57

Business associations Section 3b: SH litigation Prof. Amitai Aviram [email protected] University of Illinois College of Law Copyright © Amitai Aviram. All Rights Reserved F13

| Date post: | 11-Dec-2015 |

| Category: |

Documents |

| Upload: | piper-perrins |

| View: | 217 times |

| Download: | 1 times |

Business associationsSection 3b:

SH litigationProf. Amitai [email protected]

University of Illinois College of LawCopyright © Amitai Aviram. All Rights Reserved

F13

Copyright © Amitai Aviram. All Rights Reserved2

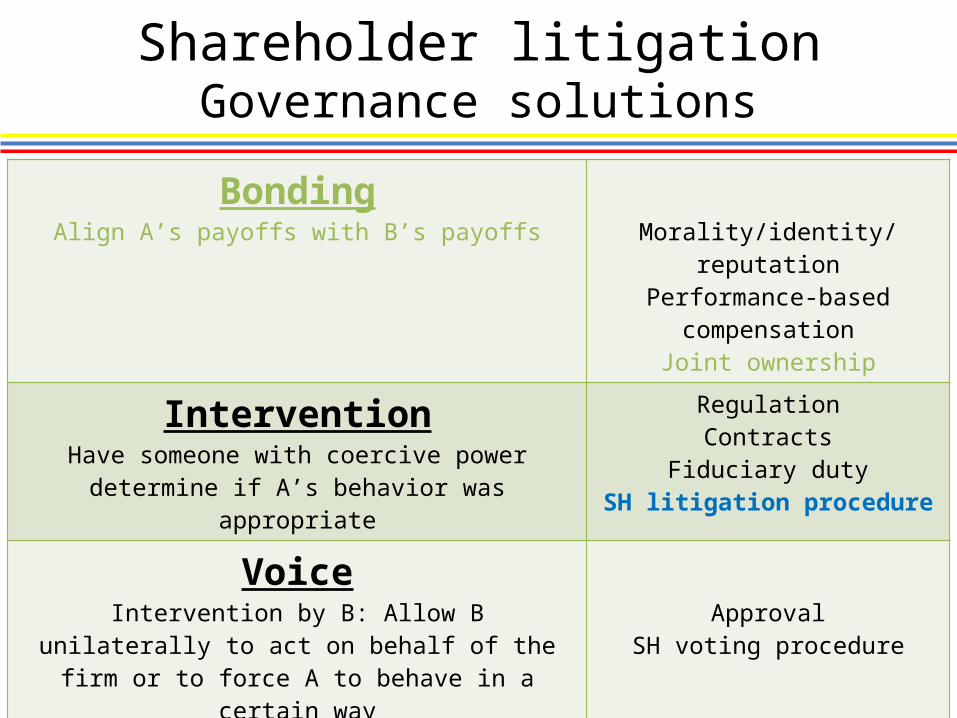

Shareholder litigationGovernance solutions

BondingAlign A’s payoffs with B’s payoffs Morality/identity/reputation

Performance-based compensationJoint ownership

InterventionHave someone with coercive power determine if A’s

behavior was appropriate

RegulationContracts

Fiduciary dutySH litigation procedure

VoiceIntervention by B: Allow B unilaterally to act on behalf of

the firm or to force A to behave in a certain wayApproval

SH voting procedure

ExitAllow B unilaterally to end her relationship & receive her

share of the value produced by the relationship

TerminationDissociationAlienation

Shareholder litigationOverview of Section 3b

1. Litigation concepts– Process of litigation– Economics of settlement– Economics of class actions

2a. Derivative actions2b. Derivative actions (continued)3. SH inspection rights

© Amitai Aviram. All rights reserved.3

Process of litigation

• In the next few slides I will highlight some aspects of the litigation process that are most relevant for BA2– I teach this material so you understand the policy behind the rules for SH

litigation & so you are familiar with the process if you’ll practice SH litigation

• Stages of litigation– Preliminaries– Pleadings– Discovery/ pre-trial– Trial– Post-trial

© Amitai Aviram. All rights reserved.4

Process of litigation Preliminaries

• Choice of law– The “internal affairs doctrine” provides that the internal affairs of a firm

(disputes between the firm, corporate actors & SHs) are governed by the law of the state of incorporation (McDermott Inc. v. Lewis [Del. 1987])

• Jurisdiction– Del. Court of Chancery has jurisdiction “to hear and determine all matters and

causes in equity” (10 Del. C. 341), and doesn’t have jurisdiction “to determine any matter wherein sufficient remedy may be had by common law, or statute [before another jurisdiction]” (10 Del. C. 342)

• Venue– Courts outside Delaware may have jurisdiction over SH litigation of Delaware

corporations; in recent years, Delaware has been losing market share in SH litigation of Delaware corporations.

• In response, companies have started to adopt forum selection bylaws directing disputes to Delaware courts (recall the Chevron case in Section 3a3)

© Amitai Aviram. All rights reserved.5

Process of litigationPleadings

• Complaint– Plaintiff’s complaint commences the lawsuit; must allege:

• Jurisdiction• Claim (facts showing that plaintiff is entitled to relief)• Relief (a demand for an appropriate remedy)

• Provisional remedies– Plaintiff can ask judge for immediate (provisional) remedies when waiting for a

post-trial remedy would cause irreparable harm– TRO (temporary restraining order): issued before opponent can respond– Preliminary injunction: issued after opponent responds (but before trial)– Standard (for both): (a) reasonable probability of success on the merits; (b)

reasonable likelihood moving party will suffer irreparable harm absent the provisional remedy & that harm outweighs harm to non-moving party from granting the provisional remedy

© Amitai Aviram. All rights reserved.6

Process of litigationPleadings

• Pre-answer motions (motion to dismiss)– Can be based on procedural flaw (lack of jurisdiction, improper venue, faulty

process or service) or substantive flaw (failure to state a claim)– Standard for dismissal for failure to state a claim (Rule 12(b)(6))

• Federal courts: “a complaint must contain sufficient factual matter, accepted as true, to state a claim to relief that is plausible on its face” (Twombly [US 2007], Iqbal [US 2009])

• Delaware: complaint dismissed for failing to state a claim only if, accepting plaintiff’s factual allegations as true, “plaintiff would not be entitled to recover under any reasonably conceivable set of circumstances” (Central Mortgage [Del. 2011])

• Non-moving party’s well-pled allegations are accepted as true, and factual inferences are made in light most favorable to non-moving party

• Answer– Defendant responds to complaint, including asserting defenses, counter-claims

(against plaintiff) & joinder (requesting that other necessary parties be included in the litigation)

• Post-pleading motions (motion for judgment on the pleadings)– Rule 12(c): granted if pleadings fail to reveal existence of any disputed material

fact & movant is entitled to judgment as a matter of law– Same standard as a motion to dismiss for failure to state a claim.– Is defendant more likely to use a Rule 12(b)(6) or a Rule 12(c) motion?

© Amitai Aviram. All rights reserved.7

Process of litigationLater stages of litigation

• Discovery– Initial disclosures (info on witnesses, documents & objects that party may use

to support its claims or defenses; computation of damages; insurance information)

– Discretionary discovery (e.g., interrogatories, depositions, requests for producing evidence)

• Motion for summary judgment– No genuine dispute as to any material fact, and the moving party is entitled to

a judgment as a matter of law• Genuine dispute: if a rational factfinder could rule in favor of non-moving party• Material fact: if fact could affect the outcome of the lawsuit

– Factual inferences are made in light most favorable to non-moving party• Trial

– No jury trials in Delaware Court of Chancery (it is an equity court)• Post-trial

– Post-trial motions, enforcement of judgment, appeal

© Amitai Aviram. All rights reserved.8

Economics of settlementExtortion by litigation

• Various legal mechanisms constrain SHs who sue the firm & corporate actors– Enhanced pleading standards

• Persuasiveness of claim (plausible vs. conceivable)• Higher expectation of using available information (e.g., SH inspection rights)

– “Safe harbors” in substantive law• E.g., avoiding entire fairness SoR if “robust procedural protections” implemented

• Why impose these constraints? Because SH litigation imposes costs asymmetrically, creating opportunities to extort the firm– Firm’s reputation can be harmed by litigation; plaintiff usually doesn’t have a

reputation to risk– Typically firm/actors can’t counterclaim against SH (so SH stands to lose no

more than attorney’s fees)– Typically firm/actors can’t impose significant discovery costs on SH

© Amitai Aviram. All rights reserved.9

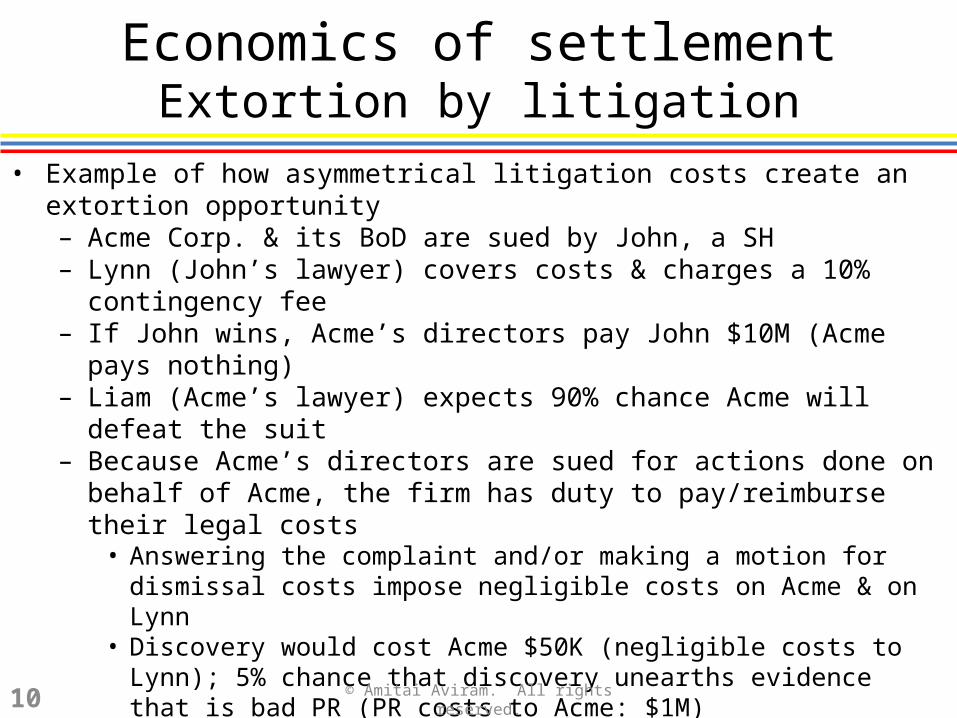

Economics of settlementExtortion by litigation

• Example of how asymmetrical litigation costs create an extortion opportunity– Acme Corp. & its BoD are sued by John, a SH– Lynn (John’s lawyer) covers costs & charges a 10% contingency fee– If John wins, Acme’s directors pay John $10M (Acme pays nothing)– Liam (Acme’s lawyer) expects 90% chance Acme will defeat the suit– Because Acme’s directors are sued for actions done on behalf of Acme, the firm

has duty to pay/reimburse their legal costs• Answering the complaint and/or making a motion for dismissal costs impose

negligible costs on Acme & on Lynn• Discovery would cost Acme $50K (negligible costs to Lynn); 5% chance that

discovery unearths evidence that is bad PR (PR costs to Acme: $1M)• Trial would cost Acme $100K (and cost Lynn the same), negative media

attention from the trial has 5% chance of causing bad PR if Acme wins (PR costs to Acme: $1M) & 100% chance if it loses

• How much would Acme agree to pay to settle the suit?

© Amitai Aviram. All rights reserved.10

Economics of settlementExtortion by litigation

• Lynn’s calculus (when she sues): Cost: $100K; benefit: $100K (10% of $1M) + high chance of settling suit

• Liam’s calculus– If he can win motion to dismiss: no settlement– If he can win motion for summary judgment: settle for <$100K (Lynn likely

accepts, since at this point she has no meaningful costs)– If he has to go to trial (w/90% chance of winning): settle for <$345K

(if Lynn already spent legal costs, she will reject any settlement under $1M)

Litigation is terminated… John Acme Accumulated costs (Acme)

Pre-discovery (motion to dismiss/motion for judgment on the pleadings)

--- --- ---

After discovery (motion for summary judgment)• Legal costs• PR costs

---------

$100K$50K$50K

$100K

After trial• Legal costs• PR costs

$100K$100K

---

$245K$100K

$145K (45K+100K)

$345

© Amitai Aviram. All rights reserved.11

Economics of settlementExtortion by litigation

• Another strategic (and sometimes extortionate) form of litigation involves suits against time-sensitive events; e.g.:– M&A deals– Initial Public Offerings (IPOs)– SH meetings– Why are the above events time-sensitive?

• Suit requests a preliminary injunction to enjoin the event until the trial is over

• Here, the battle is over satisfying the conditions to receive a preliminary injunction; if one is given, defendant will likely settle the suit immediately or abandon the challenged transaction– So, allegations in complaint are crafted to demonstrate irreparable harm to

plaintiff if the event takes place before the trial

© Amitai Aviram. All rights reserved.12

Litigation conceptsEconomics of class actions

• When a party inflicts a small amount of harm on a large number of parties, individual lawsuits aren’t a strong deterrent– E.g., a store illegally overcharges each of its 1M customers $1/month over two

years (total benefit for store: $24M)• Total cost for each customer: $24 (not enough to hire a lawyer to sue)

– This is a common problem in SH litigation• Each SH has a small stake in the firm, so directors can steal $24M from the firm

& it won’t make sense for each of firm’s 1M SHs to sue• Is it a problem?

– Would harm to reputation suffice to deter the store/directors?– Would government enforcement suffice to deter the store/directors?

• The solution: class actions– Class actions allow an individual plaintiff to sue on behalf of all persons with

the same cause of action, and in return plaintiff is reimbursed the legal expenses incurred in the class action

– When a SH sues to vindicate a cause of action belonging to the firm, it is called a derivative action, and is in essence a class action for all SHs

© Amitai Aviram. All rights reserved.13

Economics of class actionsThe Tooley case

• Tooley [Del. 2004]: Credit Suisse acquires DLJ (investment bank)1. Credit Suisse buys from AXA (owner of 71% of DLJ) its DLJ shares2. Credit Suisse launches a tender offer for the remaining 29%3. DLJ merges with Credit Suisse subsidiary (triangular freezeout merger)

• SFM is Credit Suisse reaches 90% ownership of DLJ; otherwise, LFM• The tender offer

– Tender offer to expire after 20 days, but extension is allowed:• Unilaterally by Credit Suisse, under certain circumstances• By agreement between DLJ & Credit Suisse

– Credit Suisse unilaterally invoked a five-day extension– DLJ & Credit Suisse agree on additional 22-day extension

• The lawsuit– Tooley (former DLJ SH) challenges a 22-day extension of the tender offer– He doesn’t challenge the fairness of the price, but demands (as damages for an

allegedly unlawful extension) the interest he would have received had the tender offer closed 22 days earlier

© Amitai Aviram. All rights reserved.14

Economics of class actionsWho is behind derivative actions?

• Why does Tooley bother suing?– Interest rate Tooley could have received on his money in Oct.-Nov. 2000: 6.55%

[Avg. interest rate on a 1-month CD in October 2000]• For 22 days, this equals ~0.39%

– If Tooley had $10K DLJ stock, he’d sue for $39.48• Would you sue for that much?

– With $39.48 you can hire an experienced attorney (20+ yrs.) for 6 minutes, 14 seconds; or hire an inexperienced attorney (fresh out of law school) for 13’, 10” [03-04 Laffey Matrix, U.S. Attorney’s Office, District of Columbia]

• Who has the incentive to initiate this lawsuit?• Conclusion: class actions mitigate a collective action problem among

plaintiffs at the cost of creating an agency problem for those plaintiffs– In the corporate law context, it reduces SH vs. management agency costs but

creates SH vs. lawyer agency costs

© Amitai Aviram. All rights reserved.15

Economics of class actionsDysfunctional outcomes

• In re Oracle Corp. Derivative Litigation [Cal. Super. 2005]– Larry Ellison, CEO of software giant Oracle Corp., allegedly

engaged in insider trading, selling some Oracle shares while he knew non-public, disappointing information about Oracle (which ultimately resulted in a 22% drop in share price)

– Joseph Tobacco Jr., a lawyer, brings a class action in California on behalf of Oracle SHs. The settlement:

• Ellison promises to donate $100M over five years, in Oracle’s name, to a charity of Ellison’s choice

– Ellison had already been donating over $30M a year• Oracle will pay Tobacco’s legal fees of $22.5M

– Benefit to Oracle SHs from this settlement?

© Amitai Aviram. All rights reserved.16

Economics of class actionsDysfunctional outcomes

• In re Oracle Corp. Derivative Litigation (cont’d)– WSJ, quoting Joseph Tobacco: “The settlement is a ‘very fair

result’ because it shined a light on Mr. Ellison’s conduct… the company has already determined that corporate giving benefits shareholders, and the settlement lets them make the donations using someone else’s money.”

– Settling derivative actions is subject to a judge’s approval• Why would a judge approve a settlement like this one?

– Outcome: In Nov. 2005, a San Mateo Superior Court judge approved the settlement, but only after it was modified so that Ellison, rather than Oracle, paid Tobacco’s legal fees.

© Amitai Aviram. All rights reserved.17

Economics of class actionsDysfunctional outcomes

• Why do we see these dysfunctional outcomes?– Guilty defendants may “bribe” plaintiff’s lawyer

to extinguish a meritorious suit

– Innocent defendants may be extorted byplaintiff’s lawyer to extinguish a frivolous suit

• Recall Lynn vs. Liam hypo earlier in this section

– Good faith plaintiff’s lawyer mayhave preferences that do notrepresent most SHs’ preferences

• Explained in next slide

© Amitai Aviram. All rights reserved.18

Economics of class actionsDysfunctional outcomes

• Example of the unrepresentative plaintiff problem– Assume that Oracle can extract $100 million from Ellison in

settlement of the derivative suit– Plaintiff SH believes in corporate philanthropy & would like to see

Oracle donate $100M to charity– However, most SHs want Oracle to use the $100M to develop new

software, or distribute it as dividends– Problem: SH bringing the derivative suit may not be

representative of most SHs’ preferences

© Amitai Aviram. All rights reserved.19

• Litigation (sue the lawyers if they do not represent faithfully)– SHs won’t sue; decision to sue lawyers suffers from same collective action

problem that justified having class actions in the first place• Exit (allow dissenting SHs not to participate in the suit)

– This is allowed in many class actions, but is not practical in derivative actions, where the issue is legal rights of the firm (any action the firm takes affects all SHs; can’t limit the impact to only some SHs)

• Voice (allow SHs to dismiss the suit)– SH review (SH meetings to decide whether to pursue each suit)?

• Not feasible: very costly, so extortion problem may become worse

• Compromise solution: BoD review (acting as a representative of SHs)– If BoD finds that a derivative suit is not justified & decision is protected by BJR,

it is an indicator that it is not in the firm’s interest to pursue the suit– But SH, not BoD, initiates the suit, so a process (called a demand on the board)

is needed to facilitate BoD review:• Alert BoD to plaintiff’s allegations• Allow BoD to make a business judgment whether firm should sue

Economics of class actionsAgency solutions in SH litigation

© Amitai Aviram. All rights reserved.20

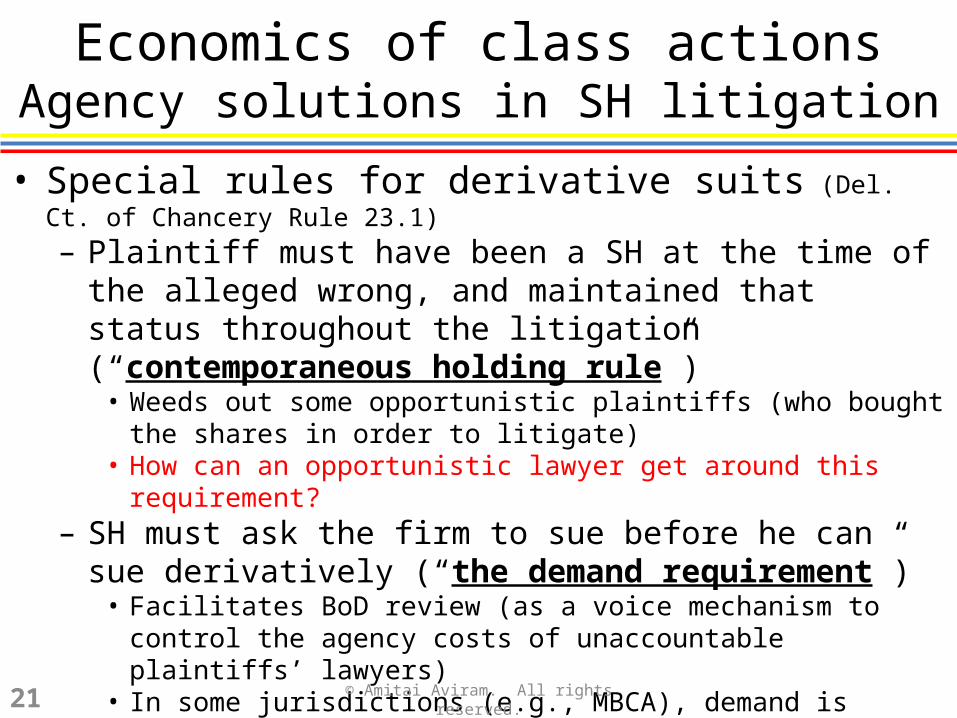

Economics of class actionsAgency solutions in SH litigation

• Special rules for derivative suits (Del. Ct. of Chancery Rule 23.1)– Plaintiff must have been a SH at the time of the alleged wrong,

and maintained that status throughout the litigation (“contemporaneous holding rule”)

• Weeds out some opportunistic plaintiffs (who bought the shares in order to litigate)

• How can an opportunistic lawyer get around this requirement?– SH must ask the firm to sue before he can sue derivatively (“the

demand requirement”)• Facilitates BoD review (as a voice mechanism to control the agency costs of

unaccountable plaintiffs’ lawyers)• In some jurisdictions (e.g., MBCA), demand is universal (must always be

made); in other jurisdictions (e.g., Delaware), demand is excused when it is futile – the differences will be explored later

© Amitai Aviram. All rights reserved.21

Shareholder litigationOverview of Section 3b

1. Litigation concepts2a. Derivative actions

– Legal personality & litigation– Is the action derivative?– Demand

2b. Derivative actions (continued)– Special litigation committees

3. SH inspection rights

© Amitai Aviram. All rights reserved.22

Derivative actionsLegal personality & litigation

• Charlie, a widower, gets run over by Tanya– He refuses to sue Tanya because of his infatuation with

her, but his injuries cause him financial hardship• He tells his daughter, Sarah, that he will not be able to pay

her college tuition– Can Sarah sue Tanya for the loss

of her father’s financial support?

© Amitai Aviram. All rights reserved.23

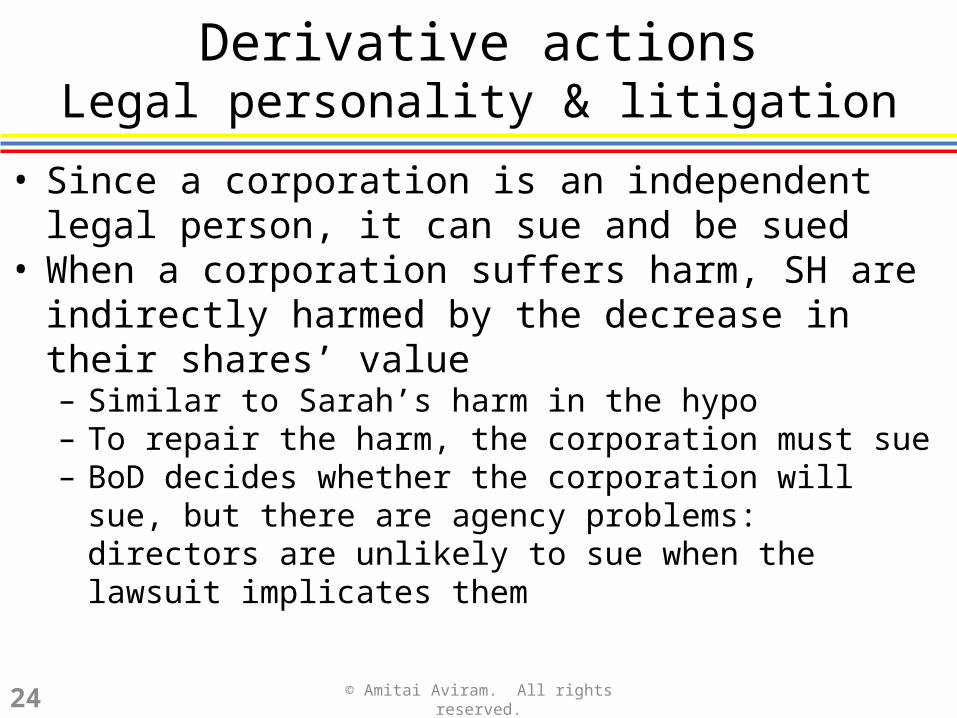

• Since a corporation is an independent legal person, it can sue and be sued

• When a corporation suffers harm, SH are indirectly harmed by the decrease in their shares’ value– Similar to Sarah’s harm in the hypo– To repair the harm, the corporation must sue– BoD decides whether the corporation will sue, but there are

agency problems: directors are unlikely to sue when the lawsuit implicates them

Derivative actionsLegal personality & litigation

© Amitai Aviram. All rights reserved.24

Derivative actionsLegal personality & litigation

• Agency problem with firm’s causes of action – hypo– Danny, David and Dana, C Corp.’s three directors, embezzle $1

million from C Corp.’s treasury• Steve, a SH, wants to sue the directors• Does he have a cause of action against the directors?

– Steve writes an angry letter to the corporation, demanding that it sue its directors

• BoD convenes to decide on Steve’s request & votes 3-0 not to sue• Can’t SHs just vote the directors out?• Can Steve do something against the directors?

© Amitai Aviram. All rights reserved.25

Derivative actionsLegal personality & litigation

• Modified hypo– C Corp. has two classes of shares:

• A shares are entitled to one vote & one share of the profits• B shares are entitled to one vote & ten shares of the profits

– The three directors do not embezzle money from the corporation. Instead, they reconfigure the rights of B shares so that each provides only two shares of the profits.

• Steve, a B SH, wants to sue the directors• Did this change harm the corporation?• Did it harm class B SHs?• Does Steve have a cause of action against the directors?

© Amitai Aviram. All rights reserved.26

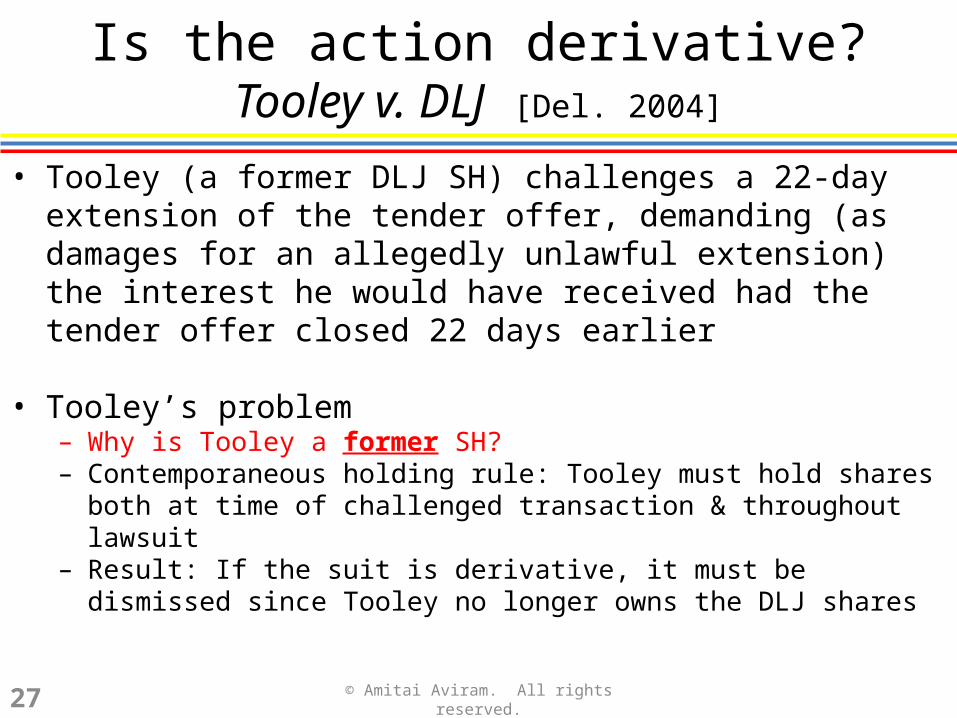

Is the action derivative?Tooley v. DLJ [Del. 2004]

• Tooley (a former DLJ SH) challenges a 22-day extension of the tender offer, demanding (as damages for an allegedly unlawful extension) the interest he would have received had the tender offer closed 22 days earlier

• Tooley’s problem– Why is Tooley a former SH?– Contemporaneous holding rule: Tooley must hold shares both at time of

challenged transaction & throughout lawsuit– Result: If the suit is derivative, it must be dismissed since Tooley no longer

owns the DLJ shares

© Amitai Aviram. All rights reserved.27

Is the action derivative?Tooley v. DLJ

• Del. Ch. Court Rule 23.1: “In a derivative action brought up by 1 or more shareholders… to enforce a right of a corporation…”– A suit is derivative when the cause of action belongs to the firm; but how do

we know if a cause of action belongs to the firm or the SHs?• Tooley court rejects two old tests:

– Whether there was a “special injury” suffered only by some SHs (Lipton)– Presumption that claim is derivative if it affects all SH equally (Bokat)

• Tooley test – whether suit is derivative or direct is based on:– Who suffered the alleged harm – corporation or plaintiff SH individually?– Who would receive the benefit of recovery or other remedy?

• Agostino v. Hicks is endorsed by the Tooley court– “Looking at the body of the complaint and considering the nature of the wrong

alleged and the relief requested, has the plaintiff demonstrated that he or she can prevail without showing an injury to the corporation?”

© Amitai Aviram. All rights reserved.28

Is the action derivative?Tooley v. DLJ

• Applying the Tooley test to the DLJ situation– Court: The complaint does not state a derivative action, because it

does not show how DLJ suffered an injury– However, claim is not direct either, because Tooley had no

contractual right to be paid on Oct. 5 rather than Nov. 2– Result: Complaint states no claim at all – neither direct nor

derivative. Dismissal was proper, but on different grounds than the Chancery Court stated.

© Amitai Aviram. All rights reserved.29

Is the action derivative?Who can sue derivatively? (In Del.)

• Common SHs - Yes• Preferred SHs – Yes, unless this right was specifically limited in

charter or another “appropriate document” [Maginn (Del. Ch. 2010)]• Creditors [Gheewalla (Del. 2007)]

– Yes, when firm is insolvent– Unclear, when firm is in the “zone of insolvency”– No, in all other situations

• Directors – No (though courts may allow in future if needed to prevent “complete failure of justice”) [Schoon (Del. 2008)]

© Amitai Aviram. All rights reserved.30

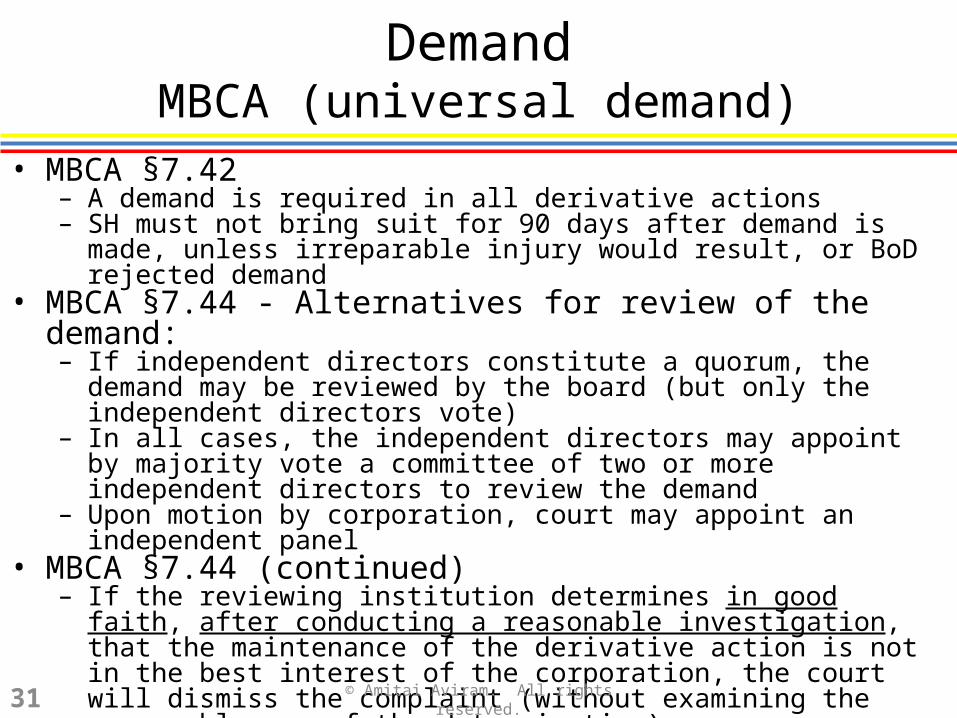

DemandMBCA (universal demand)

• MBCA §7.42– A demand is required in all derivative actions– SH must not bring suit for 90 days after demand is made, unless irreparable

injury would result, or BoD rejected demand• MBCA §7.44 - Alternatives for review of the demand:

– If independent directors constitute a quorum, the demand may be reviewed by the board (but only the independent directors vote)

– In all cases, the independent directors may appoint by majority vote a committee of two or more independent directors to review the demand

– Upon motion by corporation, court may appoint an independent panel• MBCA §7.44 (continued)

– If the reviewing institution determines in good faith, after conducting a reasonable investigation, that the maintenance of the derivative action is not in the best interest of the corporation, the court will dismiss the complaint (without examining the reasonableness of the determination)

– Burden of proof as to good faith and reasonable investigation lies on:• SH, if majority of BoD is independent, or review was by court appointed panel• Corporation, if majority of BoD is not independent

© Amitai Aviram. All rights reserved.31

DemandDelaware

• Delaware has a narrower demand requirement: Where the directors cannot be expected to make a fair decision, demand would be futile and is excused

• If a demand was made, the directors may reach a decision whether the company should pursue the cause of action– This is a BoD decision, so BJR applies unless rebutted

© Amitai Aviram. All rights reserved.32

DemandDelaware: litigation strategy

• Under Del. law, demand must be made unless it is futile– Making a demand is deemed a concession that a demand was

required• If demand is made, BoD’s decision regarding the demand

benefits from the BJR, unless it is rebutted– At this point, plaintiff isn’t entitled to discovery, so info on firm

must come from public sources & SH inspection rights– Why is this important?

• Result: Plaintiff usually loses if demand was made & BoD rejected it

© Amitai Aviram. All rights reserved.33

DemandDelaware: litigation strategy

• Harm to plaintiff from foregoing demand?– If demand is required & plaintiff does not make the demand, it is

not fatal to plaintiff’s case; litigation will be stayed while plaintiff makes the demand

• Can BoD benefit from BJR when no demand is made?– BoD needs to reach affirmative decision to benefit from BJR.

Suppose it meets, discusses the cause of action the plaintiff is expected to raise, and dismisses it.

– What should plaintiff do to sidestep BJR?• Conclusion: Typically, a plaintiff will not make a demand,

and instead argue that demand was excused– Shifts the litigation from whether demand was wrongfully

rejected, to whether it was futile

© Amitai Aviram. All rights reserved.34

DemandDelaware: demand excusal

• Primary test: Aronson v. Lewis [Del. 1984]: Demand requirement is excused if plaintiff shows reasonable doubt that either:– Majority of BoD is independent for purpose of responding to the

demand (@ time complaint is filed)– Challenged action is protected by the BJR

• Alternative test: Rales v. Blasband [Del. 1993]: test includes only 1st prong (BoD independence in responding to demand); applies when:– P’s claim arises out of BoD inaction– P’s claims arise out of transaction not involving BoD decision– A majority of directors that decided on underlying transaction was

replaced by independent directors

© Amitai Aviram. All rights reserved.35

DemandDelaware: demand excusal

• Beam v. Stewart (Del. 2004): “To create a reasonable doubt as to an outside director’s independence, a plaintiff must plead facts that would support the inference that… the non-interested director would be more willing to risk his or her reputation than risk the relationship with the interested director.”

• A director is not independent if she:– has a material interest in the challenged transaction; or– is dominated/controlled by the alleged wrongdoer or an interested party

• A director may be independent even if she:– approved the challenged transaction;– was named as a defendant in the derivative action; or– was nominated by the alleged wrongdoer

• In Beam, Martha Stewart controlled 94% of MSO, but in itself this did not create a reasonable doubt regarding the directors’ independence

© Amitai Aviram. All rights reserved.36

DemandZucker v. Andreessen [Del. Ch. 2012]

• Actress Jodie Fisher accuses Hewlett-Packard CEO Mark Hurd of sexual harassment, falsifying expense reports & disclosing sensitive information

• BoD investigates, finds evidence of falsifying reports (but notharassment); decides to fire Hurd

© Amitai Aviram. All rights reserved.37

DemandZucker v. Andreessen

• Severance agreement gives Hurd $40M in benefits (more than HP was obligated to give if he resigned or was fired for cause)

• Severance agreement requires Hurd:– to extend provisions in Hurd’s earlier confidentiality agreements– to release any claims he has against HP– not to disparage HP– to cooperate with HP re future investigations & CEO succession

• BoD appoints CFO as interim CEO; begins CEO search• Zucker, a SH, sues derivatively, alleging that BoD:

– committed waste in awarding Hurd $40M while HP received no benefit– breached duty of care in failing to implement CEO succession plan

• No demand was made, so Zucker needs to show demand was excused or the suit will be dismissed

• Does Aronson or Rales apply to each of these claims:– committing waste in awarding Hurd $40M while HP received no benefit?– breaching duty of care in failing to implement CEO succession plan?

© Amitai Aviram. All rights reserved.38

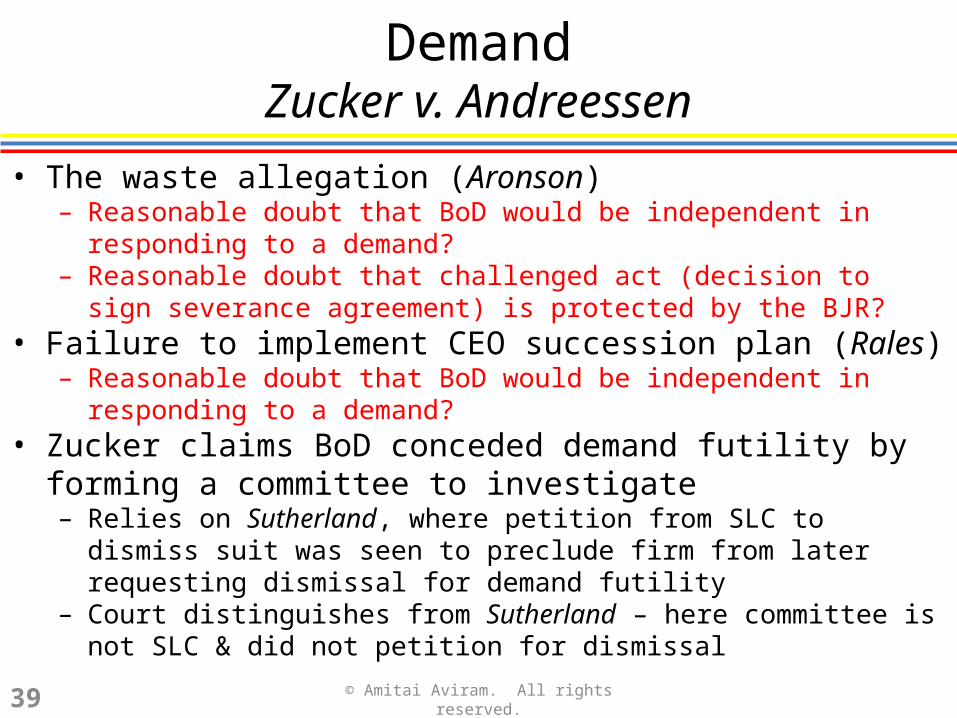

DemandZucker v. Andreessen

• The waste allegation (Aronson)– Reasonable doubt that BoD would be independent in responding to a demand?– Reasonable doubt that challenged act (decision to sign severance agreement) is

protected by the BJR?• Failure to implement CEO succession plan (Rales)

– Reasonable doubt that BoD would be independent in responding to a demand?• Zucker claims BoD conceded demand futility by forming a committee

to investigate– Relies on Sutherland, where petition from SLC to dismiss suit was seen to

preclude firm from later requesting dismissal for demand futility– Court distinguishes from Sutherland – here committee is not SLC & did not

petition for dismissal

© Amitai Aviram. All rights reserved.39

Shareholder litigationOverview of Section 3b

1. Litigation concepts2a. Derivative actions

– Legal personality & litigation– Is the action derivative?– Demand

2b. Derivative actions (continued)– Special litigation committees

3. SH inspection rights

© Amitai Aviram. All rights reserved.40

Special litigation committeesVulnerability of biased boards

• Sometimes BoD must make a decision when a majority of directors is not independent– Hypo: Pepsi owns 99% of EuroPepsi (its bottler in Europe); all of EuroPepsi’s

directors are Pepsi employees– Pepsi & EuroPepsi sign deal that EuroPepsi pay Pepsi $10M/year for using

Pepsi’s trademark, secret formula & technical assistance– Pierre, a EuroPepsi MSH, sues derivatively, claiming that $10M is too high. Is

demand excused? If price is fair, can Pepsi be extorted by suing?• When a majority of the BoD is not independent:

– BJR rebutted (can’t trust BoD’s decision that derivative claim lacks merit)– But for that reason, firm is an attractive target for strike suits

• Solution: firm asks court to apply BJR (i.e., defer) to a decision of an SLC (composed of disinterested directors) that the derivative action lacks merit– Unlike demand futility litigation, in SLC litigation plaintiff is entitled to discovery

as to the independence of the SLC members

© Amitai Aviram. All rights reserved.41

Special litigation committeesDifferences between state laws

• Most states simply apply BJR analysis to SLC’s decision

• Delaware analyzes SLC decisions in 2 steps (Zapata Corp. v. Maldonado [Del. 1981])– Quasi-BJR analysis to SLC’s decision

• SLC independence• SLC good faith• Reasonable bases for the SLC’s recommendations

– Court may apply its own “independent business judgment” as to whether to dismiss the suit

© Amitai Aviram. All rights reserved.42

Special litigation committeesIn re Oracle Deriv. Litig. [Del. Ch. 2003]

• Plaintiffs allege that four directors of Oracle – Ellison, Henley, Lucas and Boskin - engaged in insider trading

• Upon being sued, Oracle appoints an SLC of two new directors (weren’t on BoD when alleged events took place)– Garcia-Molina: chairman of Stanford’s computer science department– Grundfest: professor at Stanford law school

• Directs Stanford’s director college & the program in law, business and corporate governance. Is this a coincidence?

• Why does the BoD appoint an SLC rather than reach a business decision itself?

© Amitai Aviram. All rights reserved.43

Special litigation committeesOracle

• Compensation: $250/hour (below their market price)– To preserve their objectivity, SLC members agreed to give up

compensation if court determined that it impaired their impartiality• Advisors’ objectivity

– The SLC hires legal counsel (Simpson Thacher) & economists (NERA). Court examines the advisors’ objectivity and finds no problem.

– What evidence would taint the advisors’ objectivity?• SLC’s report

– SLC interviewed 70 witnesses. Its report was 1,110 pages long. Court finds no problems with the SLC’s investigation procedure

– SLC recommends to dismiss the claims

© Amitai Aviram. All rights reserved.44

Special litigation committeesOracle

Legal analysis (Zapata)

• Step 1: Quasi-BJR analysis– SLC members’ independence

– SLC members’ good faith

– Reasonable bases for the SLC’s recommendations

• Step 2: “Independent business judgment”

© Amitai Aviram. All rights reserved.45

Special litigation committeesOracle

Ellison

Boskin

Lucas

Garcia-Molina

Grundfest

SLC members’ independence

What the SLC report disclosed:• Boskin is a Stanford Professor

• Lucas made certain donations to Stanford, and donated $50,000 to after Grundfest delivered a speech to a Venture Capital Fund in which Lucas’ son is a partner (half the money went to Grundfest’s research account)

© Amitai Aviram. All rights reserved.46

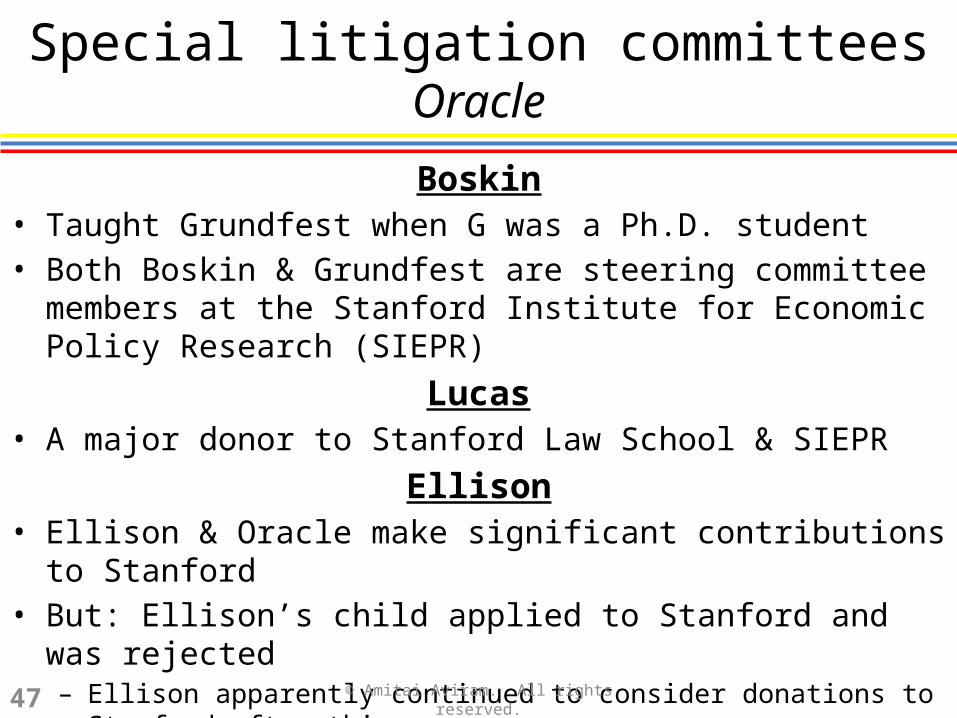

Special litigation committeesOracle

Boskin• Taught Grundfest when G was a Ph.D. student• Both Boskin & Grundfest are steering committee members at the

Stanford Institute for Economic Policy Research (SIEPR)Lucas

• A major donor to Stanford Law School & SIEPREllison

• Ellison & Oracle make significant contributions to Stanford• But: Ellison’s child applied to Stanford and was rejected

– Ellison apparently continued to consider donations to Stanford after this

© Amitai Aviram. All rights reserved.47

Special litigation committeesComparing Beam & Oracle

• Why is the analysis and outcome different?

Beam: “…for presuit demand purposes, friendship must be accompanied by substantially more…”

Oracle: “Homo sapiens is not merely homo economicus… an array of other motivations exist to influence human behavior… envy… love, friendship, and collegiality.”

© Amitai Aviram. All rights reserved.48

Shareholder litigationOverview of Section 3b

1. Litigation concepts2a. Derivative actions2b. Derivative actions (continued)3. SH inspection rights

© Amitai Aviram. All rights reserved.49

SH inspection rightsPurposes

• SH inspection rights can:– Facilitate SH voting: getting non-public information that will

persuade SHs to support an insurgent in proxy contest (e.g., uncovering info that shows the BoD did a poor job managing the firm, and should not be re-elected)

– Facilitate SH litigation: getting non-public information that sufficiently substantiates allegations that the complaint survives a motion to dismiss

• Why not give SH an automatic right to access all of the corporation’s info?

© Amitai Aviram. All rights reserved.50

SH inspection rightsDGCL

• Proper purpose (DGCL §220(b))– SH must make a written demand, presenting a “proper purpose”

(i.e., a purpose “reasonably related to such person’s interest as a stockholder”)

• BoP as to whether purpose is proper (DGCL §220(c))– If SH seeks access to the SH list, BoP on the firm to show that SH

does not have a “proper purpose”– If SH seeks access to other corporate records, BoP on the SH to

prove “proper purpose”

© Amitai Aviram. All rights reserved.51

SH inspection rightsPershing Square v. Ceridian [Del. Ch. 2007]

• Pershing Square, a hedge fund, is Ceridian’s largest SH (11.3%). Ackman is its portfolio manager.

• Comdata is Ceridian’s largest operating subsidiary. Krow is Comdata’s president.

• Ackman learns that Krow sold Ceridian stock. He calls Krow to learn why.– How does Ackman know about Krow’s sale of stock?

© Amitai Aviram. All rights reserved.52

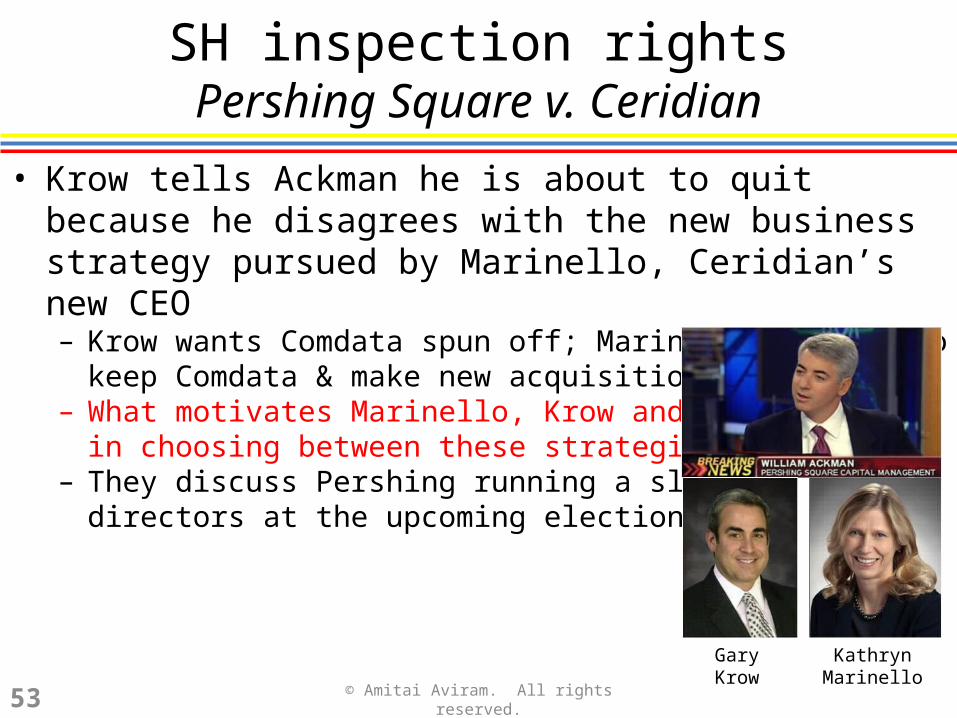

SH inspection rightsPershing Square v. Ceridian

• Krow tells Ackman he is about to quit because he disagrees with the new business strategy pursued by Marinello, Ceridian’s new CEO– Krow wants Comdata spun off; Marinello prefers to keep Comdata &

make new acquisitions– What motivates Marinello, Krow and Ackman

in choosing between these strategies?– They discuss Pershing running a slate of

directors at the upcoming elections

GaryKrow

Kathryn Marinello

© Amitai Aviram. All rights reserved.53

SH inspection rightsPershing Square v. Ceridian

• Krow meets with Ackman at an airport– Tells Ackman which Ceridian SHs supported a Comdata spin-off and

would support PS’s director slate– Also tells Ackman that he wrote two letters to Ceridian’s BoD, detailing

mismanagement by the previous Ceridian CEO & hinting that the BoD’s failed to oversee the CEO

– How is the info useful for Pershing’s bid to elect directors?• CEO was terminated & replaced by Marinello, but Krow thinks

that the letters damaged his relationship with the BoD & Marinello was hired with the intention of firing Krow

© Amitai Aviram. All rights reserved.54

SH inspection rightsPershing Square v. Ceridian

• Pershing makes a DGCL §220 demand to:– Inspect SH list materials– Receive a copy of Ceridian’s current bylaws– Receive copies of the two letters Krow mentioned

• What purposes does Pershing cite?• Ceridian provides bylaws & SH list, but

refuses to provide copies of the letters– Claims confidentiality & lack of proper purpose

• Pershing already knows what’s in the letters– Why does Pershing need to get the letters from Ceridian?

© Amitai Aviram. All rights reserved.55

SH inspection rightsPershing Square v. Ceridian

• Court examines stated purposes• Legal standard: Purpose is proper if it is reasonably related to

one’s interest as a stockholder– Investigating suitability of directors– Communicating with fellow shareholders re BoD elections

• Ceridian: This would make every board-level document available for inspection– Court: stating a proper purpose does not automatically grant

inspection rights

© Amitai Aviram. All rights reserved.56

SH inspection rightsPershing Square v. Ceridian

• Court: conditions for SH inspection right– SH’s true/primary purpose must be a proper purpose– SH must have evidence establishing credible basis for that

purpose– SH must show that requested info is necessary & essential for

that purpose– Court may impose safeguards to protect confidential

communications• In this case:

– Pershing’s stated purposes are proper– But Pershing’s true purpose is improper: finding a legal vehicle to

publicly broadcast improperly obtained confidential information

© Amitai Aviram. All rights reserved.57