Page 1 of 16 www.cushwakelandfl.com/tampa Bruce K. Erhardt, ALC Cushman & Wakefield of Florida, Inc. Tampa Bay Land Market Overview 3Q – 2014 The following represents excerpts from economic and real estate journals, notes from conventions, seminars and other meetings I attended, along with personal opinions of my own and others that affect the land market in the Tampa Bay Region. Previous Market Overviews can be found at www.cushwakelandfl.com/tampa. Erhardt’s Quick Look at the Land Market ˙ Multifamily land – Rental continues to be very active. For sale townhomes and condominiums are under contract or construction in urban and suburban markets, and are gaining momentum. ˙ Single Family – As for the last 20 quarters, builders and developers are closing and making offers on A and B locations. Starting to see some “drive until you qualify” subdivisions opening. ˙ Retail – For the first time in 29 quarters, I am seeing land prices for outparcels, neighborhood and community center sites, increase. We continue to believe that in A+ markets, we will see the emergence of unanchored strip centers. ˙ Industrial – New developers are contracting land positions in Tampa and Lakeland. ˙ Office – No change, users only. Medical office building construction is active. ˙ Hospitality – For the sixth quarter, development activity continues. ˙ Bank Deals – Continues to slow down. Not much left from the Great Recession. ˙ Agricultural Land – Active, but prices have leveled out for all but citrus, which is declining. ˙ Cycle – I’m predicting the overall Tampa Bay land cycle has five to six years left. The Big Picture Cushman & Wakefield Research Publication, U.S. Regional Economic Overview: A More Balanced Recovery, September 2014 Opportunities in commercial real estate over the next year or two, are most likely to be in the secondary markets. Economic recovery is returning to long term trends. Cities like Atlanta and San Diego, in some cases, are over taking coastal markets that have dominated this recovery. The U.S. economy is accelerating. For the full update, click here: http://flyers.cushmanwakefield.com/flyers/A More Balanced Recovery- Monthly Economic Update 9-14.pdf To subscribe to Cushman & Wakefield’s Economic Update, please contact Ken McCarthy at [email protected].

Transcript

Page 1 of 16

www.cushwakelandfl.com/tampa

Bruce K. Erhardt, ALC Cushman & Wakefield of Florida, Inc.

Tampa Bay Land Market Overview 3Q – 2014

The following represents excerpts from economic and real estate journals, notes from conventions, seminars and other meetings I attended, along with personal opinions of my own and others that affect the land market in the Tampa Bay Region. Previous Market Overviews can be found at www.cushwakelandfl.com/tampa. Erhardt’s Quick Look at the Land Market

˙ Multifamily land – Rental continues to be very active. For sale townhomes and condominiums are under contract or construction in urban and suburban markets, and are gaining momentum.

˙ Single Family – As for the last 20 quarters, builders and developers are closing and making offers on A and B locations. Starting to see some “drive until you qualify” subdivisions opening.

˙ Retail – For the first time in 29 quarters, I am seeing land prices for outparcels, neighborhood and community center sites, increase. We continue to believe that in A+ markets, we will see the emergence of unanchored strip centers.

˙ Industrial – New developers are contracting land positions in Tampa and Lakeland.

˙ Office – No change, users only. Medical office building construction is active.

˙ Hospitality – For the sixth quarter, development activity continues.

˙ Bank Deals – Continues to slow down. Not much left from the Great Recession.

˙ Agricultural Land – Active, but prices have leveled out for all but citrus, which is declining.

˙ Cycle – I’m predicting the overall Tampa Bay land cycle has five to six years left.

The Big Picture Cushman & Wakefield Research Publication, U.S. Regional Economic Overview: A More Balanced Recovery, September 2014

Opportunities in commercial real estate over the next year or two, are most likely to be in the secondary markets.

Economic recovery is returning to long term trends.

Cities like Atlanta and San Diego, in some cases, are over taking coastal markets that have dominated this recovery.

The U.S. economy is accelerating.

For the full update, click here: http://flyers.cushmanwakefield.com/flyers/A More Balanced Recovery-

Monthly Economic Update 9-14.pdf To subscribe to Cushman & Wakefield’s Economic Update, please contact Ken

Bernanke has predicted the Fed will only raise rates, and probably do so later than many forecast, because the labor market still has a lot more room to recover from the financial crisis and recession.

Bernanke, 60, does not expect the federal funds rate, the Fed’s main benchmark interest rate, to rise back to its long term average of around 4% in Bernanke’s lifetime.

Bernanke said the Fed aims to hit its 2% inflation target at all times, and that it is not necessarily a ceiling.

For the entire article, please click this link: http://flyers.cushmanwakefield.com/flyers/Reuters.pdf

June 2014 Builder Developer Magazine - Land and Lot Market, Greg Vogel, Land Advisors Organization

We have fully exited the distressed land and lot market with relevant inventory, now mainly held by strong balance sheet builders, well financed developers and private equity firms that all have high financial return expectations.

The U.S. is still producing single family permits at about 40% of what would be considered a normal market.

The reality of supplying 1,000,000 units per year requires a vast majority to occur in suburban developments.

The next age of homebuilding in certain markets will require flexibility as the wave of aging buyers is still at its infancy and their needs and preferences are continuing to evolve.

Homebuilders are generally just beginning to understand and innovate to address urban and infill growing demand.

There is now consensus that the continued low end single family production can now be blamed on tight lending and under employment. This is forcing the millennial generation to delay first time home purchases, as they postpone marriage. These factors have also led to the boom in multifamily and urban living.

Industrial – Chinese Manufacturers and Suppliers Quickly Finding a Home in the U.S., Automotive News, August 4, 2014

Some Chinese companies are buying established U.S. suppliers, while others are building their own plants.

Miller Canfield, a Detroit law firm, has more than 100 Chinese clients, of whom 80% are automotive manufacturers.

Factory wages in China are rising 10% annually and shipping costs are high.

Nexteer Automotive was required by Pacific Century Motors, an affiliate of the Beijing municipal government in 2010. Chinese owners gave Nexteer the capital they lacked to develop new products and expand in China, India, Brazil and North America.

Cushman & Wakefield’s Statewide Meeting, August 22, 2014, Retail

Convert a mall to a hospital.

C&W is #1 in urban retail worldwide.

Retail will change more in the next five years than the past 50 years.

Walgreens is putting sushi and prepared foods in their locations. Florida ICSC, August 25, 2014

Consumption has stabilized.

Retail demand recovery continues.

Historically low completions even five years out.

Florida will have a population of 23,608,972 by 2030.

82% in migration, of which, 41% is domestic, and 41% is international.

Ecommerce – doubled since 2009.

Urbanization – retailers know demographics. The drivers are 25-35 years old and 45-65 years old.

Population is growing faster in the suburbs in Florida, everywhere except Miami.

Mixed use – live, work, play is alive and well. Expect to see office in shopping centers.

Demographics are changing. For millennials, the smart phone cost is a car payment.

EBay sells more cars than anyone.

Advice to retailers – minimize friction and maximize experience.

5% of meals outside the house are from food trucks. There are 3,000 food trucks in New York City.

Amazon can reach 15% of the U.S. in one day.

Big boxes are getting smaller.

Whole Foods is adding a bar.

Spending habits change every three to four years with technology.

In the U.S., we have added 60 million square feet every 10 years, and 0 in the last five.

Between 2015 and 2020, the U.S. will build 30 million square feet, 70% of norm.

Ecommerce has a one to two percent margin, and bricks and mortar has an eight percent margin.

Target Express Tour Link: https://www.youtube.com/watch?v=aXTXHkgJuok&feature=youtu.be Please click on the 17,000 square foot Target Express tour, located in St. Paul, Minneapolis. By comparison, Walgreens is 15,000 square feet.

Wall Street Journal, October 5, 2014, Multifamily Rental

Rental rates increased one percent during the third quarter to an average of $1,111/month nationwide, according to REIS.

That is up 3.3% the same quarter one year ago.

Apartment rents have risen nationally for 23 straight quarters and are 15.2% higher than they were at the end of the recession in 2009.

The figures suggest a five year squeeze on renters shows local sign of easing.

The Apartment Report, July 22, 2014

Hard costs hit developers – construction costs escalations, along with decreasing yields and returns on costs, will be the most concerning market conditions for developers with 2015 starts. Developers will have to grapple with hard cost increases of 5% to more than 10% next year, forcing some to adopt larger contingencies that exceed 5%.

American Land Ventures expects hard costs to be up nearly 12% for its 2015 starts in Orlando, Ft. Lauderdale and Tampa. Altman Companies has at least three South Florida starts lined up, and underwrites for a 6%/per year escalation in construction costs for each deal.

Miami Herald, August 24, 2014, 35,000 Proposed Condo Units for South Florida, Miami-Dade, Broward and Palm Beach Counties

256 towers, 35,132 units. 27,642 or 78.7% are in Miami-Dade. These are pre-construction.

Frank Nothaft, Chief Economist for Freddie Mac

Multifamily starts highest in eight years.

Rental highest in 25 years.

Absorption fastest in 10 years.

Over the past year, household formations are renters.

Vacancy lowest in 14 years.

Most markets remain tight with modest rental increases. Dividend Capital Research Cycle Monitor – Real Estate Market Cycles, Q2-2014, www.dividendcapital.com, 866-324-7348 Physical Market Cycle Analysis of All Five Major Property Types in More Than 50 MSAs. Economic forecast options are changing and we like to think that the economy is moving from a slow recovery phase into a moderate growth phase of the cycle. Gross domestic product is growing at above 2% and employment growth is sustaining at a level of more than 200,000 jobs per month. This seems to have created moderate, but sustainable demand for most real estate. It has also kept new supply at low and sustainable levels for the foreseeable future, except in

the case of apartments. New apartment supply is too high, mainly due to low interest rate government financing availability.

Office occupancies improved 0.1% in Q2-2014, and rents grew 1.0% for the quarter and 3.8% annually.

Industrial occupancies improved 0.1% in Q2-2014, and rents grew 1.1% for the quarter and 4.6% annually.

Apartment occupancies declined 0.1% in Q2-2014, but rents grew 0.8% for the quarter and 2.5% annually.

Retail occupancy improved 0.1% in Q2-2014, and rents grew 1.3% for the quarter and 3.0% annually.

Hotel occupancies improved 0.8% in Q2-2014, while rents grew 3.9% for the quarter and improved 4.7% annually.

Office Market Cycle Analysis The national office market occupancy level improved 0.1% in Q2-2014, and was up 0.4% year over year. Office employment continues to grow at a rate close to 100,000 jobs per month, but space utilization has declined from the long term average of 200 square feet per person (SFPP) usage to about 170 SFPP. Thus, office space demand continues at a moderate pace that appears to be sustainable over the next year. Most office markets had very little movement in occupancies, thus the recovery phase continues. Average national rents were up 0.1% in Q2-2014 and rents were up 3.8% year over year For the sixth quarter, Tampa is at level three of the recovery phase. With Tampa are Ft. Lauderdale, Orlando and Palm Beach. Ahead of Tampa are Atlanta, Jacksonville, Miami, Charlotte, Raleigh-Durham and Nashville. Industrial Market Cycle Analysis Industrial occupancies improved 0.1% in Q2-2014, and were up 0.8% year over year. Absorption was almost 38 million square feet in Q2-2014 and has been higher than completions (29 million square feet in Q2-2014) for almost four years in a row. Manufacturing, utility and transportation employment correlates well with industrial demand and has been quite strong. Strong demand in energy driven cities like Austin, Dallas and Denver have pushed double digit rent growth in those industrial markets. While new completions are growing in some major port markets, it has not been high enough to cause concern by investors. The industrial national average rent index increased 1.1% in Q2-2014 and was up 4.6% year over year. Tampa has moved up to level six, at the beginning of the expansion phase. With Tampa are Atlanta, Ft. Lauderdale and Nashville. Ahead of Tampa is Charlotte, Raleigh-Durham, Miami and Palm Beach. Behind Tampa is Jacksonville, Orlando and Richmond. Apartment Market Cycle Analysis The national apartment occupancy average declined 0.1% in Q2-2014, and was down 0.2% year over year. Most markets are past their peak occupancy levels and are starting a moderate occupancy decline with all the new completions coming online in 2014. The cycle chart shows

Page 6 of 16

www.cushwakelandfl.com/tampa

that three markets had improving occupancies that moved them from peak occupancy backwards into the growth phase. There were five markets that had less dramatic occupancy changes that moved them backward in the hyper-supply phase of the cycle. It should be interesting to see if the developed community picks up on the hyper-supply issue and slows new starts over the next year. Remember that rents still grow in the hyper-supply phase of the cycle (as occupancies are above the long term average), but the rate of growth slows down. Average national apartment rent growth was 0.8% in Q2-2014 and was up 2.5% year over year (a lower growth rate than the previous quarter). Tampa moved back one position to twelve, which is the beginning of the hypersupply phase. With Tampa are Palm Beach, Nashville and Richmond. Ahead of Tampa is Charlotte. Behind Tampa is Jacksonville, Miami, Ft. Lauderdale, Memphis and Orlando. Retail Market Cycle Analysis Retail occupancies improved 0.1% in Q2-2014, and were up 0.3% year over year. Retail employment growth continues at a moderate pace of 40,000 jobs per month, which is a good indicator of demand for retail space. Retail sales also continued to grow at a moderate and potentially sustainable pace for the next year. The strong 2013 holiday sales caused many retailers to plan expansion in 2014 which should create positive occupancy increase in 2014 and 2015. National average retail rents increased 1.3% in Q2-2014 and were up 3.0% year over year. Tampa moved up again to level six, the beginning of the expansion phase. With Tampa is Palm Beach. Ahead of Tampa is Raleigh-Durham and Miami. Behind Tampa is Atlanta, Nashville, Richmond, Memphis, Charlotte, Jacksonville, Ft. Lauderdale and Orlando. Hotel Market Cycle Analysis Hotel occupancies improved an average of 0.8% in Q2-2014, and were up 1.9% year over year. Business expansions and the use of conferences to train employees and promote business with customers have been strong. Industry organizations are also creating more conference demand. Many markets are now seeing new construction to meet the increasing demand, but few are in danger of going into the hyper-supply phase of the cycle. With more than 60% of all hotel markets in the growth phase of the cycle, hoteliers are now able to raise room rates at above inflation levels. National average hotel rents improved 3.9% in Q2-2014 and were up 4.7% year over year. Tampa has moved up again to level eight, in the middle of the expansion phase. With Tampa is Atlanta. Ahead of Tampa are Ft. Lauderdale, Miami, Orlando and Palm Beach. Behind Tampa is Charlotte, Nashville, Raleigh-Durham, Richmond, Norfolk, Memphis and Jacksonville.

Page 7 of 16

www.cushwakelandfl.com/tampa

Tampa Bay Retail Market Overview Marcus & Millichap Q3-2014 Tampa Bay Metro Area Market Overview Economy

Tampa expanded 2.1 percent over the past 12 months ending midyear with the addition of 24,800 jobs. In the corresponding period last year, employers created 27,700 positions.

Steady hiring and strengthening consumer confidence is supporting retail spending, though at a slightly slower pace than recent years of aggressive growth. Retail sales advanced 4.6 percent year over year in June, slightly above the national average.

The region’s life science industry cluster continues to attract companies. Quest Diagnostics, a provider of medical testing services, will create up to 350 jobs over the next year at its new logistics hub in Hillsborough County. Additionally, Bristol-Myers Squibb opened its new office in Tampa early this year, with plans to add 580 positions by 2017.

Outlook – This year, local employers will generate 33,000 jobs, lifting employment 2.8 percent.

Construction

Over the last four quarters, developers finished 800,000 square feet of retail space, on par with deliveries in the previous period one year earlier.

The largest project completed year to date is a 198,000 square foot Wal-Mart Supercenter in Pinellas County. Two Wal-Mart build-to-suits, a 148,000 and 125,000 square foot building, were delivered in the first half of the year.

Nearly 1.3 million square feet is underway, including the 880,000 square foot shopping mall in Sarasota that is slated for completion this fall. Additionally, the planning pipeline contains 7.4 million square feet, though only a handful of projects have target start dates.

Outlook – Builders will finish 1.9 million square feet in 2014, lifting inventory 1 percent. Vacancy

The improving economy contributed to healthy demand for retail space, pulling down metro-wide vacancy. Overall, vacancy dropped an annual 80 basis points on net absorption of 2.3 million square feet to 7.1 percent in the second quarter, the lowest rate since late 2008. In the previous year long period, vacancy ticked up 30 basis points.

During the last 12 month period, every submarket in the metro posted annual vacancy reductions. Average vacancy improved the most in the Central Tampa and Pasco County submarkets, falling 170 and 140 basis points to 6.0 and 9.1 percent, respectively.

In the multi-tenant segment, vacancy tumbled 120 basis points over the last 12 months to 9.2 percent. Despite the decline, the rate remains more than 250 basis points above the pre-recession low.

Outlook – By year end 2014, vacancy will fall an annual 30 basis points to 7.4 percent, the lowest level in five years.

Page 8 of 16

www.cushwakelandfl.com/tampa

Rents

As conditions tightened, the pace of rent reductions slowed. During the last 12 months, asking rents edged down 0.5 percent in the second quarter. In the previous period one year earlier, rents fell 1.9 percent. Five years of flat or negative growth has paced rents 24 percent below the peak reached in mid-2008.

Over the past year, three out of eight submarkets posted annual rent gains. The Central Tampa submarket, which boasts the highest rents in the metro, recorded a 4.5 percent year over year increase to $17.51 per square foot. The lowest rents are in the Eastern Outlying submarket at $11.63 per square foot.

Multi-tenant rents ticked up 0.1 percent over the last 12 months to $12.90 per square foot, up from the 1.5 percent decline last year. Meanwhile, average rents in the single tenant sector contracted 0.9 percent to $14.36 per square foot.

Outlook – As new inventory comes online through the remainder of the year, average asking rents will moderately rise. Rents will reach $13.89 per square foot in 2014, marking a 1 percent year over year increase.

ERHARDT COMMENT:

˙ A lot will follow Simon’s outlet mall going vertical on a Prime Outlets Center at I-75 and S.R. 56, Wesley Chapel

Tampa Bay Single Family Market Overview Tampa Bay Builders Association, July 18, 2014

Tampa Bay home starts normal is 16,649 per year. 2000 predicted to be 8,149 and 2015 predicted to be 13,097 starts.

Tony Polito, American MetroStudy TAMPA August 2014: Metrostudy today released the results of its 2Q14 survey of the Tampa Bay housing market, which showed that the “pause” that began last Fall is showing some signs of abating as 2Q14 starts were up 31.8% over 1Q14. During 2Q, 1,529 single-family units were started, which was down 17.4% from the 2Q13 level of 1,851 starts (the best post-recession quarter). The annual starts rate, compared to last year, decreased by 6.1%, to 5,850 annual starts. Single-family quarterly closings totaled 1,396 units, up 5.1% from 2Q13 levels. The annual closings rate was 6,458 units, 23.8% above the rate for the twelve months ending 2Q13. A review of deed records indicates that the “pause” had more effect on volume than pricing. The price increases pushed thru in early 2013 have held and now builders must face the question of volume versus price.

Page 9 of 16

www.cushwakelandfl.com/tampa

“As in the rest of the state, the Tampa Bay region is showing a precipitous drop in construction of units for first time and lower income homebuyers, as the number of annual starts under $150k has declined 57% since 2Q13,” said Tony Polito, Regional Director of Metrostudy’s Tampa Market. “Builders are instead concentrating on higher-priced inventory, which is booming. Annual starts of units priced over $450k more than doubled since 2Q13, and we expect to see this trend continue.”

Annual Starts by Price Range

For the twelve months ending June 2014, annual new home starts in price ranges under $200k totaled 1,436 units, down 37.5% from the 2Q13 annual activity in that range. New home starts in prices over $200k were up 12.3% for 2Q14 versus 2Q13. The marginal 379 unit decrease in the annual start pace was split: 861 less units under $200k and 482 more units above $200k (127.2% of the marginal growth). Total single-family inventory, composed of units under construction, finished vacant and models equaled 3,494 units on the ground at the end of the 2Q14; a 6.5-month supply. Inventories fell by 14.8% compared to 2Q13. Compared to last year, the number of units under construction fell by 348 homes to 1,862 homes. Finished vacant inventory decreased by 17.8% from last year to 1,335. The number of move-ins exceeded completions during the quarter and FV inventory decrease by 183 units versus 1Q14. The FV MOS of single family units fell from 2.1 as of 1Q14 to 1.8 months as of 2Q14. Hillsborough County remained the most active county within the Tampa market during the second quarter. However, market share declined from 65.1% for 1Q14 to 63.3% for 2Q14, in spite of quarterly starts rising from 738 in 1Q14 to 929 in 2Q14. Market share in Pasco fell from 24.8% for 1Q14 to 24.4% for 2Q14 despite quarterly starts rising from 284 in 1Q14 to 379 for

2Q14. The VDL supply throughout all of Hillsborough County stood at 25.3 months. The VDL supply in Pasco stood at 52.2 months as of June 30, 2014. These two major counties accounted for 87.7% of all annual start activity in Tampa Bay.

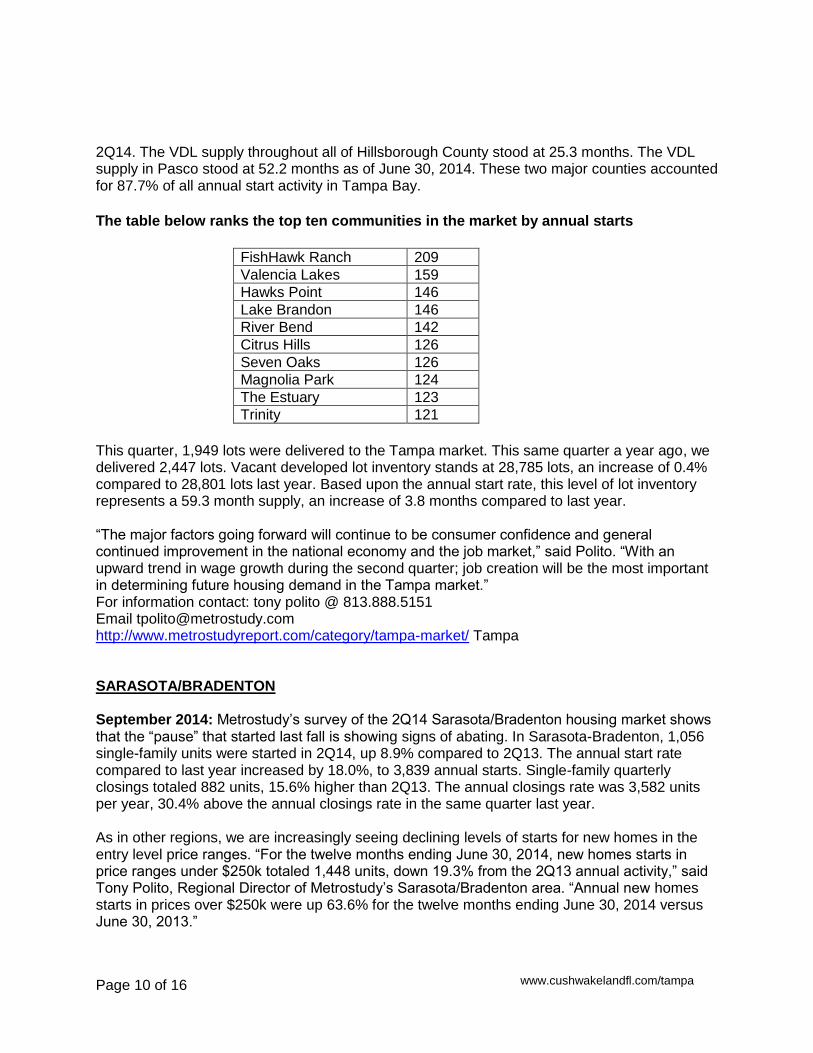

The table below ranks the top ten communities in the market by annual starts

FishHawk Ranch 209

Valencia Lakes 159

Hawks Point 146

Lake Brandon 146

River Bend 142

Citrus Hills 126

Seven Oaks 126

Magnolia Park 124

The Estuary 123

Trinity 121

This quarter, 1,949 lots were delivered to the Tampa market. This same quarter a year ago, we delivered 2,447 lots. Vacant developed lot inventory stands at 28,785 lots, an increase of 0.4% compared to 28,801 lots last year. Based upon the annual start rate, this level of lot inventory represents a 59.3 month supply, an increase of 3.8 months compared to last year. “The major factors going forward will continue to be consumer confidence and general continued improvement in the national economy and the job market,” said Polito. “With an upward trend in wage growth during the second quarter; job creation will be the most important in determining future housing demand in the Tampa market.” For information contact: tony polito @ 813.888.5151 Email [email protected] http://www.metrostudyreport.com/category/tampa-market/ Tampa SARASOTA/BRADENTON September 2014: Metrostudy’s survey of the 2Q14 Sarasota/Bradenton housing market shows that the “pause” that started last fall is showing signs of abating. In Sarasota-Bradenton, 1,056 single-family units were started in 2Q14, up 8.9% compared to 2Q13. The annual start rate compared to last year increased by 18.0%, to 3,839 annual starts. Single-family quarterly closings totaled 882 units, 15.6% higher than 2Q13. The annual closings rate was 3,582 units per year, 30.4% above the annual closings rate in the same quarter last year. As in other regions, we are increasingly seeing declining levels of starts for new homes in the entry level price ranges. “For the twelve months ending June 30, 2014, new homes starts in price ranges under $250k totaled 1,448 units, down 19.3% from the 2Q13 annual activity,” said Tony Polito, Regional Director of Metrostudy’s Sarasota/Bradenton area. “Annual new homes starts in prices over $250k were up 63.6% for the twelve months ending June 30, 2014 versus June 30, 2013.”

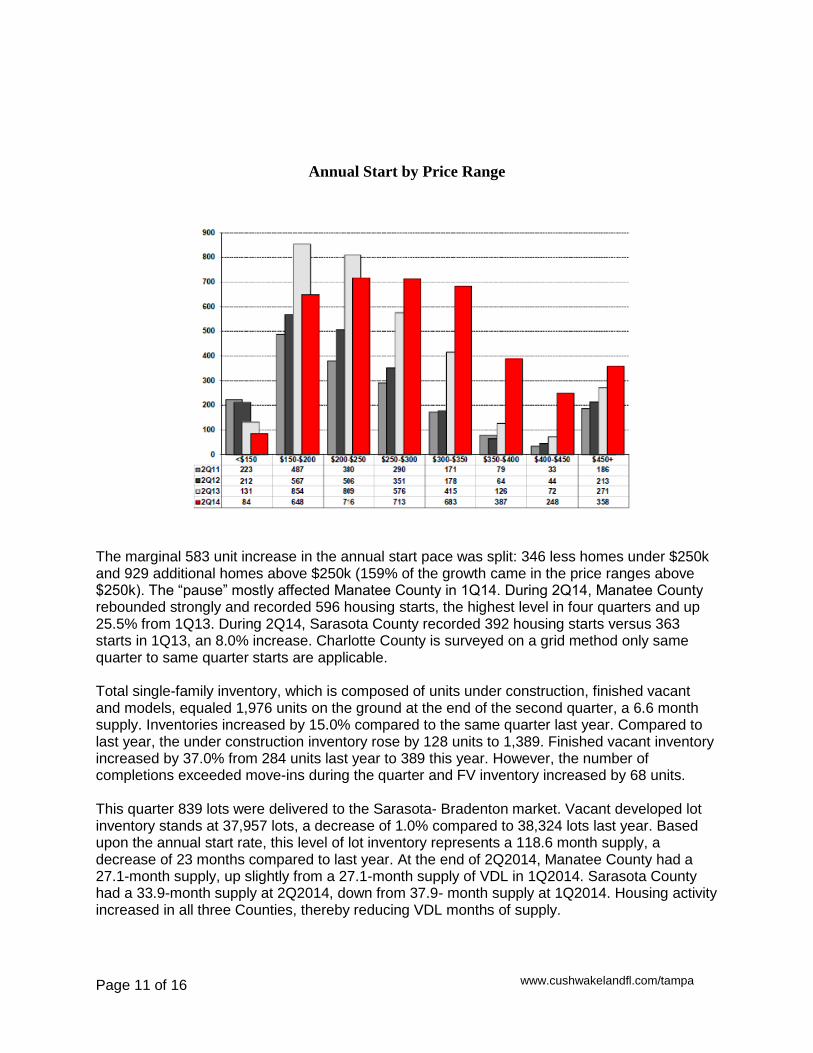

The marginal 583 unit increase in the annual start pace was split: 346 less homes under $250k and 929 additional homes above $250k (159% of the growth came in the price ranges above $250k). The “pause” mostly affected Manatee County in 1Q14. During 2Q14, Manatee County rebounded strongly and recorded 596 housing starts, the highest level in four quarters and up 25.5% from 1Q13. During 2Q14, Sarasota County recorded 392 housing starts versus 363 starts in 1Q13, an 8.0% increase. Charlotte County is surveyed on a grid method only same quarter to same quarter starts are applicable. Total single-family inventory, which is composed of units under construction, finished vacant and models, equaled 1,976 units on the ground at the end of the second quarter, a 6.6 month supply. Inventories increased by 15.0% compared to the same quarter last year. Compared to last year, the under construction inventory rose by 128 units to 1,389. Finished vacant inventory increased by 37.0% from 284 units last year to 389 this year. However, the number of completions exceeded move-ins during the quarter and FV inventory increased by 68 units. This quarter 839 lots were delivered to the Sarasota- Bradenton market. Vacant developed lot inventory stands at 37,957 lots, a decrease of 1.0% compared to 38,324 lots last year. Based upon the annual start rate, this level of lot inventory represents a 118.6 month supply, a decrease of 23 months compared to last year. At the end of 2Q2014, Manatee County had a 27.1-month supply, up slightly from a 27.1-month supply of VDL in 1Q2014. Sarasota County had a 33.9-month supply at 2Q2014, down from 37.9- month supply at 1Q2014. Housing activity increased in all three Counties, thereby reducing VDL months of supply.

“A review of deed records indicates that the “pause” had more effect on volume than pricing,” said Polito. “While Sarasota is seeing both volume and price increases, the price increases are more moderate than in 2013. The major factors going forward will continue to be consumer confidence and general continued improvement in the national economy and the job market, which help retirees sell northern homes.” TOP COMMUNITIES BY ANNUAL STARTS

Lakewood Ranch 559

The West Villages 216

South Gulf Cove 173

Grand Palm 144

Palmer Ranch 129

Esplanade by Siesta Key 119

Heritage Harbour 111

Harrison Ranch 102

Greyhawk Landing 87

Woodlands 073

For information contact: Tony Polito @ 813.888.5151 Email [email protected] http://www.metrostudyreport.com/category/sarasota-bradenton-market/ Sarasota/Bradenton

Tampa Bay Multifamily Market Overview Marcus & Millichap Q3-2014 Tampa Bay Metro Area Market Overview Economic Overview The Tampa Bay economy continues to grow, recording nearly 38,000 new jobs added over the past 12 months. Hospitality, financial and business services remain the dominant drivers of the area’s economy. Additionally, the recent revival in the housing market, a substantial increase in population growth and improved confidence among consumers have all contributed to the improving economy. Apartment Overview Continued employment growth and a greater propensity to rent bolstered rental demand. New additions to supply have been picking up throughout the region, but absorption still exceeds deliveries. Favorable supply and demand have resulted in increasing occupancy and rents throughout Tampa Bay.

Market wide vacancy remained flat at approximately 6.0% over the past 12 months. Average rents have increased 3.0% to $923 per month during the past year and concessions, which were prevalent in previous years, have been reduced significantly. Tampa MSA Market Rate Supply There are approximately 867 existing properties in the Tampa Bay MSA, totaling 193,000 units. A total of 2,314 new units have been completed during the first half of the year, and there are another 5,868 units currently under construction within the market.

Tampa Office Market Overview Cushman & Wakefield Market Overview – Tampa

Westshore Office Overview: Overall vacancy at the end of 3rd quarter 2014 is 13.5% compared to 14.5% last year and 15.1% last quarter. Class A is at 12.4% compared to 15.3% last year and 11.8% last quarter.

I-75 Office Overview: Overall vacancy at the end of the 3rd quarter 2014 is at 20.0% compared to 18.2% a year ago and 20.6% last quarter. Class A is at 22.1% compared to 16.7% a year ago and 21.0% last quarter.

Tampa Central Business District: Overall vacancy at the end of the 3rd quarter 2014 is at 13.5% compared to15.4% a year ago and 13.6% last quarter. Class A is at 11.5% compared to 14.5% a year ago and 11.8% last quarter.

Tampa Industrial Market Overview Cushman & Wakefield Market Overview – Tampa

West Tampa Industrial Overview: The overall vacancy at the end of the 3rd quarter, 2014 is 5.9% compared to 6.8% a year ago and 5.9% last quarter.

Warehouse distribution is at 3.7% vacancy compared to 4.6% a year ago and 4.0% last quarter.

Office Service Center is at 12.5% vacancy compared to 13.6% a year ago and 11.7% last quarter.

East Tampa Industrial Overview: The overall vacancy at the end of the 3rd quarter 2014 was 7.8% compared to 8.2% a year ago and 7.4% last quarter.

Page 14 of 16

www.cushwakelandfl.com/tampa

Warehouse distribution is at 7.9% vacancy compared to 8.5% a year ago and 8.1% last quarter. Office Service Center is at 13.9% vacancy compared to 15.1% last year and 15.1% last quarter.

Plant City Industrial Market Overview: The overall vacancy at the end of the 3rd quarter 2014 was 3.2% vacancy compared to 1.2% a year ago and 1.8% last quarter.

Warehouse distribution is at 4.4% vacancy compared to 1.8% a year ago and 2.2% last quarter.

Lakeland Industrial Market Overview: The overall vacancy at the end of the 3rd quarter 2014 was 4.7% vacancy compared to 4.1% a year ago and 5.1% last quarter.

Warehouse distribution is at 5.8% vacancy compared to 4.8% a year ago and 6.2% last quarter. Service center is at 18.5% compared to 17.1% a year ago and 18.0% last quarter.

**Preliminary Industrial Statistics 3Q14 – Subject to change**

Tampa Hospitality Market Overview Hillsborough County Hotel and Motel Organizations, Annual Trends and Forecasting Forum, July 24, 2014

Lou Plasencia, CEO of Independent Hotel Partners, predicts we will see the highest amount of transaction activity we have seen in 10 years.

Plasencia expects several large, new investors to enter the market in the coming months. Money from the Middle East, Russia, Brazil and China has nearly exhausted opportunities for Class A product in Gateway markets. They are now moving to second tier – Tampa, Nashville, Dallas, Houston, Charlotte and Phoenix.

Tampa area is lagging about one and one-half to two years, behind other competing markets.

ERHARDT COMMENT:

˙ Jeff Viniks’ purchase of the Marriott Waterside Hotel and submittal of another convention hotel contiguous to the Lightning Hockey Arena, bodes well for the convention business, as well as, an additional four star hotel.

Page 15 of 16

www.cushwakelandfl.com/tampa

Please click on the following link for renderings of the Detroit Red Wings proposed development around their hockey arena. They are proposing over 2,000 residential units, some of which are contiguous to the arena, and five, different urban neighborhoods. http://www.mlive.com/business/detroit/index.ssf/2014/10/650_million_detroit_red_wings_4.html

Land Sales Single Family

1. Mattamy Homes purchased 374 home sites in south Hillsborough County in the Triple Creek development for $16,000,000. 176 of the lots were developed and 198 were not. Mattamy will be building homes ranging from 1,700 to 3,600 square feet and from $200,000 to $325,000.

2. Taylor Morrison purchased 15.12 acres on the west side of Sheldon Road, north of Linebaugh Avenue in northwest Hillsborough County, for $4,000,000. This represents $54,000 per lot and 4.9 units per acre density. Taylor Morrison plans on building homes for $275,000+.

3. Primerica Group purchased 200 acres at I-75 and Moccasin Wallow in Manatee County for $18,000 per acre. The property is zoned for 104 single family units, 268,206 square foot of retail and office space, and 340,400 square feet of light industrial.

Industrial

1. An undisclosed buyer purchased 7.53 acres at U.S. Highway 301 and I-75 to build 120,000 square feet of office and 85,000 square feet of industrial space for $1,800,000. $5.49 per ground foot developed and $8.78 per building foot.

2. Trader Joe’s purchased a 76 acre developed site in Daytona Beach for an 800,000 square foot distribution center. This represents $2.35 per land foot and $9.75 per building foot. The incentives provided by municipalities were to prepare the site to be pad ready, and $3,000,000 worth of road improvements related to the project. The additional incentives are tied to certain employment and salary milestones.

Mixed Use

1. China – Authorities sold a parcel of land in Beijing for $1.5 billion, representing $1,100 per square foot. This was a record.

2. Hyundai paid $10.1 billion for 18.6 acres in the Gangnam area of Seoul, Korea for $11,826 per square foot. Hyundai has not decided how tall its headquarters tower will be, but said it will be the highest in the area. The 55 story World Trade Center Seoul is across the road from the land and the 123 story lotte World Trade Center is under construction about three kilometers to the east. Hyundai beat out Samsung with its bid.

3. Kolter Group purchased a 1.84 acre site in downtown St. Petersburg for $115.22 per square foot. They are planning a residential condominium, hotel and retail space.

1. Michael Galinski purchased 4,515 acres near Myakka River State Park in eastern Manatee County for $2,879 per acre.

Multifamily

1. The Richman Group purchased 3.9 acres in the Tampa CBD for $66.00 per square foot and $32,079 per unit for 351 units or 90 units per acre. This was a Cushman & Wakefield transaction.

2. An undisclosed rental apartment developer purchased 7.49 acres in the southwest quadrant of Fruitville and I-75 for $6,737 per unit for 282 units, which is 32 units per acre, on the pad ready site.

3. Florida Crystals purchased a 1.88 acre site in the Channelside area of downtown Tampa for $47.00 per square foot and $14,222 per unit based on 270 units, which is 144 units per acre. This will be a seven story, midrise building with a six and one half story parking garage.

4. The Bainbridge Company has purchased an 18 acre, pad ready site in the northwest quadrant of I-75 and Leroy Selmon Expressway for $9.05 per land square foot and $16,904 per unit for 420 units.

5. M/I Homes purchased 80 gross acres, 27 net acres, in the northwest quadrant of Sheldon Road and Linebaugh Avenue in northwest Hillsborough County. They plan on building 226 townhomes ($15,486 per unit).