SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended December 31, 2002 OR Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the transition period from to Commission file number 1-9356 Buckeye Partners, L.P. (Exact name of registrant as specified in its charter) Delaware 23-2432497 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification number) 5002 Buckeye Road P. O. Box 368 Emmaus, Pennsylvania 18049 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (484) 232-4000 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered LP Units representing limited partnership interests........................................... New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None (Title of class) Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No Indicate by check mark whether the registrant is an accelerated filer (as defined in Exchange Act 12b-2). Yes No At June 28, 2002, the aggregate market value of the registrant’s LP Units held by non-affiliates was $888 million. The calculation of such market value should not be construed as an admission or conclusion by the registrant that any person is in fact an affiliate of the registrant. LP Units outstanding as of March 13, 2003: 28,702,346

Transcript

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K (Mark One)

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2002

OR

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to

Commission file number 1-9356

Buckeye Partners, L.P. (Exact name of registrant as specified in its charter)

Delaware 23-2432497 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification number)

5002 Buckeye Road P. O. Box 368 Emmaus, Pennsylvania 18049 (Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (484) 232-4000

Securities registered pursuant to Section 12(b) of the Act: Title of each class

Name of each exchange on which registered

LP Units representing limited partnership interests........................................... New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act:

None (Title of class)

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No

Indicate by check mark whether the registrant is an accelerated filer (as defined in Exchange Act 12b-2). Yes No At June 28, 2002, the aggregate market value of the registrant’s LP Units held by non-affiliates was $888 million. The calculation of such market value should not be construed as an admission or conclusion by the registrant that any person is in fact an affiliate of the registrant.

LP Units outstanding as of March 13, 2003: 28,702,346

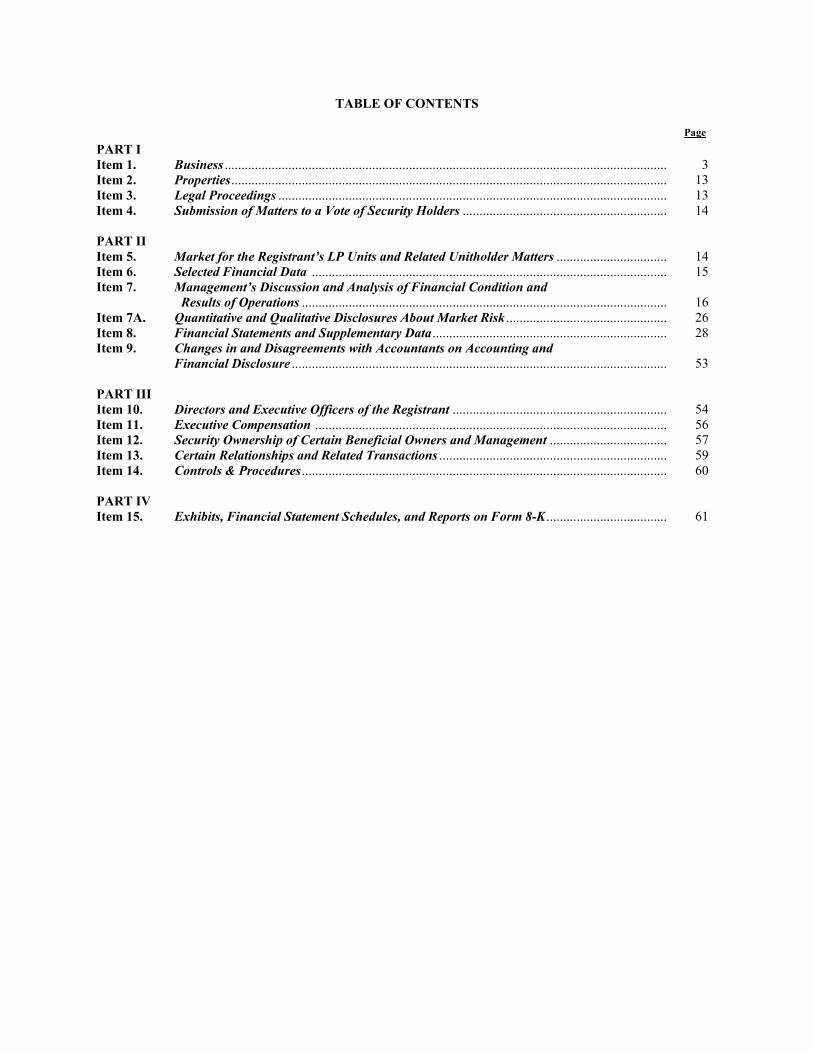

TABLE OF CONTENTS

Page

PART I Item 1. Business .................................................................................................................................... 3Item 2. Properties.................................................................................................................................. 13Item 3. Legal Proceedings .................................................................................................................... 13Item 4. Submission of Matters to a Vote of Security Holders ............................................................. 14 PART II Item 5. Market for the Registrant’s LP Units and Related Unitholder Matters ................................. 14Item 6. Selected Financial Data .......................................................................................................... 15Item 7. Management’s Discussion and Analysis of Financial Condition and

Results of Operations ............................................................................................................. 16Item 7A. Quantitative and Qualitative Disclosures About Market Risk ................................................ 26Item 8. Financial Statements and Supplementary Data...................................................................... 28Item 9. Changes in and Disagreements with Accountants on Accounting and

Financial Disclosure ................................................................................................................ 53 PART III Item 10. Directors and Executive Officers of the Registrant ................................................................ 54Item 11. Executive Compensation ......................................................................................................... 56Item 12. Security Ownership of Certain Beneficial Owners and Management ................................... 57Item 13. Certain Relationships and Related Transactions .................................................................... 59Item 14. Controls & Procedures............................................................................................................. 60 PART IV Item 15. Exhibits, Financial Statement Schedules, and Reports on Form 8-K .................................... 61

3

PART I

Item 1. Business Introduction Buckeye Partners, L.P. (the “Partnership”), the Registrant, is a master limited partnership organized in 1986 under the laws of the state of Delaware. The Partnership’s principal line of business is the transportation, terminalling and storage of refined petroleum products for major integrated oil companies, large refined product marketing companies and major end users of petroleum products on a fee basis through facilities owned and operated by the Partnership. The Partnership also operates pipelines owned by third parties under contracts with major integrated oil and chemical companies. The Partnership conducts all its operations through subsidiary entities. These operating subsidiaries are Buckeye Pipe Line Company, L.P. (“Buckeye”), Laurel Pipe Line Company, L.P. (“Laurel”), Everglades Pipe Line Company, L.P. (“Everglades”) and Buckeye Pipe Line Holdings, L.P. (“BPH”). (Each of Buckeye, Laurel, Everglades and BPH is referred to individually as an “Operating Partnership” and collectively as the “Operating Partnerships”). The Partnership owns approximately a 99 percent interest in each of the Operating Partnerships. BPH owns directly, or indirectly, a 100 percent interest in each of Buckeye Terminals, LLC (“BT”), Norco Pipe Line Company, LLC (“Norco”) and Buckeye Gulf Coast Pipe Lines, L.P. (“BGC”). BPH also owns a 75 percent interest in WesPac Pipeline-Reno Ltd., WesPac Pipeline-San Diego, Ltd. and related WesPac entities (collectively known as “WesPac”) and an 18.52 percent interest in West Shore Pipe Line Company. Buckeye Pipe Line Company (the “General Partner”) serves as the general partner to the Partnership. As of December 31, 2002, the General Partner owned approximately a 1 percent general partnership interest in the Partnership and approximately a 1 percent general partnership interest in each Operating Partnership, for an effective 2 percent interest in the Partnership. The General Partner is a wholly-owned subsidiary of Buckeye Management Company (“BMC”). BMC is a wholly-owned subsidiary of Glenmoor, Ltd. (“Glenmoor”). Glenmoor is owned by certain directors and members of senior management of the General Partner and trusts for the benefit of their families and by certain other management employees of Buckeye Pipe Line Services Company (“Services Company”). Services Company employs a significant portion of the employees that work for the Operating Partnerships. At December 31, 2002, Services Company had 506 full-time employees. Services Company entered into a Services Agreement with BMC and the General Partner in August 1997 to provide services to the Partnership and the Operating Partnerships through March 2011. Services Company is reimbursed by BMC or the General Partner for its direct and indirect expenses, which in turn are reimbursed by the Partnership, except for certain executive compensation costs. BT, Norco and BGC directly employed 115 full-time employees at December 31, 2002. Buckeye is one of the largest independent pipeline common carriers of refined petroleum products in the United States, with 2,909 miles of pipeline serving 9 states. Laurel owns a 345-mile common carrier refined products pipeline located principally in Pennsylvania. Norco owns a 482-mile pipeline in Indiana, Illinois and Ohio. Everglades owns 37 miles of refined petroleum products pipeline in Florida. Buckeye, Laurel, Norco and Everglades conduct the Partnership’s refined products pipeline business. BPH, through facilities it owns in Taylor, Michigan, provides bulk storage service with an aggregate capacity of 260,000 barrels of refined petroleum products. BT, with facilities located in New York, Pennsylvania, Ohio, Indiana and Illinois provides bulk storage services with an aggregate capacity of 4,848,000 barrels of refined petroleum products. BGC owns and operates petrochemical pipelines in the Gulf Coast area. BGC also provides engineering and construction management services to major chemical companies in the Gulf Coast area. WesPac provides turbine fuel transportation services to the Reno/Tahoe International Airport through a 3.0-mile pipeline and to the San Diego International Airport through a 4.3-mile pipeline. In March 1999, the Partnership acquired the fuels division of American Refining Group, Inc. (“ARG”) for approximately $13.7 million. The Partnership operated the former ARG processing business under the name of Buckeye Refining Company, LLC (“BRC”). BRC was sold to Kinder Morgan Energy Partners, L.P. (“Kinder Morgan”) on October 25, 2000 for approximately $45.7 million. BRC processed transmix at its Indianola,

4

Pennsylvania and Hartford, Illinois refineries. Transmix represents refined petroleum products, primarily fuel oil and gasoline that becomes commingled during normal pipeline operations. The refining process produced separate quantities of fuel oil, kerosene and gasoline that BRC then marketed at the wholesale level. In March 1999, the Partnership also acquired pipeline operating contracts and a 16-mile pipeline from Seagull Products Pipeline Corporation and Seagull Energy Corporation (“Seagull”) for approximately $5.8 million. The Partnership operates the assets acquired from Seagull under the name of Buckeye Gulf Coast Pipe Lines, LLC. BGC is an owner and contract operator of pipelines owned by major chemical companies in the Gulf Coast area. BGC leases its 16-mile pipeline to a major chemical company. In June 2000, the Partnership also acquired six petroleum products terminals from Agway Energy Products LLC (“Agway”) for approximately $20.7 million. The terminals acquired had an aggregate capacity of approximately 1.8 million barrels and are located in Brewerton, Geneva, Marcy, Rochester and Vestal, New York and Macungie, Pennsylvania. The Partnership operates the assets acquired from Agway under the name of Buckeye Terminals, LLC. On July 31, 2001, the Partnership acquired a refined products pipeline system and related terminals from affiliates of TransMontaigne Inc. for approximately $62.3 million. The assets included a 482-mile refined petroleum products pipeline that runs from Hartsdale, Indiana west to Fort Madison, Iowa and east to Toledo, Ohio, with an 11-mile pipeline connection between major storage terminals in Hartsdale and East Chicago, Indiana. These assets are operated by the Partnership under the name of Norco Pipe Line Company, LLC. The acquired assets also included 3.2 million barrels of pipeline storage and trans-shipment facilities in Hartsdale and East Chicago, Indiana and Toledo, Ohio; and four petroleum products terminals located in Bryan, Ohio; South Bend and Indianapolis, Indiana; and Peoria, Illinois. The storage and terminal assets are operated by Buckeye Terminals, LLC. On October 29, 2001, the Partnership acquired 6,805 shares of common stock of West Shore Pipe Line Company (“West Shore”) from TransMontaigne Pipeline Inc. for approximately $23.3 million. The common stock represents an 18.52 percent interest in West Shore. West Shore owns and operates a pipeline system that originates in the Chicago, Illinois area and extends north to Green Bay, Wisconsin and west and then north to Madison, Wisconsin. The pipeline system transports refined petroleum products to users in northern Illinois and Wisconsin. The other stockholders of West Shore are major oil companies. The pipeline is operated under contract by Citgo Pipeline Company. Refined Products Transportation The Partnership receives petroleum products from refineries, connecting pipelines and marine terminals, and transports those products to other locations. In 2002, refined petroleum products transportation accounted for approximately 86% of the Partnership’s consolidated revenues. The Partnership transported an average of approximately 1,101,400 barrels per day of refined products in 2002. The following table shows the volume and percentage of refined petroleum products transported over the last three years.

Volume and Percentage of Refined Petroleum Products Transported (1) (Volume in thousands of barrels per day)

(1) Excludes local product transfers. (2) Includes diesel fuel, heating oil, kerosene and other middle distillates.

5

The Partnership provides refined product pipeline service in the following states: Pennsylvania, New York, New Jersey, Indiana, Ohio, Michigan, Illinois, Connecticut, Massachusetts, Nevada, California and Florida. Pennsylvania—New York—New Jersey Buckeye serves major population centers in the states of Pennsylvania, New York and New Jersey through 943 miles of pipeline. Refined petroleum products are received at Linden, New Jersey from approximately 17 major source points, including 2 refineries, 6 connecting pipelines and 9 storage and terminalling facilities. Products are then transported through two lines from Linden, New Jersey to Allentown, Pennsylvania. From Allentown, the pipeline continues west, through a connection with Laurel, to Pittsburgh, Pennsylvania (serving Reading, Harrisburg, Altoona/Johnstown and Pittsburgh) and north through eastern Pennsylvania into New York (serving Scranton/Wilkes-Barre, Binghamton, Syracuse, Utica and Rochester and, via a connecting carrier, Buffalo). Buckeye leases capacity in one of the pipelines extending from Pennsylvania to upstate New York to a major oil company. Products received at Linden, New Jersey are also transported through one line to Newark International Airport and through two additional lines to J. F. Kennedy International and LaGuardia airports and to commercial bulk terminals at Long Island City and Inwood, New York. These pipelines supply J. F. Kennedy, LaGuardia and Newark airports with substantially all of each airport’s jet fuel requirements. Laurel transports refined petroleum products through a 345-mile pipeline extending westward from five refineries and a connection to Colonial Pipeline Company in the Philadelphia area to Reading, Harrisburg, Altoona /Johnstown and Pittsburgh, Pennsylvania. Indiana—Ohio—Michigan—Illinois Buckeye and Norco transport refined petroleum products through 2,336 miles of pipeline (of which 246 miles are jointly owned with other pipeline companies) in southern Illinois, central Indiana, eastern Michigan, western and northern Ohio and western Pennsylvania. A number of receiving and delivery lines connect to a central corridor which runs from Lima, Ohio, through Toledo, Ohio to Detroit, Michigan. Products are received at East Chicago, Indiana; Robinson, Illinois and at refinery and other pipeline connection points near Detroit, Toledo and Lima. Major market areas served include Peoria, Illinois; Huntington/Fort Wayne, Indianapolis and South Bend, Indiana; Bay City, Detroit and Flint, Michigan; Cleveland, Columbus, Lima and Toledo, Ohio; and Pittsburgh, Pennsylvania. Other Refined Products Pipelines Buckeye serves Connecticut and Massachusetts through 112 miles of pipeline (the “Jet Lines System”) that carry refined products from New Haven, Connecticut to Hartford, Connecticut and Springfield, Massachusetts. Everglades transports primarily turbine fuel on a 37-mile pipeline from Port Everglades, Florida to Hollywood-Ft. Lauderdale International Airport and Miami International Airport. Everglades supplies Miami International Airport with substantially all of its turbine fuel requirements. WesPac Pipeline-Reno Ltd., owns a 3.0-mile pipeline serving the Reno/Tahoe International Airport. WesPac Pipeline – San Diego Ltd. owns a 4.3-mile pipeline serving the San Diego International Airport. Both of these pipelines transport turbine fuel. Each of these WesPac entities is a joint venture between BPH and Kealine Partners in which BPH owns a 75 percent ownership interest. The Partnership also provides $8.9 million in debt financing to WesPac entities. Other Business Activities BPH provides bulk storage services through facilities located in Taylor, Michigan that have the capacity to store an aggregate of approximately 260,000 barrels of refined petroleum products. BT, a wholly-owned subsidiary of BPH, operates 14 terminals located in New York, Pennsylvania, Ohio, Indiana and Illinois that provide bulk storage and throughput services and have the capacity to store an aggregate of approximately 4,848,000 barrels of refined petroleum products. Together, these terminalling and storage activities provided approximately 8% of the Partnership’s revenue in 2002. BPH also owns an 18.52 percent stock interest in West Shore Pipe Line Company.

6

West Shore owns and operates a pipeline system that originates in the Chicago, Illinois area and extends north to Green Bay, Wisconsin and west and then north to Madison, Wisconsin. The pipeline system transports refined petroleum products to users in northern Illinois and Wisconsin. The other stockholders of West Shore are major oil companies. West Shore is operated under contract by Citgo Pipeline Company. BGC, a wholly-owned subsidiary of BPH, is a contract operator of pipelines owned by major chemical companies in the state of Texas. BGC currently has seven operations and maintenance contracts in place. In addition, BGC owns a 16-mile pipeline located in the state of Texas that it leases to a third-party chemical company. A subsidiary of BGC also owns approximately 63 percent of a crude butadiene pipeline between Deer Park, Texas and Port Arthur, Texas that was completed in March 2003. In 2002, BGC’s contract operations provided approximately 6% of the Partnership’s revenue. BGC also provides engineering and construction management services to major chemical companies in the Gulf Coast area. Competition and Other Business Considerations The Operating Partnerships conduct business without the benefit of exclusive franchises from government entities. In addition, the Operating Partnerships pipeline operations generally operate as common carriers, providing transportation services at posted tariffs and without long-term contracts. The Operating Partnerships do not own the products they transport. Demand for the services provided by the Operating Partnerships derives from demand for petroleum products in the regions served and the ability and willingness of refiners, marketers and end-users to supply such demand by deliveries through the Operating Partnerships’ pipelines. Demand for refined petroleum products is primarily a function of price, prevailing general economic conditions and weather. The Operating Partnerships’ businesses are, therefore, subject to a variety of factors partially or entirely beyond their control. Multiple sources of pipeline entry and multiple points of delivery, however, have historically helped maintain stable total volumes even when volumes at particular source or destination points have changed. The Partnership’s business may in the future be affected by changing oil prices or other factors affecting demand for oil and other fuels. The Partnership’s business may also be impacted by energy conservation, changing sources of supply, structural changes in the oil industry and new energy technologies. The General Partner is unable to predict the effect of such factors. Changes in transportation and travel patterns in the areas served by the Partnership’s pipelines as well as further improvements in average fuel efficiency could adversely affect the Partnership’s results of operations and financial condition. In 2002, the pipeline transportation business had approximately 110 customers, most of which were either major integrated oil companies or large refined product marketing companies. The largest two customers accounted for 6.5 percent and 6.3 percent, respectively, of consolidated transportation revenues, while the 20 largest customers accounted for 64.3 percent of consolidated transportation revenues. Generally, pipelines are the lowest cost method for long-haul overland movement of refined petroleum products. Therefore, the Operating Partnerships’ most significant competitors for large volume shipments are other pipelines, many of which are owned and operated by major integrated oil companies. Although it is unlikely that a pipeline system comparable in size and scope to the Operating Partnerships’ pipeline system will be built in the foreseeable future, new pipelines (including pipeline segments that connect with existing pipeline systems) could be built to effectively compete with the Operating Partnerships in particular locations. In the Midwest, several petroleum product pipeline expansions and two new petroleum product pipeline construction projects are in various stages of completion. Generally, these projects will increase the capacity to bring additional refined products into the Partnership’s service area. Because the Operating Partnerships own multiple pipelines throughout the Partnership’s service area and these projects do not impact local petroleum product supply and demand, the General Partner believes that the completion of these pipeline projects may result in volumes shifting from one Operating Partnership pipeline segment to another, but will not, in the aggregate, have a material adverse effect on the Operating Partnership’s results of operations or financial condition. The Operating Partnerships compete with marine transportation in some areas. Tankers and barges on the Great Lakes account for some of the volume to certain Michigan, Ohio and upstate New York locations during the

7

approximately eight non-winter months of the year. Barges are presently a competitive factor for deliveries to the New York City area, the Pittsburgh area, Connecticut and Ohio. Trucks competitively deliver product in a number of areas served by the Operating Partnerships. While their costs may not be competitive for longer hauls or large volume shipments, trucks compete effectively for incremental and marginal volumes in many areas served by the Operating Partnerships. The availability of truck transportation places a significant competitive constraint on the ability of the Operating Partnerships to increase their tariff rates. Privately arranged exchanges of product between marketers in different locations are an increasing but non-quantified form of competition. Generally, such exchanges reduce both parties’ costs by eliminating or reducing transportation charges. In addition, consolidation among refiners and marketers that has accelerated in recent years has altered distribution patterns, reducing demand for transportation services in some markets and increasing them in other markets. Distribution of refined petroleum products depends to a large extent upon the location and capacity of refineries. However, because the Partnership’s business is largely driven by the consumption of fuel in its delivery areas and the Operating Partnerships’ pipelines have numerous source points, the General Partner does not believe that the expansion or shutdown of any particular refinery would have a material effect on the business of the Partnership. The General Partner is unable to determine whether refinery expansions or shutdowns will occur or what their specific effect would be. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Forward-Looking Information – Competition and Other Business Conditions.” The Operating Partnerships’ mix of products transported tends to vary seasonally. Declines in demand for heating oil during the summer months are, to a certain extent, offset by increased demand for gasoline and jet fuel. Overall, operations have been only moderately seasonal, with somewhat lower than average volume being transported during March, April and May and somewhat higher than average volume being transported in November, December and January. Neither the Partnership nor any of the Operating Partnerships, other than BPH’s subsidiaries, has any employees. The Operating Partnerships are managed and operated by employees of Services Company, BGC, Norco and BT. In addition, Glenmoor provides certain management services to BMC, the General Partner and Services Company. At December 31, 2002, Services Company had a total of 506 full-time employees, 145 of whom were represented by two labor unions. At December 31, 2002, BGC had a total of 63 full-time, non-union employees, Norco had a total of 30 full-time, non-union employees and BT had a total of 22 full-time, non-union employees. The Operating Partnerships (and their predecessors) have never experienced any significant work stoppages or other significant labor problems. Capital Expenditures The Partnership incurs capital expenditures in order to maintain and enhance the safety and integrity of its pipelines and related assets, to expand the reach or capacity of its pipelines, to improve the efficiency of its operations or to pursue new business opportunities. During 2002 the Partnership incurred $71.6 million of capital expenditures, of which $28.2 million related to maintenance and integrity, $6.6 million related to expansion or cost reduction projects and $36.8 million related to the construction of a 90-mile crude butadiene pipeline. Financing for the Partnership’s capital expenditures was provided by cash from operations, borrowings under the Partnership’s revolving credit facilities and, with respect to the crude butadiene pipeline, $14.2 million from advances provided by two petrochemical companies involved in the project. The crude butadiene pipeline was completed in March 2003. In 2003, the Partnership anticipates capital expenditures of approximately $40 million, of which approximately $25 million is expected to relate to maintenance and integrity projects and approximately $15 million is expected to relate to expansion and cost reduction projects. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources.”

8

Regulation General Buckeye and Norco are interstate common carriers subject to the regulatory jurisdiction of the Federal Energy Regulatory Commission (“FERC”) under the Interstate Commerce Act and the Department of Energy Organization Act. FERC regulation requires that interstate oil pipeline rates be posted publicly and that these rates be “just and reasonable” and non-discriminatory. FERC regulation also enforces common carrier obligations and specifies a uniform system of accounts. In addition, Buckeye, Norco and the other Operating Partnerships are subject to the jurisdiction of certain other federal agencies with respect to environmental and pipeline safety matters. The Operating Partnerships are also subject to the jurisdiction of various state and local agencies, including, in some states, public utility commissions which have jurisdiction over, among other things, intrastate tariffs, the issuance of debt and equity securities, transfers of assets and pipeline safety. FERC Rate Regulation Buckeye's rates are governed by a market-based rate regulation program initially approved by FERC in March 1991 and subsequently extended. Under this program, in markets where Buckeye does not have significant market power, individual rate increases: (a) will not exceed a real (i.e., exclusive of inflation) increase of 15 percent over any two-year period (the "rate cap"), and (b) will be allowed to become effective without suspension or investigation if they do not exceed a "trigger" equal to the change in the Gross Domestic Product implicit price deflator since the date on which the individual rate was last increased, plus 2 percent. Individual rate decreases will be presumptively valid upon a showing that the proposed rate exceeds marginal costs. In markets where Buckeye was found to have significant market power and in certain markets where no market power finding was made: (i) individual rate increases cannot exceed the volume-weighted average rate increase in markets where Buckeye does not have significant market power since the date on which the individual rate was last increased, and (ii) any volume-weighted average rate decrease in markets where Buckeye does not have significant market power must be accompanied by a corresponding decrease in all of Buckeye's rates in markets where it does have significant market power. Shippers retain the right to file complaints or protests following notice of a rate increase, but are required to show that the proposed rates violate or have not been adequately justified under the market-based rate regulation program, that the proposed rates are unduly discriminatory, or that Buckeye has acquired significant market power in markets previously found to be competitive. The Buckeye program is an exception to the generic oil pipeline regulations issued under the Energy Policy Act of 1992. The generic rules rely primarily on an index methodology, whereby a pipeline is allowed to change its rates in accordance with an index (currently the Producer Price Index) that FERC believes reflects cost changes appropriate for application to pipeline rates. Alternatively, a pipeline is allowed to charge market-based rates if the pipeline establishes that it does not possess significant market power in a particular market. In addition, the rules provide for the rights of both pipelines and shippers to demonstrate that the index should not apply to an individual pipeline's rates in light of the pipeline's costs. The final rules became effective on January 1, 1995. The Buckeye program was subject to review by FERC in 2000 when FERC reviewed the index selected in the generic oil pipeline regulations. FERC decided to continue the generic oil pipeline regulations with no material changes and did not modify or discontinue Buckeye’s program. The General Partner cannot predict the impact that any change to Buckeye’s rate program would have on Buckeye’s operations. Independent of regulatory considerations, it is expected that tariff rates will continue to be constrained by competition and other market factors. Norco’s tariff rates are governed by the generic FERC index methodology, and therefore are subject to change annually according to the index. Environmental Matters The Operating Partnerships are subject to federal, state and local laws and regulations relating to the protection of the environment. Although the General Partner believes that the operations of the Operating Partnerships comply in all material respects with applicable environmental laws and regulations, risks of substantial liabilities are

9

inherent in pipeline operations, and there can be no assurance that material environmental liabilities will not be incurred. Moreover, it is possible that other developments, such as increasingly rigorous environmental laws, regulations and enforcement policies thereunder, and claims for damages to property or injuries to persons resulting from the operations of the Operating Partnerships, could result in substantial costs and liabilities to the Partnership. See “Legal Proceedings” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Environmental Matters.” The Oil Pollution Act of 1990 (“OPA”) amended certain provisions of the federal Water Pollution Control Act of 1972, commonly referred to as the Clean Water Act (“CWA”), and other statutes as they pertain to the prevention of and response to petroleum product spills into navigable waters. The OPA subjects owners of facilities to strict joint and several liability for all containment and clean-up costs and certain other damages arising from a spill. The CWA provides penalties for any discharges of petroleum products in reportable quantities and imposes substantial liability for the costs of removing a spill. State laws for the control of water pollution also provide varying civil and criminal penalties and liabilities in the case of releases of petroleum or its derivatives into surface waters or into the ground. Regulations are currently being developed under OPA and state laws that may impose additional regulatory burdens on the Partnership. Contamination resulting from spills or releases of refined petroleum products is not unusual in the petroleum pipeline industry. The Operating Partnerships’ pipelines cross numerous navigable rivers and streams. Although the General Partner believes that the Operating Partnerships comply in all material respects with the spill prevention, control and countermeasure requirements of federal laws, any spill or other release of petroleum products into navigable waters may result in material costs and liabilities to the Partnership. The Resource Conservation and Recovery Act (“RCRA”), as amended, establishes a comprehensive program of regulation of “hazardous wastes.” Hazardous waste generators, transporters, and owners or operators of treatment, storage and disposal facilities must comply with regulations designed to ensure detailed tracking, handling and monitoring of these wastes. RCRA also regulates the disposal of certain non-hazardous wastes. As a result of these regulations, certain wastes typically generated by pipeline operations are considered “hazardous wastes” which are subject to rigorous disposal requirements. The Comprehensive Environmental Response, Compensation and Liability Act of 1980 (“CERCLA”), also known as “Superfund,” governs the release or threat of release of a “hazardous substance.” Releases of a hazardous substance, whether on or off-site, may subject the generator of that substance to liability under CERCLA for the costs of clean-up and other remedial action. Pipeline maintenance and other activities in the ordinary course of business generate “hazardous substances.” As a result, to the extent a hazardous substance generated by the Operating Partnerships or their predecessors may have been released or disposed of in the past, the Operating Partnerships may in the future be required to remedy contaminated property. Governmental authorities such as the Environmental Protection Agency, and in some instances third parties, are authorized under CERCLA to seek to recover remediation and other costs from responsible persons, without regard to fault or the legality of the original disposal. In addition to its potential liability as a generator of a “hazardous substance,” the property or right-of-way of the Operating Partnerships may be adjacent to or in the immediate vicinity of Superfund and other hazardous waste sites. Accordingly, the Operating Partnerships may be responsible under CERCLA for all or part of the costs required to cleanup such sites, which costs could be material. The Clean Air Act, amended by the Clean Air Act Amendments of 1990 (the “Amendments”), imposes controls on the emission of pollutants into the air. The Amendments required states to develop facility-wide permitting programs over the past several years to comply with new federal programs. Existing operating and air-emission requirements like those currently imposed on the Operating Partnerships are being reviewed by appropriate state agencies in connection with the new facility-wide permitting program. It is possible that new or more stringent controls will be imposed upon the Operating Partnerships through this permit review process. The Operating Partnerships are also subject to environmental laws and regulations adopted by the various states in which they operate. In certain instances, the regulatory standards adopted by the states are more stringent than applicable federal laws.

10

In 1986, certain predecessor companies acquired by the Partnership, namely Buckeye Pipe Line Company and its subsidiaries (“Pipe Line”), entered into an Administrative Consent Order (“ACO”) with the New Jersey Department of Environmental Protection and Energy under the New Jersey Environmental Cleanup Responsibility Act of 1983 (“ECRA”) relating to all six of Pipe Line’s facilities in New Jersey. The ACO permitted the 1986 acquisition of Pipe Line to be completed prior to full compliance with ECRA, but required Pipe Line to conduct in a timely manner a sampling plan for environmental conditions at the New Jersey facilities and to implement any required clean-up plan. Sampling continues in an effort to identify areas of contamination at the New Jersey facilities, while clean-up operations have begun and have been completed at certain of the sites. The obligations of Pipe Line were not assumed by the Partnership and the costs of compliance have been and will continue to be paid by American Financial Group, Inc. Pipeline Regulation and Safety Matters The Operating Partnerships are subject to regulation by the United States Department of Transportation (“DOT”) under the Hazardous Liquid Pipeline Safety Act of 1979 (“HLPSA”) relating to the design, installation, testing, construction, operation, replacement and management of their pipeline facilities. HLPSA covers petroleum and petroleum products and requires any entity that owns or operates pipeline facilities to comply with applicable safety standards, to establish and maintain a plan of inspection and maintenance and to comply with such plans. The Pipeline Safety Reauthorization Act of 1988 requires coordination of safety regulation between federal and state agencies, testing and certification of pipeline personnel, and authorization of safety-related feasibility studies. The General Partner has initiated drug and alcohol testing programs to comply with the regulations promulgated by the Office of Pipeline Safety and DOT. HLPSA requires, among other things, that the Secretary of Transportation consider the need for the protection of the environment in issuing federal safety standards for the transportation of hazardous liquids by pipeline. The legislation also requires the Secretary of Transportation to issue regulations concerning, among other things, the identification by pipeline operators of environmentally sensitive areas; the circumstances under which emergency flow restricting devices should be required on pipelines; training and qualification standards for personnel involved in maintenance and operation of pipelines; and the periodic integrity testing of pipelines in unusually sensitive and high-density population areas by internal inspection devices or by hydrostatic testing. Effective in August 1999, the DOT issued its Operator Qualification Rule, which required a written program by April 27, 2001, for ensuring operators are qualified to perform tasks covered by the pipeline safety rules. All persons performing covered tasks must have been qualified under the program by October 28, 2002. The General Partner has identified the tasks that must be performed to comply with this rule, has filed its written plan and has qualified its employees and contractors as required. In addition, on December 1, 2000, DOT published notice of final rulemaking for Pipeline Integrity Management in High Consequence Areas (Hazardous Liquid Operators with 500 or more Miles of Pipeline). This rule sets forth regulations that require pipeline operators to assess, evaluate, repair and validate the integrity of hazardous liquid pipeline segments that, in the event of a leak or failure, could affect populated areas, areas unusually sensitive to environmental damage or commercially navigable waterways. Under the rule, pipeline operators were required to identify line segments which could impact high consequence areas by December 31, 2001. Pipeline operators were required to develop “Baseline Assessment Plans” for evaluating the integrity of each pipeline segment by March 31, 2002 and to complete an assessment of the highest risk 50 percent of line segments by September 30, 2004, with full assessment of the remaining 50 percent by March 31, 2008. Pipeline operators will thereafter be required to re-assess each affected segment in intervals not to exceed five years. In December 2002 the Pipeline Safety Improvement Act of 2002 (“PSIA”) became effective. The PSIA imposes additional obligations on pipeline operators, increases penalties for statutory and regulatory violations, and includes provisions prohibiting employers from taking adverse employment action against pipeline employees and contractors who raise concerns about pipeline safety within the company or with government agencies or the press. Many of the provisions of the PSIA are subject to regulations to be issued by the Department of Transportation. While the PSIA imposes additional operating requirements on pipeline operators, the General Partner does not believe that cost of compliance with the PSIA is likely to be material in the context of the Partnership’s operations. The General Partner believes that the Operating Partnerships currently comply in all material respects with HLPSA and other pipeline safety laws and regulations. However, the industry, including the Partnership, will, in the

11

future, incur additional pipeline and tank integrity expenditures and the Partnership is likely to incur increased operating costs based on these and other government regulations. During 2002, the Partnership’s integrity expenditures increased to approximately $21 million. The General Partner expects integrity expenditures to continue at this level during 2003 in order to complete most of its initial assessment and pipeline improvements required by HLPSA. Once this initial assessment is complete, re-assessments are expected to cost significantly less and will be expensed. The General Partner believes these additional capital and operating expenditures with respect to HLSPA requirements will be offset, to some degree, by a reduced need for other facility improvements and lower operating expenses associated with improved pipeline facilities. The Operating Partnerships are also subject to the requirements of the Federal Occupational Safety and Health Act (“OSHA”) and comparable state statutes. The General Partner believes that the Operating Partnerships’ operations comply in all material respects with OSHA requirements, including general industry standards, record- keeping, hazard communication requirements and monitoring of occupational exposure to benzene and other regulated substances. The General Partner cannot predict whether or in what form any new legislation or regulatory requirements might be enacted or adopted or the costs of compliance. In general, any such new regulations would increase operating costs and impose additional capital expenditure requirements on the Partnership, but the General Partner does not presently expect that such costs or capital expenditure requirements would have a material adverse effect on the Partnership’s results of operations or financial condition. Tax Treatment of Publicly Traded Partnerships under the Internal Revenue Code The Internal Revenue Code of 1986, as amended (the “Code”), imposes certain limitations on the current deductibility of losses attributable to investments in publicly traded partnerships and treats certain publicly traded partnerships as corporations for federal income tax purposes. The following discussion briefly describes certain aspects of the Code that apply to individuals who are citizens or residents of the United States without commenting on all of the federal income tax matters affecting the Partnership or the holders of LP units (“Unitholders”), and is qualified in its entirety by reference to the Code. UNITHOLDERS ARE URGED TO CONSULT THEIR OWN TAX ADVISOR ABOUT THE FEDERAL, STATE, LOCAL AND FOREIGN TAX CONSEQUENCES TO THEM OF AN INVESTMENT IN THE PARTNERSHIP. Characterization of the Partnership for Tax Purposes The Code treats a publicly traded partnership that existed on December 17, 1987, such as the Partnership, as a corporation for federal income tax purposes, unless, for each taxable year of the Partnership, under Section 7704(d) of the Code, 90 percent or more of its gross income consists of “qualifying income.” Qualifying income includes interest, dividends, real property rents, gains from the sale or disposition of real property, income and gains derived from the exploration, development, mining or production, processing, refining, transportation (including pipelines transporting gas, oil or products thereof), or the marketing of any mineral or natural resource (including fertilizer, geothermal energy and timber), and gain from the sale or disposition of capital assets that produce such income. Because the Partnership is engaged primarily in the refined products pipeline transportation business, the General Partner believes that 90 percent or more of the Partnership’s gross income has been qualifying income. If this continues to be true and no subsequent legislation amends that provision, the Partnership will continue to be classified as a partnership and not as a corporation for federal income tax purposes. Passive Activity Loss Rules The Code provides that an individual, estate, trust or personal service corporation generally may not deduct losses from passive business activities, to the extent they exceed income from all such passive activities, against other (active) income. Income that may not be offset by passive activity losses includes not only salary and active business income, but also portfolio income such as interest, dividends or royalties or gain from the sale of property that produces portfolio income. Credits from passive activities are also limited to the tax attributable to any income from passive activities. The passive activity loss rules are applied after other applicable limitations on deductions, such as the at-risk rules and basis limitations. Certain closely held corporations are subject to slightly different rules that can also limit their ability to offset passive losses against certain types of income.

12

Under the Code, net income from publicly traded partnerships is not treated as passive income for purposes of the passive loss rule, but is treated as non-passive income. Net losses and credits attributable to an interest in a publicly traded partnership are not allowed to offset a partner’s other income. Thus, a Unitholder’s proportionate share of the Partnership’s net losses may be used to offset only Partnership net income from its trade or business in succeeding taxable years or, upon a complete disposition of a Unitholder’s interest in the Partnership to an unrelated person in a fully taxable transaction, may be used to (i) offset gain recognized upon the disposition, and (ii) then against all other income of the Unitholder. In effect, net losses are suspended and carried forward indefinitely until utilized to offset net income of the Partnership from its trade or business or allowed upon the complete disposition to an unrelated person in a fully taxable transaction of the Unitholder’s interest in the Partnership. A Unitholder’s share of Partnership net income may not be offset by passive activity losses generated by other passive activities. In addition, a Unitholder’s proportionate share of the Partnership’s portfolio income, including portfolio income arising from the investment of the Partnership’s working capital, is not treated as income from a passive activity and may not be offset by such Unitholder’s share of net losses of the Partnership. Deductibility of Interest Expense The Code generally provides that investment interest expense is deductible only to the extent of a non-corporate taxpayer’s net investment income. In general, net investment income for purposes of this limitation includes gross income from property held for investment, gain attributable to the disposition of property held for investment (except for net capital gains for which the taxpayer has elected to be taxed at special capital gains rates) and portfolio income (determined pursuant to the passive loss rules) reduced by certain expenses (other than interest) which are directly connected with the production of such income. Property subject to the passive loss rules is not treated as property held for investment. However, the IRS has issued a Notice which provides that net income from a publicly traded partnership (not otherwise treated as a corporation) may be included in net investment income for purposes of the limitation on the deductibility of investment interest. A Unitholder’s investment income attributable to its interest in the Partnership will include both its allocable share of the Partnership’s portfolio income and trade or business income. A Unitholder’s investment interest expense will include its allocable share of the Partnership’s interest expense attributable to portfolio investments. Unrelated Business Taxable Income Certain entities otherwise exempt from federal income taxes (such as individual retirement accounts, pension plans and charitable organizations) are nevertheless subject to federal income tax on net unrelated business taxable income and each such entity must file a tax return for each year in which it has more than $1,000 of gross income from unrelated business activities. The General Partner believes that substantially all of the Partnership’s gross income will be treated as derived from an unrelated trade or business and taxable to such entities. The tax-exempt entity’s share of the Partnership’s deductions directly connected with carrying on such unrelated trade or business are allowed in computing the entity’s taxable unrelated business income. ACCORDINGLY, INVESTMENT IN THE PARTNERSHIP BY TAX-EXEMPT ENTITIES SUCH AS INDIVIDUAL RETIREMENT ACCOUNTS, PENSION PLANS AND CHARITABLE TRUSTS MAY NOT BE ADVISABLE. State Tax Treatment During 2002, the Partnership owned property or conducted business in the states of Pennsylvania, New York, New Jersey, Indiana, Ohio, Michigan, Illinois, Connecticut, Massachusetts, Florida, Texas, Nevada and California. A Unitholder will likely be required to file state income tax returns and to pay applicable state income taxes in many of these states and may be subject to penalties for failure to comply with such requirements. Some of the states have proposed that the Partnership withhold a percentage of income attributable to Partnership operations within the state for Unitholders who are non-residents of the state. In the event that amounts are required to be withheld (which may be greater or less than a particular Unitholder’s income tax liability to the state), such withholding would generally not relieve the non-resident Unitholder from the obligation to file a state income tax return.

13

Certain Tax Consequences to Unitholders Upon formation of the Partnership in 1986, the General Partner elected twelve-year straight-line depreciation for tax purposes. For this reason, starting in 1999, the amount of depreciation available to the Partnership has been reduced significantly and taxable income has increased accordingly. Unitholders, however, will continue to offset Partnership income with individual LP Unit depreciation under their IRC section 754 election. Each Unitholder’s tax situation will differ depending upon the price paid and when LP Units were purchased. Generally, those who purchased LP Units within the past few years will have adequate depreciation to offset a considerable portion of Partnership income, while those who purchased LP Units more than several years ago will experience the full increase in taxable income. Unitholders are reminded that, in spite of the additional taxable income beginning in 1999, the current level of cash distributions exceed expected tax payments. Furthermore, sale of LP Units will result in taxable ordinary income as a consequence of depreciation recapture. UNITHOLDERS ARE ENCOURAGED TO CONSULT THEIR PROFESSIONAL TAX ADVISORS REGARDING THE TAX IMPLICATIONS TO THEIR INVESTMENT IN LP UNITS. Available Information The Partnership files annual, quarterly, and current reports and other documents with the SEC under the Securities Exchange Act of 1934. The public can obtain any documents that we file with the SEC at http://www.sec.gov. We also make available free of charge our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after filing such materials with, or furnishing such materials to, the SEC, on or through our Internet website, www.buckeye.com. We are not including the information contained on our Web site as a part of, or incorporating it by reference into, this Annual Report on Form 10-K. Item 2. Properties As of December 31, 2002, the principal facilities of the Partnership included 3,761 miles of 6-inch to 24-inch diameter pipeline, 49 pumping stations, 90 delivery points, various sized tanks having an aggregate capacity of approximately 14.7 million barrels and 15 bulk storage and terminal facilities. The Operating Partnerships and their subsidiaries own substantially all of these facilities. In general, the Partnership’s pipelines are located on land owned by others pursuant to rights granted under easements, leases, licenses and permits from railroads, utilities, governmental entities and private parties. Like other pipelines, certain of the Operating Partnerships’ and their subsidiaries rights are revocable at the election of the grantor or are subject to renewal at various intervals, and some require periodic payments. The Operating Partnerships and their subsidiaries have not experienced any revocations or lapses of such rights which were material to their business or operations, and the General Partner has no reason to expect any such revocation or lapse in the foreseeable future. Most delivery points, pumping stations and terminal facilities are located on land owned by the Operating Partnerships or their subsidiaries. The General Partner believes that the Operating Partnerships and their subsidiaries have sufficient title to their material assets and properties, possess all material authorizations and revocable consents from state and local governmental and regulatory authorities and have all other material rights necessary to conduct their business substantially in accordance with past practice. Although in certain cases the Operating Partnerships’ and their subsidiaries title to assets and properties or their other rights, including their rights to occupy the land of others under easements, leases, licenses and permits, may be subject to encumbrances, restrictions and other imperfections, none of such imperfections are expected by the General Partner to interfere materially with the conduct of the Operating Partnerships’ or their subsidiaries’ businesses. Item 3. Legal Proceedings The Partnership, in the ordinary course of business, is involved in various claims and legal proceedings, some of which are covered in whole or in part by insurance. The General Partner is unable to predict the timing or outcome

14

of these claims and proceedings. Although it is possible that one or more of these claims or proceedings, if adversely determined, could, depending on the relative amounts involved, have a material effect on the Partnership for a future period, the General Partner does not believe that their outcome will have a material effect on the Partnership’s consolidated financial condition or results of operations. With respect to environmental litigation, certain Operating Partnerships (or their predecessors) have been named in the past as defendants in lawsuits, or have been notified by federal or state authorities that they are potentially responsible parties (“PRPs”) under federal laws or a respondent under state laws relating to the generation, disposal or release of hazardous substances into the environment. Typically, an Operating Partnership is one of many PRPs for a particular site and its contribution of total waste at the site is minimal. However, because CERCLA and similar statutes impose liability without regard to fault and on a joint and several basis, the liability of an Operating Partnership in connection with such proceedings could be material. Although there is no material environmental litigation pending against the Partnership or the Operating Partnerships at this time, claims may be asserted in the future under various federal and state laws, and the amount of such claims or the potential liability, if any, cannot be estimated. See “Business—Regulation—Environmental Matters.” Item 4. Submission of Matters to a Vote of Security Holders No matters were submitted to a vote of the holders of LP Units during the fourth quarter of the fiscal year ended December 31, 2002.

PART II

Item 5. Market for the Registrant’s LP Units and Related Unitholder Matters The LP Units of the Partnership are listed and traded principally on the New York Stock Exchange. The high and low sales prices of the LP Units in 2002 and 2001, as reported in the New York Stock Exchange Composite Transactions, were as follows: 2002 2001 Quarter High Low High Low First ............................................................................................ $40.200 $35.510 $34.990 $28.375Second ........................................................................................ 40.000 34.000 38.100 31.270Third ........................................................................................... 38.850 26.500 38.000 28.500Fourth ......................................................................................... 39.500 33.700 37.640 34.550 During the months of December 2002 and January 2003, the Partnership gathered tax information from its known LP Unitholders and from brokers/nominees. Based on the information collected, the Partnership estimates its number of beneficial LP Unitholders to be approximately 24,000. Cash distributions paid during 2001 and 2002 were as follows: Record Date

Payment Date

Amount Per Unit

February 6, 2001................................................................................................... February 28, 2001 $ 0.600 May 4, 2001.......................................................................................................... May 31, 2001 0.600 August 6, 2001 ..................................................................................................... August 31, 2001 0.625 November 6, 2001 ................................................................................................ November 30, 2001 0.625 February 6, 2002................................................................................................... February 28, 2002 $ 0.625 May 5, 2002.......................................................................................................... May 31, 2002 0.625 August 6, 2002 ..................................................................................................... August 30, 2002 0.625 November 6, 2002 ................................................................................................ November 29, 2002 0.625

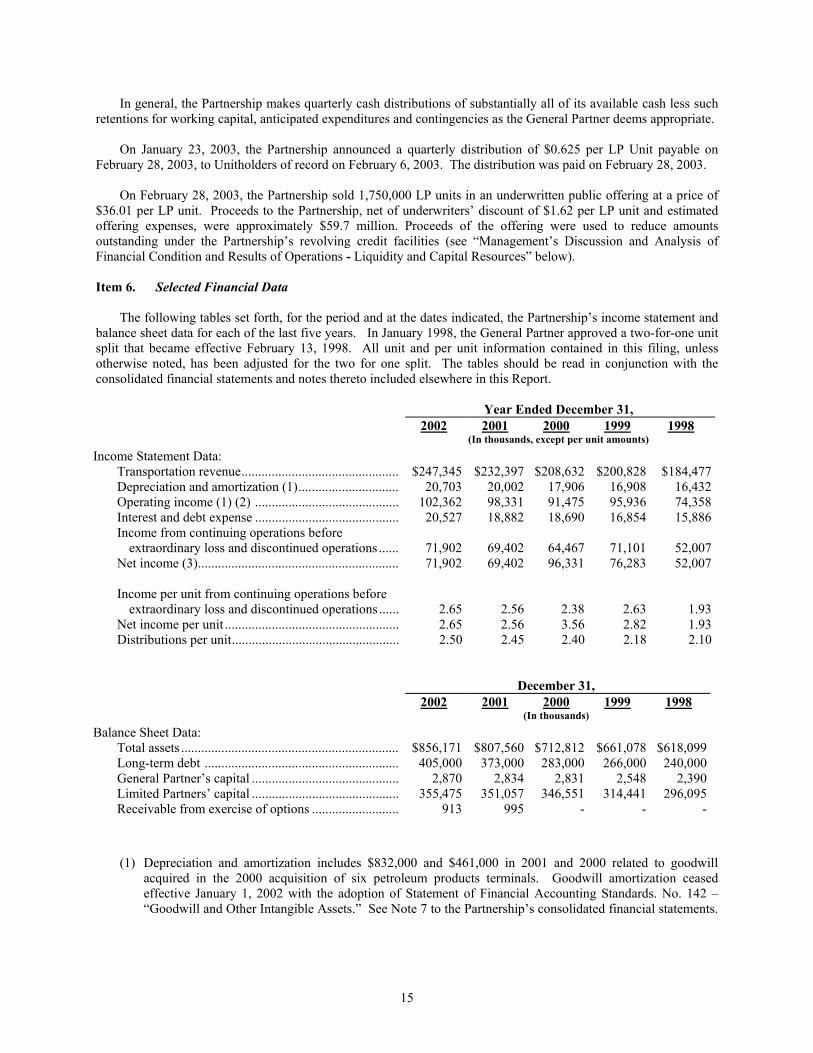

15

In general, the Partnership makes quarterly cash distributions of substantially all of its available cash less such retentions for working capital, anticipated expenditures and contingencies as the General Partner deems appropriate. On January 23, 2003, the Partnership announced a quarterly distribution of $0.625 per LP Unit payable on February 28, 2003, to Unitholders of record on February 6, 2003. The distribution was paid on February 28, 2003. On February 28, 2003, the Partnership sold 1,750,000 LP units in an underwritten public offering at a price of $36.01 per LP unit. Proceeds to the Partnership, net of underwriters’ discount of $1.62 per LP unit and estimated offering expenses, were approximately $59.7 million. Proceeds of the offering were used to reduce amounts outstanding under the Partnership’s revolving credit facilities (see “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources” below). Item 6. Selected Financial Data The following tables set forth, for the period and at the dates indicated, the Partnership’s income statement and balance sheet data for each of the last five years. In January 1998, the General Partner approved a two-for-one unit split that became effective February 13, 1998. All unit and per unit information contained in this filing, unless otherwise noted, has been adjusted for the two for one split. The tables should be read in conjunction with the consolidated financial statements and notes thereto included elsewhere in this Report.

Year Ended December 31, 2002 2001 2000 1999 1998 (In thousands, except per unit amounts)

Income Statement Data: Transportation revenue............................................... $247,345 $232,397 $208,632 $200,828 $184,477 Depreciation and amortization (1).............................. 20,703 20,002 17,906 16,908 16,432 Operating income (1) (2) ........................................... 102,362 98,331 91,475 95,936 74,358 Interest and debt expense ........................................... 20,527 18,882 18,690 16,854 15,886 Income from continuing operations before extraordinary loss and discontinued operations ...... 71,902 69,402

64,467

71,101 52,007

Net income (3)............................................................ 71,902 69,402 96,331 76,283 52,007 Income per unit from continuing operations before extraordinary loss and discontinued operations ...... 2.65 2.56

2.38

2.63 1.93

Net income per unit .................................................... 2.65 2.56 3.56 2.82 1.93 Distributions per unit.................................................. 2.50 2.45 2.40 2.18 2.10

December 31, 2002 2001 2000 1999 1998 (In thousands)

Balance Sheet Data: Total assets ................................................................. $856,171 $807,560 $712,812 $661,078 $618,099 Long-term debt .......................................................... 405,000 373,000 283,000 266,000 240,000 General Partner’s capital ............................................ 2,870 2,834 2,831 2,548 2,390 Limited Partners’ capital ............................................ 355,475 351,057 346,551 314,441 296,095 Receivable from exercise of options .......................... 913 995 - - -

(1) Depreciation and amortization includes $832,000 and $461,000 in 2001 and 2000 related to goodwill acquired in the 2000 acquisition of six petroleum products terminals. Goodwill amortization ceased effective January 1, 2002 with the adoption of Statement of Financial Accounting Standards. No. 142 – “Goodwill and Other Intangible Assets.” See Note 7 to the Partnership’s consolidated financial statements.

16

(2) Operating income for 1999 includes a one-time property tax expense reduction of $11.0 million following the settlement of a real property tax dispute with the City and State of New York.

(3) Net income includes income from discontinued operations of BRC of $5,682,000 in 2000 and $5,182,000

in 1999 and, in 2000, the gain of the sale of BRC of $26,182,000.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations The following is a discussion of the liquidity and capital resources and the results of operations of the Partnership for the periods indicated below. This discussion should be read in conjunction with the consolidated financial statements and notes thereto, which are included elsewhere in this report. Results of Operations Through its Operating Partnerships and their subsidiaries, the Partnership is principally engaged in the pipeline transportation of refined petroleum products and, between March 1999 and October 25, 2000, the refining of transmix. Products transported via pipeline include gasoline, jet fuel, diesel fuel, heating oil, kerosene and liquid propane gases (“LPGs”). The Partnership’s revenues derived from the transportation of refined petroleum products are principally a function of the volumes of refined petroleum products transported by the Partnership, which are in turn a function of the demand for refined petroleum products in the regions served by the Partnership’s pipelines, and the tariffs or transportation fees charged for such transportation. The Partnership is also engaged, through BPH, BT and BGC, in the terminalling and storage of petroleum products and in contract operations of pipelines for third parties. Revenues for each of the three years in the period ended December 31, 2002 were as follows: Revenues 2002

2001

(in thousands) 2000

Pipeline transportation $214,052 $206,332 $193,845 Terminalling, storage and rentals 18,859 16,353 7,092 Contract operations 14,434 9,712 7,695 Total $247,345 $232,397 $208,632 Results of operations are affected by factors that include general economic conditions, weather, competitive conditions, demand for refined petroleum products, seasonal factors and regulation. See “Business— Competition and Other Business Considerations.” 2002 Compared With 2001 Total revenue for the year ended December 31, 2002 was $247.3 million, $14.9 million or 6.4 percent greater than revenue of $232.4 million in 2001. Revenue from pipeline transportation was $214.1 million in 2002 compared to $206.3 million in 2001. Of the $7.8 million increase in pipeline transportation revenue, $4.3 million is related to a full-year of Norco operations in 2002 compared to five months of Norco operations in 2001. Volumes delivered during 2002 averaged 1,101,400 barrels per day, 11,000 barrels per day or 1.0 percent greater than volume of 1,090,400 barrels per day delivered in 2001. Revenue from the transportation of gasoline of $114.1 million increased by $6.5 million, or 6.0 percent, from 2001 levels. $2.0 million of the increase in gasoline transportation revenue was related to a full-year of Norco operations. Total gasoline volumes of 556,400 barrels per day in 2002 were 15,700 barrels per day, or 2.9 percent greater than 2001 volumes of 540,700 barrels per day. Norco gasoline volumes for a full-year of operations in 2002 were 17,200 barrels per day compared to 16,800 barrels per day for five months of operations in 2001. In the East, gasoline volumes of 245,700 barrels per day were approximately 9,400 barrels per day, or 4.0 percent, greater than 2001 volumes. The increase was primarily due to greater deliveries to the upstate New York and Pittsburgh, Pennsylvania areas. In the Midwest, gasoline volumes of 164,000 barrels per day were 6,900 barrels per day, or 4.0

17

percent, less than gasoline volumes delivered during 2001. Demand for gasoline transportation was generally lower throughout the region with the largest declines occurring in the Detroit and Bay City, Michigan areas. Long Island System gasoline volumes of 111,300 barrels per day were up 5,700 barrels per day, or 5.4% percent, due to additional available capacity on this system following reductions in turbine fuel demand after September 11, 2001. On the Jet Lines System, gasoline volumes of 18,200 barrels per day were 2,700 barrels per day, or 12.8 percent, less than 2001 volumes due to lower transportation demand in the Hartford, Connecticut area. Revenue from the transportation of distillate of $57.7 million increased by $0.4 million, or 0.7 percent, from 2001 levels. Norco’s distillate transportation revenue increased by $1.9 million in 2002 reflecting a full year of operations. Total volumes of 265,400 barrels per day in 2002 were 1,400 barrels per day, or 0.5 percent less than 2001 distillate volumes of 266,800 barrels per day. Norco distillate volumes for a full-year of operations in 2002 were 12,900 barrels per day compared to 12,800 barrels per for five months of operations in 2001. In the East, distillate volumes of 145,000 barrels per day were approximately 5,300 barrels per day, or 3.5 percent, less than 2001 volumes. In the Midwest, distillate volumes of 68,100 barrels per day were 1,200 barrels per day, or 1.8 percent, less than volumes delivered during 2001. Long Island System distillate volumes of 18,400 barrels per day were down 700 barrels per day or 3.9 percent less than volumes delivered during 2001. On the Jet Lines system, distillate volumes of 20,700 barrels per day were 1,800 barrels per day, or 8.1 percent, less than 2001 volumes. Distillate volumes declined during the first quarter of 2002 compared to the first quarter 2001 due to milder than normal winter conditions. During the fourth quarter 2002, distillate volumes increased over fourth quarter 2001 volumes as winter conditions returned to more normal levels. The increase, however, did not fully offset the decline that occurred during the first quarter of the year. Revenue from the transportation of jet fuel of $36.9 million decreased by $0.4 million, or 1.0 percent, from 2001 levels. Norco does not transport turbine fuel. In May, 2001 WesPac commenced turbine fuel deliveries to San Diego airport. WesPac’s turbine fuel revenue was up $0.9 million primarily due to a full-year of deliveries to San Diego Airport during 2002. Total jet fuel volumes of 250,900 barrels per day in 2002 were 9,100 barrels per day, or 3.5 percent less than 2001 jet fuel volumes of 260,000 barrels per day. WesPac’s jet fuel volumes of 11,700 barrels per day were up 3,600 barrels per day due to a full year of deliveries to San Diego Airport. Deliveries to New York City airports declined by 9,100 barrels per day, or 6.6 percent. Deliveries to Pittsburgh Airport declined by 2,100 barrels per day, or 18.0 percent, while deliveries to Miami airport declined 2,900 barrels per day, or 5.4 percent. Volumes to all major airports declined as a result of reduced airline travel following the terrorist attacks on September 11, 2001. Although deliveries to major airports have improved from the dramatic decline immediately following September 11, 2001, the outlook for further recovery of turbine fuel volumes to pre-September 11, 2001 levels is uncertain due to airline schedule reductions, reduced consumer air travel and the threat of further terrorist attacks. Terminalling, storage and rental revenue of $18.9 million increased by $2.5 million in 2002 primarily due to a full year of Norco operations.

Contract operation services revenues of $14.4 million increased by $4.7 million due to additional contracts obtained by BGC during 2002 and 2001. Contract operations revenues typically consist of costs reimbursable under the contracts plus an operator’s fee. Accordingly, revenues from these operations carry a lower gross profit percentage than revenues from pipeline transportation or terminalling, storage and rentals. The Partnership’s costs and expenses for 2002 were $145.0 million compared to $134.1 million for 2001. BGC’s costs and expenses increased by $4.5 million over 2001 as a result of additional contract services provided. A full year of Norco operations resulted in an additional $4.4 million of operating expense. Other increases of $2.0 million are primarily related to general wage increases, increases in payroll overhead costs, increases in the use of outside services, increases in power costs related to additional pipeline volumes and higher insurance premiums. Other income and expense for 2002 was a net cost of $30.5 million compared to $28.9 million in 2001. The increase is primarily due to higher interest expense on additional borrowings during 2002 and 2001 related to acquisitions and certain capital expenditures.

18

2001 Compared With 2000 Total revenue for the year ended December 31, 2001 was $232.4 million, $23.8 million or 11.4 percent greater than revenue of $208.6 million in 2000. Revenue derived from the pipeline transportation of refined products was $206.3 million in 2001 compared to $193.8 million in 2000. Of the $12.5 million increase in pipeline transportation revenue, $2.7 million of the increase was related to the Norco acquisition. Volumes delivered during 2001 averaged 1,090,400 barrels per day, 28,900 barrels per day or 2.7 percent greater than volume of 1,061,500 barrels per day delivered in 2000. The Norco acquisition represented 14,700 barrels per day of the volumes transported in 2001. Revenue from the transportation of gasoline increased by $5.5 million, or 5.4 percent, from 2000 levels, of which $1.2 million was related to the Norco acquisition. In the East, deliveries to the Pittsburgh, Pennsylvania and upstate New York areas increased compared to 2000 volumes due to strong demand there. In the Midwest, volumes and revenue declined compared to 2000 volumes primarily as the result of decreased deliveries to the Bay City, Michigan area. Deliveries to Bay City were unusually high in 2000 following the closure of a refinery in that area. Revenue from the transportation of distillate volumes increased by $3.8 million, or 7.0 percent, over 2000 levels, of which $1.3 million was related to the Norco acquisition. Distillate deliveries for the year were up primarily due to the colder than normal weather experienced during the first and second quarter of 2001. Revenue from the transportation of jet fuel decreased by $0.2 million, or 0.6 percent, from 2000 levels. Norco does not transport turbine fuel. In May, 2001 WesPac commenced turbine fuel deliveries to San Diego airport. This new business added $1.4 million to 2001 revenues. Through September 11, 2001, turbine fuel revenue was approximately 4 percent above prior year levels. However, the terrorist attacks of September 11th greatly curtailed air travel during the balance of September and the fourth quarter of 2001. Turbine fuel deliveries declined by 18 percent overall during the fourth quarter of 2001. Turbine fuel volumes improved in December 2001 as air travel began to recover but was still down by approximately 10 percent overall from December 2000 levels. Deliveries to New York area airports were particularly affected, with a 24 percent decline in October 2000, a 28 percent decline in November 2001 and an 18 percent decline in December 2001 from year earlier volumes. This greater than average decline reflects the larger percentage of international flights at these airports as compared to other jet fuel delivery locations. Revenue from the transportation of liquefied petroleum products (“LPG”) increased by $1.3 million, or 49.3 percent, over 2000 levels. Norco does not transport LPG product. The increase in LPG revenues is related to primarily to new business at Lima, Ohio. Terminalling, storage and rental revenue of $16.4 million increased by $9.3 million in 2001. $3.4 million is due to an increase in terminalling and storage revenue of which $1.9 million is related to the Norco acquisition with the balance primarily resulting from a full year of operations related to the Agway terminal acquisition on June 30, 2000. Rental revenue increased by $5.2 million during 2001 of which $2.1 million is related to the Norco and Agway acquisitions. Contract operation services revenue of $9.7 million increased by $2.0 million due to additional contracts obtained by BGC during 2001 and 2000. Costs and expenses for 2001 were $134.1 million compared to costs and expenses of $117.2 million for 2000. BGC’s costs and expenses increased by $4.4 million over 2000 as result of additional contract services provided. Another $4.4 million of the expense increase is related to the Norco and Agway acquisitions. Other increases of $8.1 million are primarily related to general wage increases, increased payroll overhead costs, an increase in the use of outside services, increased power costs related to additional pipeline deliveries and higher insurance premiums. Other expenses for 2001 were $28.9 million compared to $27.0 million in 2000. A $1.6 million gain realized on the sale of property in 2000 did not recur in 2001. In addition, incentive compensation payments to the General Partner that are based on the level of Partnership distributions were approximately $0.6 million greater during 2001 than 2000 due to an increase in the level of cash distributions paid to limited partners. Investment income increased primarily as the result of a $0.6 million gain on the tendering of preferred stock back to Aerie Networks, Inc.

19