30

BUDGET 2002 Discussion of Tax Proposals TAX POLICY CHIEF DIRECTORATE NATIONAL TREASURY PORTFOLIO AND SELECT COMMITTEES ON FINANCE: CAPE TOWN, 26 FEBRUARY 2002

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | erik-evans |

| View: | 219 times |

| Download: | 0 times |

BUDGET 2002Discussion of Tax Proposals

TAX POLICY CHIEF DIRECTORATE

NATIONAL TREASURY

PORTFOLIO AND SELECT COMMITTEES ON FINANCE:

CAPE TOWN, 26 FEBRUARY 2002

Contents• Tax Policy since 1995 to 2001

• Tax Structure – SA vis-à-vis rest of the world

• 2001 outstanding tax reform measures

• 2002 tax proposals

• Direct tax

• Indirect tax

• 2001/02 outstanding technical corrections

• The way forward :– Retirement fund tax review

– Tax framework for banking sector

Tax policy ’95 – ’01• PIT relief - R34 billion since 1995• 1995 - R2 billion• 1996 - R2 billion• 1997 - R2,8 billion• 1998 - R3,7 billion • 1999 - R4,9 billion• 2000 - R9,9 billion• 2001 - R8,4 billion• 2002 - R15 billion

• Supporting economic activity– 1997: Tax holiday scheme– 1999: Corporate rate reduced to 30%– 2000: Split rate for SMMEs– 2001:

• Strategic investment programme• Immediate expensing of investment by Small Business Corporations

– Diesel fuel rebates: primary sector

Tax policy ’95 – ’01, cont. • Infrastructure development

– 2000: Depreciation of oil and gas pipelines; electricity and telephone transmission lines, railway lines

– 2001: Depreciation of airport infrastructure• Poverty and inequality

– Distribution of PIT relief– Broadening tax base

• Residence-based income tax • Capital gains tax

– Excise duty elimination on soft drinks– VAT zero-rating of IP– Wage subsidy turned into a learnership programme, effective

1 October 2001

TAX STRUCTURE

Tax mix: 1984/85 - 2004/05

0%

20%

40%

60%

80%

100%

Other

Stamp duty

Customs

Adv dom

Fuel

Sp excise

VAT

Trade Taxes

Transfer

SDL

Ret funds

STC

Companies

PIT

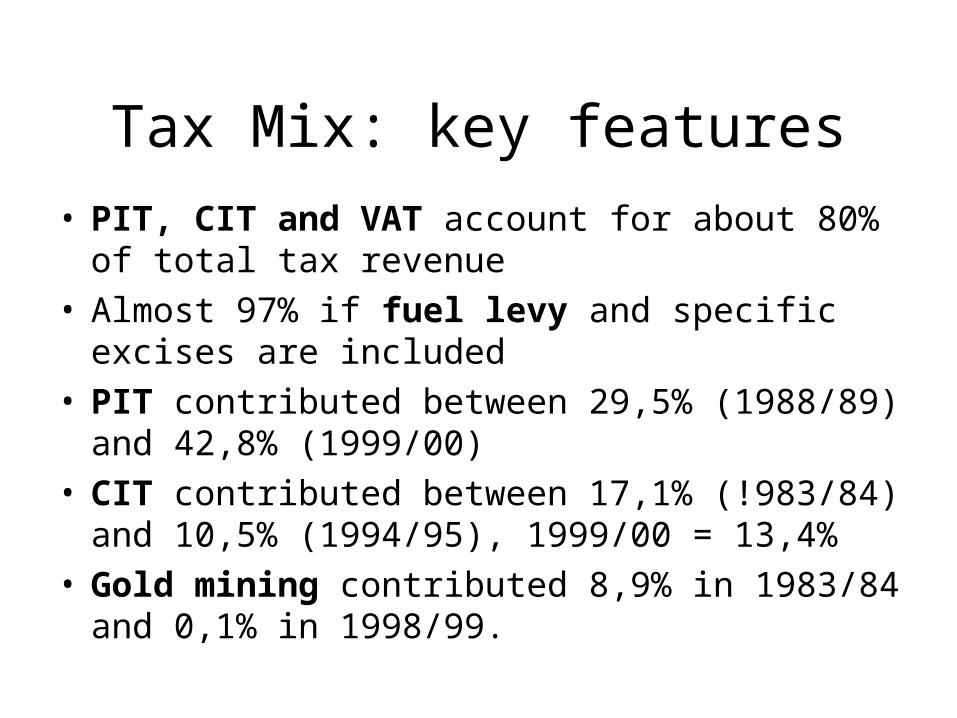

Tax Mix: key features

• PIT, CIT and VAT account for about 80% of total tax revenue

• Almost 97% if fuel levy and specific excises are included

• PIT contributed between 29,5% (1988/89) and 42,8% (1999/00)

• CIT contributed between 17,1% (!983/84) and 10,5% (1994/95), 1999/00 = 13,4%

• Gold mining contributed 8,9% in 1983/84 and 0,1% in 1998/99.

Tax Mix: key features 2

• Fuel levy: currently generate about 7% of total

tax revenue (from 1% in early - mid 1980’s)

• Specific excise taxes: 8,7% in 1983/84 – has

dropped to 4,1% in 2000/01

• Trade taxes: 8,6% in 1988/89 – has dropped to

3,7% in 2000/01

SA’s Tax - GDP ratio

18%

19%

20%

21%

22%

23%

24%

25%

26%

PRELIMINARY OUTCOME&

FISCAL FRAMEWORK

2000/01 preliminary outcome

• Headline trends:

– PIT income up by R878 million– Corp tax up by R14 billion– STC up by R2,5 billion– VAT revenue shortfall of R1,75 billion

Summary of proposals2002/03

Effect of RevenueR million Tax proposals

Revenue

Estimate of revenue before tax proposals 280,382

Tax proposals

Direct tax proposals -15,824

Personal income tax: -14,855 Adjust personal income tax rate structure -15,000 Administrative changes -50 Adjustments to deductions 105 Taxation of trusts at a flat rate of 40 per cent 90

Corporate income tax: -335 Accelerated depreciation allowances -295 Extend small business corporations tax relief -40

Financial transaction taxes: -430 Exempt certain warrant repurchases from MST and UST -80 Remove stamp duties on certain financial instruments -35 Withdraw levy on Lloyd's insurance premiums -15 Adjust transfer duty rate structure -300

Increase monetary thresholds: -204

Indirect tax proposals 659

Specific excise taxes: Net Impact 663 - Increase in duties on alcoholic beverages 355 - Increase in excise duties on tobacco products (50% incidence) 443 - Remove duties on soft drinks (-6c/l) -135

Extend fuel rebate for offshore vessels -4

Estimate of revenue after tax proposals 265,217

DIRECT TAX MEASURES

2002 key features - individuals

• R15 billion PIT relief

• Interest and dividend income exemption

• Transfer duty – R300 million

• Taxation of deemed foreign income

• Taxation of trusts

• Amendment of monetary thresholds and

miscellaneous PIT provisions

2002 key features - corporations

• Accelerated depreciation for new manufacturing assets

• Tax relief for small business

• Taxation of trusts – flat 40% rate

• Further tax reform:– Taxation of retirement industry

– Taxation of banking sector

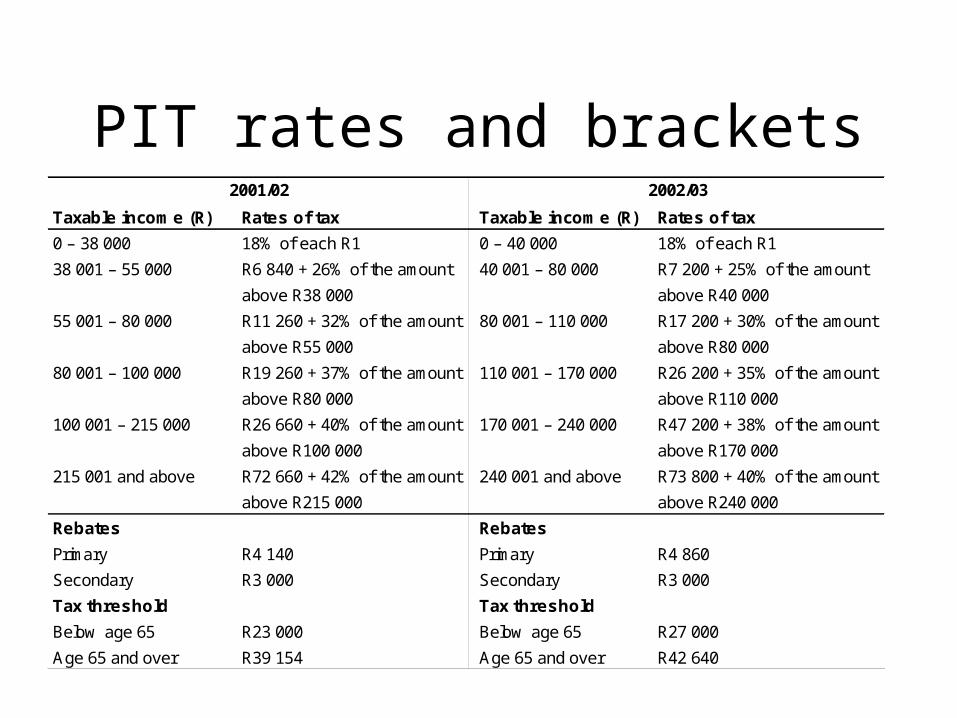

PIT rates and bracketsTaxable income (R) Rates of tax Taxable income (R) Rates of tax

0 – 38 000 18% of each R1 0 – 40 000 18% of each R1

38 001 – 55 000 R6 840 + 26% of the amount 40 001 – 80 000 R7 200 + 25% of the amount

above R38 000 above R40 000

55 001 – 80 000 R11 260 + 32% of the amount 80 001 – 110 000 R17 200 + 30% of the amount

above R55 000 above R80 000

80 001 – 100 000 R19 260 + 37% of the amount 110 001 – 170 000 R26 200 + 35% of the amount

above R80 000 above R110 000

100 001 – 215 000 R26 660 + 40% of the amount 170 001 – 240 000 R47 200 + 38% of the amount

above R100 000 above R170 000

215 001 and above R72 660 + 42% of the amount 240 001 and above R73 800 + 40% of the amount

above R215 000 above R240 000

Rebates Rebates

Primary R4 140 Primary R4 860

Secondary R3 000 Secondary R3 000

Tax threshold Tax threshold

Below age 65 R23 000 Below age 65 R27 000

Age 65 and over R39 154 Age 65 and over R42 640

2001/02 2002/03

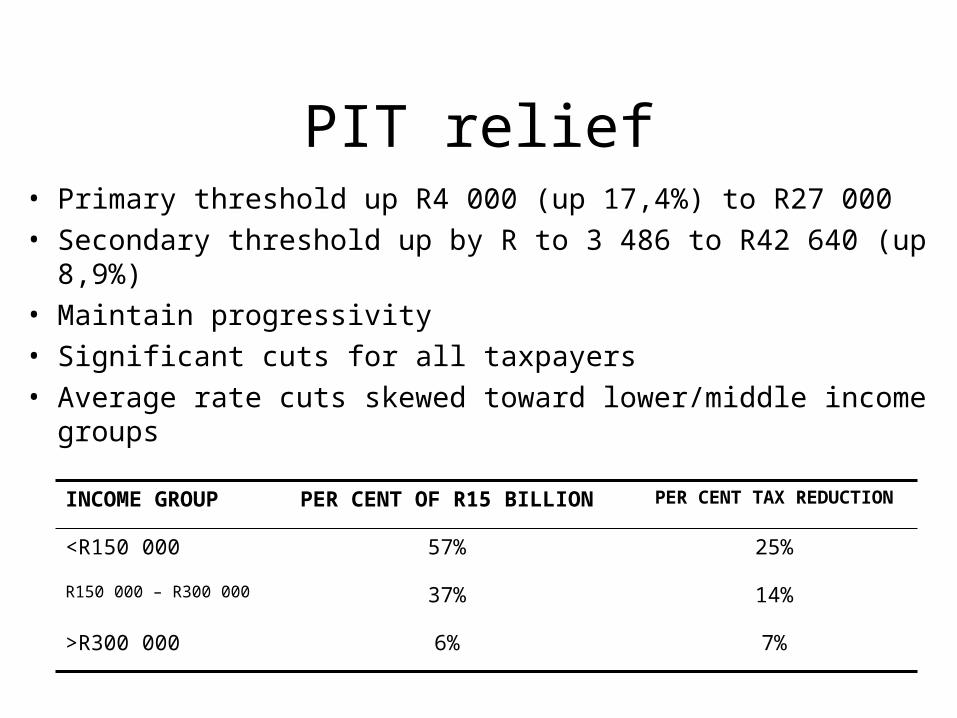

PIT relief• Primary threshold up R4 000 (up 17,4%) to R27 000

• Secondary threshold up by R to 3 486 to R42 640 (up 8,9%)

• Maintain progressivity

• Significant cuts for all taxpayers

• Average rate cuts skewed toward lower/middle income groups

7%6%>R300 000

14%37%R150 000 – R300 000

25%57%<R150 000

PER CENT TAX REDUCTIONPER CENT OF R15 BILLIONINCOME GROUP

Transfer duty relief

• R300 million relief

• Rates cut at all property values

Proposed rates:

• R0 – R100 000 …… 0%

• R100 001 – R300 000 …… 5%

• R300 001 and above …. 8%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Ave

rage

rat

e

50 250

450

650

850

1,25

0

Property value (R 000)

Old rates

New rates

Other individual tax changes

• Domestic interest and dividend income exemption raised

– R6 000 under 65

– R10 000, age 65 and over

– R1 000 limit on exemption of foreign source income

• Monetary thresholds:

– Bravery and long service awards

– Donations tax up to R30 000 & estate duty up to R1,5 million

– Bursaries and scholarships

– Medical aid deductions

Other individual changes 2• Limit employee deductions

– Business travel deduction against car allowance– Certain medical expenses– Contributions to pension and retirement annuity funds– Donations to certain public benefit organisations– Specific expenditure against allowances of holders of public office– Wear and tear allowances on equipment.

• Taxation of deemed foreign income• Eliminate deemed accommodation costs in subsistence

allowance• Occasional free services – R500 fringe benefit• Administrative reforms

– Single year for all taxpayers– Raising provisional threshold limits– Reviewing SITE

Company tax changes 1• Accelerated depreciation – 3 years

– 40% of cost in year 1– 20% a year for subsequent 3 years

• Focus on building manufacturing base• Stimulate investment and create jobs• Small business tax relief:

– 15% tax on first R150 000 of taxable income– Limit on small business corporation turnover raised to R3 million– Reduce administrative burden

• Immediate expensing:– Manufacturing assets – cost R2 000– Intellectural property – cost R5 000

• Trusts: 40% tax rate

Ongoing tax reform• Taxation of banking sector

– Announced in 2001 Budget

– Questionnaire highlights sources of reduced tax rates

– Better enforcement and compliance – R792 million

– Further review in 2002/03:

• Taxation of financial derivative instruments

• Taxation of financial leases

• Taxation of retirement industry

– Holistic review during 2002

– Issues paper to be tabled for discussion shortly

INDIRECT TAX MEASURES

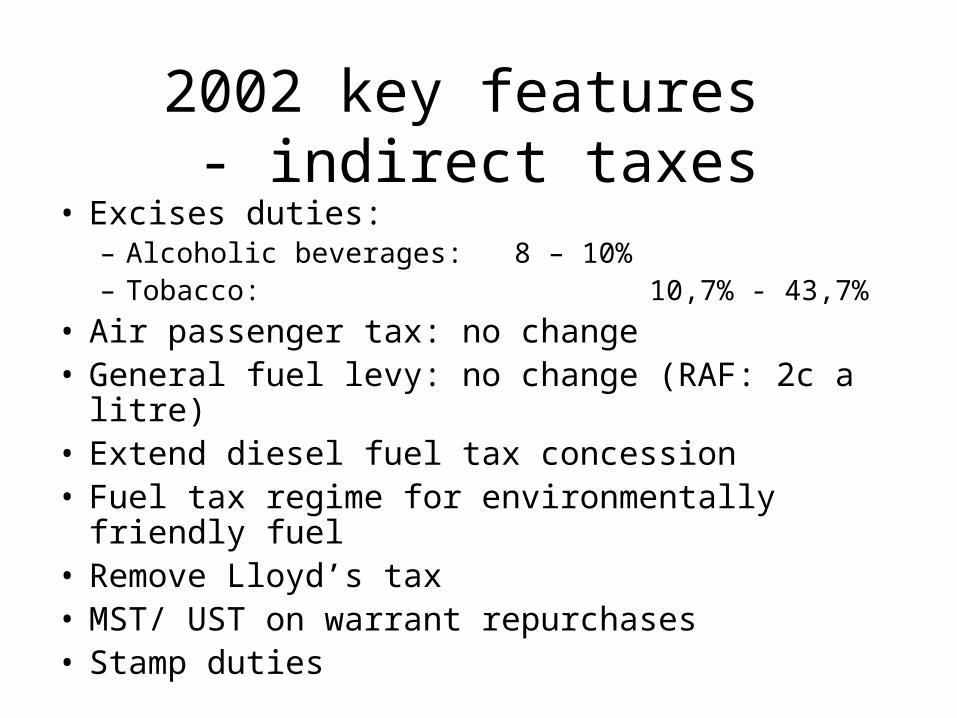

2002 key features - indirect taxes

• Excises duties: – Alcoholic beverages: 8 – 10%– Tobacco: 10,7% - 43,7%

• Air passenger tax: no change• General fuel levy: no change (RAF: 2c a litre)• Extend diesel fuel tax concession• Fuel tax regime for environmentally friendly fuel• Remove Lloyd’s tax• MST/ UST on warrant repurchases• Stamp duties

FUEL LEVY

• No increase in General Fuel Levy• Intended to help limit inflationary impact of

significant devaluation of Rand during December 2001

• Road Accident Fund Levy to be increased by 2 cents per litre

• Renewable, environmentally friendly diesel fuel (e.g. Biodiesel ) to be taxed at 70% of General Fuel Levy

• In addition, such diesel fuels (e.g. Biodiesel) used in certain primary production processes will qualify for diesel fuel levy concession

TOBACCO PRODUCTS

• 50.0 per cent total tax incidence (Excise + VAT) to be maintained

• Average increase of 12.% ( Cigarettes at 10.7%)

Other charges and levies

• Remove Lloyd’s insurance premium levy

• MST and UST on warrants:– Warrants are retail derivative instruments

– Account for 20% of JSE trades

– To ensure equity, remove MST/UST on repurchase of warrants issued by market maker

• Stamp duties, remove:– Listed debt instruments (UST as well)

– Cession of mortgage bonds

– Insurance policies against accident, bodily injury, incapacity or sickness

– Insurance contracts referred to in the Export Credit and Foreign Investments Reinsurance Act, 1957

– Cession of insurance policies.

TECHNICAL CORRECTIONS ON CGT & RESIDENCE-BASED

INCOME TAX

Technical corrections: CGT and residence-based IT

• No relief for financial instrument companies

• Trade debts in financial instrument definition

• Designated country exception – review of list

• Foreign asset reporting – deemed inclusion

• Foreign currency regulations – individuals

• Outbound restructurings

– STC technical correction on liquidation

– Unbundling – 5% rule

• Interpretative guideline

Key Tax Proposals

• R15 billion PIT relief• Major interest income exemption• Accelerated depreciation for manufacturing• SMMEs threshold adjustments• Transfer duty relief of R300 million• No general fuel levy increase• Discounted general fuel levy on biodiesel• Reduction of financial transaction taxes