25

Brazil Pharma Institutional Presentation August, 2012

Brazil Pharma

Institutional Presentation

August, 2012

2

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

Shareholder’s Structure Analysis

BTG Pactual + FIPs Managers Operating Partners Free Float

35.7% 36.6% 27.1% 0.6%

100% 100% 100% 100% 100% 100%

Note: Considering 15 millions shares to be issued from Sant’ana’s incorporation.

Company Overview

and Industry

Dynamics

4

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

7.008.30 9.40 10.30 11.20 11.60

13.1014.80

17.2019.20

21.5023.60

26.40

30.20

36.00

43.00

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Sales Performance in the Brazilian Pharmacy Retail Sector from 1996-2011 (R$ Billion)

Drugstores A Growth and Accelerating History

Source: IBGE. Farmácia Popular. Health. OMS IMS. Brazil Banco Central do Brasil

Drivers Micro Timing

Regional Brands Fragmented

Market Formalization and

Consolidation

Drivers Macro

Income Growth Population Aging Generics Drugs

1997 – 2000

1997: Asian Crisis

1998: Russian Crisis

1999: Real Depreciation

2000: Internet Bubble burst

2001 - 2002

2002: Crisis pre-Lula

election

2001: Argentine Default

2003 – 2005

2003-04: First years of

Lula´s election

2004: Mensalão scandal

2006 – 2007

2006: Second Lula

election

2008 – 2011

2008: Subprime

Crisis

2010: Greece Debt

Crisis

5

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

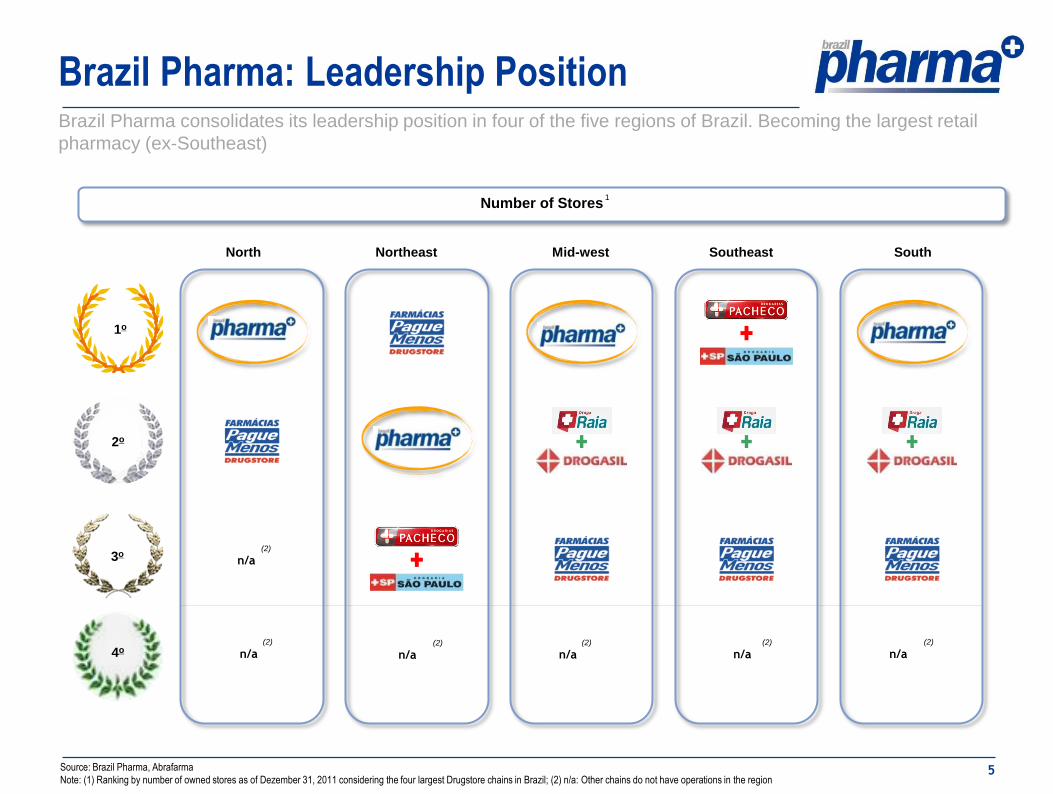

Source: Brazil Pharma, Abrafarma

Note: (1) Ranking by number of owned stores as of Dezember 31, 2011 considering the four largest Drugstore chains in Brazil; (2) n/a: Other chains do not have operations in the region

Brazil Pharma consolidates its leadership position in four of the five regions of Brazil. Becoming the largest retail

pharmacy (ex-Southeast)

Number of Stores 1

4o

2o

1o

Northeast

n/a (2)

3o

North

n/a (2)

n/a (2)

Southeast

n/a (2)

Mid-west

n/a (2)

South

n/a (2)

Brazil Pharma: Leadership Position

6

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

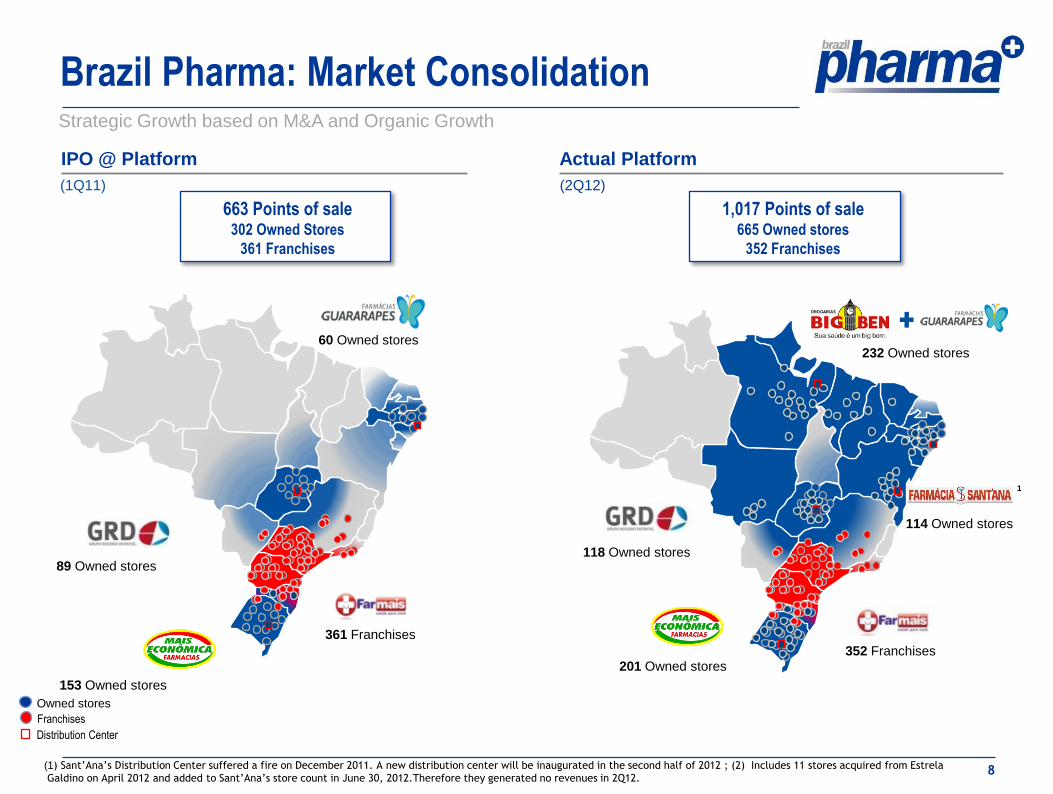

Brazil Pharma: Footprint

86

Largest Drugstore Chain in the Brazilian Retail: Ready to Growth and Consolidating

North 104

Northest 242

Midwest 118

Southeast

South 201

REGIONS Owned stores

10

1

103 20

15

19

10

193

7

75

114

1

8

232 ¹ Owned stores

114 ² Owned stores

118 Owned stores

352 Franchises

201 Owned stores

05³ Distribution centers

Footprint

1.017 stores

665 owned stores

352 Franchises

89

1) Includes 69 stores from Guararapes’ platform ; 2) Includes 11 stores acquired from Estrela Galdino on April 2012 and added to Sant’Ana’s store count in June 30, 2012.Therefore they generated no revenues in

2Q12 ; 3) Sant’Ana’s Distribution Center has suffered a fire on December 2011. A new distribution center will be inaugurated in the second half of 2012.

7

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

Large Growth Capacity

Organic Growth (# owned stores)

Brazil Pharma: Market Penetration

Brazil Pharma Abrafarma

Branded Generics HPC

Diversified Sales Mix

(2Q12)

Market Growth

(CAGR07’-11’)

Maturation of Owned Stores

(2Q12)

Growth already contracted

8

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

Brazil Pharma: Market Consolidation Strategic Growth based on M&A and Organic Growth

663 Points of sale 302 Owned Stores

361 Franchises

IPO @ Platform Actual Platform

201 Owned stores

352 Franchises

232 Owned stores

118 Owned stores

114 Owned stores

1,017 Points of sale 665 Owned stores

352 Franchises

89 Owned stores

60 Owned stores

153 Owned stores

361 Franchises

(1) Sant’Ana’s Distribution Center suffered a fire on December 2011. A new distribution center will be inaugurated in the second half of 2012 ; (2) Includes 11 stores acquired from Estrela

Galdino on April 2012 and added to Sant’Ana’s store count in June 30, 2012.Therefore they generated no revenues in 2Q12.

1

(1Q11) (2Q12)

Distribution Center

Owned stores

Franchises

Focus on Integration

10

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

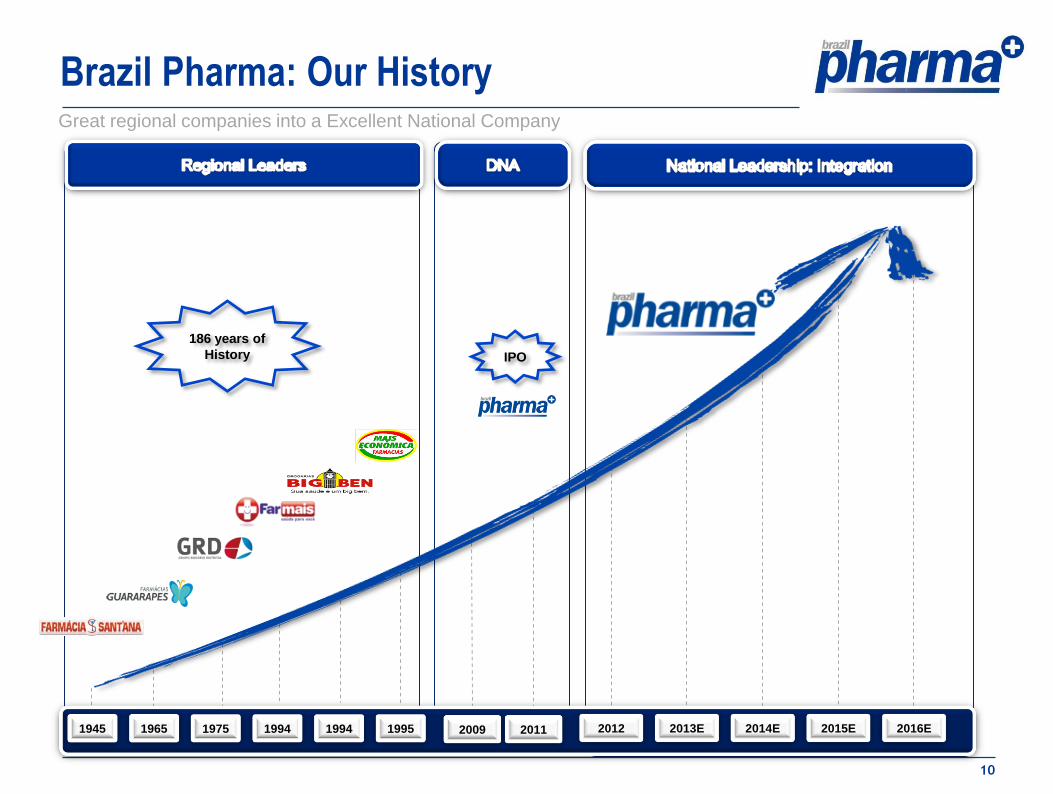

Brazil Pharma: Our History Great regional companies into a Excellent National Company

2012 2013E 2014E 2016E2015E1945 1965 1975 1994

IPO

1994 2009 20111995

186 years of

History

11

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

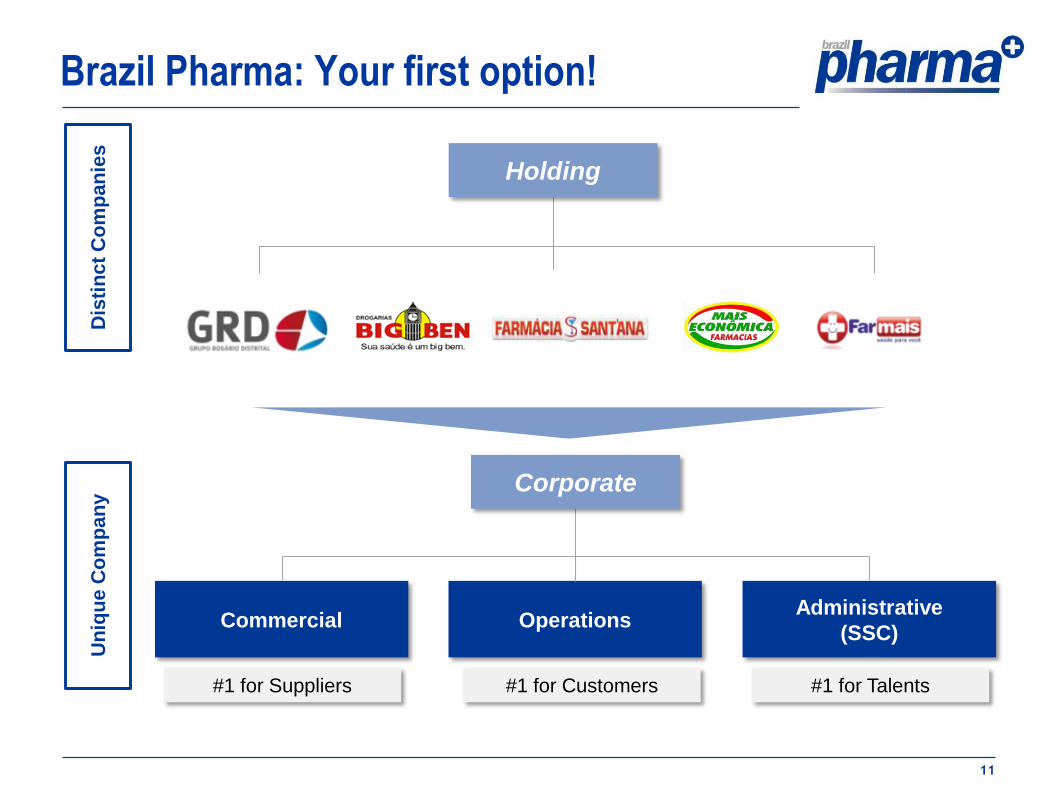

Brazil Pharma: Your first option!

Holding

OperationsAdministrative

(SSC)Commercial

Corporate

#1 for Suppliers #1 for Customers #1 for Talents

Dis

tin

ct

Co

mp

an

ies

Un

iqu

eC

om

pa

ny

12

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

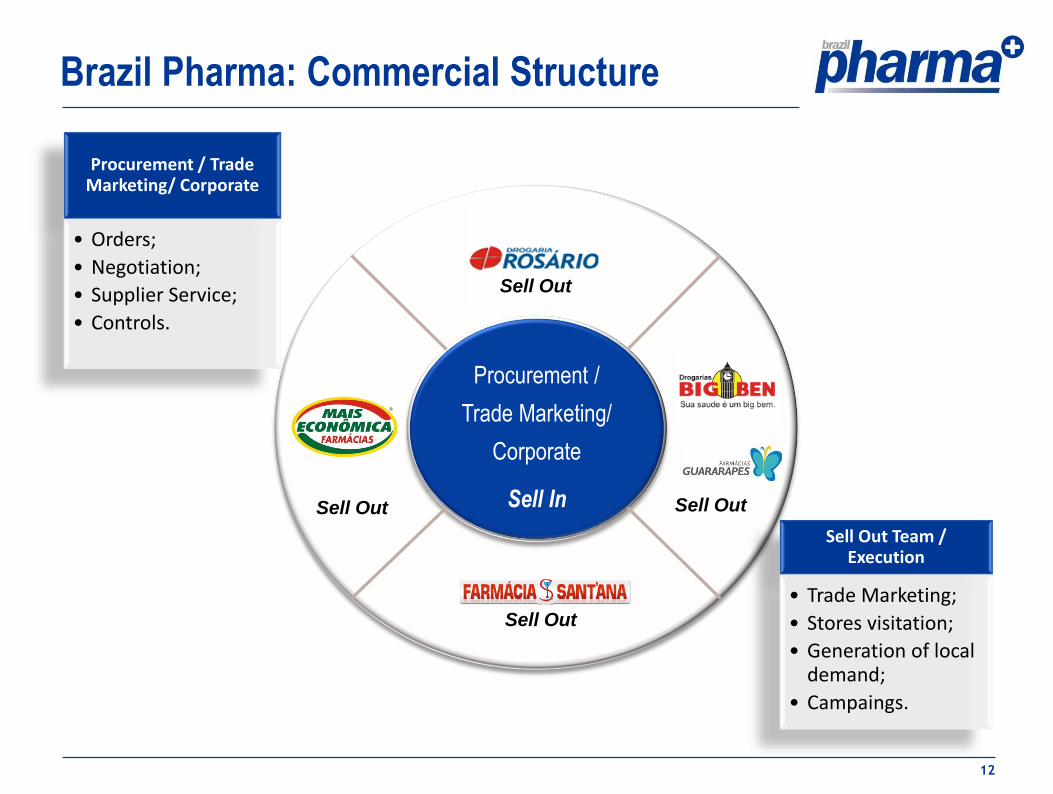

Brazil Pharma: Commercial Structure

Procurement /

Trade Marketing/

Corporate

Sell In

Sell Out Team / Execution

• Trade Marketing;

• Stores visitation;

• Generation of local demand;

• Campaings.

Sell Out

Sell Out

Sell Out

Sell Out

Procurement / Trade Marketing/ Corporate

• Orders;

• Negotiation;

• Supplier Service;

• Controls.

Company

Highlights

14

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

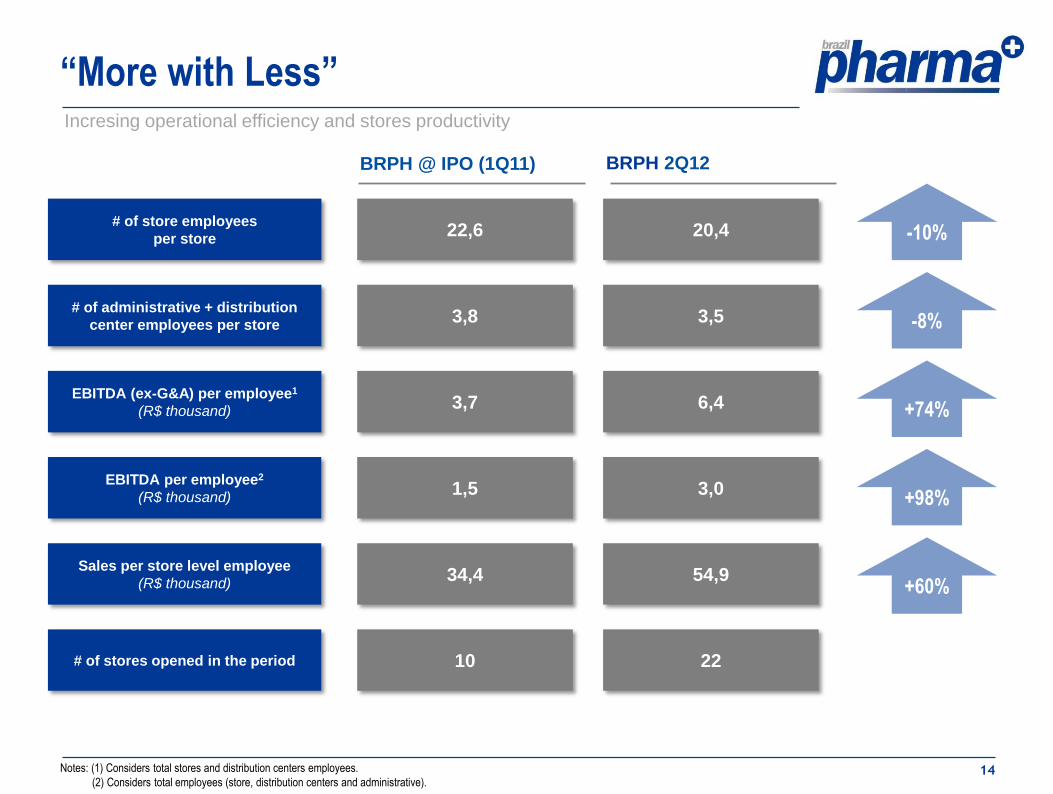

“More with Less” Incresing operational efficiency and stores productivity

Notes: (1) Considers total stores and distribution centers employees.

(2) Considers total employees (store, distribution centers and administrative).

3,8 3,5

3,7 6,4

22,6 20,4

BRPH @ IPO (1Q11)

34,4 54,9

BRPH 2Q12

10 22

1,5 3,0

-10%

-8%

+74%

+98%

+60%

# of administrative + distribution

center employees per store

EBITDA (ex-G&A) per employee1

(R$ thousand)

# of store employees

per store

Sales per store level employee

(R$ thousand)

# of stores opened in the period

EBITDA per employee2

(R$ thousand)

15

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

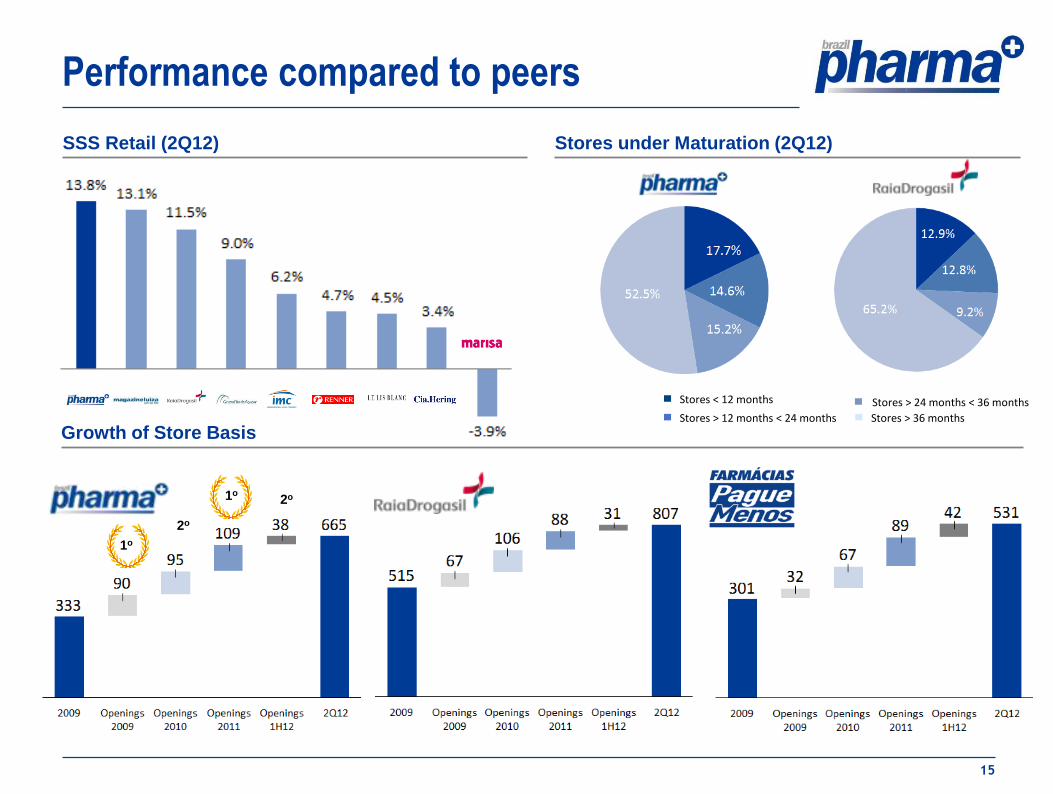

Performance compared to peers

Stores under Maturation (2Q12)

Growth of Store Basis

SSS Retail (2Q12)

Stores < 12 months Stores > 24 months < 36 months

Stores > 12 months < 24 months Stores > 36 months

1o

1o

2o

2o

16

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

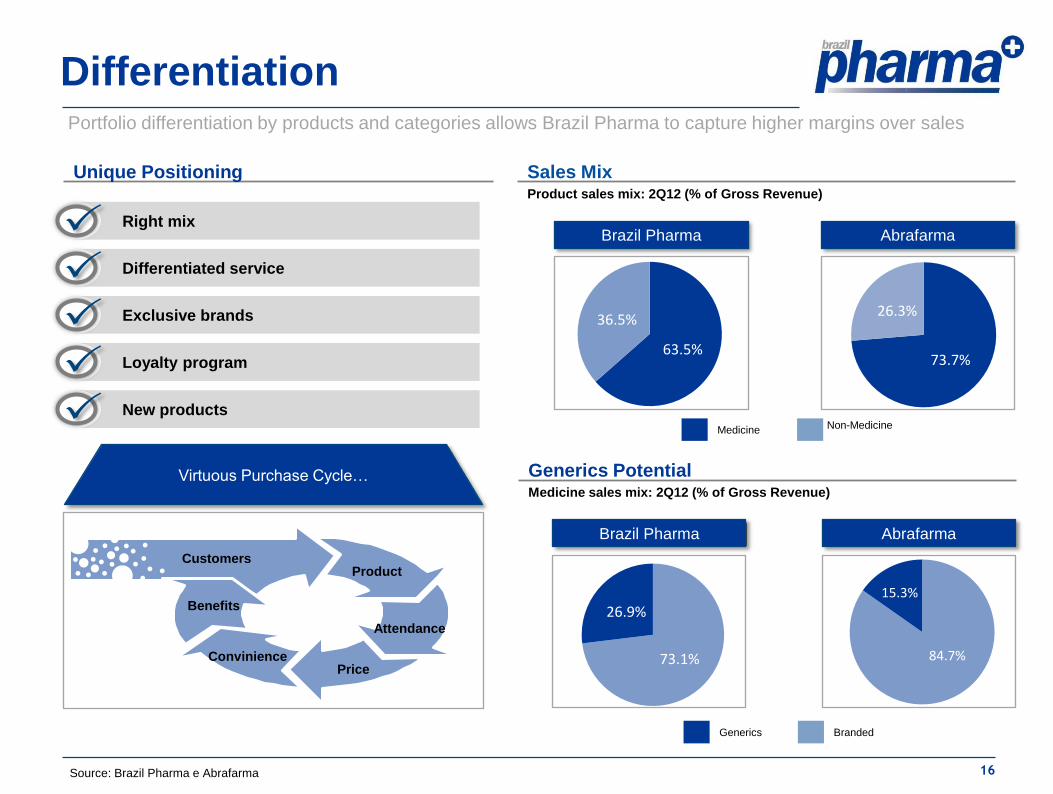

Differentiation Portfolio differentiation by products and categories allows Brazil Pharma to capture higher margins over sales

Medicine sales mix: 2Q12 (% of Gross Revenue)

Generics Potential

Brazil Pharma Abrafarma

Generics Branded

Product sales mix: 2Q12 (% of Gross Revenue)

Sales Mix

Abrafarma

Medicine Non-Medicine

Brazil Pharma

Unique Positioning

Source: Brazil Pharma e Abrafarma

Virtuous Purchase Cycle…

Customers Product

Attendance

Price Convinience

Benefits

73.7%

26.3%

73.1%

26.9%

63.5%

36.5%

84.7%

15.3%

Right mix

Differentiated service

Exclusive brands

Loyalty program

New products

17

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

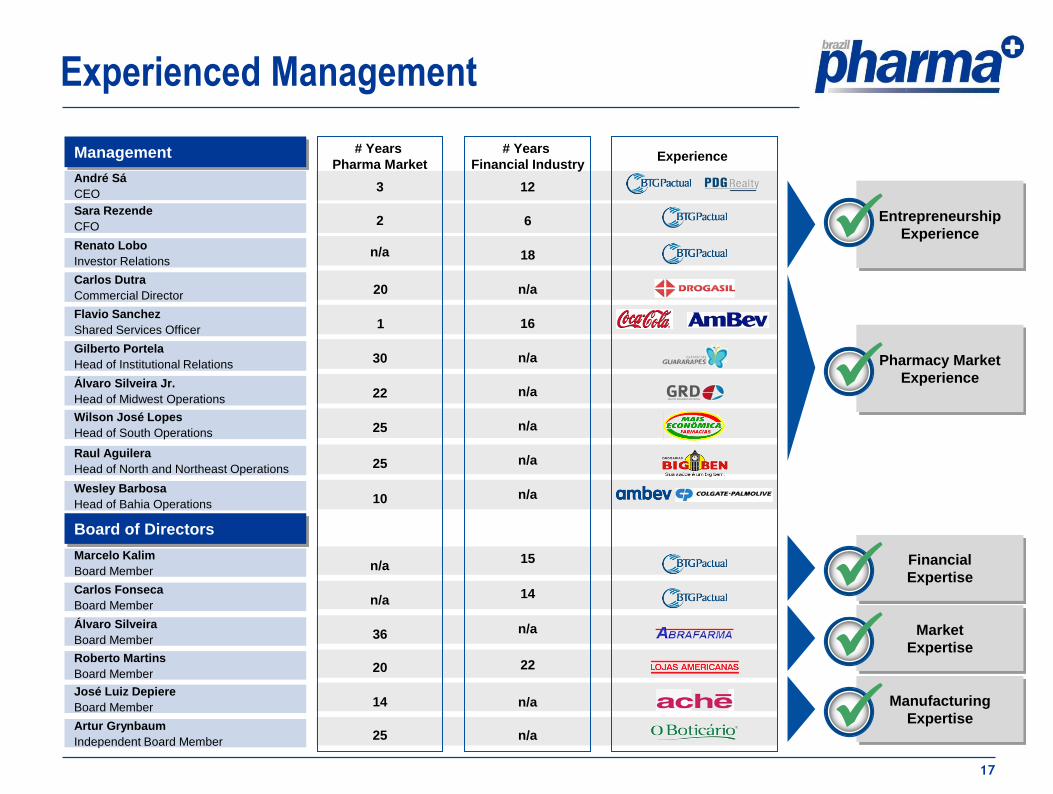

Experienced Management

Roberto Martins

Board Member 20

José Luiz Depiere

Board Member 14

Artur Grynbaum

Independent Board Member 25

Álvaro Silveira

Board Member 36

Marcelo Kalim

Board Member n/a

Carlos Fonseca

Board Member n/a

Álvaro Silveira Jr.

Head of Midwest Operations 22

Wilson José Lopes

Head of South Operations 25

Gilberto Portela

Head of Institutional Relations 30

Sara Rezende

CFO 2

Raul Aguilera

Head of North and Northeast Operations 25

Carlos Dutra

Commercial Director 20

André Sá

CEO 3

Renato Lobo

Investor Relations n/a

Wesley Barbosa

Head of Bahia Operations 10

Flavio Sanchez

Shared Services Officer 1

Management

Board of Directors

Entrepreneurship

Experience

# Years

Pharma Market

# Years

Financial Industry

n/a

n/a

n/a

22

n/a

n/a

n/a

6

n/a

n/a

12

18

15

14

n/a

16

Experience

Pharmacy Market

Experience

Financial

Expertise

Market

Expertise

Manufacturing

Expertise

18

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

Performance of BPHA3 versus IBOV Since its IPO, Brazil Pharma stock outperformed the Ibovespa by 48.2%.

Indexed Stock Price (Base 100)

06/27/2011 to 09/05/2012

12/26/2011:

Stock Split

11/28/2011:

Estrela

Galdino MoU

11/03/2011:

Big Ben

MoU

02/13/2012:

Sant’ana

MoU

04/16/2012:

Beauty’In

MoU

Acquisitions Corporate Events

Source: Econométrica in 05 September, 2012.

Note: “MoU” means Memorandum of Undestanding

06/21/2012:

Follow-on

R$ 12.77

R$ 22.00

56.863

Since IPO (06/24/11):

Brazil Pharma: + 48.2%

Raia Drogasil: + 115.3%

Ibovespa: (6.8%)

2012 YTD:

Brazil Pharma: + 46.0%

Raia Drogasil: + 67.3%

Ibovespa: (1.7%)

IPO

Operational and

Financial Highlights

20

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

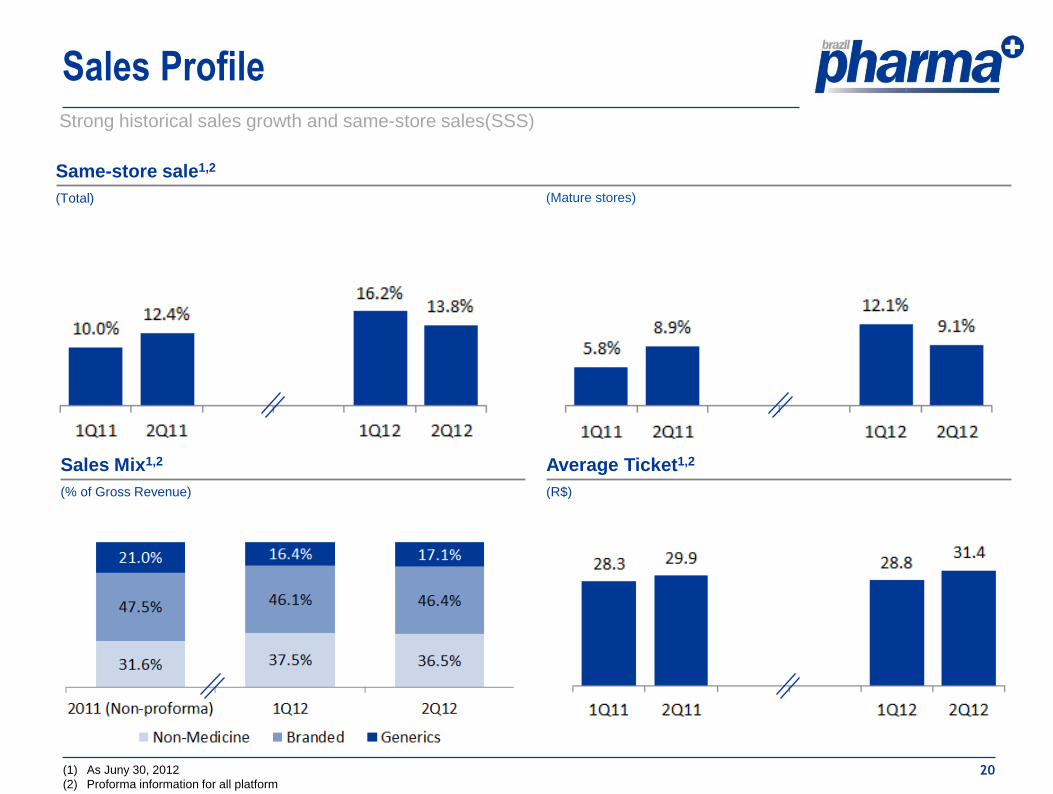

Strong historical sales growth and same-store sales(SSS)

Sales Profile

Sales Mix1,2

(% of Gross Revenue)

Average Ticket1,2

(R$)

(1) As Juny 30, 2012

(2) Proforma information for all platform

Same-store sale1,2

(Total)

(Mature stores)

21

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

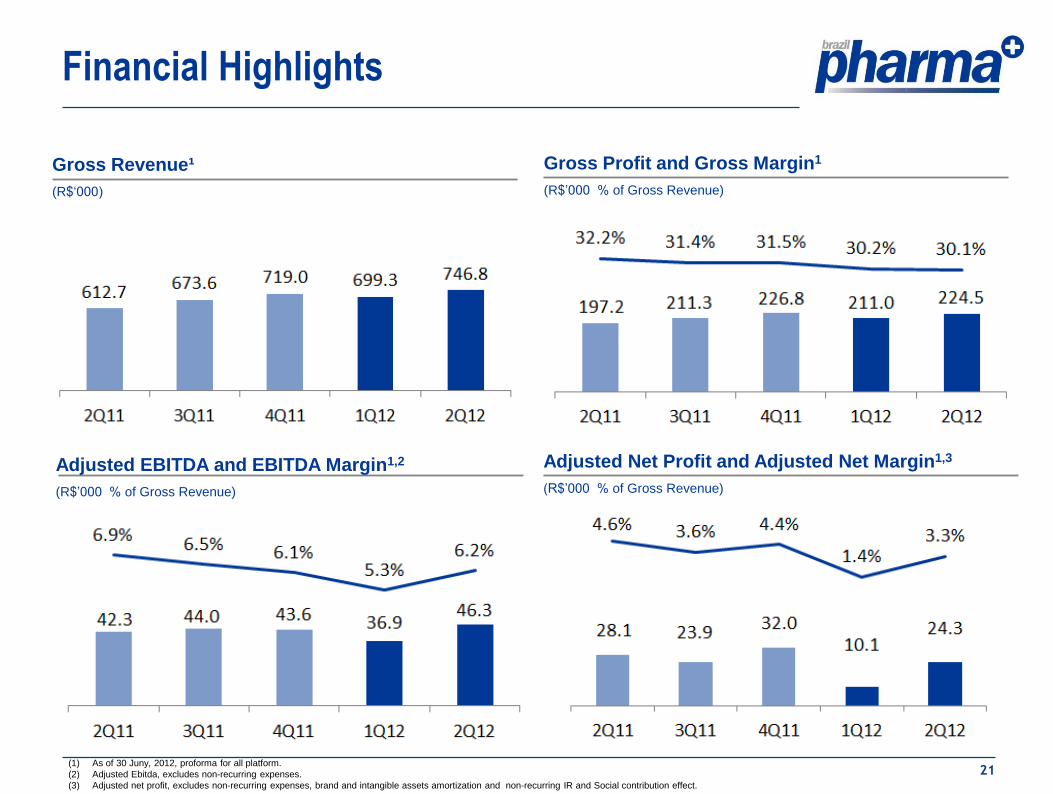

Financial Highlights

Gross Profit and Gross Margin1

(R$’000 % of Gross Revenue)

Adjusted Net Profit and Adjusted Net Margin1,3

(R$’000 % of Gross Revenue)

Adjusted EBITDA and EBITDA Margin1,2

(R$’000 % of Gross Revenue)

Gross Revenue¹

(R$‘000)

(1) As of 30 Juny, 2012, proforma for all platform.

(2) Adjusted Ebitda, excludes non-recurring expenses.

(3) Adjusted net profit, excludes non-recurring expenses, brand and intangible assets amortization and non-recurring IR and Social contribution effect.

22

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

Use of Proceeds

R$

476mm

R$

190mm

R$

238mm

R$

48mm

Constant focus on the reduction of the cash cycle

100 news stores in 2012; (~R$650 thousand for each new store)

Improvement and capacity expansion on the DCs

Invested Capex of R$47,7 million in 2012

Non current Debt Amortization timetable2

(1) Considers net cash of R$69,8 million related to the exercise of the Supplemental Option (Green Shoe)

(2) Non current debt amortization of R$613,2 million, as of 30 June, 2012 (2Q12).

Source of Proceeds

(Primary Offering¹) Use of

Proceeds

Optimization

of the capital

structure

Operational

Efficiency and

Systems

Working Capital,

M&A and

Organic Growth

IT and systems: first class ERP and managing and integration

system optimization

SSC and unification of the call center

48.5

99.7 91.1

229.4

144.6

Appendix

24

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

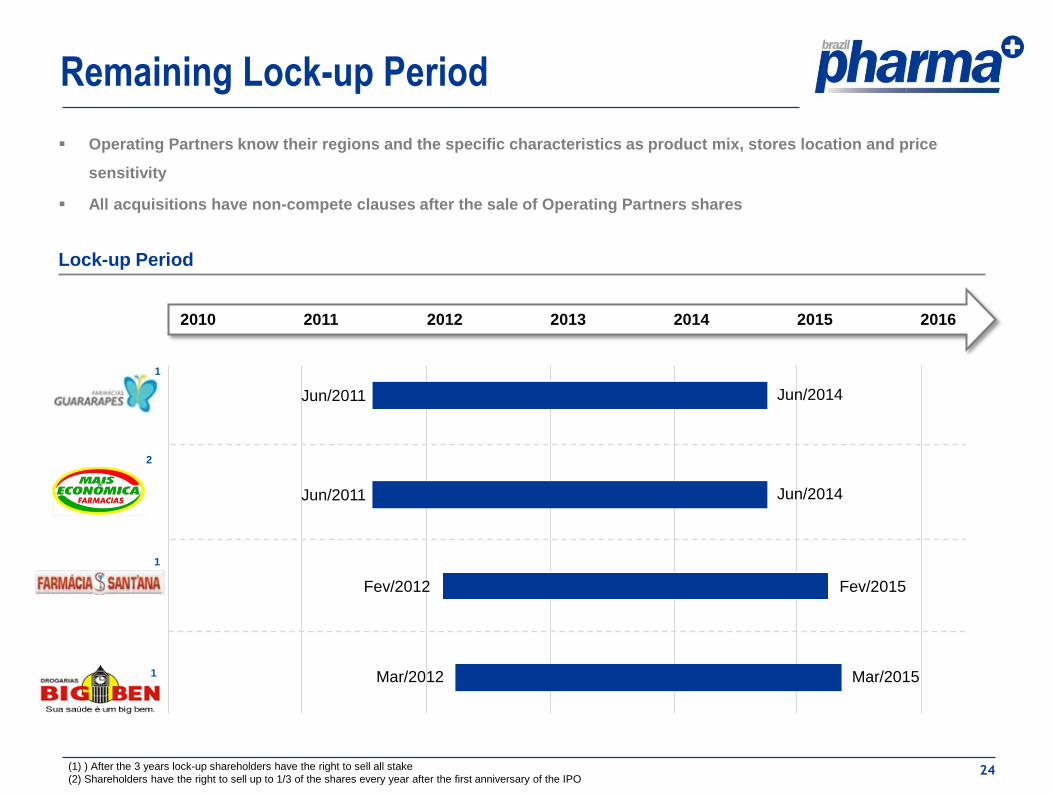

Remaining Lock-up Period

Lock-up Period

Operating Partners know their regions and the specific characteristics as product mix, stores location and price

sensitivity

All acquisitions have non-compete clauses after the sale of Operating Partners shares

(1) ) After the 3 years lock-up shareholders have the right to sell all stake

(2) Shareholders have the right to sell up to 1/3 of the shares every year after the first anniversary of the IPO

2010 2011 2012 2013 2014 2015 2016

Fev/2012 Fev/2015

Mar/2012 Mar/2015

Jun/2011 Jun/2014

Jun/2011 Jun/2014

1

2

1

1

25

127 / 155 / 202

127 / 127 / 127

0 / 56 / 150

217 / 217 / 217

204 / 215 / 234

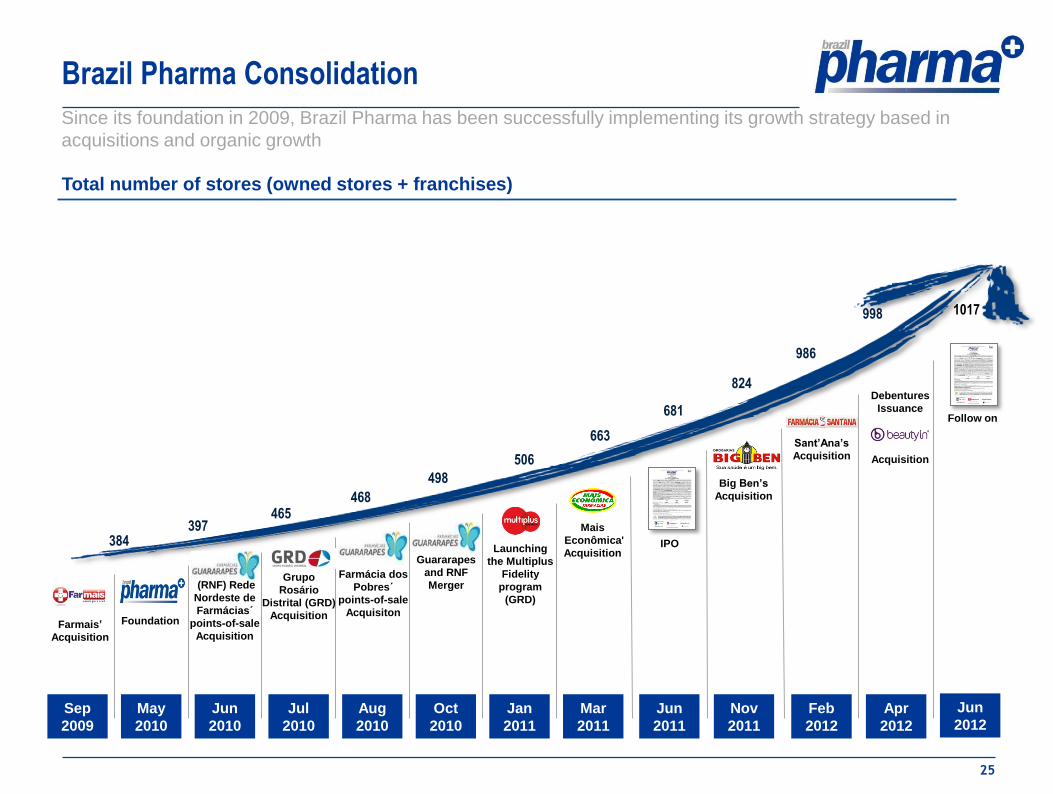

Brazil Pharma Consolidation

Since its foundation in 2009, Brazil Pharma has been successfully implementing its growth strategy based in

acquisitions and organic growth

Total number of stores (owned stores + franchises)

Farmais’

Acquisition

Foundation

Farmácia dos

Pobres´

points-of-sale

Acquisiton

Guararapes

and RNF

Merger (RNF) Rede

Nordeste de

Farmácias´

points-of-sale

Acquisition

Launching

the Multiplus

Fidelity

program

(GRD)

Mais

Econômica'

Acquisition

Grupo

Rosário

Distrital (GRD)

Acquisition

384 397

465 468

506

663

Sep

2009

Aug

2010

Oct

2010

May

2010

Jun

2010

Jan

2011

Mar

2011

Nov

2011

681

IPO

Jul

2010

Jun

2011

498 Big Ben’s

Acquisition

824

Feb

2012

Sant’Ana’s

Acquisition

986

998

Apr

2012

Debentures

Issuance

Acquisition

Jun

2012

Follow on

1017