130

Business Valuation 101 Demystifying Business Valuation for Small Business Owners Theresa Zeidler- Shonat Director of Valuation Services 1

| Date post: | 15-Jul-2015 |

| Category: |

Business |

| Upload: | theresa-zeidler-shonat |

| View: | 745 times |

| Download: | 9 times |

Business Valuation

101Demystifying Business Valuation for

Small Business Owners

Theresa Zeidler-

ShonatDirector of Valuation Services

1

What is Business Valuation?

2

The Short Answer

• Business valuation is a process and a

set of procedures used to estimate the

economic value of an owner's interest

in a business.

3

Poll Question

4

Let’s Start with Terminology…

• What’s the difference between “Valuation” and “Appraisal?”

5

Definition: Valuation

• Valuation – (noun) the act or process of determining the value of a business, business ownership interest, security, or intangible asset.

6

Definition: Appraisal

• Appraisal - (noun) the act or process of developing an opinion of value; an opinion of value.

7

WHEN DO YOU NEED A VALUATION?

8

Estate and Gifting

• Death of business owner

• Transfer of business ownership to the

next generation through gift of shares

9

Divorce

• A party in the divorce holds an equity

position in a closely-held company, or

owns intellectual property that is

considered part of the divisible marital

property (“undivided one-half marital

property interest”)

10

Lending Scenarios

• Some SBA loans require a business

valuation if a specific set of conditions

exist

• Intangible assets are being used as

collateral and the lender wants an

idea of their worth

11

Business Planning

• Strategic planning - company is

considering several options and is

wanting to determine the impact

of several scenarios

• Succession planning

• Exit Planning

• Impact of expanding into new

industry or making an acquisition

12

Financial Reporting

• Company has just been acquired or

made an acquisition: purchase price

allocations (ASC 805)

– Total purchase consideration is allocated

to the acquired assets.

– Includes intangible asset valuations

13

Financial Reporting

• Company has goodwill or indefinite-

lived intangible assets on their balance

sheet from a previous acquisition -

impairment testing (ASC 350)

14

Financial Reporting

• Company holds a minority interest in

another company and is required to

mark that investment to market

15

Stock-Based Compensation

• 409A valuations.

– Private companies are required by

the IRS (Section 409A) to show that

their common stock options are

issued at fair market value, and

therefore must conduct a formal

valuation opinion at least once

every 12 months to avoid potential

tax penalties.

16

Stock-Based Compensation

• ASC 718 valuations. – ASC 718 requires that all equity

awards granted to employees, consultants, and board members be accounted for at "fair value" and then expensed over the vesting term of the grant.

– This can become more difficult as additional grants are made and vesting and forfeitures add complexity to the calculations.

17

Intangible Asset / Intellectual

Property Monetization

• Company is considering

monetizing assets - either through

use as collateral or licensing the

asset to a third party

• Company is contemplating sale

of the asset and need help

determining a price

• Company is contemplating

purchase of an asset and looking

to determine if price is fair 18

Buy-Sell Agreement

Development • Most buy-sell agreements have a

provision for determining the price at

which an interest in the company is

sold.

– Basing this on a valuation, or requiring a

valuation in the buy-sell agreement

mitigates risk

19

Shareholder Buyouts

• Not all companies have a buy-sell

agreement in place.

• Business valuations can provide a

good point to begin negotiations, and

smooth the process.

20

21

You’ve Decided to do a Business

Valuation.

What Happens Next?

Business Valuation Timeline

22

I.

•Project Scoping and Engagement Letter

•This typically takes a few days between initial discussions and the engagement letter

II.

•Information and Data Request

•This length of this step depends on how quickly client responds with requested information

III.

•Initial Modeling and industry research

•This portion should take 4 to 6 days to complete

IV.

•Follow up questions for client

•Questions arise during step III. Timing depends on client response time.

V.

•Finish model and finalize report

•A few days to a week depending on responses received in Step IV.

VI.

•Submit final report to client

•In total process typically takes 3 to 6 weeks.

Poll Question

23

So What is “Value?”

• “Value” expresses an economic concept. As such, it is never a fact but always an opinion of the worth of a property (asset)

• “Value” should always be qualified; e.g., “fair market value,” “liquidation value,” or “investment Value

24

Definition: Value(USPAP, paraphrased)

• Value is the monetary relationship between properties (assets) and those who buy, sell, or use those properties (assets)

25

The “Definitions of Value”

• Fair Market Value

• Fair Value

• Investment Value

• Intrinsic Value

• Liquidation Value

– Orderly

– Forced

26

Fair Market Value

• “The price at which the property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of relevant facts. Court decisions frequently state in addition that both the hypothetical buyer and seller are assumed to be able, as well as willing, to trade and to be well informed about the property and concerning the market for such property.” 27

Source: IRS Revenue Ruling 59-60

Fair Market Value

• "The price, expressed in terms of cash equivalents, at which property would change hands between a hypothetical willing and able buyer and a hypothetical willing and able seller, acting at arms length in an open and unrestricted market, when neither is under compulsion to buy or sell and when both have reasonable knowledge of the relevant facts."

28Source: The International Glossary of Business Valuation

Terms

Fair Value (Financial

Reporting) • "The price that would be received to

sell an asset or paid to transfer a

liability in an orderly transaction

between market participants at the

measurement date."

29

Source: ASC 820

Fair Value

• Can also be defined on a state-by-

state basis in divorce matters.

30

Investment Value

• "The value to a particular investor based on

individual requirements and

expectations."

31Source: The International Glossary of Business Valuation

Terms

Intrinsic Value

• "The value that an investor considers, on the basis of an evaluation or available facts, to be the "true" or "real" value that will become the market value when other investors reach the same conclusion. When the term applies to options, it is the difference between the exercise price or strike price of an option and the market value of the underlying security." 32

Source: The International Glossary of Business Valuation

Terms

Liquidation Value

• The most probable price that a

specified interest in real property is

likely to bring under extreme

compulsion to sell.

33

Source: Paraphrased from the Appraisal Institute, The Dictionary of Real Estate

Appraisal

34

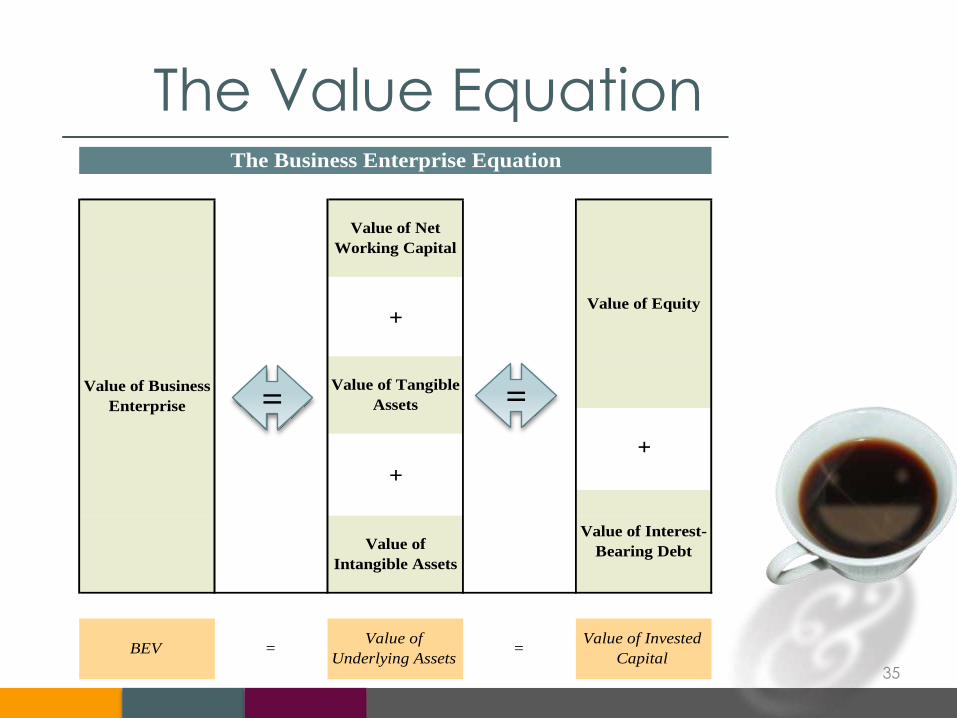

What (Exactly) is Being Valued Here?

The Value Equation

35

+

+

+

The Business Enterprise Equation

Value of Business

Enterprise

Value of Net

Working Capital

Value of Equity

Value of Tangible

Assets

Value of Interest-

Bearing DebtValue of

Intangible Assets

BEV =Value of

Underlying Assets=

Value of Invested

Capital

= =

Invested Capital

• Invested capital (sometimes

called business enterprise value)

is the value of the entire business

– Think of it like the price you would

receive if you were to sell the whole

business today

• Its equal to the value of the

equity in the business plus the

value of the debt. 36

Equity

• The value of the business available to

equity holders after debt service.

• Equity can be valued as a 100%

interest, or a fractional interest.

37

Levels of Value

• Business Enterprise Value (Total

Invested Capital)

• Equity Value, 100%

• Equity Value, Non-controlling

• Equity Value, Non-marketable

• Equity Value, non-controlling, non-

marketable

• Equity Value, non-controlling, non-

marketable, non-voting 38

Intangible Assets

• Intellectual Property (IP)

• Marketing Intangibles

• Contract-Based Intangibles

• Customer-Relationship-Based

Intangibles

• Artistic Intangibles

39

40

Does WHEN a Valuation is Done

Make a Difference?

41

Point in time Measurement• Value Changes over time

• “Valuation Date” is important

42

Some Valuations have Date Requirements or Deadlines

• Estate tax: date of death

• Financial Reporting: fiscal year end

43

Let too

much time

elapse…

… and

gathering

information can

be like an

archaeological

dig44

45

How Much Valuation Do I Need?

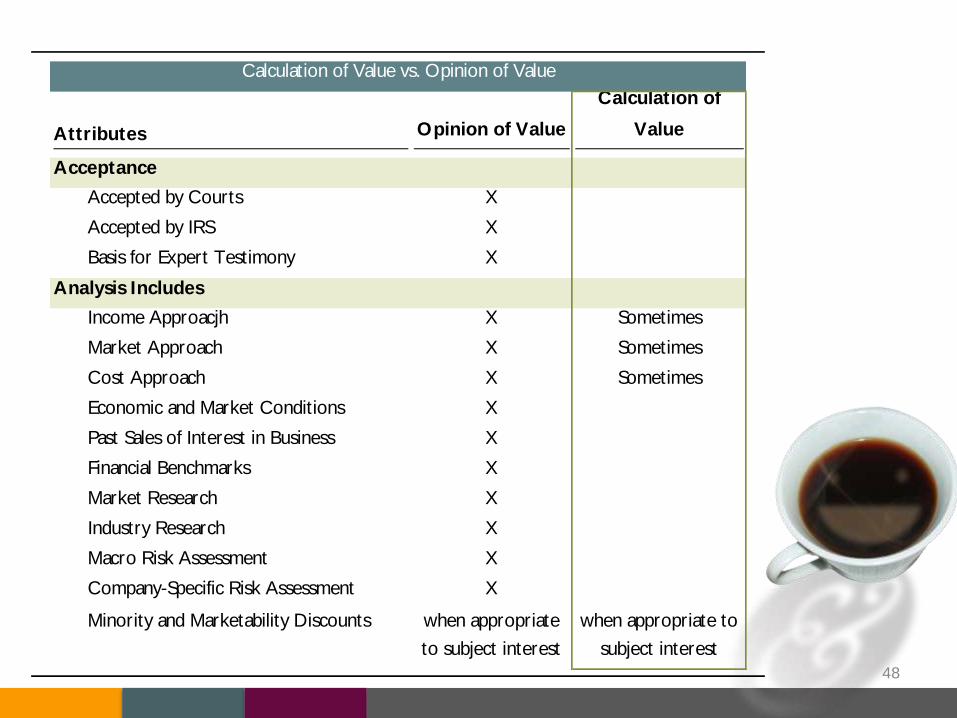

Opinion of Value (Appraisal)• a. An Appraisal is the act or process of determining the

value of a business, business ownership interest, security, or intangible asset.

• b. The objective of an appraisal is to express an unambiguous opinion as to the value of a business, business ownership interest, security or intangible asset which opinion is supported by all procedures that the appraiser deems to be relevant to the valuation.

• c. An appraisal has the following qualities:

• (1) Its conclusion of value is expressed as either a single dollar amount or a range

• (2) It considers all relevant information as of the appraisal date available to the appraiser at the time of performance of the valuation

• (3) The appraiser conducts appropriate procedures to collect and analyze all information expected to be relevant to the valuation

• (4) The valuation considers all conceptual approaches deemed to be relevant by the appraiser

46

Calculation of Value• Calculation engagement, as defined in the

Statement on Standards for Valuation Services (SSVS)

• A valuation analyst performs a calculation engagement when – (1) the valuation analyst and the client agree on the

valuation approaches and methods the valuation analyst will use and the extent of procedures the valuation analyst will perform in the process of calculating the value of a subject interest (these procedures will be more limited than those of a valuation engagement) and

– (2) the valuation analyst calculates the value in compliance with the agreement. The valuation analyst expresses the results of these procedures as a calculated value. The calculated value is expressed as a range or as a single amount.

• A calculation engagement does not include all of the procedures required for a valuation engagement and were a valuation engagement to be performed, the results may be different. 47

48

Attributes Opinion of Value

Calculation of

Value

Acceptance

Accepted by Courts X

Accepted by IRS X

Basis for Expert Testimony X

Analysis Includes

Income Approacjh X Sometimes

Market Approach X Sometimes

Cost Approach X Sometimes

Economic and Market Conditions X

Past Sales of Interest in Business X

Financial Benchmarks X

Market Research X

Industry Research X

Macro Risk Assessment X

Company-Specific Risk Assessment X

Minority and Marketability Discounts when appropriate

to subject interest

when appropriate to

subject interest

Calculation of Value vs. Opinion of Value

49

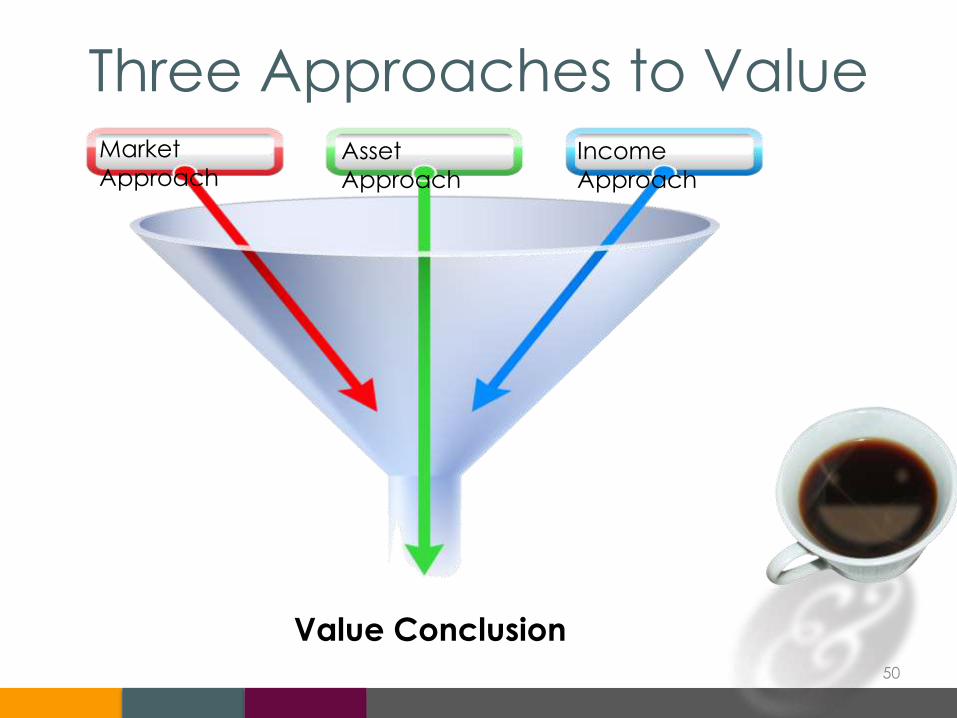

How Is Value

Determined?

Three Approaches to Value

50

Market

ApproachAsset

Approach

Income

Approach

Value Conclusion

Market Approach

51

Market Approach Theory

• The value of the company (or asset)

reflects the price at which

comparable companies (or assets) are

purchased under similar circumstance.

• Requires that comparable transactions

be available.

52

Market Approach - Methods

• Guideline publicly-traded

company method

– Based on similar and relevant

comparable entities

– Adjustments are often necessary to

make the comparables more similar

• Comparative transaction method

– Based on actual transactions of

similar entities

53

Public Company Method• Valuation relies on information

from comparable publicly

traded companies

• Should have several

“comparables”

• Adjustments may be necessary

to make them more

comparable or to normalize the

comps

• Sometimes it just doesn’t make

sense to use public companies 54

Comparative Transaction

Methods• Transaction

database

multiples

• Prior “arm’s-

length”

transactions

• Rules of thumb

55

Comparability?

• Public companies tend to be much

larger, have greater resources and

access to capital

– Public company multiples often need to

be adjusted

• Private companies – usually don’t

know terms of transaction, which can

impact price

56

Asset Approach

57

Asset Approach Theory

• The value of the company is estimated

as a function of the current cost to

purchase or replace all assets held

within the operating entity.

• It is based upon the principal of

substitution, which states that no

prudent investor would pay more for a

company (or asset) than the amount

to re-create or buy it.58

Asset Approach

• Useful for:

– Asset-intensive businesses

– Real estate holding

companies

– Entities that hold mostly

securities (or cash)

– Some contracting businesses

that bid for work

59

Asset Approach

• Often requires outside appraisals

• Must identify non-operating

assets like excess cash or

obsolete inventory

• Company may have intangible

assets that contribute to business

value that aren’t listed on the

books

60

Income Approach

61

Income Approach Theory

• Predicated upon the value of the future cash flows that an asset will generate over its remaining useful life.

• It involves the projection of the cash flows the company (or asset) is expected to generate.

• These cash flows are then converted into a present value equivalent through discounting.

62

Income Approach - Methods

• Discounted cash flow method

• Capitalization of earnings method

• Other methods exist, but are less

commonly used

63

Discounted Cash Flow

Method• Converts a stream of projected

earnings or other benefit stream into

present value by applying a discount

rate

• The earnings from each period are

discounted to present value and then

a “terminal” value is added to arrive at

the total value

64

65

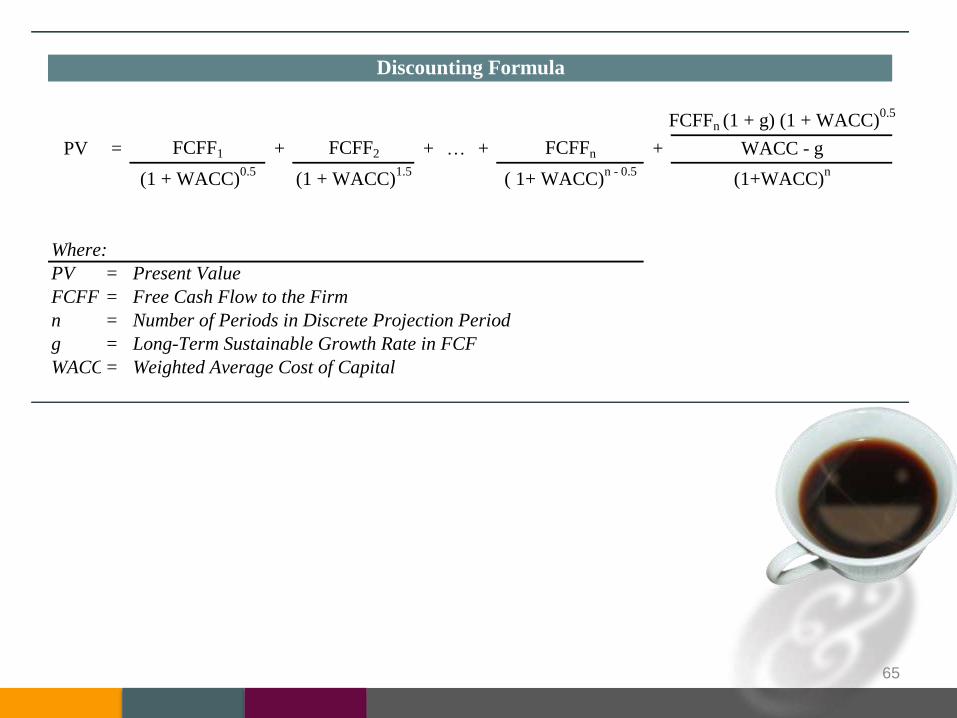

FCFFn (1 + g) (1 + WACC)0.5

PV = FCFF1 + FCFF2 + … + FCFFn + WACC - g

(1 + WACC)0.5

(1 + WACC)1.5

( 1+ WACC)n - 0.5

(1+WACC)n

Where:

PV = Present Value

FCFF = Free Cash Flow to the Firm

n = Number of Periods in Discrete Projection Period

g = Long-Term Sustainable Growth Rate in FCF

WACC= Weighted Average Cost of Capital

Discounting Formula

Present Value

66

Value today Years of saving

$1.00 1 year

$1.00 2 years

$1.00 3 years

Amount received Years till cash flow

$1.10 1 year

$1.21 2 years

$1.33 3 years

$1.00

$1.00

What will savings be worth?

Examples of Present Value

$1.21

$1.33

$1.10

Saving Today at 10%

Discounting Future Cash Flows at 10%

What is this cash flow worth today?

$1.00

Projected Earnings

• Predict future performance

based on analysis of historical

performance and current and

expected operating and industry

conditions

– Various tools are available to assist

the valuator in predicting future

performance

– Common sense and informed

judgment must be the deciding

factors67

What Is the Discount Rate?

• The rate of return, or cost of capital,

necessary to convert a monetary sum,

payable or receivable in the future,

into present value

68

How Do We Develop a

Discount Rate?

• Weighted Average Cost of Capital

(WACC)

– Capital Asset Pricing Model (CAPM)

• Published industry standards

69

Weighted Average Cost of

Capital

70

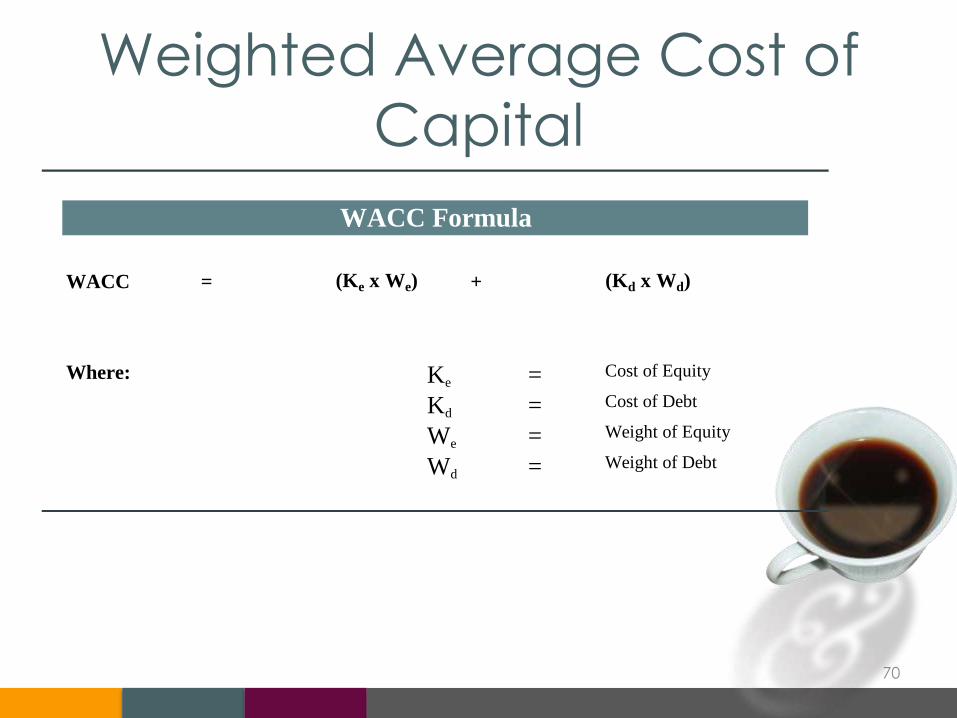

WACC = (Ke x We) + (Kd x Wd)

Where: Ke = Cost of Equity

Kd = Cost of Debt

We = Weight of Equity

Wd = Weight of Debt

WACC Formula

Cost of Equity

71

Cost of Equity = Rf + β(RPm) + RPs + RPu

Where: Rf =

β =

RPm =

RPs =

RPu =

(1) Modified Capital Asset Pricing Model

Risk premium for specific company

("unsystematic risk)

Risk premium for small size

Cost of Equity Formula (1)

Rate of Return for a risk-free security as of the

valuation date

Subject company's beta coefficient

Equity risk premium for the market

Cost of Equity

72

Cost of Equity = RPm + Rf + RPs + IP + RPu

Where: RPm =

Rf =

RPs =

IP =

RPu =

(1) Modified Capital Asset Pricing Model - Build-Up Method

Risk premium for specific company ("unsystematic risk")

Cost of Equity Formula (1)

Equity risk premium for the market

Rate of Return for a risk-free security as of the valuation

date

Risk premium for small size

Industry Risk Premium

Example of a Build-Up Method

to Developing the WACC

Risk-Free Rate (20-year Treasury-Bill) 2.5%

Equity Risk Premium 7.0%

Size Premium 3.5%

Company and Industry Specific Risk Premium 5.0%

Total Equity Discount Rate 18.0%

Less: Long-Term Growth 5.0%

Equity Capitalization Rate 13.0%

73

Capitalization of Earnings

Method• Like other income approach

methods, this is based on the principle that the value of the business can be estimated by the future benefits received from ownership of the business.

• Future benefits of ownership are assumed to be reliably predicted by past performance,

• Only appropriate for companies in stable growth phases

74

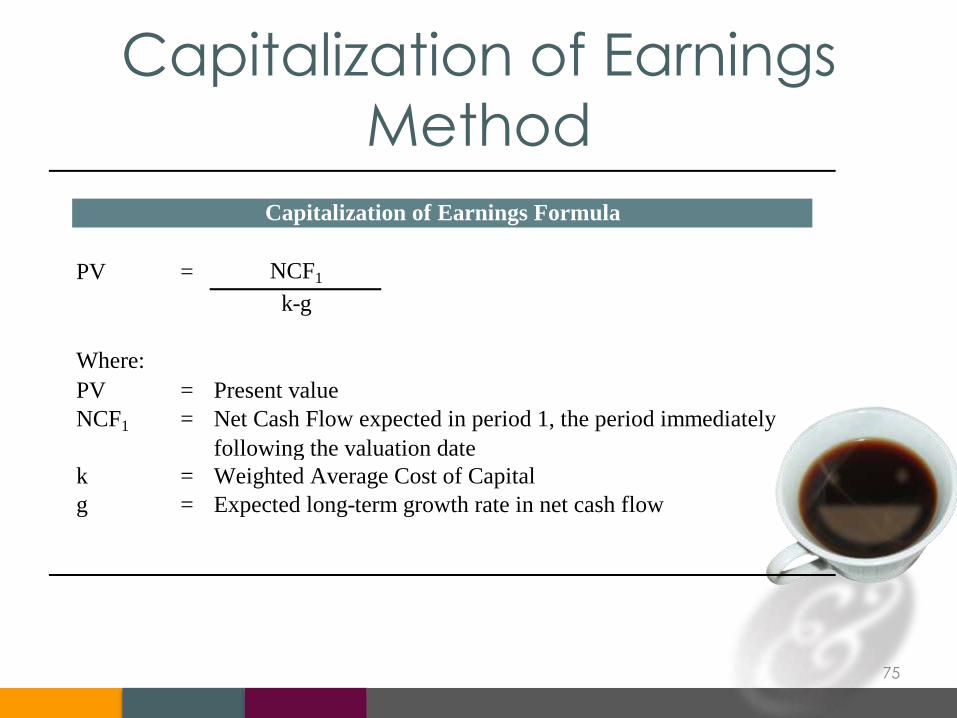

Capitalization of Earnings

Method

75

PV = NCF1

k-g

Where:

PV =

NCF1 =

k =

g =

Present value

Net Cash Flow expected in period 1, the period immediately

following the valuation date

Weighted Average Cost of Capital

Expected long-term growth rate in net cash flow

Capitalization of Earnings Formula

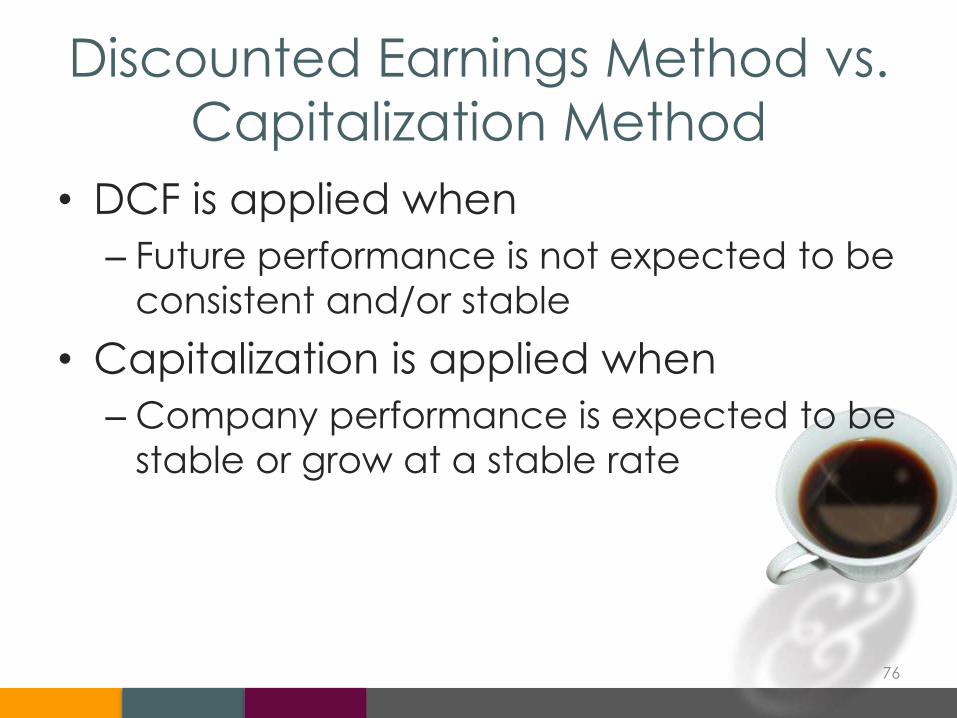

Discounted Earnings Method vs.

Capitalization Method

• DCF is applied when

– Future performance is not expected to be

consistent and/or stable

• Capitalization is applied when

– Company performance is expected to be

stable or grow at a stable rate

76

77

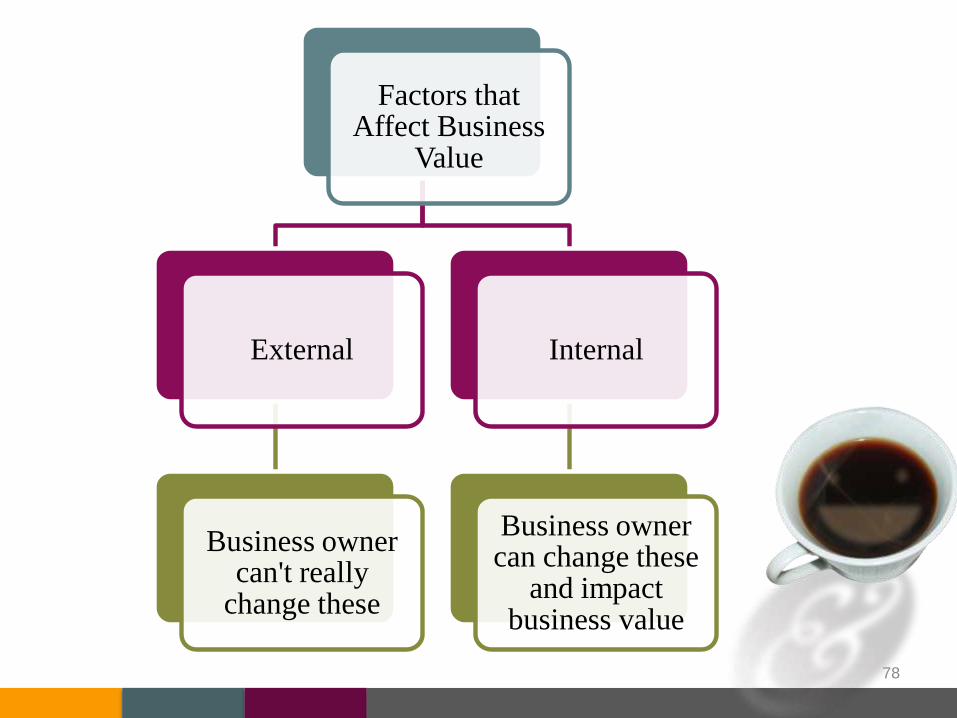

What Impacts Value?

78

Factors that Affect Business

Value

External

Business owner can't really

change these

Internal

Business owner can change these

and impact business value

External Factors That Impact

Company Value

Increase Value

• Expanding markets

• A dominant market

position

• Barriers to entry

• Expanding industry

• Expanding economy

• Shift in consumer

preference to

company product

Decrease Value

• Shrinking market

• Challenged market

share

• Lack of barriers to entry

• Contracting industry

• Contracting Economy

• Shift in consumer

preference away from

company product

79

Market Timing

80

SIC Code Industry Pre-Recession (1) Recession (2) Post-Recession (3)

5812 Eating Places 0.49 0.38 0.35

7231 Beauty Shops 0.49 0.40 0.36

7349 Building Cleaning and Maintenance Services 0.68 0.65 0.65

7389 Business Services, Not Elsewhere Classified 1.01 0.99 0.93

7538 General Automotive Repair 0.48 0.42 0.39

7991 Physical Fitness Facilities 0.66 0.76 0.64

8299 Schools and Education Services, NEC 1.07 0.66 0.94

Notes: (1) Pre-recession is defined as 1/1/03 through 11/31/07

(2) Recession is defined as 12/1/07 through 8/31/09

(3) Post-recession is defined as 9/1/09 through 12/1/14

Transactions Multiples Throughout the Business Cycle

MVIC to Sales

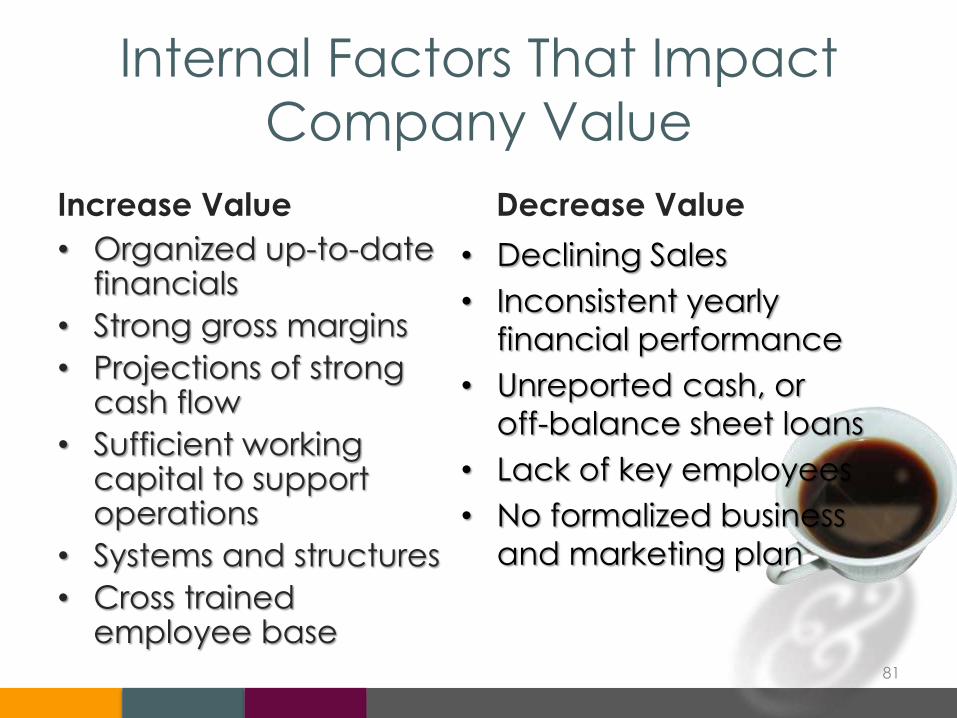

Internal Factors That Impact

Company Value

Increase Value

• Organized up-to-date financials

• Strong gross margins

• Projections of strong cash flow

• Sufficient working capital to support operations

• Systems and structures

• Cross trained employee base

Decrease Value

• Declining Sales

• Inconsistent yearly

financial performance

• Unreported cash, or

off-balance sheet loans

• Lack of key employees

• No formalized business

and marketing plan

81

DISCOUNTS FOR LACK OF CONTROL

AND MARKETABILITY

82

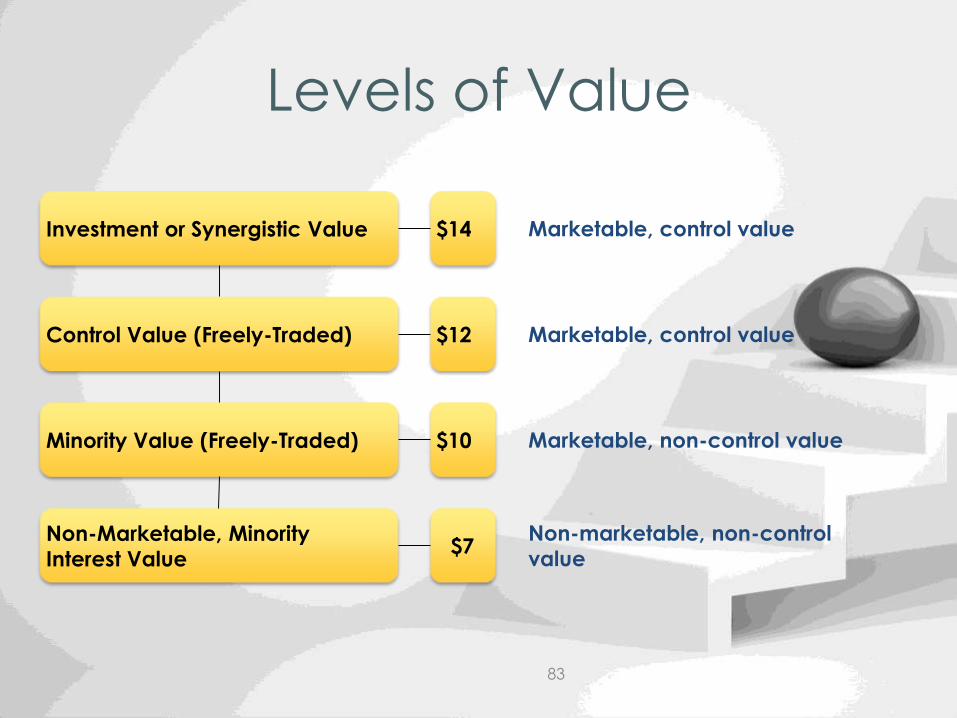

Levels of Value

83

Investment or Synergistic Value

Control Value (Freely-Traded)

Minority Value (Freely-Traded)

Non-Marketable, Minority

Interest Value

$14

$12

$10

$7

Marketable, control value

Marketable, control value

Marketable, non-control value

Non-marketable, non-control

value

Discounts & Premiums

• Discount for lack of control

• Premium for control

• Discount for lack of marketability

• Key person discount

• Depend on the interest to be valued

and the techniques used to establish

the value conclusion

84

Value of Control

• Control attributes

– Hire and fire

– Distribute earnings/declare dividends

– Buy and sell assets

– Enter into contracts

– Liquidate the business

– Set strategic objectives and goals

– Set compensation and performance

standards85

Lack of Control

• Lack of control in a closely held

company implies you are at the mercy

of the controlling owner(s)

• Substantial discounts may be

necessary to attract an investor to

purchase a minority interest in a closely

held company

86

Determination of

Discount/Premium

• Control premium studies

• Mergerstat Control Premium Studies

– Measures how much over the market price

is paid to gain control of a company

– Looks at the price of the stock before and

after the announcement of an acquisition or

merger

87

Marketability

• Ability to convert ownership interest to cash

• Time required to do so affects the level of marketability

• Other factors that affect marketability– Distributions of earnings

– Active market or industry roll-up

– Key person

– Number and profile of owners

– Restrictions on transfer of stock

88

Discount for Lack of

Marketability• From Pre-IPO studies

– Comparing the price of a company’s

stock before and after the

announcement of “going public”

• From Restricted Stock Studies

– Compare Letter Stock restricted from

trading for a certain time period to its

publicly traded counterpart

89

90

Marketable, control value 5,000,000$

Discount for lack of control 20% 1,000,000$

Marketable, minority value 4,000,000$

Discount for lack of marketability 30% 1,200,000$

Non-Marketable, minority value 2,800,000$

Example of Lack of Control and Lack of Marketablility Discounts

WHAT ARE THE ADJUSTMENTS TO MY FINANCIAL

DATA AND WHY HAVE YOU DONE THEM?

91

Adjustments to Financial

Statements• One objective of

financial statement

analysis is to

provide a financial

picture that can be

reliably used to

estimate future

performance.

92

Adjustments to Financial

Statements

• Historical financial statements may

need to be adjusted for certain items

that distort the picture of the true

operating performance of the

business.

93

Reasons for Financial

Adjustments• To develop a starting point

from which to predict future

earnings

• To present historical financial

information on a normalized

basis

• To adjust for accounting

practices that are a departure

from industry or GAAP

standards 94

Reasons for Financial

Adjustments• To facilitate comparison of a given

company to itself, to other companies

within the same industry, or to an

accepted industry standard.

• To compare the debt and/or capital

structure of the company to that of its

competition or peers

• To compare compensation with

industry norms95

What is Adjusted?

• Unusual items

• Nonrecurring items

• Extraordinary items (both unusual and nonrecurring)

• Non-operating items

• Items affected by changes in accounting principle

• Items that are not in conformance with GAAP

• Degree of ownership interest, including whether interest has control

96

Unusual Items

• Events or transactions that posses a

high degree of abnormality

• Unrelated to, or only incidentally

related to, the ordinary and typical

activities of the entity

97

Nonrecurring Items

• Events or transactions that are not

reasonably expected to recur in the

foreseeable future

98

Extraordinary items

• Events or transactions that are

distinguished by their unusual nature

and infrequency of occurrence

• Item must be both unusual and

nonrecurring to be classified as

extraordinary

99

Extraordinary items

• Events or transactions that are

distinguished by their unusual nature

and infrequency of occurrence

• Item must be both unusual and

nonrecurring to be classified as

extraordinary

100

Unusual, Nonrecurring, and

Extraordinary items

• Strikes and other types of work

stoppages

• Litigation expense or recoveries

101

Unusual, Nonrecurring, and

Extraordinary items

• Uninsured losses due to unforeseen

disasters like fire or flood

• One-time realization of revenues or

expenses due to nonrecurring

contracts

• Gain or loss on the sales of a business

unit or business assets

102

Unusual, Nonrecurring, and

Extraordinary items

• Discontinuation of operations

• Insurance proceeds received on the

life of a key person or from property or

casualty claim

103

Non-Operating Items

• Excess cash

• Marketable securities (in excess of

reasonable needs of the business)

• Real estate (if not used in business

operations)

• Private planes, entertainment, or sports

facilities

• Antiques, private collections, etc.

104

105

Changes in Accounting Principal

• A change in the method of pricing

inventory (e.g., LIFO to FIFO)

• A change in the method of depreciating

previously-recorded assets (e.g., straight-

line to MACRS)

Changes in Accounting Principal

• A change in the method of accounting for

long-term construction-type contracts

• A change to or from the full-cost method

of accounting in extractive industries

106

Nonconformance with

GAAP• Financial statements prepared on

a tax or cash accounting basis

• Unrecorded revenue in cash

business

• Inadequate bad debt reserve

107

Nonconformance with

GAAP• Understated amounts of

inventory, failure to write off

obsolete or slow moving

inventory, etc.

• Unrecorded liabilities such as

capital lease obligations,

workforce-related costs (wages,

sick/vacation pay), deferred

income taxes

• Capitalization/expense policies

for fixed assets and prepaid

expenses108

What Are Adjustments Based

On?• Industry ratios

• Market wage data

• Company historical data

109

GOODWILL?

110

What is Goodwill?

Two commonly used definitions of

goodwill- The bundle of all intangible assets of a

company

- The residual intangible value remaining

after all identifiable intangible assets have

been valued.

111

What Is Goodwill?

• Entity goodwill is the

goodwill that attaches to

the business enterprise.

112

What Is Goodwill?

• Personal Goodwill is the

goodwill that attaches to

the persona and

personal efforts of the

individual.

– Generally considered to

be difficult to transfer, if it

is transferable at all

113

When Does Goodwill Matter?

• Divorce Valuations

• Financial Reporting

114

Where Does Personal

Goodwill Arise?

• Traditionally, the issue of personal

goodwill arose almost exclusively in

the context of a professional practice

owner.

• The line gets “fuzzy” in the

commercial business arena

• Personal goodwill in a commercial

business might be more “key person

risk” than actual personal goodwill

• Look for special relationships with

customers or suppliers115

Separating Personal from

Entity• No generally accepted methodologies to

divide goodwill into personal and entity

components

– Methods to calculate personal goodwill can

depend on case or jurisdiction

– Multi-Attribute Utility Model

– With and Without Analysis

– Excess Earnings

116

Factors the Impact Personal

Goodwill

• Age and health of professional

• Earning power

• Reputation

• Comparative success

• Practice duration

• Marketability

• Types of Clients and Services

117

Factors that Impact Personal

Goodwill

• Location and Demographics

• Fees

• Source of New Clients

• Production

• Workforce

• Competition

• Non-Compete Agreements

118

DIVORCE-SPECIFIC VALUATION

CHALLENGES

119

Valuation isn’t Taught in Law

School• Judges don’t necessarily understand

valuation theory– Contradictory Case Law proves this out

– Valuation report needs to make valuation theory

and the intuition behind it crystal clear

120

Short Window in

which to Obtain

Info• Need to

anticipate all

future info

needs as part

of discovery

process

121

Short Window in which to Obtain

Info• Valuation Process Often Goes Like This:

1. Request info

2. Go through info and determine if additional info is

required

3. Request follow on info

4. Repeat step two/three as needed

5. Valuation and report writing

6. Last round of questions to cover issues that came up in

the valuation process/dot the i’s and cross the t’s.

7. Finalize and issue report

• Steps 3, 4, and 6 can be challenging

122

Short Window in which to Obtain

Info• If you miss key info, you are out of luck

123

Problematic Information Flow

• Spouse may be unwilling to

share info, or actively

attempting misdirection

124

Incentive to Hide Value

• Perceived advantage to

making business look less

valuable

• Postpone signing contracts

that guarantee business

income

• Defer follow-on rounds of

financing

• “Business Shift” Syndrome

125

“BS”• A sudden shift in

business performance around the time of the divorce filing.

• Business owner trying to make business appear less valuable.

• Could also be the result of macroeconomic or industry conditions. Careful assessment is necessary

126

In summary…

• Valuation is a process that leads to an opinion of value.

• There are many scenarios in which a valuation is needed or helpful.

• There are three approaches to value, but many valuation methods.

• You can value invested capital, equity, or individual assets.

• Certain situations have special considerations to be aware of.

127

Questions?

128

129

Theresa Zeidler-Shonat

Director of Valuation Services

Smith & Gesteland, LLP

608.828.3154

130