Page 1

1Sotogrande 15 May [email protected]

Bunkering in the Straits Bunkering in the Straits

Bunker Summit 2009Bunker Summit 2009Mediterranean and Black SeaMediterranean and Black Sea

Sotogrande Sotogrande 15 May 200915 May 2009

Robin MeechRobin Meech

Marine and Energy Consulting LimitedMarine and Energy Consulting Limited

Page 2

2Sotogrande 15 May [email protected]

5 Miles

TangiersMed

Straits of Gibraltar bunker market

Page 3

3Sotogrande 15 May [email protected]

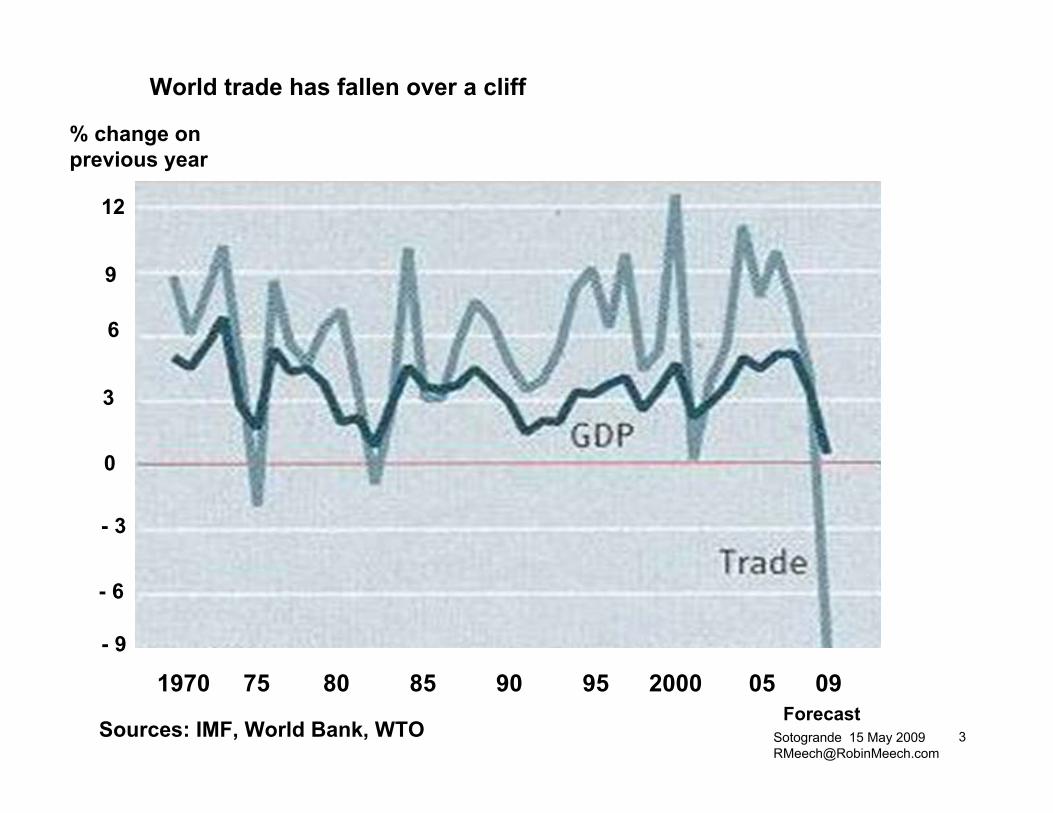

World trade has fallen over a cliff

Sources: IMF, World Bank, WTO

% change on previous year

12

9

6

3

0

- 3

- 6

- 9

1970 75 80 85 90 95 2000 05 09Forecast

Page 4

4Sotogrande 15 May [email protected]

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2012 2023 2024 2025

Global Cap 4.5%Baltic and North Sea

SOx ECA 1.5%

All SECA 1.0% S

Jul

All SECA 0.1% SJan

Global Cap0.5% SJan

Global Cap3.5% SJan

Review

Global Cap0.5% S

Jan

Likely delay

1 3

42

Reducing the sulphur content of fuels will increase costs more than any other single factor

Annex VI incorporatesfour key steps

20101.5% S $3351.0% S $390Diff $55

20151.0% S $6700.1% S $970Diff $300

20203.5% S $7100.5% S $1,180Diff $470

Not changing significantly

Page 5

5Sotogrande 15 May [email protected]

Global bunker Demand with the introduction of 0.5% sulphur cap between 2020 and 2025 (million tons)

0

50

100

150

200

250

300

350

400

450

500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Residual Max 1.5% Residual Max 1.0% Residual Max 4.5% Residual max 3.5%Distillate Max 0.1% Distillate 0.1 to 0.5% Distillate - Other

Page 6

6Sotogrande 15 May [email protected]

REST OF ASIA

0

20

40

60

SINGAPORE

0

20

40

60

Global demand of all types of bunkers

0

10

20

30

40

2008 2015 2020

SOUTH AMERICA

010203040

MIDDLE EAST

0

20

40

60

NORTH ASIA

0

20

40

60

EUROPE

020406080

AFRICA

0

10

20

30

Mediterranean

0

20

40

60

Million tons

Page 7

7Sotogrande 15 May [email protected]

Demand for residual bunkers in the East and West

7

WEST EAST

Milli

on to

ns

Page 8

8Sotogrande 15 May [email protected]

Mediterranean market will recover to 2008 levels by 2012

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

1.5% Residual 1.0% Residual 4.5% Residual 3.5% Residual Distillates

But overall growth will stall thereafter

Page 9

9Sotogrande 15 May [email protected]

0

200

400

600

800

1,000

1,200

1,400

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

HSBFO 1.5% S 1.0% S 0.1% S 0.5% S Other Diesel

Average prices for main engine fuels will rise above $1200/ton

$/ton

Page 10

10Sotogrande 15 May [email protected]

However, the market value in the Mediterranean will increase four fold

0

5

10

15

20

25

30

35

40

45

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Demand million tons Value $ billion

Page 11

11Sotogrande 15 May [email protected]

St. of Gibraltar 6.9 mill tons

Northern Med12.8 mill tons

Black Sea5.2 mill tons

Eastern & Suez8.5 mill tonsNorth Africa

1.8 mill tons

The Straits of Gibraltar bunker market is 20% of the region

Page 12

12Sotogrande 15 May [email protected]

20%

AlgecirasRefinery

30%

5%

20%15%

Other10%

Fuel suppliers into western Mediterranean / Straits of Gibraltar Market

LowSulphurproduct

Page 13

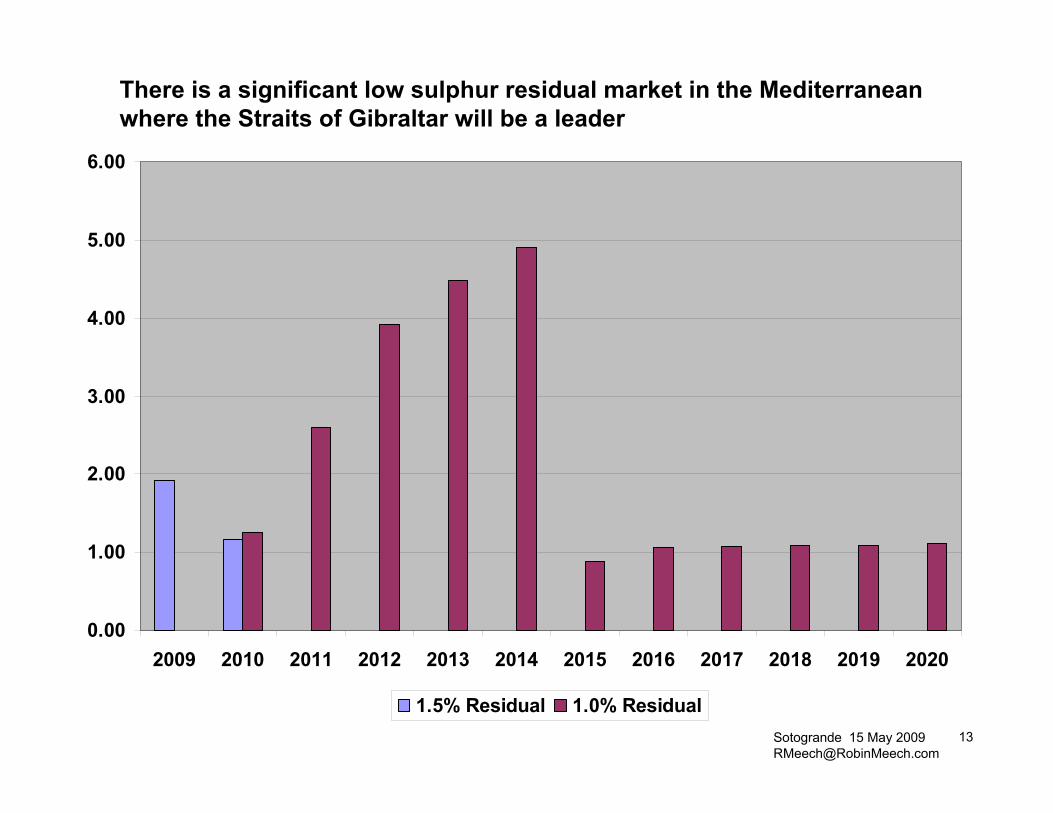

13Sotogrande 15 May [email protected]

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

1.5% Residual 1.0% Residual

There is a significant low sulphur residual market in the Mediterranean where the Straits of Gibraltar will be a leader

Page 14

14Sotogrande 15 May [email protected]

It is extremely unlikely that there will be an ECA in the Mediterraneanfor over a decade

• Can not be justified economically/technically

• Not an equal desire by the 25 countries bordering the Mediterranean

• North African countries will benefit from SOx deposition

• Enforcement would be intermittent – difficult with transit traffic

• There isn’t enough suitable product available

• Little political cohesion

Page 15

15Sotogrande 15 May [email protected]

GibraltarBunkerAnchorages

GibraltarHabour

Port of Algeciras

CepsaRefinery

AlgecirasBunkerAnchorages

EastAnchorages

Bay of Gibraltar

Page 16

16Sotogrande 15 May [email protected]

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

GibraltarCeutaAlgeciras

Gibraltar has maintained a 60% market share over the past decadewith demand growing faster than the global average

Page 17

17Sotogrande 15 May [email protected]

Sales by company in Gibraltar (million tons)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

2005 2006 2007 2008

Bunkers GibGIBUNCOFAMMAegeanVemaoilShell - Gib

Page 18

18Sotogrande 15 May [email protected]

Tanker Name Operator Age DWTLeader Aegean 23 83,890Europa Venture Bunkers Gibraltar 23 76,000Vemabaltic Vemaoil 22 107,544

267434

• Until 2006 the MoD Kings Lines, underground 250,000 cub of tankage augmented the floating storage

- Requires renovation- Could offer lower costs than floating storage

• Into ship deliveries are performed by a fleet of some 15 barges

• There are 11 bunkering anchorages, three of which are occupied bythe floating storage vessels

• This lack of anchorages inhibits further market growth

• Growing competition could further reduce sales

Gibraltar will need to compete even more rigorously if it is to maintainIts current market position

Page 19

19Sotogrande 15 May [email protected]

Kings Lines

Existing hydrants

Gibraltar

North Mole

South Mole

MOD hydrants – not available for commercial use

Detached Mole

BUNKER ANCHORAGES

EASTERN ANCHORAGES

Page 20

20Sotogrande 15 May [email protected]

Route for underwater lines2 x 14” and 1 x 10”About 300 metres

Requirement for 4 or 6 hydrant pointsand tanker berth

Or dredge to permit floating storage tomoor alongside

Marine Option 1 – Detached Mole hydrants

Extension Jetty

Page 21

21Sotogrande 15 May [email protected]

Requirement for 4 or 6 hydrant pointsand tanker berth

Marine Option 2 – Perpendicular mole

Page 22

22Sotogrande 15 May [email protected]

Requirement for 4 or 6 hydrant pointsand tanker berth

Marine Option 3 – Reclaimed land

400,000 cub tankage

Page 23

23Sotogrande 15 May [email protected]

• There has been pressure to curtail floating storage for environmental reasons but these are unfounded

• Replacing the floating storage with land based tankage or mooring the storage tankers along side the Detached Mole will increase potential throughput by some 30% to over 600,000 tpa

• Increasing the capacity is no guarantee that Gibraltar will grow its market

• Permitting bunkering in the Eastern Anchorages is very unlikely for some time even with the new VTS

• The bunker sector is economically as valuable to the Gibraltar economyas the cruise business and it can be expected that the Government will support the important bunker sector

• If Aegean move to Tanger Med it is unlikely they will retain floating storage in Gibraltar and nobody will replace them the capacity by 30%

Gibraltar future

Page 24

24Sotogrande 15 May [email protected]

Algeciras has growing potential

• Supplies have grown by 7 % pa over the past five years amounting to 35% of the Straits of Gibraltar bunker market

• Dominated by Cepsa and Repsol but about to change

• The new Alpetrol terminal - Will come on stream in 2011/2- Developed by Vilma and Novaro- Have a capacity of 300,000 cub in 29 tanks - Significant capacity dedicated to bunkers- With be capable of supplying over 2 million tons pa- Can accommodating Suezmax tankers- Low cargo import costs

• CLH upgrading its terminal- Doubling capacity to 140,000 cub- Draft of 14,5 m

• There are five bunker barges operating in the port

Page 25

25Sotogrande 15 May [email protected]

There are further ways in which the port might extend it bunker market

• Eventually introduce more barges

• Optimising anchorage management

• Introduction of more players increasing competition

• Although currently over 60% of stems are delivered in the anchoragesthe port will need to maintain cargo traffic growth to further developthe bunker business

Page 26

26Sotogrande 15 May [email protected]

Ceuta is a well established bunker centre but with restricted capacity

• Petrolifera Ducar, S.A operate two facilities of - 55,000 cub fuel oil- 28,500 cub gas oil

• The facilities in need of some upgrading

• In 1993 some 750,000 tons bunkers delivered but activity athalf this level recently

• Restricted space for additional expansion although plans existing for a 1.0 million cub terminal

• Capable of accommodating 40,000 dwt tankers

• Potential for growth is limited

Page 27

27Sotogrande 15 May [email protected]

Oil Terminal

Jetty

Tangier Med I:• Maersk (containers) operational since 2007.• Eurogate consortium operational 2010• Car Export Facility to be operational 2015Tangier Med II:• Operational end 2014• Bulk terminal

Tanger Med rapidly developing

Page 28

28Sotogrande 15 May [email protected]

A new tank terminal is under construction

• Capacity 500,000 cub in 17 tanks

• Due for commissioning in 2011

• Some 60% dedicated to bunkering

• Capacity to turnover 3 million tons of bunkers

• Remainder used for import of clean products into Northern Morocco and trading

• Accommodate Suezmax tankers and a barge jetty

• 25 year concession

• Recent reports suggest that Aegean will be the sole supplier of bunkers

• Intension to service in-port and passing traffic

Page 29

29Sotogrande 15 May [email protected]

Demand for residual bunkers in the Port of Tanger Med

1.060.422,5801,900Total `

0.060.027008040Tankers

0.400.201,0001,000800CMA CGM Consortium

0.600.201,0001,500700Maersk

PotentialMarketmillion

tons2020

PotentialMarketMilliontons2011

Typical Bunker StemTons

Number of VesselCalls 2020

Number ofVessel

Calls 2011

Number of Vessel Calls

Significant other traffic by 2020

Page 30

30Sotogrande 15 May [email protected]

44,500Potential market

4,500Container ships unlikely to make bunker only calls

500Bunkering at Ceuta

8,500Bunkering at Gibraltar

7,000Calling at Algeciras for bunkers and cargo(excluding ferries)

30,000Ferries and smaller vessels

Stemming 5% of these vessels at the average stem of 800 tons presents a potential additional market of 1.5 million tons

There is a significant unsatisfied bunker-only market

Vessels pa

Total vessels thorough the Straits 95,000

LESS

Page 31

31Sotogrande 15 May [email protected]

There is a significant up side to these forecasts

• TMSA have significant expansion plans with Stage 2 of the port - operational by 2014

• A new ferry port is under construction providing further demand subject to- Provision of low sulphur, competitively priced fuels- Delivery by hydrant if the volume justifies this approach

• A new car export facility and a bulk terminal are under development

• Provision of lower sulphur fuels to vessels on route to the North and Baltic Seas

• With low freight rates and as bunker prices harden, then there will be a greater propensity to seek competitively priced off shore(bunker-only) supplies

Potential market of 2 million tons by 2015

Page 32

32Sotogrande 15 May [email protected]

Tanger Med could reduce sales in Gibraltar and inhibit growth in Algeciras

Overall growth in the Straits will be above the global average

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

AlgecirasCeutaGibraltar Tanger MedTotal

Page 33

33Sotogrande 15 May [email protected]

In summary

• Difficult times over the next five years

• Life is becoming more complex

• Storage capacity in the Straits growing by 1 million cub

• Gibraltar may be the most vulnerable marker in need of Government support

• Tanger Med will have a significant impact on the Straits market

• Bunker demand in the Straits will grow faster than the global average

• Revenues will increase four fold over the next decade

Page 34

34Sotogrande 15 May [email protected]

Bunkering in the StraitsBunkering in the Straits

Bunker Summit 2009Bunker Summit 2009Mediterranean and Black SeaMediterranean and Black Sea

Sotogrande Sotogrande 15 May 200915 May 2009

Robin MeechRobin Meech

Marine and Energy Consulting LimitedMarine and Energy Consulting Limited