22

Business Cycles in the Open Economy Mundell‐Fleming with Fixed Exchange Rates 1 Andrew Rose, Global Macroeconomics 10

| Date post: | 08-Mar-2018 |

| Category: |

Documents |

| Upload: | phamnguyet |

| View: | 218 times |

| Download: | 0 times |

Business Cycles in the Open Economy

Mundell‐Fleming with Fixed Exchange Rates

1Andrew Rose, Global Macroeconomics 10

Three Important AssumptionsThree Important Assumptions

• Prices are StickyPrices are Sticky– Business Cycle Model, Short Run

• Capital is InternationallyMobile No• Capital is Internationally Mobile – No Substantial Barriers to Private Capital Flows

Ri h i i k (b l– Rich countries, some emerging markets (but only recently)

N i l E h R fi d b C l B k• Nominal Exchange Rates fixed by Central Bank– Some economies, though more have fixed in past

2Andrew Rose, Global Macroeconomics 10

Add Net Exports to Real Economy (IS)Add Net Exports to Real Economy (IS)

• Recall that net exports (NX≡X M; current account)• Recall that net exports (NX≡X‐M; current account)

determined by:

1. Domestic output Y, raises imports (M)

2 Foreign output Y* (assumed to be exogenous since2. Foreign output Y* (assumed to be exogenous, since

foreign), raises exports (X)

3. Real exchange rate (eP/P*), “competitiveness”

affects both X and M

3Andrew Rose, Global Macroeconomics 10

Add Net Exports to Real Economy (IS)Add Net Exports to Real Economy (IS)

• Thus IS now: Y = A(G,i,Y) + NX(,Y,Y*)Thus IS now: Y A(G,i,Y) + NX(,Y,Y )– A is domestic absorption

4Andrew Rose, Global Macroeconomics 10

Financial Equilibrium (LM):h d h ?What is a Fixed Exchange Rate?

N i l h t fi d l h• Nominal exchange rate fixed, so real exchange

rate (=eP/P*) fixed in short run( / )

• Fixed Exchange Rate Regime authorities

take either side of FX transaction in unlimited

quantity

5Andrew Rose, Global Macroeconomics 10

Fixed Exchange Rate RegimeFixed Exchange Rate Regime

Th “A th iti ” G t h t fi• The “Authorities”: Government chooses to fix

exchange rate (or not); Central Bank enacts policy

– Fix: Authorities promise to use international reserves

k h d fto take either side of any FX transaction in any size at

fixed exchange rate (or within bands)

– Hence fix may affect IR, HPM, thus money supply

6Andrew Rose, Global Macroeconomics 10

Financial EquilibriumFinancial Equilibrium• LM looks same but not under complete control of Central Bank

– Recall M=μ*HPM; HPM=(IR+CBC); IR used to fix exchange rate

7Andrew Rose, Global Macroeconomics 10

Balance of Payments (BoP)Balance of Payments (BoP)

R ll / k/ ORS 0• Recall: c/acc + k/acc + ORS = 0

– Current Account given by net exports (NX)Current Account given by net exports (NX)

– Capital Account – private capital flows

– ORS – authorities must keep exchange rate fixed

• “Credible Fi ” is e pected to remain fi ed• “Credible Fix” is expected to remain fixed

• Can loosen assumption, allow “imperfect credibility”

8Andrew Rose, Global Macroeconomics 10

Capital Mobility 1Capital Mobility 1

• Assume capital can flow freely without (serious) ssu e cap ta ca o ee y t out (se ous)restrictions between the small open (home) economy and large (“center” or “anchor”)

hb ( / )neighbor(US/EMU)• Assume domestic & foreign bonds “perfect

b tit t ” id ti l i li idit t it tsubstitutes,” identical in liquidity, maturity, taxes, risk…– Can also easily add country risk premiumCan also easily add country risk premium

• Also assume nominal exchange rate is fixed and expected to stay fixed (“credible fix”)p y f ( )

9Andrew Rose, Global Macroeconomics 10

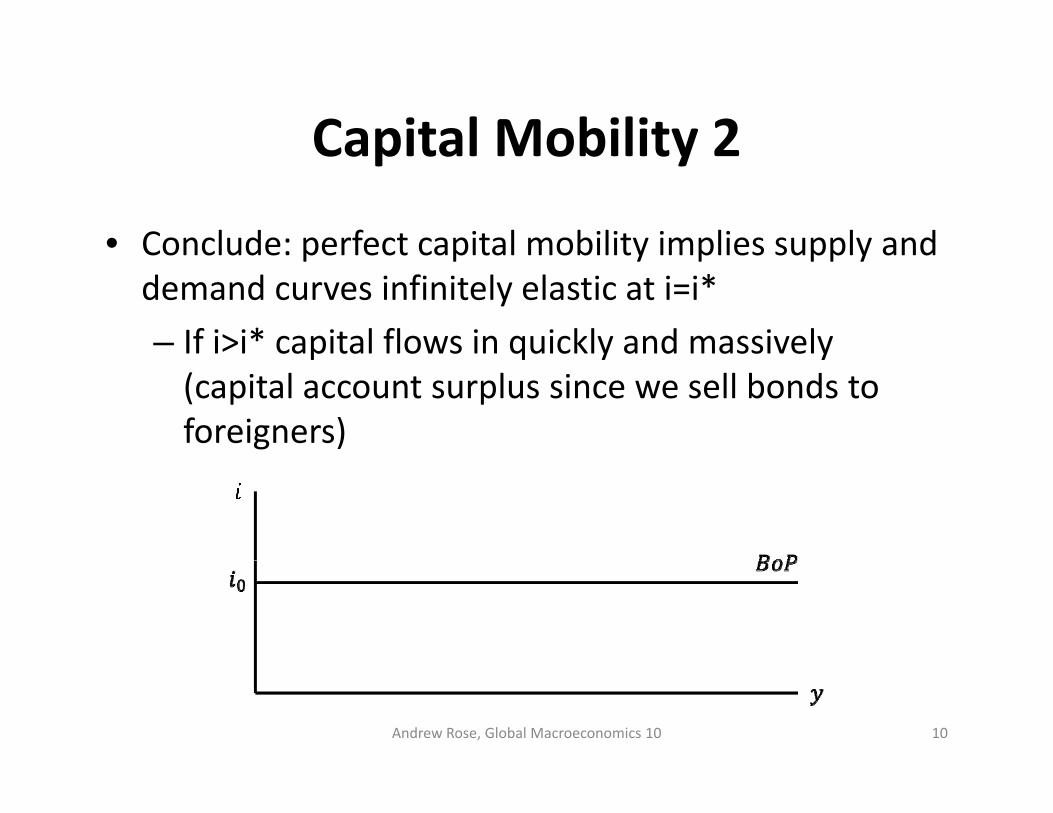

Capital Mobility 2Capital Mobility 2

• Conclude: perfect capital mobility implies supply andConclude: perfect capital mobility implies supply and demand curves infinitely elastic at i=i*– If i>i* capital flows in quickly and massively p q y y(capital account surplus since we sell bonds to foreigners)

10Andrew Rose, Global Macroeconomics 10

Summary: Mundell‐Fleming ModelSummary: Mundell Fleming Model

• Real economy (IS)Real economy (IS)– Looks same as before, but NX added (foreign income and real exchange rate fixed)

• Financial markets (LM)– Looks same as before, though now money is endogenous (international reserves used to defend exchange rate, affect money supply)

B l f P (B P)• Balance of Payments (BoP)– New: horizontal because of capital mobility: i=i*

11Andrew Rose, Global Macroeconomics 10

FormallyFormally

IS Y A(G i Y) + NX( YY*)• IS: Y = A(G,i,Y) + NX(,Y,Y*)

where A= {1/(1 ‐ c(1‐t))}*[C0 + cTr + I0 – bi + G0],0 0 0

and ,Y* exogenous

• LM: Ms/P = L(i, Y)

where Ms = HPM = (IR + CBC)where Ms = HPM = (IR + CBC)

• BoP: c/acc + k/acc + ORS = 0

12Andrew Rose, Global Macroeconomics 10

GraphicallyLM

i

Graphically

BoPi*

A

IS

YAndrew Rose, Global Macroeconomics 10 13

Y*

Monetary Policy (LM) ShockMonetary Policy (LM) Shock• Expansionary Open Market Opera on (CBC↑)

d ↓ l l• Leads to i↓, capital ou lows, interven on

LMi

A

LM'

BoPi*

BB

14Andrew Rose, Global Macroeconomics 10 Y

IS

Enduring EffectEnduring Effect

N t th t t l b k l h• Note that central bank can only change

composition of high‐powered money since it p g p y

defends fixed exchange rate (IR↓) to offset

capital outflow (HPM and Ms unchanged)

15Andrew Rose, Global Macroeconomics 10

Key Concept: Mundell’s bl / lIncompatible/Holy Trinity

• The following are individually desirable butThe following are individually desirable but mutually incompatible:1 Independent national monetary policy1. Independent national monetary policy

(“Monetary Sovereignty”)2 Perfect capital mobility2. Perfect capital mobility3. Fixed/stable exchange rates

• Different countries make different “sacrifices”• Different countries make different sacrifices and choices also change over time

16Andrew Rose, Global Macroeconomics 10

Fiscal PolicyFiscal Policy• G↑ (debt‐financed) leads to capital inflows, IR↑, HPM↑, Ms↑ and Y↑

IS'

LM

i

B

IS'

LM

IS

B

ALM'

BoPi*

A

C

17Andrew Rose, Global Macroeconomics 10

Y

Enduring EffectEnduring Effect

Hi hl t t ( “ di t” i• Highly potent (no “crowding out” since

interest rates given from abroad)g )

• Changes composi on of output (G↑, NX↓)

– Can explain “twin deficits” of government, c/acc

Andrew Rose, Global Macroeconomics 10 18

Foreign (Interest Rate) ShockForeign (Interest Rate) Shock

• Foreign (large country) interest rate rise (i*↑)Foreign (large country) interest rate rise (i ↑)

– BoP schedule shifts upLM’

BLM

LM

A

IS

19Andrew Rose, Global Macroeconomics 10

Foreign Shocks, ContinuedForeign Shocks, Continued

• Role in crises/regime switchRole in crises/regime switch– Mexico 1994, EMS 1992– Decline in Northern rates 2001, 2007‐8Decline in Northern rates 2001, 2007 8

• Sterilization of reserve flows: offsetting change in international reserves with equal and oppositeinternational reserves with equal and opposite change in central bank credit– As IR falls, CBC rises 1:1As IR falls, CBC rises 1:1– HPM unchanged– Only possible temporarilyy p p y

20Andrew Rose, Global Macroeconomics 10

NotesNotes

• Can generalize (im‐) potency ofCan generalize (im ) potency of monetary/fiscal shocks to all financial/real shocksshocks

• Can allow for imperfect capital mobility with upwards sloping BoP (must raise interest ratesupwards sloping BoP (must raise interest rates above foreign to attract inflows)

O t d l “l ” t– One way to model a “large” country

21Andrew Rose, Global Macroeconomics 10

Key TakeawaysKey Takeaways

• Credible fixes constrain monetary policyCredible fixes constrain monetary policy• Real shocks have large effects during fixes

d ll’ il d ff b• Mundell’s Trilemma: tradeoffs between open capital markets, stable exchange rates, and

imonetary sovereignty

Andrew Rose, Global Macroeconomics 10 22