Business Accounts An account is a location within an accounting system in which the increases and decreases in a specific asset, liability, or owner’s equity are recorded and stored. e accounts of a business are grouped together in a A ledger is a book or a file containing a separate page for each business account. The ledger serves as a permanent record of financial transactions. That sounds a little confusing.

Transcript

Business AccountsAn account is a location within an accounting system in which the increases and decreases in a specific asset, liability, or owner’s equity are recorded and stored.

All the accounts of a business are grouped together in a ledger.

A ledger is a book or a file containing a separate page for each business account. The ledger serves as a permanent record of financial transactions.

That sounds a little confusing.

Chart of AccountsTo keep track of its accounts, a business develops a Chart of Accounts.Let’s take another look at the list of accounts for Roadrunner Delivery Service Assets = Liabilities + Owner’s Equity

Cash in BankAccounts ReceivableComputer EquipmentOffice EquipmentDelivery Equipment

Accounts Payable M. Sanchez, Capital

We should probably make this look a little

more official.

Numbering the Chart of Accounts

All Liability accounts begin with 2.

All Owner’s Equity accounts begin with 3.

All Asset accounts begin with 1.

All Revenue accounts begin with 4.

All Expense accounts begin with 5.

Let’s see what the Roadrunner Delivery Service Accounts would look like.

Roadrunner Delivery Service Chart of Accounts

Chart of Accounts

Roadrunner Delivery Service

Assets

Cash in BankAccounts Receivable – City NewsAccounts Receivable – Green CompanyComputer EquipmentOffice EquipmentDelivery Equipment

101105110115120125

Liabilities

Accounts Payable – Beacon AdvertisingAccounts Payable – North Shore Auto

201205

Owner’s Equity

M. Sanchez, CapitalM. Sanchez, WithdrawalsIncome Summary

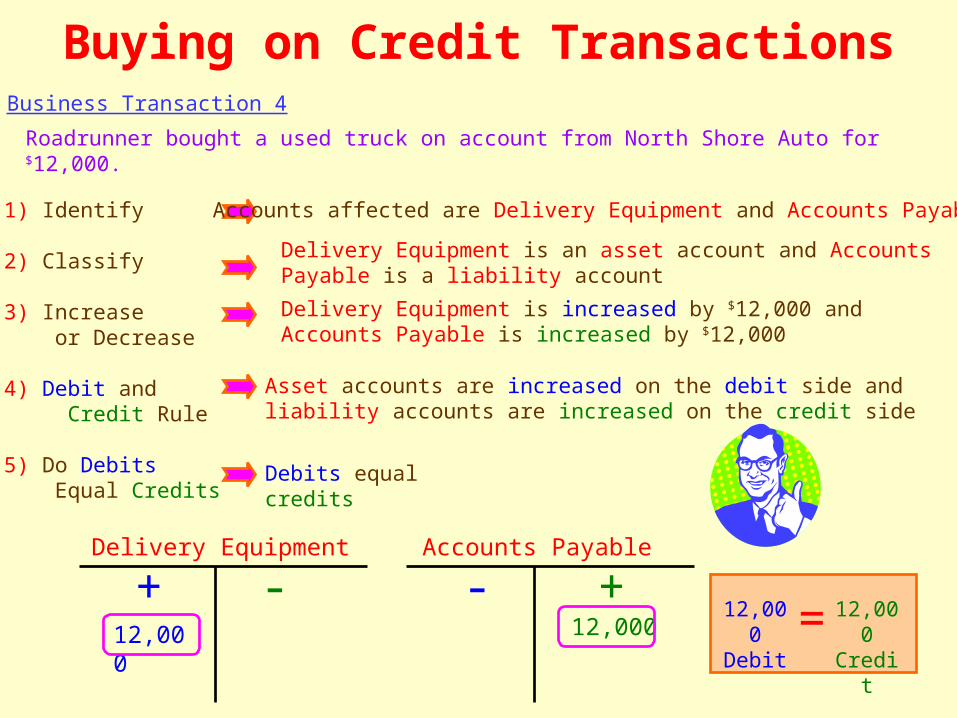

Roadrunner received and deposited a check for $200 from Green Company. The check received was full payment for the telephone sold on account in transaction 5.

1) Identify

2) Classify

3) Increase or Decrease

4) Debit and Credit Rule

5) Do Debits Equal Credits

Accounts affected are Cash in Bank and Accounts Receivable

Cash in Bank is an asset account and Accounts Receivable is an asset account

Cash in Bank is increased by $200 and Accounts Receivable is decreased by $200

Asset accounts are increased on the debit side and asset accounts are decreased on the credit side

![€¦ · Web view2009. 4. 23. · [Cr2O72-] Reverse Rate. A. increases increases. B. increases decreases. C. decreases decreases. D. decreases increases. 31. A small amount of H2SO4](https://static.documents.pub/doc/80x56/608f2c47b9e3f5096f2e5efc/web-view-2009-4-23-cr2o72-reverse-rate-a-increases-increases-b-increases.jpg)

![butane.chem.uiuc.edubutane.chem.uiuc.edu/flener/chem102sum06/pictures/chem102he3.pdfAs the hydroxide ion concentration of a solution increases, POH and the [H+] a) increases, decreases](https://static.documents.pub/doc/80x56/5e688f821a902f6684374206/as-the-hydroxide-ion-concentration-of-a-solution-increases-poh-and-the-h-a.jpg)