37

Business Case June 1993

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | alan-williamson |

| View: | 216 times |

| Download: | 1 times |

Business Case

June 1993

Presentations 04/19/23 @ 13:36 - 2 -

BUSINESS CASE

Content

• Objective

• Approach and Assumptions

• Project Impact

– Quantifiable benefits

· Revenue enhancement

· Cost reduction

· Asset reduction

– Non- quantifiable benefits

– Intangible benefits

• Appendix

Presentations 04/19/23 @ 13:36 - 3 -

BUSINESS CASE

Objective

To begin to estimate the timing and sequence of benefits during implementation

To establish a logical business justification for change

To create a rationale for making the tough decisions and staying on track after the emotion of discovery has worn off and the challenges of implementation set in

Presentations 04/19/23 @ 13:36 - 4 -

BUSINESS CASE

Approach and Assumptions

The goal is to overachieveThe goal is to overachieve

• Financial information was gathered from

– 1988 to 1992 Budgets

– 1988 to 1992 Financial Reports (Actuals)

– 1993 YTD Financial Report

– 1993 Budget

• Benefits are quantified conservatively by design

• Margin for revenue enhancement opportunities is 40%

• Weighted average cost of capital is assumed to be 18%

• Benefits include U.S. and W.R.C. only and does not include Seeds or Canada

Presentations 04/19/23 @ 13:36 - 5 -

BUSINESS CASE

The Project will yield Quantifiable, Non-quantifiable and Intangible Benefits

Asset Reduction Margin Contribution

Cost Reduction

CarryingCosts

LowerAccountsreceivable

Finished Goods Inventory

DealerInventory

Improved Productivityfrom effective

teamwork

Strategic Value Of PD&I

WIP & Finished Goods Inventory

CustomerFocus

EmployeeMorale

Intangible

ReducedFrustration

ProductFocus Improved

Team work Culture

Customersatisfaction

Raw Material Inventory

Maintenance Productivity SAP Implementation

Sales Productivity

ManufacturingProductivity

Enhanced Revenue

MaintenanceSupplies

Procurement PD&I and Customer Service

Rework

Qua

ntifi

ed

Non-

QuantRevenuesassociatedwith cycle time reduction

Presentations 04/19/23 @ 13:36 - 6 -

BUSINESS CASE

Asset Reduction Benefits Come From Reduced Plant And Finished Goods Inventory and Amount To $49 Million

• Cold Creek $6.2 M– Raw– WIP– Maintenance

• Bayport $0.9 M– Raw– Maintenance

• Omaha $1.2 M– WIP– Maintenance

• St. Gabriel $0.7 M

– WIP

• Reduction in Finished Goods Inventory $40.0 M

Total Asset Reduction Benefit $ 49.0 M

Verified by Larry Lapple, Joe Gallagher and Jim Wissmiller

Presentations 04/19/23 @ 13:36 - 7 -

BUSINESS CASE

Cost Reduction Benefits Come From Several Areas And Range From $18 Million to $25 Million

Manufacturing - Productivity Improvement

Market Impact - Carrying cost of FG Inventory and faster title transfer

PD&I - Reducing backup projects, formulation tests

Order processing - Containers, sub optimal shipping

S.A.P. & I.T. - Productivity

Infrastructure - Productivity

Procurement - Process Improvement

$1.4 M - $1.8 M

$8.6 M - $10.0 M

$1.3 M

$0.6 M

$1.7 M

$1.0 M - $1.3 M

$4.1 M - $8.5 M

$18.7 M - $25.2 MTotal Cost Reduction Benefit

Verified by Joe Gallagher, Joe Powell, Larry Lapple, Carol Johnson, Al Willard, and Stanley Oliver

Presentations 04/19/23 @ 13:36 - 8 -

BUSINESS CASE

Quantification of Potential Sales Revenue From all Activities

1994 vs. 93 1995 vs. 93

RevenueIncrease (budget)

+$64M +$135M

Target AmountBelieved Possible

$100M $150M

Net Incremental RevenuePotential From:

(At 40% Margin)• Increased volume of ‘Force’• Increased volume of ‘Reflex’• Additional TSR’s• 20% TSR efficiency increase• ‘Karate’ labels• Re-engineering• Other registration• Sales tools

$14M $6M

$36M $15M

Verified by Keelan Pulliam (?) and Jim Wissmiller

Expected margin benefit = $0 - 20 MExpected margin benefit = $0 - 20 M

Presentations 04/19/23 @ 13:36 - 9 -

BUSINESS CASE

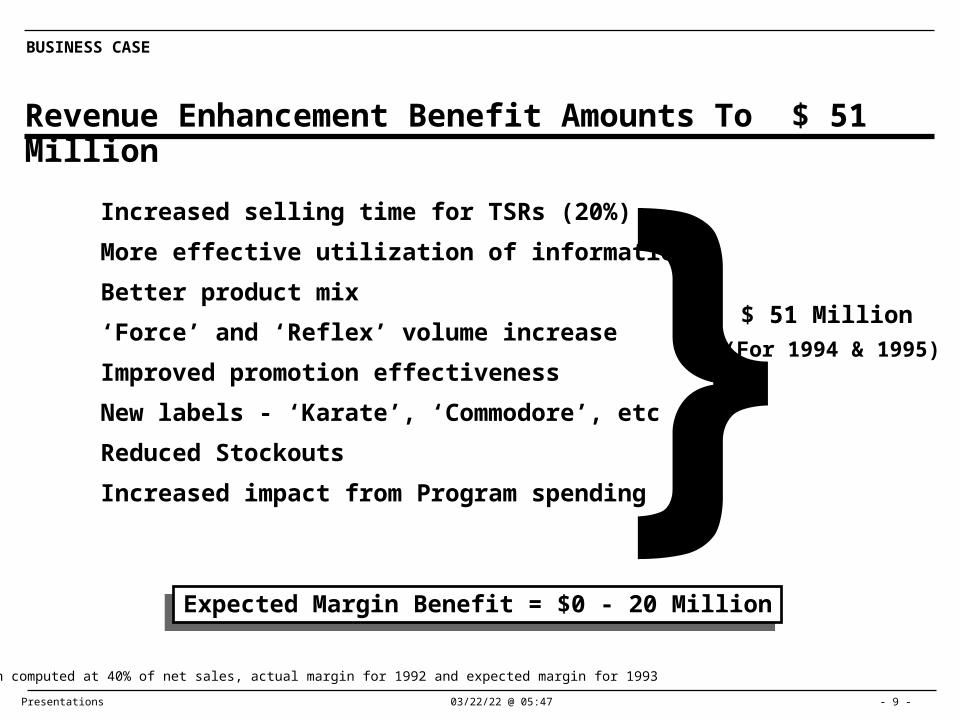

Revenue Enhancement Benefit Amounts To $ 51 Million

Increased selling time for TSRs (20%)

More effective utilization of information

Better product mix

‘Force’ and ‘Reflex’ volume increase

Improved promotion effectiveness

New labels - ‘Karate’, ‘Commodore’, etc

Reduced Stockouts

Increased impact from Program spending

Expected Margin Benefit = $0 - 20 MillionExpected Margin Benefit = $0 - 20 Million

Margin computed at 40% of net sales, actual margin for 1992 and expected margin for 1993

$ 51 Million}(For 1994 & 1995)

Presentations 04/19/23 @ 13:36 - 10 -

BUSINESS CASE

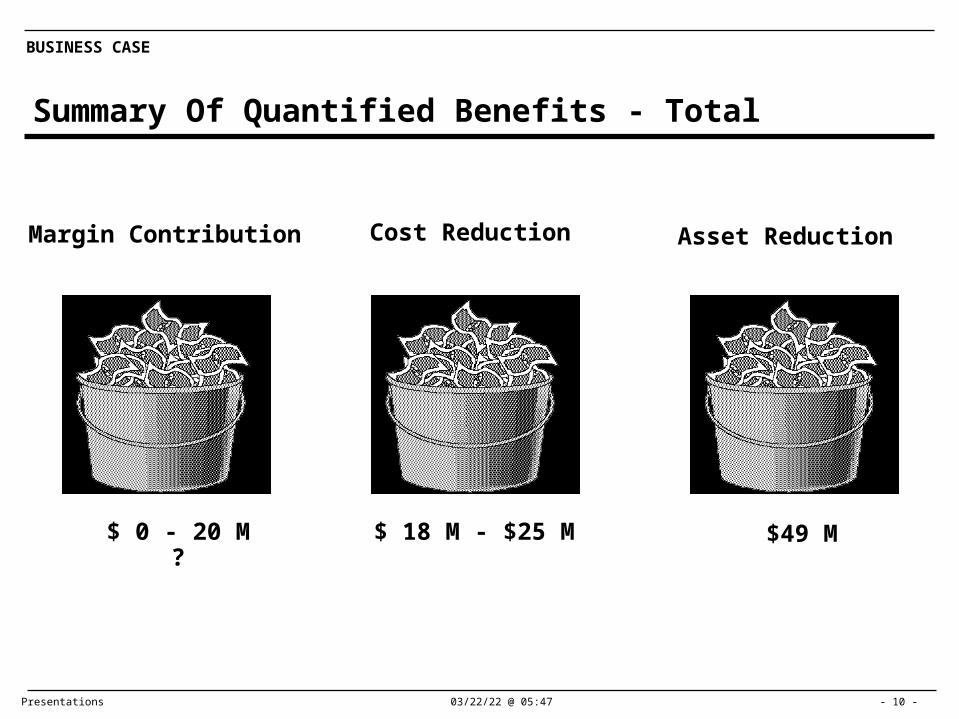

Summary Of Quantified Benefits - Total

Cost Reduction Asset ReductionMargin Contribution

$ 18 M - $25 M $49 M$ 0 - 20 M?

Presentations 04/19/23 @ 13:36 - 11 -

BUSINESS CASE

Quantified Benefits

Margin Contribution Target For 1994 & 1995 (Revenue enhancement - $51M)

Cost Reduction

Asset Reduction

U.S. U.K.

$ 0 - 20 M

$ 8 M - $14 M $ 10 - 11 M

$ 41 M $ 8 M

Presentations 04/19/23 @ 13:36 - 12 -

BUSINESS CASE

Non - Quantifiable Benefits (External Focus Benefits)

• Enhanced customer satisfaction

• Improved productivity from effective team work, communications

• Enhanced strategic value of Product Development

• Revenues associated with cycle time reduction and earlier time to market

• Better decision making from timely and effective information

• Focusing initiatives

Presentations 04/19/23 @ 13:36 - 13 -

BUSINESS CASE

Intangible Benefits (Internal Focus Benefits)

• Reduced frustration and complexity throughout the organization

• Ability to focus on customers and products

• Improved teamwork and cohesiveness of the executive management team

• Increased employee morale

• A foundation and beginning of a new culture

• Clearer roles / responsibilities, accountabilities and authority levels throughout the organization

• Effective and consistent decision making throughout all levels of the organization

• Motivation and movement in one clear strategic direction

Presentations 04/19/23 @ 13:36 - 14 -

BUSINESS CASE

0

20

40

60

80

100

1993 1994 1995

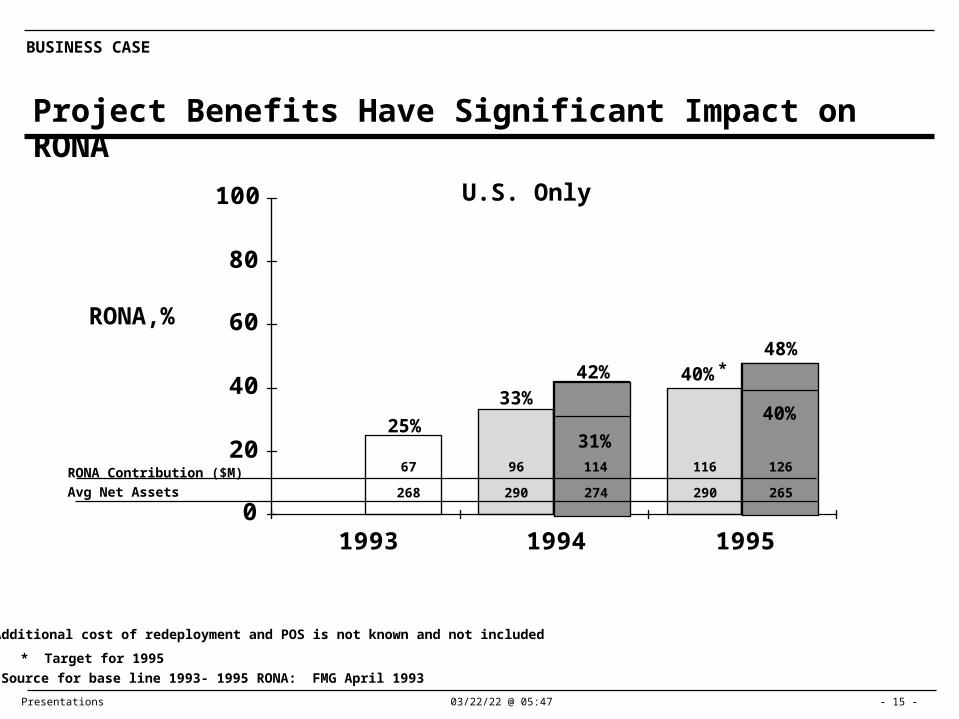

Project Benefits Have Significant Impact on RONA

* Target for 1995

Source for base line 1993- 1995 RONA: FMG April 1993

RONA Contribution ($M)

Avg Net Assets

RONA,%

25%

33%

45%40%

50%

Additional cost of redeployment and POS is not known and not included

*

Total

67

268

96

290

119

266

116

290

131

264

Presentations 04/19/23 @ 13:36 - 15 -

BUSINESS CASE

0

20

40

60

80

100

1993 1994 1995

Project Benefits Have Significant Impact on RONA

* Target for 1995

Source for base line 1993- 1995 RONA: FMG April 1993

RONA Contribution ($M)

Avg Net Assets

RONA,%

25%

33%42%

31%

40%48%

40%

Additional cost of redeployment and POS is not known and not included

*

U.S. Only

67

268

96

290

114

274

116

290

126

265

Presentations 04/19/23 @ 13:36 - 16 -

BUSINESS CASE

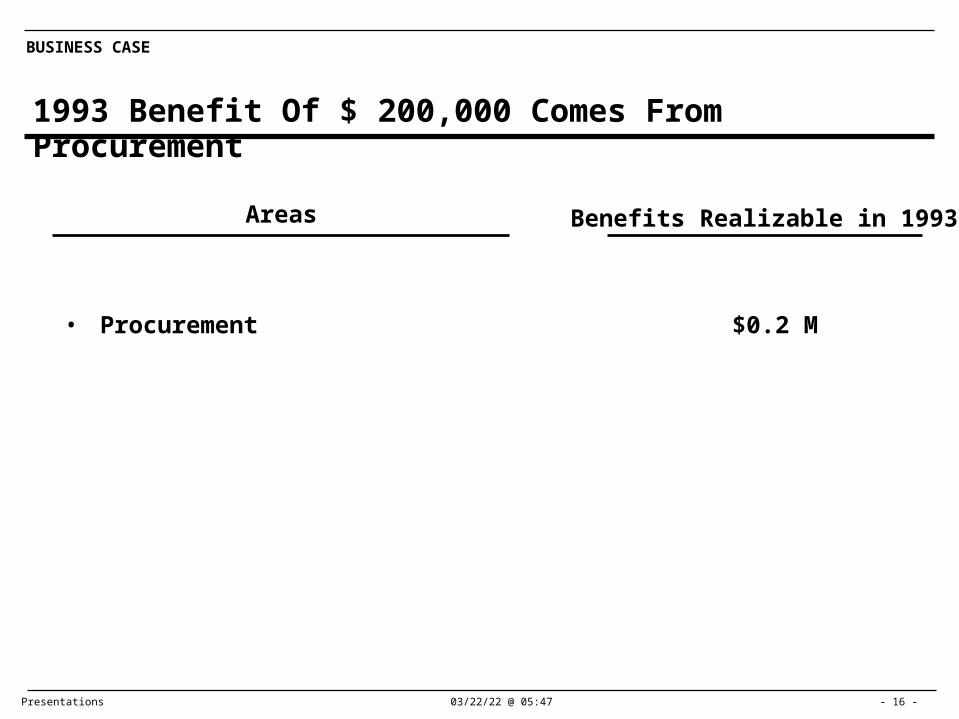

1993 Benefit Of $ 200,000 Comes From Procurement

• Procurement $0.2 M

Areas Benefits Realizable in 1993

Presentations 04/19/23 @ 13:36 - 17 -

BUSINESS CASE

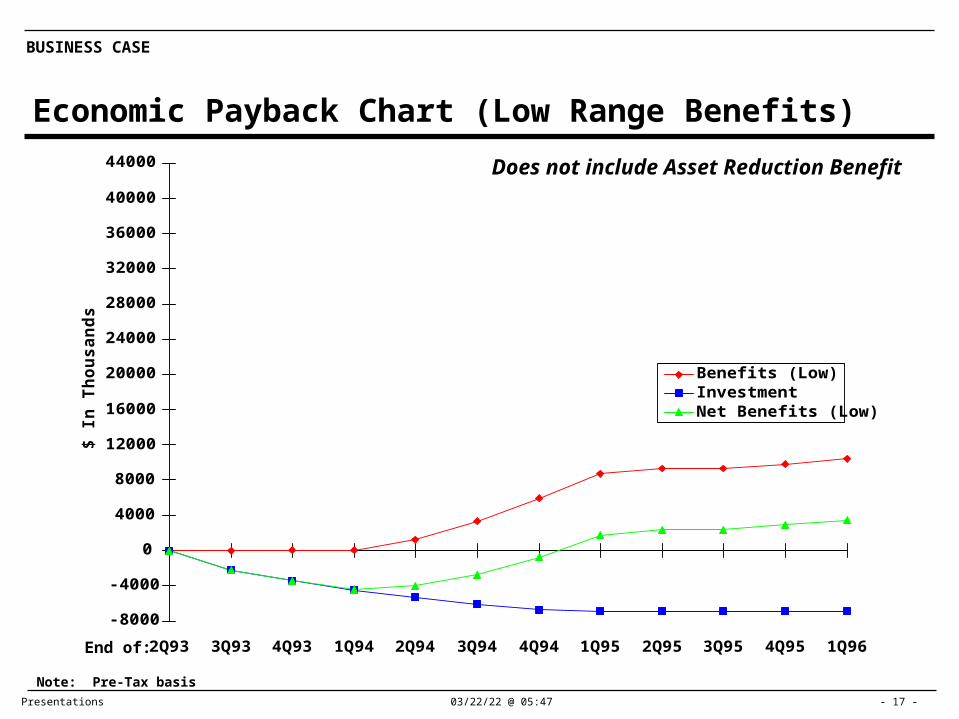

Economic Payback Chart (Low Range Benefits)$

In

Th

ou

sa

nd

s

-8000

-4000

0

4000

8000

12000

16000

20000

24000

28000

32000

36000

40000

44000

2Q93 3Q93 4Q93 1Q94 2Q94 3Q94 4Q94 1Q95 2Q95 3Q95 4Q95 1Q96

Benefits (Low)InvestmentNet Benefits (Low)

End of:

Note: Pre-Tax basis

Does not include Asset Reduction Benefit

Presentations 04/19/23 @ 13:36 - 18 -

BUSINESS CASE

Economic Payback Chart (High Range Benefits)$

In

Th

ou

sa

nd

s

-8000

-4000

0

4000

8000

12000

16000

20000

24000

28000

32000

36000

40000

44000

2Q93 3Q93 4Q93 1Q94 2Q94 3Q94 4Q94 1Q95 2Q95 3Q95 4Q95 1Q96

Benefits (High)InvestmentNet Benefits (High)

End of:

Note: Pre-Tax basis

Does not include Asset Reduction Benefit

Presentations 04/19/23 @ 13:36 - 19 -

BUSINESS CASE

Accounting Payback Chart (Low Range Benefits Without Interest)

$ In

Th

ou

sa

nd

s

-8000

-4000

0

4000

8000

12000

16000

20000

24000

28000

32000

36000

40000

44000

2Q93 3Q93 4Q93 1Q94 2Q94 3Q94 4Q94 1Q95 2Q95 3Q95 4Q95 1Q96

Benefits (Low)InvestmentNet Benefits (Low)

End of:

Note: Pre-Tax basis

Does not include Asset Reduction Benefit

Presentations 04/19/23 @ 13:36 - 20 -

BUSINESS CASE

Accouting Payback Chart (High Range Benefits Without Interest)

$ In

Th

ou

sa

nd

s

-8000

-4000

0

4000

8000

12000

16000

20000

24000

28000

32000

36000

40000

44000

2Q93 3Q93 4Q93 1Q94 2Q94 3Q94 4Q94 1Q95 2Q95 3Q95 4Q95 1Q96

Benefits (High)InvestmentNet Benefits (High)

End of:

Note: Pre-Tax basis

Does not include Asset Reduction Benefit

Presentations 04/19/23 @ 13:36 - 21 -

BUSINESS CASE

Project Investment

Professional fees $5.1 M

Expense $1.8 M

Total investment $6.9 M

Investment in Gemini

Presentations 04/19/23 @ 13:36 - 22 -

BUSINESS CASE

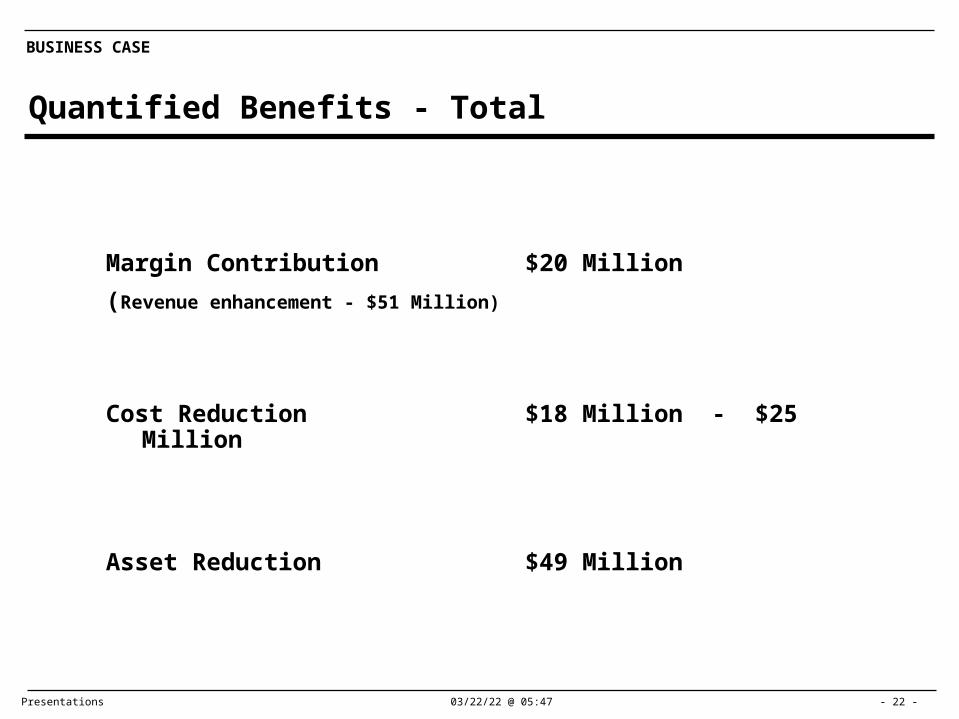

Quantified Benefits - Total

Margin Contribution $20 Million

(Revenue enhancement - $51 Million)

Cost Reduction $18 Million - $25 Million

Asset Reduction $49 Million

Presentations 04/19/23 @ 13:36 - 23 -

BUSINESS CASE

• Re-engineering benefits– Margin enhancement – 0-14.0 0-6.0 0-20.0– Cost reduction – 5.9-9.9 2.7-4.0 8.6–

13.9– 5.9-23.9 2.7-10.0 8.6-33.9

• Savings budgeted– Strategy (streamline) 0.5 4.0 – 4.0– Purchasing 0.5 1.4 – 1.4– Strategy (formulation) – 0.9 – 0.9– Woods, Pink agreement 0.2 0.2 – 0.2

1.2 6.5 – 6.5

• Re-engineering benefits– Asset reduction – 16.0 25.0 41.0

– 16.0 25.0 41.0• Savings budgeted

– Streamline 30 (ETR)* 10 (ETR) 10(ETR) 20 (ETR)

Reconciliation Of Benefits With Budget ($ in Millions)

Total

U.S. P&L Impact

U.S. B/S Impact

• ETR as of 1Q93

Note: Cummulative U.K. P&L impact of $10M - $11M and B/S impact of $8M is not recongized

Total

1993 1994 1995 Cumm

Total

Presentations 04/19/23 @ 13:36 - 24 -

BUSINESS CASE

• Re-engineering benefits– Margin enhancement – 0-14.0 0-6.0 0-20.0– Cost reduction – 10.0-15.4 8.5-9.8 18.6-25.2

– 10.0-29.4 8.5-15.8 18.5-45.2• Savings budgeted

– Strategy (streamline) 0.5 4.0 – 4.0– Purchasing 0.5 1.4 – 1.4– Strategy (formulation) – 0.9 – 0.9– Woods, Pink agreement 0.2 0.2 – 0.2

1.2 6.5 – 6.5

• Re-engineering benefits– Asset reduction – 24.0 25.0 49.0

– 24.0 25.0 49.0• Savings budgeted

– Streamline 30 (ETR)* 10 (ETR) 10(ETR) 20 (ETR)

Reconciliation Of Benefits With Budget - Total ($ in Millions)

Total

Total P&L Impact

Total B/S Impact

• ETR as of 1Q93

Total

1993 1994 1995 Cumm

Total

Presentations 04/19/23 @ 13:36 - 25 -

BUSINESS CASE

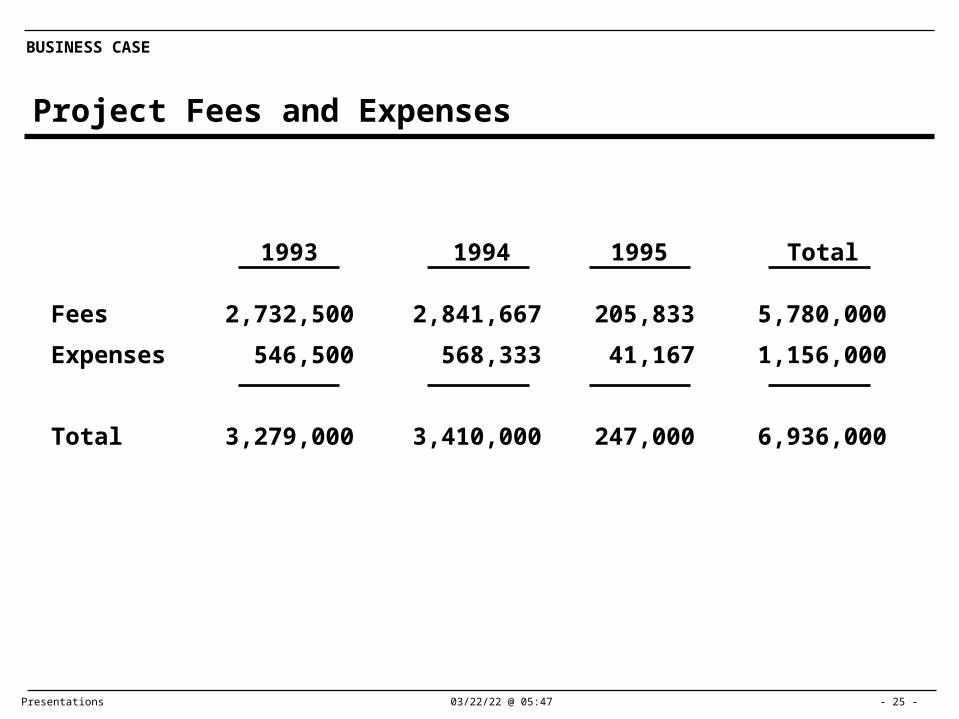

Project Fees and Expenses

Fees

Expenses

Total

2,732,500

546,500

3,279,000

2,841,667

568,333

3,410,000

205,833

41,167

247,000

5,780,000

1,156,000

6,936,000

1993 1994 1995 Total

Appendix

Presentations 04/19/23 @ 13:36 - 27 -

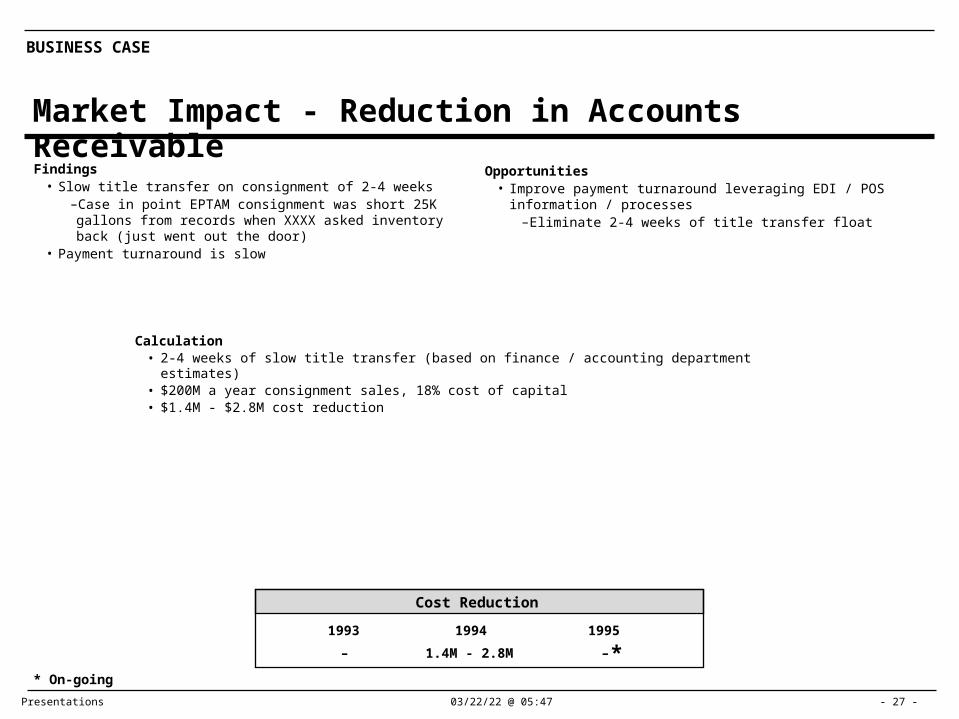

BUSINESS CASE

Market Impact - Reduction in Accounts Receivable

Calculation• 2-4 weeks of slow title transfer (based on finance / accounting department estimates)• $200M a year consignment sales, 18% cost of capital• $1.4M - $2.8M cost reduction

Findings• Slow title transfer on consignment of 2-4 weeks

–Case in point EPTAM consignment was short 25K gallons from records when XXXX asked inventory back (just went out the door)

• Payment turnaround is slow

Opportunities• Improve payment turnaround leveraging EDI / POS information /

processes–Eliminate 2-4 weeks of title transfer float

1.4M - 2.8M–

Cost Reduction

1994 19951993

– ** On-going

Presentations 04/19/23 @ 13:36 - 28 -

BUSINESS CASE

Market Impact - Revenue Enhancement

Calculation• TSR’s expect (sales survey) 12% sales increase based on 20% more selling time. $460M sales, yield $55M

sales increase• DSM expect $45M to $85M sales increase based on better targeting, optimized product mix, and automation.

$85M is best case estimate. $45M is average of best case and most likely and worst case ÷ 3• Industry report sales increase range of 10% - 25% based on POS implementation. $460M sales = $45M - $115M

sales increase

Findings• 60% of TSR’s felt they were not effectively focused on the most

attractive target groups• 73% of TSR’s felt that XXXX was not the superior performer in

delivering value to the market place• TSR’s expect 12% sales increase with more selling time• DSM expect sales increase of 10% - 18% with POS implementation

–Better targeting–Better product mix–Lower administration time

• XXXX can not measure impact of advertisements and promotions• XXXX does not have sufficient detailed product demand patterns• Sales reps and customers suggest that the dealer programs are

overly complex and diffused as an incentive

Opportunities• Focus for more selling time from sales force• Better, faster and more complete user information for targeting efforts• Optimize product mix• Fewer stockouts, product delays• Reallocation of program budgets• Improve promotion effectiveness• Improve product introduction effectiveness

Revenue Enhancement

1994 19951993

Rev. Increase

Margin Increase

* On-going

–

–

$32M

$13M

$19M

$7M

**

**

Presentations 04/19/23 @ 13:36 - 29 -

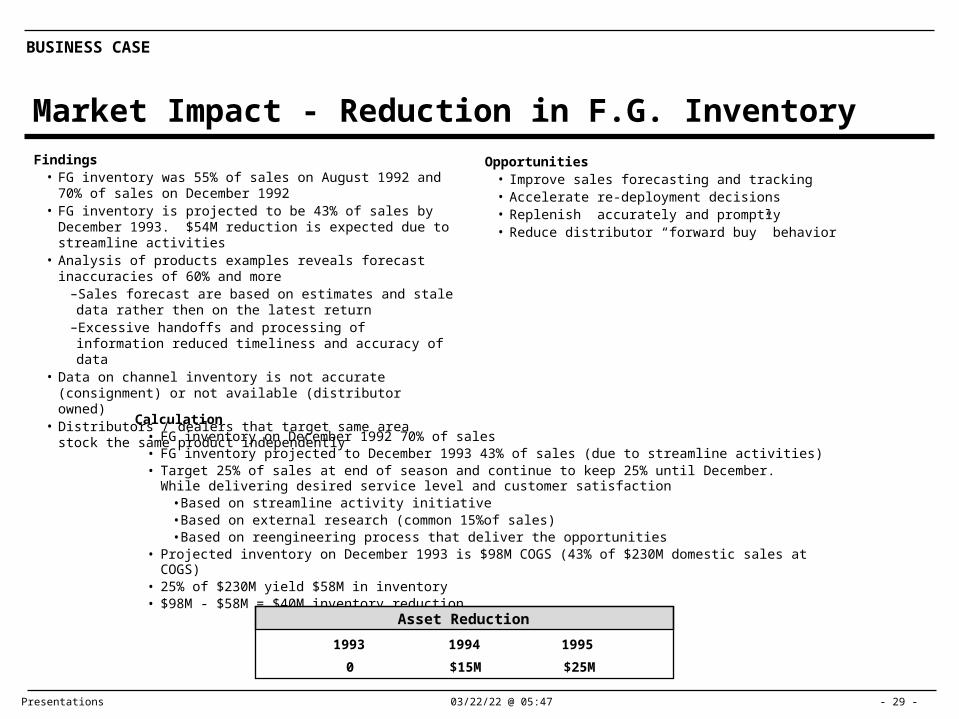

BUSINESS CASE

Market Impact - Reduction in F.G. Inventory

Calculation• FG inventory on December 1992 70% of sales• FG inventory projected to December 1993 43% of sales (due to streamline activities)• Target 25% of sales at end of season and continue to keep 25% until December. While delivering desired

service level and customer satisfaction• Based on streamline activity initiative• Based on external research (common 15%of sales)• Based on reengineering process that deliver the opportunities

• Projected inventory on December 1993 is $98M COGS (43% of $230M domestic sales at COGS)• 25% of $230M yield $58M in inventory• $98M - $58M = $40M inventory reduction

Findings• FG inventory was 55% of sales on August 1992 and 70% of sales

on December 1992• FG inventory is projected to be 43% of sales by December 1993.

$54M reduction is expected due to streamline activities• Analysis of products examples reveals forecast inaccuracies of

60% and more–Sales forecast are based on estimates and stale data rather then on the latest return

–Excessive handoffs and processing of information reduced timeliness and accuracy of data

• Data on channel inventory is not accurate (consignment) or not available (distributor owned)

• Distributors / dealers that target same area stock the same product independently

Opportunities• Improve sales forecasting and tracking• Accelerate re-deployment decisions• Replenish accurately and promptly• Reduce distributor “forward buy” behavior

Asset Reduction

$15M $25M0

1994 19951993

Presentations 04/19/23 @ 13:36 - 30 -

BUSINESS CASE

Market Impact – Inventory Carrying Cost of Reduced F.G. Inventory

Calculation• $40M inventory asset reduction, 18% cost of capital

Findings• XXXX finances the entire channel• Non selling activities account for 42% of TSR’s time• Main non selling activities

•Paper work•Program administration •Processing mail

• CSR spent significant time allocating inventory• CSR operates in crisis mode to satisfy customers on demanded

products while other products are idle (e.g., high inventory levels)• XXXX’s product portfolio is one of the largest, but individual product

profitability is the lowest of the major competitor’s• Product mix inaccuracies cause excessive rework• Product mix opportunities are significant in mature products (e.g.,

Eradicame, Dyfonate, Sutam)

Opportunities• Reduction in inventory carrying cost• Reduce admin expense associated with dealer programs• Reduce customer service expense• Rationalize product portfolio• Reduce rework

Cost Reduction

$2.7M $4.5M0

1994 19951993

Presentations 04/19/23 @ 13:36 - 31 -

BUSINESS CASE

Manufacturing - Plant Inventory

Calculation• Increase Cold Creek raw material turns from 13.4 to 20 ($5.2 - $3.6 = $1.6)• Decrease average work-in-process at St. Gabriel by 50% ($1.3 x 50.% = $0.7)• Increase Cold Creek work-in-process turns from 9.3 to 12 turns ($18.5 - $14.3 = $4.2)• Decrease Omaha work-in-process by 4 days supply (20% x $6.6 = $1.2)• Increase turns of viable maintenance parts inventory from 1.4 to 3 ($0.8 - $0.4 = $0.4)• Decrease Bayport safety stocks of Pyaidivc, Sodium, and MLCI by 10 days or $0.9 million

Findings• Low turns in raw material• High work-in-process inventory• Slow turning maintenance inventory• High pre-mix inventory at St. Gabriel

Opportunities• Reduce safety stocks of raw materials• Increase equipment reliability to support higher production rates and

reduce lead time and reduce work-in-process• Clean-up rework and packaging inventory at formulation plants• Accelerate flow of pre-mix at St. Gabriel

Inventory Reduction

Carrying Cost

1994 19951993

$7.1M –One-Time

$0.3M

$1.9M

$1.6M –**

* On-going

Presentations 04/19/23 @ 13:36 - 32 -

BUSINESS CASE

Manufacturing – Productivity Improvement

• Omaha reduce FG rework by 25%• .25 x $.400 (annual expense) = .100

• Omaha shift avoidance (direct labor saving)• $800 per shift x 391 avoided shifts = .300

• Eliminate 7 rail cars by accelerating flow of AI’s - $75,000

Findings• Contract services are currently used to perform maintenance

services while full time employees are idle• NLR plant downtime impacts operator productivity• Cold Creek plant downtime impacts operator productivity• Significant finished goods rework at Omaha• Omaha continuous unit and Canner downtime impacts operator

productivity

Opportunities• Improve Cold Creek maintenance effectiveness by utilizing full time

employees to complete work now done by contractors• Increase operator productivity at NLR through increased uptime and

throughput of product• Increase operator productivity at Cold Creek through increased uptime

and throughput of product• Avoid rework of finished goods at Omaha by formulating and

packaging close to market demand• Increase throughput at Omaha of continuous unit output to 140,000

pounds per shift and canners to 8000 gallons per shift

Cost Reduction

$1.5M–

19941993

Calculation• 50% contract services could be picked up by Cold Creek staff

• $1,712 (actual 1992) x .50 = $856• 50% contract services is material

• $856 x .50 = $428• NRL operator productivity valued at

• 15 - 20X x 12 = 1.8 - 2.4• 1.8 x $45,700 = $.082• 2.4 x $45,700 = $.110

• Cold Creek operator productivity valued at• 10 - 20% x 94 operators• 9.0 x $46,800 = $.421• 18.0 x 46,800 = $.842

$0.3M

1995

* ** On-going

Presentations 04/19/23 @ 13:36 - 33 -

BUSINESS CASE

Procurement

Findings• Raw material cost rising as a percent of sales• Over 100 supplies with purchases less than $100,00 annually• Costly process for purchasing MRO and WRC supplies• Communications and plant coordinations issues• Complex packaging buying process

Opportunities• Streamline packaging procurement and graphics change process• Simplify MRO / supplies procurement• Concentrate more time on vendor development and selection

Cost Reduction

$0.3M–

19941993

Calculation

• Raw material 1.5% x $142mm = $2.1

• U.K. purchasing 1.5% x $83mm = $1.2

• Packaging 3.0% x $13mm = $0.4

• WRC 2.0% x $12mm = $0.2

MRD 6.0% x $4mm = $0.2

$0.3M

1995

* ** On-going

Presentations 04/19/23 @ 13:36 - 34 -

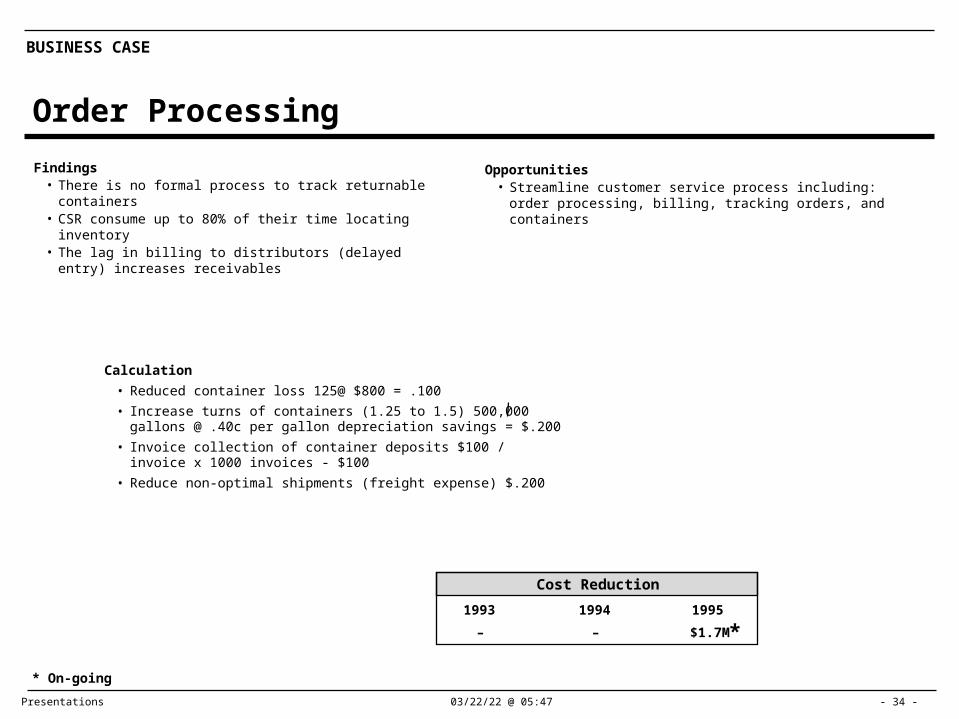

BUSINESS CASE

Order Processing

Findings• There is no formal process to track returnable containers• CSR consume up to 80% of their time locating inventory• The lag in billing to distributors (delayed entry) increases

receivables

Opportunities• Streamline customer service process including: order processing,

billing, tracking orders, and containers

Cost Reduction

––

19941993

Calculation

• Reduced container loss 125@ $800 = .100

• Increase turns of containers (1.25 to 1.5) 500,000 gallons @ .40c per gallon depreciation savings = $.200

• Invoice collection of container deposits $100 / invoice x 1000 invoices - $100

• Reduce non-optimal shipments (freight expense) $.200

$1.7M

1995

*

* On-going

Presentations 04/19/23 @ 13:36 - 35 -

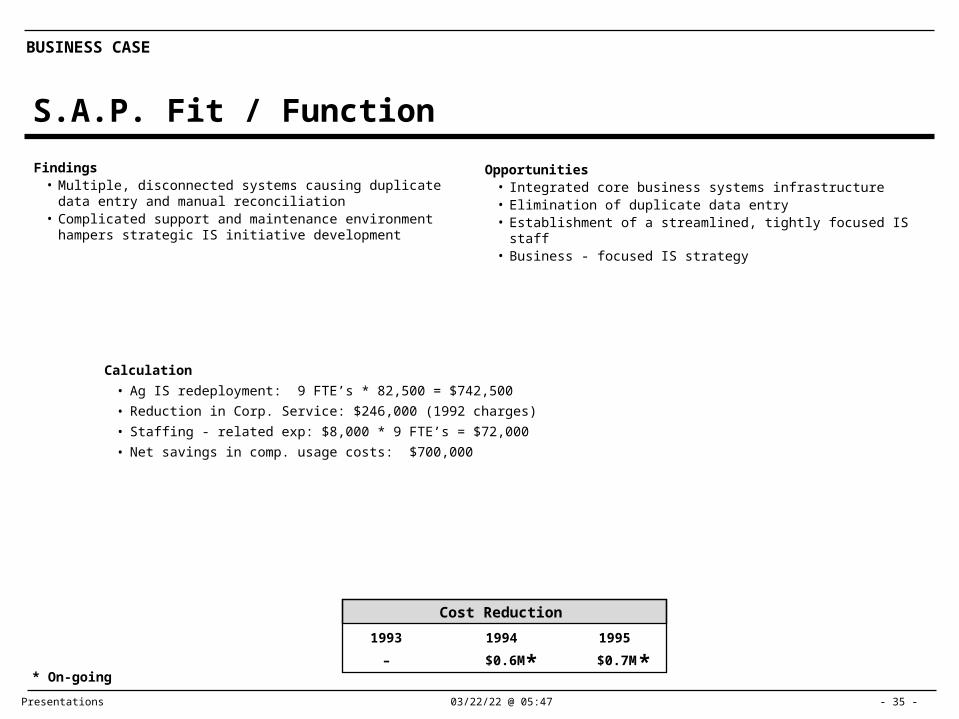

BUSINESS CASE

S.A.P. Fit / Function

Findings• Multiple, disconnected systems causing duplicate data entry and

manual reconciliation• Complicated support and maintenance environment hampers

strategic IS initiative development

Opportunities• Integrated core business systems infrastructure• Elimination of duplicate data entry• Establishment of a streamlined, tightly focused IS staff• Business - focused IS strategy

Cost Reduction

19941993

Calculation

• Ag IS redeployment: 9 FTE’s * 82,500 = $742,500

• Reduction in Corp. Service: $246,000 (1992 charges)

• Staffing - related exp: $8,000 * 9 FTE’s = $72,000

• Net savings in comp. usage costs: $700,000

$0.7M

1995

– $0.6M * ** On-going

Presentations 04/19/23 @ 13:36 - 36 -

BUSINESS CASE

Product Development and Introduction

Findings• Work priorities of existing projects are not re-prioritized regularly

causing unnecessary expense on potentially discontinued projects• Excessive back-up formulations projects cause added work efforts

to compensate for complex approval process• Insufficient level of commercial / technical group coordination

causes•Unnecessary effort spent on questionable formulation projects•Formulation rework

Opportunities• How to identify costly, unrealistic projects early in the process before

investing significant effort• How to minimize development of back-up formulations which involves

formulation / repackaging as well as field trail effort• How to integrate technical input into commercial business cases early

in project planning process to establish feasibility, ownership and accountability for project decisions

Cost Reduction

19941993

Calculation• 14 man-months per year can be saved (based on Fusilade, Reflex, Karate examples)• $200K (overhead dollars) can be saved in formulations effort

• $200K savings in overheaded dollars equals• $125K savings in direct dollars (overhead not included)

• Savings = 25% of evaluation trials on formulations of established products• Yearly average = 800 - 900 trails total• 256 trials are “evaluation” formulations of established products, in 1992• Savings = 25% of 256 trails = 64 trials• $960k potential savings on evaluation efficacy trails based on $15k / trail

• $960k savings in overheaded dollars equals• $760K savings in direct dollars (overhead not included)

• 0.5 project per year• 50% success rate on new technology project• 66% of failures are predictable

1995

• Potential savings = 0.5 x 0.5 x 0.660.16 project / year

• Project takes 2 man-years of Product Development and Process Technology effort / year

• + 10 field trails / year• Pilot plant capital

$1.1M– $3.0M * ** On-going

Presentations 04/19/23 @ 13:36 - 37 -

BUSINESS CASE

Infrastructure

Findings• Wilmington budget process consumes 30 - 40% excess resources• Month end close processing utilizes 50 - 60% extra effort• Accounts payable activities hold opportunity in best practices and

S.A.P. implementation ranging from 50% to 400% implement• Excessive reporting consumes resources and creates confusion• Span of control too low• 38% of site accountants time is spend on administrative duties

Opportunities• Streamline operating and capital budget process• Simplify and streamline the monthly close process• Simplify reporting and reduce number of reports• Redeploy accounts payable personnel

Cost Reduction

19941993

Calculation

• Wilmington accounting 30% x 27 FTE = $.5

• WRC A/P 50% x 3 FTE = .1

• Plant A/P 50% x 8 FTE = .3

• Plant accounting 20% x 15FTE = .2

1995

* On-going

$0.6M– $0.5M * *