37

BUDGETARY OVERVIEW OF 2007-2008 BUDGET DEVELOPMENT April 10, 2007 Board of Education Meeting

| Date post: | 31-Dec-2015 |

| Category: |

Documents |

| Upload: | darrell-gabriel-ross |

| View: | 217 times |

| Download: | 0 times |

BUDGETARY OVERVIEW OF 2007-2008 BUDGET

DEVELOPMENT

April 10, 2007Board of Education Meeting

2007-2008 SCHOOL BUDGETSignificant Budgetary Considerations

1. Impact of Tax Certiorari Claims/Settlements

2. Changes in Assessed Valuation3. Transportation

1. BOCES and purchase of replacement buses, or Bid for new service

4. Incarcerated Youth1. Increase in allocation/increase in

resulting state aid

2007-2008 SCHOOL BUDGETSignificant Budgetary Considerations5. Health Insurance Increases6. Salary Increases7. Retirement Cost Increases8. Workers Compensation/Liability

Insurance Cost Increases9. High School Tuition Increases

2007-2008 March 6, Draft # 1 Budget$22,284,194

The Initial Draft Budget provides for: Budget to Budget Increase of 9.28% Projected Tax Rate Increase:

With Assessment Changes:Greenburgh 18.72%

Mt. Pleasant 18.20% Without Assessment Changes:

Greenburgh 7.50%

Mt. Pleasant 7.03%

2007-2008 March 12 Draft # 2 Budget$21,830,565

Draft # 2 Budget dated March 12, 2007 provides for: Budget to Budget Increase of 7.05% Projected Tax Rate Increase:

With Assessment Changes:Greenburgh

16.34%

Mt. Pleasant15.83%

Without Assessment Changes:Greenburgh

5.35%

Mt. Pleasant4.88%

2007-2008 March 12 Draft # 3 Budget$22,041,265

Draft # 3 Budget Dated March 12 2007 Provides for: Budget to Budget Increase of 8.09% Projected Tax Rate Increase:

With Assessment Changes:

Greenburgh 17.09%

Mt. Pleasant 16.57% Without Assessment Changes:

Greenburgh 6.02%

Mt. Pleasant 5.55%

March 26, 2007 Possible Budget Deletions From Draft # 3

A1010-BOARD OF EDUCATION Page 2

400-CONTRACTUAL EXPENSES $ 4,150

450-Supplies & Materials $ 2,000 $6,150

A1040-District Clerk Page 2

400-Contractual Expenses $ 8,000$8,000

A1240 – SUPERINTENDENT Page 3

400-Contractual Expenses $ 1,200

450-Supplies & Materials $ 1,900 $3,100

March 26, 2007 Possible Budget Deletions From Draft # 3

A1310-Business Administration Page 4

160-Non Instructional Salaries $ 7,500

450-Materials & Supplies $ 1,500

490-BOCES Service $ 2,500$11,500$11,500

A 1325-Treasurer Page 5

160 Non-Instructional Salary $ 5,000 $ 5,000

A1380-Fiscal Agent $ 650 $ 650

March 26, 2007 Possible Budget Deletions From Draft # 3

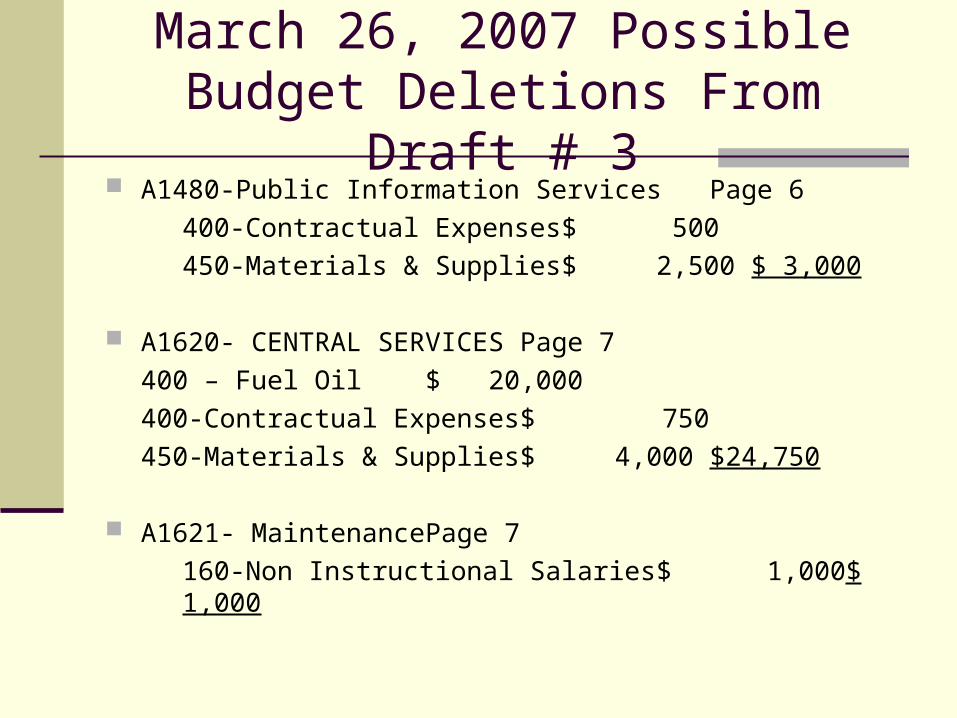

A1480-Public Information Services Page 6

400-Contractual Expenses $ 500

450-Materials & Supplies $ 2,500 $ 3,000

A1620- CENTRAL SERVICES Page 7

400 – Fuel Oil $ 20,000

400-Contractual Expenses $ 750

450-Materials & Supplies $ 4,000 $24,750

A1621- Maintenance Page 7

160-Non Instructional Salaries $ 1,000 $ 1,000

March 26, 2007 Possible Budget Deletions From Draft # 3

A2020-INSTRUCTIONAL SUPERVISION Page 10

160 - Non Instructional Salaries $ 2,500

400- Contractual $ 2,000 $ 4,500

A2110 – TEACHING REGULAR SCHOOL Page 10

120-Teacher Salary 1-5 $ 90,000

160-Non Instructional Salaries $ 19,110

200-Equipment $ 5,500

400-Contractual $ 2,000

450-Materials & Supplies $ 7,831

480-Textbooks $ 35,210 $ 159,651

March 26, 2007 Possible Budget Deletions From Draft # 3

A2250- STUDENTS WITH DISABILITES Page 11

160-Teacher Aide $ 19,110

200-Equipment $ 1,000$20,110

A2610-SCHOOL LIBRARY & AV Page 12

450-Materials & Supplies $ 16,125

A2630-Computer Assisted Instruction

490-BOCES SERVICES $ 12,506$28,631

March 26, 2007 Possible Budget Deletions From Draft # 3

A2855-INTERSCHOLASTIC ATHLETICS Page 13160-Non Instructional Salaries $ 5,000 $ 5,000

A8070-CENSUS Page 15400-Contractual $ 15,000460-Software $ 2,048490-BOCES Services $ 5,940 $22,988

TOTAL $316,6552007-2008 Draft 3 $22,041,2652007-2008 Draft 4 $21,724,610 Difference $ 316,655

March 26, 2007 Possible Budget Deletions From Draft # 3

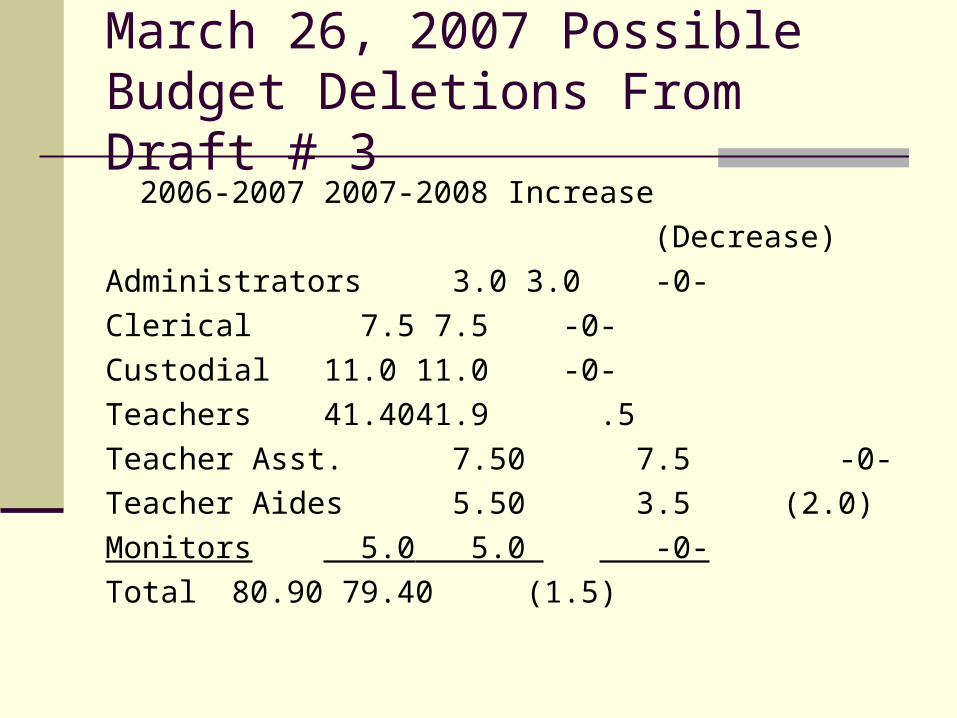

2006-2007 2007-2008 Increase

(Decrease)

Administrators 3.0 3.0 -0-

Clerical 7.5 7.5 -0-

Custodial 11.0 11.0 -0-

Teachers 41.40 41.9 .5

Teacher Asst. 7.50 7.5 -0-

Teacher Aides 5.50 3.5 (2.0)

Monitors 5.0 5.0 -0-

Total 80.90 79.40 (1.5)

2007-2008 Draft #4 BudgetHighlights of The Budget Partial Playground Replacement $ 8,000 Tractor Replacements $ 43,270 Social Worker Salary/Benefits $ 50,000 Instructional Supplies & Materials $ 100,074 Replacement of 2 large buses $ 50,000 Interscholastic Program $ 45,398 Summer Camp $ 260,688 Swim Program $161,754 After School Program $ 52,948

2007-2008 March 6, Draft # 4 Budget$21,724,610

The Draft 4 Budget provides for: Budget to Budget Increase of 6.53% Projected Tax Rate Increase:

With Assessment Changes:Greenburgh 15.02%

Mt. Pleasant 14.51% Without Assessment Changes:

Greenburgh 4.09%

Mt. Pleasant 3.63%

Summary of Draft 4 Budgetary Increases/ (Decreases)

Salaries $ 368,424 Equipment $ ( 1,014) Contractual $ 7,534 Supplies $ ( 29,461) Tuition $ 677,658 Textbooks $ (43,313) BOCES $ 129,933 Incarcerated Youth $ 437,424 Benefits $ 186,536 Debt Service $ 48,866 Capital Projects $ (450,000)

Total $ 1,332,587

Tax Rate Comparison 2006-2007 Tax Rates

School True Value Taxes onDistrict Tax Rate $500,000 Index

1 19.08 $9,540 2.6910 15.75 $7,875 2.2220 14.64 $7,320 2.0630 12.46 $6,230 1.7540 10.56 $5,280 1.4945 8.78 $4,390 1.24

Pocantico 7.10 $3,550 1.00

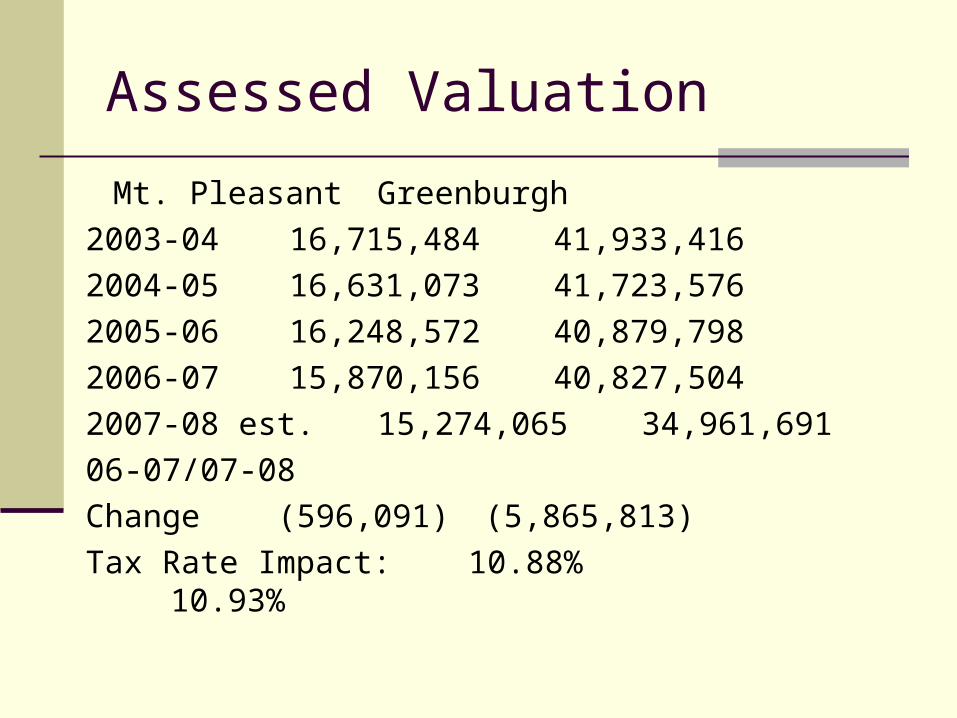

Assessed Valuation

Mt. Pleasant Greenburgh

2003-04 16,715,484 41,933,416

2004-05 16,631,073 41,723,576

2005-06 16,248,572 40,879,798

2006-07 15,870,156 40,827,504

2007-08 est. 15,274,065 34,961,691

06-07/07-08

Change (596,091) (5,865,813)

Tax Rate Impact: 10.88% 10.93%

Assessed Valuation Mt. PleasantBefore Changes Affecting 2007-2008

Mt Pleasant

15,200,000

15,400,000

15,600,000

15,800,00016,000,000

16,200,000

16,400,000

16,600,000

16,800,000

2003-04 2004-05 2005-2006

2006-2007

2007-2008

Mt Pleasant

Assessed Valuation Mt. PleasantAfter Tax Certiorari Claim Settlements

Decrease of $596,091

Mt Pleasant

14,500,000

15,000,000

15,500,000

16,000,000

16,500,000

17,000,000

2003-04 2004-05 2005-2006

2006-2007

2007-2008

Mt Pleasant

Assessed Valuation – Greenburgh Before Changes Affecting 2007-2008

Greenburgh

39,000,000

39,500,000

40,000,000

40,500,000

41,000,000

41,500,000

42,000,000

42,500,000

2003-04 2004-05 2005-2006

2006-2007

2007-2008

Greenburgh

Assessed Valuation – GreenburghAfter Tax Certiorari Claim Settlements

Decrease of $5,825,813

Greenburgh

30,000,000

32,000,000

34,000,000

36,000,000

38,000,000

40,000,000

42,000,000

44,000,000

2003-04 2004-05 2005-2006

2006-2007

2007-2008

Greenburgh

Questions/Comments Received Since March 26, 2007

1. Since the newsletter has already been designed and formatted for some time, have someone in-house layout the information or get a price from the printer to continue the same. This is how the newsletter at the Katonah Museum is done.

2. Allow the custodians to make routine repairs around the school, rather than hiring consultants and only use outside companies when they can’t.

Questions/Comments Received Since March 26, 2007

1. Add some tuition paying students during the school year. One per each grade year would make a difference. Actively advertise the camp for tuition paying students so the cost of the camp is a wash.

2. When appropriate, hire new staff at lower salaries than retiring staff.

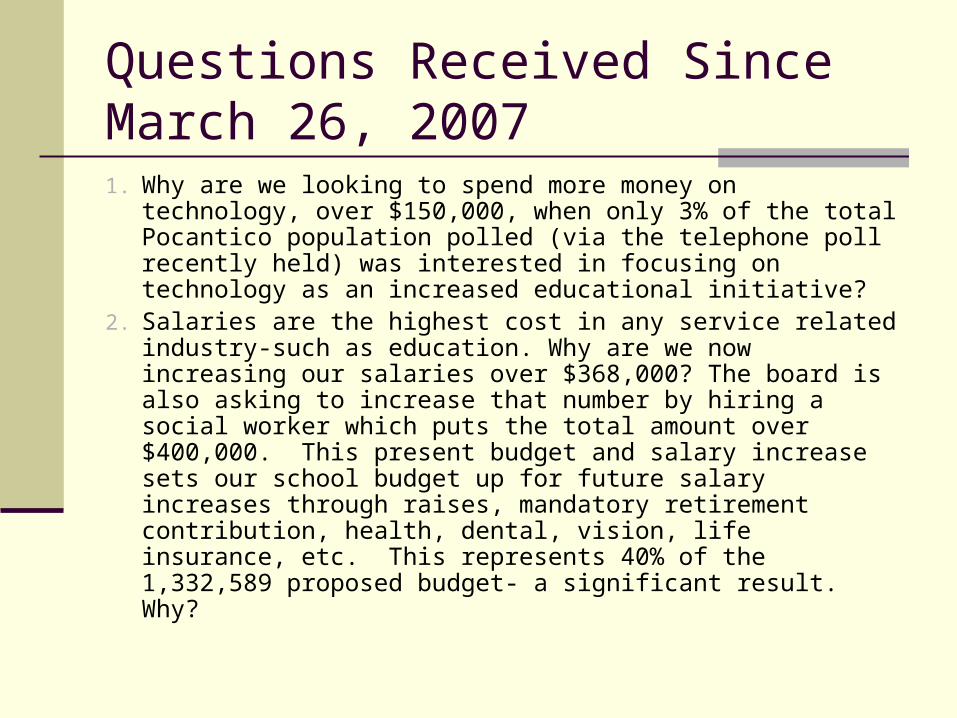

Questions Received Since March 26, 20071. Why are we looking to spend more money on technology, over

$150,000, when only 3% of the total Pocantico population polled (via the telephone poll recently held) was interested in focusing on technology as an increased educational initiative?

2. Salaries are the highest cost in any service related industry-such as education. Why are we now increasing our salaries over $368,000? The board is also asking to increase that number by hiring a social worker which puts the total amount over $400,000. This present budget and salary increase sets our school budget up for future salary increases through raises, mandatory retirement contribution, health, dental, vision, life insurance, etc. This represents 40% of the 1,332,589 proposed budget- a significant result. Why?

Questions Received Since March 26, 20071. Health benefits are escalating in every industry which in turn, is

requiring the individuals to incur a higher percentage responsibility. Benefits are projected at $186,536 for the proposed budget. What can we do to help control our costs for benefits?

2. 2610-school library- why are we asking for a proposed salary of $107,725 when the past librarian who is now retiring was making $104,513?

3. 1620-operations and maintenance-160-non-instr salaries-why are we looking for more than $75,000 in overtime/part time?

4. 5510-district related transportation-you are asking us to approve a budget over 45,000 in overtime. Why are we spending so much money on overtime and why are we projecting such a huge increase in future overtime?

Questions Received Since March 26, 2007

1. What are the 9th and 10th period costs, and are there other options?

2. What is the minimum that the District can budget for the IPA to maintain the effort to date?

3. How much has overtime for non-instructional staff increased in the draft 2007-2008 budget?

Questions Received Since March 26, 2007

1. How much money would we save if the 9th and 10th periods were eliminated?

2. What classes does this impact?

3. How many students would this impact?

Contingency Budgets

Single revote: Upon the defeat of the original proposed school budget, a district may resubmit the original budget, submit a revised budget, or adopt a contingency budget. If the voters fail to approve the budget upon the second vote, the district must adopt a contingency budget. Expanded definition: Interscholastic athletics, field trips, other extracurricular activities, and related transportation expenses are contingent expenses.

Contingency Budgets

Administrative cap: The administrative component of a contingency budget will be limited to the lesser of: 1) the percentage of the administrative component in the prior year’s budget or 2) the percentage of the administrative component in the last defeated proposed budget. Cap on total spending: Total spending under a contingency budget may not increase by more than 120 % of national CPI or 4.00%, whichever is lower. For 2007-08 the cap is 3.84 %.

2007-2008 Contingency Budget

How the contingency/austerity budget cap is calculated:

2006-2007 Adopted Budget $19,916,971 Less Debt Service $

( 489,309) Adjusted Base Year Budget $19,427,662

2007-2008 Contingency Budget

How the maximum contingency/austerity budget cap is calculated:

Adjusted Base Year Budget $19,427,662 Adjusted Budget x 120% of CPI 3.84%

$20,173,684 Debt Service $ 538,175 Growth Related Expenditures $ 726,925 Maximum Contingency Budget $21,438,784 Required Budgetary Cuts $ 285,826 Projected Tax Rate Increase:

Greenburgh: 15.98%Mt. Pleasant: 15.47%

Tax Rate Impact 2007-2008 Draft 4 Budget

GreenburghA/V 2007-08 2007-08 ContingencyDifference

Annual Tax Tax Increase Tax Increase

Annual Monthly 1,000 $250 $ 33 $ 3 $ 35 ( $ 2) 5,000 $1,087 $ 163 $ 14 $174 ( $10) 10,000 $2,523 $ 327 $ 27 $382 ( $20) 14,000 $3,532 $ 457 $ 38 $ 487 ( $29) 17,000 $4,253 $ 556 $ 46 $ 591 ( $35) 20,000 $5,004 $ 654 $ 54 $695 ( $42)

Note: Contingency Budget does not contain revenue producing programs such as summer camp and swim program.

Tax Rate Impact 2007-2008 Draft 4 Budget

Mt. PleasantA/V 2007-08 2007-08 ContingencyDifference

Annual Tax Tax Increase Tax Increase

Annual Monthly 1,000 $ 545 $ 69 $ 6 $ 74 ( $ 5) 5,000 $ 2,726 $ 345 $ 29 $ 368 ( $23) 10,000 $ 5,451 $ 691 $ 58 $ 736 ( $45) 14,000 $ 7,632 $ 967 $ 81 $1,031 ( $64) 17,000 $ 9,267 $1,174 $ 98 $1,252 ( $77) 20,000 $10,902 $1,382 $115 $1,473 ( $91)

Note: Contingency Budget does not contain revenue producing programs such as summer camp and swim program.

Possible Areas of Expense Reduction

Summer Camp/Swim Program Student Supplies Community Use of Buildings and Grounds Certain Equipment Software Staff Technology Overtime Field Trips

Tax Rate Table

BUDGET AMOUNT IMPACT ON TAX RATE$ 100,000 .68%

$ 150,000 1.00%

$ 250,000 1.69%

$ 500,000 3.37%

$ 750,000 5.05%

$ 1,000,000 6.74%

BUDGETARY OVERVIEW OF 2007-2008 BUDGET DEVELOPMENT