39

BUY-BACK OF SHARES 1

| Date post: | 15-Apr-2017 |

| Category: |

Economy & Finance |

| Upload: | 92neil |

| View: | 458 times |

| Download: | 0 times |

1

BUY-BACK OF SHARES

2

Introduction

It was introduced by Companies Amendment Act,1999

Buy-back refers to purchase by a company of its own shares

It takes place at a specified price generally determined on the basis of average price of shares in past few months

3

Reasons for buy-back of shares

Signaling Effect

Realign the capital structure

Avert hostile takeovers

4

Agency Conflict

Increase the earnings per share

Improve returns to the stakeholders

5

Disadvantages of buy-back of shares

It puts companies at a risk

Buy-back of shares sends out negative signals to the investors

If a company pays too much for its own shares, it might become a disadvantage

6

Provisions governing Buy-back of shares under Companies

Act,2013

Power of company to purchase its own securities

Purchases can be made out of:• Free reserves• Securities premium account• Proceeds of any shares or other specified securities

7

Preliminary conditions for buy-back:

• Must be authorized by its articles• A special resolution has been passed at a general meeting of the

company authorizing the buy-back• The buy-back is twenty-five per cent or less of the aggregate of

paid-up capital and free reserves of the company• All the shares or other specified securities for buy-back are fully

paid-up

8

If shares or securities are listed, buy back will be in accordance with the regulations made by SEBI

The buy-back in respect of unlisted shares or other specified securities is in accordance Share Capital and Debentures Rules, 2014

No offer of buy-back shall be made within a period of one year from the date of the closure of the preceding offer of buy-back, if any

9

The notice of the meeting at which the special resolution is proposed to be passed shall be accompanied by an explanatory statement

Time Limit

Options for Buy-back

Solvency Declaration

10

Extinguishment of Certificate

No further issue till 6 months

Register to be maintained

Return of Buy Back & a Declaration

11

Punishment for any Default

Transfer of certain sums to capital redemption reserve account

Capital Redemption Reserve

Utilization of Capital Redemption Reserves

12

Prohibition for Buy Back in certain circumstances

Restriction on Buy Back

Prohibitions

13

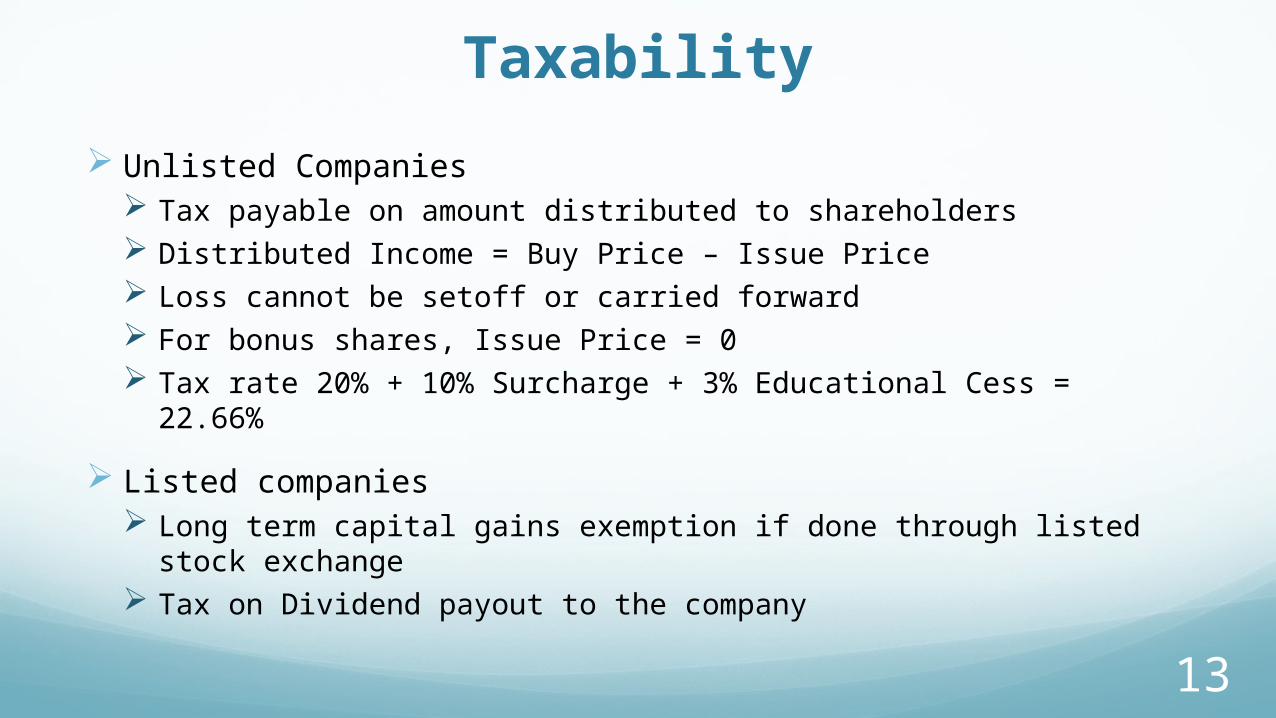

Taxability

Unlisted Companies Tax payable on amount distributed to shareholders Distributed Income = Buy Price – Issue Price Loss cannot be setoff or carried forward For bonus shares, Issue Price = 0 Tax rate 20% + 10% Surcharge + 3% Educational Cess = 22.66%

Listed companies Long term capital gains exemption if done through listed stock

exchange Tax on Dividend payout to the company

14

SEBI Guidelines

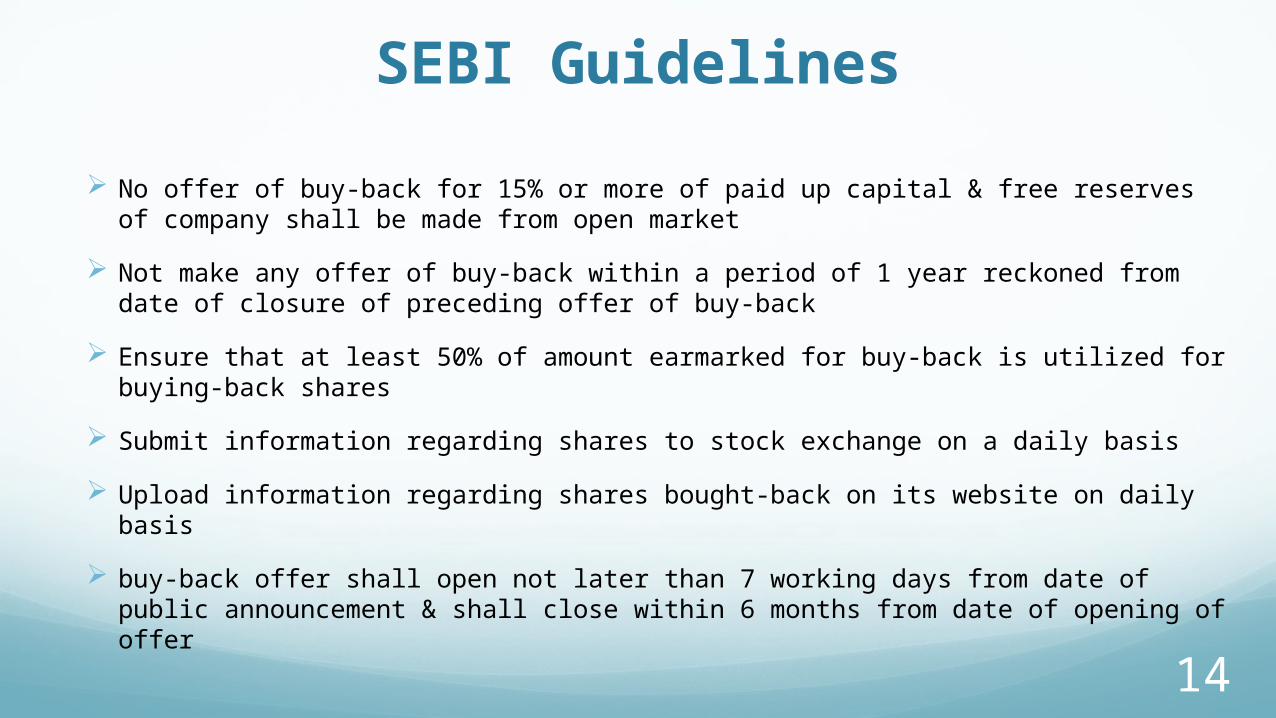

No offer of buy-back for 15% or more of paid up capital & free reserves of company shall be made from open market

Not make any offer of buy-back within a period of 1 year reckoned from date of closure of preceding offer of buy-back

Ensure that at least 50% of amount earmarked for buy-back is utilized for buying-back shares

Submit information regarding shares to stock exchange on a daily basis Upload information regarding shares bought-back on its website on daily basis buy-back offer shall open not later than 7 working days from date of public

announcement & shall close within 6 months from date of opening of offer

15

Escrow Account Create an escrow account for performance of its obligations Deposit 25% of the amount earmarked for the buy-back Escrow Account may be in the form of

cash deposited with any scheduled commercial bank OR bank guarantee issued in favour of the merchant banker by any

scheduled commercial bank May be released for making payment to the shareholders subject

to at least 2.5% of the amount earmarked for buy-back

16

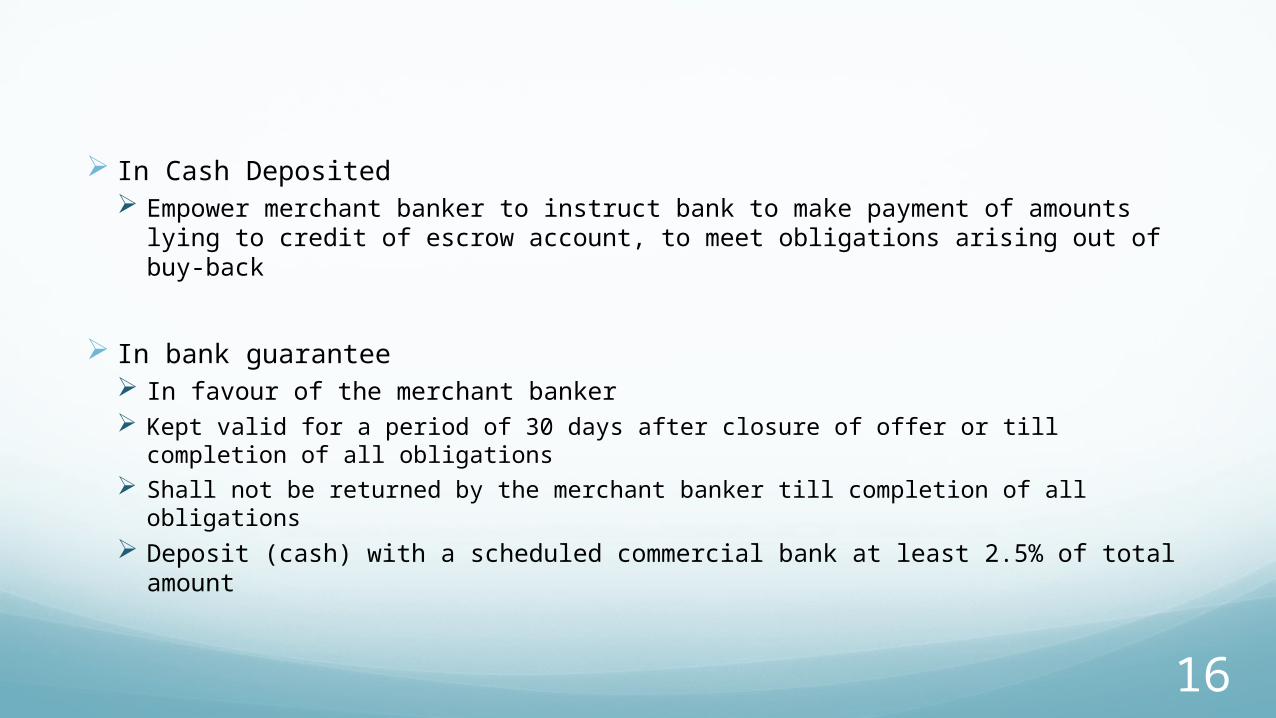

In Cash Deposited Empower merchant banker to instruct bank to make payment of amounts

lying to credit of escrow account, to meet obligations arising out of buy-back

In bank guarantee In favour of the merchant banker Kept valid for a period of 30 days after closure of offer or till completion of all

obligations Shall not be returned by the merchant banker till completion of all obligations Deposit (cash) with a scheduled commercial bank at least 2.5% of total

amount

17

Fulfilling obligation, amount & guarantee remaining in escrow account shall be released to company

Non-compliance - forfeit escrow account VWAMP of shares of company during buy-back period was higher than

buy-back price as certified by Merchant banker based on inputs provided by Stock Exchanges

Inadequate sell orders despite buy orders placed by company as certified by e Merchant banker based on inputs provided by Stock Exchanges

Circumstances which were beyond the control of company & in opinion of Board merit consideration

18

Methods of Buyback of Listed Companies

Tender Offer

Method

Through Open

Market

Stock Exchange

Book Building Process

From Odd Lot

Holders

19

Buy-back through tender offer Shareholders may be presented with a tender offer by the company to

submit, a portion or all of their shares within a time frame.

The size & price is fixed by the company (always at a premium to market price)

Basic entitlement of the shareholders

Excess tenders are not gauranteed to be bought back by the company

20

Procedure File declaration of solvency with SEBI.

21

The date of opening the offer shall not be earlier than 7 days or later than 30 days after the ‘specified date’.

22

Deposit in an escrow account.

Make payment to the shareholders, whose offer for buy back has been accepted .

23

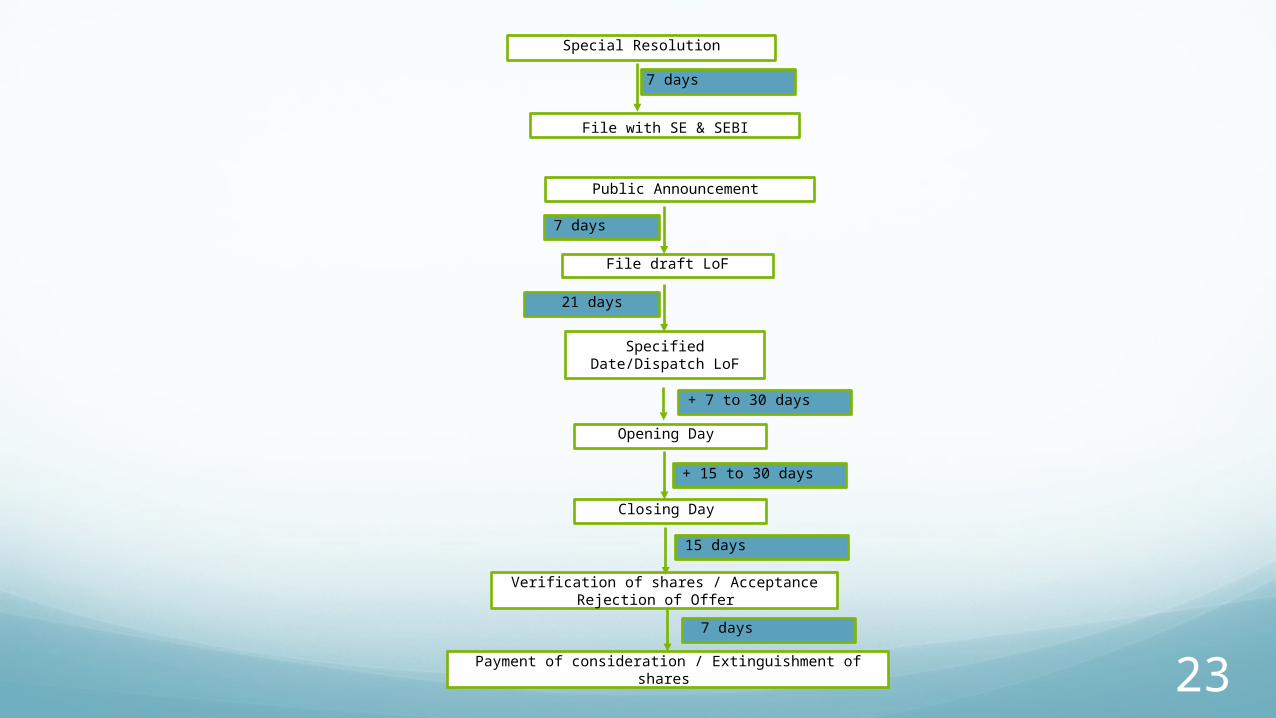

Special Resolution

7 days

File with SE & SEBI

Public Announcement

7 days

File draft LoF

Specified Date/Dispatch LoF

21 days

+ 7 to 30 days

Opening Day

+ 15 to 30 days

Closing Day

Verification of shares / Acceptance Rejection of Offer

15 days

Payment of consideration / Extinguishment of shares

7 days

24

Buy back from open market through stock exchanges

File declaration of solvency with SEBI.

25

Buy back shall be made only on stock exchanges with electronic trading facility through order matching mechanism.

26

Complete verification of acceptances & File the particulars of share certificates that are extinguished with stock exchanges.

27

Public Announcement

File copy with SEBI

Commencement of Buy Back

2 days 7 days

Purchase of Shares

15 days

Verification of Acceptances

Closure Date

Extinguishment of shares

7 days

Special / BOD Resolution

File Copy with SEBI

7 days

28

Buy-back from open market through book building

Special Resolution

Declaration Of Solvency

Appointment of Merchant

Banker

Opening of Escrow Account

Verification of the offers received

Closing of offer for buy-

back

Opening of offer for Buy-

back

Public Announceme

nt

29

Price Determination The final offer price shall be determined as the price at which the maximum

number of shares has been offered.

If the acquirers accept final price, they have to accept offers up to and including the final price i.e. 480 shares (i.e. 100+164+216 shares) at the final price of Rs. 260/-.

Offer Quantity (in nos.)

Offer Price (Rs)

Remarks

100 240 Floor Price is Rs. 240 as fixed by the company.

164 250216 260 Final Price is Rs. 260 –

Maximum Quantity54 27010 280

30

15 to 30 days

Public Announcement

File copy with SEBI

Commencement of Buy Back

2 days 7 days

Completion of Buy Back

Verification of shares / Acceptance Rejection of Offer

15 days

Payment of consideration / Extinguishment/ Return of Shares

7 days

31

Odd lot holders An odd-lot buyback occurs when a company offers to purchase

shares of its stock back from people who hold less than 100 shares.

A popular method that companies use to buy back stocks is called a Dutch auction

This type of offer makes it less expensive both for the company and for the shareholders

32

Buy-back for unlisted companies Method

From the existing shareholders on proportionate basis By purchasing the securities issued to employees of the company

Special Resolution

Filing Letter Of Offer along with declaration of solvency with the registrar of companies.

Offer Procedure Dispatch the offer letter immediately Buy back shall remain open from a period not less than 15 days & not exceeding 30 days Acceptance is on a proportionate basis Deemed acceptance

33

Payment to Shareholders Open a special bank account Make payment within 7 days of acceptance

General Obligations Of the Company The letter of offer shall contain true, factual and material information. the company shall not issue any shares including by way of bonus The company shall testify the availability of funds Company shall not withdraw the offer once the draft letter of offer has been filed The company shall not utilise any money borrowed from Banks/Financial

instituitions

34

Returns to be filed with Registrar

Extinguishment of Certificate Extinguish & physically destroy Furnish a certificate to the registrar of companies duly verified by: i. Two whole time directorsii. Company secretary Maintain records of cancelled shares

35

Difference between buy-back ,dividends & bonus share

Buyback of Shares Dividend Bonus Share

Share buybacks represent cash distributed to existing shareholders in exchange for company’s outstanding equity.

Dividends are the portion of corporate profits paid out to stockholders in the form of cash.

Bonus Share is an increase in the amount of shares of the company with the new shares given to share holders.

Share buybacks there's a total flexibility for the company

Dividend payments require a commitment from the company. -

36

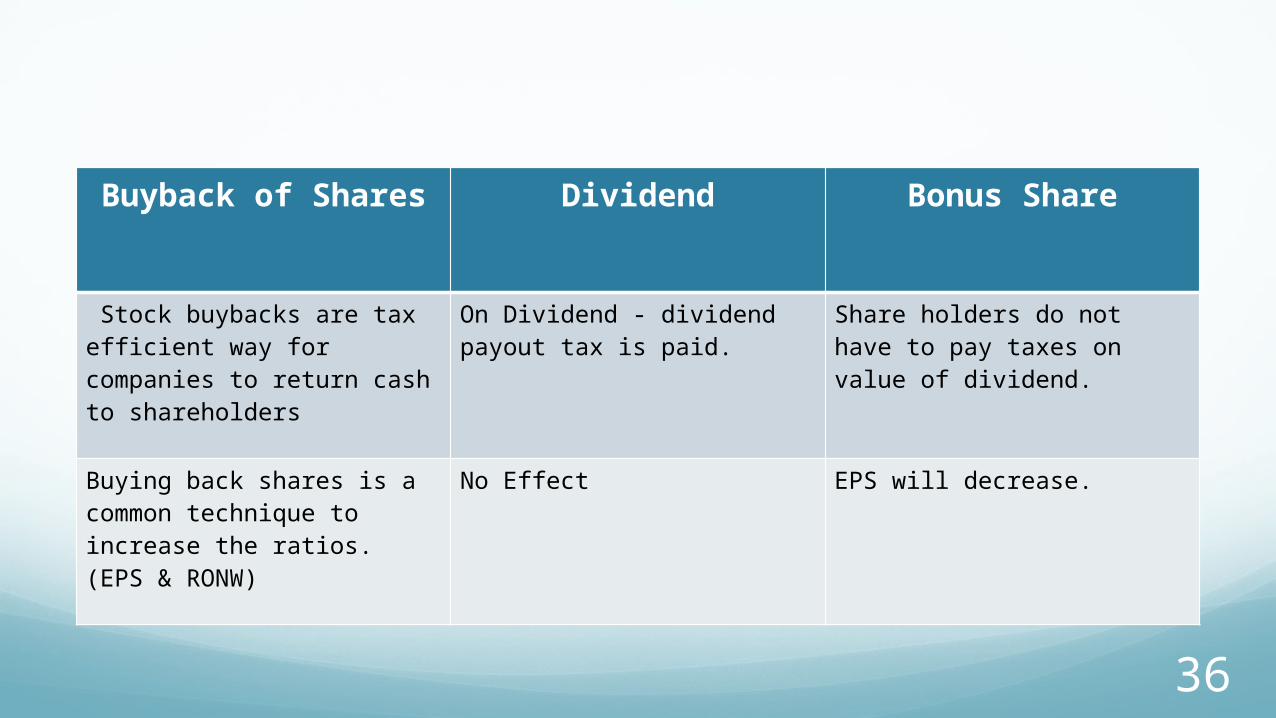

Buyback of Shares Dividend Bonus Share

Stock buybacks are tax efficient way for companies to return cash to shareholders

On Dividend - dividend payout tax is paid.

Share holders do not have to pay taxes on value of dividend.

Buying back shares is a common technique to increase the ratios. (EPS & RONW)

No Effect EPS will decrease.

37

Bayer Cropscience Limited It is an Agri Care Company.

Announced buy back on September 18, 2013

Total shares for buy back 28,79,746

Representing 7.29% of total paid up capital

38

Total buy back size is Rs. 454,99,98,680.

Buy back price Rs. 1,580.

Premium of 18.3% over the average closing prices of the Equity Shares on BSE for 3 months.

39

Buy back price is 223.14% more than the book value of each share Rs.488.95 as at March 31, 2013.

Tender offer

Buy back to reward the share holders.

Increase ratios for the company.EPS will increase form Rs. 294.11 to Rs. 317.23RONW will increase from 60.15% to 78.69%