31

Bryan Cunningham ENDOGENEITY AND THE SP–FP RELATIONSHIP Does Social Performance Really Lead to Financial Performance? Accounting for Endogeneity An article review PRESENTED BY

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | ethan-russell |

| View: | 213 times |

| Download: | 0 times |

Bryan Cunningham

ENDOGENEITY AND THE SP–FP RELATIONSHIP

Does Social Performance Really Lead to Financial Performance? Accounting for Endogeneity

An article review

PRESENTED BY

Endogeneity and the SP-FP Relationship

Does Social Performance Really Lead to Financial Performance?

DOES SOCIAL PERFORMANCE REALLY LEAD TO FINANCIAL PERFORMANCE? ACCOUNTING FOR ENDOGENEITYRoberto Garcia-Castro, Miguel A. Arin˜o & Miguel A. Canela

ARTICLE REVIEW

ENDOGENEITY AND THE SP–FP RELATIONSHIP

Contents Article summary Critical reflections Findings Implications

Purpose How to explain the heterogeneity of

these findings? Is it possible to generalize the positive

link between SP and FP found in the majority of previous studies?

Does such a positive link hold in the long run and also in the short run?

Three important purposes of this article

The key players in the SP-FP Link

The mystique link of SP-FP link

Heterogeneity in KLD research

Far from clear

Sample and data Panel based on the 658 US based firms

included in KLD database of 3000 covering a 15 year time horizon (1991 – 2005).

Financial data and firm level control variables from Datastream.

Neutralizing sample selection bias Neutralized sample selection bias by

including firms listed in S&P 500 and Domini 400 social index.

Neutralizing Common Method Bias Obviated the common method bias by

choosing data for the independent and dependant variables.

Comparison between methods of estimation

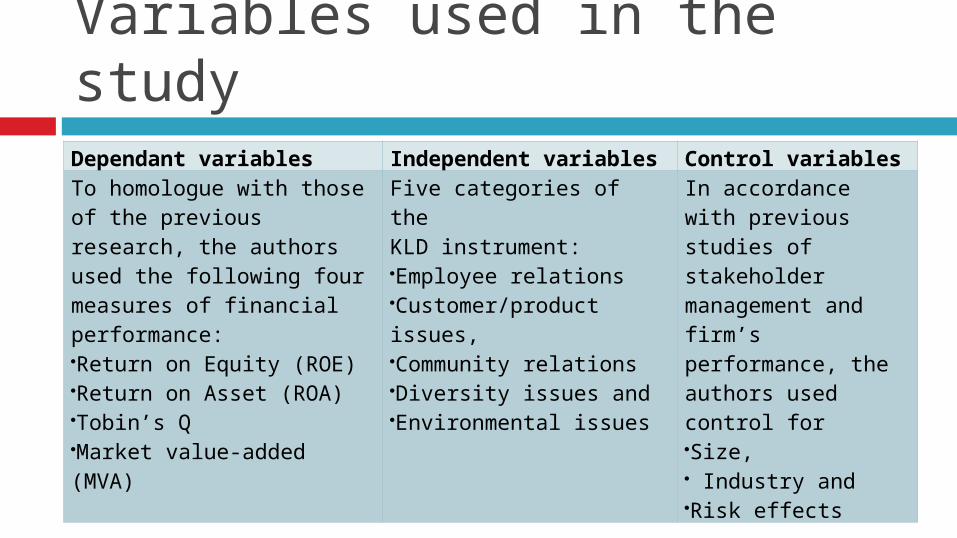

Dependant variables Independent variables Control variablesTo homologue with those of the previous research, the authors used the following four measures of financial performance:Return on Equity (ROE)Return on Asset (ROA)Tobin’s QMarket value-added (MVA)

Five categories of theKLD instrument: Employee relationsCustomer/product issues, Community relationsDiversity issues and Environmental issues

In accordance with previous studies of stakeholder management and firm’s performance, the authors used control forSize, Industry and Risk effects

Variables used in the study

Baseline Model

∏it = α + β1KLDit+ β2 Riskit + β3 Salesit+ β4 R&Dit

+ β5 Leverageit + β6 + β14 (Industryj) + θi+ εit

Where,

∏it = ROE, ROA, Tobin’s Q or MVA of firm ‘i’ in time ‘t’

KLDit = social performance of firm ‘i’ in time ‘t’ = Σ Community relations + Employee relations + Diversity policies + Environmental concern + Product (customer concern) of firm ‘I’ in time ‘t’,

Riskit = Beta of firm ‘i’ in time ‘t’,

Salesit = Total sales of firm ‘i' in time ‘t’,

R&Dit = R&D expenses over sales of firm ‘i' in time ‘t’,

Leverageit = Total debt over total equity of firm i in time t,

Industryj = 9 time-invariant dummy variables,

i = 1,…, 658 firms,

t = 1991–2005,

j = 1,…,9 industries,

θi is the time-invariant error term and

εit is the time-varying error term.

Testing for Endogeneity Hausman’s test Mundlak’s test

Hausman’s test Produced a non-positive definitive

covariance matrix of the differences between the random and the fixed effects, making it impossible to compute the test.

Mundlak’s test Four dependent variables used - ROE, ROA, MVA and

Tobin’s Q. The four regression coefficients proved to be

significant (p<0.01) for the means of the KLD variable.

Hence, we can reject the null hypothesis of no endogeneity. This result confirms the relevance of endogeneity in this kind of research and the need to account for endogeneity in our sample.

Comparison Model

∏it = αi + β1KLDit+ β2 Riskit + β3 Salesit+ β4 R&Dit + β5 Leverageit + β6

- β42 (Industryj) + εit

The Findings

The findings of the study

Finding #1 The positive impact of of social performance

on financial performance found in previous studies is mainly due to the fact that firms adopted high standards of KLD self-selected themselves.

These positive effects are diluted when endogeneity is taken into account appropriately.

Finding#2 The future research should critically examine

the firm-specific characteristics that prompt firms to adopt those KLD practices in the first place.

Only when the reasons behind KLD adoption by managers is understood, the logical cause-and-effect connection between SP and FP can be established effectively.

Finding#3 A critical examination of the KLD measurement of

SP is required to rule out the possibility of missing the dimensions related with quality of management.

Future methodology developments to measure a firm’s SP should look more carefully at the management quality dimension if they are to improve their predictive power in terms of FP in the long and the short run.

Implication

Research implications

Implication#1 There will be a research methodological

consequence given the magnitude of bias included by the endogeneity and self-selection problems shown by the authors.

Implication#2 The authors believe that a systematic aspect

missing in SP indexes such as KLD or SAM (Sustainable Asset Management) is a sound measure of the quality of management.

The nature of SP indexes and measurement tools adopted so far and their limitations to capture the quality of management is required to be reviewed.

Conclusion The authors assert in this article that there is a

more powerful reason for the heterogeneity of previous findings that may affect all of them.

The decision of the top management to improve a firm’s SP (i.e., decisions oriented to improving the quality of the relationships between the firm and its stakeholders) is endogenous.

The authors urge that very little progress has been made to advance our knowledge about the interaction between quality of management and SP.

In their article they suggest that such an interaction may be not only important for theoretical purposes but also in that it may affect empirical findings, therefore vigorous research initiatives may be required to establish the exact nature of SP-FP relationship.

![endogeneity 2.ppt [호환 모드]](https://static.documents.pub/doc/80x56/61ed282de663cc41923b0a15/endogeneity-2ppt-.jpg)