Business for Development in Latin America Javier Santiso Deputy Director and Chief Economist OECD Development Centre Organisation for Economic Cooperation and Development Exporta 2007 Sevilla ICEX June 13-14 2007

Transcript

Business for Developmentin Latin America

Javier Santiso

Deputy Director and Chief Economist

OECD Development Centre

Organisation for Economic Cooperation and Development

Exporta 2007 Sevilla ICEX June 13-14 2007

2

11 Spain and Latin America: A Helping HandSpain and Latin America: A Helping Hand

Emerging Multinationals: New Developers?Emerging Multinationals: New Developers?22

Source: OECD Development Centre, 2007; based on Annual Reports.

Percentage of sales to Latin America

0%10%20%30%40%50%60%

RepsolYPF

GasNatural

Iberdrola Endesa Santander Telefónica BBVA

20042005

30%

5

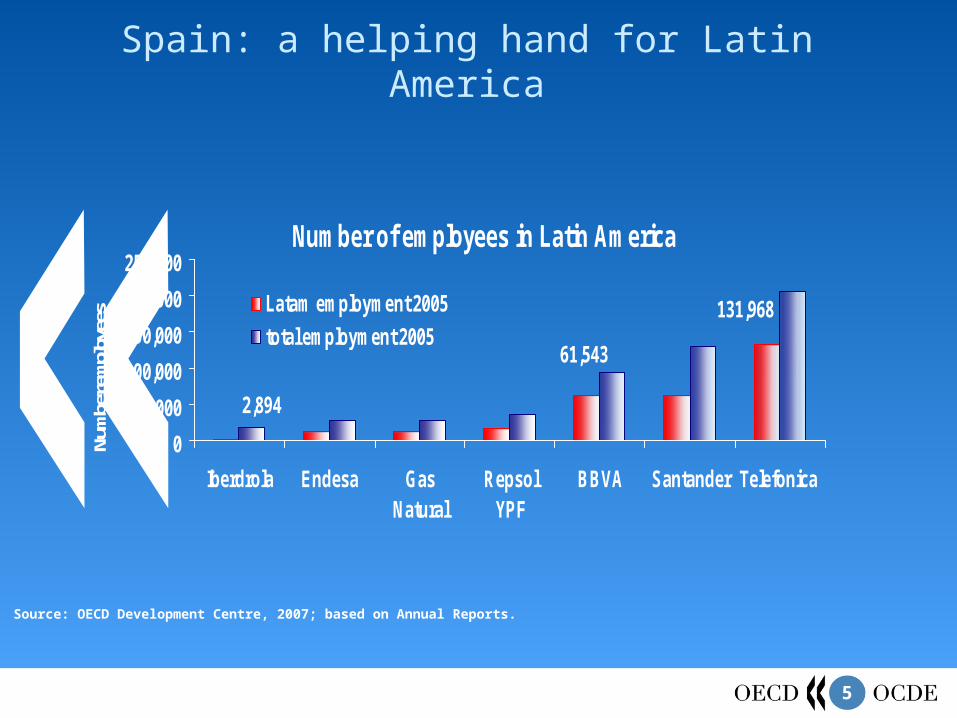

Spain: a helping hand for Latin America

Number of employees in Latin America

131,968

61,543

2,894

0

50,000

100,000

150,000

200,000

250,000

Iberdrola Endesa GasNatural

RepsolYPF

BBVA Santander Telefonica

Num

ber e

mpl

oyee

s Latam employment 2005

total employment 2005

Source: OECD Development Centre, 2007; based on Annual Reports.

6

Spanish multinationals: a helping hand for Latin America

Fiscal contribution of Telefónica per country in 2005

0

500

1000

1500

2000

2500

3000

3500

México Colombia Chile Venezuela Perú Argentina España Brasil

Euro

s Milli

ons

Source: OECD Development Centre, 2007; based on Telefónica Annual Report.

To

tal fis

ca

l co

ntrib

utio

n E

uro

72

66

Fiscal contribution of Telefonica as % of GDP in 2005

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

México Colombia Chile Venezuela Perú Argentina España Brasil

7

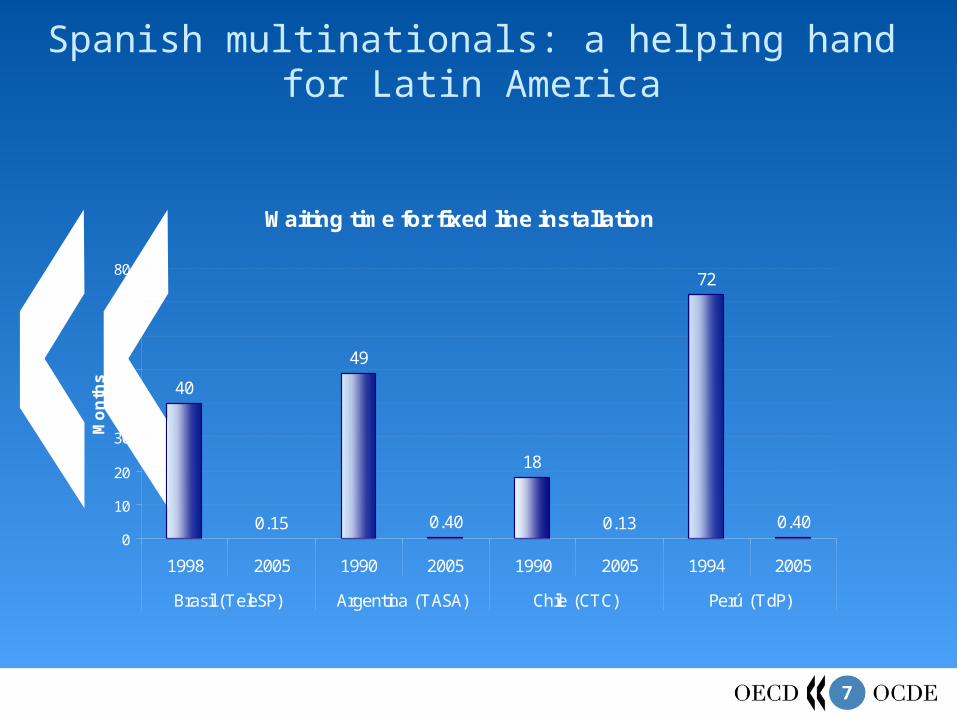

Spanish multinationals: a helping hand for Latin America

Waiting time for fixed line installation

40

0.15

49

0.40

18

0.13

72

0.400

10

20

30

40

50

60

70

80

1998 2005 1990 2005 1990 2005 1994 2005

Brasil (TeleSP) Argentina (TASA) Chile (CTC) Perú (TdP)

Mo

nth

s

8

Spanish FDI flows to Latin America

0

5000

10000

15000

20000

25000

30000

35000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Th

ou

san

ds

Eu

ros

Total FDI stock to Latin America Vs. cumulative Spanish flows

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Mil

lio

ns

US

Do

llar

s

Source: UNCTAD, World Investment Report 2006

Spain has become one of the leading direct foreign investors in Latin America

Source: Ministerio de Industria Turismo y Comercio de España, 2006

9

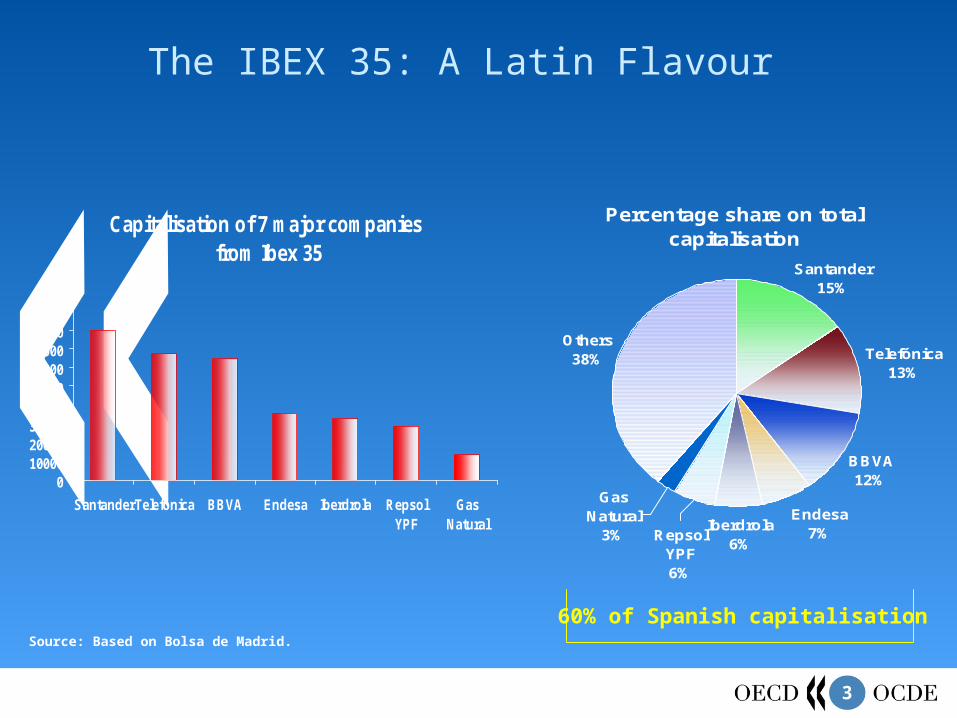

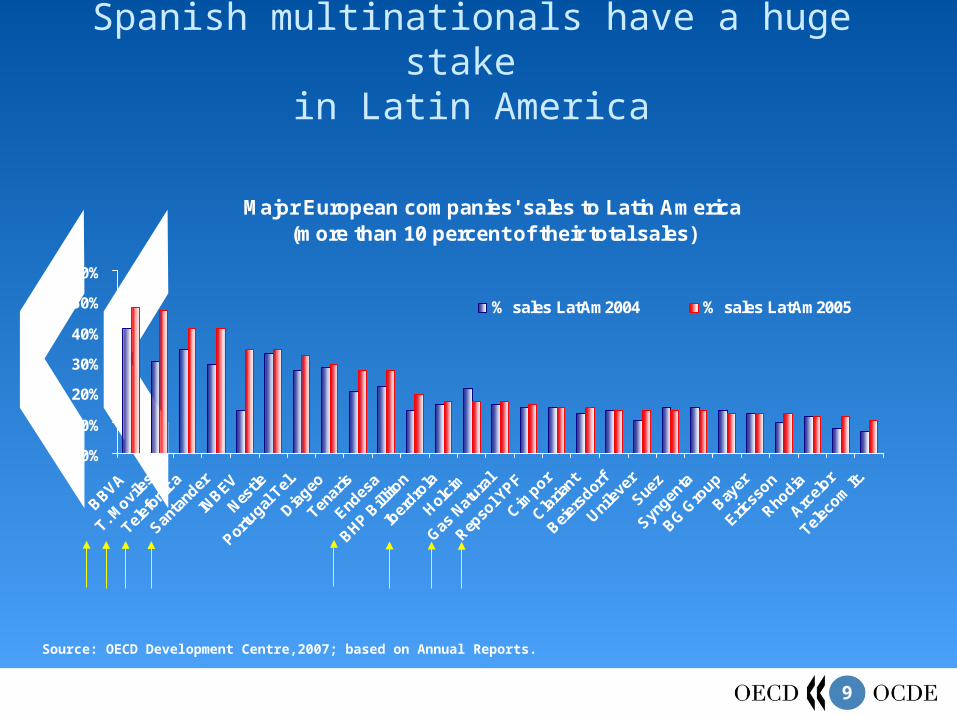

Spanish multinationals have a huge stake in Latin America

Major European companies' sales to Latin America(more than 10 percent of their total sales)

0%

10%

20%

30%

40%

50%

60%

BBVA

T. Movi

les

Telef

onica

Santa

nder

INBEV

Nestle

Portu

gal T

el.

Diageo

Tenar

is

Endes

a

BHP Bill

iton

Iber

drola

Holci

m

Gas N

atura

l

Repso

l YPF

Cimpor

Claria

nt

Beier

sdor

f

Unile

ver

Suez

Syngen

ta

BG Gro

up

Bayer

Ericss

on

Rhodia

Arcel

or

Telec

om It

.

% sales LatAm2004 % sales LatAm2005

Source: OECD Development Centre,2007; based on Annual Reports.

10

…leaving other European firms far behind

European companies' sales to Latin America (5-10 percent of total)

0%

2%

4%

6%

8%

10%

12%

% sales LatAm2004 % sales LatAm2005

Source: OECD Development Centre, 2007; based on Annual Reports.

11

…leaving other European firms far behind

0%

1%

2%

3%

4%

5%

6%

Volvo PernodRicard

Linde Sabmiller Havas Invensys SaintGobain

DeutscheLufthansa

EADS Heineken CRH

% sales LatAm2004 % sales LatAm2005

Source: OECD Development Centre, 2007; based on Annual Reports.

12

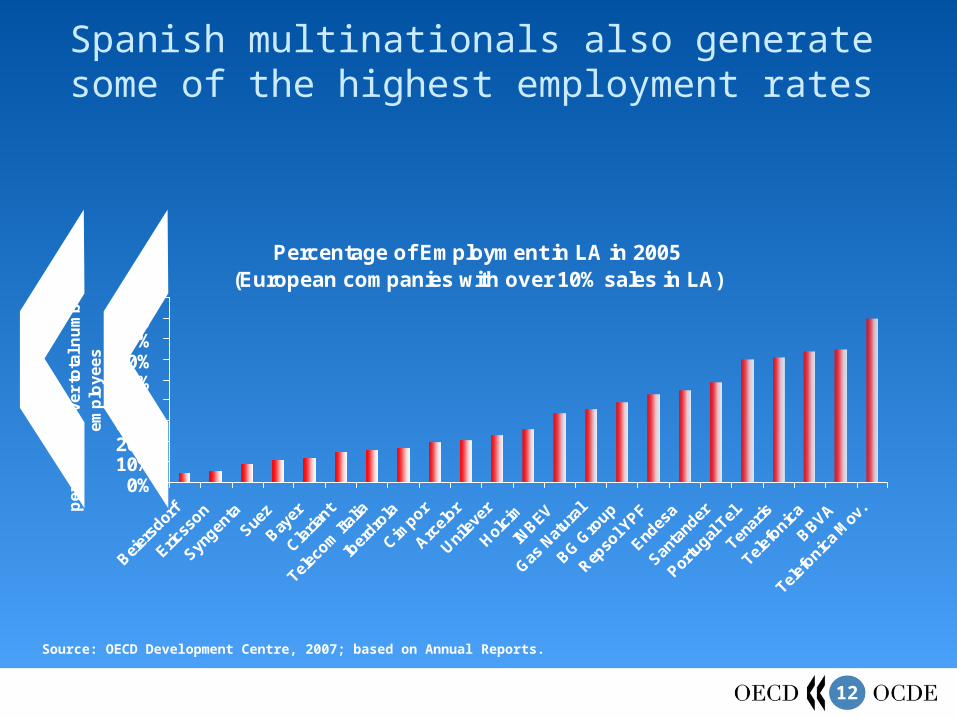

Spanish multinationals also generate some of the highest employment rates

Percentage of Employment in LA in 2005(European companies with over 10% sales in LA)

0%10%20%30%40%50%60%70%80%90%

Beier

sdor

f

Ericss

on

Syngen

taSue

z

Bayer

Claria

nt

Telec

om It

alia

Iber

drola

Cimpor

Arcel

or

Unile

ver

Holci

m

INBEV

Gas N

atura

l

BG Gro

up

Repso

l YPF

Endes

a

Santa

nder

Portu

gal T

el.

Tenar

is

Telef

onica

BBVA

Telef

onica

Mov

.pe

rce

nta

ge

ov

er

tota

l nu

mb

er

of

em

plo

ye

es

Source: OECD Development Centre, 2007; based on Annual Reports.

13

11 Spain and Latin America: A Helping HandSpain and Latin America: A Helping Hand

Emerging Multinationals: New Developers?Emerging Multinationals: New Developers?22

33 ConclusionsConclusions

14

Increasing capital flows south-south connection:

Source: UN Comtrade datababase, World Bank staff estimates, Global Development Finance, 2006.

Source: Global Development Finance, 2006.

SOUTH - SOUTH CAPITAL FLOWS BY TYPE, 2005

0

10

20

30

40

50

60

70

80

90

100

Export revenues Remittances Syndicated Loans FDI

% o

f Tot

al fl

ows

to L

DC .

South-South

North-South

SOUTH - SOUTH FDI AS A SHARE OF GLOBAL FDI 1999-2003

0

20

40

60

80

100

120

140

160

180

1995 1999 2000 2001 2002 2003

US B

illions

.

Total inflows

South-south FDI

15

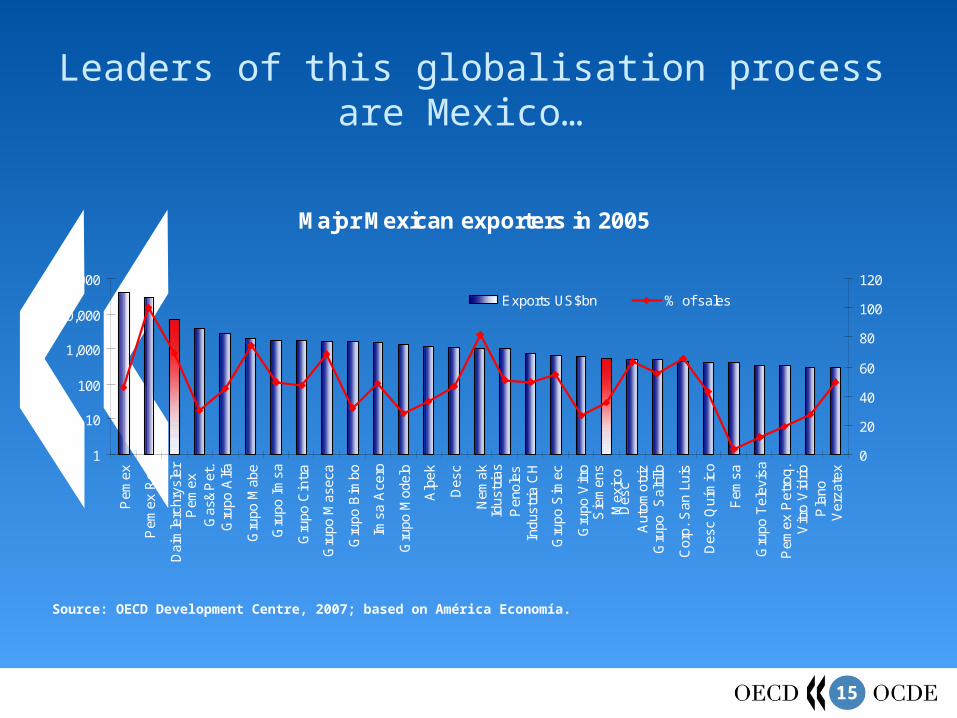

Leaders of this globalisation process are Mexico…

Source: OECD Development Centre, 2007; based on América Economía.

Major Mexican exporters in 2005

1

10

100

1,000

10,000

100,000

Pem

ex

Pem

ex R

ef.

Dai

mle

rchr

ysle

rP

emex

Gas

&P

et.

Gru

po A

lfa

Gru

po M

abe

Gru

po I

msa

Gru

po C

intr

a

Gru

po M

asec

a

Gru

po B

imbo

Imsa

Ace

ro

Gru

po M

odel

o

Alp

ek

Des

c

Nem

akId

ustr

ias

Pen

oles

Indu

stria

CH

Gru

po S

imec

Gru

po V

itro

Sie

men

sM

exic

oD

esc

Aut

omot

rizG

rupo

S

altil

lo

Cor

p. S

an L

uis

Des

c Q

uím

ico

Fem

sa

Gru

po T

elev

isa

Pem

ex P

etro

q.V

itro

Vid

rioP

lano

Ver

zate

x

0

20

40

60

80

100

120

Exports US$bn % of sales

16

…and Brazil

Top Brazilian exporters in 2005

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Pet

robr

asV

ale

de R

ioO

derb

rech

tE

mbr

aer

Car

gill

Bun

geV

olks

wag

enG

rupo

Gen

eral

Mot

ors

Sad

iaG

erda

uD

aim

lerc

hrys

ler

CS

TA

DM

MB

RS

amar

coC

ater

pilla

rP

edirg

aoB

rask

emA

racr

uzC

SN

Alb

rás

Vol

voR

ober

t B

osch

Cop

ersu

car

Fia

t A

uto.

Sea

ra A

lim.

Pet

robr

asS

hell

Sie

men

s B

rasi

lS

uzan

oA

cesi

taA

luno

rte

Car

aiba

Met

ais

CB

AP

irelli

Pne

usC

oam

oR

enau

ltE

mbr

aco

Cop

esul

WE

GS

ouza

Cru

z

0

10

20

30

40

50

60

70

80

90

100Exports % of sales

Source: OECD Development Centre, 2007; based on América Economía.

17

Increasing appetite for overseas expansion can also be seen in other countries such as

India…

Source: OECD Development Centre. Based on Dealogic and local press.

RECENT INDIAN INVESTMENTS 2006(EXCLUDING CORUS-TATA DEAL)

9%

22%

43%

26%

USEurope

Latin AmericaAfrica

RECENT INDIAN INVESTMENTS

4%

61%

22%

13%

US

Europe

Latin America

Africa

Target Nationality Acquirer Deal Value ($m)

Corus UK/NL Tata Group 7700Oil & Gas Assets (Campos Basin) Brazil Oil & Natural Gas Corp 1670Omnimex de Colombia Colombia Oil & Natural Gas Corp: China Group 850Oil & Gas Assets (Brazil) Brazil ONGC Videsh 820Greater Nile Petroleum (25%) Sudan Oil & Natural Gas Corp 783Glaceau (30%) US Tata tea 677

Shell Development Angola Angola Oil & Natural Gas Corp 600Oil & Gas Assets (Syria) Syria Oil & Natural Gas Corp: China Group 581

Betapharm Arzneimittel Germany Dr Reddy's Lab 572Hansen Transmissions Belgium Suzlon Energy 562Eve Holding Belgium Suzlon Energy 548Terapia Rumania Ranbaxy 324Total 15687

18

11 Spain and Latin America: A Helping HandSpain and Latin America: A Helping Hand

Emerging Multinationals: New Developers?Emerging Multinationals: New Developers?22

33 ConclusionsConclusions

19

Globalisation strategies have turned into success stories in Spain, Latin America and other emerging markets.

Spanish expansion abroad is moving towards new markets, beyond Latin America: OECD countries and Asia.

The region remains however a strategic bet for both old and newcomers. Above all the internationalization of Spanish economy could capitalize on this 10 years of increasing linkages:

Spain as a business hub for European corporations operating in Latin America.

Spain as a business hub for Latin American corporations operating in Europe.

Conclusions: Spain as a Latin American Business Hub?