35

Business Opportunities in Uruguay April 2011

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 216 times |

| Download: | 3 times |

Business Opportunities in Uruguay

April 2011

• Very strong democracy and social and political stability

• Continued growth and investment

• Strategic location

• Best labor value for money in the region

• Highest internet and PC penetration in Latin America

• Attractive promotion regimes which encourage investment

These are exciting times for Uruguay:

2

Outstanding Value

Democracy Index(Economist Intelligence Unit 2010)

Worldwide

Noruega 1

Nueva Zelanda 5

Irlanda 12

EE.UU. 17

España 18

Corea del Sur 20

Uruguay 21

Costa Rica 24

Portugal 26

Italia 29

Within South America

Uruguay 1

Economic Freedom Index(Heritage Foundation 2011)

Worldwide

Nueva Zelanda 4

Irlanda 7

EE.UU. 9

Chile 11

Noruega 30

España 31

Uruguay 33

Corea del Sur 35

Colombia 45

Costa Rica 49

Within South America

Uruguay 2

Low Corruption (Transparency International 2010)

Worldwide Nueva Zelanda 1Noruega 10Irlanda 14Chile 21EE.UU. 22Uruguay 24Francia 25España 30Portugal 32Corea del Sur 39

Within South AmericaUruguay 2

Political and Social Stability3

Quality of Life• Free from natural disasters

• Tolerant country: no ethnic, racial or religious conflicts

• Excellent sanitary level. Child mortality rate: 9.5 every 1,000 (2009), vs. 22.8 in Latin America (2007)

• One of Latin America’s safest countries, evidenced by the booming second home market (3rd in Latin Business Chronicle 2009 Index)

• Ranked among the first countries, with the Scandinavian countries and Japan, in US-based Freedom House’s Freedom in the World Survey 2009

4

Global Peace Index (ranking)

New Zealand 1

Ireland 6

Uruguay 24

Spain 25

Chile 28

UK 31

Italy 40

Argentina 71

Brazil 83

US 85Source: Economist Intelligence Unit 2010

1.7%2.6%2.8%3.3%4.0%

5.0%5.0%

7.5%7.5%8.3%8.5%

9.7%10.5%

15.3%

0% 5% 10% 15% 20%

EurozoneUSA

JapanGermany

RussiaChile

MexicoBrazil

ArgentinaPeru

UruguayIndia

ChinaParaguay

5

Cumulative Annual Growth Rate (2004–2010): 6.3%

Sources: Central Bank of Uruguay : IMF, World Economic Outlook, October 2010

GDP growth in constant values

Source: IMF, World Economic Outlook, October 2010

Estimated GDP growth in 2010

A Growing Economy

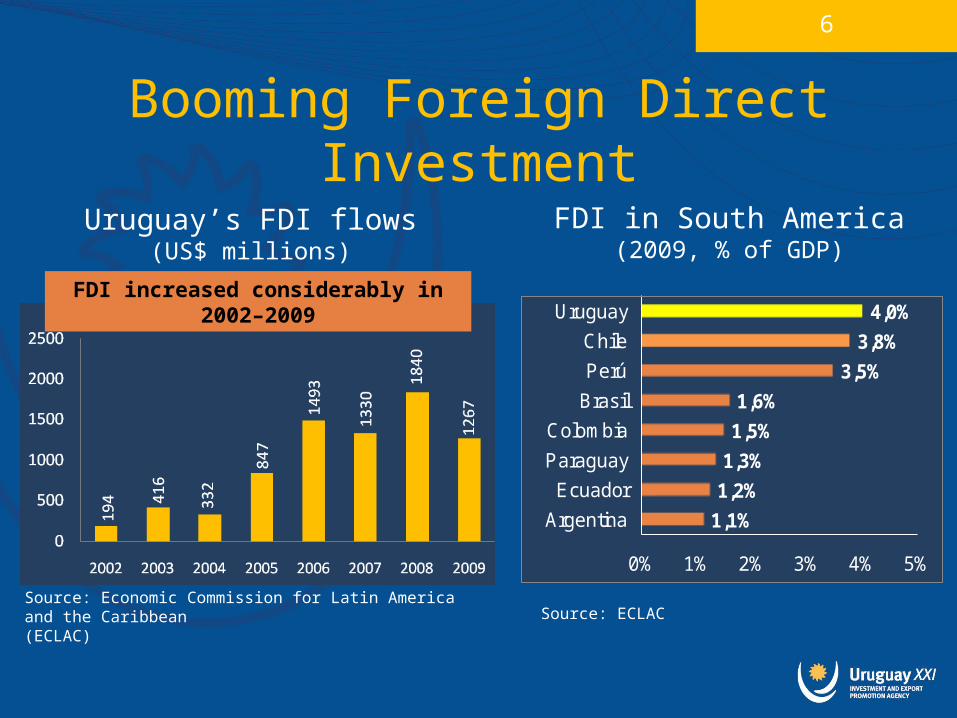

Booming Foreign Direct Investment

FDI in South America (2009, % of GDP)

Uruguay’s FDI flows (US$ millions)

6

FDI increased considerably in 2002–2009

Source: Economic Commission for Latin America and the Caribbean (ECLAC)

Source: ECLAC

1,1%

1,2%

1,3%

1,5%

1,6%

3,5%

3,8%

4,0%

0% 1% 2% 3% 4% 5%

Argentina

Ecuador

Paraguay

Colombia

Brasil

Perú

Chile

Uruguay

Goods and Services (2010, % of total exports)

Strong Growth in Exports

7

0100020003000400050006000700080009000

10000Services

Goods

Exports have tripled in the past 6 years

Uruguayan Exports (US$, millions)

Source: Central Bank of Uruguay (BCU) * Forecast for 2010 Source : Central Bank of Uruguay (BCU)* Forecast for 2010

Export Break-OutMain products and services

Goods (2010) Services (2010)

8

Sources: Central Bank of Uruguay (BCU) and Trademap; Uruguay XXI’s calculations

Meat 19%

Cereals 12%

Oil, Soy-beans and Seeds 11%

Wood pulp 10%Dairy products 8%

Wood products

4%

Plastics 4%Wool 3%

Other 30%

Other 30%Raw hides, skins and leather

3%

Vehicles and auto parts

3%

Fish 3%Malt, wheat flour 2%Livestock 2%Petroleum oils 2%Fruits 2%Fats, Oils 2%Pharmaceuticals 2%Rest 9%

Transport 17%

Travel 61%

Other Services

22%

Main Destinations of Goods Exports2010

9

Source: National Customs Administration

2000

Uruguay- Greece

Trade Balance Uruguay - Greece

2006 - 2010

11

Source: National Customs Administration Note: Date does not include stadistics of oil

-2

-1

0

1

2

3

4

5

2006 2007 2008 2009 2010

Export Import Trade Balance

US$ millions

Main Exported ProductsUruguay-Greece

2010

12

Source: National Customs Administration

(NCM 1201)Soya beans

85%

(NCM 0805)Citrus fruit

6%

(NCM 0303)Fish,frozen

5%

(NCM 0201)Meat of bovine

animals, fresh or chilled

2%

Others2%

Main Imported ProductsUruguay-Greece

2010

13

(NCM 2401)Tobacco

unmanufactured52%

(NCM 8507)Electric

accumulator18%

(NCM 8424)Machinery for

projecting, liquids or powders

12%

(NCM 9504)Articles for funfair,

table or parlour games

4%

(NCM 6002)Knitted or crocheted

fabrics3%

Others11%

Source: National Customs Administration. Note: Date does not include Stadistics of Oil

Strategic Location

14

Rio de Janeiro1,490mi

72-96 hrs

São Paulo1,225mi

72-96 hrs

Porto Alegre540mi

24-48 hrs

MontevideoBuenos Aires

155mi24 hrs

Asunción960mi

72-96 hrs

Santiago1,180mi

72-92 hrs

Uruguay:A safe, reliable and

competitive location, providing an unbeatable logistics base in the heart of the wealthiest region of

South America

Gateway to the Region

15

Access to a Large and Wealthy MarketAccess to a large and growing consumer market due to our

membership in MERCOSUR and our open economy

Uruguay MERCOSUR

Population (millions) 3.3 241

Area (km2) 176,215 11,878,244

GDP 2010* (US$ billions) 38.4 2,283

GDP per capita 2010* (US$) 11,454 9,467

GDP growth rate 2010* (%) 8.4 7.5

16

Sources: Central banks and national statistics institutes* Forecast for 2010, source: IMF (WEO)

Goods in transit:2009: 47.3% – 2010: 51.4%

Platform for the RegionMovement of containerized cargo in the port of Montevideo

17

Source: National Ports Authority (ANP)

Notes:• Includes imports, exports, transit and transfer • TEU = twenty-foot equivalent unit

Modern Infrastructure• World-class port facilities in Montevideo, a regional

hub par excellence for South America’s Southern Cone region

• Boasts Latin America’s most dense highway network

• 2009: new airport terminal, Colonia ferry port and Montevideo ring road

• Reliable electric supply (mostly from renewable sources)

18

Quality of electricity supply (ranking)

UK 15

Ireland 25

Chile 30

Spain 36

Uruguay 37

Hungary 46

Italy 47

New Zealand 56

Brazil 63

Argentina 93

Source: World Economic Forum’s Global Competitiveness Report 2010-2011

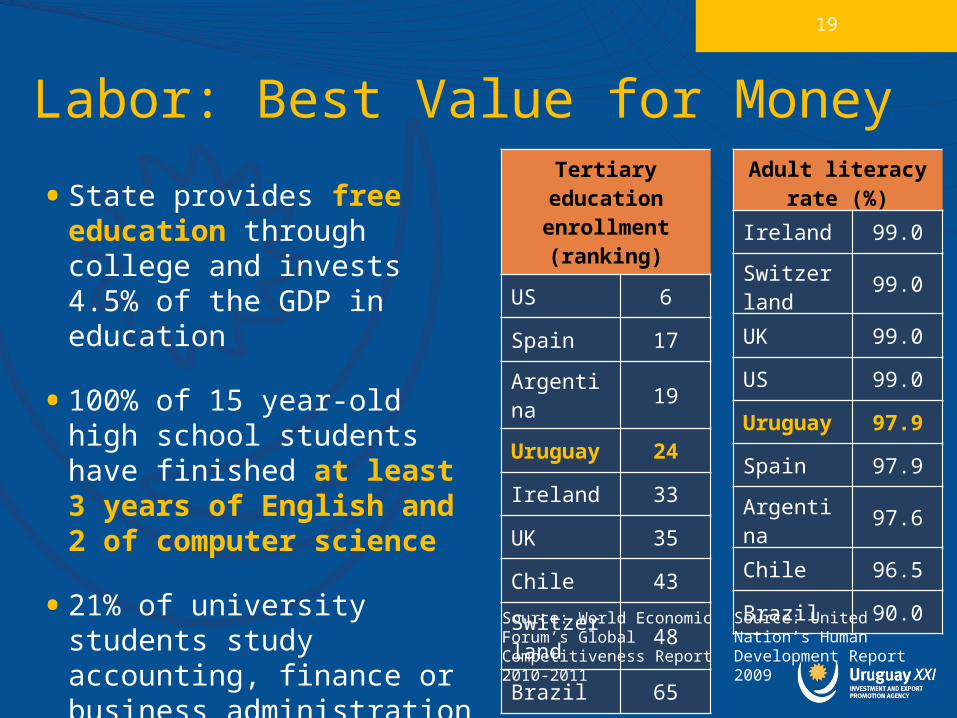

• State provides free education through college and invests 4.5% of the GDP in education

• 100% of 15 year-old high school students have finished at least 3 years of English and 2 of computer science

• 21% of university students study accounting, finance or business administration

19

Tertiary education enrollment (ranking)

US 6

Spain 17

Argentina 19

Uruguay 24

Ireland 33

UK 35

Chile 43

Switzerland 48

Brazil 65

Source: World Economic Forum’s Global Competitiveness Report 2010-2011

Labor: Best Value for Money Adult literacy rate

(%)

Ireland 99.0

Switzerland 99.0

UK 99.0

US 99.0

Uruguay 97.9

Spain 97.9

Argentina 97.6

Chile 96.5

Brazil 90.0

Source: United Nation’s Human Development Report 2009

Highest Ranked in LatAm in Use of Modern Communications

Mobile telephone subscribers

Fixed telephone lines Internet users Internet access

in schoolsRank Rank Rank Rank

UK 24 UK 11 UK 9 UK 18

Argentina 25 Ireland 18 Ireland 28 Uruguay 26

Uruguay 44 Costa Rica 38 Uruguay 41 Chile 42

Ireland 51 Uruguay 48 Colombia 47 Ireland 58

Chile 64 Argentina 53 Brazil 57 Costa Rica 64

Colombia 74 Brazil 62 Costa Rica 66 Brazil 72

Brazil 76 Chile 63 Chile 68 Colombia 88

Mexico 93 Mexico 72 Argentina 74 Mexico 89

Costa Rica 119 Colombia 77 Mexico 85 Argentina 111

Source: World Economic Forum’s Global Competitiveness Report 2010-2011

20

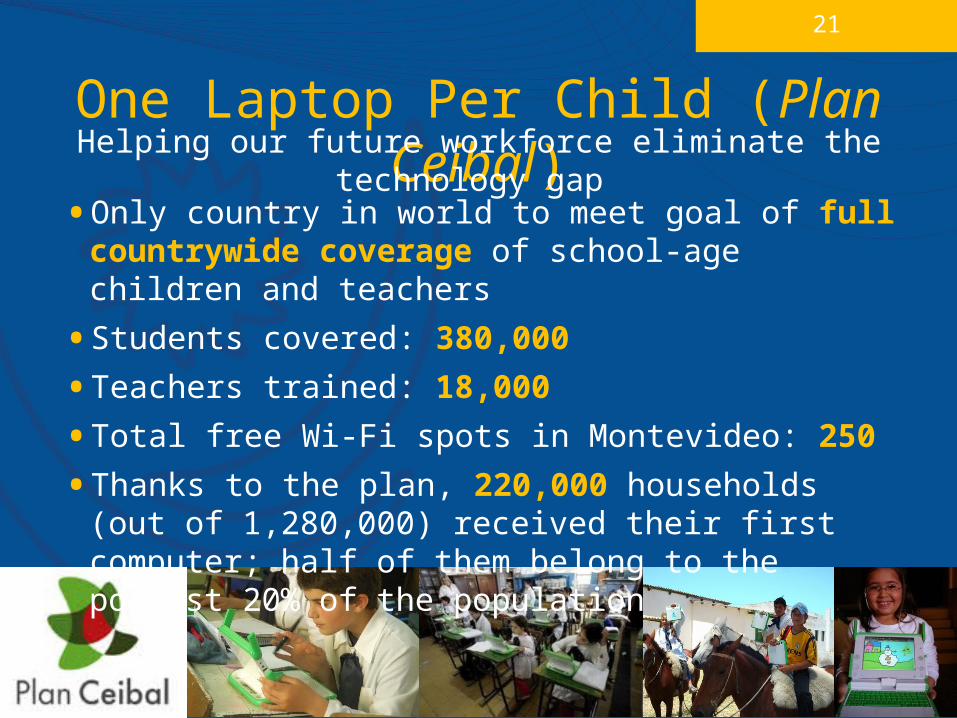

• Only country in world to meet goal of full countrywide coverage of school-age children and teachers

• Students covered: 380,000

• Teachers trained: 18,000

• Total free Wi-Fi spots in Montevideo: 250

• Thanks to the plan, 220,000 households (out of 1,280,000) received their first computer; half of them belong to the poorest 20% of the population

One Laptop Per Child (Plan Ceibal)Helping our future workforce eliminate the technology gap

21

Beneficial Promotion Systems

• The government recognizes the important role of the FDI and maintainsa favorable investment climate

• Uruguay has a track record of attracting large investments in agricultural, industrial, services and infrastructure

• Investment Law (Nº 16,906) - January 1998:

Domestic and foreign investors are treated equally Foreign investments do not require prior authorization or registration Free transferability of capital and profits overseas

• In 2008 the government created a one-stop shop to assist investors and an automatic, predictable, transparent and effective mechanism that benefits a broader base of firms and specifies objective criteria for granting incentives

• The United Kingdom and Uruguay signed an Investment Promotion and Protection Agreement between the two nations in 1997

Comprehensive legal framework for investment

22

• Exemption from Corporate Income Tax* for up to 100% of the amount invested and for a period of up to 25 years, which depend on a matrix of targets and indicators, and the size of the project

• Exemption of Wealth Tax on civil works for 8 to 10 years, and on fixed assets throughout their life

• Exemption of import taxes and fees on fixed assets declared non-competitive with the domestic industry

• 100% refund of VAT, under the exporters regime, on the acquisition of materials and services for civil works in the domestic market

23

Beneficial Promotion SystemsTax benefits

* Corporate Income Tax exists only at the national level (25%)

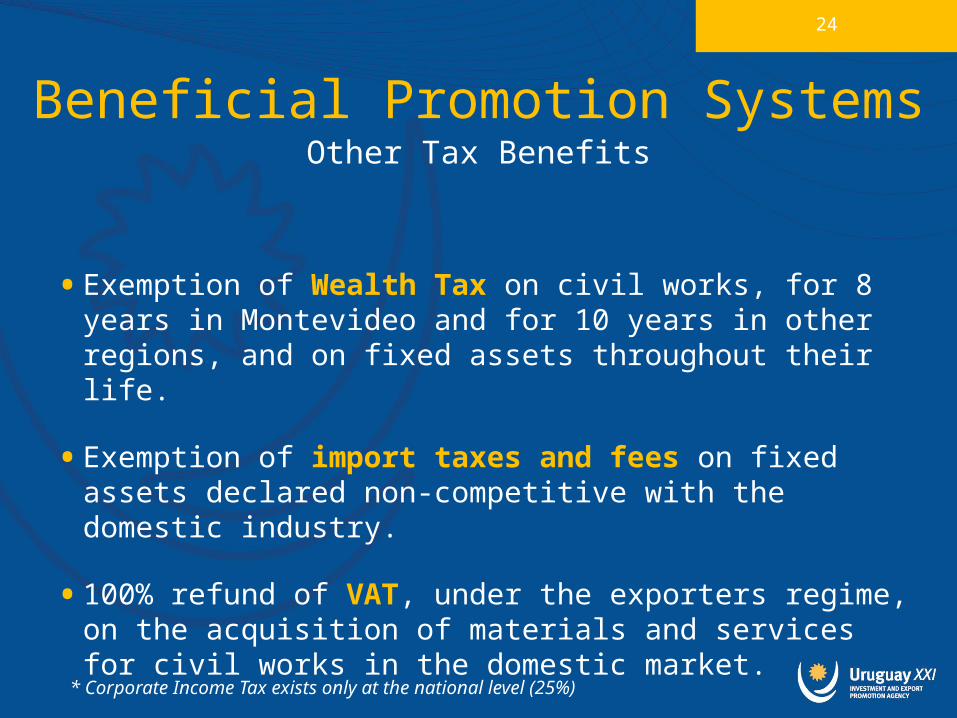

24

Beneficial Promotion SystemsOther Tax Benefits

* Corporate Income Tax exists only at the national level (25%)

• Exemption of Wealth Tax on civil works, for 8 years in Montevideo and for 10 years in other regions, and on fixed assets throughout their life.

• Exemption of import taxes and fees on fixed assets declared non-competitive with the domestic industry.

• 100% refund of VAT, under the exporters regime, on the acquisition of materials and services for civil works in the domestic market.

25

•Temporary Admission is the tax-free introduction of foreign goods to the domestic market

•Goods to be exported, within 18 months, in the same state they were introduced or after having been subject to certain processing (manufacturing, repairing or value added processes)

•The Temporary Admission regime also applies to machinery and equipment from any source, entering temporarily for maintenance, repair or upgrade.

Temporary Admission(similar to the drawback regime)

Free Trade Zones• Users 100% exempt from:

• Corporate Income Tax • Wealth Tax• Import levies• Any other tax created or to be created in the future*

• Can develop industrial, commercial or service activities

• Technology and service-oriented business parks operating as FTZs in Montevideo:

• Zonamerica• Aguada Park• World Trade Center Free Zone (2011)• Parque de las Ciencias (2011)

2626

*Companies within the FTZs must pay social security contributions for their Uruguayan employees.

Free Ports and Free Airports• Only free ports on South America’s Atlantic coast

• Free transit of goods, no authorizations or formal procedures are required

• Within port facilities, goods are exempt from:oall import taxes or chargesoall domestic taxes (e.g. VAT)

• Services rendered are exempt from VAT

• Foreign registered companies are exempt from wealth tax and income tax

• Diverse operations may be performed on the merchandise, including warehousing, repackaging, relabeling, classification, grouping, ungrouping, consolidation, deconsolidation, manipulation or fractioning as well as value adding tasks that do not modify the nature of the product

27

• Optimal logistic location in South America’s Southern Cone where the Río de la Plata, Paraná and Uruguay Rivers converge with the Atlantic Ocean

• Unique and favourable legal system for logistics activities: Bonded Warehouses, Free Zones, Free Ports and Free Airports

• RDCs in Uruguay allow users to:Cut logistic costs, delays and inventories in neighbouring

countriesStore and perform diverse operations on the goodsGenerate financial savings on delayed levies at final market

• Uruguay boasts Latin America’s densest highway network and excellent connectivity to neighbouring countries

• Lorry time to reach main destinations: Argentina: 24hs, Brazil: 24-96 hs, Chile: 72-96 hs

28

Regional Distribution Centers (RDCs)

Foreign Investors

29

In Summary

These are exciting times for Uruguay:

• Our economy is growing

• We top many Latin American rankings

• Investments are pouring in

• We are carrying out many innovative programs

Do business with us!

30