly expanding production and strong metal prices

lead us to expect FY2007 and FY2008 to be a very significant period with

respect to earnings for the company. As discussed, the company produces

metal in concentrate and as a result does not receive the full value for thecontained metal due to refining and treatment charges. In the table below we

have attempted to estimate the basket price the company will receive for

both the 3E and 5E PGE plus gold baskets in the coming years. We have

also provided estimates of the revenue that the company receives for its

base metal output, which are also subject to charges from the company’s

refining partners.

Seymour Pierce –estimates of prices received for metal in concentrate

Year end 30 June 2004 2005 2006 2007E 2008E

Full prices

Platinum (US$/oz) 773 863 1,006 1,156 1,044

Palladium (US$/oz) 210 218 268 324 293

Rhodium (US$/oz) 640 1,119 3,015 5,146 5,124

Gold (US$/oz) 410 445 604 620 485

Ruthenium (US$/oz) 48 67 131 395 535

Iridium (US$/oz) 133 166 247 367 356

Nickel (US$/lb) 5.30 6.42 8.57 10.64 8.62

Copper (US$/lb) 1.04 1.43 2.31 2.89 2.50

Cobalt (US$/lb) 19.02 14.92 15.15 15.30 15.45

Estimated received prices3E+Au basket price (US$/oz) 1,027 958

5E+Au basket price (US$/oz) 934 891

Nickel (US$/lb) 8.83 7.15

Copper (US$/lb) 2.39 2.08

Cobalt (US$/lb) 12.70 12.83

Source: Aquarius Platinum Limited and Seymour Pierce Limited estimates

Despite a modest reduction in metal prices from their 2007 level, FY2008

should bring record financials with turnover of US$751.0m, profit before tax

of US$432.3m and attributable profit of US$186.0m.

The combination of increasing production and strong metal prices means

Aquarius has the potential to be extremely cash rich in coming years.

Operating cash flow is forecast to rise to US$446.2m in FY2008 and will

continue at a healthy rate thereafter. Best use of the funds is obviously a keystrategy point for Aquarius. The company has already stated its intention to

pay off interest-bearing loans, and we have included full payment of the

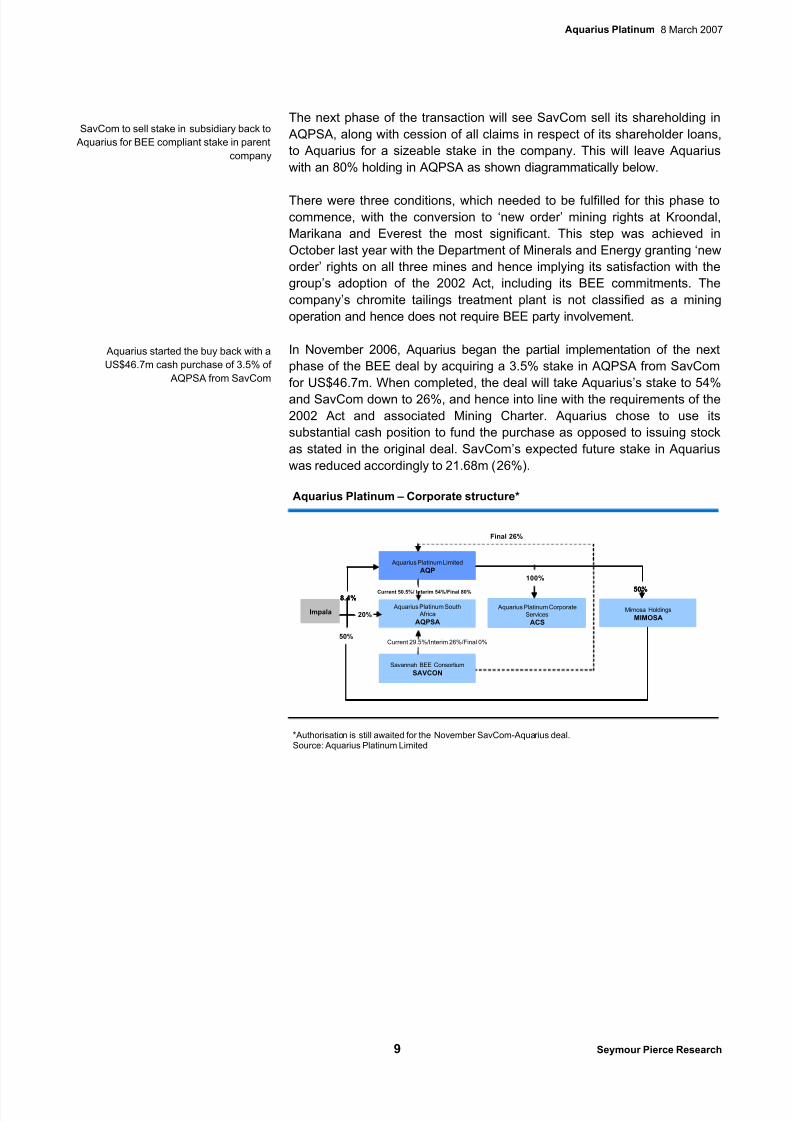

US$13.8m loan from SavCom in the FY2007 cash flow. As discussed, a

cash payment for a small percentage of SavCom’s holding in AQPSA has

also been made. Additional uses include acquisitions and exploration. To

this end the company entered a farm-in agreement with Bakgaga Mining late

last year to conduct exploration and feasibility studies over five farms on the

northern tip of the Bushveld’s western limb. We await news of any significant

acquisitions.

Aquarius Platinum Limited - Cash flow estimates

Year end 30 June (US$m) 2004 2005 2006 2007E 2008E

Operating profit 60.5 30.8 193.3 347.1 432.3

Dep'n and Amor’n 12.2 26.5 28.8 31.2 32.5

Other non-cash 0.0 0.0 0.0 0.0 0.0

Change in working cap 16.6 -17.8 -25.6 -31.3 -18.6

Operating cash flow 89.2 39.5 196.5 347.1 446.2

Net interest -8.4 -3.2 -2.1 2.0 5.1

Dividends -4.8 -5.0 -9.1 -50.1 -93.0

Taxation -3.7 -1.6 -32.0 -104.7 -131.2

-16.9 -9.8 -43.3 -152.8 -219.1

Net capital expenditure -28.5 -92.4 -102.9 -54.6 -30.0

Acquisitions/disposals 18.2 4.3 0.0 0.0 0.0

66.8 -53.5 59.5 189.7 290.0

Debt raised 4.6 28.1 29.1 -13.8 0.0

Shares issued 16.0 31.7 7.2 0.0 0.0

BEE Transaction 0.0 0.0 0.0 -46.7 0.0

Cash flow 82.6 1.4 86.7 79.2 197.1

Forex movements 0.0 -0.9 -2.6 0.0 0.0Cash at start of year 40.3 77.9 78.4 162.4 241.6

Cash at end of year 122.9 78.4 162.4 241.6 438.7

Source: Aquarius Platinum Limited and Seymour Pierce Limited estimates

The key point for shareholders remains the dividend policy the company will

adopt in coming years. Dividend payouts from the other major South African

platinum producers in 2006 ranged between 32% (Lonmin) up to 93%

(Northam) of earnings attributable to ordinary shareholders. Aquarius paid

24% in comparison. Going forward, we have assumed Aquarius will increase

its dividend rate to move into line with its producing peers. A rate equivalent

to Northam’s may be too high, but a rate of 50% would place Aquarius in linewith Impala (48%, excluding special dividends). The company has pledged

to return cash to shareholders if suitable corporate projects can not be

Our research recommendations are issued and approved for distribution within the UnitedKingdom by Seymour Pierce Limited only to market counterparties and intermediate customersas defined under the FSA rules. Our research is not directed at, may not be suitable for andshould not be relied upon by any other person. The information contained in our research iscompiled from a number of sources and is believed to be correct, but cannot be guaranteed. Itis not to be construed as an offer, invitation or solicitation to buy or sell any securities of any of the companies referred to within it. All statements made and opinions expressed are made asat the date on the face of the material and are subject to change without notice. Where pricesof securities are mentioned, these are the mid-market prices as at the close-of-business on the

business day immediately preceding the date of the research. The meanings of our researchratings, together with the proportion of our recommendations issued during the previous quarter carrying each rating, is set out on our website at www.seymourpierce.com. Seymour PierceLimited and/or its associated companies and ultimate holding company may from time-to-timeprovide investment or other services to, or solicit such business from, any of the companiesreferred to in research material. In addition, they and/or their directors and employees and/or any connected persons may have an interest in the securities of any of the companies in thereport and may from time-to-time add to or dispose of such interests. Details of the significantconflicts relating to the companies that we research are set out on our websitewww.seymourpierce.com, together with a summary of our policies for managing conflicts of interest. Seymour Pierce does not meet all of the FSA standards for managing conflicts of interest, as a result our research should not be regarded as an impartial or objectiveassessment of the value or prospects of its subject matter, though of course we will alwaysensure that it remains clear, fair and not misleading.

Seymour Pierce Limited is authorised and regulated by the Financial Services Authority, and isa member of the London Stock Exchange.

Key to material interests

1. The analyst has a personal holding of the securities issued by the company, or of derivativesrelated to such securities.

2. Seymour Pierce Limited or an affiliate owns more than 5% of the issued share capital of thecompany.

3. Seymour Pierce Limited or an affiliate is party to an agreement with the company relating tothe provision of investment banking services, or has been party to such an agreement withinthe past 12 months. Our corporate broking agreements include a provision that we will

prepare and publish research at such times as we consider appropriate.4. Seymour Pierce or an affiliate has been lead manager or co-lead manager of a publiclydisclosed offer of securities for the company within the past 12 months.

5. Seymour Pierce is a market maker or liquidity provider in the securities issued by thecompany.

6. Seymour Pierce is party to an agreement with the company relating to the production of research recommendations.

Distribution of ratingsOur research ratings are defined with reference to the amount by which we expect the absolutereturn to change over the next 12 months:

Rating Definition

Buy Absolute return expected to increase by more than 10%

Outperform Absolute return expected to increase by between 5% and 10%

Hold Absolute return expected to change by between -5% and +5%Underperform Absolute return expected to decrease by between 5% and 10%

Sell Absolute return expected to decrease by more than 10%

As at 31 December 2006 the distribution of all our published recommendations is as follows: