112

I.2. Innovation 1 Thursday 14 November 13

I.2. Innovation

1

Thursday 14 November 13

the essence of free market economics• Capitalism is an evolutionary process;

capitalism never can be stationary.

• The fundamental impulse comes from the new consumers' goods, the new methods of production or transportation, the new markets, the new forms of industrial organization that capitalist enterprise creates. These incessantly revolutionize the economic structure from within, incessantly destroying the old one, incessantly creating a new one.

• Creative destruction is the essential fact about capitalism. it is what capitalism consists in and what every capitalist concern has got to live in.

2

Joseph Alois Schumpeter: Capitalism, socialism and

democracy 1942eigen samenvatting

Thursday 14 November 13

32

oops...

technology strategy for managers and entrepreneurs, Scott Shane 2009

Thursday 14 November 13

Some thoughts• Innovation are only relevant if they add value

• Why innovate as a company?• To differentiate

• New! Improved!• More value for customer -> higher price + better market position• Create new market; first mover advantage

• To catch up• Neutralize the above

• To reduce costs• Colruyt and IT, RF-ID, electric cars...• = make more money

4

Thursday 14 November 13

2.1. some typologies of innovation

5

Thursday 14 November 13

Some typologies of innovation

6

• Technology innovations vs. Business innovations

• The kind of people behind the innovation

• Redefining the engineerings specs...

• Redefining the value chain....

• The impact of the innovation from the perspective of the current suppliers

Thursday 14 November 13

2.1.1 Technology innovation vs. business innovation

7

Thursday 14 November 13

Technology innovation...

8

Thursday 14 November 13

Business innovation• Innovation in the way the business is conducted

• Innovation in manufacturing methods and processes• Henri Ford and mass production

• Innovation in distribution channels• Dell• Tupperware

• Innovation in revenue/business models• Free newspapers• Internet

• ...

9

Thursday 14 November 13

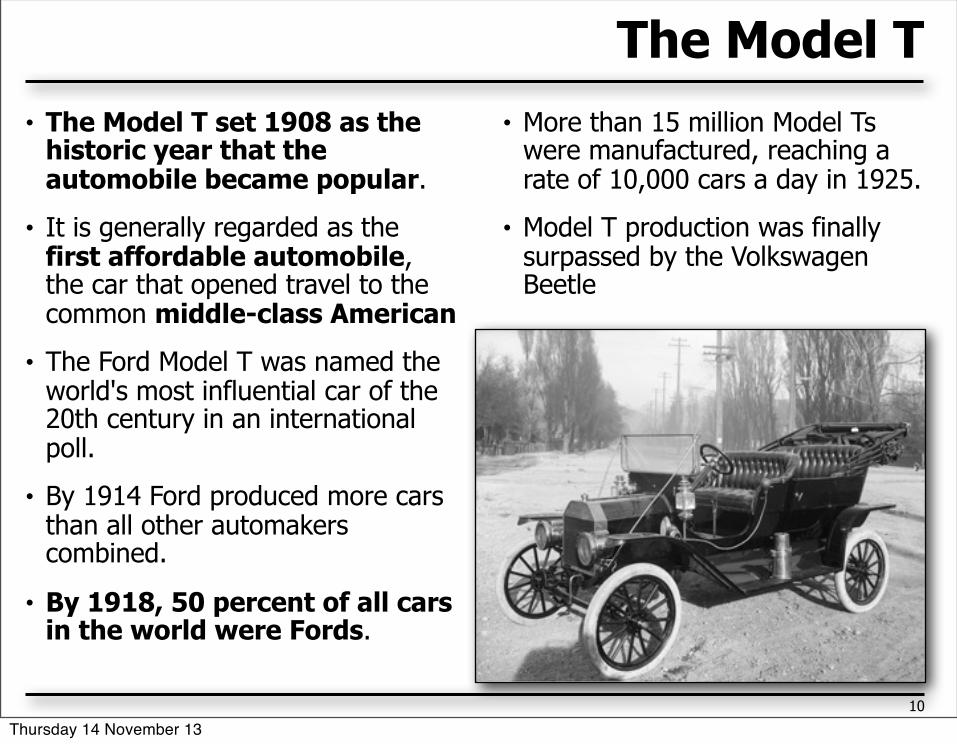

The Model T• The Model T set 1908 as the

historic year that the automobile became popular.

• It is generally regarded as the first affordable automobile, the car that opened travel to the common middle-class American

• The Ford Model T was named the world's most influential car of the 20th century in an international poll.

• By 1914 Ford produced more cars than all other automakers combined.

• By 1918, 50 percent of all cars in the world were Fords.

• More than 15 million Model Ts were manufactured, reaching a rate of 10,000 cars a day in 1925.

• Model T production was finally surpassed by the Volkswagen Beetle

•

10

Thursday 14 November 13

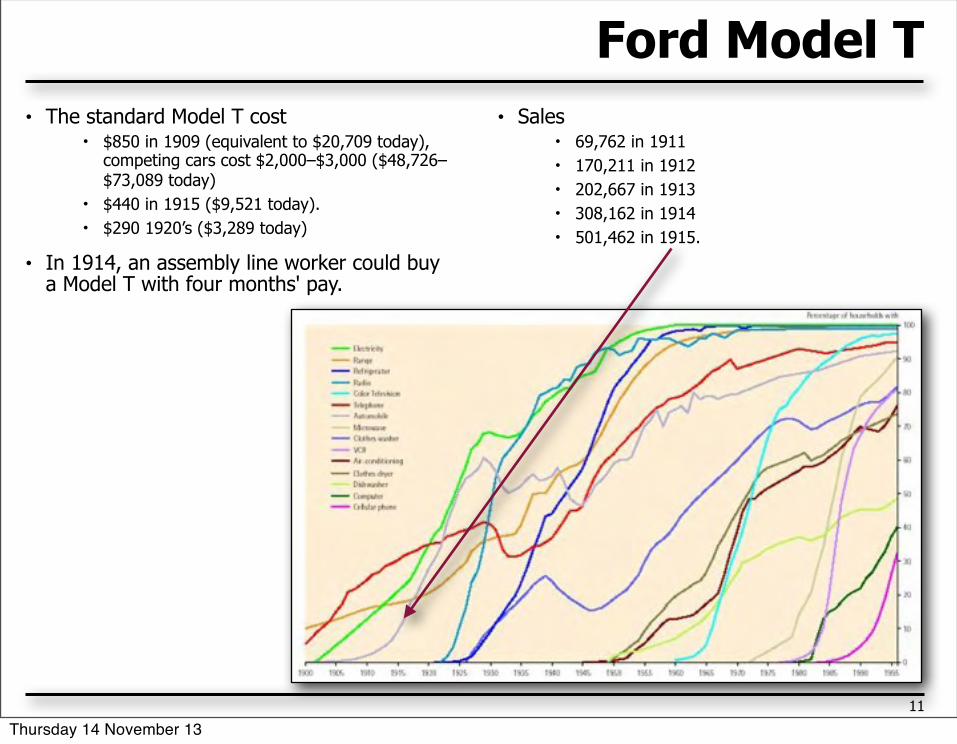

Ford Model T• The standard Model T cost

• $850 in 1909 (equivalent to $20,709 today), competing cars cost $2,000–$3,000 ($48,726–$73,089 today)

• $440 in 1915 ($9,521 today).• $290 1920’s ($3,289 today)

• In 1914, an assembly line worker could buy a Model T with four months' pay.

• Sales • 69,762 in 1911• 170,211 in 1912• 202,667 in 1913• 308,162 in 1914• 501,462 in 1915.

11

Thursday 14 November 13

Business innovation: the assembly line• The Model T was the first automobile

mass produced on assembly lines with completely interchangeable parts.

• Before the 20th century, most manufactured products were made individually by hand. A single craftsman or team of craftsmen would create each part of a product and assemble them into the final product, making cut-and-try changes in the parts until they fit and could work together

• The assembly line concept was introduced after a visit by an employee to a slaughterhouse and viewing what was referred to as the "disassembly line". The efficiency of one person removing the same piece over and over caught his attention.

• In 1910 Ford's cars came off the line in three-minute intervals, reducing production time by a factor of eight (requiring 12.5 hours before, 93 minutes afterwards), while using less manpower.

• The knowledge and skills needed by a factory worker were reduced to 84 areas.

• 1913 Experimenting with mounting body on Model T chassis. Ford tested various

assembly methods to optimize the procedures before permanently installing the equipment. The actual assembly line

used an overhead crane to mount the body.

12

Thursday 14 November 13

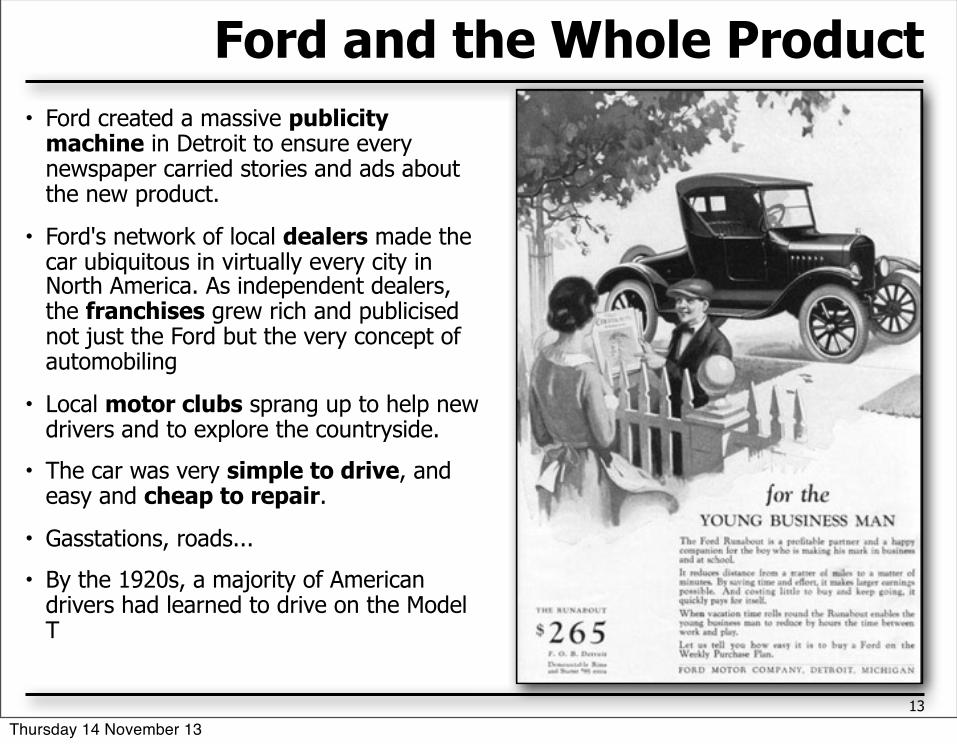

Ford and the Whole Product• Ford created a massive publicity

machine in Detroit to ensure every newspaper carried stories and ads about the new product.

• Ford's network of local dealers made the car ubiquitous in virtually every city in North America. As independent dealers, the franchises grew rich and publicised not just the Ford but the very concept of automobiling

• Local motor clubs sprang up to help new drivers and to explore the countryside.

• The car was very simple to drive, and easy and cheap to repair.

• Gasstations, roads...

• By the 1920s, a majority of American drivers had learned to drive on the Model T

13

Thursday 14 November 13

Welfare capitalism à la manière de Ford• Ford astonished the world in 1914 by offering a $5 per day wage ($110 in

current dollar terms), which more than doubled the wage of most of his workers.

• The move proved extremely profitable; instead of constant turnover of employees, the best mechanics in Detroit flocked to Ford, bringing their human capital and expertise, raising productivity, and lowering training costs.

• It also set a new, reduced workweek in 1922 a six 8-hour days, giving a 48-hour week. The program started with Saturdays as workdays and sometime later it was changed to a day off.

• Ford's policy also proved that paying people more would enable Ford workers to afford the cars they were producing and be good for the economy.

• The ‘profit-sharing’ was offered to employees who conducted their lives in a manner of which Ford's "Social Department" approved. They frowned on heavy drinking, gambling, and parents that don’t financially support their child. The Social Department used 50 investigators, plus support staff, to maintain employee standards; a large percentage of workers were able to qualify for this "profit-sharing."

14

Thursday 14 November 13

Business innovation at Ford• The assembly line

• Other organisation of work• Substantial productivity increase• But can be copied...

• Low-cost, high volume business model• Opens the car to middle class America

• High salary policy • Hire the best and keep them• Push labour prices up so people can afford cars

15

Thursday 14 November 13

Business innovation: Dell • Michael Saul Dell (born February 23, 1965) is an

American business magnate and the founder and chief executive officer of Dell Inc. He is one of the richest people in the world, with a net worth of US$14 billion in 2010.

• While a student at the University of Texas at Austin in 1984, Michael Dell founded the company with capital of $1000. Operating from Michael Dell's off-campus dormitory room at Dobie Center, the startup aimed to sell IBM PC-compatible computers built from stock components.

• The company advertised the systems in national computer magazines for sale directly to consumers, and custom assembled each ordered unit according to a selection of options. This offered buyers prices lower than those of retail brands.

• In 1992, Fortune magazine included Dell Computer Corporation in its list of the world's 500 largest companies. Michael Dell became the youngest CEO of a Fortune 500 company.

• In 1996, Dell began selling computers via its web site.

• Dell had 13.6% of the global PC market in the third quarter of 2008, and is second in global computer sales, behind Hewlett-Packard.

•

16

Thursday 14 November 13

Value chain innovation

17

Order Manufacturer Shipment

Manufacturer Distributor Retailer Enduser

Enduser

Thursday 14 November 13

Et alors?

18

Order Manufacturer Shipment

Manufacturer Distributor Retailer Enduser

Enduser

Stock

Cash in

Thursday 14 November 13

Dell business model innovation • Build to order, ship direct

• Instead of manufacturer -> distributor -> retailer -> customer

• Existing PC suppliers Compaq, IBM,Olivetti... Were tied to their channel and could (initially) not follow Dells example

• Advantages of Dell business model• No stock @ manufacturer,

distributor, retailer -> cost reduction • Online custom configiration• No outdated inventory• (Generally): cash in before

production begins• Ride on Internet adoption wave

19

Thursday 14 November 13

Last 10 years...

20

Thursday 14 November 13

Business innovation at Tupperware • Tupperware pioneered the direct

marketing strategy made famous by the Tupperware party.

• A Tupperware party is run by a Tupperware consultant for a host who invites friends and neighbors into his or her home to see the product line.

• Tupperware hosts are rewarded with free products based on the level of sales made at their party. Parties also take place in workplaces, schools, and other community groups.

21

Thursday 14 November 13

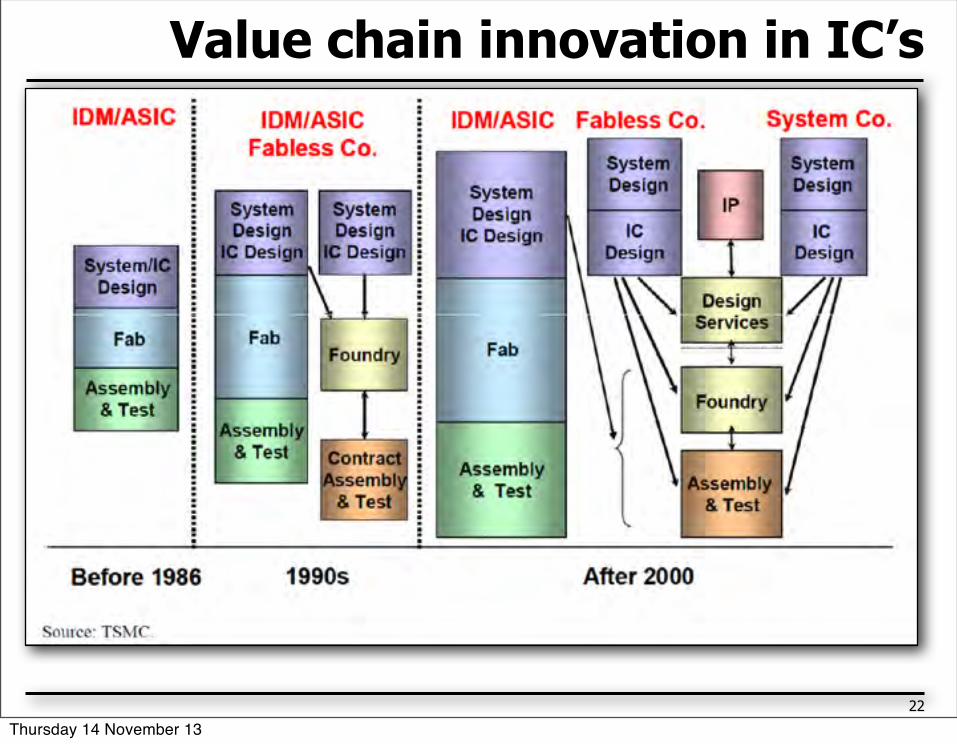

Value chain innovation in IC’s

22

Thursday 14 November 13

2.2.5 The kind of people behind the innovation

23

Thursday 14 November 13

Who initiates the innovation?• Industry veterans

• ‘The product starter’ (Prof Clarysse)• Innovation/ venture started by an individual or a small team with roots in the

industry• Their business focus is a product, often a creative use of existing technologies

to design new ways of solving a business problem. • ‘Let’s port this software from a minicomputer to a Macintosh’

• They often leave the company they work for because they could not develop their ideas inside this organization.

• Often they become competitors of their previous employer. • As the cycle to get to a product is often quite short and market contacts have

been established, they rarely need large amounts of capital to start.• Example: Artwork Systems

• Researchers• Technology starter• Innovation generated in scientific + research context• Results often in patents • Often in initial phase, requiring significant developments.

• Extensive funding is a must• Researchers often lack industry expertise• And should find partners• See Optrima

• The egg-of-columbus• Great idea, but no IP position, no network, no credentials...• Often quite difficult to successfully go to market

24

Thursday 14 November 13

2.2.1 changing the engineering specs:radical innovation vs. incremental innovation

25

Thursday 14 November 13

• Incremental innovation

• Improvements

• Introduces relatively minor changes

• Often happens once standards has been established

• Typically drives rapid performance improvement

• Exploits the potential of the established design

• Typically reinforces position of incumbent

• Radical innovation

• redefining the engineering specs

• Based on a different set of engineering principles

• May open up whole new markets and potential applications

• May create great difficulties for incumbent firms

• Can be basis for successful entry by insurgent

• It may take while...

26

Thursday 14 November 13

45

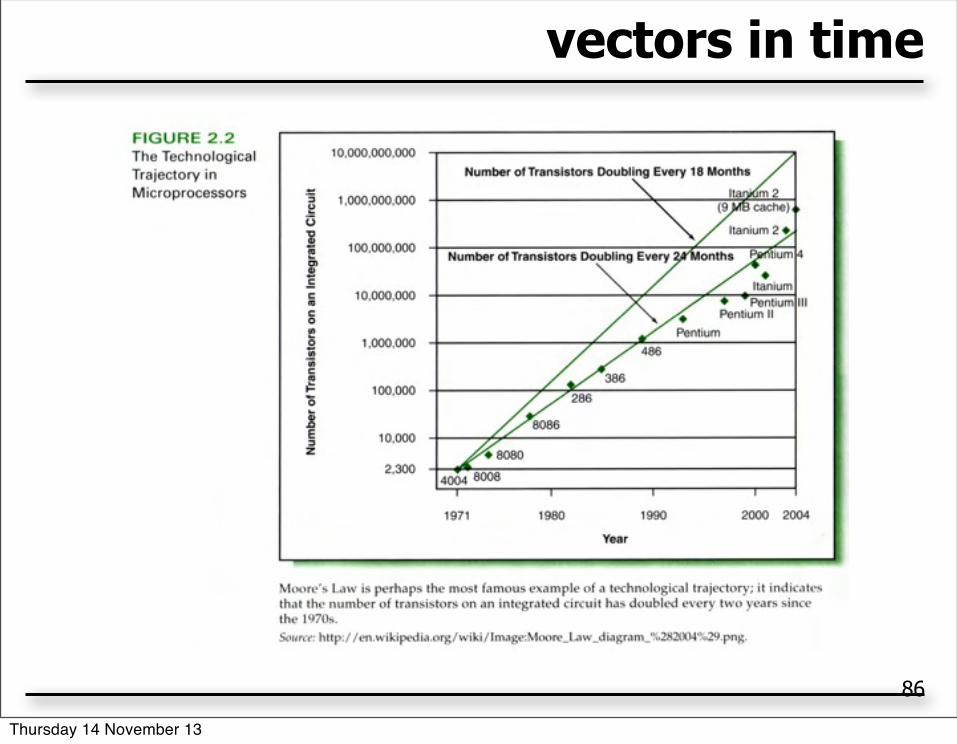

The mother of all incremental innovations: Moore’s Law

Thursday 14 November 13

Incremental innovation• Powershot G5 Features (2003):

• 5-megapixel CCD• Still images up to 2592 x 1944

pixels• ISO 50 - 400• 1.8-inch 270° Vari-Angle color LCD

viewfinder/monitor• Movie mode with sound: 320x240

and 160x120 up to 180 sec.

• Powershot G10 Features (2008):• 14.7-megapixel CCD• Image sizes up to 4416x 3312

pixels• ISO 50 - 1600• 3.0-inch 270° Vari-Angle color LCD

viewfinder/monitor• Movie clips 640 x 480 @ 30fps,

Maximum clip length 1 hour

28

Thursday 14 November 13

Radical technology trajectory...

29

512 byte

10 kilobyte

5 megabyte

140 kilobyte

Thursday 14 November 13

2.2.2 changing the value chain: sustaining innovation vs. disruptive innovation

30

Thursday 14 November 13

Clayton Christensen ‘the innovator’s dilemma’

• Sustaining innovations• those innovations that respond to the needs of the present (sophisticated)

customers of the company• Examples in harddisk industry: all innovations leading to higher storage capacity,

more reliability, higher speed, lower cost• All sustaining (radical or incremental) innovations were introduced by the market

leaders, even if they required investments, write-off of existing expertise… • Sustaining innovations almost never dislocates a market leader

• Disruptive innovations• those innovation that (initially) did not respond to the requirements of

existing customers, but ‘redefined’ the product and (thus) often initially address unserved customers

• Example in harddisk industry: smaller disks• These innovations are almost always ignored by the markt leader

• Who ‘do the right thing’: listen to their customers• It happens that these disruptive technologies mature and conquer the

mainstream market...

31

Thursday 14 November 13

The history of radio’s...

Thursday 14 November 13

The customer base of the disruptor New customers

– Teenagers and (portable) transistor radio’s– PC and 5,25 inch harddisks– Excavation of trenches in city areas

Overserved customers– Technologies may evolve too fast for the average customer– ‘Don’t need that extra storage’– Low-end customers are first to be open for new technology

The companies that want to adapt the technology to their market often fail, the ones that search a market for a given technology often succeed

51

Thursday 14 November 13

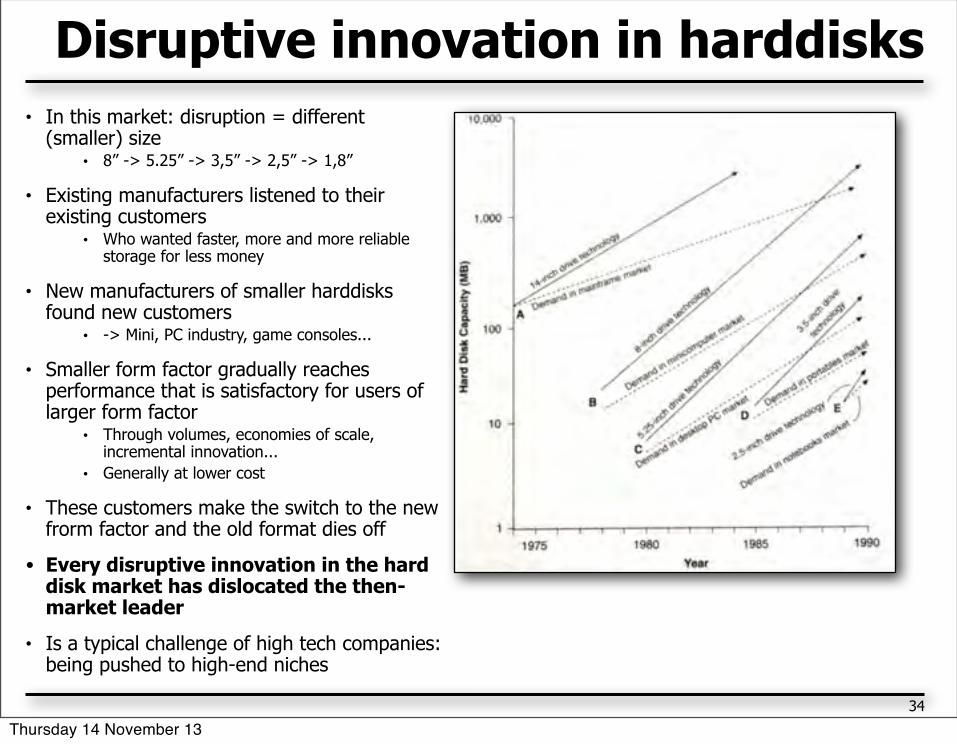

Disruptive innovation in harddisks • In this market: disruption = different

(smaller) size • 8” -> 5.25” -> 3,5” -> 2,5” -> 1,8”

• Existing manufacturers listened to their existing customers

• Who wanted faster, more and more reliable storage for less money

• New manufacturers of smaller harddisks found new customers

• -> Mini, PC industry, game consoles...

• Smaller form factor gradually reaches performance that is satisfactory for users of larger form factor

• Through volumes, economies of scale, incremental innovation...

• Generally at lower cost

• These customers make the switch to the new frorm factor and the old format dies off

• Every disruptive innovation in the hard disk market has dislocated the then-market leader

• Is a typical challenge of high tech companies: being pushed to high-end niches

34

Thursday 14 November 13

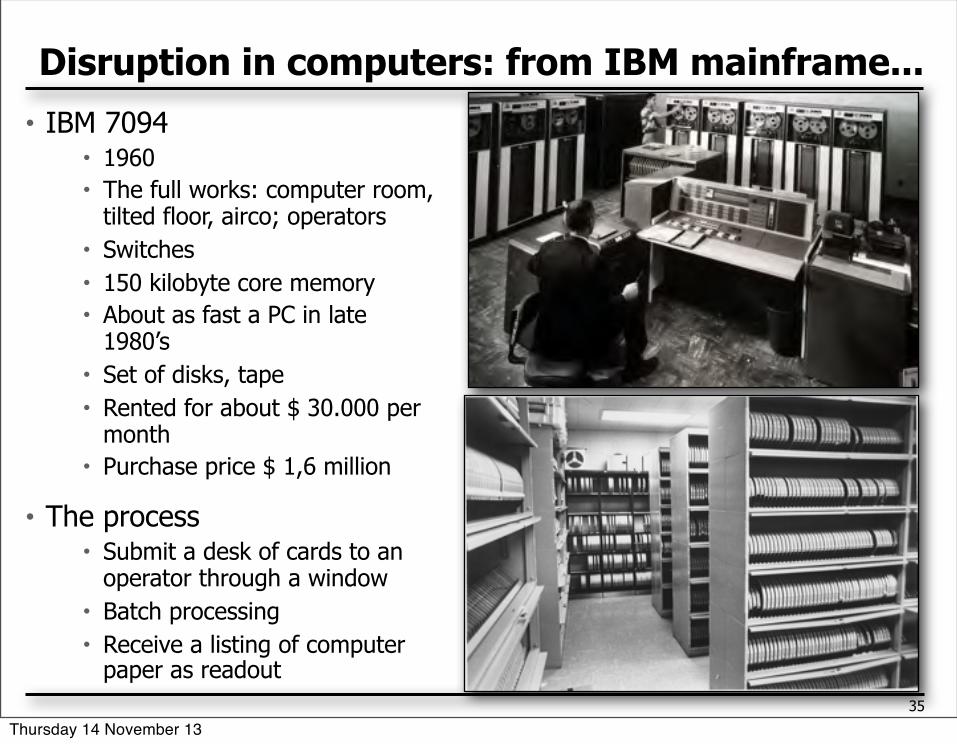

Disruption in computers: from IBM mainframe...• IBM 7094

• 1960• The full works: computer room,

tilted floor, airco; operators• Switches• 150 kilobyte core memory• About as fast a PC in late

1980’s• Set of disks, tape • Rented for about $ 30.000 per

month• Purchase price $ 1,6 million

• The process• Submit a desk of cards to an

operator through a window• Batch processing• Receive a listing of computer

paper as readout35

Thursday 14 November 13

IBM in the 60’s• IBM

• The technostructure (Galbraith): large, highly organized, vertically integrated

• The Organization Man; The IBM Way• 1963: $1,2 billion, 1965 $3 billion, 1970 $7,5 billion• 70% market share: IBM and the seven dwarfs • Socially responsible company: colored,

handicapped employees, benefits..• Offered computer at up to 60% discount if

universities offer course in computing

• 7 reserach labs• Solid state electronics• Tape and disk storage (Silicon Valley)• Programming languages• Logic circuits• Fundamentals of solid state physics and

mathematics

• Resdearch gave IBM advantage over its competitors

• Huge customer base to recoup investements• High barriers of entry in industry• Take off...

36

Thursday 14 November 13

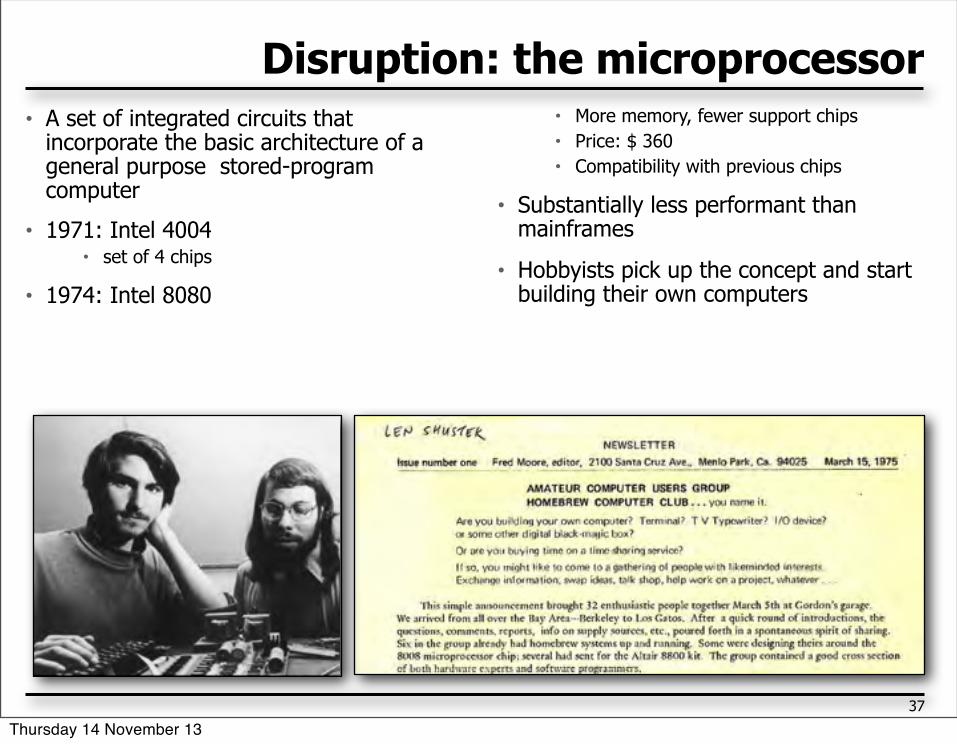

Disruption: the microprocessor• A set of integrated circuits that

incorporate the basic architecture of a general purpose stored-program computer

• 1971: Intel 4004• set of 4 chips

• 1974: Intel 8080

• More memory, fewer support chips• Price: $ 360• Compatibility with previous chips

• Substantially less performant than mainframes

• Hobbyists pick up the concept and start building their own computers

37

Thursday 14 November 13

...to the first personal computer• Altair 8800

• Company MITS• Edward Robert: designer• Small model-rocket hobby shop in

Alburquerque...

• Sold as kit for < $400• + option fully assembled & tested for $495 (1

year delivery delays...) • Around Intel 8080

• Cost $75 each

• Designed and promoted as a capable minicomputer

• Properties of Altair (and following PC’s)• Size• Micro-processor based• Prize• Capabilities• Open Bus architecture

• Plug-in devices possible

• The first users were hobbyists, and the first uses were games

38

Thursday 14 November 13

Microsoft• After reading the January 1, 1975

issue of Popular Electronics, Bill Gates called the creators of MITS, offering to demonstrate an implementation of the BASIC programming language for the system.

• Gates had neither an interpreter nor an Altair system, in the eight weeks before the demo he and Allen developed it. The interpreter worked and MITS agreed to distribute Altair BASIC.

• Gates left Harvard University, moved to Albuquerque, New Mexico where MITS was located, and founded Microsoft there.

• Price: $ 60 to $150 for ‘extended version’, sold with memory board. More expensive for other Intel 8080 systems

• Competitors existed, ‘but none was as good and Gate’s and Allen’s, and it was not long before word of that got around’

39

"to get a workstation running our software onto every desk and

eventually in every home”

Thursday 14 November 13

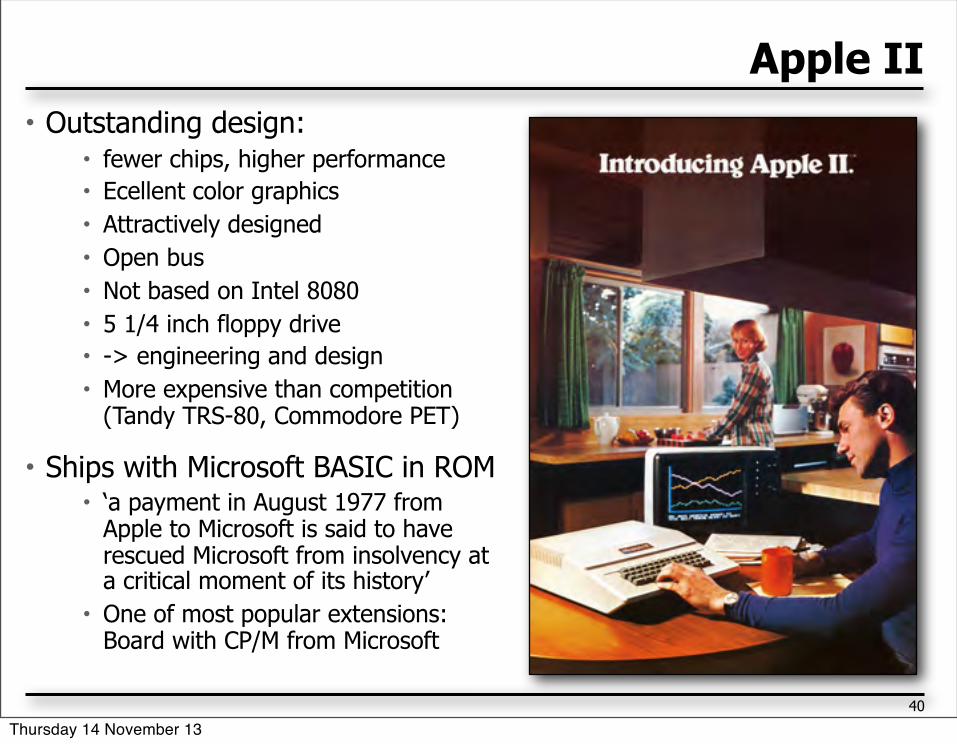

Apple II • Outstanding design:

• fewer chips, higher performance• Ecellent color graphics• Attractively designed• Open bus• Not based on Intel 8080• 5 1/4 inch floppy drive• -> engineering and design• More expensive than competition

(Tandy TRS-80, Commodore PET)

• Ships with Microsoft BASIC in ROM• ‘a payment in August 1977 from

Apple to Microsoft is said to have rescued Microsoft from insolvency at a critical moment of its history’

• One of most popular extensions: Board with CP/M from Microsoft

40

Thursday 14 November 13

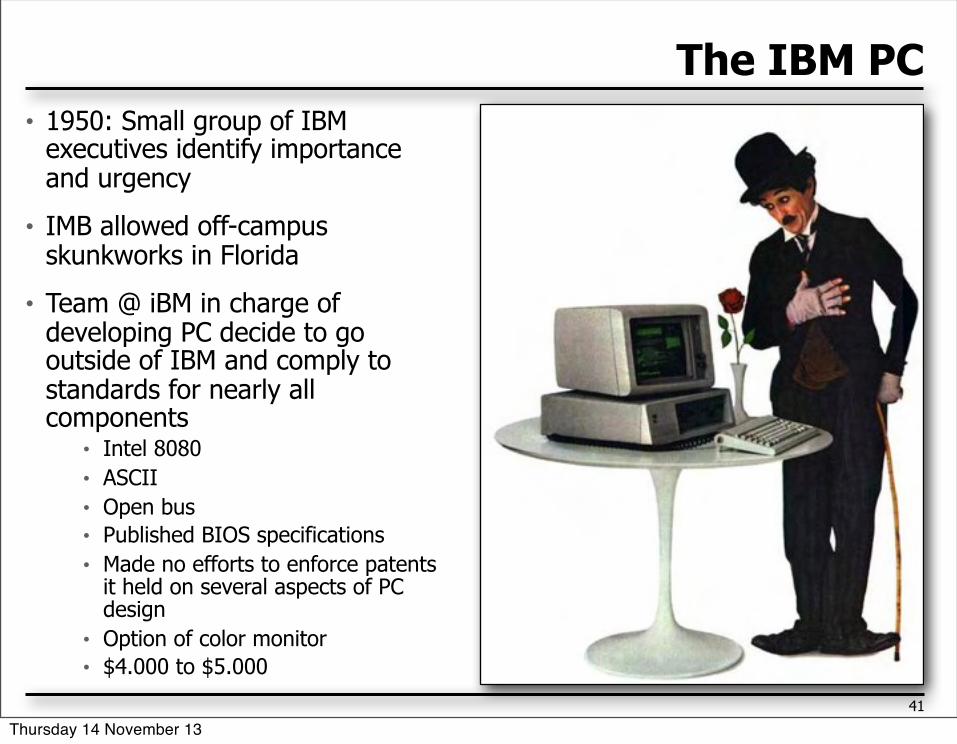

The IBM PC• 1950: Small group of IBM

executives identify importance and urgency

• IMB allowed off-campus skunkworks in Florida

• Team @ iBM in charge of developing PC decide to go outside of IBM and comply to standards for nearly all components

• Intel 8080• ASCII• Open bus• Published BIOS specifications• Made no efforts to enforce patents

it held on several aspects of PC design

• Option of color monitor• $4.000 to $5.000

41

Thursday 14 November 13

Still... 1984-1995

42

• Microsoft

• Intel

• Dell

• Novell

• Dow Jones/ Nasdaq

• Apple

• IBM

Thursday 14 November 13

Disruptive innovations• Disruptive innovation...

• Address different customers• Add different value• Use different value chain

• Radical innovations can be disruptive• Digitial photography• Microprocessor, PC

• Radical innovations can be sustaining...• All innovations that inceased performance and reliability and decreased cost

of HD• All innovations that increased performance and reliability and decreased cost

of computers

43

Thursday 14 November 13

2.2.3 The kind of innovation from the perspective of the current suppliers:

competence enhancing innovation vs. competence destroying innovation

44

Thursday 14 November 13

54

Innovation and core competencies

– Michael Tushman, Harvard Business School

there are two types of radical innovations from the perspective of an incubent firm– competence enhancing innovation

makes use of the firms’ existing knowledge, skills, abilities, structure, design, production processes, plants, equipment...

(makes use of the firms’ existing business model)– competence destroying innovation

when it undermines the usefulness of the firms’ existing knowledge, skills, abilities, structure, design, production processes, plants, equipment..

Thursday 14 November 13

55

competence enhancing/destroying innovation

Thursday 14 November 13

56

disruptive for who?

Thursday 14 November 13

48

Thursday 14 November 13

57

an opportunity for who?

Thursday 14 November 13

Eastman kodak agfa dow jones canon

58

Thursday 14 November 13

Why incumbents often miss the boat of radical and disruptive innovations

• Managers do not see the technology as a threat or opportunity• ‘What is this toy?’

• No incentive to introduce new technology• ‘We’re doing just fine’

• Can improve the performance of their technology• Disruptive technology often spurs technological development in leading technology

• They face organizational obstacles to change their core technology• New products will cannibalize existing sales• They have investments in existing technology• The department in charge of established technology claims resources

• New business incompatible with their business model• Channels

• You could not at the same time sell via channels (as IBM, Compaq) and via the internet (Dell): dealer channel (100% of current sales) would revolt

• Sales model• If you’re selling high-end / high margin solutions on mini-computers through costly direct sales

forces you can’t switch to selling low cost PC’s hardware and software

• Market leaders have hard time do redirect resources away from their current customers

51

Thursday 14 November 13

2.1 some perpectives on innovation

52

Thursday 14 November 13

Definitions of innovation

53

• Innovation is the useful application of new inventions or discoveries. (Wikipedia)

• "Innovation is the embodiment, combination, or synthesis of knowledge in original, relevant, valued new products, processes, or services. (Luecke and Katz)

• "Innovation is the multi-stage process whereby organizations transform ideas into new/improved products, service or processes, in order to advance, compete and differentiate themselves successfully in their marketplace."(Baregheh et al. 2009)

• The scholarly literature on innovation typically distinguish between invention, an idea made manifest, and innovation, ideas applied successfully in practice.

• My ‘definition’: ‘the new technology/product/service...’• Just how new can vary enormously

Thursday 14 November 13

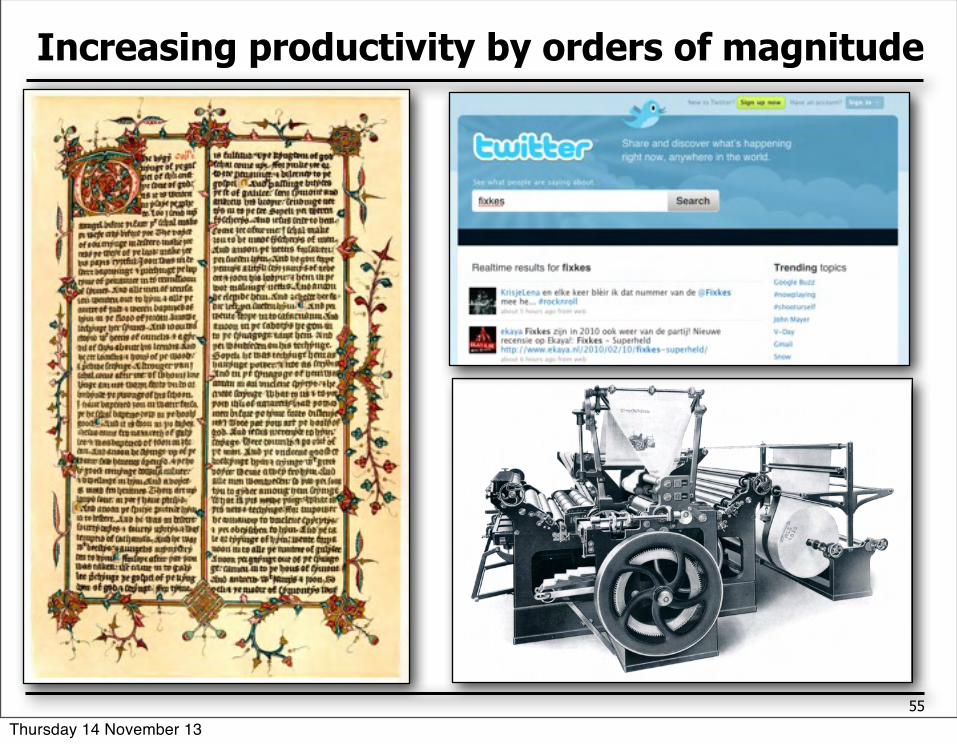

When the ‘new’ doesn’t make it there...• The most important

innovations increase productivity by orders of magnitude

• Steam, electricity, radio, IT…

• And thus reduce the need for manpower

• Primary -> secondary -> tertiary sector

• In a cumulative process

54

Thursday 14 November 13

Increasing productivity by orders of magnitude

55

Thursday 14 November 13

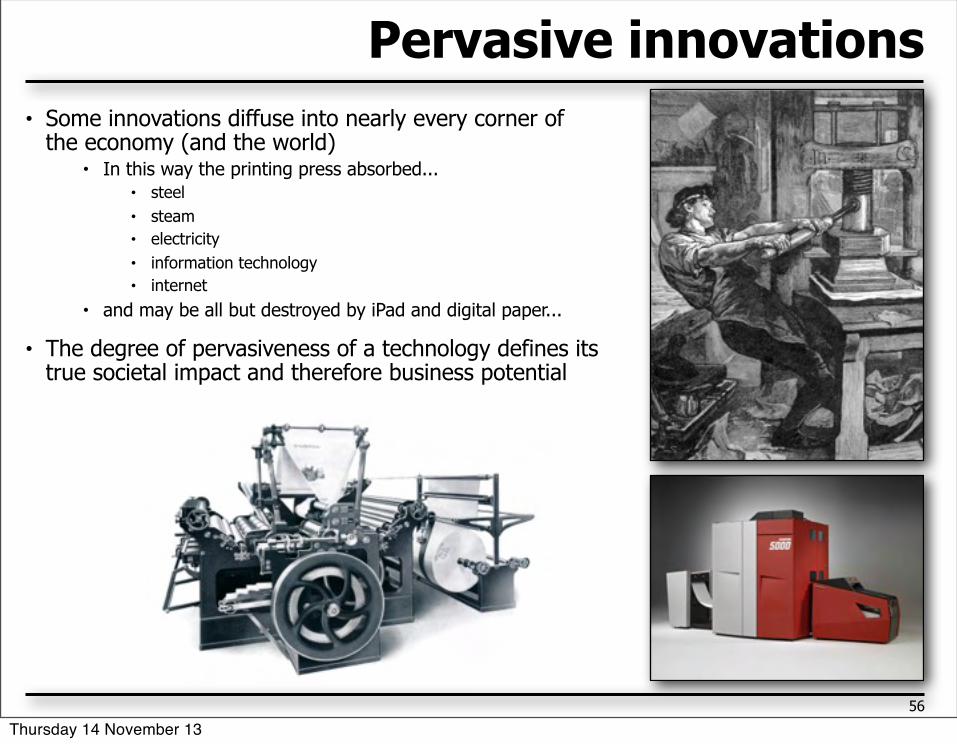

Pervasive innovations• Some innovations diffuse into nearly every corner of

the economy (and the world)• In this way the printing press absorbed...

• steel• steam• electricity• information technology• internet

• and may be all but destroyed by iPad and digital paper...

• The degree of pervasiveness of a technology defines its true societal impact and therefore business potential

56

Thursday 14 November 13

36

Technology trajectories...• Technologies follow a trajectory of gradual improvement, up to a

point where it really complies to user needs

• This can result in a massive wave of adoption: Palm, iPhone, GSM, railways, electricity...

• -> when is a technology ready for adoption?

Thursday 14 November 13

Context • A technology very often depends on complementary assets

• Complementary technologies• Complementary infrastructure

• Examples • Car and oil, roads• Integrated circuits and telecom, storage, displays• Digital camera’s and IT

58

Thursday 14 November 13

The importance of an innovation depends on it’s (and your) place in the value chain...

• The impact of LED vs OLED in LCD TVs

• LED: incremental from perpective of FPD manufacturer, radical for component suppliers

• OLED redefines the product flat panel display

59

Thursday 14 November 13

When technologies compete...

60

Thursday 14 November 13

Technologies compete...

61

Thursday 14 November 13

3. Industry life cycles

62

Thursday 14 November 13

67

the industry life cycle a framework to understand the dynamics of growth (and decline)

of:– industries

Analog and digital photography commercial sailing ships information technology GSM fitness centers

– companies enfocus, sportopolis agfa, polaroid

– regions wallonia silicon valley

Thursday 14 November 13

the industry life cycle

performance

Time/effort

Ferment

Takeoff

Maturity

Disruption

MIT Sloan School of Management Technology Strategy Course 2005 Rebecca Henderson

(adoption)

Thursday 14 November 13

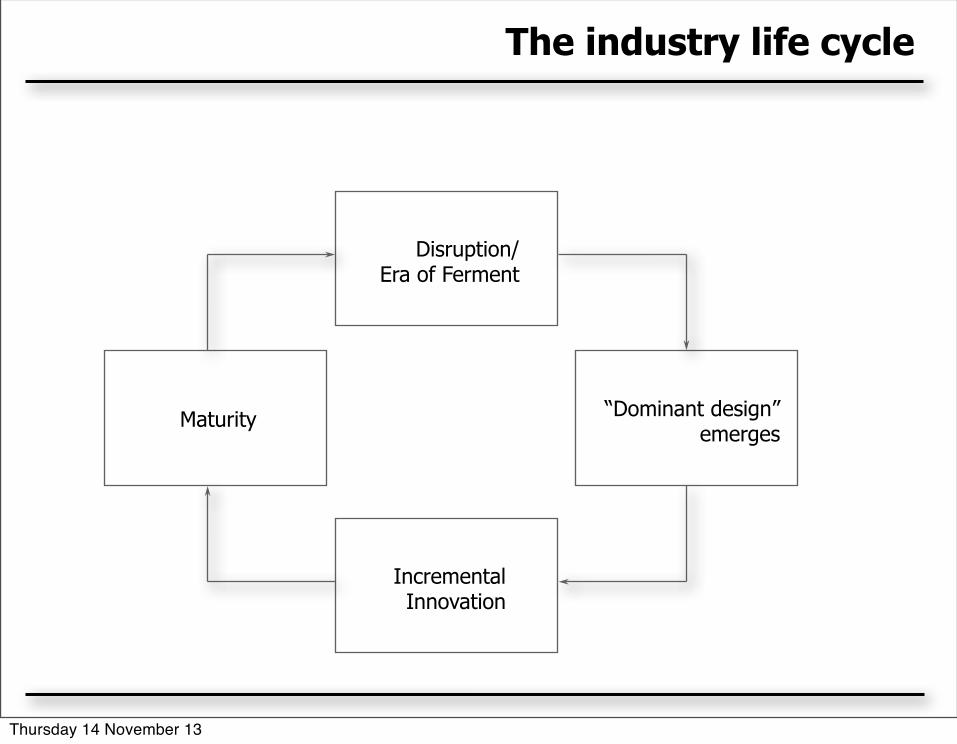

The industry life cycle

Disruption/Era of Ferment

“Dominant design” emerges

Maturity

IncrementalInnovation

Thursday 14 November 13

70

què sera, sera

Thursday 14 November 13

3.2 dimensions of industry life cycles

67

Thursday 14 November 13

68

key punctuations in the lifecycle

Tech

nica

lE

ffici

ency

R&D EffortFERMENT

TAKE-OFF

MATURITY

Selection

Retention

Variation

Time

Performance

Thursday 14 November 13

69

the nature of technical work changes

will it work? exploration, fun, creativity key

performance

Time

Ferment

Takeoff

Maturity

(adoption)

Can we make 100,000? And service them?

We need to be responsive & flexible but controlled

Thursday 14 November 13

70

the marketing challenge evolves

performance

Time

Ferment

Takeoff

Maturity

(adoption)

do we have reference customers?

who needs this?

do we have the channels to cope with early majority customers?

Thursday 14 November 13

71

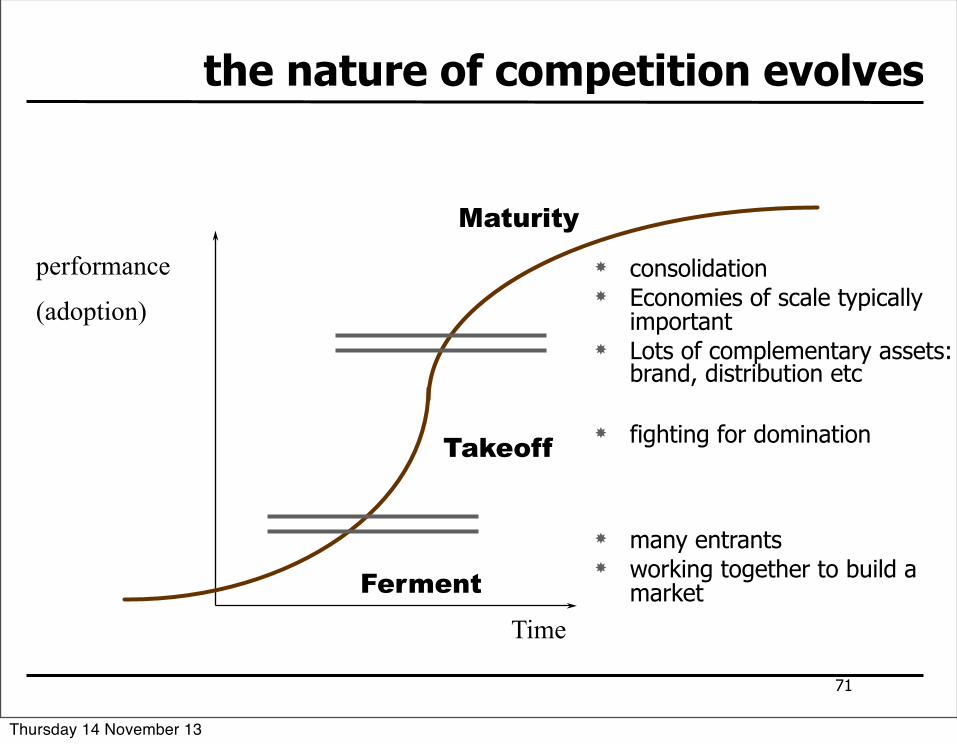

the nature of competition evolves

performance

Time

Ferment

Takeoff

Maturity

(adoption)

fighting for domination

many entrants working together to build a

market

consolidation Economies of scale typically

important Lots of complementary assets:

brand, distribution etc

Thursday 14 November 13

72

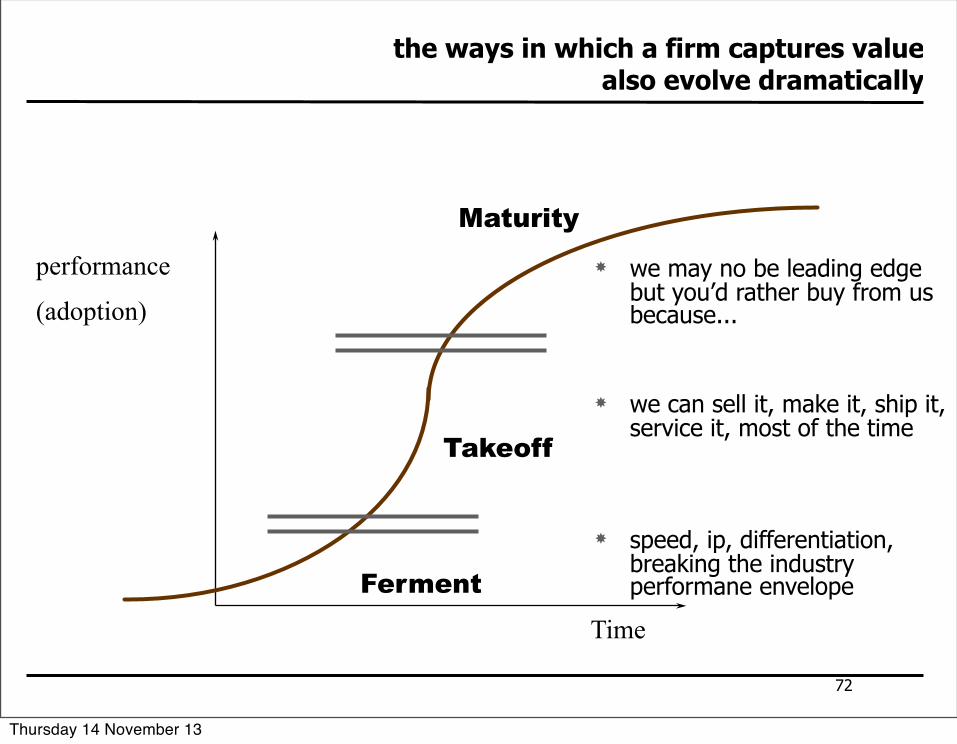

the ways in which a firm captures value also evolve dramatically

performance

Time

Ferment

Takeoff

Maturity

(adoption)

we can sell it, make it, ship it, service it, most of the time

speed, ip, differentiation, breaking the industry performane envelope

we may no be leading edge but you’d rather buy from us because...

Thursday 14 November 13

73

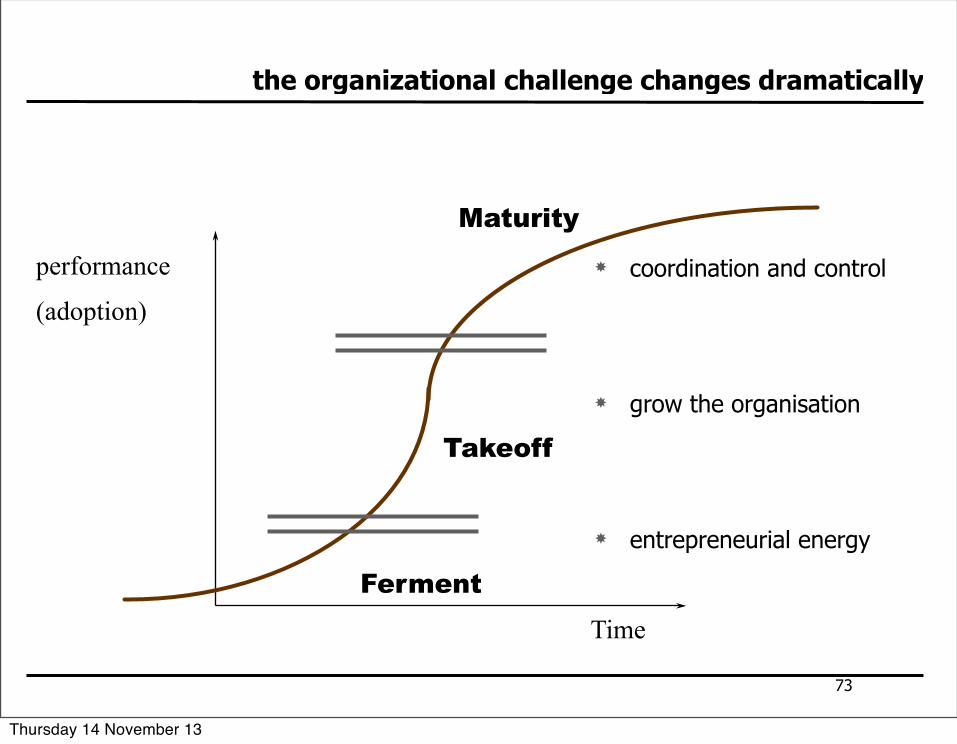

the organizational challenge changes dramatically

performance

Time

Ferment

Takeoff

Maturity

(adoption)

grow the organisation

entrepreneurial energy

coordination and control

Thursday 14 November 13

74

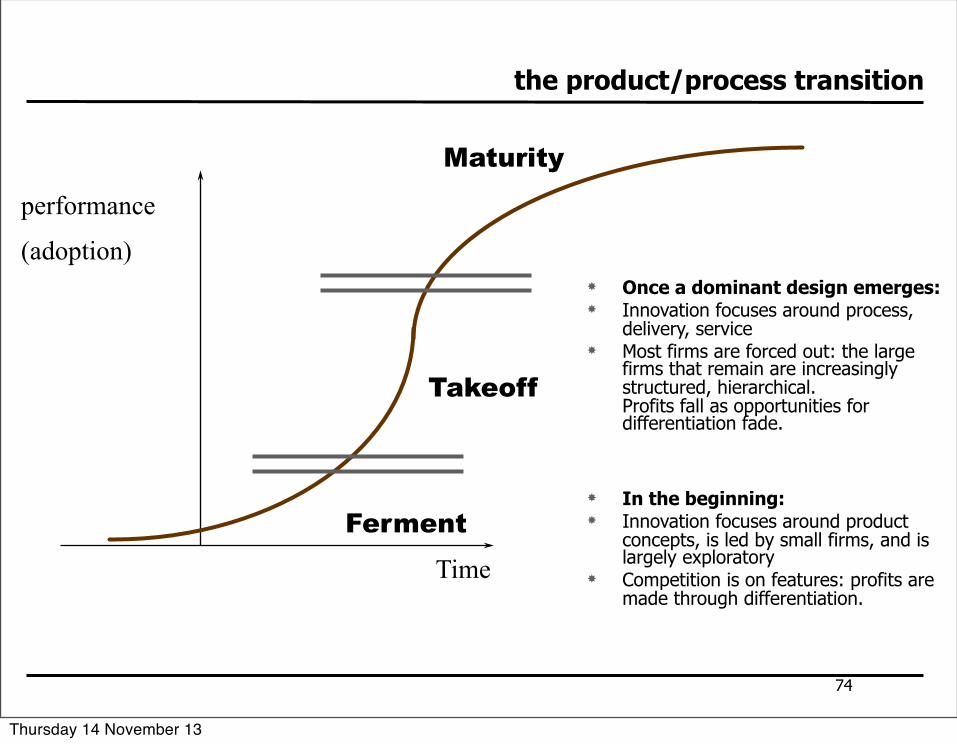

the product/process transition

performance

Time

Ferment

Takeoff

Maturity

(adoption)

In the beginning: Innovation focuses around product

concepts, is led by small firms, and is largely exploratory

Competition is on features: profits are made through differentiation.

Once a dominant design emerges: Innovation focuses around process,

delivery, service Most firms are forced out: the large

firms that remain are increasingly structured, hierarchical.Profits fall as opportunities for differentiation fade.

Thursday 14 November 13

entrepreneurial opportunities over the lifecycle

Ferment

Takeoff

Maturity

Opportunities

New technologies & new markets to be explored

Lower cost solution to the dominant design – compete on production, distribution, or enabling technology

Few opportunities, but “disruption” is possibleEntrants with complementary assets

-Explore new markets-Establish legitimacy-Build an industry association-Survive

-Ensure yours is the DD-Protect DD or share with others-Build customer base w/ appropriate $$$ in manu/distr.

-Find ways to disrupt current industry-Establish a successful niche-Dominate one component of current architecture

Actions

Thursday 14 November 13

76

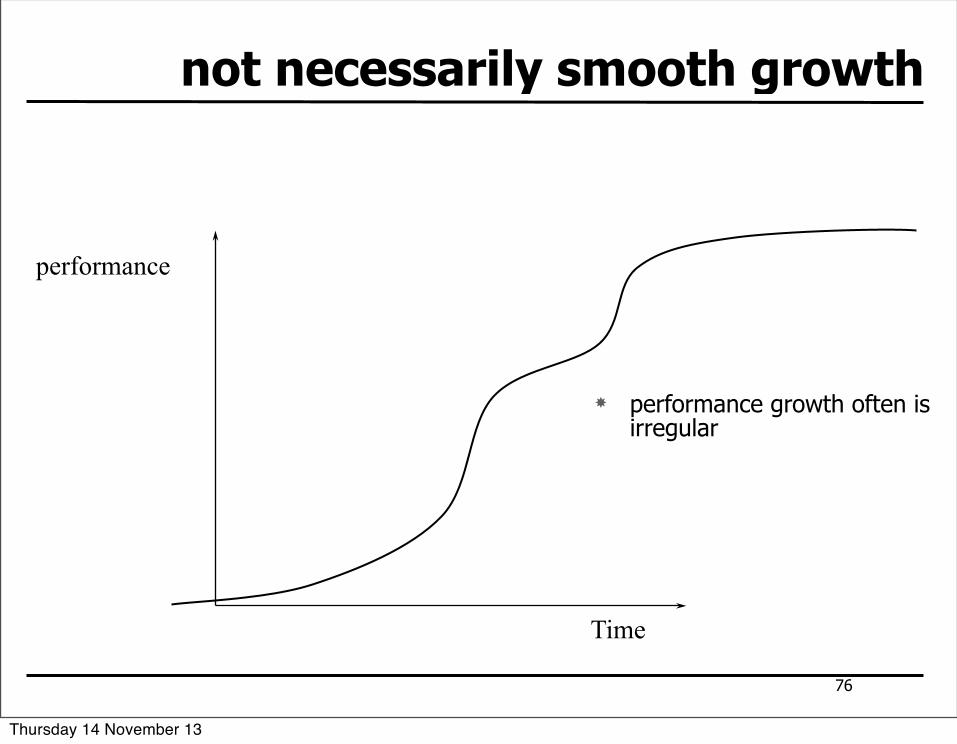

not necessarily smooth growth

performance

Time

performance growth often is irregular

Thursday 14 November 13

77

do all good things come to and end?technological exhaustion

performance

Time

(adoption) performance may be

ultimately constrained by physical limits:

– sailing ships and the power of wind

– copper wire and transmission capability

– semiconductors and the speed of the electron

Thursday 14 November 13

78

the rate at which new technologies diffuse can vary widely

Thursday 14 November 13

101

a summary by MIT

Thursday 14 November 13

Life cycles...

80

• Embedded in each other• Electricity • Electronics • Integrated circuits• Computers• Operating systems• Software• Plug-ins

•

Thursday 14 November 13

83

ILC dimensions technology s-curves

entrants and shake-outs

dominant design

customer typology

Thursday 14 November 13

Technology S-curve

82

Thursday 14 November 13

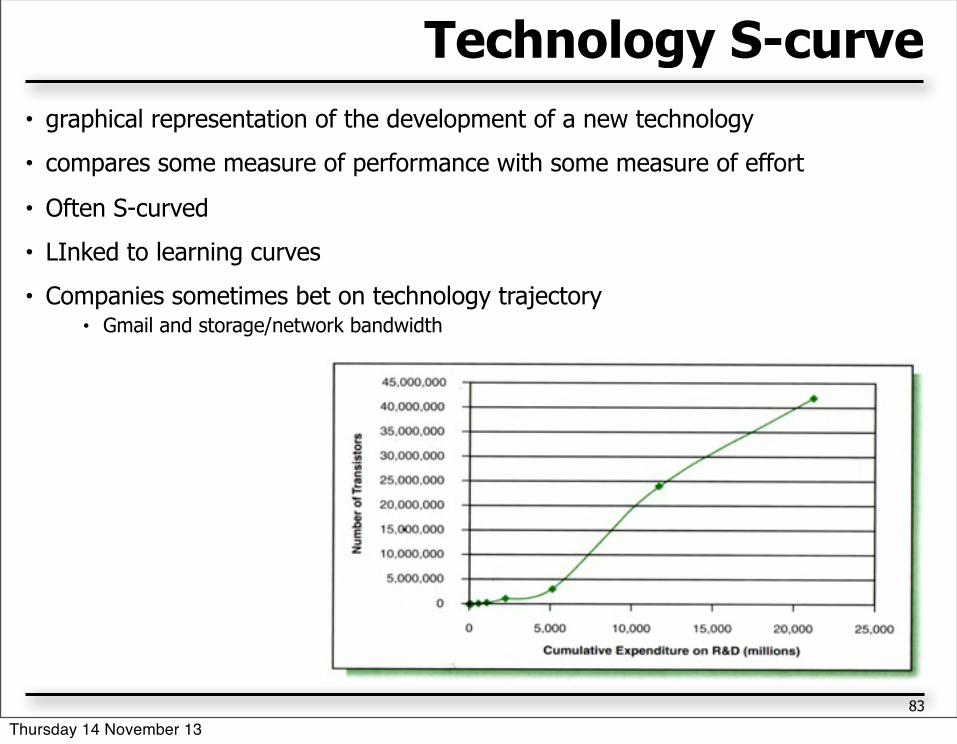

Technology S-curve• graphical representation of the development of a new technology

• compares some measure of performance with some measure of effort

• Often S-curved

• LInked to learning curves

• Companies sometimes bet on technology trajectory• Gmail and storage/network bandwidth

83

Thursday 14 November 13

86

vectors in time

Thursday 14 November 13

Entrants and shake-out

85

Thursday 14 November 13

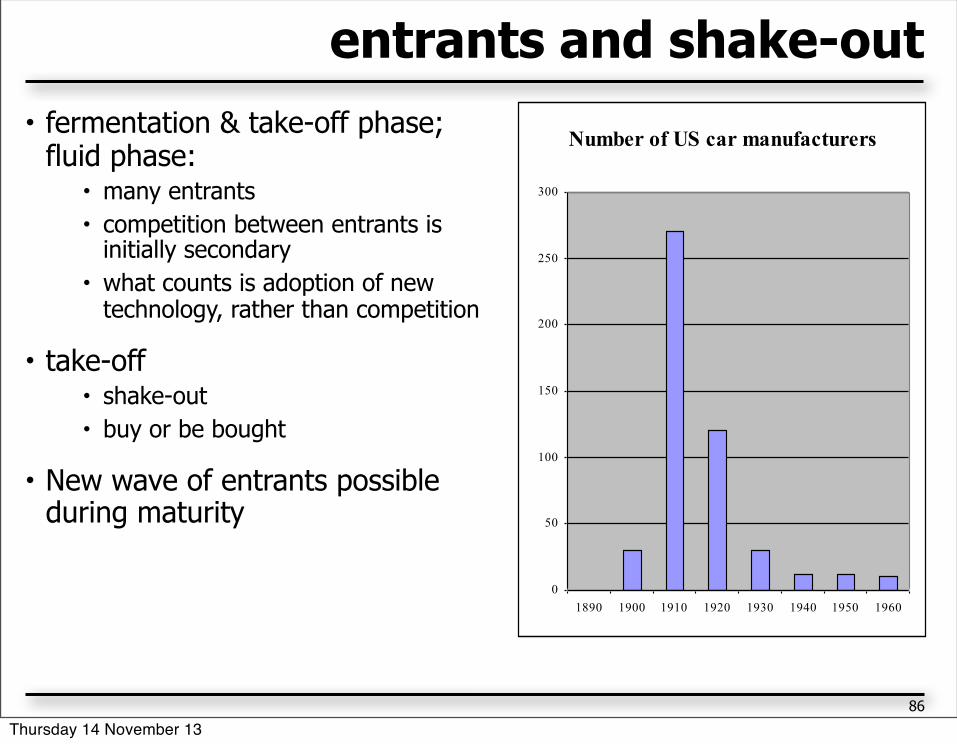

entrants and shake-out• fermentation & take-off phase;

fluid phase:• many entrants• competition between entrants is

initially secondary• what counts is adoption of new

technology, rather than competition

• take-off• shake-out• buy or be bought

• New wave of entrants possible during maturity

86

Thursday 14 November 13

Dominant Design

87

Thursday 14 November 13

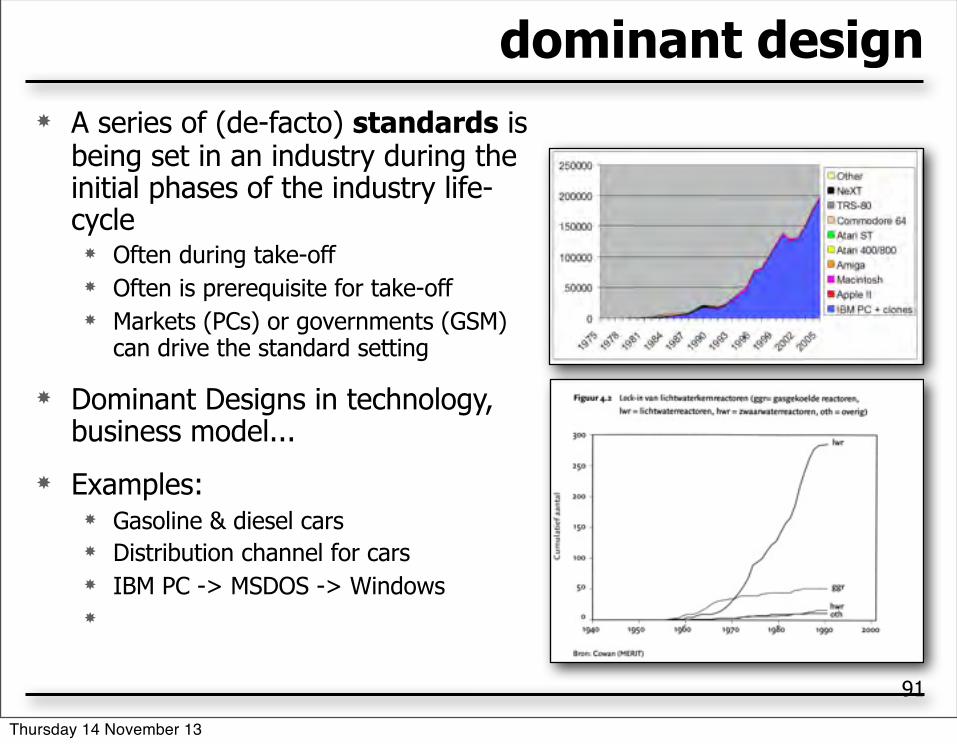

91

dominant design A series of (de-facto) standards is

being set in an industry during the initial phases of the industry life-cycle Often during take-off Often is prerequisite for take-off Markets (PCs) or governments (GSM)

can drive the standard setting

Dominant Designs in technology, business model...

Examples: Gasoline & diesel cars Distribution channel for cars IBM PC -> MSDOS -> Windows

Thursday 14 November 13

Customer typology

89

Thursday 14 November 13

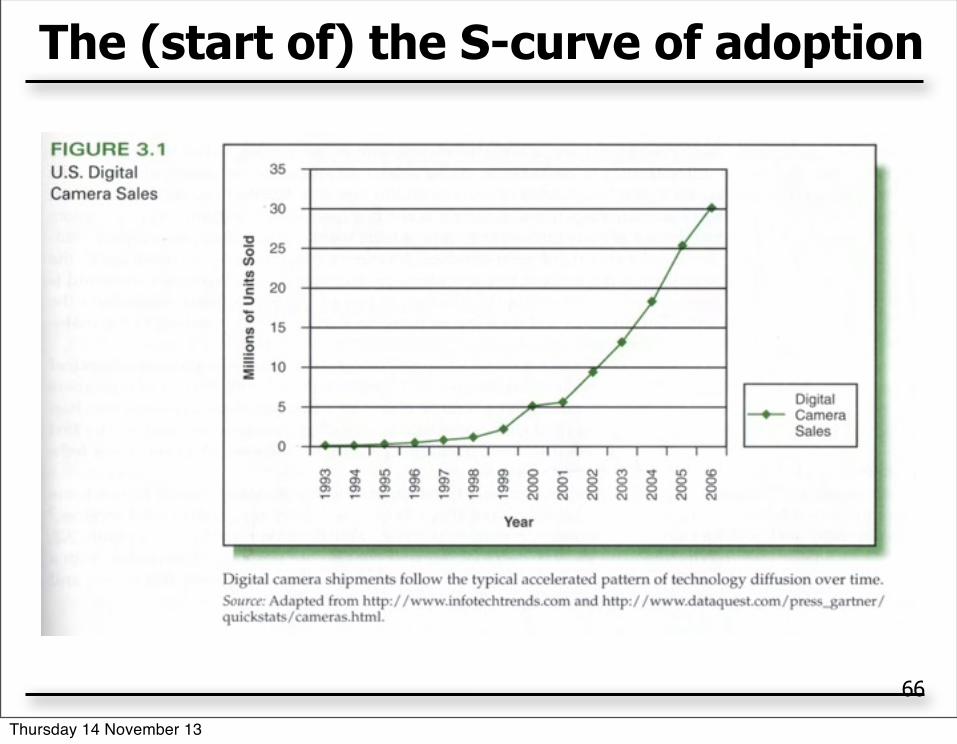

66

The (start of) the S-curve of adoption

Thursday 14 November 13

95

customer profiles

Thursday 14 November 13

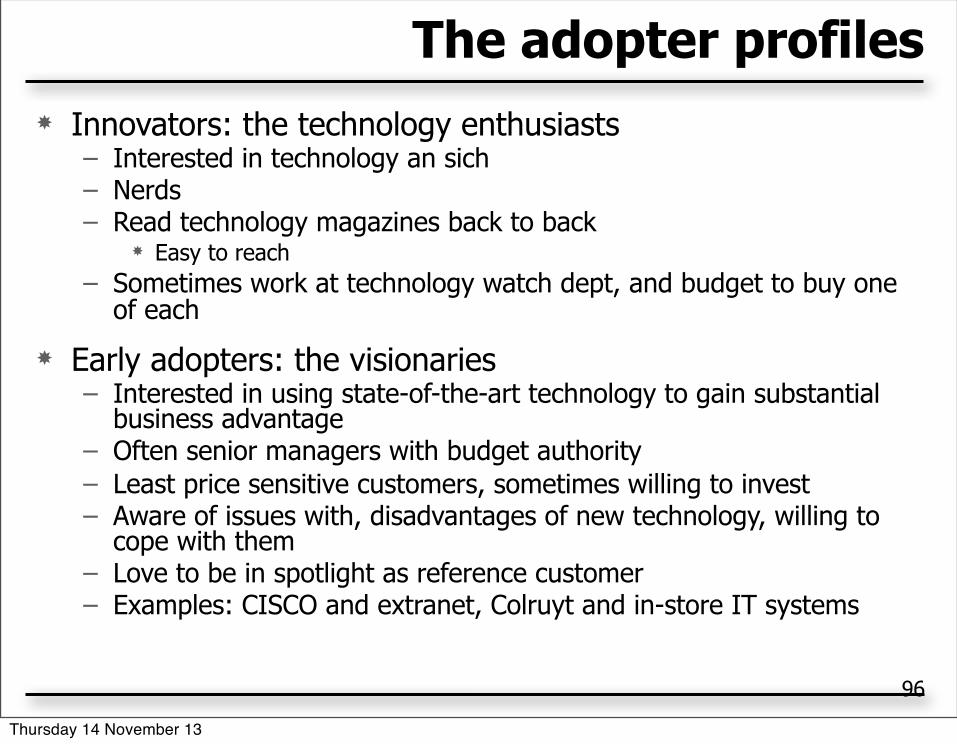

The adopter profiles Innovators: the technology enthusiasts

– Interested in technology an sich– Nerds– Read technology magazines back to back

Easy to reach– Sometimes work at technology watch dept, and budget to buy one

of each

Early adopters: the visionaries– Interested in using state-of-the-art technology to gain substantial

business advantage– Often senior managers with budget authority– Least price sensitive customers, sometimes willing to invest– Aware of issues with, disadvantages of new technology, willing to

cope with them– Love to be in spotlight as reference customer– Examples: CISCO and extranet, Colruyt and in-store IT systems

96

Thursday 14 November 13

the chasm – arises when the early market is saturated and the mainstream market is

not ready to adopt– there is no-one to sell to

Early majority: the pragmatist– Risk is a word with a negative connotation– Want incremental innovation– By proven product from market leader– Based on accepted standards– Through known channel– They don’t go to technology fairs, they go to industry fares– They want partners that are knowledgeable about their industry– When they have chosen they remain faithful

Late majority– Don’t like technology, are afraid of change and complain about the

weather

97

Thursday 14 November 13

Crossing the chasm Focus all efforts on a single niche, where your product solves the

greatest problem– Example document management: submission of files of pharmaceutical

companies– Size is not so important: market leadership is what counts

Build the whole product, set up an appropriate distribution channel, conquer this niche

Jump to the next niche– Bowling pins

– Not the sole option, not necessarily succesful– Mass adoption of non-specialised technology can supplant your technology

98

Thursday 14 November 13

Other comments on customer typology

my definition of ‘take-off’: – ’when not wanting to be the first is replaced by not wanting to be the last’

Mission critical customers

Sometimes the niche-per-niche strategy fails– Especially when large scale product enters market

PC and Wang, GSM and Mobitex

99

Thursday 14 November 13

100

mission-critical users for whom the technology is of major strategic importance

– colruyt and radio frequency – identification (rf-id)– vtb/touring wegenhulp and wireless data communications

willing to invest– high roi– strategic importance (de laagste prijs)– capabilities to absorb new technology

Thursday 14 November 13

ILCs applied to Optrima

97

Thursday 14 November 13

98

Thursday 14 November 13

99

Thursday 14 November 13

100

Thursday 14 November 13

Bubbles

101

Thursday 14 November 13

The first bubble?

Thursday 14 November 13

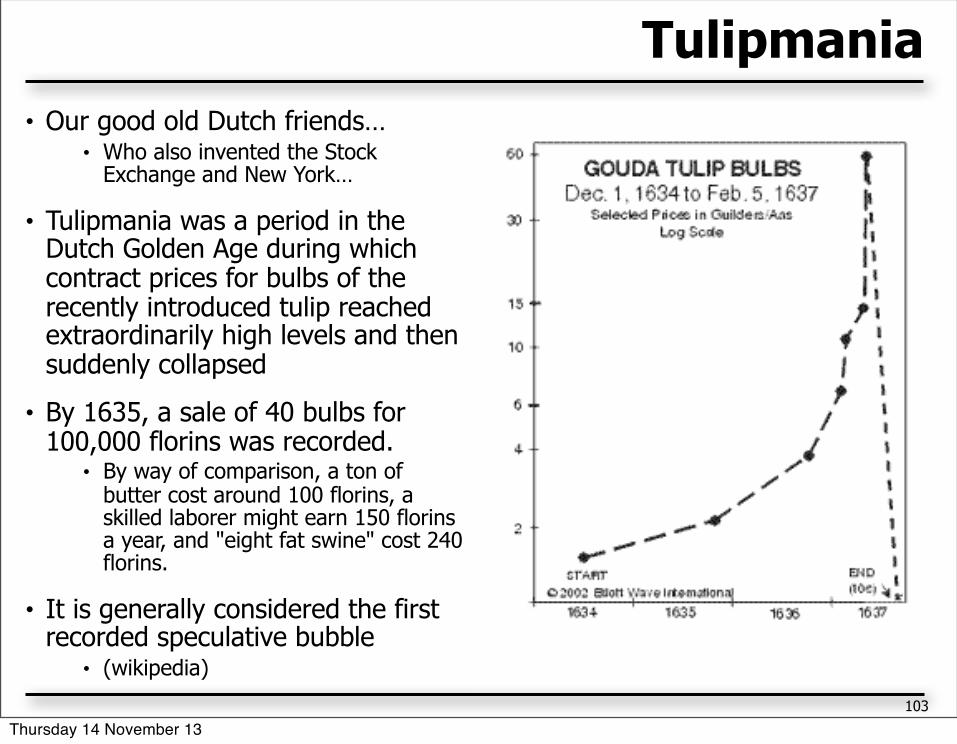

Tulipmania• Our good old Dutch friends…

• Who also invented the Stock Exchange and New York…

• Tulipmania was a period in the Dutch Golden Age during which contract prices for bulbs of the recently introduced tulip reached extraordinarily high levels and then suddenly collapsed

• By 1635, a sale of 40 bulbs for 100,000 florins was recorded.

• By way of comparison, a ton of butter cost around 100 florins, a skilled laborer might earn 150 florins a year, and "eight fat swine" cost 240 florins.

• It is generally considered the first recorded speculative bubble

• (wikipedia)

103

Thursday 14 November 13

The telecom bubble

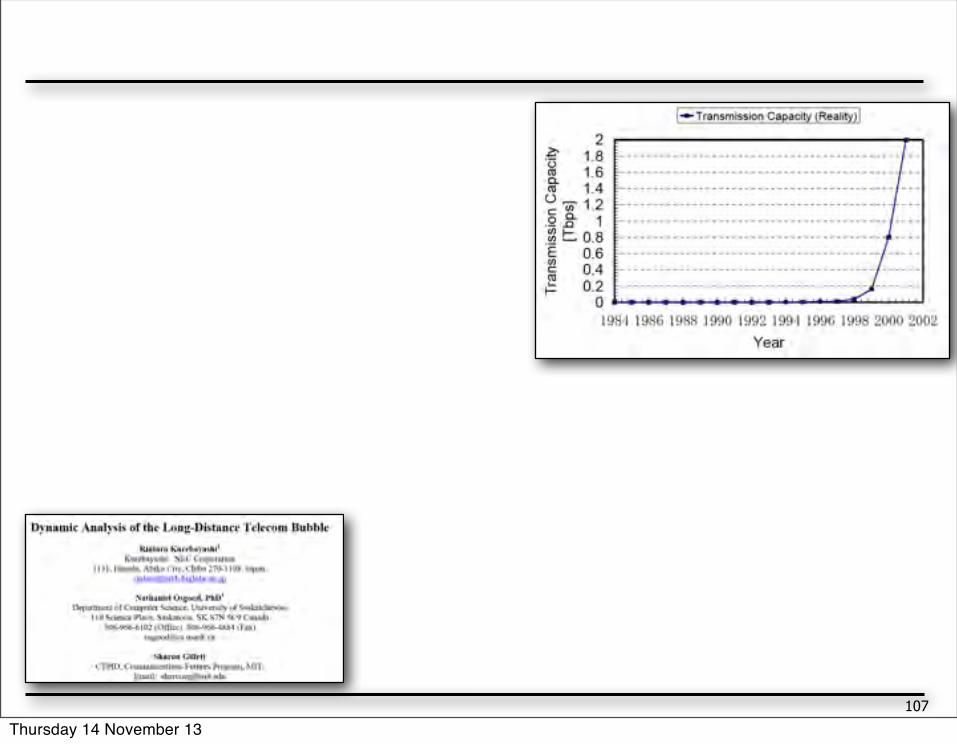

• 7/2001-7/2002: More than $1 trillion in value has evaporated from the telecommunications industry.

• A wave of liquidations, reorganizations and bankruptcy filings has engulfed both small upstarts and the “financially unassailable” titans.

• Telecom companies developed business models for expansion premised on one industry-adopted myth: Internet and broadband applications would fuel an unforeseeable demand for network capacity to support the increasing flow of data traffic.

• Telecom evangelists believed that data traffic would double every 100 days, and that it would continue to do so for the foreseeable future.

• Buzz surrounding “killer applications.” A demand for exponential data growth rested on the assumption that e-mail would be trailed by new killer broadband applications that would only accelerate Internet adoption and thus increase traffic on the network.

• Venture capitalists invested billions of dollars in new technologies and applications that never passed the Alpha phase of development.

•

104

Thursday 14 November 13

Telecom Operators in 2002• “Distressed carriers” are companies of all sizes and business models, from local

incumbents to international competitive carriers. Their balance sheets are laden with debts that were used to fuel rapid network and operational expansions.

• They must devise a plan to restructure their business successfully, making crucial decisions about which assets and operations to sustain and shut down. Next they must decide whether to seek the protection of a bankruptcy filing, which offers tremendous flexibility in restructuring operations, but typically by removing equity holders.

• Ironically, the carriers that appear to be in the most enviable position are the companies that were often ballyhooed as dinosaurs while the bubble was forming: they could or chose not to keep pace during the communications revolution. These carriers have cash flow positive balance sheets and profitable operations.

• They include operators worldwide, from PTTs and incumbent local network operators, to RBOCs and smaller regional or independent operators. Whether through prudent vision or a fortunate lack of vision, these operators now hold the prized tokens as the Global Asset Reallocation game begins.

• They have an unprecedented opportunity to acquire and integrate network infrastructure and technology developed by their industry peers, at a fraction of the original investment. These more cautious operators are mindful that overcapacity and overextension led to the demise of their competitors, yet they recognize that NOW is the time to strategically enhance their networks for future growth.

105

Thursday 14 November 13

Worldcom • Their company began providing service as a long

distance reseller in 1984. For 15 years it grew quickly through acquisitions and mergers.

• Bernard Ebbers was named CEO in 1985 and the company went public in Aug. 1989. The company was a favorite with investors and Wall Street analysts. To many, WorldCom personified the new breed of telecommunications companies, whose potential for growth seemed almost limitless.

• The stock ran up to a peak of $64.51 in June 1999.

• Its $40 billion merger with MCI in 1998 was the largest in history at the time. In October 1999, WorldCom attempted to purchase Sprint in a stock buyout for $129 billion in stock and debt. The deal was vetoed by the Department of Justice.

• At the same time, the success began to unravel with the accumulation of debt and expenses, the fall of the stock market, long distance rates and revenue. It would tale 2 years for extent of these problems to become public.

• WorldCom does have valuable assets. It has the world's largest internet backbone, thousands of profitable government contracts and 20 million customers.

• On July 21 2002 WorldCom Inc., the nation's second largest long-distance carrier, filed for Chapter 11 bankruptcy.

• Company auditors had found approximately $7 billion in overstated earnings.

• WorldCom improperly booked $3.8 billion as capital expenditures, boosting cash flow and profit. WorldCom did not account for expenses when it incurred them, but hid the expenses by pushing them into the future, giving the appearance of spending less and therefore making more money.

• WorldCom's 2002 has been a horror story with accounting scandals, SEC investigations, the resignation of CEO Bernard Ebbers, possible bankruptcy and a stock that is worth less than a payphone call.

• Unfortunately, WorldCom now is renowned for filing the largest bankruptcy claim in U.S. history.

• It is estimated that WorldCom alone owed incumbent local exchange carriers (ILECs) hundreds of millions of dollars for services provided at the time it filed bankruptcy.

106

Thursday 14 November 13

107

Thursday 14 November 13

Gartners hype cycle

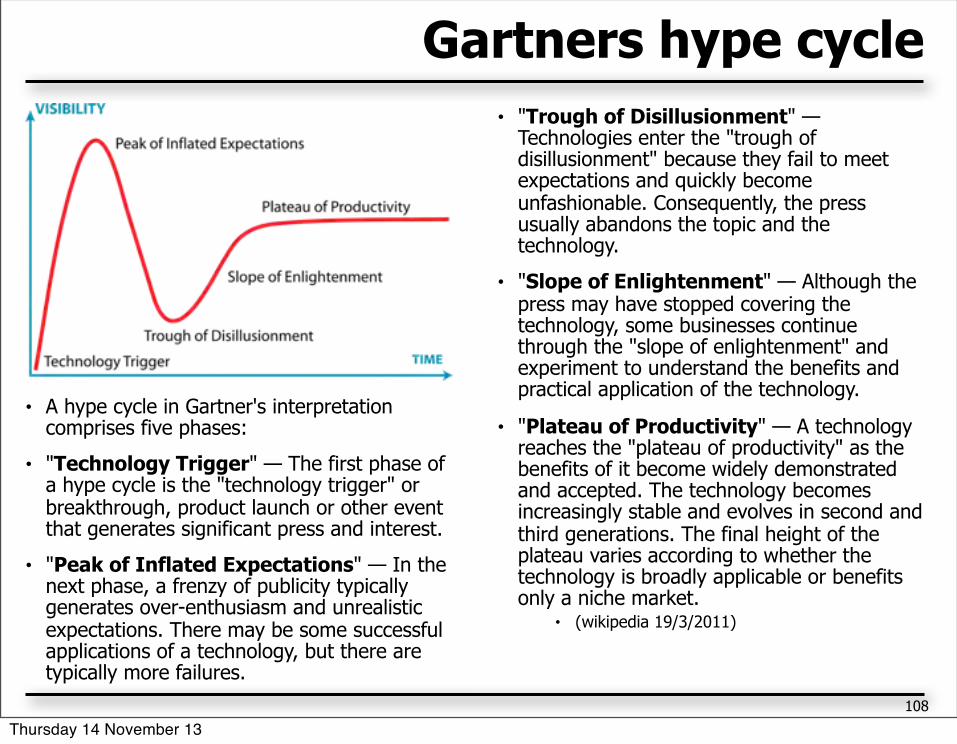

• A hype cycle in Gartner's interpretation comprises five phases:

• "Technology Trigger" — The first phase of a hype cycle is the "technology trigger" or breakthrough, product launch or other event that generates significant press and interest.

• "Peak of Inflated Expectations" — In the next phase, a frenzy of publicity typically generates over-enthusiasm and unrealistic expectations. There may be some successful applications of a technology, but there are typically more failures.

• "Trough of Disillusionment" — Technologies enter the "trough of disillusionment" because they fail to meet expectations and quickly become unfashionable. Consequently, the press usually abandons the topic and the technology.

• "Slope of Enlightenment" — Although the press may have stopped covering the technology, some businesses continue through the "slope of enlightenment" and experiment to understand the benefits and practical application of the technology.

• "Plateau of Productivity" — A technology reaches the "plateau of productivity" as the benefits of it become widely demonstrated and accepted. The technology becomes increasingly stable and evolves in second and third generations. The final height of the plateau varies according to whether the technology is broadly applicable or benefits only a niche market.

• (wikipedia 19/3/2011)

108

Thursday 14 November 13

109Thursday 14 November 13

110Thursday 14 November 13

Identifying a peak of inflated expectations

• ...and the subsequent fall...

• It is very hard to judge what is real and what is a bubble• Spectacular growth of an industry/market IS possible

• See Integrated Circuits, GSM...• Companies involved in this market CAN deliver on a high valuation

• Some considerations• Is the market potential real? Will it develop that rapidly?• Will the individual company really make money on the adoption wave?• Is press and public opinion going in overdrive?

111

Thursday 14 November 13

• Sadly, the telecom crusaders failed to take into account two impediments to hyper-growth:

• adoption of new technology is generally slow except with early adopters who were echoing their Gospel

• the development and implementation cycle to achieve stable technology solutions is generally long.

112

Thursday 14 November 13