Page 1

Accelerating Our Momentum

1

Accelerating Our Momentum

Business and Franchise MomentumNorfolk Southern Investor and Financial Analyst ConferenceJune 8, 2011 Donald W. Seale

Executive Vice President & Chief Marketing Officer

Page 2

Accelerating Our MomentumAccelerating Our Momentum

Agenda

Strong platform for accelerated rail growth

NS business trends and franchise update

NS market drivers, network and outlook

NS long term focus and strategy

2

Page 3

Accelerating Our MomentumAccelerating Our Momentum

Favorable Environment for Rail

Favorable Rail Environment

Seizing the opportunity from

manufacturing growth

Foreign trade growth & increased

domestic containerization

Impact of CSA 2011

Increasing focus on environmental

stewardship

Tightening capacity across all modes

Public sentiment

Rail productivity gains

3

Page 4

Accelerating Our MomentumAccelerating Our Momentum

0

50,000

100,000

150,000

200,000

250,000

300,000

2006 2007 2008 2009 2010

Units U.S. Class 8 Sales U.S. Trailer Production

Shrinking Truckload Capacity Trends

Source: FTR Associates, Paccar

Class 8 Replacement Rate

4

Page 5

Accelerating Our MomentumAccelerating Our Momentum

Compliance Safety Accountability Program 2011 & The Changing Truckload Market

CSA 2011 safety rating program Calculates carriers’ and drivers’ safety ratings using defined set of criteria

Hours of service regulations Reduction of workday to 10 hours of driving time

FMCSA training requirements New regulations governing recruitment and improving training

ID requirements Imposes strict national standards for issuance of state ID documents

Net Effect

More than 300,000 drivers will be disqualified between now and 2012 –doubling current driver shortage

Driver shortage may cost shippers an additional $25 billion

Estimated that new regulations will decrease trucking productivity by over 5%

5

Page 6

Accelerating Our MomentumAccelerating Our Momentum

251,169 156,874

258,691 128,655 133,212

1,259,969

663,075

Agriculture Chemicals MetCon Paper Automotive Intermodal Coal

NS Railway VolumeYTD through Week 21 vs. 2010

Source: AAR carloadings, which are reported weekly and may not equal NS’ reported volumes.

(3%)(5%)

3%(3%)

9%

15%

7%

2.9 million units YTD, up 153,894 or 6% vs. 2010

6

Page 7

Accelerating Our MomentumAccelerating Our Momentum

Record Revenue Per Unit in 1st Quarter 2011

$0

$300

$600

$900

$1,200

$1,500

$1,800

$2,100

$2,400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

RPU Merchandise Intermodal Coal Total

7

70% increase

since 2000

2010 vs. 2000RPU CAGR

4.6%

Page 8

Accelerating Our MomentumAccelerating Our Momentum

Highest Revenue Per Ton Mile among U.S. Class I RRs

020406080

100120140160180200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Indexed to 2000 NS Carrier A Carrier B Carrier C

Source: AAR for UP, BNSF; NS and CSXT from Financial Statements, revenue per revenue ton mile

8

68% increase

since 2000

2010 vs. 2000RPTM CAGR

5.3%

Page 9

Accelerating Our MomentumAccelerating Our Momentum

Source: AAR, FTR, Global Insight, NS

NS Volume vs. Low Tech IPI and Motor Carriers

9

80859095

100105110115120125130

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Indexed to 1Q 00 NS Volume Other U.S. RRs Volume less NS Truck Tonnage Low Tech IPI

Page 10

Accelerating Our MomentumAccelerating Our Momentum

020406080

100120140160180200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Indexed to 2000 NS Revenue Other U.S. RRs Revenue less NS Truck Revenue Low Tech IPI

Source: AAR, FTR, Global Insight, NS

NS Revenue vs. Low Tech IPI and Motor Carriers

10

Page 11

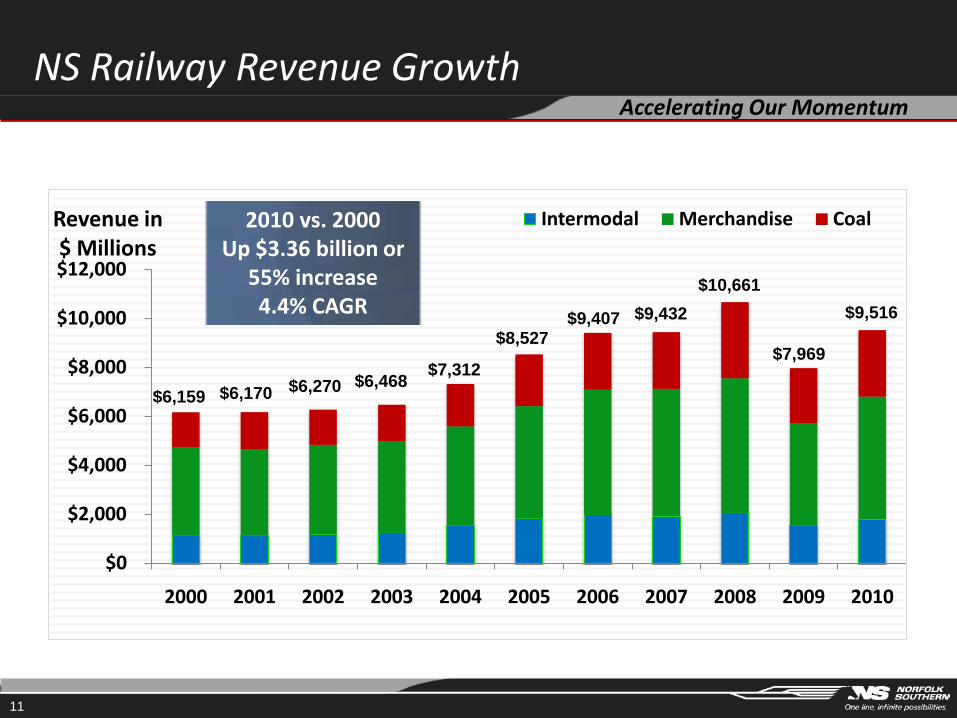

Accelerating Our Momentum

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Revenue in $ Millions

Intermodal Merchandise Coal

NS Railway Revenue Growth

$9,407$8,527

$7,312$6,468$6,270$6,170$6,159

$9,432$10,661

$7,969

$9,516

2010 vs. 2000Up $3.36 billion or

55% increase 4.4% CAGR

11

Page 12

Accelerating Our MomentumAccelerating Our Momentum

Major Group Revenue2000 - 2010

Revenue in $ Millions

2000 2002 2004 2006 2008 2010 CAGR

Agriculture $609 $637 $727 $994 $1,282 $1,326 8.1%

Coal $1,435 $1,441 $1,728 $2,330 $3,111 $2,719 6.6%

Chemicals $756 $755 $864 $1,079 $1,238 $1,302 5.6%

Intermodal $1,119 $1,181 $1,537 $1,971 $2,058 $1,796 4.8%

MetCon $689 $692 $818 $1,168 $1,251 $1,013 3.9%

Paper $630 $603 $684 $891 $898 $712 1.2%

Automotive $921 $961 $954 $974 $823 $648 (3.5%)

Total $6,159 $6,270 $7,312 $9,407 $10,661 $9,516 4.4%

12

Page 13

Accelerating Our MomentumAccelerating Our Momentum

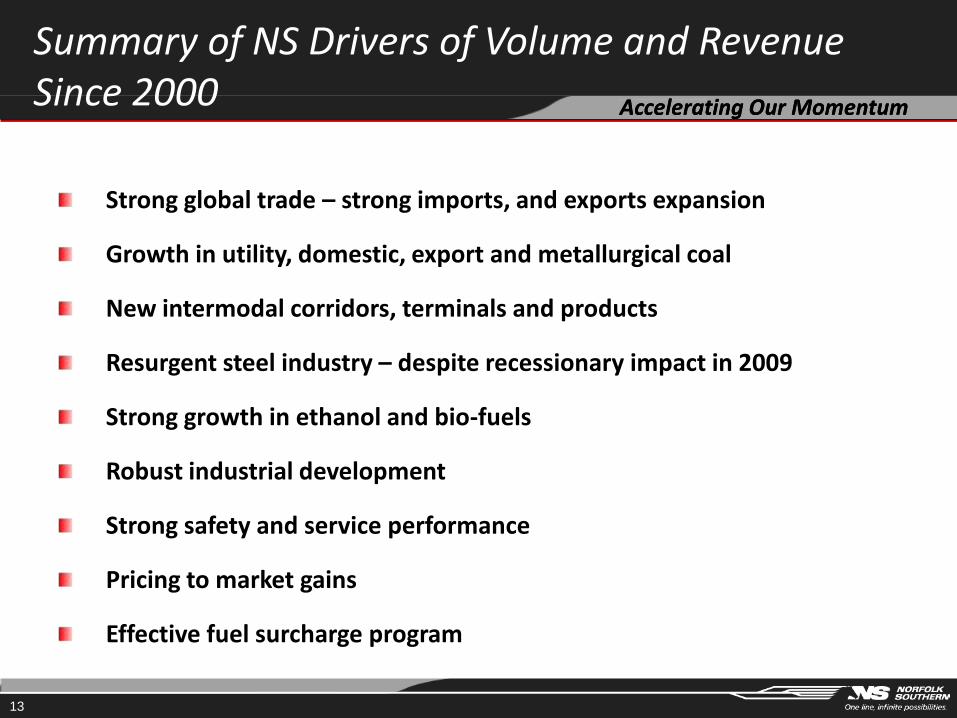

Summary of NS Drivers of Volume and Revenue Since 2000

Strong global trade – strong imports, and exports expansion

Growth in utility, domestic, export and metallurgical coal

New intermodal corridors, terminals and products

Resurgent steel industry – despite recessionary impact in 2009

Strong growth in ethanol and bio-fuels

Robust industrial development

Strong safety and service performance

Pricing to market gains

Effective fuel surcharge program

13

Page 14

Accelerating Our MomentumAccelerating Our Momentum

Balanced Portfolio of Business

% of 2010 NS Revenue

NS Network

74% of U.S. population

58% of total energy consumption in U.S.

63% of U.S. manufacturing

Estimate 30M+ truck shipments over 550 miles touch our network

Extensive port access

Intermodal19%

Coal28%

Agriculture14%

Manufacturing39%

14

Page 15

Accelerating Our MomentumAccelerating Our Momentum

NY / NJPhiladelphia

WilmingtonBaltimore

Morehead City

Charleston

Savannah

Brunswick

Jacksonville

NorfolkPortsmouth

Mobile

New OrleansBraithwaite

St. Bernard

15

NS Railway& Ports served by NS

Seaports 16

River Ports 8

Lake Ports 7

Cleveland

ErieAshtabula

Detroit

Toledo

Chicago

Burns Harbor

Granite City, IL

Jeffersonville, IN

Cincinnati

Louisville

NaplesPortsmouth, OH

Pittsburgh

Memphis

A Network of Key Corridors andPort Access

Camden / South Jersey

Page 16

Accelerating Our MomentumAccelerating Our Momentum

Our Coal Network

Coal Robust electrical generating base

Strong export network with increased demand in European, Asian & South American markets

Custom coking coal blending

Expansive coal sourcing

More productive coal car fleet

Corridor/terminal investment

Cutting edge supply chain management (CTMS)

16

6.6%

10 Year CAGR Revenue

6.6%

% of 2010 Tonnage

Utility 71%

Industrial4%

Domestic Met12%

Export13%

Page 17

Accelerating Our MomentumAccelerating Our Momentum

Our Coal Network

17

Utility Coal

Reaches 103 utility coal generation plants

Directly serves 86 plants 55 in the North 31 in the South

Access to an additional 17 plants through connecting carriers and lake service

Page 18

Accelerating Our MomentumAccelerating Our Momentum

Lamberts Point, VA Coal Terminal

18

Export Coal

Largest and fastest export coal loading terminal in the Northern Hemisphere

Handled 40 million tons in 1990

2011 Tonnage vs. 2010 1st Q 15% April 34% May 59%

Available for capacity growth

Steam coal opportunities ahead

Page 19

Accelerating Our MomentumAccelerating Our Momentum

CNX Marine Terminal, Baltimore, MD

19

Export Coal

CONSOL announced Baltimore export terminal expansion April 28, 2011

2 million ton capacity expansion to 16 million tons/year

Rail infrastructure expansion online in 2012

Long term potential for additional expansion

Page 20

Accelerating Our MomentumAccelerating Our Momentum

Fairless, PA and Charleston, SCCoal Tonnage Moving Today

20

Norfolk Southern Railway and its Railroad Operating Subsidiaries- - - NS Trackage and Haulage Rights

Illinois Basin

Northern Appalachia

Powder River Basin

CentralAppalachia

Fairless, PA

Charleston, SC

Page 21

Accelerating Our MomentumAccelerating Our Momentum

Wheelersburg, OH Coal Terminal

21

Domestic Met Coal

9 million tons/year throughput

1.2 million tons ground storage capacity, with optimized pile configuration

Custom blending for domestic coke production

Expansion plans to support new steam coal

Page 22

Accelerating Our MomentumAccelerating Our Momentum

NS Coal Network Flows

22

Tonnage % ChangeYTD thru May vs. 2010

Utility 7%

Export 26%

Domestic Met (9%)

Industrial (5%)

% of 2010 Tonnage

Utility 71%

Industrial4%

Domestic Met12%

Export13%

Page 23

Accelerating Our MomentumAccelerating Our Momentum

Norfolk Southern Railway and its Railroad Operating Subsidiaries- - - NS Trackage and Haulage Rights

Illinois Basin

11.1 M Tons8%

Northern Appalachia45.3 M Tons

29%

Powder River Basin

32.8 M Tons 21%

CentralAppalachia64.8 M Tons

42%

NS Origin Coal 2010 Volume (Tons)

23

Page 24

Accelerating Our MomentumAccelerating Our Momentum

Norfolk Southern Railway and its Railroad Operating Subsidiaries- - - NS Trackage and Haulage Rights

Illinois Basin

11.1 M Tons8%

NS Mid-America Corridor to reach Illinois Basin

24

Corinth, MS

Page 25

Accelerating Our Momentum

Increased Coal Car Capacity

Hoppers

Old steel hopper payload capacity: 104 tons

New stainless body hopper payload capacity: 113 tons

Gons

Old steel gondola payload capacity: 112 tons

New hybrid body gondola payload capacity: 118 tons

25

Page 26

Accelerating Our MomentumAccelerating Our Momentum

Our Manufacturing Network

Manufacturing

Resurgence of U.S. Manufacturing

Metals, Construction, Chemicals, Automotive and Paper

63% of U.S. manufacturing in our service territory

Highest revenue per unit network for NS

26

10 Year CAGR Revenue

2.1%

% of NS Mfg. 2010 Revenue

Auto18%

Paper19%

Chemicals35%

MetCon28%

Page 27

Accelerating Our MomentumAccelerating Our Momentum

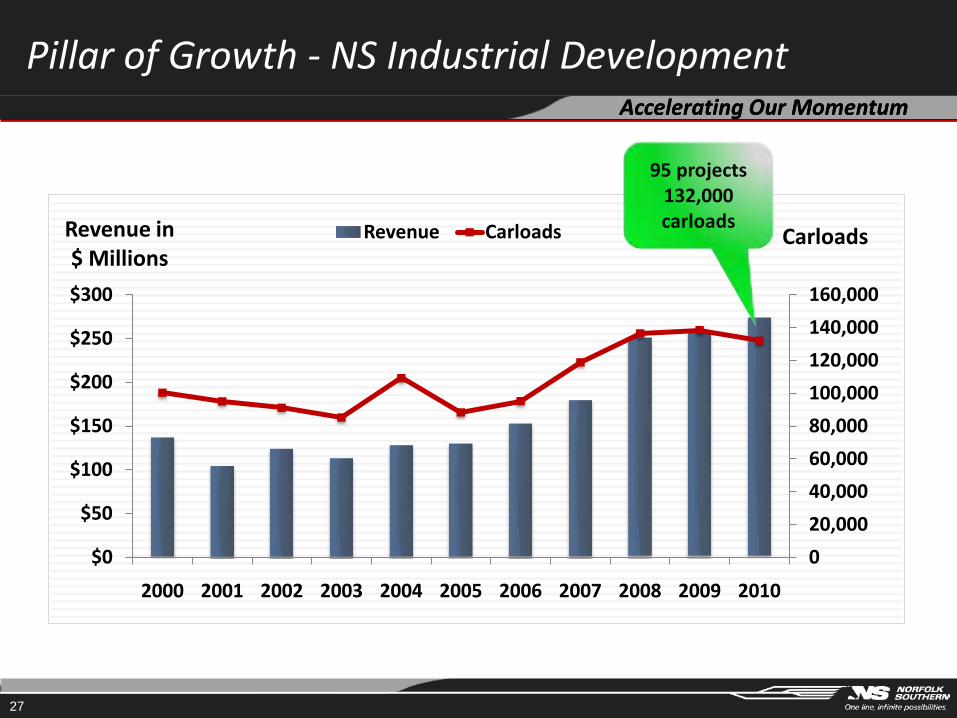

Pillar of Growth - NS Industrial Development

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

$0

$50

$100

$150

$200

$250

$300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

CarloadsRevenue in $ Millions

Revenue Carloads

27

95 projects132,000 carloads

Page 28

Accelerating Our MomentumAccelerating Our Momentum

$5 billion investment

5.3 million metric tons of annual production

3,460 acres (155 under roof)

Our Manufacturing Network Continues to Expand

ThyssenKrupp Steel and Stainless USA,

Calvert, AL

28

Page 29

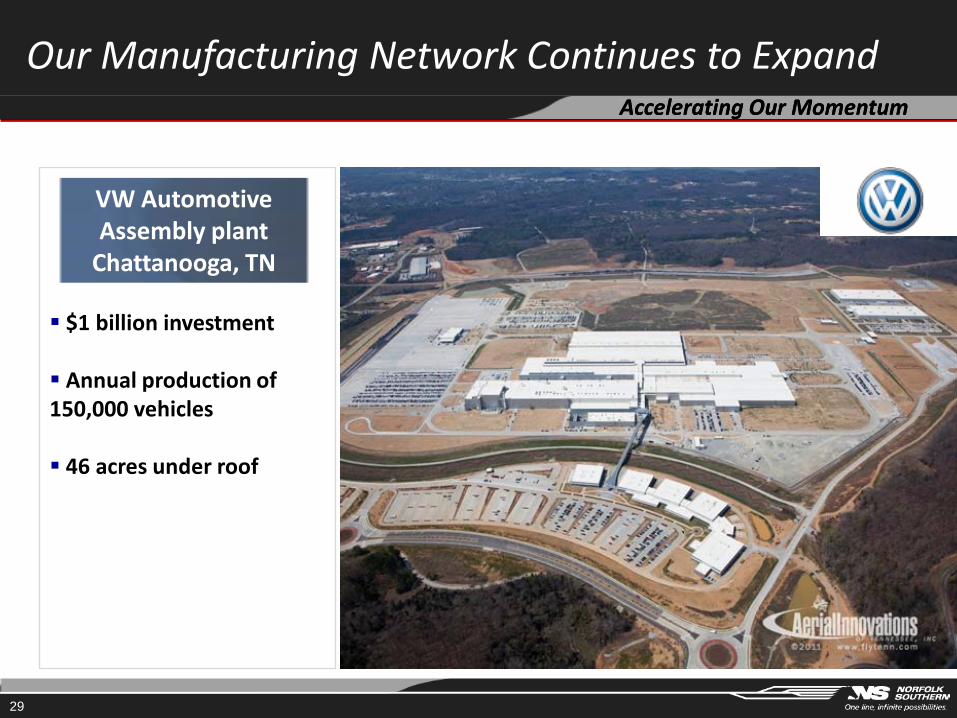

Accelerating Our MomentumAccelerating Our Momentum

Our Manufacturing Network Continues to Expand

29

$1 billion investment

Annual production of 150,000 vehicles

46 acres under roof

VW Automotive Assembly plant

Chattanooga, TN

Page 30

Accelerating Our MomentumAccelerating Our Momentum

Major Auto Projects

30

Our Manufacturing Network Continues to Expand

Page 31

Accelerating Our MomentumAccelerating Our Momentum

Our Manufacturing Network Continues to Expand

31

First Quality TissueAnderson, SC

$1 billion investment

1,000 new jobs

Among the “Top Ten Deals” for industrial development projects in North America in 2010

Page 32

Accelerating Our MomentumAccelerating Our Momentum

Our Manufacturing Network Continues to Expand

32

PBF Energy Partners, LP Delaware City, DE

$130 million reinvestment in the facility

Previously dormant refinery

Reopened due to increased demand for refinery production and byproducts

Page 33

Accelerating Our MomentumAccelerating Our Momentum

Biofuels and Energy Investments

Our Manufacturing Network Continues to Expand

33

Page 34

Accelerating Our MomentumAccelerating Our Momentum

34

Volume % ChangeYTD thru May vs. 2010

MetCon 3%

Chemicals (5%)

Paper (3%)

Automotive 15%

NS Manufacturing Network Flows

% of NS Mfg. 2010 Revenue

Auto18%

Paper19%

Chemicals35%

MetCon28%

Page 35

Accelerating Our MomentumAccelerating Our Momentum

Our Agriculture Network

Agriculture

NS serves more than 330 shippers and receivers of corn and soybeans

Extensive Ag network for domestic and export grain markets

Extensive supply chain support for ethanol producers and distributors

Projected rise in global demand

10 Year CAGR Revenue

8.1%

35

% of NS Agriculture2010 Revenue

Ethanol16%

Fertilizers10%

Sweeteners12%

Corn18%

Soybeans4%

Other40%

Page 36

A l ti O M tA l ti O M t

Our Unit GrainTrain Network Accelerating Our MomentumAccelerating Our MomentumTrain Network

NSNSUnit Grain TrainUnit Grain Train

NetworkNetwork

Shreveport

30 75‐Car Unit Train Receivers

44 75‐Car Unit Train Loaders

3636

Page 37

Accelerating Our MomentumAccelerating Our Momentum

Our Agriculture Network

Ethanol

74 terminals served

25 production plants in service territory

2.4 billion production gallons annually, 16% of U.S. demand

E15 long term growth

Yr. 2000-2005

Yr. 2005-2010

Carload Growth

2011 Three new NS

Terminals Opening in VA, TN

and PA

124%226%

37

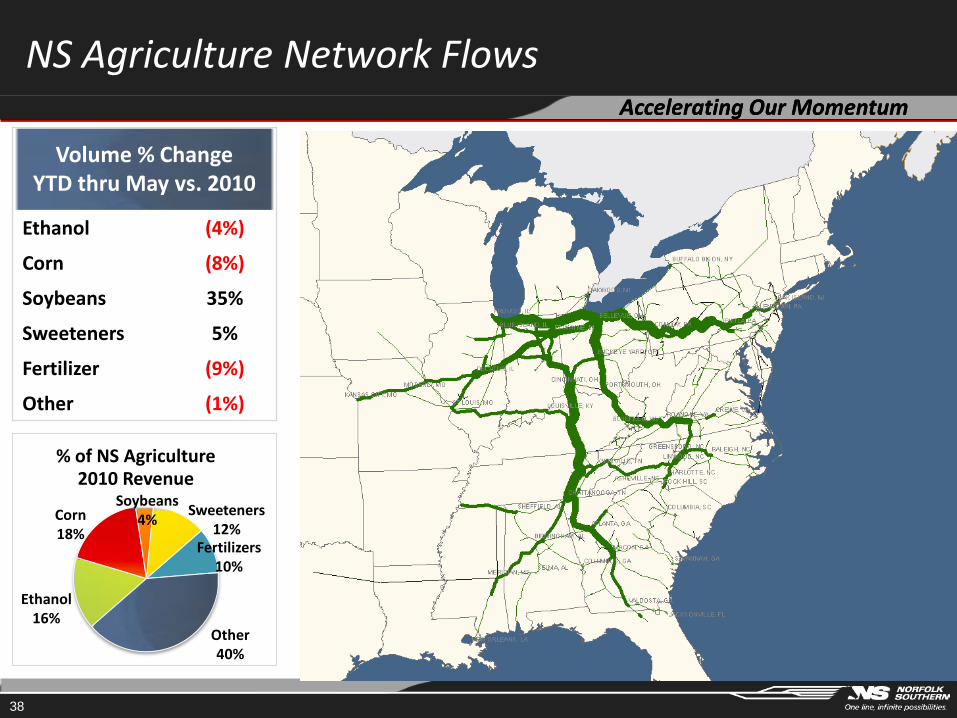

Page 38

Accelerating Our MomentumAccelerating Our Momentum

NS Agriculture Network Flows

Volume % ChangeYTD thru May vs. 2010

Ethanol (4%)

Corn (8%)

Soybeans 35%

Sweeteners 5%

Fertilizer (9%)

Other (1%)

38

% of NS Agriculture 2010 Revenue

Ethanol16%

Fertilizers10%

Sweeteners12%

Corn18%

Soybeans4%

Other40%

Page 39

Accelerating Our MomentumAccelerating Our Momentum

10 Year CAGR Revenue

4.8%

Our Intermodal Network

Intermodal

Extensive distribution network

97% of network cleared for doublestack

Public/private partnerships

Investment in key corridors and equipment

Terminal network supports East Coast and West Coast flows

39

% of NS Intermodal 2010 Revenue

International29%

Premium11%

Domestic42%

Triple Crown18%

Page 40

Accelerating Our MomentumAccelerating Our Momentum

U.S. Intermodal Year-over-Year Change in Units Since 2009

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar

% Change in Units Y-o-Y Domestic International

2009 2010Source: IANA

2011

40

Page 41

Accelerating Our MomentumAccelerating Our Momentum

NS Domestic and International Intermodal Long-Term Growth

Source: NS traffic data

0

100,000

200,000

300,000

400,000

500,000

600,000Units Domestic Units International Units

41

Page 42

Accelerating Our MomentumAccelerating Our Momentum

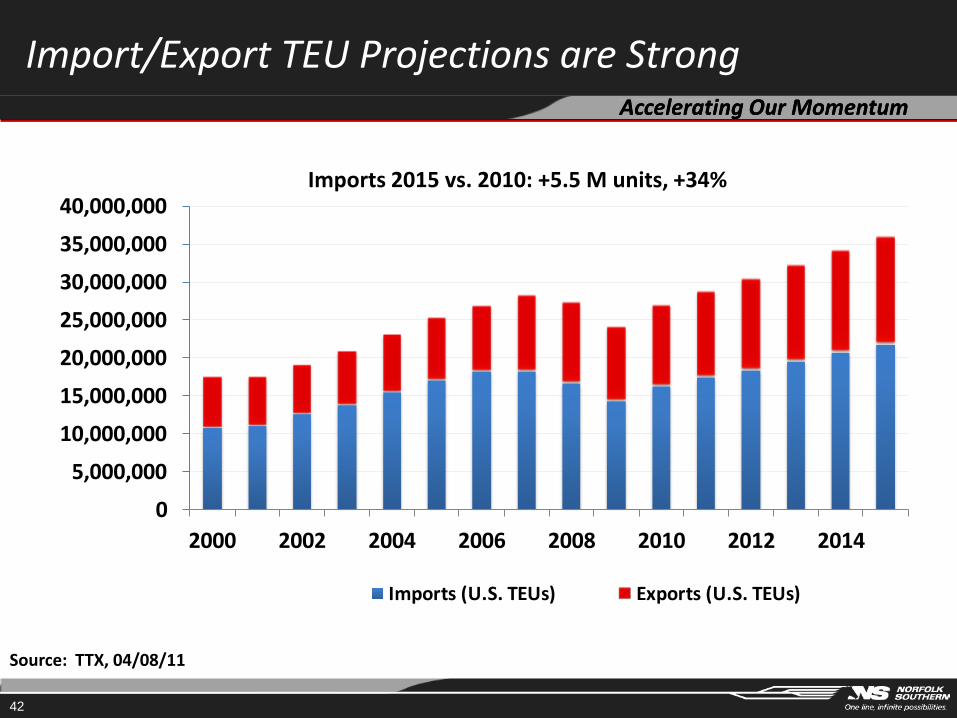

Import/Export TEU Projections are Strong

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2000 2002 2004 2006 2008 2010 2012 2014

Imports (U.S. TEUs) Exports (U.S. TEUs)

Source: TTX, 04/08/11

Imports 2015 vs. 2010: +5.5 M units, +34%

42

Page 43

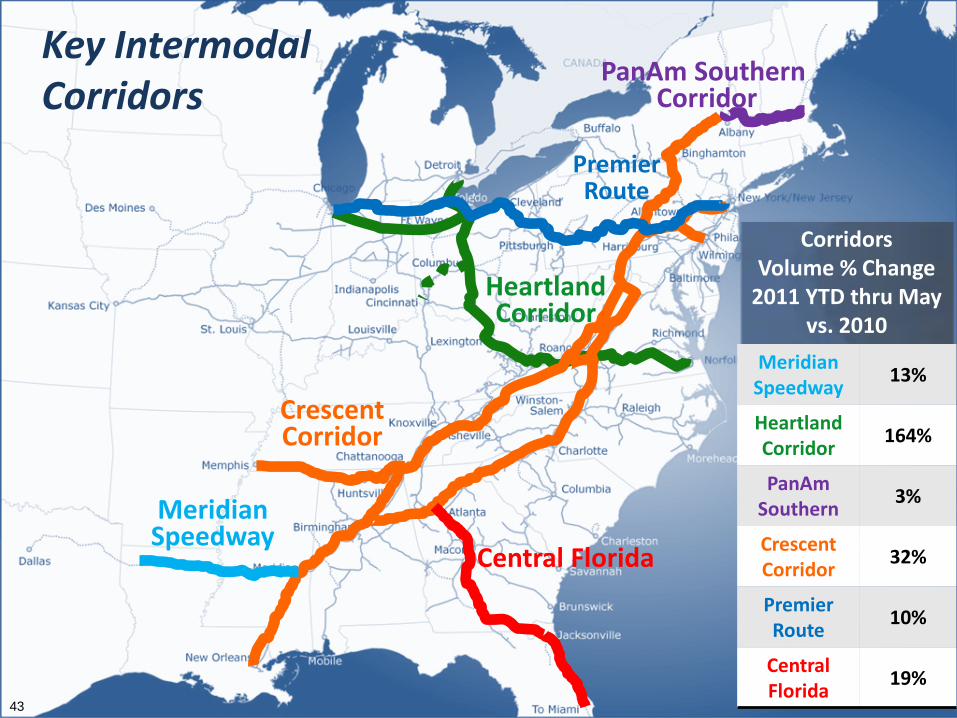

Accelerating Our MomentumAccelerating Our Momentum

Key IntermodalCorridors

Corridors Volume % Change

2011 YTD thru Mayvs. 2010

Meridian Speedway

13%

HeartlandCorridor

164%

PanAmSouthern

3%

CrescentCorridor

32%

Premier Route

10%

Central Florida

19%

HeartlandCorridor

CrescentCorridor

MeridianSpeedway

PanAm Southern Corridor

43

Central Florida

PremierRoute

Page 44

Accelerating Our MomentumAccelerating Our Momentum

Key IntermodalCorridors

MeridianSpeedway

44

MeridianSpeedway

JV with KCS

NS investment of $300 million

Fastest route LA to Atlanta (4 days)

Volume up 13% YTD thru May 2011

Domestic and international growth

Page 45

Accelerating Our MomentumAccelerating Our Momentum

Key IntermodalCorridors

HeartlandCorridor

45

HeartlandCorridor

Completed in Sept. 2010

Total investment $191 million (NS 51%, 49% public)

Reduced over 200 route miles

Volume up 164% YTD thru May 2011

Port, corridor, and terminals ready for big ships NOW

MeridianSpeedway

Page 46

Accelerating Our MomentumAccelerating Our Momentum

Key IntermodalCorridors

HeartlandCorridor

MeridianSpeedway

PanAm Southern Corridor

46

PanAm SouthernCorridor

JV with PanAmRailway

Initial investment $140 million

Direct access to Boston & New England markets

Volume up 3% YTD thru May 2011

Mechanicville / Albany terminal under construction

Efficient intermodal terminal at Ayer, MA

Page 47

Accelerating Our MomentumAccelerating Our Momentum

Key IntermodalCorridors

HeartlandCorridor

CrescentCorridor

47

PanAm Southern Corridor

CrescentCorridor

Largest NS corridor project

Total investment $599 million (NS 55%, public 45%)

Targets I-81 and I-40 truck corridors

Volume up 32% YTD thru May 2011

4 new terminals under construction

MeridianSpeedway

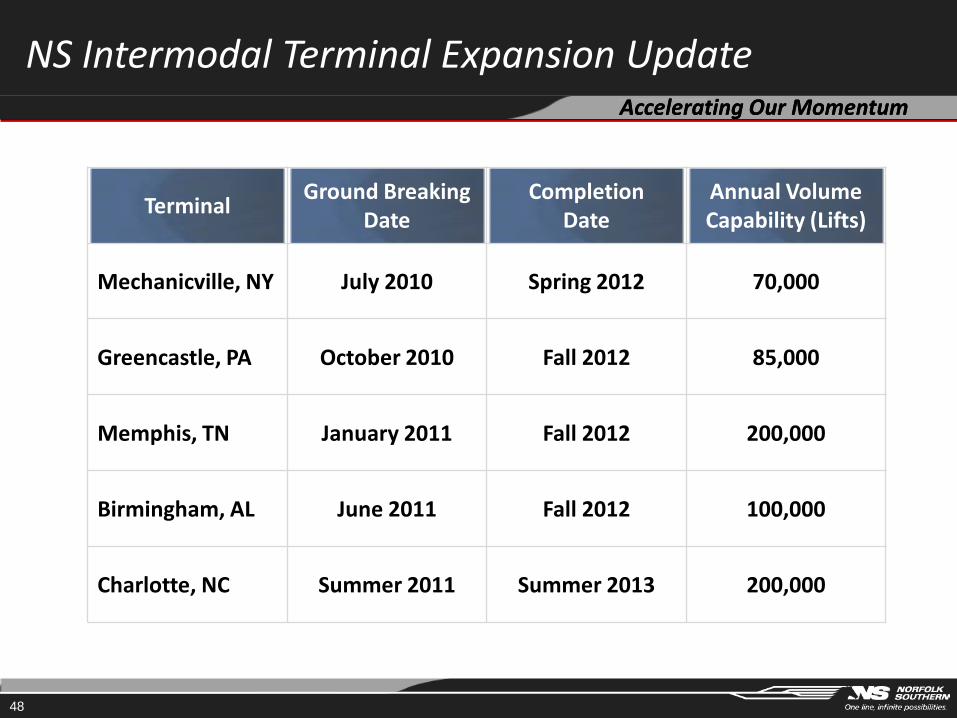

Page 48

Accelerating Our MomentumAccelerating Our Momentum

TerminalGround Breaking

DateCompletion

DateAnnual Volume Capability (Lifts)

Mechanicville, NY July 2010 Spring 2012 70,000

Greencastle, PA October 2010 Fall 2012 85,000

Memphis, TN January 2011 Fall 2012 200,000

Birmingham, AL June 2011 Fall 2012 100,000

Charlotte, NC Summer 2011 Summer 2013 200,000

48

NS Intermodal Terminal Expansion Update

Page 49

Accelerating Our MomentumAccelerating Our Momentum

Volume % ChangeYTD thru May vs. 2010

Domestic 17%

International 2%

49

NS Intermodal Network Flows

Chicago

Golden Triangle volume represents

approx. 90% of total NS Intermodal

volume

Harrisburg

Atlanta

% of NS Intermodal 2010 Revenue

International29%

Premium11%

Domestic42%

Triple Crown18%

Page 50

Accelerating Our MomentumAccelerating Our Momentum

Market and volume growth across all markets

Collaboration with supply chain partners in support of

manufacturing resurgence

Collaboration with key global trade partners in support of continued

international bulk and intermodal growth

Strategic investments in network and terminals to support

profitable growth

Pricing to the market, exceeding rail inflation

Long-Term Business Focus and Strategy

50

Page 51

Accelerating Our MomentumAccelerating Our Momentum

Thank You

51