32

Protect the profitability and viability of your business BUSINESS CONTINUATION PLANNING A GUIDE FOR BUSINESS OWNERS

Protect the profitability and viability of your business

Business Continuation PlanningA guide for business owners

The information presented in this document is for general information purposes only. Sun Life Assurance Company of Canada does not provide legal, accounting, taxation or other professional advice to advisors or their clients. Before you act on any of this information, always obtain advice from qualified professionals including a thorough examination of your specific situation and the current tax and legal rules.

This guide is one of a series of planning guides that Sun Life Financial has developed on subjects

of interest to business owners. Topics include continuation planning (risk management),

succession planning, estate planning and planned giving. Other guides, intended primarily for

your professional advisors, examine the tax and legal aspects of related financial concepts using

life insurance such as shared ownership and leveraging. Ask your financial advisor for a copy.

TAble of conTenTs

Business continuation basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-3

What is business continuation planning and how does it fit with your overall

financial plan?

Protecting your business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-17

How do you manage potential risks and threats to your business?

Loss of a key person. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-6

Loss of an owner. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-9

Funding methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10-15

Tax planning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16-17

Finding an appropriate business valuation method . . . . . . . . . . . . . . . . . . . . . . 18-19

There are a number of ways to determine the value of your business at a given

point in time. This section provides a brief overview of common business

valuation methods.

Corporate accounting and life insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20-22

Here is an overview of key accounting and tax treatments relating to

corporate-owned life insurance policies.

appendices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23-28

Appendix A – Quantifying potential key person losses . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Appendix B – Individually owned and corporate-owned cross

purchase method. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Appendix C – Corporate redemption method. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25-26

Appendix D – Post stop-loss: Comparison of 50 per cent capital

dividend vs. 100 per cent capital dividend . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Appendix E – Redeem and cross-purchase arrangement (50 per cent)

under stop-loss rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

2 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

There are good reasons for addressing these risks. While a business represents a source of current income for many business owners, the value of the business can also represent a primary source of income in retirement. Business continuation strategies are critical not only for the immediate survival of the business, but to ensure that the business can be relied upon to generate the expected value for the owners when they exit the business.

This guide provides an overview of some key strategies that can help you protect the profitability and viability of your business. It also provides a more detailed look at the ways in which life insurance can be used to fund many of these strategies.

business conTinuATion bAsics

Business continuation planning is the process of identifying issues that may

put your business at risk, such as the death or disability of a key employee

or owner, and adopting risk management strategies to minimize, eliminate

or transfer these risks.

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 3

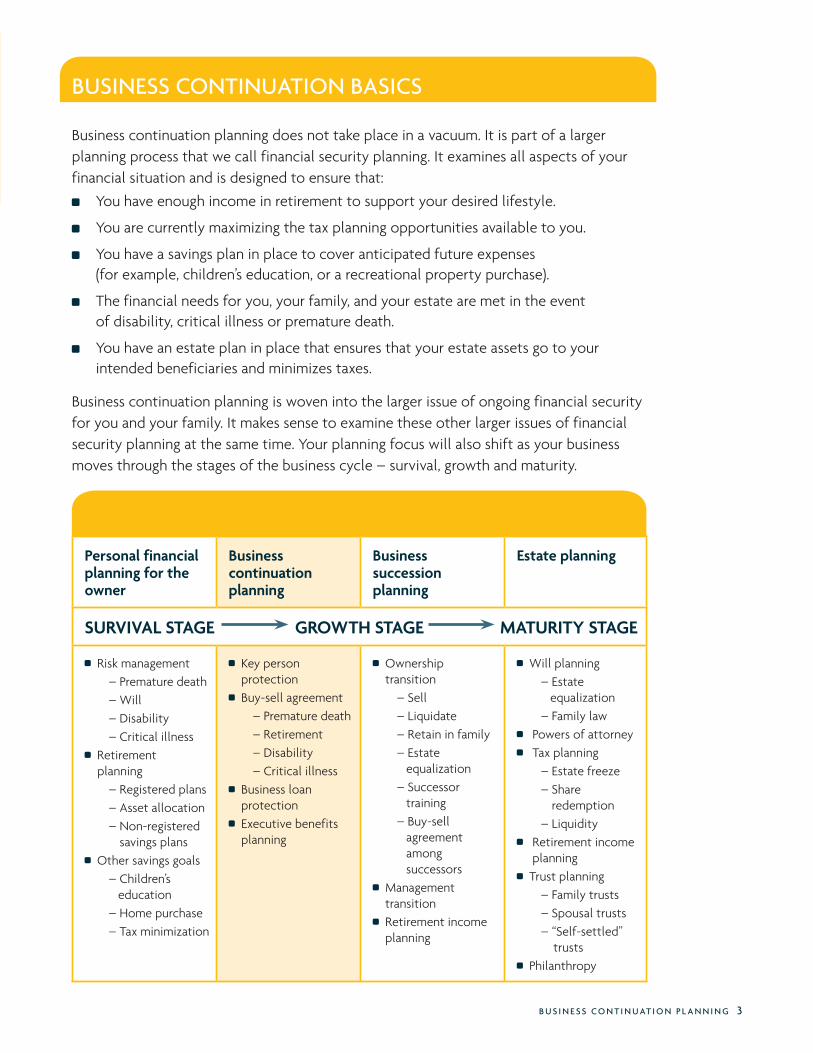

business conTinuATion bAsics

Business continuation planning does not take place in a vacuum. It is part of a larger planning process that we call financial security planning. It examines all aspects of your financial situation and is designed to ensure that:

You have enough income in retirement to support your desired lifestyle.

You are currently maximizing the tax planning opportunities available to you.

You have a savings plan in place to cover anticipated future expenses (for example, children’s education, or a recreational property purchase).

The financial needs for you, your family, and your estate are met in the event of disability, critical illness or premature death.

You have an estate plan in place that ensures that your estate assets go to your intended beneficiaries and minimizes taxes.

Business continuation planning is woven into the larger issue of ongoing financial security for you and your family. It makes sense to examine these other larger issues of financial security planning at the same time. Your planning focus will also shift as your business moves through the stages of the business cycle – survival, growth and maturity.

Personal financial planning for the owner

Business continuation planning

Business succession planning

estate planning

survival stage growth stage Maturity stage

Risk management – Premature death – Will – Disability – Critical illness Retirement

planning – Registered plans – Asset allocation – Non-registered

savings plans Other savings goals

– Children’s education – Home purchase – Tax minimization

Key person protection

Buy-sell agreement – Premature death – Retirement – Disability – Critical illness Business loan protection

Executive benefits planning

Ownership transition

– Sell – Liquidate – Retain in family – Estate equalization – Successor training – Buy-sell agreement

among successors

Management transition

Retirement income planning

Will planning – Estate equalization – Family law Powers of attorney Tax planning

– Estate freeze – Share

redemption – Liquidity Retirement income

planning Trust planning

– Family trusts – Spousal trusts – “Self-settled” trusts Philanthropy

4 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

ProTecTing your business

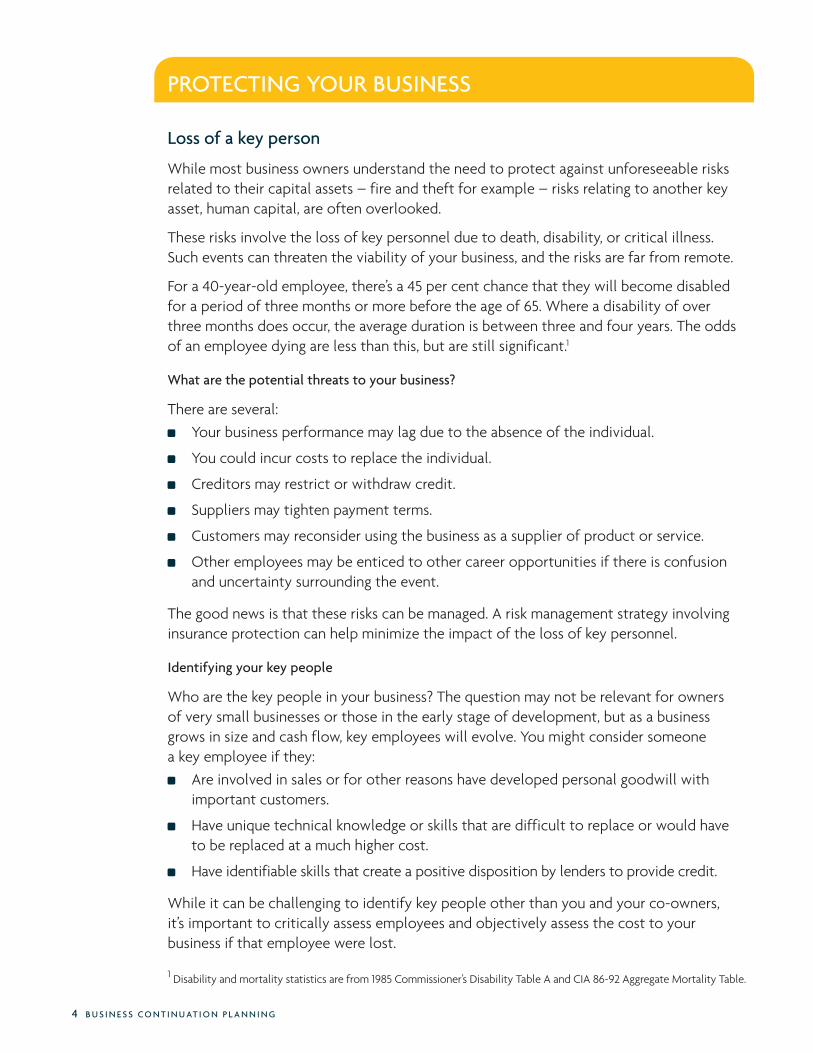

loss of a key person

While most business owners understand the need to protect against unforeseeable risks related to their capital assets – fire and theft for example – risks relating to another key asset, human capital, are often overlooked.

These risks involve the loss of key personnel due to death, disability, or critical illness. Such events can threaten the viability of your business, and the risks are far from remote.

For a 40-year-old employee, there’s a 45 per cent chance that they will become disabled for a period of three months or more before the age of 65. Where a disability of over three months does occur, the average duration is between three and four years. The odds of an employee dying are less than this, but are still significant.1

what are the potential threats to your business?

There are several:

Your business performance may lag due to the absence of the individual.

You could incur costs to replace the individual.

Creditors may restrict or withdraw credit.

Suppliers may tighten payment terms.

Customers may reconsider using the business as a supplier of product or service.

Other employees may be enticed to other career opportunities if there is confusion and uncertainty surrounding the event.

The good news is that these risks can be managed. A risk management strategy involving insurance protection can help minimize the impact of the loss of key personnel.

identifying your key people

Who are the key people in your business? The question may not be relevant for owners of very small businesses or those in the early stage of development, but as a business grows in size and cash flow, key employees will evolve. You might consider someone a key employee if they:

Are involved in sales or for other reasons have developed personal goodwill with important customers.

Have unique technical knowledge or skills that are difficult to replace or would have to be replaced at a much higher cost.

Have identifiable skills that create a positive disposition by lenders to provide credit.

While it can be challenging to identify key people other than you and your co-owners, it’s important to critically assess employees and objectively assess the cost to your business if that employee were lost.

1 Disability and mortality statistics are from 1985 Commissioner’s Disability Table A and CIA 86-92 Aggregate Mortality Table.

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 5

Assessing your potential losses

Once you’ve identified your key personnel, you need to assess your potential sources of loss.

These might include:

The cost of searching for, recruiting and attracting an equally effective replacement.

The cost of temporary support hired or contracted in the interim period.

The estimated loss in productivity or revenue until an equally effective replacement is up and running.

Business loans that may be called or for which there is a desire to retire.

Lines of credit that may be reduced or retracted.

The impact of some suppliers moving to cash on delivery for a period of time.

The increased cost of debt service if carrying charges are increased.

Quantifying your potential loss is often an art as much as a science, but it’s a necessary process in order to determine the amount of insurance protection that your business will need. For an example of how potential losses might be quantified, see appendix A.

How key person insurance can help

While it may be possible for a business to retain their key person risk if the potential losses are small enough, the impact of a loss for some businesses can often be sufficiently catastrophic to destroy the viability of the business. The business simply won’t have the cash flow or available credit to withstand the losses and credit contraction that would occur.

In such cases, many businesses choose to transfer the risk, usually through the purchase of life, disability, or critical illness insurance. The insurance proceeds can ensure there is an injection of liquid capital to allow family or management time to appoint and pay for interim management, pay off creditors, and cover the cost to the business of the lost key person. The availability of this cash, along with a viable transition plan, can also act to reassure employees, creditors, suppliers, and customers.

Here is an overview of the three types of insurance typically used to provide key person protection.

Key person life insurance

Life insurance is usually the cornerstone of a key person protection strategy. It provides an instantaneous injection of capital into the business upon the death of the key person. The company receives death benefits tax-free.

Renewable term insurance is usually the most economical option over the short-term. However, there are situations in which a more permanent insurance solution should be considered, such as when protection is expected to extend over a longer time frame, or there is a need to create a funded supplemental compensation structure for the insured individual.

If the parties intend to use life insurance policy values to provide retirement income for the insured, care must be taken to ensure that the policy will not be deemed to be a retirement compensation arrangement. If it is, adverse tax consequences may apply. The parties should speak with their tax advisors if they want to use the policy to provide retirement income for the insured.

6 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

Key person disability insurance

Disability insurance can be used for two purposes in a key person context:

The insurance can provide salary continuation to a key person in the event they become disabled, usually until the earlier of age 65 or recovery from the disability.

Owner-managers can purchase insurance that provides continued payment of office expenses and salaries during the period of disability, usually for a limited time period.

Critical illness insurance

Critical illness insurance provides protection in a situation where a key person is afflicted by specified diseases or health problems that do not necessarily render them disabled but nevertheless affect their productivity or their desire to work to the same extent as before.

This coverage will pay a lump sum, or in some cases a stream of income, to the business to help cover losses created by the absence or lower productivity of the individual.

loss of an owner

A sole owner is by definition a key person, and in many business situations may be the only key person. But the business continuation issues for sole owners differ in many ways from those involving other key persons.

Very small businesses, or those in the early stage of development, may not be sustainable in the absence of a sole owner. Often, the owner is the business. In that instance, life, disability or critical illness insurance will likely be useful only from the standpoint of income replacement for the owner’s family. It could also help provide the cash flow required to terminate the business, including payment of liquidation fees, and other debts like income tax due at that time, rather than for business continuation purposes.

In other situations, however, the business has grown beyond the sole owner and has a sustainable value, even in the owner’s absence. In such cases, insurance protection may be needed for additional reasons.

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 7

If a sole owner dies for example, additional funding may be needed for a number of reasons:

The potential sources of loss associated with the loss of a key person, such as lower productivity and reduced or retracted credit, are even more likely to occur if the key person lost is the sole owner.

Even if productivity is lower, the business must continue to pay staff and cover other overhead expenses.

Time may be needed to find an appropriate buyer for the business. The additional funding that insurance protection provides can buy the time needed to sell the business to the right buyer at the right price.

The deemed disposition of assets at death can lead to a significant tax liability for the owner’s estate. Insurance proceeds can cover this liability, without requiring the estate to liquidate other assets.

While the protection solutions for sole owners – life, disability and critical illness insurance – are the same as for other key persons, the risks covered will differ due to the central role and equity position that the owner enjoys.

Protecting your business if a co-owner dies

While key person protection is an important element of business continuation planning, it can be even more crucial to address the potential issues that can arise upon the death of a co-owner.

Many businesses have multiple owners, either because they carry on business as a partnership or corporation. If one of your co-owners dies, this could have a serious impact on your business. The reason? If you have a partnership, and you don’t have a partnership agreement that deals with a partner’s death, the law requires you to dissolve the partnership if a partner dies. This means that your business would end and your business accounts would be frozen. You and any other surviving partners would have to liquidate the business and pay the deceased partner’s share to his or her surviving spouse or heirs before you could create a new partnership and continue your business.

Something different but equally severe could happen if you are a shareholder in an incorporated business and a shareholder dies. That shareholder’s heirs, such as their spouse or children, will inherit the shares. Your business will have a new shareholder, even if he or she lacks the qualifications or experience needed to participate in the business.

Avoiding these consequences requires special planning, including a partnership or shareholder’s agreement funded with life insurance. This will help ensure a smooth transition if a partner or shareholder dies, and will help minimize the business risk.

8 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

how death changes everything

When a co-owner dies, the surviving business owners usually have five options in dealing with the deceased owner’s business interest. Here is a brief description of each:

buy out the heirs: This is usually the most preferred option. After all, the surviving owners know how to run their business. It usually makes sense to buy out the heirs and carry on business from there, especially in cases where the heirs lack business expertise or interest in running the business.

Keep the heirs in the business: While heirs can remain as owners in either an active or inactive role, there are risks to this arrangement, in particular the potential for conflicting opinions about key issues such as compensation and the overall direction of the business.

Take on an outsider who purchases the deceased’s business interest: Outside buyers are seldom interested in purchasing a deceased’s business interest in a closely held business. However, if the situation does occur, the risk lies in the new owner not sharing the same business vision as current owners, and the potential for strains in the working relationship.

sell to the heirs: This alternative is feasible if the current owners are at a stage where they want to sell, and the heirs are qualified to operate the business and have access to adequate capital.

liquidate the business or sell to a third party: Unless an alternative can be agreed upon, the sale or liquidation of the business may be the only option, although it is far from ideal as only a fraction of going concern value may be realized, and the liquidation proceeds may not be enough to pay the tax and meet other estate obligations.

the need for a buy-sell agreement

To avoid the potential problems associated with the options described earlier, advance planning is essential. One of the most effective planning tools is a buy-sell agreement.

A buy-sell agreement can take the form of a stand-alone contract or form part of an overall shareholder’s agreement. Such agreements set out the conditions in which an owner has the right to buy the ownership share of another owner. This can include items such as how the business will be valued and the method and conditions of payment. The agreement can also govern the conditions of a voluntary sale of the business by one or more owners.

The buy-sell agreement on its own, however, does not provide all the protection that the owners and business require in the event of an owner’s death.

For the buy-sell agreement to be effective, it must be properly funded. Surviving owners need a source of funds to not only buy out the deceased owner’s interest, but to boost the organization’s working capital if necessary to compensate for the loss of the deceased’s services and financial backing.

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 9

A properly constructed and funded buy-sell agreement provides benefits to all parties. It can address the needs of the deceased’s heirs by providing full value and a guaranteed and timely cash payment for what is in most cases a non-liquid asset.

For the surviving owners, a properly funded agreement ensures the deceased’s family members will not have to be involved in the business, and that the business can continue uninterrupted without additional debt. It can also ensure that the confidence of employees, creditors, and customers can be maintained.

Because there are tax consequences to the various methods of funding, it’s also important that the funding arrangement be structured to minimize the short and long-term tax consequences for both the deceased and their estate, and the surviving owners.

DiD you Know

A buy-sell AgreemenT HAs mAny uses

While this guide discusses the use of a buy-sell agreement in the event of the death or disability of an owner, an agreement can also cover other situations, such as:

The retirement of an owner.

A non-resolvable dispute between owners.

Marital breakdown, where an owner’s spouse has, or may become entitled to, an interest in the business.

Personal insolvency of an owner.

Any illegal actions by an owner.

A buy-sell agreement is also an effective planning tool when included in a partnership agreement.

Family businesses can also take advantage of a buy-sell agreement.

1 0 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

funding methods

Funding options for a buy-sell agreement

There are several ways to access the necessary funding to buy-out a deceased owner’s business interest under a buy-sell agreement. Here is a brief overview of each:

borrow the funds: If the business has a good credit rating it can borrow the funds needed to buy out the heirs. However, it’s important to remember that while the business may be a good credit risk today, there is no guarantee it will be in the same position many years later, or that anyone will be willing to lend to it immediately after an owner’s death.

issue a promissory note: A promissory note is an unconditional written promise to pay for the deceased owner’s shares. The main shortcoming of this arrangement is that it doesn’t provide the deceased owner’s estate with an immediate, and often much needed, cash payment. A promissary note may or may not be secured with corporate assets.

use business earnings: Business earnings can be used to either fund repayment of a promissory note or to pay the surviving owners to fund the purchase. This is a viable option if the business is in a solid cash position, but it could deprive the business of needed capital to grow and expand.

sell business assets: Selling assets can be a problematic choice since the timing of the sale is dictated by an outside event – the death of an owner – and not on market conditions. This means the business may get less than full value for the asset.

use life insurance: A life insurance policy on the life of each business owner is a relatively low cost alternative to other funding methods, and provides the necessary cash immediately upon death. While the business must pay an annual premium amount for the insurance coverage, the premium is relatively low when compared to the tax-free proceeds that the business would receive should a death occur.

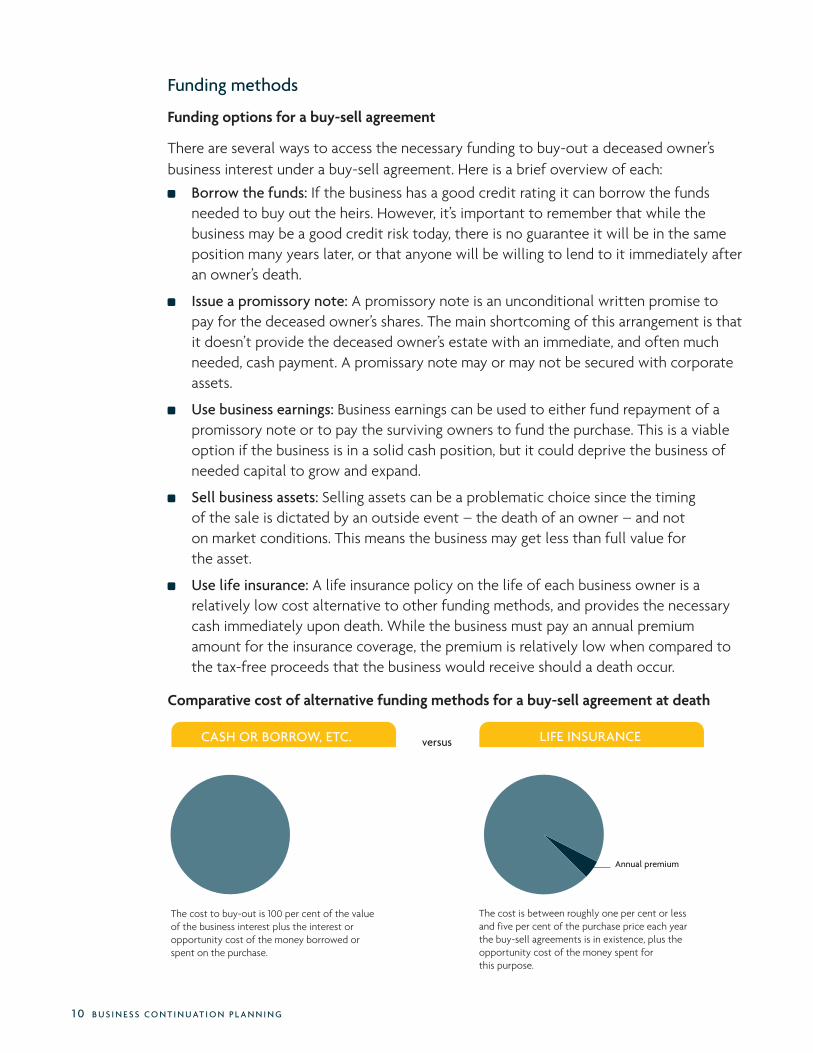

Comparative cost of alternative funding methods for a buy-sell agreement at death

The cost to buy-out is 100 per cent of the value of the business interest plus the interest or opportunity cost of the money borrowed or spent on the purchase.

CASH OR BORROW, ETC.

Annual premium

Le coût du rachat représente 100 % de la valeur de la part dans l’entreprise augmenté des intérêts à payer ou du potentiel de rendement perdu par suite de l’emprunt ou de la dépense occasionnée par le rachat.

LIQUIDITÉS, EMPRUNT, ETC. ASSURANCE-VIE

Prime annuelle

Le coût de l’assurance est d’environ 1 % à 5 % du prix d’achat par année d’existence de la convention, augmenté du potentiel de rendement perdu par suite du paiement des primes.

LIFE INSURANCEversus

vs

The cost is between roughly one per cent or less and five per cent of the purchase price each year the buy-sell agreements is in existence, plus the opportunity cost of the money spent for this purpose.

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 1 1

Funding a buy-sell agreement using life insurance

Life insurance not only provides effective low-cost funding of a buy-sell agreement, it also offers considerable flexibility in how an arrangement is structured.

The life insurance funding arrangement that works best for your business will depend on many factors, such as the date the arrangement was put in place, your specific business continuation needs, and the legal structure of your business.

This section of the guide provides a quick overview of the funding arrangements available, and then sets out more detailed examples and analysis of how each arrangement works from a tax standpoint.

1 2 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

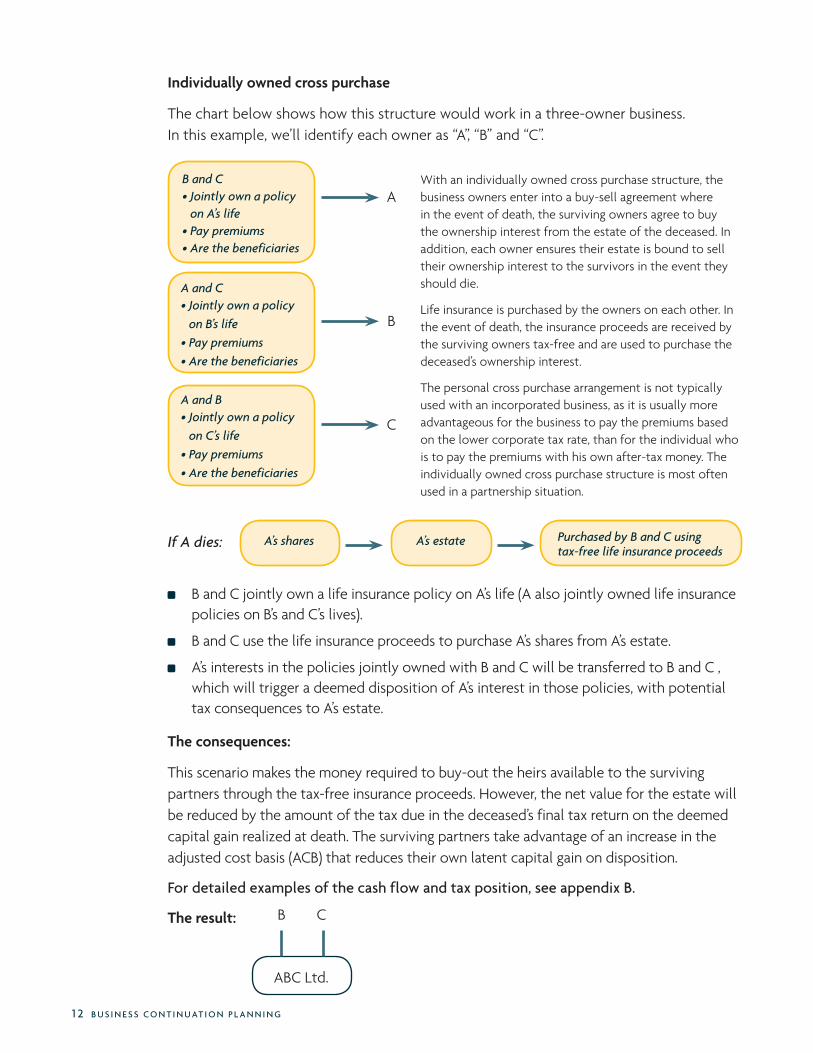

individually owned cross purchase

The chart below shows how this structure would work in a three-owner business. In this example, we’ll identify each owner as “A”, “B” and “C”.

B and C jointly own a life insurance policy on A’s life (A also jointly owned life insurance policies on B’s and C’s lives).

B and C use the life insurance proceeds to purchase A’s shares from A’s estate.

A’s interests in the policies jointly owned with B and C will be transferred to B and C , which will trigger a deemed disposition of A’s interest in those policies, with potential tax consequences to A’s estate.

the consequences:

This scenario makes the money required to buy-out the heirs available to the surviving partners through the tax-free insurance proceeds. However, the net value for the estate will be reduced by the amount of the tax due in the deceased’s final tax return on the deemed capital gain realized at death. The surviving partners take advantage of an increase in the adjusted cost basis (ACB) that reduces their own latent capital gain on disposition.

for detailed examples of the cash flow and tax position, see appendix b.

the result:

With an individually owned cross purchase structure, the business owners enter into a buy-sell agreement where in the event of death, the surviving owners agree to buy the ownership interest from the estate of the deceased. In addition, each owner ensures their estate is bound to sell their ownership interest to the survivors in the event they should die.

Life insurance is purchased by the owners on each other. In the event of death, the insurance proceeds are received by the surviving owners tax-free and are used to purchase the deceased’s ownership interest.

The personal cross purchase arrangement is not typically used with an incorporated business, as it is usually more advantageous for the business to pay the premiums based on the lower corporate tax rate, than for the individual who is to pay the premiums with his own after-tax money. The individually owned cross purchase structure is most often used in a partnership situation.

A’s shares A’s estate Purchased by B and C using tax-free life insurance proceeds

If A dies:

ABC Ltd.

B C

B and C• Jointly own a policy

on A’s life• Pay premiums• Are the beneficiaries

A and C • Jointly own a policy

on B’s life• Pay premiums• Are the beneficiaries

A and B • Jointly own a policy

on C’s life• Pay premiums• Are the beneficiaries

A

B

C

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 1 3

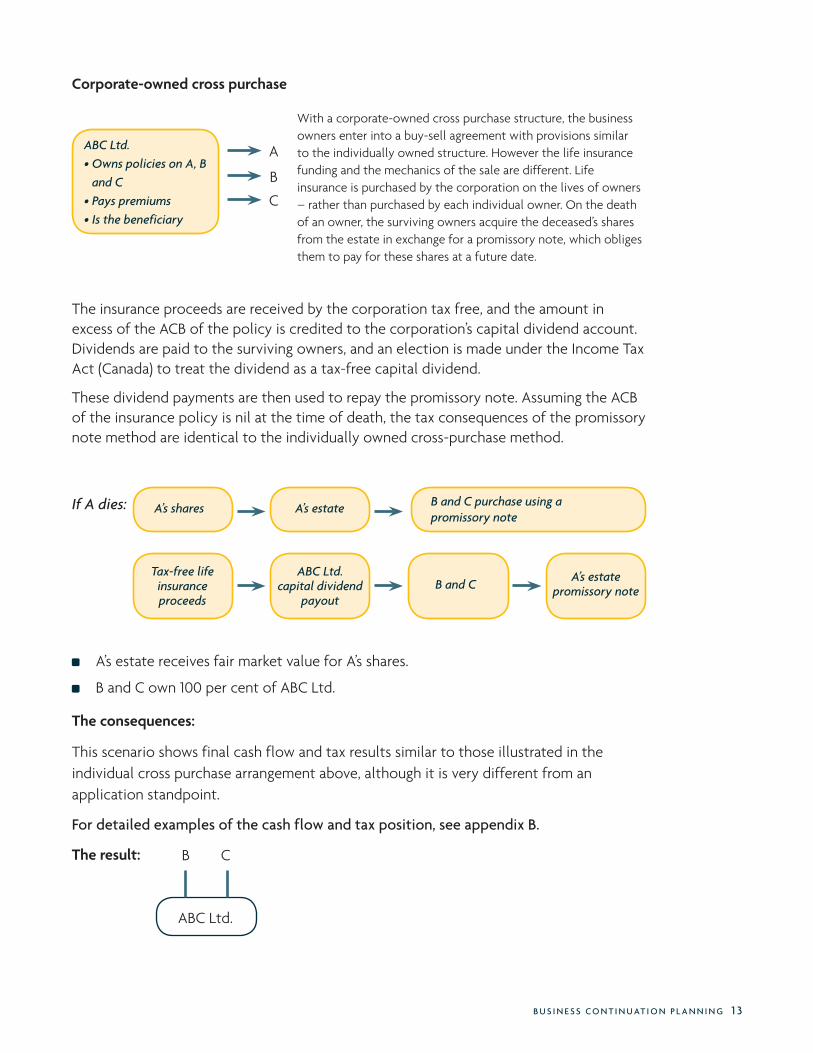

ABC Ltd.

B C

Corporate-owned cross purchase

With a corporate-owned cross purchase structure, the business owners enter into a buy-sell agreement with provisions similar to the individually owned structure. However the life insurance funding and the mechanics of the sale are different. Life insurance is purchased by the corporation on the lives of owners – rather than purchased by each individual owner. On the death of an owner, the surviving owners acquire the deceased’s shares from the estate in exchange for a promissory note, which obliges them to pay for these shares at a future date.

The insurance proceeds are received by the corporation tax free, and the amount in excess of the ACB of the policy is credited to the corporation’s capital dividend account. Dividends are paid to the surviving owners, and an election is made under the Income Tax Act (Canada) to treat the dividend as a tax-free capital dividend.

These dividend payments are then used to repay the promissory note. Assuming the ACB of the insurance policy is nil at the time of death, the tax consequences of the promissory note method are identical to the individually owned cross-purchase method.

A’s estate receives fair market value for A’s shares.

B and C own 100 per cent of ABC Ltd.

the consequences:

This scenario shows final cash flow and tax results similar to those illustrated in the individual cross purchase arrangement above, although it is very different from an application standpoint.

for detailed examples of the cash flow and tax position, see appendix b.

the result:

If A dies:

A

B

C

A’s shares A’s estate B and C purchase using a promissory note

Tax-free life insurance proceeds

ABC Ltd. capital dividend

payoutB and C

A’s estate promissory note

ABC Ltd.• Owns policies on A, B

and C• Pays premiums• Is the beneficiary

1 4 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

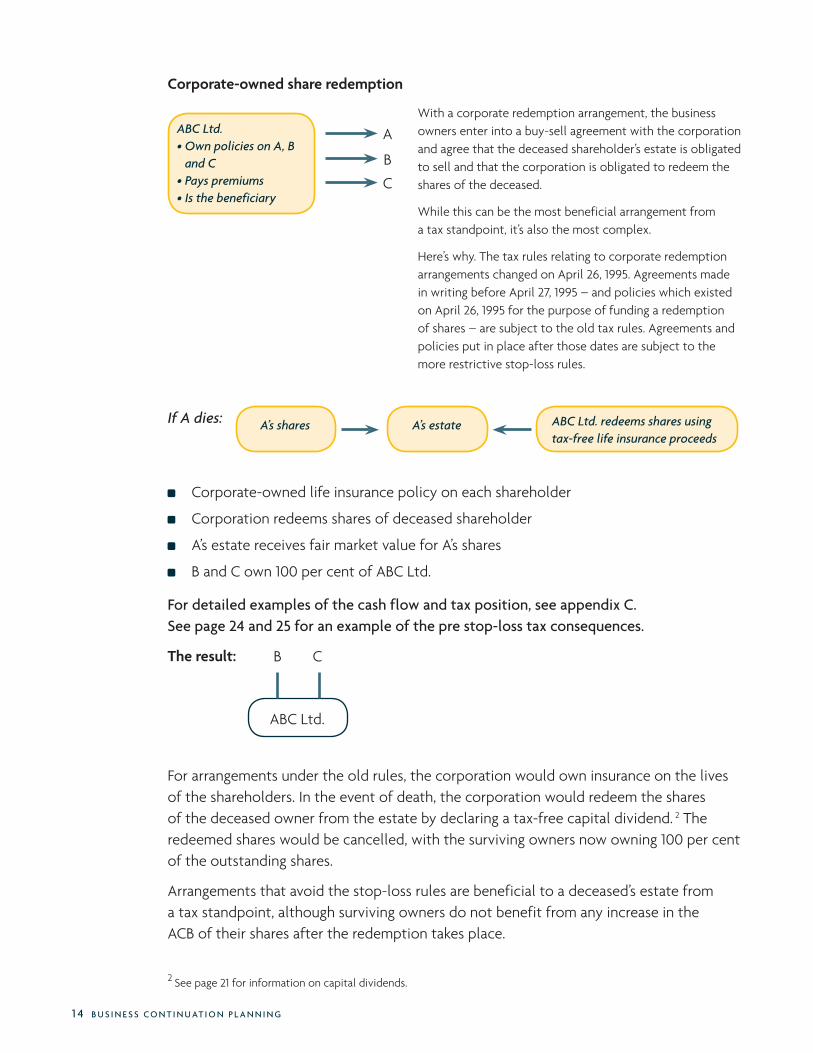

Corporate-owned share redemption

With a corporate redemption arrangement, the business owners enter into a buy-sell agreement with the corporation and agree that the deceased shareholder’s estate is obligated to sell and that the corporation is obligated to redeem the shares of the deceased.

While this can be the most beneficial arrangement from a tax standpoint, it’s also the most complex.

Here’s why. The tax rules relating to corporate redemption arrangements changed on April 26, 1995. Agreements made in writing before April 27, 1995 – and policies which existed on April 26, 1995 for the purpose of funding a redemption of shares – are subject to the old tax rules. Agreements and policies put in place after those dates are subject to the more restrictive stop-loss rules.

A

B

C

Corporate-owned life insurance policy on each shareholder

Corporation redeems shares of deceased shareholder

A’s estate receives fair market value for A’s shares

B and C own 100 per cent of ABC Ltd.

for detailed examples of the cash flow and tax position, see appendix c. see page 24 and 25 for an example of the pre stop-loss tax consequences.

the result:

For arrangements under the old rules, the corporation would own insurance on the lives of the shareholders. In the event of death, the corporation would redeem the shares of the deceased owner from the estate by declaring a tax-free capital dividend. 2 The redeemed shares would be cancelled, with the surviving owners now owning 100 per cent of the outstanding shares.

Arrangements that avoid the stop-loss rules are beneficial to a deceased’s estate from a tax standpoint, although surviving owners do not benefit from any increase in the ACB of their shares after the redemption takes place.

2 See page 21 for information on capital dividends.

If A dies:

ABC Ltd.• Own policies on A, B

and C• Pays premiums• Is the beneficiary

A’s shares A’s estate ABC Ltd. redeems shares using tax-free life insurance proceeds

ABC Ltd.

B C

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 1 5

FaCts/inForMation

stop-loss rules explainedUnder the old tax rules, which apply to arrangements in effect before April 27, 1995 or policies in-force on April 26, 1995, the estate of a deceased shareholder could reduce its taxable capital gain to zero by declaring a capital loss equal to the amount of the capital dividends received when the corporation redeemed its shares. The stop-loss rules under subsection 112(3.2) of the Income Tax Act (Canada) (ITA) do just what the name suggests, they reduce the capital loss that the estate can claim.

Under the stop-loss rules, the estate’s capital loss is determined to be the lesser of:

(1) capital dividends on the shares received by the estate, and

(2) the capital loss minus any taxable dividend received by the estate.

Minus 50 per cent of the lesser of:

(a) the deceased’s capital gain from the deemed disposition at death, and

(b) the estate’s capital loss.

Be careful with grandfathered arrangements

In order to maintain the privilege of grandfathering under the pre-stop-loss tax rules, the owners must be very careful when any further transactions are contemplated, such as:

The sale of the shares to a third party who is not party to the buy-sell agreement.

Corporate reorganizations and mergers.

Revisions to the terms of the existing buy-sell agreement.

Entering into a new separate buy-sell agreement that cancels, nullifies or replaces the grandfathered agreement.

In contrast, a very broad range of changes could occur on an existing life insurance policy, up to cancellation and replacement, without resulting in the loss of the old rules. Nevertheless, the policyholder must be able to document that the main purpose for purchasing the policy was to fund the redemption, acquisition or cancellation of shares.

So a safe keeping of documents issued by the life insurance company, minutes of the corporation, and any correspondence from a legal advisor and accountant, is highly recommended.

If an arrangement falls under the stop-loss rules, the corporation can still redeem the shares of the deceased owner, but for tax reasons, may declare a tax-free capital dividend of less than 100 per cent of the insurance proceeds.

Alternative strategies that have been developed to work with the stop-loss rules seek to maximize the value of the life insurance for the corporation and the shareholders and to avoid the wasting of capital dividend account credits. In effect, there is now an opportunity for a more equitable spreading of the tax burden between the deceased’s estate and the surviving owners. For alternative strategies, see page 16. For detailed examples of the tax treatment under corporate redemption arrangements, see appendix C.

1 6 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

Tax planning

strategies to maximize immediate tax effectiveness

The stop-loss rules have reduced the tax advantages enjoyed by a deceased owner’s estate when the company redeems the owner’s shares. But the rules have also prompted business owners to look at alternative ways to structure corporate redemption arrangements to maximize the immediate tax advantages still available. Here are three alternate strategies to consider:

rollover and redeem

If an owner dies and is survived by his or her spouse, the shares can be transferred to a spouse or a spousal trust, on a tax-free basis. To qualify for a tax-deferred rollover, the shares must vest indefeasibly with the spouse. If certain conditions are met, the share redemption could be done with no limitation through a tax-free capital dividend.

However, some other stop-loss rules could apply in such circumstances, so great care must be taken in drafting the agreement and the owner’s will.3

the 50 per cent solution

The 50 per cent solution refers to the percentage of the life insurance proceeds that a company deems to be a capital dividend. Here’s how it works. After the death of a shareholder, the life insurance proceeds received by the company are used to redeem the deceased’s shares from the estate. The portion of the dividend deemed to be a capital dividend would be the lesser of 50 per cent of the deceased’s deemed gain on death, or 50 per cent of the loss realized by the estate. The balance of the redemption price is treated as a regular taxable dividend. There is also a capital dividend account credit retained by the company and used for the distribution of tax-free dividends.

Why choose 50 per cent instead of some other percentage for a deemed capital dividend? Even though the deceased’s estate will have a higher immediate tax bill, the total tax payable by all parties is considerably less when the arrangement as a whole is taken into account. For a detailed example of how the 50 per cent solution works for shares that do not qualify for grandfathering under the stop-loss rules and the tax comparison of the total tax burden between the 50 per cent deemed capital dividend and a 100 per cent deemed capital dividend, see appendix D.

redeem and cross-purchase

Upon the death of an owner, 50 per cent of the deceased’s shares are redeemed with the life insurance proceeds, and a capital dividend election is made for the amount paid. The balance of the shares are bought after a corporate reorganization where new shares – or a demand note – are issued for the remaining shares.

3 S.40 (3.6) ITA

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 1 7

The remaining 50 per cent of the insurance proceeds are distributed to the surviving shareholders as a tax-free capital dividend. This amount is used to acquire the newly issued shares or to repay the demand note from the estate. This triggers an increase in the ACB of the shares owned by the surviving owner. This solution also allows the deceased owner to take advantage of the $750,000 small business capital gain exemption if available. For a detailed example of a redeem and cross purchase arrangement, see appendix E.

use of a holding company structure

In some situations, the use of insurance to fund a buy-sell agreement is most effective when a holding company structure is established. With such a structure, the holding company owns shares of the business – the operating company.

The holding company would also own the life insurance that funds the buy-sell agreement.

There are several buy-out strategies that could be put in place through the buy-sell agreement to respond to the needs of the shareholders for flexibility and tax advantages.

Here are some of the advantages that these strategies try to address:

When the holding company owns the policy, and the operating company is the beneficiary, the entire amount of the insurance proceeds can be credited to the capital dividend account of the operating company when received, with no reduction for the adjusted cost basis of the policy, provided there is a business purpose for the beneficiary designation.

If the holding company owns the policy, the cash value of the policy may be protected from creditors of the operating company, provided no guarantees have been made by the holding company to the creditors of the operating company.

Because the cash value of the insurance policy belongs to the holding company, it will not taint or disqualify the shares of the operating company from the $750,000 capital gains exemption.

If a holding company owns insurance on the owners of the business and the operating company is sold, there will be no need to transfer the policy before the business changes owners and there will be no taxable disposition since the policy owner does not change.

The benefits of using a holding company to own life insurance for business continuation purposes will vary depending on the corporate structure involved and the specific business continuation needs of your organization. But it can be an advantageous arrangement in many cases.

1 8 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

finding An APProPriATe business vAluATion meTHod

Business valuation is an integral part of the buy-sell planning process. If a withdrawing event occurs, and one party must buy the business interest of another, the value of the interest must be determined for the sale to take place.

A business valuation is an examination conducted to estimate the fair market value (FMV) of a business interest at a given point in time. FMV is defined as the highest price obtainable in an open and unrestricted market between knowledgeable, prudent and willing parties. These parties are fully informed, dealing at arm’s length, and not under compulsion to act.

The valuation of a company is not an exact science. In particular, the valuation of a private company is complicated by several unique problems, including:

Lack of information and comparability.

Risk factors – determination of the multiplier.

Personal goodwill.

Normalization adjustments.

Income tax issues.

For the purposes of buy-sell planning, the valuation should usually be performed at the time of the withdrawing event – such as death or disability. Some shareholder agreements require an annual update of the valuation of the shares. This allows for the insurance to be adjusted on an annual basis and ensures that the agreement remains appropriately funded. Ideally, the buy-sell agreement should either specify a valuation formula, or make reference to an accepted valuator to determine the value at the time the event occurs.

The method of valuation chosen for a buy-sell agreement will depend on the specifics of the situation, the goals and objectives of the shareholders, and the industry. In ascertaining a value for the business, a professional accountant or business valuator should be consulted.

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 1 9

Here is a brief overview of several common business valuation methods.

capitalized earnings: A maintainable level of operations is determined with reference to financial and operating risks.

capitalized cash flow: Before-tax historical and forecasted cash flows are determined, adjustments are made for unusual transactions and owner/management salaries and bonuses to determine the level of maintainable cash flow. The maintainable cash flow level is then capitalized by an appropriate multiple.

discounted cash flow: This method attempts to state in current dollars the value of future cash inflows and outflows. It is therefore most relevant for valuing concerns with a limited life, such as a natural resource company.

Adjusted net tangible equity: With this method, all the assets and liabilities of the company are restated to their current market values. If shares are being valued, the tax-shield related to the incremental market value of depreciable assets should be deducted and consideration should be given to any contingent liabilities.

liquidation: This approach is used primarily when a business is no longer a viable concern and the liquidation value of its assets is higher than its going concern value.

In certain industries, a rule of thumb may serve as a guide to valuation. For a detailed explanation of valuation methods, see “Valuation of Businesses, A Practical Guide” published by CCH Canada.

2 0 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

corPorATe AccounTing And life insurAnce

The treatment of life insurance for accounting and tax purposes will depend on a number of factors, such as whether the policy is term or permanent insurance, when the policy was bought, and the business reasons for its purchase.

Here is an overview of some key accounting and tax treatments relating to corporate-owned life insurance policies.

Deductibility of premiums

In general, life insurance premiums are not deductible for tax purposes. When life insurance premiums are paid, the full amount is expensed. At year-end, an adjustment is made when filing the company’s corporate tax return, with the premium amount added back into income for tax purposes.

There are some exceptions to this general rule, the most common being the ability to deduct a portion of the premium for tax purposes where the insurance is required as collateral against a debt owed to a restricted financial institution, such as a bank, trust company, or credit union.

Presenting cash surrender value (Csv) in the financial statements

Most permanent insurance policies have a CSV. This is the amount of money the policy owner will receive if the policy owner cancels the coverage and surrenders the policy to the insurance company.

The CSV of a corporate-owned life insurance policy is a corporate asset and should be included in the company’s balance sheet. The materiality of the amount and the intention of the corporation’s management will determine where the amount should be included.

If there is no intention to dispose of the policy, the CSV should be classified in the “non-current asset” section under “other assets” or as “life insurance cash surrender value” on the balance sheet. Disclosure is optional depending on the materiality of the amount. If management’s intention is to do a full or partial disposition of the policy, the cash surrender value should be classified as “cash and cash equivalents” in the “current assets” section of the balance sheet.

At the point in time that CSV become available to the business, year-end adjustments should be made to the retained earnings account to set up the CSV in the financial statements. The adjustment could also be made to the income statement and then backed out of the income for tax purposes on the reconciliation of taxable income.

The typical entry for an increase in cash surrender value of $5,000 might be:

Other assets – CSV

Retained earnings – Investment income $5000

$5000

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 2 1

insurance proceeds and the capital dividend account

When a private corporation is both the owner and beneficiary of a life insurance policy, and the insured shareholder or employee dies, the portion of the life insurance proceeds that exceeds the ACB is credited to the capital dividend account of the corporation for tax purposes.4

The ACB is the base value from which accrued income and policy gains are measured, and changes with each policy transaction. ACB is defined in subsection 148(9) of the Income Tax Act (Canada).

The capital dividend account is a notional account that records tax-exempt amounts received by a privately owned corporation that is resident in Canada. The purpose of this account is to allow a corporation to flow amounts it receives on a tax-free basis out to Canadian resident shareholders without creating tax in the shareholders’ hands. An amount equal to the balance in the capital dividend account can be paid out as a tax-free capital dividend to shareholders, if proper tax elections are filed.

For example, if the life insurance proceeds are $100,000 and the ACB of the policy is $20,000, then $80,000 can be credited to the capital dividend account and can be paid out as a tax-free dividend. The balance of the life insurance proceeds can be paid out as a taxable dividend to shareholders.5

In the early years of a permanent life insurance policy the ACB may be high. In later years, the ACB will normally be low or equal to “nil”.

The insurance policy carrier can provide an accurate calculation of your policy’s ACB. Here is a quick look at the factors that will increase or decrease it:

the aCB is increased by the following amounts:

For policies last acquired on or before December 1, 1982, the full premium for the policy, including premiums for all riders.

For policies last acquired on or after December 2, 1982, the premium for the basic policy and term insurance riders paid by or on behalf of the owner of the policy, less the net cost of pure insurance (NCPI).

The cost of all interests in the policy acquired by the owner of the policy.

Policy gains previously included in income from dividends, policy loans received, etc.

Certain policy loan repayments.

Any mortality gain resulting from the death of the policyholder where an interest in the policy has not been rolled over to the surviving spouse.

4 The ACB of the policy will not reduce the credited amount where the corporation is the beneficiary but not the owner of the policy, so long as there is a business purpose for the designation.

5 The capital dividend account can be reduced by certain amounts, such as the non-deductible 50 per cent of a capital loss, and itself become a negative amount. If the capital dividend account is negative when it records an increase for life insurance proceeds, the available capital dividend could be less than the insurance proceeds actually received by the corporation.

2 2 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

aCB is decreased by the following amounts:

The total of all amounts, each of which is the proceeds of disposition of the policyholder’s interest in the policy that the policyholder became entitled to receive before that time.

The amount of a policy loan outstanding at March 31, 1978.

For the policy acquired after December 1, 1982, all the premium related to an accidental death benefit, a disability benefit, an age rating or extra premium on account of a substandard life, a guaranteed insurability option and any other prescribed benefits that are ancillary to the policy (S.148(9).ITA).

taxation on disposition of a policy

The owner of the policy must include taxable policy gains in income for tax purposes. The taxable gain is equal to the proceeds of disposition, minus the ACB. The gain is excluded from the description of a “capital gain for a taxation year from the disposition of any property” so that 100 per cent of the gain is included in, and taxed as, ordinary income and not as a taxable capital gain with a 50 per cent income inclusion.6

dispositions include:

A surrender, including a partial surrender such as a policy withdrawal and a transfer of funds to a segregated fund of the insurer. For a partial surrender, each dollar of cash value removed from the policy will be taxable in the same proportion as the total cash value would be if a full surrender occurred.

Policy loans made after March 31, 1978, including automatic premium loans and capitalization of unpaid loan interest. Policy loans are considered to come first from the ACB on a tax-free basis and then from the taxable portion of the cash value.

The dissolution of the owner’s interest on maturity of the policy.

A disposition by operation of law – such as voiding a policy.

Lapse due to non-payment of premiums where the policy is not reinstated during the calendar year of lapse or within 60 days thereafter.

Annuitization of a policy last acquired after December 1, 1982.

Proceeds of disposition

The proceeds of disposition of an interest in a life insurance policy are the amount that the policyholder receives or the beneficiary is entitled to receive on disposition.

When an interest in a life insurance policy is disposed of by way of gift or distribution from a corporation to a person with whom the policyholder is not dealing at arm’s length, the proceeds of disposition is deemed to equal the cash surrender value of the policy.

In addition, if a corporation transfers a life insurance policy to its employee or shareholder for payment that is less than the FMV of the policy at the time, the difference may be included in the income of the new owner and taxable as an employee or shareholder benefit.

6 S. 39(1)(a)(iii) ITA

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 2 3

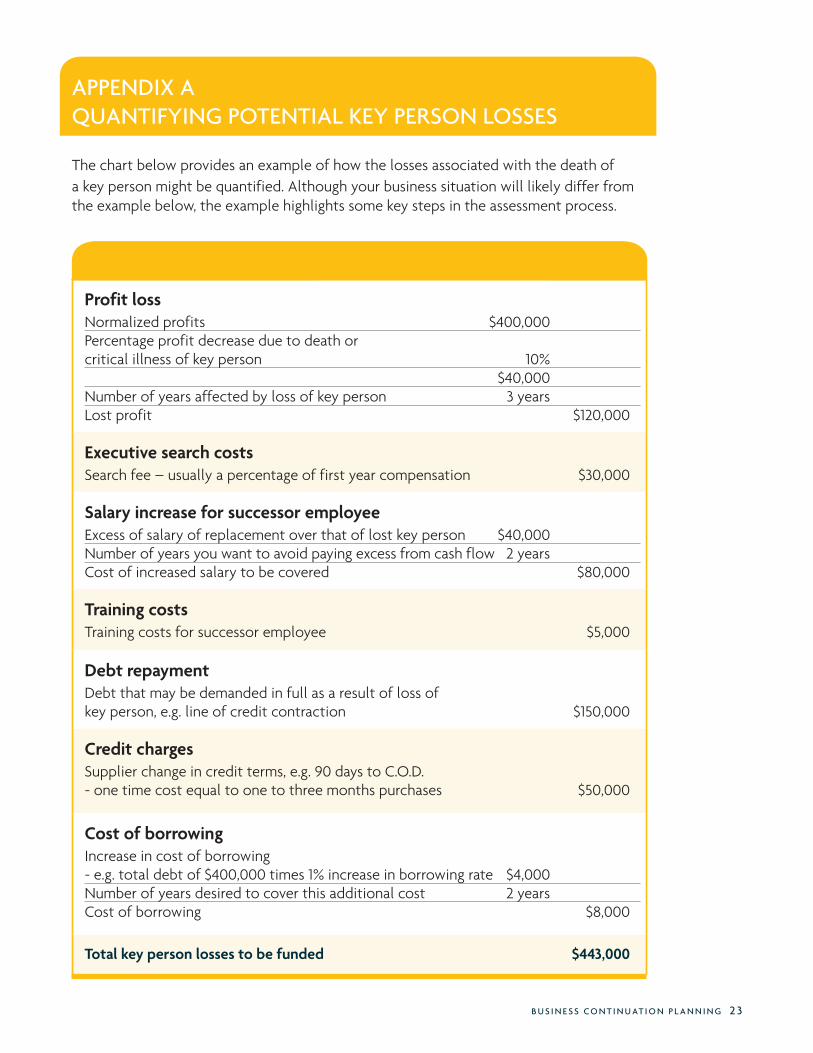

APPendix A QuAnTifying PoTenTiAl Key Person losses

The chart below provides an example of how the losses associated with the death of a key person might be quantified. Although your business situation will likely differ from the example below, the example highlights some key steps in the assessment process.

Profit lossNormalized profits $400,000Percentage profit decrease due to death or critical illness of key person 10% $40,000Number of years affected by loss of key person 3 yearsLost profit $120,000

executive search costsSearch fee – usually a percentage of first year compensation $30,000

salary increase for successor employeeExcess of salary of replacement over that of lost key person $40,000Number of years you want to avoid paying excess from cash flow 2 yearsCost of increased salary to be covered $80,000

training costsTraining costs for successor employee $5,000

Debt repaymentDebt that may be demanded in full as a result of loss of key person, e.g. line of credit contraction $150,000

Credit chargesSupplier change in credit terms, e.g. 90 days to C.O.D.- one time cost equal to one to three months purchases $50,000

Cost of borrowingIncrease in cost of borrowing- e.g. total debt of $400,000 times 1% increase in borrowing rate $4,000Number of years desired to cover this additional cost 2 yearsCost of borrowing $8,000

total key person losses to be funded $443,000

2 4 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

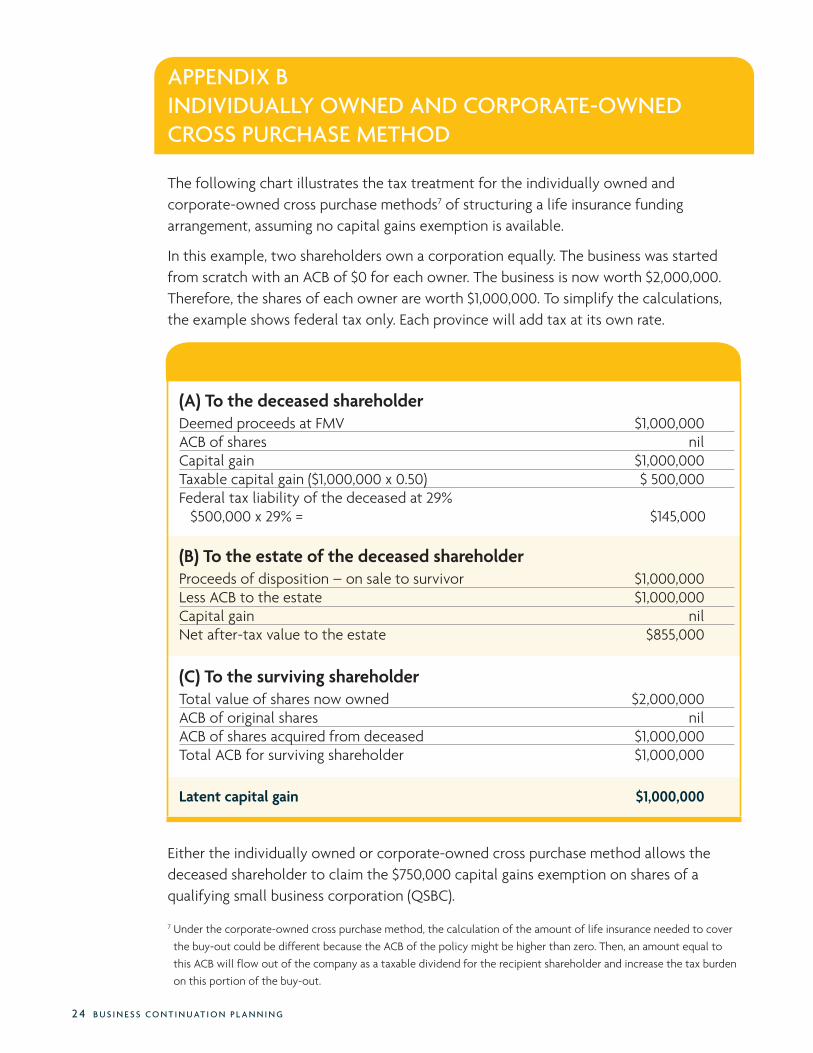

APPendix b individuAlly owned And corPorATe-owned cross PurcHAse meTHod

The following chart illustrates the tax treatment for the individually owned and corporate-owned cross purchase methods7 of structuring a life insurance funding arrangement, assuming no capital gains exemption is available.

In this example, two shareholders own a corporation equally. The business was started from scratch with an ACB of $0 for each owner. The business is now worth $2,000,000. Therefore, the shares of each owner are worth $1,000,000. To simplify the calculations, the example shows federal tax only. Each province will add tax at its own rate.

Either the individually owned or corporate-owned cross purchase method allows the deceased shareholder to claim the $750,000 capital gains exemption on shares of a qualifying small business corporation (QSBC).

7 Under the corporate-owned cross purchase method, the calculation of the amount of life insurance needed to cover

the buy-out could be different because the ACB of the policy might be higher than zero. Then, an amount equal to

this ACB will flow out of the company as a taxable dividend for the recipient shareholder and increase the tax burden

on this portion of the buy-out.

(a) to the deceased shareholderDeemed proceeds at FMV $1,000,000ACB of shares nilCapital gain $1,000,000Taxable capital gain ($1,000,000 x 0.50) $ 500,000Federal tax liability of the deceased at 29% $500,000 x 29% = $145,000

(B) to the estate of the deceased shareholderProceeds of disposition – on sale to survivor $1,000,000Less ACB to the estate $1,000,000Capital gain nilNet after-tax value to the estate $855,000

(C) to the surviving shareholderTotal value of shares now owned $2,000,000ACB of original shares nilACB of shares acquired from deceased $1,000,000Total ACB for surviving shareholder $1,000,000

latent capital gain $1,000,000

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 2 5

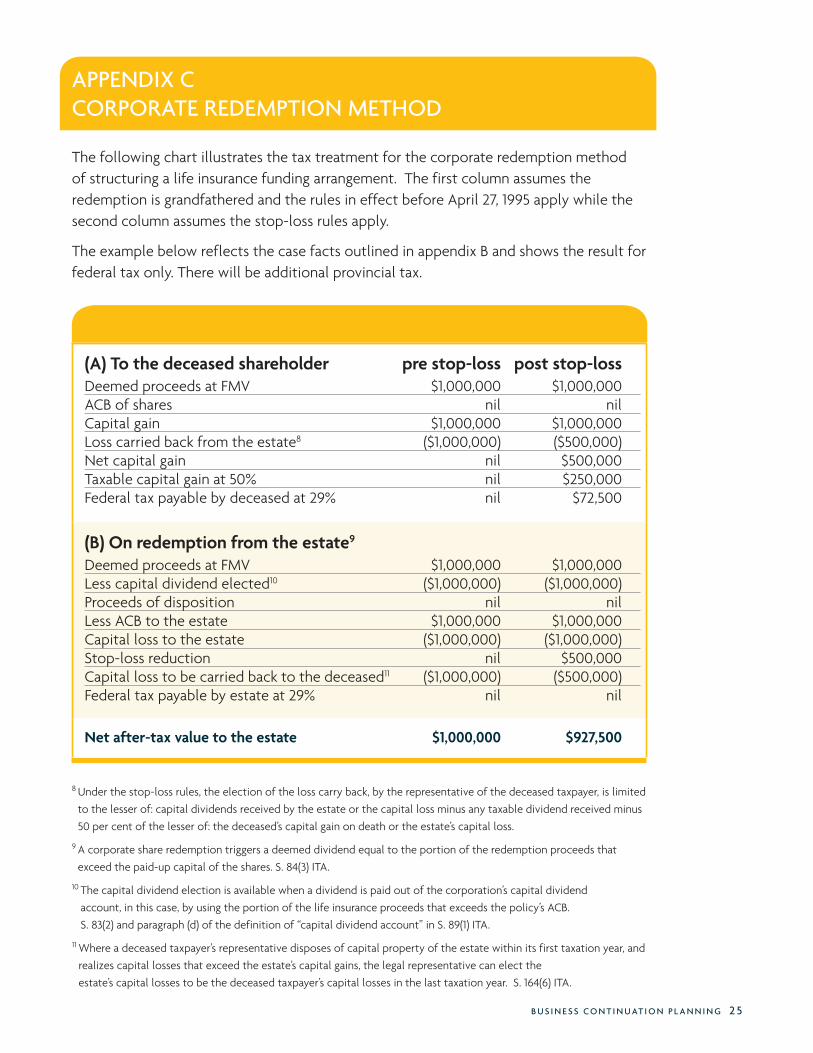

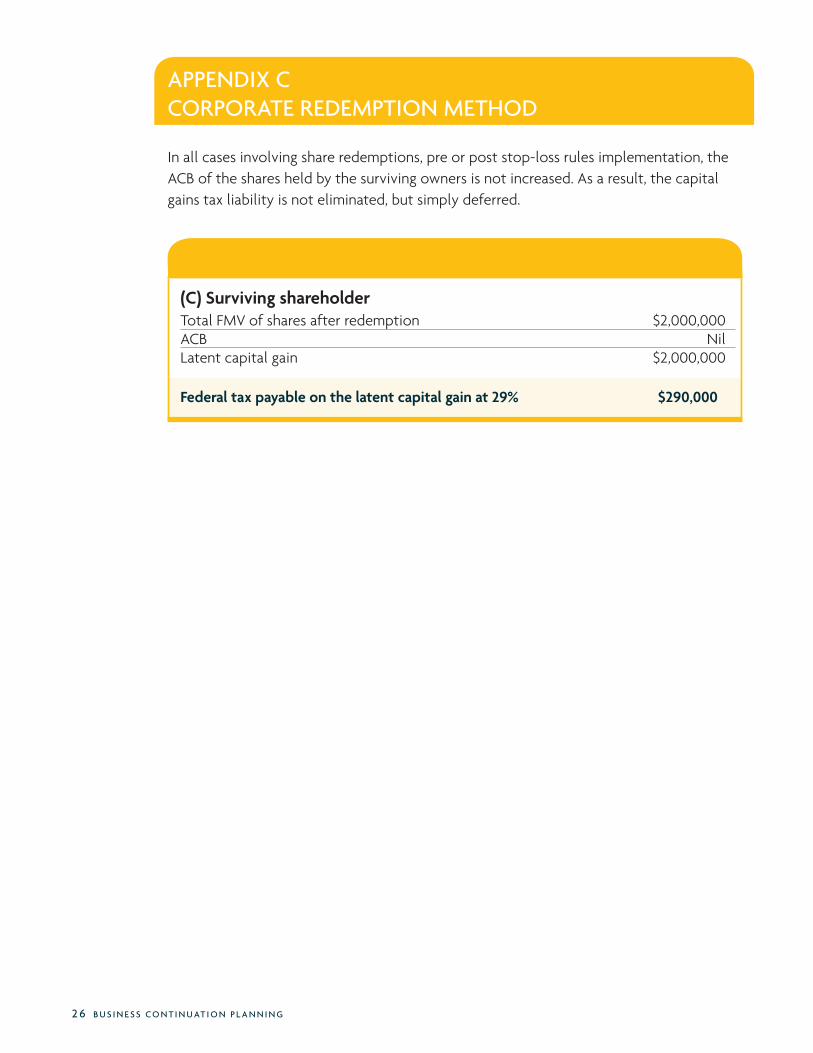

APPendix c corPorATe redemPTion meTHod

The following chart illustrates the tax treatment for the corporate redemption method of structuring a life insurance funding arrangement. The first column assumes the redemption is grandfathered and the rules in effect before April 27, 1995 apply while the second column assumes the stop-loss rules apply.

The example below reflects the case facts outlined in appendix B and shows the result for federal tax only. There will be additional provincial tax.

8 Under the stop-loss rules, the election of the loss carry back, by the representative of the deceased taxpayer, is limited

to the lesser of: capital dividends received by the estate or the capital loss minus any taxable dividend received minus

50 per cent of the lesser of: the deceased’s capital gain on death or the estate’s capital loss.

9 A corporate share redemption triggers a deemed dividend equal to the portion of the redemption proceeds that

exceed the paid-up capital of the shares. S. 84(3) ITA.

10 The capital dividend election is available when a dividend is paid out of the corporation’s capital dividend

account, in this case, by using the portion of the life insurance proceeds that exceeds the policy’s ACB.

S. 83(2) and paragraph (d) of the definition of “capital dividend account” in S. 89(1) ITA.

11 Where a deceased taxpayer’s representative disposes of capital property of the estate within its first taxation year, and

realizes capital losses that exceed the estate’s capital gains, the legal representative can elect the

estate’s capital losses to be the deceased taxpayer’s capital losses in the last taxation year. S. 164(6) ITA.

(a) to the deceased shareholder pre stop-loss post stop-lossDeemed proceeds at FMV $1,000,000 $1,000,000ACB of shares nil nilCapital gain $1,000,000 $1,000,000Loss carried back from the estate8 ($1,000,000) ($500,000)Net capital gain nil $500,000Taxable capital gain at 50% nil $250,000Federal tax payable by deceased at 29% nil $72,500

(B) on redemption from the estate9

Deemed proceeds at FMV $1,000,000 $1,000,000Less capital dividend elected10 ($1,000,000) ($1,000,000)Proceeds of disposition nil nilLess ACB to the estate $1,000,000 $1,000,000Capital loss to the estate ($1,000,000) ($1,000,000)Stop-loss reduction nil $500,000Capital loss to be carried back to the deceased11 ($1,000,000) ($500,000)Federal tax payable by estate at 29% nil nil

net after-tax value to the estate $1,000,000 $927,500

2 6 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

APPendix c corPorATe redemPTion meTHod

In all cases involving share redemptions, pre or post stop-loss rules implementation, the ACB of the shares held by the surviving owners is not increased. As a result, the capital gains tax liability is not eliminated, but simply deferred.

(C) surviving shareholder Total FMV of shares after redemption $2,000,000ACB NilLatent capital gain $2,000,000

Federal tax payable on the latent capital gain at 29% $290,000

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 2 7

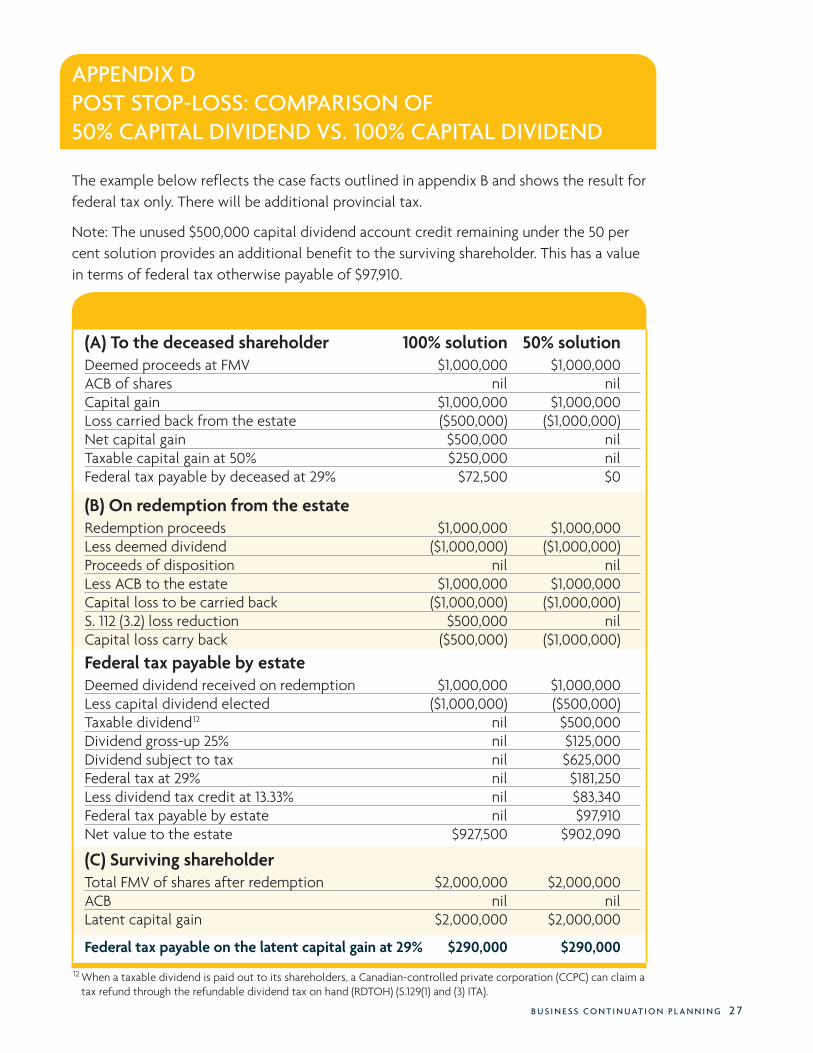

APPendix d PosT sToP-loss: comPArison of 50% cAPiTAl dividend vs. 100% cAPiTAl dividend

The example below reflects the case facts outlined in appendix B and shows the result for federal tax only. There will be additional provincial tax.

Note: The unused $500,000 capital dividend account credit remaining under the 50 per cent solution provides an additional benefit to the surviving shareholder. This has a value in terms of federal tax otherwise payable of $97,910.

12 When a taxable dividend is paid out to its shareholders, a Canadian-controlled private corporation (CCPC) can claim a tax refund through the refundable dividend tax on hand (RDTOH) (S.129(1) and (3) ITA).

(a) to the deceased shareholder 100% solution 50% solutionDeemed proceeds at FMV $1,000,000 $1,000,000ACB of shares nil nilCapital gain $1,000,000 $1,000,000Loss carried back from the estate ($500,000) ($1,000,000)Net capital gain $500,000 nilTaxable capital gain at 50% $250,000 nilFederal tax payable by deceased at 29% $72,500 $0

(B) on redemption from the estateRedemption proceeds $1,000,000 $1,000,000Less deemed dividend ($1,000,000) ($1,000,000)Proceeds of disposition nil nilLess ACB to the estate $1,000,000 $1,000,000Capital loss to be carried back ($1,000,000) ($1,000,000)S. 112 (3.2) loss reduction $500,000 nilCapital loss carry back ($500,000) ($1,000,000)

Federal tax payable by estateDeemed dividend received on redemption $1,000,000 $1,000,000Less capital dividend elected ($1,000,000) ($500,000)Taxable dividend12 nil $500,000Dividend gross-up 25% nil $125,000Dividend subject to tax nil $625,000Federal tax at 29% nil $181,250Less dividend tax credit at 13.33% nil $83,340Federal tax payable by estate nil $97,910Net value to the estate $927,500 $902,090

(C) surviving shareholderTotal FMV of shares after redemption $2,000,000 $2,000,000ACB nil nilLatent capital gain $2,000,000 $2,000,000

Federal tax payable on the latent capital gain at 29% $290,000 $290,000

2 8 b u s i n e s s c o n T i n u AT i o n P l A n n i n g

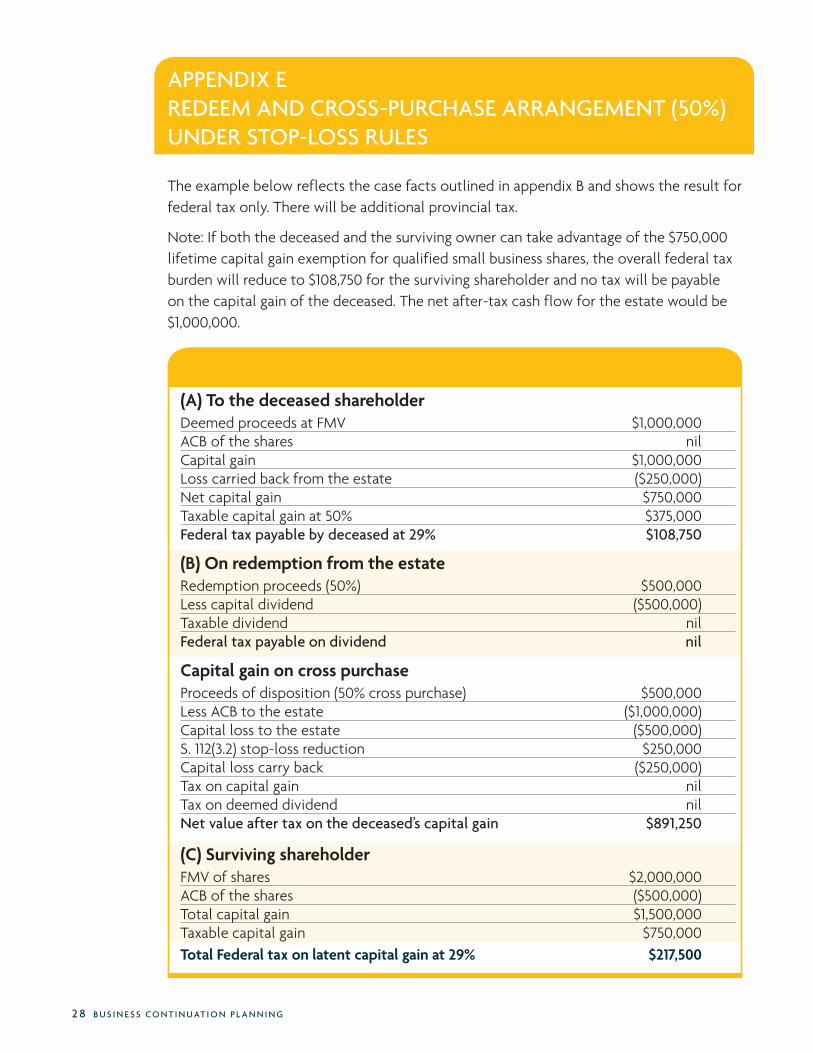

APPendix e redeem And cross-PurcHAse ArrAngemenT (50%) under sToP-loss rules

The example below reflects the case facts outlined in appendix B and shows the result for federal tax only. There will be additional provincial tax.

Note: If both the deceased and the surviving owner can take advantage of the $750,000 lifetime capital gain exemption for qualified small business shares, the overall federal tax burden will reduce to $108,750 for the surviving shareholder and no tax will be payable on the capital gain of the deceased. The net after-tax cash flow for the estate would be $1,000,000.

(a) to the deceased shareholderDeemed proceeds at FMV $1,000,000ACB of the shares nilCapital gain $1,000,000Loss carried back from the estate ($250,000)Net capital gain $750,000Taxable capital gain at 50% $375,000federal tax payable by deceased at 29% $108,750

(B) on redemption from the estateRedemption proceeds (50%) $500,000Less capital dividend ($500,000)Taxable dividend nilfederal tax payable on dividend nil

Capital gain on cross purchaseProceeds of disposition (50% cross purchase) $500,000Less ACB to the estate ($1,000,000)Capital loss to the estate ($500,000)S. 112(3.2) stop-loss reduction $250,000Capital loss carry back ($250,000)Tax on capital gain nilTax on deemed dividend nilnet value after tax on the deceased’s capital gain $891,250

(C) surviving shareholderFMV of shares $2,000,000ACB of the shares ($500,000)Total capital gain $1,500,000Taxable capital gain $750,000total Federal tax on latent capital gain at 29% $217,500

b u s i n e s s c o n T i n u AT i o n P l A n n i n g 2 9

noTes

© Sun Life Assurance Company of Canada, 2012.810-2882-02-12

life’s brighter under the sun

Sun Life Financial is a leading international financial services organization providing a diverse range of

wealth accumulation and protection products and services to individuals and corporate customers.

Tracing its roots back to 1865, Sun Life Financial and its partners today have operations in key markets

worldwide, including Canada, the United States, the United Kingdom, Hong Kong, the Philippines, Japan,

Indonesia, India, China and Bermuda.

Sun Life Financial Inc. trades on the Toronto (TSX), New York (NYSE) and Philippine (PSE) stock exchanges

under ticker symbol “SLF”.

Questions? We’re here to help.

for more information about any sun life financial products or services, visit www.sunlife.ca | call 1 877 sun-life (1 877 786-5433)