16

Growth Equities & Company Research Analyst: Thomas Jones [email protected] 020 7562 3371 Vatukoula Gold Mines* Buy at 0.91p with a 4.7p Target Price

Growth Equities & Company Research

Analyst: Thomas [email protected]

020 7562 3371

Vatukoula Gold Mines*Buy at 0.91p with a 4.7p Target Price

Page 2 of 12

Vatukoula Gold Mines Plc will be a clear winner from rising gold prices as its flagship asset is the eponymous Fijian mine which is already producing and operating profitably but which is set to enjoy a mammoth ramp up in production during the next 12 months. The Vatukoula mine has a JORC standard 5 million ounce resource and while the AIM listed company is currently producing at a rate of 48,000 ounces of gold per annum, it is targeting a production rate of 117,000 ounces per annum within the next 24 months. The company also owns a portfolio of legacy assets in Brazil, Sierra Leone and Lesotho from which value may be realised and has a positive net cash balance which is set to grow as the flagship operation is increasingly cash generative.

The genesis of the present quoted company was in August 2000 with the formation of River Diamonds. This fledgling diamond and gold explorer listed on AIM on August 26th 2005. However the management team recognised in early 2008 that investor appetite for pure exploration plays was waning and between June and December 2008 it agreed a transformational deal which saw Viso Gero International, the owner of the Vatukoula Mine in Fiji, reversed into the AIM company. That deal completed in August 2008. The mine, which has produced over 7 million ounces of gold during its working life, is now the sole focus of operation and in recognition of that the company changed its name to Vatukoula Gold Mines in August 2008.

While the Vatukoula gold mine contains a proven resource and is profitable its operation is not without challenges. An almost exclusive reliance on self-generated power means the company faces high fixed costs from diesel – recent movements in the oil price therefore work in its favour. An inherited, insufficient fleet of trucks and haulage vehicles provided an immediate restriction to production, while the carrying capacity of its 3 shafts followed by the processing capacity of its plant has presented the company with subsequent production bottlenecks. However, Vatukoula is confident these obstacles can be overcome and the cash it is generating is allowing it to upgrade the equipment on site.

Vatukoula Gold Mines* – Buy at 0.91p with a 4.7p Target Price

Analyst: Thomas [email protected]

020 7562 337113th January 2009

Key Data

EPIC VGM

Share Price 0.91p

Spread 0.85p – 0.97p

Total no of shares 1,902,371,072

Market Cap £17.4 million

12 Month Range 0.88p – 4.75p

Net Cash £2.2 million

NMS 30,000

Market AIM

Websitewww.

vatukoulagoldmines.com

Sector Mining

ContactDavid Paxton, CEOTel: +44 (0)20 7016

7861

Our valuation of Vatukoula Plc is derived from an estimated value of the company’s net cash position and the Vatukoula gold mine itself. The company’s $3.8 million in net cash or cash equivalents has been valued at par. Our valuation of the gold mine is based on the assumption that the company will achieve a production ramp up to 117,000 ounces of gold per annum in the 2011 financial year and will operate with a long term cost per ounce of $525, at an average gold price of $775 per ounce. We assume that the company will secure $30 million of debt funding in 2010 in order to accelerate the ramp up in production and will bear a Fijian tax rate of 31%, a government royalty of 3% and export tax of 6% (waived for 5 years). Our DCF valuation on the mine uses a 10% discount rate, a USD/GBP exchange rate of $1.70, a FJD/USD of F$1.75 and a secondary risk weighting of 5% to discount for country specific risk. Our sum of the parts valuation generates a target share price of 4.7p.

However there is real potential to expand production and major upside may also come from higher gold prices (and we note that gold is currently trading at $820 oz and we expect it to reach $1250 during 2009). A higher gold output could be achievable through the construction of an additional shaft and upgrade of the processing plant. Assuming such work is competed at a cost of $200 million, output could be doubled to 230,000 ounces of gold per annum and consequently average operating costs lowered to $450 per ounce. This would see our valuation jumps to 6.8p under the same remaining assumptions. On the other hand a higher gold price of $900 per ounce would see our base case valuation climb to 7.4p per share and expansion case up to 11.2p. Gold is already trading at $820 and many commentators expect it to move sharply higher - with Vatukoula clearly a geared play on such a movement.

At 0.91p our stance is buy.

Page 3 of 12

Key Data

EPIC VGM

Share Price 0.91p

Spread 0.85p – 0.97p

Total no of shares 1,902,371,072

Market Cap £17.4 million

12 Month Range 0.88p – 4.75p

Net Cash £2.2 million

NMS 30,000

Market AIM

Websitewww.

vatukoulagoldmines.com

Sector Mining

ContactDavid Paxton, CEOTel: +44 (0)20 7016

7861

Forecast Table:

Year to 31st August

Sales (£ Million)

Pre-tax Profit (£ Million)

Earnings Per Share

(p)

Price Earnings

Ratio

Dividends Per Share

(p)

Dividend Yield (%)

2007A 0 (0.98) (0.05) NA 0 0.02008A 3.8 (4.1) (0.30) NA 0 0.02009E 24 3 0.15 6.1 0 0.02010E 40 8 0.29 3.1 0 0.0

*Vatukoula is a corporate client of Bishopsgate Communications, which is owned by RSH, the owner of GE&CR. RSH also owns shares in Vatukoula.

Page 4 of 16

Background

Vatukoula Gold Mines Plc began life as River Diamonds Plc which was formed in November 2000 as an explorer and developer of Brazilian diamond interests. River Diamonds listed on AIM in August 2004 as the holding company for 57,000 hectares of exploration licences in the Mato Grosso region of Brazil.

Having entered into a joint venture with Olympus Development Company Ltd in June 2005 for the Panguma Diamond Project in Sierra Leone, River acquired the remaining 49% interest in December 2006. The joint venture had sampled, mapped and drilled the kimberlite dykes at Panguma with total mini bulk sampling having recovered 6.71 carats from 12.5 tonnes.

River purchased a 4.8% interest in the Lesotho Diamond Corporation Plc, holding company for the Kao Diamond Project, in April 2007. In July 2007, River acquired its first interest in the Vatukoula gold mine by way of a 12.5% interest in Viso Gero International - 94% owner of Westech Gold Pty Ltd whose subsidiary owned the Vatukoula (nee Emperor) gold mine. In August Westech negotiated several key tax concessions with the Fijian government regarding the Vatukoula gold mine, while in October 2007 River increased its stake in Viso Gero to 20%. Finally in December 2007 River announced that it would acquire the remaining 80% of Visio under the condition that Visio acquire the remaining 6% interest in Westech before River’s acquisition. Four months later on 1st April 2008 River completed the acquisition of 100% ownership in Viso for A$2.1 million in cash and 477,633,333 in shares (at 6p per share), valuing the 100% stake at £33,811,000. To more accurately reflect its operational focus River Diamonds Plc changed its name to Vatukoula Gold Mines Plc effective 20th August 2008.

The Vatukoula mine is an underground gold mine located within the Tavua Basin, which itself is within the Tavua volcano. The volcano is in the northern part of the Fijian island of Viti Levu – one of the two main islands in the country. Gold has been produced from Vatukoula since 1933 and has switched between an open-pit and underground mine as the ore body and technology dictated. Approximately 7.1 million ounces of gold at an average grade of 11 g/t and over 2 million ounces of silver has been extracted during the mine’s life from the treatment of around 22.5 million tonnes of ore. At its peak between 1996 and 2005, the mine produced an average 121,059 ounces of gold per annum from an average of 563,242 tonnes of ore per annum.

In December 2008 the company reported its first operating profit at the Vatukoula gold mine since full control was achieved in March. The F$2.74 million (approximately £1 million) in operating profit was posted in the month of October and, although boosted by an exchange rate gain, provides a launching pad for the company which is steadily progressing towards full production.

Page 5 of 16

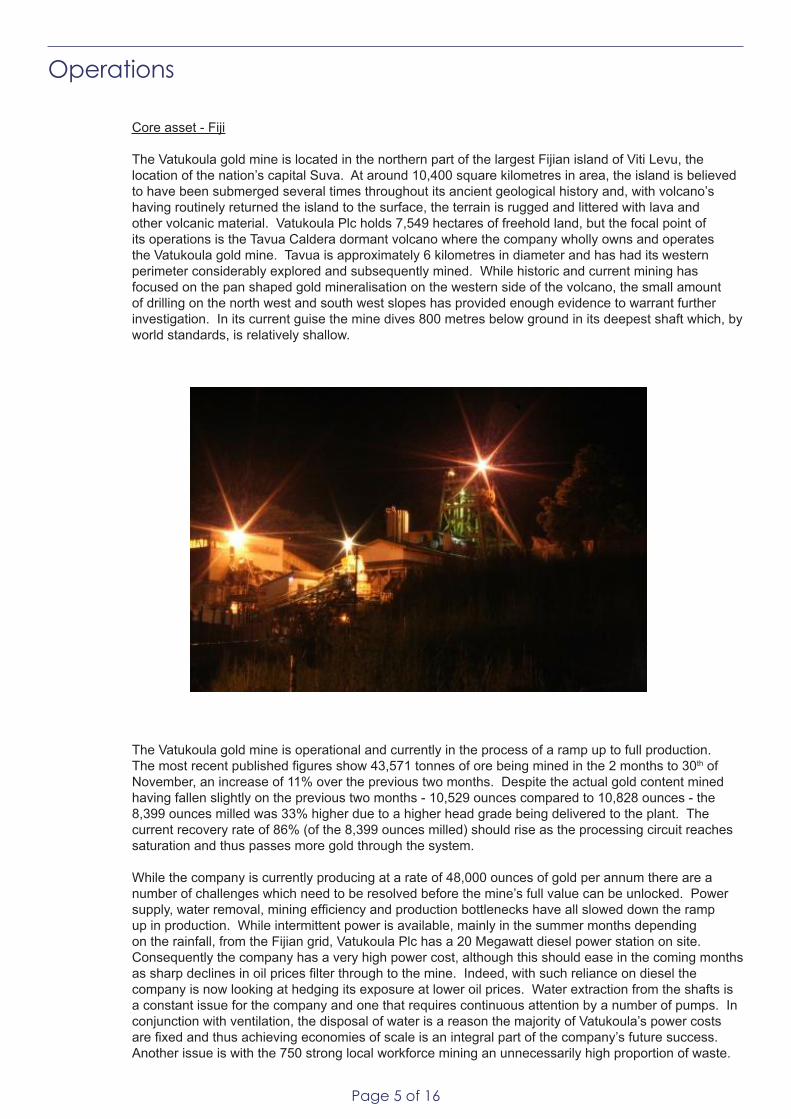

Operations

Core asset - Fiji

The Vatukoula gold mine is located in the northern part of the largest Fijian island of Viti Levu, the location of the nation’s capital Suva. At around 10,400 square kilometres in area, the island is believed to have been submerged several times throughout its ancient geological history and, with volcano’s having routinely returned the island to the surface, the terrain is rugged and littered with lava and other volcanic material. Vatukoula Plc holds 7,549 hectares of freehold land, but the focal point of its operations is the Tavua Caldera dormant volcano where the company wholly owns and operates the Vatukoula gold mine. Tavua is approximately 6 kilometres in diameter and has had its western perimeter considerably explored and subsequently mined. While historic and current mining has focused on the pan shaped gold mineralisation on the western side of the volcano, the small amount of drilling on the north west and south west slopes has provided enough evidence to warrant further investigation. In its current guise the mine dives 800 metres below ground in its deepest shaft which, by world standards, is relatively shallow.

The Vatukoula gold mine is operational and currently in the process of a ramp up to full production. The most recent published figures show 43,571 tonnes of ore being mined in the 2 months to 30th of November, an increase of 11% over the previous two months. Despite the actual gold content mined having fallen slightly on the previous two months - 10,529 ounces compared to 10,828 ounces - the 8,399 ounces milled was 33% higher due to a higher head grade being delivered to the plant. The current recovery rate of 86% (of the 8,399 ounces milled) should rise as the processing circuit reaches saturation and thus passes more gold through the system.

While the company is currently producing at a rate of 48,000 ounces of gold per annum there are a number of challenges which need to be resolved before the mine’s full value can be unlocked. Power supply, water removal, mining efficiency and production bottlenecks have all slowed down the ramp up in production. While intermittent power is available, mainly in the summer months depending on the rainfall, from the Fijian grid, Vatukoula Plc has a 20 Megawatt diesel power station on site. Consequently the company has a very high power cost, although this should ease in the coming months as sharp declines in oil prices filter through to the mine. Indeed, with such reliance on diesel the company is now looking at hedging its exposure at lower oil prices. Water extraction from the shafts is a constant issue for the company and one that requires continuous attention by a number of pumps. In conjunction with ventilation, the disposal of water is a reason the majority of Vatukoula’s power costs are fixed and thus achieving economies of scale is an integral part of the company’s future success. Another issue is with the 750 strong local workforce mining an unnecessarily high proportion of waste.

Page 6 of 16

While not immediately apparent as a major issue, the downstream effects soon add up in terms of the time spent and money consumed mining, transporting and milling the additional waste. The company is very aware of this issue and is implementing a number of measures to increase its mining. The final significant challenge is with current and predicted bottlenecks in the system. Currently the inherited mining fleet (diggers and haulers) is not of sufficient size and quality to supply the shafts and processing plant with the targeted annual 117,000 ounces of gold (approximately 585,000 tonnes of ore per annum). While fleet refurbishments and additions are currently being made, at 117,000 ounces per annum the 3 operating mine shafts and one decline become a constraint. Beyond 700,000 tonnes of ore per annum the processing plant reaches its limit. Vatukoula plc is targeting 117,000 ounces of gold per annum in the next 12-24 months and will then start investigating the addition of a mine shaft and plant expansion programme.

A competent person’s report on the Vatukoula gold mine quantified a JORC compliant reserve and resource of 16.84 million tonnes at an average grade of 9.49 grams of gold per tonne (g/t) for a total contained metal estimate of 5.15 million gold ounces. Of this resource, 2.26 million tonnes at 11.41 g/t are in the reserve category for 0.83 million ounces of contained gold, while one of the tailings dams contains 5.18 million tonnes at a grade of 1.47 g/t for 250,000 ounces of contained gold.

Page 7 of 16

Despite having a mine life of around 40 years at the targeted production rate, Vatukoula intends to conduct a step-out drill programme at previous drill locations to the north and south of the current mine site. While cash constrained at the moment, as the current operation begins to consistently produce positive cash flows the company will look to commence the drill programme to better define and add to the current mineralisation.

Vatukoula Plc has not hedged any of its gold output and is thus positioned to benefit from any future strengthening in the commodity’s price. The company’s entire current output is sold directly to the Perth Mint in Australia which collects the gold directly from the mine on a weekly basis and pays the prevailing spot price 5 days later.

Satellite assets – Brazil, Sierra Leone, Lesotho

Located in the under-explored Tapajos province in Brazil, the 100% owned Rio Novo is comprised of 4 claims covering 30,000 hectares of gold prospective land in close proximity to the productive Palito gold mine. Having conducted a geological review of the area in 2006, the subsequent competent person’s report recommended the acquisition of satellite images, access to Rio Tinto’s exploration results of the area and eventually a full desk study by an exploration geologist to identify an exploration plan. As with Panguma, because of the company’s focus in Fiji, Rio Novo has been mothballed and an adjacent licensee has been found to rent the mine’s equipment.

The 100% owned Panguma project in Sierra Leone is seeking diamonds in a 5,400 hectare licence area adjacent to the prolific Tongo Dyke Field (produced $2.75 billion worth of diamonds in its history). In its previous guise as River Diamonds, the company conducted a detailed exploration programme in 2006 with surveying, geological mapping, mini-bulk samples, core drilling and geochemical soil sampling. The Company reapplied for the exploration license in early 2008, but as yet has not received any confirmation of its renewal. As a conservative measure the Company is assuming that this license will not be renewed and has written off its investment in the project.

The final piece in the company’s portfolio is a 0.46% interest in Global Diamond Resources Plc, an African focused unlisted diamond company with the 93% owned Kao diamond project in Lesotho its core asset. Kao has an estimated diamond resource of 10.19 million carats from its kimberlite deposit and Vatukoula hopes that value can be unlocked via a trade sale or flotation of Global Diamond Resources although in the current climate this has to be viewed as a medium term aspiration.

Page 8 of 16

Strategy

Having achieved two of its near-term goals of bringing the Vatukoula gold mine back into production and profitability, the company is now looking to maintain that profitability while increasing output to its current target of 117,000 ounces of gold per annum and exploring the surrounding area. Target production is expected to be achieved once the current fleet of loaders and haul trucks are refurbished and added to.

Once target production is achieved, Vatukoula has a number of initiatives planned. More efficient mining, finding a cheaper power source, increasing production capacity and expanding the resource are challenges that upon being overcome will take the mine to a new level of operation and profitability.

The company’s focus is in Fiji, its Brazilian project is mothballed and awaiting funding. Value from the non-core assets will be realised in due course via disposals. Vatukoula is strictly a one project company and will explore the options of expanding the current mine, tap into other underground mines with its labour cost advantage or look at paying dividends once it is generating sufficient free cash flow.

Financially the company’s strategy has been to limit its funding to equity capital raisings which has served the company well and avoided the cash drain of debt repayment obligations. However with its gold mine now producing cash flows, debt repayments are more manageable and thus debt is likely to form some part of the company’s forward funding strategy.

Having avoided hedging either its gold output or diesel costs thus far, the company is well aware of such issues. With both commodities price potential arguably more skewed on the upside, Vatukoula is considering diesel hedging, but it wishes to remain exposed to the gold price since it views the outlook as bullish – a view shared by GE&CR.

Page 9 of 16

SWOT Analysis

Strengths

Resource size – for a junior mining company, a 5 million ounce plus gold JORC compliant resource is a major strength. At a gold price of $750 an ounce, the in-ground value is $3.75 billion which, for a company currently capitalised around £20 million, represents immense upside.

Production status / Cash flow generative – the Vatukoula gold mine is operational and productive with a current recovered gold rate of 48,000 ounces per annum. With gold one of the few commodities holding its value and with weekly cash receipts from its current client, the Perth Mint, Vatukoula is well positioned to survive and even prosper in the current economic environment.

Debt free – having acquired its assets through the sole funding method of equity issues, Vatukoula has avoided the cash drain of interest payments. While it is likely future fund raisings may incorporate a debt component, cash flows from the gold mine should be more than sufficient to cover repayment obligations and thus be entirely manageable and preserve shareholder value.

Low cost workforce – while we expect the current enthusiastic underground workforce’s mining of an unnecessary amount of waste to improve over time, the employees are cheap compared to many of its peers. This cost advantage offsets some of its high power costs to bring Vatukoula in line with other underground mine’s cost profile.

Weaknesses

Reliance on Diesel – to ensure a sufficient and reliable power supply, the Vatukoula gold mine is predominantly powered by a diesel power plant on site. While some power is available from the grid, Fiji lacks the critical mass necessary to allow a large electrical consumer to draw its requirements entirely from the domestic supply. While oil prices have fallen sharply in recent weeks there is no guarantee that this will not be reversed and, unless a hedging programme is implemented (the company is looking into this), Vatukoula Plc is at the mercy of volatile spot prices.

High fixed costs – underground mines are notoriously high consumers of power and with a large permanent workforce, onsite assay labs, workshops, staff housing and sports facilities, Vatukoula Plc’s operating costs have a high fixed component. The opportunity here is that as output ramps up average operating costs will fall sharply, so it is imperative that the company rapidly increases its gold production.

Opportunities

Increased mining efficiency – the current local workforce, while well qualified to carry out their roles, continue to mine a large amount of waste. With the not insignificant costs of transferring this dead weight to the surface, there is much to be gained from increased mining efficiency.

Extra shaft / upgraded pant – Vatukoula admits that a company with over 5 million ounces of gold beneath its feet should, at full production, be producing more than its current limit of 117,000 ounces of gold per annum and it is the belief of the directors that output could be increased to 136,000 oz per annum. Truck and hauler issues aside (these should be resolved shortly), the transfer of ore to the surface and subsequent processing are limited by the existing infrastructure. An additional shaft and upgraded processing plant would see output capacity more than double and should be considered once the current output target is achieved.

Alternative power source – moving away from diesel to a cheaper power source would represent a major cost saving for the company. While options are limited by the small island nation location, management is keen to lower power costs and as such will continue to evaluate its options.

Expanded / upgraded resource – while the current 5 million ounce gold resource is good for around 40 years of production at the target rate of 117,000 ounces per annum, the company’s licence covers the entire Tavua Caldera volcano so further mineralisation finds are highly possible. The currently defined

Page 10 of 16

ore body is situated on the western side of the volcano, and with interesting targets to both the north and south of the current site, the company is optimistic of an increased resource.

Threats

Gold price – while we believe that a dramatic easing of monetary and fiscal policy across the globe will push the gold price sharply higher during 2009 and 2010, with a high fixed cost base, Vatukoula would be vulnerable if the gold price fell sharply.

Diesel price – as the mine’s dominant power source, diesel is an integral part of Vatukoula’s operation. The company is currently looking at hedging at least some of its diesel exposure, and while this will offer some certainty, is not without its own costs and risks.

Fund raising – while the company is currently debt free and revenue generating, working capital requirements are likely to necessitate some external funding. The need for a new tailings dam is clear, and while gold recoveries from one of the current dams may produce some payback, the company cannot fully internally fund this estimated $20 million cost. With debt funding hard to come by and expensive when it does, the company may have to look for shareholder support or a more creative solution such as a royalty agreement.

Country risk – since its independence from Britain in 1970, Fiji has been the subject of periodic social unrest as hostilities between the Indo-Fijians and the ethnic-Fijians come to the boil. Two military coups in 1987, a civilian-led coup in 2000 and another military coup in 2006 have marred the political landscape and led to the current military dominated regime. While Vatukoula has a good relationship with the current government, the country’s social tensions remain.

Shareholders

Of the 1,902,371,072 Vatukoula shares in issue, the following shareholders each hold over 3% of the issued capital.

Name Shares Percentage (%)

Pershing Nominees Limited 329,851,066 17.34%

Templar Minerals Limited 285,000,000 14.98%

Laytons Trustee Company Limited 143,290,000 7.50%Viso Gero Global Ink 121,290,000 6.97%Euroclear Nominees Limited 101,616,154 6.65%State Street Nominees Limited 95,000,000 4.99%

In addition, Vatukoula has 194.7 million options on issue at exercise prices of between 2p and 6p and dates from August 2010 to November 2013.

Page 11 of 16

Management / Directors

Chief Executive – David Paxton, age 54. A professional engineer with a career of over 35 years in the mining industry, Paxton brings important capital raising and market knowledge from his previous position as a mining analyst at Hichens Harrison & Co. Having been appointed to his current position in November 2008, Paxton is a well respected industry professional as demonstrated by his current directorships with India Minerals Plc, Adit Investment Ltd, Sahara Mines Ltd, Ortac Resources Plc, Far North Platinum Ltd and the Mining and Dining Club Ltd.

Executive Chairman – Ian Colin Orr-Ewing, age 66. Having graduated with a geography degree from Oxford University, Orr-Ewing entered the world of finance as an investment manager for the Shell Pension Fund after qualifying as a Certified Accountant. Orr-Ewing has gone on to accumulate over 35 years of natural resource industry experience including positions with many corporations in the North Sea, Libya, Nigeria and Algeria. An experienced board member having held directorships with UK and Canadian oil companies and Irish and Canadian mining companies, Orr-Ewing currently advises a leading fund manager on its natural resources portfolio.

Executive Director – David Anthony Lenigas, age 47. A mining engineering graduate Lenigas is currently executive chairman of Pan-African investment company Lonrho Plc, Leni Gas & Oil Plc, Lonrho Mining Plc and Lonzim Plc. Also a director of Global Coal Management Plc and Templar Minerals Ltd, Lenigas is very familiar with the Vatukoula gold mine having held the position of managing director of the Western Mining / Emperor Mine’s joint venture that previously ran the project.

Finance Director - Kiran Caldas Morzaria, age 34. Educated at the Camborne School of Mines (B.Eng) and CASS Business School (MBA), Morzaria spent his early resources career in exploration, mining and civil engineering. Finance director of Vatukoula Plc since 2004, Morzaria is well experienced in corporate acquisitions, joint venture agreements, valuations, qualified person’s reports and due diligence. With over 12 years of diamond and gold industry experience, Morzaria is also a non-executive director of Immersion Technologies International Plc and Hot Tuna (International) Plc.

Non-executive Director - John Ian Stalker, age 55. Having held the enviable CEO position of Uramin Inc at the time of the Areva takeover, Stalker could have retired two years ago, but instead decided to lend his valuable expertise to Vatukoula. Prior to Uramin the chemical engineering graduate worked for Gold Fields Ltd, Lycopodium, Ashanti Goldfields Company Ltd, Caledonia Mining Corporation, AGC Ltd and Zambia Consolidated Copper Mines Ltd.

Non-executive Director - Neil Lindsey Herbert, age 41. Another Uramin graduate, Herbert was Finance Director of the company at the time of the Areva takeover in 2007. As a fellow of the Association of Chartered Accountants and having worked for PricewaterhouseCoopers, Herbert is an industry recognised finance expert. This experience has been developed over the years with finance directorships at Galahad Gold Plc, International Molybdenum Plc, Kalahari Diamond Resources Plc and HPD Exploration Plc, as Chief Financial Officer at Brancote Holdings Plc and Group Financial Controller of Antofagasta Plc. Herbert is also a non-executive director of Templar Minerals Ltd.

Page 12 of 16

Peer Group Comparison

Operating in a small Pacific Island nation brings its own opportunities and challenges, and although there are no directly comparable listed companies to Vatukoula Plc, we have selected what we regard as seven of its closest peers (either in terms of market capitalisation, recognised gold resource or annual gold production) to produce a peer comparison. Our peer group’s data has been taken from the companies most recent published records to the 5th of January 2009 and although it should be noted that such an exercise is highly subjective - with the figures used representing only a snapshot at a particular moment in time and the nuisances of each company meaning a true comparison is not possible – it does help put Vatukoula’s valuation into some sort of context.

While Vatukoula is the smallest company of our selection in terms of market capitalisation, its gold resource of 5.15 million ounces places it clearly in third place in that category and, although its current annual gold production is at it the lower end of its peer group, the company’s targeted output of 117,000 ounces per annum would see the company move into forth position in this category.

Adjusting each company’s market capitalisation for net cash and evaluating on a resource and production basis provides a clearer evaluation of the relative value the market is currently attributing. This process shows Vatukoula as the second cheapest in terms of resource ounces and third on production ounces. However, at its targeted rate of 117,000 ounces per annum, Vatukoula’s adjusted market capitalisation per production ounce falls from £477 to £196 which would also place it second on this metric – again behind only Russian focussed Highland Gold. Perhaps Vatukoula’s closest peer is Aurizon Mines who, with a single operational underground mine and a 3.9 million ounce resource, is currently valued at £302 million.

Page 13 of 16

Our valuation of Vatukoula Plc is derived from the company’s net cash position and the Vatukoula gold mine. With zero debt, we have estimated the company’s net cash position at $3.8 million, while the assumptions to our discounted cash flow model of the Vatukoula gold mine begin with production where 60,000 ounces of gold are sold in FY2009 (31st August year end), 100,000 ounces in FY2010 and full production of 117,000 ounces is achieved in FY2011. In our base case, production of 117,000 ounces of gold per annum is assumed for the life of the mine which, with 5 million ounces of estimated reserves, represents around 40 years. Like other underground mines, Vatukoula’s fixed costs are substantial and thus achieving the economies of scale necessary to reduce operating costs to a sustainable level is critical. As such we have assumed a cost per ounce of $525 based on our above production assumptions which if bettered would reduce average operating costs per ounce further. Our base case assumption is that the company can realise an average gold price of $775 per ounce over the mine’s life. Equipment upgrades, general working capital requirements and the $20 million dollar cost of a new tailings dam have prompted us to assume $30 million is raised through a debt issue at 12% per annum over 4 years for the 2010 financial year. While the company is subject to a Fijian tax rate of 31%, we have assumed losses carried forward mean Vatukoula Plc don’t pay tax until the 2015 financial year. With a government royalty of 3% and export tax of 6% (waived for 5 years) payable on revenues and using a discount rate of 10% per annum, we derive a net present value of $157 million. Using a USD/GBP exchange rate of $1.70, a FJD/USD of F$1.75 and applying a secondary risk weighting of 5% to incorporate such things as exchange rate and political risk, we derive a target share price of 4.7p per share.

Upside potential to the project is immense and includes a higher annual gold output, a reduction in waste mined, a cheaper power source and an increased resource from the rest of the volcano within the company’s licence area. While the latter 3 items are difficult to predict, a higher gold output would be achievable through an additional shaft and upgrade of the processing plant. Assuming such work is completed at a cost of $200 million, output could be doubled to 230,000 ounces of gold per annum and average operating costs consequently lowered to $450 per ounce. This sees our valuation jump to 6.8p under the same remaining assumptions. On the other hand a higher gold price of $900 per ounce would see our base case valuation climb to 7.4p per share and expansion case up to 11.2p. Gold is already trading at $820 and many commentators expect it to move sharply higher – with Vatukoula clearly a geared play on such a movement. We also note that Vatukoula looks undervalued in relation to peer group companies and with profit beginning to flow, cash on hand, a proven resource and increasing output, our stance at 0.91p is buy. Operational challenges do remain but an initial target of 4.7p looks eminently achievable – with clear potential for more than 11.2p should, for example, the gold price increase as many commentators expect. Buy.

Valuation

Forecast Table:

Year to 31st August

Sales (£ Million)

Pre-tax Profit (£ Million)

Earnings Per Share

(p)

Price Earnings

Ratio

Dividends Per Share

(p)

Dividend Yield (%)

2007A 0 (0.98) (0.05) NA 0 0.02008A 3.8 (4.1) (0.30) NA 0 0.02009E 24 3 0.15 6.1 0 0.02010E 40 8 0.29 3.1 0 0.0

*Vatukoula is a corporate client of Bishopsgate Communications, which is owned by RSH, the owner of GE&CR. RSH also owns shares in Vatukoula.

Page 14 of 16

This research note cannot be regarded as impartial as GE&CR has been commissioned to produce it by Vatukoula Gold Mines*

The information in this document has been obtained from sources believed to be reliable, but cannot be guaranteed. Growth Equities & Company Research is owned by t1ps.com Ltd which is commissioned by companies to produce re-search material under the Growth Equities & Company label. However the estimates and content of the reports are, in all cases, those of t1ps.com Ltd not of the companies concerned.

t1ps.com Limited is regulated by the Financial Services Authority .This research report is for general guidance only and t1ps.com Ltd cannot assume legal liability for any errors or omissions it might contain. The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not necessarily a guide to future performance. The difference between the buy price and the sell price for smaller company shares can be significant. Before investing, readers should seek professional advice from a Financial Services Authority authorised Stockbroker or Financial Adviser.

t1ps.com limited can be contacted at 5-11 Worship Street, London EC2A 2BH - email [email protected] - fax 020 7628 3815 - tel 020 7562 3371

Notes

Page 15 of 16

Notes

Growth Equities & Company Research