24

Comparing profitability of firms in US, Germany and Japan By: Group 4 Gayatri Bhuvanagiri 13 Manas Mendiratta26 Mehul Gahrana 27 Rajesh TR 36 Sahil Sharma 38

Comparing profitability of firms in US,

Germany and Japan

By: Group 4Gayatri Bhuvanagiri 13Manas Mendiratta 26Mehul Gahrana 27

Rajesh TR 36Sahil Sharma 38

AGENDA

Introduction

Parameters of profitability

Points of distinction

Review of previous studies

Review of present study

Conclusion

Globalization leads to identical environmental threats and opportunities

Firms in similar environment follow similar organizational structures

Similar firms located in different countries would not have significant differences in profitability

Other Factors:

Differences in business practices Difference in Accounting

standards Not all firms are global Ability of governments to

dictate competitive environment

General Perception

Countries studied:US, Germany and Japan

INTRODUCTION

Measures of profitability: Return on Assets Return on Equity Operating Margin

𝑅𝑒𝑡𝑢𝑟𝑛𝑜𝑛𝐸𝑞𝑢𝑖𝑡𝑦=𝑛𝑒𝑡 𝑖𝑛𝑐𝑜𝑚𝑒

𝑎𝑣𝑒𝑟𝑎𝑔𝑒𝑡𝑜𝑡𝑎𝑙𝑒𝑞𝑢𝑖𝑡𝑦

Factors affecting profitability: Tax Rate Effect of using debt vs equity to finance

firm’s activity Accepted method of accounting for

Depreciation R&D spending Minority investments Leases Currency Transactions

• ROA and ROE affected more• Large portion of income is not from

operational activities

PARAMETERS OF PROFITABILITY

Difference in methods to account for depreciation

Straight line depreciation

•Depreciation is the same amount each year•Higher incomes and assets in short run•US•Germany

Accelerated depreciation•More depreciation in early years and less in later years•Lower incomes and assets in short run•Japan•Germany

German & Japanese firms report lower operating margins, ROE & ROA than American ones

Difference in methods to prepare consolidated financial statements

US

• Most firms consolidate since 1950s

• Equity method

Germany

• Consolidate majority owned subsidiaries in EU

• Flexible requirement tend to improve reported earnings

• Cost method

Japan

• Do not fully consolidate their activities

• Flexible requirement tend to improve reported earnings

• Depends on no. of majority owned subsidiaries

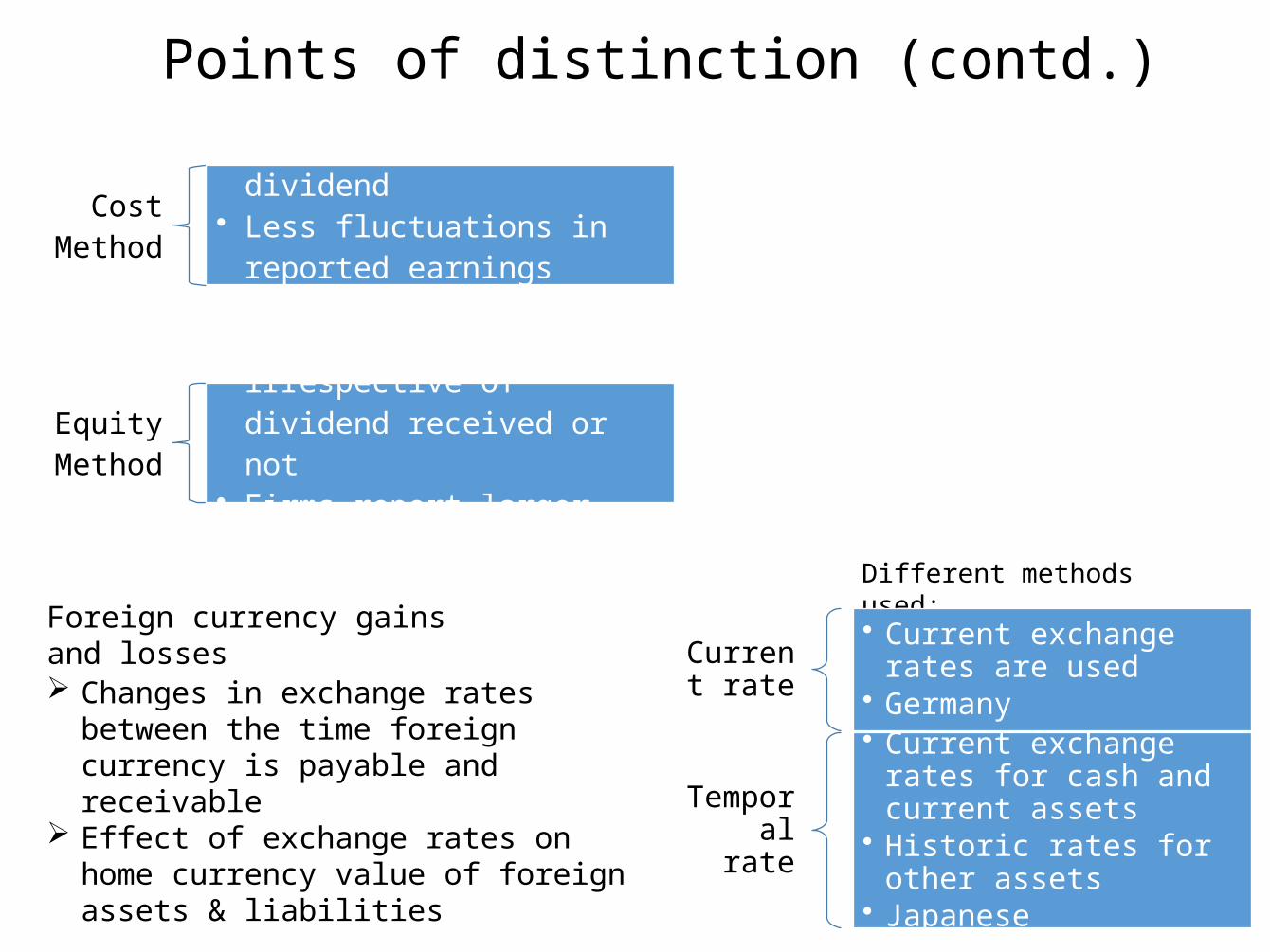

Points of distinction

Cost Method

• Earnings from minority investment reported only when it receives a dividend

• Less fluctuations in reported earnings

• ROAs, ROEs more stable• Firms report higher incomes

Equity Method

• Earnings from minority investment reported irrespective of dividend received or not

• Firms report larger assets• Lower ROAs

Foreign currency gains and losses

Changes in exchange rates between the time foreign currency is payable and receivable

Effect of exchange rates on home currency value of foreign assets & liabilities

Different methods used:

Current rate

• Current exchange rates are used

• Germany

Temporal rate

• Current exchange rates for cash and current assets

• Historic rates for other assets

• Japanese

Points of distinction (contd.)

Other factors

Use of general and special reserve funds in Germany and Japan

Difference in corporate tax rates

Difference in levels of debt finance activities

Points of distinction

Review of Previous Research• Comparison of MNEs

• In their countries is not possible• Comparison was done in a third country

• Example, in Belgium comparison was done of the largest 100 Belgian companies with 100 largest American and European companies

• Comparison in US, Japan or Germany with companies from other countries

Review of ResearchStudy by Choi

• Study of manufacturing companies in the U.S. and Japan by Choi (1982) found substantial differences in the average returns on sales (ROS) returns on assets, and returns on net worth of firms in each country• Japanese firms generated substantially lower returns than their American counterpart• When these ratios were adjusted to reflect a common set of accounting rules, Choi concluded that restatement explained only a minor portion of the observed differences

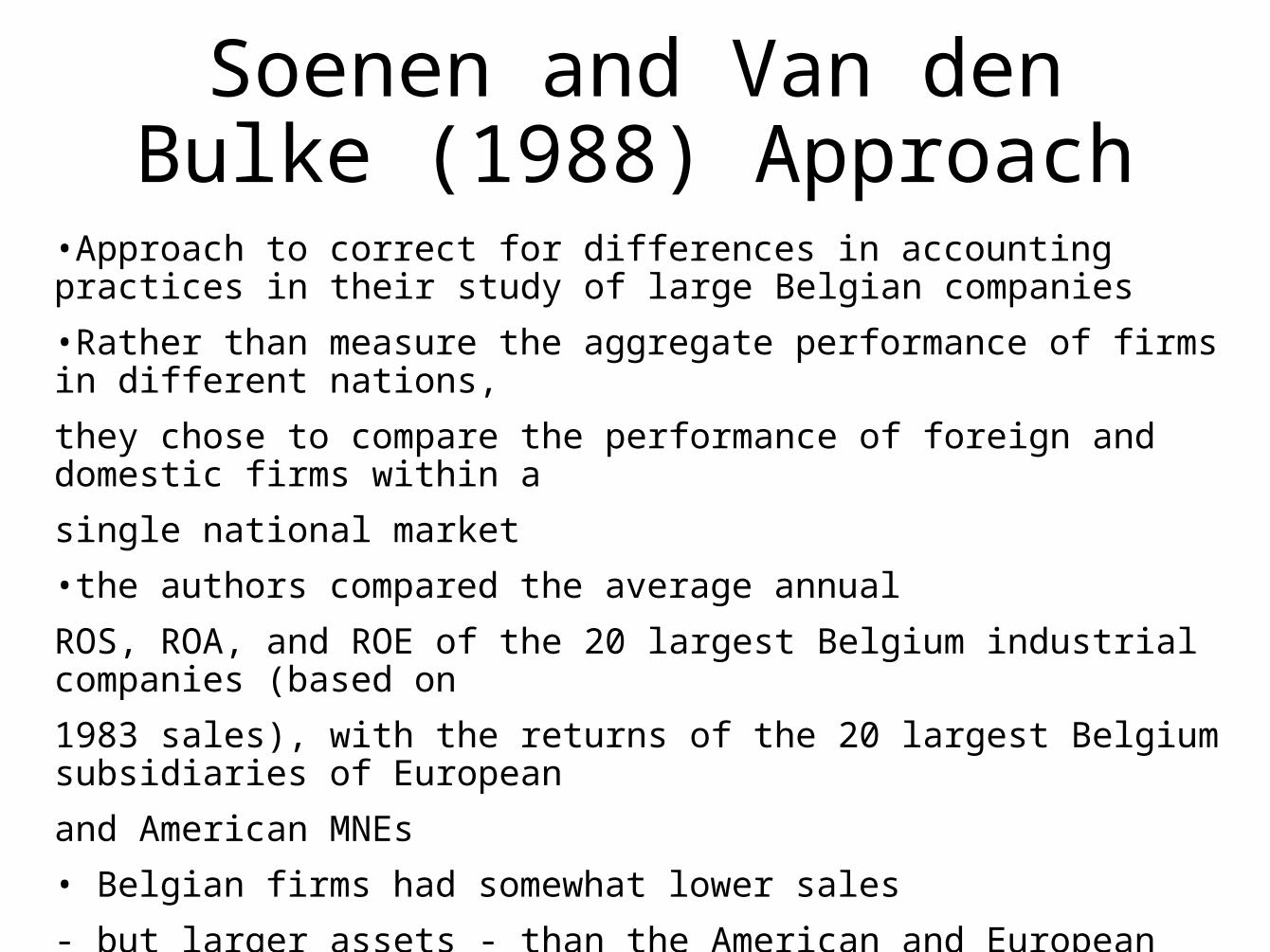

Soenen and Van den Bulke (1988) Approach

•Approach to correct for differences in accounting practices in their study of large Belgian companies

•Rather than measure the aggregate performance of firms in different nations,

they chose to compare the performance of foreign and domestic firms within a

single national market

•the authors compared the average annual

ROS, ROA, and ROE of the 20 largest Belgium industrial companies (based on

1983 sales), with the returns of the 20 largest Belgium subsidiaries of European

and American MNEs

• Belgian firms had somewhat lower sales

- but larger assets - than the American and European subsidiaries, and earned

consistently lower returns over the 1979-83 period

• American subsidiaries earned the highest return

Study of the 100 largest American and European

MNEs• Geringer, Beamish, and daCosta (1989) uncovered large differences inthe average ROSs and ROEs of each group over the 1977-81 period•U.S. •MNEs generated average annual returns on sales of 5.16%, versus 1.52% for European firms; and average returns on assets of 6.82%, compared to 2.05% for European MNEs.•No attempt was made to adjust for differences in accounting practices or tax rates since the study's primary objective was not to assess differences in profitability between nations, but rather to examine the relationship between a firm's diversification strategy and its performance

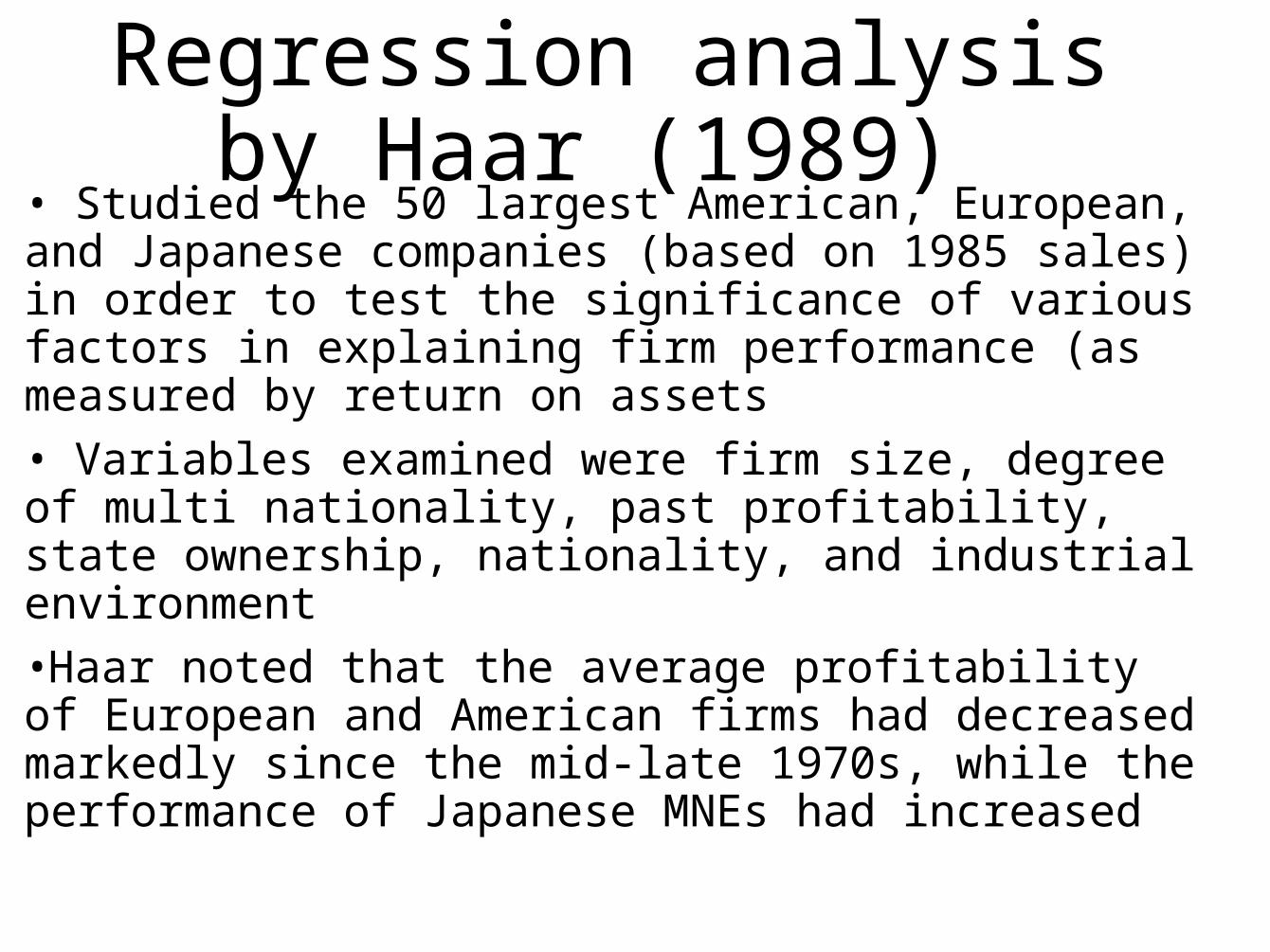

Regression analysis by Haar (1989)

• Studied the 50 largest American, European, and Japanese companies (based on 1985 sales) in order to test the significance of various factors in explaining firm performance (as measured by return on assets• Variables examined were firm size, degree of multi nationality, past profitability, state ownership, nationality, and industrial environment•Haar noted that the average profitability of European and American firms had decreased markedly since the mid-late 1970s, while the performance of Japanese MNEs had increased

Review of Previous Research• Findings:

• In 70s and early 80s American firms outperformed their Japanese and German counterparts

• By mid 80s European and American profitability had become decreased while Japanese profitability had increased

• Americans continued to outperform their rivals till late 90s

Review of Previous Research• Limitations

• Differences in accounting methods wasn’t considered• Tax rate was different and in some studies this was not

accounted for• Differences in approach of each study made them

incomparable

The Present Study

• 1984-90 data used• Data for 3000 leading companies taken and their

profitability analyzed• ANOVA was used to test variance in the ratios of

countries over a 5 year period• Findings

• ROA, Operating margin were different but ROE was same for the countries

• After adjusting for tax, ROE became different but ROA was same

• American firms exhibited more variance in general. Both out-performed and under-performed

The Present Study

• After other adjustments related to tax and accounting standards• There were still differences on Profitability ratios of the 3

countries• But these difference were not as much as the earlier

studies suggested• Japan’s increase in prof. has continued whereas America

and Europe’s decline continues so as to attain a more equal level

Overview of the Empirical Study

Primary objective of the paper: Examine relative profitability of firms in Germany, Japan and United States

•Empirical study of the average annual return on assets, return on equity and operating margin was conducted

•100 companies from each country were selected for the study of each profitability indicator

•Annual averages and a five year national average were calculated for each period

•ANOVA used to identify significant differences between the performance of firms in each nation

•Multi year averages used-to reduce impact of unique events which affect the performance of firms, like exchange rate of volatility, political events, nation’s

position on business cycle

Discussion

Identified statistically significant differences in the profitability of large American, German, and Japanese industrial companies in two of the three indicators employed

• the most important differences emerged in the operating margins of firms from each nation, where German firms consistently earned lower margins than their Japanese and

American counterparts over the 1984-90 period

• Based on five-year averages, German firms had annual operating margins only half those of Japanese and American companies

•much of this difference stemmed from the extremely poor performance of German firms between 1987 and 1990

•On the other hand, firms in all three countries appear to have broadly similar returns on assets and returns on equity

•average annual ROAs of Japanese and German companies were 40-50% less than those of American firms, but much of this apparent difference is an artifact of differences in tax

rates between the three countries

•When ROAs are adjusted to reflect a common 50% effective tax rate in each nation, differences in the five-year, adjusted annual ROAs are no longer statistically significant

•No statistically significant differences were observed in the five-year, average annual returns on equity of firms in each nation; although Japanese firms generally earned somewhat lower returns

than their American and German counterparts

•when adjustments were made to reflect equivalent tax rates in each country, significant differences were found in the five- year, adjusted annual ROEs, with German firms achieving

adjusted returns about 35% higher than similar Japanese and American companies

•This finding is difficult to explain since it was suggested that the greater use of debt in the U.S. and Japan would produce higher (not lower) ROEs.

•One possible explanation for this disparity is that Japanese and American companies are not earning enough on their invested capital to offset the additional interest expenses they must bear

•Another explanation for the difference in adjusted ROEs is that German companies generated a great deal of their incomes from sources other than operations, particularly after 1987

•As a result, the operating margins of German firms have remained low, while mea- sures of profitability based on net income have been substantially higher.

•

•One of the study's most interesting findings is that all three profitability indicators exhibited far less variability - both across firms and over time - for

Japanese and German firms than for similar American firms

• Specifically, the standard deviations of both the annual and five-year averages of all three profitability indicators were substantially lower for

Japanese and (to a lesser extent) German companies than for their American counterparts

•Two factors may explain these findings. First, specific accounting practices in Japan and Ger- many which allow firms to "control" their reported incomes

to some extent; and second, unique aspects of the institutional structures of both countries which create a more stable economic environment

•various accounting practices allow firms in Germany and Japan to "smooth" fluctuations

in their reported earnings to some extent

•Particularly important in this regard are the widespread use of reserve funds and the

cooperative nature of business relationships which could allow firms in both countries to

maintain relatively stable rates of return even during periods of economic adversity

•However, an equally compelling explanation for the stabil- ity of returns in Germany and

Japan involves several characteristics of these nations' economic and social climate

Perhaps the most important of these are:

•the high degree of government participation in the development and promotion of long-term economic policies and objectives

• the greater degree of cooperation-both between business and government

•the close relationship between workers and managers, and the greater degree of worker participation

• the ability of banks (and other corporations) to act as stable, long-term capital providers and shareholders in domestic companies

Conclusions• For large firms there seems to be only minor differences in the real performance of firms in the U.S., Germany, and Japan• Based on the results of this study, operating margins in all three nations averaged between 4-6%, ROAs between 8-12%, and pretax ROEs• Accounting practices appear to have played only a minor role in these results• Aside from Japanese and German practices which allow firms to "control" their reported earnings to some extent, specific attempts have been made to reduce the impact of other important accounting differences.• For example, ROAs and ROEs have been adjusted to reflect differences in tax rates between in three countries, and operating margins and ROAs are unaffected by differences in firms' financial structure• Rates of depreciation were broadly similar in all three countries over most of the period studied, while the effects of other accounting differences tend to counter balance each other