Buybacks and the board | i IRRC Institute and Tapestry Networks Buybacks and the board: Director perspectives on the share repurchase revolution Richard Fields, Tapestry Networks August 2016

Transcript

Buybacks and the board | iIRRC Institute and Tapestry Networks

Buybacks and the board: Director perspectives on the share repurchase revolution

Richard Fields, Tapestry Networks

August 2016

Buybacks and the board | iiIRRC Institute and Tapestry Networks

Buybacks and the board | 1IRRC Institute and Tapestry Networks

Executive summaryTo learn how companies make decisions about share repurchases, Tapestry Networks

interviewed 44 directors serving on the boards of 95 publicly traded US companies with

an aggregate market capitalization of $2.7 trillion. This report synthesizes these directors’ views and broader research on repurchase programs.

Report highlights include:

Companies are buying back shares at historically significant levels

In recent years, Standard and Poor’s 500 companies have repurchased their shares at a remarkable rate. S&P 500 companies acquired $166.3 billion of their own shares in the first quarter of 2016, more than in any other quarter since the financial crisis. In each of the last nine quarters, at least 370 S&P 500 companies repurchased shares, and over the last three years, S&P 500 companies spent over $1.5 trillion on buybacks.

Macroeconomic factors make share buybacks unusually attractive

Monetary and fiscal policies and macroeconomic forces have pushed companies to consider repurchase programs. Many directors said that they would be unlikely to find enough good opportunities to invest all their companies’ capital in today’s low-growth, low-interest-rate environment, and that it was often better to return capital to shareholders. They tend to prefer buybacks to dividends, primarily because they believe a buyback program offers greater flexibility over time.

US tax policies that discourage companies from repatriating foreign cash have also spurred buyback activity. Because creditors know that borrowers can repatriate foreign earnings at any time, some corporations are able to engage in almost costless borrowing to fund buyback programs.

Directors say that companies repurchase shares for one or more of four reasons:

• To return capital to shareholders

• To invest in the company’s shares

• To offset dilution from using equity as currency

• To alter the company’s capital structure

Success depends on the purpose of the buyback. Buybacks can only be evaluated effectively if a company is explicit about the reason or reasons for the repurchase program.

Buybacks and the board | 2IRRC Institute and Tapestry Networks

Most directors do not agree with popular criticisms of buyback programs

The two most common criticisms of buyback programs are that they jeopardize corporate growth and that they lead to large, unjust pay packages for senior managers. Some directors saw merit in these criticisms; most did not. In general:

Directors believe that buybacks do not jeopardize growth

Some research suggests that companies regularly turn down projects with positive net present value because of irrational risk aversion or excessive discounting of future cash flows. Other research correlates higher buyback activity with lower capital expenditure and revenue growth. Nonetheless, most directors think that their executives do everything they can to grow their businesses. Indeed, some embrace buybacks out of fear that companies would otherwise squander capital by chasing uneconomic growth.

Directors believe that buybacks do not unjustly enrich senior executives

Pay for top executives at major companies is almost always linked, directly or indirectly, to company share prices. Buybacks may increase executive compensation by improving the company’s performance on metrics such as earnings per share (EPS), or by causing the share price to rise, affecting total shareholder return calculations or the value of stock executives own or expect.

However, most directors said that their companies are aware of the relationship between buyback programs and compensation and that they make deliberate, informed choices to ensure that they reward executives for desired behavior rather than for financial manipulation of share prices. Anticipated buyback effects on EPS are usually factored into EPS targets, they say, and unanticipated effects can be adjusted out.

Investor and public concerns about high rewards for near-term share price growth are primarily about the risk that these incentives pose to long-term value creation. Most directors think that their companies are focused on long-term growth and that their incentive programs reward executives accordingly.

There is room to improve corporate disclosures about share repurchase programs

Few companies publicly disclose details about buyback decision-making and very few state which of the four reasons are driving any particular buyback program. Although a number of directors mentioned that their companies project how buyback activity will affect EPS and adjust targets accordingly, only 20 S&P 500 companies disclosed that they did so. Most companies and boards with robust buyback processes do not currently disclose enough to receive credit for their work.

Buybacks and the board | 3IRRC Institute and Tapestry Networks

Contents

Executive summary 1

Contents 3

Introduction 4

What is the board’s involvement in capital return decision-making? 6

Why do companies repurchase shares? 8

Buybacks to return capital to shareholders 9

Buybacks to invest in undervalued shares 14

Buybacks to offset dilution 15

Buybacks to alter a company’s capital structure 16

Are buybacks jeopardizing growth? 18

Do repurchase programs unjustly enrich senior executives? 24

Are buyback disclosures clear and effective? 30

Conclusions 32

About the author 34

Acknowledgments 34

Appendix 1: Interviewed directors and affiliated public company boards 35

Appendix 2: Analysis of public companies affiliated with interviewed directors 37

Appendix 3: Buyback disclosure examples 39

Buybacks and the board | 4IRRC Institute and Tapestry Networks

IntroductionLarge American public companies have repurchased their shares at a remarkable rate. S&P 500 companies acquired $166.3 billion of their own shares in the first quarter of 2016, more than in any other quarter since the financial crisis.1 This continued a string of broad buyback activity. In each of the last nine quarters, at least 370 S&P 500 companies repurchased shares,

2 and over the last three years, S&P 500 companies spent over $1.5 trillion on buybacks.3

Between 2003 and 2013, S&P 500 companies doubled their spending on share repurchases and dividends while cutting their spending on investments in new plants and equipment.4 According to data from McKinsey, buybacks have accounted for 47% of US companies’ income since 2011, up from 23% in the early 1990s and less than 10% in the early 1980s.5

There are reasons to believe that share buybacks will remain popular in the short term. Non-financial S&P 500 companies had $1.77 trillion in cash holdings in the fourth quarter of 2015, more than double what was on hand in 2009.6 Most people expect the low interest rates to continue for some period of time. In a low-growth and low interest rate environment, where capital is cheap and certain shareholders agitate for capital return,

buybacks are an attractive option to many companies.

Critics worry that the growth in buyback activity has come at the expense of productive investments. Larry Fink, the chief executive of BlackRock, the world’s biggest investor with more than $4.5 trillion in assets under management, recently sent a letter to leading CEOs expressing concern: “Many companies continue to engage in practices that may undermine their ability to invest for the future. Dividends paid out by S&P 500 companies in 2015 amounted to the highest proportion of their earnings since 2009. As of the end of the third quarter of 2015, buybacks were up 27% over 12 months. We certainly support returning excess cash to shareholders, but not at the expense of value-creating investment.” 7

1 Andrew Birstingl, “Key Metrics,” FactSet Buyback Quarterly, June 23, 2016.

2 Andrew Birstingl, “Key Metrics,” FactSet Buyback Quarterly, March 17, 2016, and “Key Metrics,” FactSet Buyback Quarterly, June 23, 2016.

3 Justin Lahart, “What $1.5 Trillion in Stock Buybacks Doesn’t Buy,” Wall Street Journal, November 8, 2015.

4 Vipal Monga, David Benoit, and Theo Francis, “As Activism Rises, U.S. Firms Spend More on Buybacks Than Factories,”

Wall Street Journal, May 26, 2015.

5 Tim Koller, “Are Share Buybacks Jeopardizing Future Growth?” McKinsey & Company, October 2015.

6 EY Center for Board Matters, Buybacks vs. Backlash: The Board’s Role in Weighing the Pros and Cons of Stock Repurchases, EY, June 2016, 1.

7 Laurence D. Fink letter to CEOs, February 1, 2016.

Buybacks and the board | 5IRRC Institute and Tapestry Networks

Some observers believe buybacks unjustly inflate senior managers’ pay. According to University of Massachusetts economics professor William Lazonick, in 2012, the 500 highest-paid executives in the United States received, on average, $30.3 million each, 42% of which came from stock options and 41% from stock awards.8 Because share repurchases can raise share prices, at least in the short term, managers often have a personal financial incentive to buy back shares. This incentive may be even stronger at companies that reward executives for earnings per share (EPS). In 2016, 31% of annual incentive plans and 22% of long-term incentive plans were tied to EPS.9 Buybacks tend to improve EPS and other share-based measures of profitability as they reduce the number of shares outstanding.

Against this backdrop, the Investor Responsibility Research Center Institute asked Tapestry Networks to undertake an extensive inquiry into non-executive directors’ views about share repurchase programs. Between August 2015 and May 2016, Tapestry interviewed 44 directors representing 95 publicly traded US companies with an aggregate market capitalization of $2.7 trillion and aggregate revenue of $1.4 trillion.10

Tapestry conducted interviews on a not-for-attribution basis. Unattributed quotations from the interviews are included throughout the report; they appear as italicized text in quotation marks.

This report synthesizes the perspectives of these nonexecutive directors and other research on a number of important questions related to share repurchase programs:

• What is the board’s involvement in capital return decision-making?

• Why do companies buy back shares?

• Are buybacks jeopardizing growth?

• Do repurchase programs unjustly enrich senior executives?

• Are buyback disclosures clear and effective?

8 William Lazonick, “Profits Without Prosperity,” Harvard Business Review, September 2014.

9 Mike Rourke, 2016 Trends and Developments in Executive Compensation Meridian Compensation Partners, May 2016, 13, 21.

10 See Appendix 1, page 35.

Buybacks have accounted for 47% of US companies’ income since 2011, up from 23% in the early 1990s and less than 10% in the early 1980s.

Buybacks and the board | 6IRRC Institute and Tapestry Networks

These decisions are so key to the long-term health of the company that the board has to be heavily involved … This is one issue you cannot shortchange.

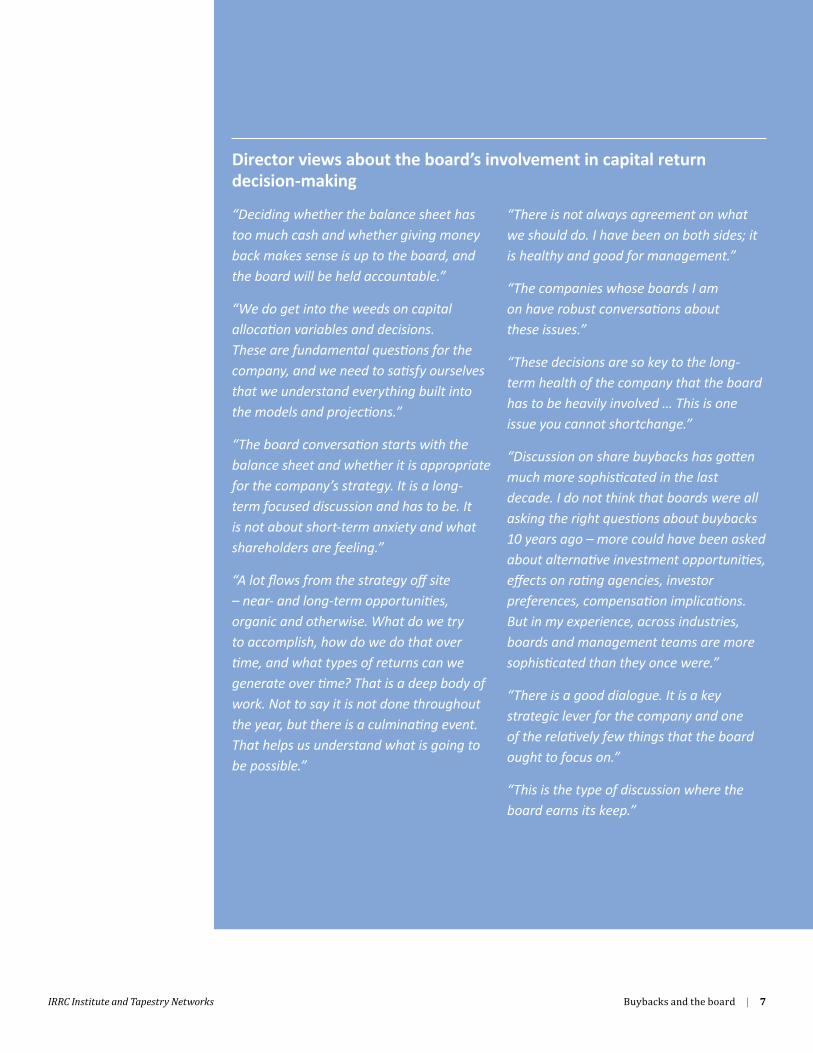

What is the board’s involvement in capital return decision-making?Boards are central players in capital return decisions, interviewed directors said. The relationship between company strategy, desired capital structure, and health of the balance sheet demands robust board attention.

The conversation about capital return at most companies happens throughout the year. A general approach typically is agreed upon at the company’s annual board meeting devoted to evaluating the strategy. However, directors come back to capital return as they evaluate investment opportunities, both external and internal, over the course of the year. “Strategy is a living thing – not a book – and at every board meeting, we are looking at what has happened with the company, the industry, and the market since the last meeting,” one director said. Another director added, “capital structure is a key element of business strategy and must balance factors including long- and short-term investment horizons, strategic and financing risk, and return expectations when considering capital return.”

Directors said the board debates are often vigorous. Interviewees noted that directors often have very strong opinions about capital structure, how much cash to have on hand, and the relative desirability of buybacks and dividends. Board members actively engage with the different views of senior managers and their colleagues to evaluate whether to return capital and how they should do it.

Buybacks and the board | 7IRRC Institute and Tapestry Networks

“Deciding whether the balance sheet has too much cash and whether giving money back makes sense is up to the board, and the board will be held accountable.”

“We do get into the weeds on capital allocation variables and decisions. These are fundamental questions for the company, and we need to satisfy ourselves that we understand everything built into the models and projections.”

“The board conversation starts with the balance sheet and whether it is appropriate for the company’s strategy. It is a long-term focused discussion and has to be. It is not about short-term anxiety and what shareholders are feeling.”

“A lot flows from the strategy off site – near- and long-term opportunities, organic and otherwise. What do we try to accomplish, how do we do that over time, and what types of returns can we generate over time? That is a deep body of work. Not to say it is not done throughout the year, but there is a culminating event. That helps us understand what is going to be possible.”

“There is not always agreement on what we should do. I have been on both sides; it is healthy and good for management.”

“The companies whose boards I am on have robust conversations about these issues.”

“These decisions are so key to the long-term health of the company that the board has to be heavily involved … This is one issue you cannot shortchange.”

“Discussion on share buybacks has gotten much more sophisticated in the last decade. I do not think that boards were all asking the right questions about buybacks 10 years ago – more could have been asked about alternative investment opportunities, effects on rating agencies, investor preferences, compensation implications. But in my experience, across industries, boards and management teams are more sophisticated than they once were.”

“There is a good dialogue. It is a key strategic lever for the company and one of the relatively few things that the board ought to focus on.”

“This is the type of discussion where the board earns its keep.”

Director views about the board’s involvement in capital return decision-making

Buybacks and the board | 8IRRC Institute and Tapestry Networks

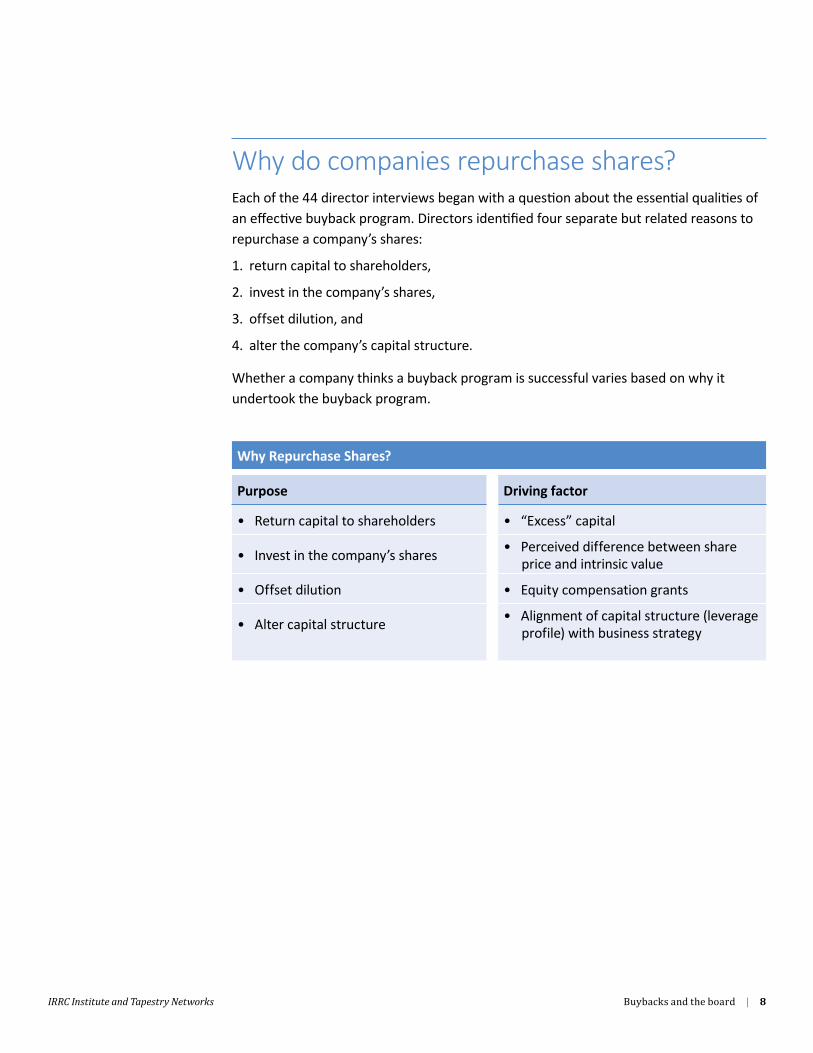

Why do companies repurchase shares?Each of the 44 director interviews began with a question about the essential qualities of an effective buyback program. Directors identified four separate but related reasons to repurchase a company’s shares:

1. return capital to shareholders,

2. invest in the company’s shares,

3. offset dilution, and

4. alter the company’s capital structure.

Whether a company thinks a buyback program is successful varies based on why it

undertook the buyback program.

Why Repurchase Shares?

Purpose Driving factor

• Return capital to shareholders • “Excess” capital

• Invest in the company’s shares • Perceived difference between share

price and intrinsic value

• Offset dilution • Equity compensation grants

• Alter capital structure • Alignment of capital structure (leverage

profile) with business strategy

Buybacks and the board | 9IRRC Institute and Tapestry Networks

Buybacks to return capital to shareholders

Successful when Capital is returned beyond what is needed for the company (working capital, capital expenditures, and investments that meet the company’s strategic objectives/return rates) without damaging the company’s ability to execute on business plan and strategy.

Key factors Desired level of working capital and capital expenditures, whether there are “good” alternative investments, dividend policy, other capital commitments

Directors universally said that excess capital should be returned to shareholders, although they had different opinions of what “excess” means. The process begins with evaluating the company’s strategy and determining the company’s capital needs (often described in terms of the balance sheet, investment, dry powder, and debt rating requirements). For the vast majority of directors, capital is “excess” only if it remains after all productive investments are made and current dividend expectations are met.

“‘Excess’ is after you make the investments in the company [through which] you will come out stronger than you are today. That can be research and development, acquisitions, and upgrades to company infrastructure and technology.”

“The question is, what capital is necessary for business and what is excess? Then, what is appropriate for the excess: Keep some powder dry? Pay your shareholders through dividends or buybacks?”

“The hierarchy of needs starts with the strategy – investing in growth, organic and inorganic – and only then moves to returning capital to the shareholders.”

“A company returns money when it does not think there’s a valuable use for that cash in the foreseeable future.”

“First thing to pay attention to is the fundamental cash needs of the business. Second, are you a growth business or not? If so, what do you need to fund growth? Generally, management, the board, and investors are supportive of using the cash to grow the business. Then, you see what is left over.”

“There are a number of vectors to consider: What are our opportunities? How can we fund them? How do they compare to each other?”

“There are a lot of cases right now where acquisitions and internal investments don’t look good. I much favor organic growth, but sometimes that’s just not there and a buyback makes a lot of sense.”

Director views about excess capital

Buybacks and the board | 10IRRC Institute and Tapestry Networks

Interviewed directors believed that their companies effectively vetted all investment options; most were very confident that their companies were not returning money that could be used more productively. Some, however, were not. For more on this point, see “Are buybacks jeopardizing growth?” pages 18-23.

Buybacks or dividends?

Companies can return cash to shareholders through dividends (either regular quarterly or annual dividends or, less commonly, special dividends) and buybacks (most frequently open-market repurchases).11

Most S&P 500 companies have regular dividends and routinely buy back shares.12

Aggregate S&P 500 dividend payments amounted to $103.3 billion during the third quarter of 2015, the third largest quarterly total in 10 years, and the total dividend payout for the trailing 12 months ending in the third quarter 2015 was $410.8 billion, marking a 10-year high.13

Most interviewed directors see a place for both dividends and buybacks, but some had a

strong preference for dividends. “Buybacks are nothing more than financial engineering. Real companies with real cash pay real dividends and do not try to manipulate EPS with buybacks. That is a minority view,” one director said. Another director agreed: “I am strongly against buybacks. I think there is a lot of evidence that says they haven’t done

11 PwC, Is Cash Burning a Hole in Your Pocket? Thinking Through Share Repurchases and Dividends, 2. Companies can buy back shares through open-market repurchases, privately negotiated repurchases, tender offers, and accelerated share-repurchase programs.

12 Andrew Birstingl, “Shareholder Distributions,” FactSet Buyback Quarterly, March 17, 2016.

13 Andrew Birstingl, “Increase in Dividends Help Push Distributions to New High,” FactSet Dividend Quarterly, December 16, 2015.

Buybacks and the board | 11IRRC Institute and Tapestry Networks

much for stock appreciation. There is too much teaching in MBA courses about the legitimacy of buybacks. I fight them on every board I am on, and I often win.”

For those without a strong bias against buybacks, the first question is how much cash remains after meeting dividend expectations. Once the dividend obligation is met, most directors favored returning whatever excess cash remained through buybacks because instituting or increasing a dividend creates an ongoing expectation, in those directors’ opinions, even if it does not create a legal obligation. The flexibility of buybacks was their chief advantage to alternative capital return options.

“You never want to institute a dividend and back off, but you can be flexible with buying back stock.”

“With dividends, you don’t switch it on and off; you need to be comfortable with a steady, consistent return of capital. With a buyback, you can turn it off, which makes it less of a long-term decision.”

“When you declare a dividend, you essentially create a new, continuing obligation with debt characteristics – you cannot cut it because of the signal about the company and its financial outlook.”

“The flexibility is important. We put a buyback plan on hold for a couple years to complete an unexpected but attractive acquisition. When there is a strain on opportunities, we can use a buyback to cover the cost.”

“In terms of the way most companies think of dividends, you may not necessarily want to raise them, but you want to be doggone sure you’re not reducing them, except when in extremis. You can be much more nimble with buybacks than with dividends.”

Director views about the relative flexibility of buybacks

Buybacks and the board | 12IRRC Institute and Tapestry Networks

A second advantage may be investor preference. Activist shareholders have pushed for greater capital return, often through buybacks. According to a March 2016 PwC report,

…with about $173 billion currently under activist management, proxy contests are more frequent – as are settlements. Activists’ strategies often involve pressuring companies to take one or more of several actions: increase share repurchases, increase dividends, restructure, spin-off a division, or even sell the company. In many of these areas, including increasing share repurchases and dividends, activists have been effective in achieving their goals … Companies targeted by activists increased spending on share repurchases and dividends to an average of 37% of operating cash flow in the first year after being approached – from 22% the year prior.14

Interviewed directors said that some shareholders put substantial pressure on a company to create or increase buyback programs. One said, “If you haven’t been doing a buyback and pick up an activist, creating [a buyback] is the easiest way to return the capital.”

Activists are motivated for different reasons. Some directors found activists’ motivations to run counter to the company’s long-term interests, but others offered a more nuanced perspective. As one director said, “A push for a greater return of capital may be driven by a belief that the company has too much low-returning cash on the balance sheet or is investing in high-risk capital projects. I would not want to defend activists but I do think their motivation is important.”

While many said that the growth of shareholder activism has focused attention on buybacks, few had experience with a company returning capital to satisfy a shareholder demand in lieu of putting the money to better use. One suggested meeting with the relevant shareholders with an open mind and buying back shares only when it made

sense. “A lot of activists are looking for a quick pop to the stock and they push buybacks, and it may not be right for the company long term. It can be useful to have open relationships with activist investors so that you both understand the company’s objectives and plans. Sometimes you can convince them there are great opportunities elsewhere – and sometimes you realize there aren’t and you buy back.”

The preferences of the company’s largest holders, activist or not, matter – and differ. One director noted, “[A company] polls the top 20–30 shareholders and asks what they prefer. They have typically preferred buybacks.” A growing number of major investors have suggested shifting the balance further to dividends – often explicitly because they are less flexible than buybacks. For example, Fidelity’s global chief investment officer of equities, Dominic Rossi, wrote, “Share buybacks are an acquisition of an asset, with

14 PwC, Is Cash Burning a Hole in Your Pocket? Thinking Through Share Repurchases and Dividends, 1.

If you haven’t been doing a buyback and pick up an activist, creating [a buyback] is the easiest way to return the capital.

Buybacks and the board | 13IRRC Institute and Tapestry Networks

a price to earnings multiple. They are not a risk-free investment; indeed they are very risky. A dividend is a long- term commitment to shareholders to distribute excess returns. It is not an acquisition. Therefore, a company will attract very different shareholders depending upon which route it takes. Buybacks will attract activist and event -driven shareholders, while dividends will attract a more stable shareholder base.”15

A company may also choose to consider preferences of potential future holders if they wish to alter the company’s investment base. This typically results in a company creating or increasing a dividend because many investors have well-defined dividend targets, directors said.

15 Dominic Rossi, “Companies Can Invest and Conduct Buybacks,” Financial Times, July 20, 2015.

“No question that there are more buybacks of size as a result of activists who have particularly looked at large cash balances, often offshore, and said that you do not need to hold that much cash. That has unquestionably spurred incremental buyback activity.”

“Activists have had an absolute impact. They push to get rid of non-performing businesses and return capital; they do not favor the risky approach of using capital to grow the business for the long term.”

“From some shareholders, including significant ones, there is pressure for buybacks.”

“Activists think you will use cash to do bad acquisitions instead of returning it to shareholders.”

“I suspect that companies are getting unduly responsive to investors who just want cash.”

“Ultimately, in my experience, the question is whether the investor base believes that the management team and strategy make sense. That’s been happening for years and years, but it’s been quieter and more behind the scenes. Activists have simply brought that conversation to the public.”

“Investor determination on buybacks blows me away.”

“Investors do punish. But why are you, as a director, there? You have to have a certain amount of courage as a director, and many of us view our responsibility as long-term value creation, not just short-term opportunity.”

Director views about investor pressure for buybacks

Buybacks and the board | 14IRRC Institute and Tapestry Networks

Buybacks to invest in undervalued shares

Successful when Company believes investing in its own shares will yield a higher return than alternative investments

Key factors Share price, perceived intrinsic company value, cost of capital, opportunity

cost, float, other investment opportunities

When considering a buyback, many corporate leaders have a strong opinion about the

importance of a company’s intrinsic business value relative to stock price. Berkshire Hathaway CEO Warren Buffett has said that an essential precondition for a company to repurchase shares is that “its stock is selling at a material discount to the company’s intrinsic business value, conservatively calculated.”16

The majority of those interviewed believe that this is an important factor when evaluating whether to repurchase shares. “The decision to buy back shares starts by asking if we think our shares are undervalued,” one director said. Another asserted, “Directors need to understand where the price is, relative to intrinsic value. You shouldn’t buy back if you’re at 90%-plus of intrinsic value. You are destroying value.”

According to several interviewed directors, companies compare the expected return over a given time horizon for a buyback program against the return from alternative investments. One director said, “For me, it is all about return on invested capital (ROIC). The ROIC for buybacks is sometimes better than the anticipated ROIC on alternative capital uses – in those cases, we buy back shares.”

Others go further: at least one company thought its shares were so undervalued that it sold part of the business, in part to generate the money to fund a buyback program, a

director said.

A vocal minority of those interviewed prefer not to link buyback programs to a

perception that the shares are undervalued, and they highlighted the following points:

• Companies tend to err in identifying when shares are undervalued. “Management teams often think that the company is undervalued,” one said. “Some executives have acumen for this, but it’s not common.” One director asked, “How many times have we seen companies buy back shares when markets are at their highest levels?” Another

added, “Few companies repurchase shares when the stock is getting killed because they need money for other things. How many meaningful buyback programs did we see after the financial crisis?”

16 Warren Buffet letter to the shareholders of Berkshire Hathaway, February 25, 2012.

Buybacks and the board | 15IRRC Institute and Tapestry Networks

Few companies consistently pick the right time to buy back shares. One analysis found that between 2004 and 2010, “a majority of companies repurchased shares when they and the market were both doing well – and were reluctant to repurchase shares when prices were low relative to their intrinsic valuations.”17

Few companies stopped

repurchase programs during the 2007 market peak and few bought their shares when the market bottomed in 2009.18

• Company managers and directors are not smarter than the markets. Some

directors go further and suggest that it is not possible for shares to be “undervalued.” “Assuming adequate disclosure, the board and management team are not smarter than the market as a whole,” one director said. Another noted, “If you believe in the efficient market theory as I do, the price accurately reflects value.”

• Companies are not and should not be in the business of picking stocks. “While some boards and managers assert that they can buy back shares to generate the best returns for shareholders, most shareholders I know say, ‘Please do not pick stocks on my behalf – give me back my money so I can choose where I want to invest,’” one

director said.

Most directors who dispute the relevance of intrinsic value to buyback decision-making still support repurchasing shares, but they do not judge success based on stock price changes. “It’s not luck; it’s long-term confidence in your strategy and belief that you will create long-term value,” one director said.

Buybacks to offset dilution

Successful when Existing owner holdings are not diluted by equity issuedKey factors Dilution rate, investor preferences

Most companies repurchase shares to offset dilution caused by executive compensation paid in equity-linked forms of compensation. “I believe you always buy stock back to offset dilution that comes from granting options. You do not want to dilute the current shareholders,” one director said. Another said, “My philosophy is that we always have a minimum buyback, at least equal to equity distributed during the year.” According

to many interviewed directors, companies attempt to offset much of their dilution. Offsetting dilution was a justification for part or all of many share buyback plans.

17 Bin Jiang and Tim Koller, “The Savvy Executive’s Guide to Buying Back Shares,” McKinsey & Company, October 2011.

Buybacks and the board | 16IRRC Institute and Tapestry Networks

There is a lot of dilution to offset. Lombard Odier Asset Management created a metric called cash flow yield to employees, which measures how much free cash flow is used to offset dilution.19 Their analysis found the median free cash flow yield to employees was 10.8% at the 100 largest non-financial S&P 500 companies. The median company’s employees take .6% of free cash flow – in the aggregate $150 billion dollars annually.20

As a result,

traditional valuation metrics such as free cash flow yields might be distorted.21

At least one director was concerned that a routine dilution offset program might inadvertently cause the company to spend more on compensation than it intends to: “If we are using hard dollars to offset stock dilution, we should treat those hard dollars as a compensation expense. Otherwise we are not recognizing what we are actually spending to compensate our people.”

Buybacks to alter a company’s capital structure

Successful when The company borrows and buys a sufficient number of shares to create a new, desired capital structure

Key factors Financing and tax rates, credit rating, offshore funds

The fourth motivation that directors mentioned for buyback programs was altering a company’s capital structure. This is typically about excess capacity, not excess capital. The company may take on debt to fund a buyback to achieve a new capital structure target.

Tax policy may indirectly lead to more buybacks by allowing a company with substantial offshore funds to generate returns for shareholders without repatriation taxes.22

Companies cannot use offshore earnings to repurchase shares directly, but corporations can leverage those earnings to drive down interest rates on debt used to fund

buybacks.23 Corporations can engage in inexpensive borrowing “because creditors know that the unrepatriated earnings can be tapped at any time.”24 For example, according to the Center for American Progress, Apple borrowed $17 billion in 10-year corporate bonds – the largest bond offering in American history – at an after-tax cost of 1.57%, 10 basis points lower than 10-year Treasuries.25

19 Bolko Hohaus, “Share Buybacks and Employee Stock Options,” CESifo Group Munich, 79.

20 Ibid., 80.

21 Ibid., 80.

22 David Benoit, “A Case for Leveraged Recaps: Stock Gains,” Wall Street Journal, May 13, 2013.

23 Kitty Richards and John Craig, “Offshore Corporate Profits: The Only Thing ‘Trapped’ is Tax Revenue,” Center for American Progress, January 9, 2014.

Buybacks and the board | 17IRRC Institute and Tapestry Networks

Directors who have considered a leveraged recapitalization are keenly focused on the company’s credit rating. These are transactions that, as one director emphasized, “fundamentally change the risk profile of the enterprise.” Executing requires the company to consider “whether we can afford to move from BB to BBB in our industry and what the shift would mean for the company.” Another director shared that activists “have a different risk profile. They are coming at us wondering why we need to have an A rating, telling us we can put a lot of debt on the balance sheet and be fine.”

These types of buybacks were the least common and most highly scrutinized, interviewed directors said. “The decision of whether the balance sheet has too much cash and whether giving money back makes sense is up to the board, and the board will be held accountable,” one said.

One director emphasized that board members “are the last guardians against bankruptcy. We cannot allow excess returns to create too much risk.” Another urged

directors to maintain their vigilance over this subject. Reflecting on personal experience, this director said, “In absolutely every case, the directors have taken a much more conservative position than the management team. Management teams seem less anxious about the risks of the balance sheet being overstrained and stressed.”

Buybacks and the board | 18IRRC Institute and Tapestry Networks

Are buybacks jeopardizing growth?The story

A common opinion today is that public companies’ high level of capital return jeopardizes economic growth. As mentioned earlier, BlackRock’s Larry Fink expressed this concern in a February 2016 letter to CEOs, warning that capital return shouldn’t come “at the expense of value-creating investment.” Similarly, the Organization for Economic Cooperation and Development’s 2015 Business and Finance Outlook lamented

the amount of US earnings devoted to buybacks instead of investment: “For general industries dividends and buybacks are running at a truly remarkable pace; even faster than capital expenditure itself in recent years. There has been plenty of scope to increase capital spending, but instead firms appear to be adjusting to the demands of investors for greater yield (dividends and buybacks).”26

Capital return has become a political issue as well, with critics linking buybacks to underinvestment and wage stagnation. Senators Elizabeth Warren (D-MA) and Tammy Baldwin (D-WI) have called on the Securities and Exchange Commission to investigate share buybacks. In a 2015 letter to SEC chair Mary Jo White, Sen. Baldwin wrote, “Stock buybacks use profits to purchase a company’s own stock instead of investing in the worker training, research, or innovation necessary to promote long-term growth ... In the past, this money went to productive investments in the form of higher wages, research and development, training, or new equipment. Today, cash is being extracted from companies and placed on the sidelines.”27

Some investment professionals are also concerned that capital return might imperil a

company’s growth prospects. In IR Magazine’s 2016 Investor Perception Study, 41% of buy-side respondents and 25% percent of sell-side respondents said yes to the question, “Do you think companies are sacrificing long-term organic growth and increasing wages to do buybacks?”28

The research: Investment activity

According to a 2015 McKinsey report, “On an absolute basis, US-based companies have increased their global capital investments by an inflation-adjusted average of 3.4 percent annually for the past 25 years – and their US investments by 2.7 percent. That exceeds the average 2.4 percent growth of the US [gross domestic product].”29

26 OECD Business and Finance Outlook 2015 Paris: OECD Publishing, 2015, 48; emphasis added.

27 Tammy Baldwin letter to Mary Jo White, Washington, DC, April 23, 2015.

28 Laurie Havelock, “Buybacks: Why Buy-Siders and Sell-Siders Disagree,” IR Magazine, April 15, 2016.

Buybacks and the board | 19IRRC Institute and Tapestry Networks

Separate research by Fidelity found that companies were able to finance both capital return and productive growth.30 Fidelity’s Rossi has argued that so long as capital expenditure runs consistently above depreciation, the company’s payout policy does not endanger its future growth.31 In the United States, the capital expenditure to depreciation ratio is 1.2 – which Rossi considers “a healthy level of reinvestment, capable of sustaining earnings growth in future years.”32

The McKinsey research found a decline only in the level of capital expenditures relative to cash flows, which fell from roughly 75% in the 1990s to 57% in the past three years.33

McKinsey’s report concluded that comparing historical capital expenditures to cash flows was flawed because of a shift in the US away from capital-hungry industries. In an industry-based analysis of aggregate US economic data from 1989 to 2014, McKinsey found relatively stable levels of capital expenditure by industry. In that time frame, though, the makeup of after-tax operating profit shifted dramatically away from capital-hungry industries to technology, pharmaceuticals, and other less capital-intensive industries.

34

30 Rossi, “Companies Can Invest and Conduct Buybacks.”

Buybacks and the board | 20IRRC Institute and Tapestry Networks

The research: Bias against investment

Even if investment activity is stable relative to historical practice, is it optimal? Several studies have demonstrated a reluctance on the part of public companies to undertake

net present value (NPV) positive projects. One reason is risk aversion. A report by McKinsey found that executives “demonstrated extreme levels of risk aversion regardless of the size of the investment, even when the expected value of a proposed project was strongly positive. Specifically, when presented with a hypothetical investment scenario for which the expected net present value would be positive even at a risk of loss of 75 percent, most respondents were unwilling to accept it on those terms. Instead they were only willing to accept a risk of loss from 1 to 20 percent – and responses varied little, even when the size of the investment was smaller by a factor of 10.”35

Another reason is the effect these NPV positive projects would have in the short term. A survey of 401 financial executives found that a majority of managers would avoid initiating an NPV positive project if it meant falling short of the current quarter’s consensus earnings.36 Over 75% of that sample would give up value to smooth economic earnings.

One can also question if companies are accurately determining if a project is NPV positive. A 2015 comparison of investment decisions of public and private companies in the United

States found that private firms invested more and that public-firm managers do not believe that investors properly value long-term projects.37

An earlier study of US and UK

companies found that there was substantial “excess discounting” of future cash flows. One-year-ahead cash-flows are discounted 5-10% more than is rational. The discounting is even more striking over longer periods: “Cash-flows 5 years ahead are discounted at rates more appropriate 8 or more years hence; 10 year ahead cash-flows are valued as if 16 or more years ahead; and cash-flows more than 30 years ahead are scarcely valued at all.”38

The research: Relationship between buybacks and investment

There is a correlation between revenue growth, capital expenditures (CapEx), and share buyback growth. A 2016 study by Pay Governance found that higher revenue growth was associated with higher CapEx and lower buyback activity, and lower revenue growth

35 Tim Koller, Dan Lovallo, and Zane Williams, “A Bias Against Investment?” McKinsey & Company, September 2011, and “Overcoming a Bias Against Risk,” McKinsey & Company, August 2012.

36 John Graham, Campbell Harvey, and Shivaram Rajgopal, “The Economic Implications of Corporate Financial Reporting,”

(SSRN, January 11, 2005).

37 John Asker, Joan Farre-Mensa, and Alexander Ljungqvist, “Corporate Investment and Stock Market Listing: A Puzzle?”

Review of Financial Studies 28, no. 2, February 2015.

38 Andrew G. Haldane and Richard Davies, “The Short Long,” speech to 29th Société Universitaire Européene de Recherches Financières Colloquium: New Paradigms in Money and Finance? Brussels, May 2011, 1.

A majority of managers would avoid initiating an NPV positive project if it meant falling short of the current quarter’s consensus earnings.

Buybacks and the board | 21IRRC Institute and Tapestry Networks

correlated with lower CapEx and higher buyback activity.39 There was no meaningful

difference in median annualized total shareholder return (TSR) for companies with higher buyback activity/lower growth and CapEx, and lower buyback activity/higher growth and CapEx. Although correlation is not causation, it is possible that – as the authors note – “share buyback capital strategies are a response to weak revenue growth opportunities.”40

A recent study found that companies would cut investments at the same time that they (1) completed a buyback program and (2) avoided a near-miss of an EPS forecast. A paper in the Journal of Financial Economics (JFE) noted that companies that narrowly miss analyst EPS consensus were significantly more likely to repurchase shares than companies that beat their EPS forecasts by a few cents.41 These repurchases were often accompanied by decreased employment, CapEx, and R&D in the four quarters following EPS-induced repurchases relative to companies who just met EPS forecasts.42

Companies

who beat EPS forecasts have a positive and significant cumulative abnormal return around the earnings announcement. Those that cut some type of real investment in the same quarter in which they beat their EPS have 0.23% lower stock performance than companies who do not cut investment.43 One conclusion is that the market is aware that some companies may sacrifice investments (even valuable ones) to finance repurchases.

Director perspectives

Very few interviewed directors thought that the pressure to return capital to shareholders jeopardized company growth. Many expressed views in agreement with the director who said, “I am not aware of any company turning down a good business opportunity to buy back stock.”

As an initial matter, directors were clear that a company should rarely invest all of its earnings. One remarked, “If you’re generating a ton of cash that means you have a great business model. That does not mean that you’ll have opportunities to deploy that cash through acquisitions or internal growth.” Many directors said that in a low-growth, low-interest-rate environment, it was highly unlikely that companies would be unable to fund any good investment opportunities. One director said, “The low cost of debt in a low-growth environment cannot be underestimated as a driver of buybacks. There is too much cash chasing too few opportunities, especially domestically.”

39 Ira Kay, Blaine Martin, and Chris Brindisi, “Myths and Realities: Assessing the True Relationship Between Executive Pay, Share Buybacks, and Managerial Short-Termism,” Pay Governance, ViewPoint on Executive Compensation, January 13, 2016, 4.

40 Ibid., 5.

41 Heitor Almeida, Vyacheslav Fos, Mathias Kronlund, “The Real Effects of Share Repurchases,” Journal of Financial Economics, June 2015, 1.

Buybacks and the board | 22IRRC Institute and Tapestry Networks

Several directors shared that they were more concerned that companies would squander investment dollars chasing growth. “I am fearful of excessive CapEx as opposed to too little,” one director said. “Companies in general will do anything to invest in growth – it is the bright shiny object they all chase – that they take all kinds of risky bets,” another

director noted.

Although in the minority, a few directors did cite some instances of buybacks or other

capital return which interfered with making appropriate investments. A very few even had experience with repurchase programs that they thought were done, as one director said, “at the expense of other options that made sense.” The other directors who were

concerned about the level of investment based it on a perception of what was happening at other companies based on short-term pressure and risk aversion. “The importance of the quarterly results is an area of concern. It makes it difficult to make bigger investments that are more difficult to forecast, like investments in new plants or technology. It is a little easier to justify acquisitions. It is easiest to justify buybacks,” one director said.

Are buybacks and depressed wages related?

Directors did not see a direct relationship between buybacks and employee wages. The labor cost needed to execute strategy is decided long before determining how much capital to return to shareholders.

“We do not view the desirability of buybacks against the desirability of raising wages. Wage discussions come much earlier than discussions about returning capital. Our first objective is to run the business well and invest what we need to invest, on wages and everything else. If we get wages wrong, employee turnover will be too high and could put us out of business.”

“The decision processes for increasing wages or doing a stock buyback are totally different. Companies gauge the competiveness of your products in market, and labor rates are part of that. If you can’t compete, you can’t survive.”

“It’s absurd to link wages and buybacks.”

Buybacks and the board | 23IRRC Institute and Tapestry Networks

“The company’s growth and future is first; buybacks are second.”

“Reinvest in business first for profitable growth. [It is] only when you reach the phase in your life cycle when you don’t need all the cash and never will that you decide on a return of capital to shareholders.”

“[Buybacks] are a tool in the tool bag but don’t substitute for organic growth of your business – you should be concerned about that first.”

“Management, on balance, would rather deploy capital to grow their business.”

“There is no loss of enthusiasm or support for investing for growth.”

“The whole idea is to capture shareholder money and put it to work productively. The question is, are you operating the business well and generating good, solid opportunities for growth? … Buybacks come about because you have too much money to deploy in the company.”

“Investment is always preferable to capital return, but you cannot just hoard cash for some uncertain possibility.”

“Nobody should cut their CapEx program to do a buyback, so long as the CapEx is reasonable and appropriate for business conditions.”

“Companies sometimes see that they cannot deploy capital in a way that can meet their growth targets. If that’s the case, a buyback makes sense.”

“It’s funny – there are very famous letters from large investors encouraging management to seek out growth and take on more operating risks, but in my experience investors are more worried that management will pursue growth projects and take on too much risk and screw things up.”

“The vast majority of investors don’t want you to chase riskier investments or investments outside of your wheelhouse for fear that you will destroy value.”

Director views about the relationship between capital return and company growth

“I have seen cases where we do buybacks at the expense of other options that make sense.”

“There is a hesitancy to take good risk in this environment. There is uncertainty with all capital options except for buybacks; it is arithmetic and easy. That risk aversion is a real issue.”

“The importance of the quarterly results is an area of concern. It makes it difficult to make bigger investments that are more difficult to forecast, like investments in new plants or technology. It is a little easier to justify acquisitions. It’s easiest to justify buybacks.”

“It can be all too easy for companies to feel like we should deliver near-term return and fail to invest.”

Contrary director views about the relationship between capital return and company growth

Buybacks and the board | 24IRRC Institute and Tapestry Networks

Do repurchase programs unjustly enrich senior executives?The story

Some critics allege that buybacks increase senior executives’ pay in two independent ways, both of which are unwarranted:

1. Share buybacks improve a company’s earnings per share (EPS). Improving EPS may result in higher payouts under annual or long-term incentive programs. This is particularly objectionable if the incentive programs are designed to reward “real” or “sustainable” growth and instead reward “financial engineering.”

2. Share buybacks improve the company’s share price, at least in the short term. Because so much executive pay is in forms such as options or restricted stock tied to the company’s share price, executives may be rewarded without creating any “real” value.

The research: EPS

EPS is a common metric in executive compensation plans; one recent study found that 31% of annual and 22% of long-term plans depended, in part, on EPS.44

A separate

analysis by Reuters found that 255 S&P 500 companies reward executives in part based on EPS.45

Executive compensation metrics and vehicles are correlated with different levels of buyback activity. The 2016 Pay Governance study found that using EPS as a metric in the annual incentive plan and using stock options as a compensation vehicle are correlated with larger share buybacks.46

The earlier-cited JFE paper that found a relationship between repurchase activity and narrow EPS misses ultimately found that “EPS-induced repurchases are on average not detrimental to shareholder value or subsequent performance.”47

44 Rourke, ”2016 Trends and Developments in Executive Compensation,” 13, 21.

45 Karen Bretell, David Gaffen, and David Rohde, “Stock Buybacks Enrich the Bosses Even When Business Sags,” Reuters Investigates, December 10, 2015.

46 Kay, Martin, Brindisi, “Myths and Realities: Assessing the True Relationship Between Executive Pay, Share Buybacks, and Managerial Short-Termism,” 4. The study notes that companies that used EPS and stock options had marginally higher annualized median TSR than those that used neither EPS nor options (18.1% to 17.3%).

47 Heitor Almeida, Vyacheslav Fos, Mathias Kronlund, “The Real Effects of Share Repurchases,” Journal of Financial Economics, June 2015, 1.

Buybacks and the board | 25IRRC Institute and Tapestry Networks

When you set executive compensation targets, you have a pretty good idea of what the current buyback program is going to add to EPS growth.

The research: share price

Attempting to determine the reason behind the increase in share repurchase activity, Professor William Lazonick wrote, “Corporate executives give several reasons ... But none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay, and in the short term buybacks drive up stock prices.”48

The largest components of total executive compensation “are realized gains from stock-based pay in the forms of stock-option grants and stock awards. In 2013 the combined gains from exercising stock options and from the vesting of stock awards totaled 80.9% of the total compensation of the 500 highest-paid executives, and in 2014 these two components were 77.6% of the total.”49

Buybacks are associated with share price growth.50 Some of this is because holding

excess cash raises the cost of capital; some of this is due to supply and demand in the share marketplace. The primary reason may be the signaling effect. A buyback may be interpreted as proof that the company believes its share price is undervalued. Buyback programs also minimize the risk that the company will spend its money on projects with a negative NPV, causing investors to value a company more highly because it is less likely that management will misuse excess funds.51

Buybacks that are the difference between a company making or missing market EPS expectations also may improve the share price. The JFE paper noted that companies that

narrowly miss analyst EPS consensus were significantly more likely to repurchase shares than companies that beat their EPS forecasts by a few cents.52

48 William Lazonick, “Profits Without Prosperity,” Harvard Business Review, September 2014.

49 William Lazonick, “Cash Distributions to Shareholders (2005–2014) & Corporate Executive Pay (2006–2014),” theAIRnet,

August 2015.

50 Robert Comment and Gregg Jarrell, “The Relative Signalling Power of Dutch-Auction and Fixed-Price Self-Tender Offers and Open-Market Share Repurchases,” Journal of Finance, 1991, Volume 46, Number 4, 1243-71; and Theo Vermaelen, “Common Stock Repurchases and Market Signaling: An Empirical Study,” Journal of Financial Economics, 1981, Volume 9, Number 2, pp. 138-83, cited in Richard Dobbs and Werner Rehm, “The Value of Share Buybacks,” McKinsey Quarterly, August 2005.

51 Richard Dobbs and Werner Rehm, “The Value of Share Buybacks,” McKinsey Quarterly, August 2005.

52 Almeida, Fos, Kronlund, “The Real Effects of Share Repurchases,” 3.

“When you set executive compensation targets, you have a pretty good idea of what the current buyback program is going to add to EPS growth”

Buybacks and the board | 26IRRC Institute and Tapestry Networks

Director perspectives

Challenges associated with EPS can be mitigated

Several directors were quick to note that EPS is not a metric in all pay plans and that there was no concern that EPS incentivized bad behavior at their companies. A few went further, saying that EPS was a “flawed metric” and that other profit measures better linked pay and performance.

Those who do or did use EPS were not concerned that management was incentivized to make bad decisions for two reasons:

• Targets factor in projected buyback EPS growth. EPS and other targets are typically set after factoring in expected buyback activity, interviewed directors said. “When you set executive compensation targets, you have a pretty good idea of what the current buyback program is going to add to EPS growth. You simply set your targets reflective of that. That is factored into the executive compensation targets to make sure you won’t overpay. It’s a very legitimate concern of investors but it is one that is controllable. I do not think management should or will get credit,” shared one director.

• Unbudgeted buyback-related EPS growth can be adjusted out. A few directors noted

that their companies had adjusted compensation downward when targets were hit due to buybacks not expected at the time the targets were set. “I can think of a few examples of us adjusting downwards because of a repurchase,” one said. Many more directors said that their companies could do this if it were ever warranted.

Concerns about the link between pay and share price are misguided

Directors were not concerned that managers would benefit financially from stock buybacks when share prices improved – many said that was the purpose of their compensation plans. “Maximizing the value of the company is the objective of the board and management so it is perfectly normal to have compensation tied to the performance of the stock,” one director said. Another put it more bluntly: “If there are people out there who think it is wrong for management to get rich for increasing the value of the company, well then shame on them.”

Buybacks and the board | 27IRRC Institute and Tapestry Networks

Many criticisms of share buyback activity are actually criticisms of the shareholder value maximization theory most commonly associated with Michael C. Jensen and William Meckling.53 While many academics, politicians, and business leaders have critiqued the theory,

54 most interviewed directors believe that their primary job is to maximize shareholder value.

Directors do not share a common definition of “shareholder value maximization.” Noting that shareholders have different objectives and expected shareholding periods, it is practically impossible to make decisions that benefit all shareholders equally. While most measure shareholder value by looking at stock price, some look for measures based less

on external valuations and expectations.55

Most directors believe that they are obliged to maximize share value in “the long term,” with different (often not precisely defined) conceptions of how long that is, and the importance of interim, short-term results. Although many directors noted that the pressure for short-term results has never been greater, very few thought that individuals were financially incentivized to take steps that benefited the company’s short-term results at the expense of its long-term growth.56

Some directors said that the senior

executives with whom they worked were wired to create long-term growth. Others said that equity vehicles with lengthy holding periods incentivize management to make decisions that will benefit the company for the long term.

It is common practice for companies to require senior executives to hold a minimum number of shares (typically equal to 3-6 times annual salary), sometimes until or after retirement.57 Such policies can give directors comfort that their executives focus on the long term. “If you ask my CEO, he’s not concerned and has no financial incentive to think about what the share price will be next quarter. He’ll be rewarded if the share price is up four years from now,” one director said.

53 Michael C. Jensen and William Meckling, “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure,” Journal of Financial Economics, October 1976.

54 See, for example, Roger Martin, Fixing the Game, (Boston: Harvard Business School Publishing, 2011); Lynn Stout, The Shareholder-Value Myth (San Francisco: Berrett-Koehler Publishers, 2012); noting criticism of shareholder value maximization from current and former CEOs Jack Welch (GE), Jack Ma (Alibaba), Paul Polman (Unilever), John Mackey (Whole Foods), Xavier Huillard (Vinci Group), and Marc Benioff (Salesforce.com): Steve Denning, “Salesforce CEO Slams ‘The World’s Dumbest Idea’: Maximizing Shareholder Value,” Forbes, February 5, 2015; Raymond V. Gilmartin, “CEOs Need a New Set of Beliefs,” Harvard Business Review, September 26, 2011.

55 See Roger Martin, Fixing the Game.

56 But see earlier discussion of investment behavior, “Are buybacks jeopardizing growth?” pages 18-23.

57 Meridian Compensation Partners, 2015 Corporate Governance and Incentive Design Survey, 2015, 15.

Buybacks and the board | 28IRRC Institute and Tapestry Networks

There is room to improve communication about the relationship between buybacks and pay

There are compensation implications of share buyback programs, but a majority of directors think that boards effectively address them. However, how those mitigations are communicated, both within the company and externally, is another matter. In some cases, activity in the compensation committee may not be known to the full board; directors who were concerned about compensation implications typically did not serve on compensation committees. One director noted that compensation implications were not discussed at the full board level: “It can be unpopular to discuss compensation implications of buybacks. I expect those discussions are happening in the compensation committee and less often at the full board. I do not see the issues discussed as openly as I might like.” Another director echoed this concern, saying: “It is something that the compensation committee should be aware of and adjust for, but I don’t personally know what they’ve done.”

“Most companies have a compensation program that is based in part on long-term plans. You can level-set those – they should include expected buyback activity.”

“As a compensation chair, that would happen in my administration. We have an expected level of buyback activity. Any buybacks beyond do not count toward achieving targets.”

“Compensation issues are handled well in advance. Buybacks are not one-off events; they are part of plans. The compensation committee looks at expected buyback activity at the time metrics and targets are set and again when the final payments are decided.”

“When you set executive compensation targets, you have a pretty good idea of what the current buyback program is going to add to EPS growth. You simply set your targets reflective of that. That is factored into the executive compensation targets to make sure you won’t overpay. It is a very legitimate concern of investors but it is one that is controllable. I do not think management should or will get credit.”

“We factor buybacks into the EPS calculation for next year. It is never an issue.”

“If we do buybacks, we adjust our metrics for our buybacks, so it doesn’t hurt or help management.”

Director views about the compensation implications of buyback programs

Buybacks and the board | 29IRRC Institute and Tapestry Networks

“Most companies have buyback programs approved by boards that are not enough to move the needle to affect EPS.”

“We want the program to reward the things they can do to influence company value, whether or not it shows up in stock price.”

“I’m not worried about manipulating the long-term plan. I think long-term plans are designed to align management interest with long-term interest. Decisions that benefit short term over long term ultimately don’t benefit management.”

“Compensation plans tied to TSR signify that you are trying to get the stock price to go up. Maximizing the value of the company is the objective of the board and management so it is perfectly normal to have compensation tied to the performance of the stock.”

“If there are people out there who think it is wrong for management to get rich for increasing the value of the company, well then shame on them.”

“The challenge is that the compensation committee has to evaluate what growth is real, especially when using time comparisons with EPS – how much of each year’s EPS was based on inorganic growth?”

“I can think of a few examples of us adjusting downwards because of a repurchase.”

“I remember one big buyback and we modified the CEO’s compensation because of it.”

“In some cases - but very few, and even fewer materially - has the conversation about share repurchases been overshadowed by concerns by management compensation.”

“I would be uncomfortable if there were a lot of buybacks in a company that used EPS as a metric.”

“The average tenure of the CEO/CFO is very short. I think that there is a conflict to implement a strategy such that you will get a big bump in share price so that when you leave, you walk away wealthy.”

“The link between pay and buybacks isn’t of huge concern to me. It is something that the compensation committee should be aware of and adjust for, but I don’t personally know what they’ve done.”

“A buyback plan that is implemented subsequent to when performance targets are established could be a big issue, especially for longer term incentives. This is where the board’s responsibility to be diligent and represent the interest of shareholders should come in.”

“It can be unpopular to discuss compensation implications of buybacks. Expect those discussions are happening in the compensation committee and less often at the full board. I do not see the issues discussed as openly as I might like.”

Contrary director views about the compensation implications of buyback programs

Buybacks and the board | 30IRRC Institute and Tapestry Networks

Are buyback disclosures clear and effective?The majority of interviewed directors said that their boards have robust discussions with management about issues related to share repurchase decision-making – everything from the company’s strategic objectives and challenges to investment alternatives and investor preferences.

Coupled with the tremendous level of buyback activity and the spotlight from investors and governance observers on the so-called “repurchase revolution,” one might expect companies would articulate what factors were important to an announced buyback program. That is not often true.

A number of companies do not clearly communicate the level of director diligence and

oversight regarding capital return. A 2015 Reuters special report found that “fewer than 20 of the S&P 500 companies disclose in their proxies whether they exclude the impact of buybacks on per-share metrics that determine executive pay.”58 Some examples are contained in Appendix 3, pages 39-41.

One immediate benefit of such disclosure might be the avoidance of a shareholder proposal. This year, the AFL-CIO has submitted shareholder proposals at several companies that would require companies to exclude the effect of buybacks on executive pay metrics.59

Companies could go further, disclosing not only how buyback decisions are factored into

compensation, but also how buyback decisions are made. Disclosures often say precious little about the decision-making process or the rationale for a buyback program. Instead, typical disclosure is exceptionally high-level; as one proxy said, “We periodically evaluate repurchases as a means of returning capital to stockholders to determine when and if

repurchases are in the best interests of our stockholders.”60

Investors may want to know the primary purpose of a given company’s repurchase plan:

1. Is the primary goal to return capital,

2. Is the primary goal to invest in the company,

3. Is the primary goal to offset dilution, or

4. Is the primary goal to change the company’s balance sheet and risk profile?

Knowing the purpose of the program would enable investors and others to better evaluate whether board members have a philosophy relating to share repurchases that represents investors’ interests, and, over time, have a basis to judge the buyback’s success.

58 Karen Bretell, David Gaffen, and David Rohde, “Stock Buybacks Enrich the Bosses Even When Business Sags,” Reuters Investigates, December 10, 2015.

59 “Why the AFL-CIO’s 2016 Shareowner Reforms Are Vital for All Working People”, last accessed July 26, 2016.

Buybacks and the board | 31IRRC Institute and Tapestry Networks

“Not sure what we disclose about buybacks. I think we say something like, ‘We constantly look at capital allocation as board and management together.’”

“I think that far too many boards do not put enough legitimate explanation and discussion in the proxy. It is too abbreviated and brief. I’m very much in favor of upping the quality there generally, and buybacks in particular.”

“I think you need to explain how the company’s strategy is related to capital

structure and allocation. You cannot get too specific; don’t want to let too much proprietary info out, but you can do it effectively without sharing too much.”

“Investors will stand down if they understand what you are doing, but if they don’t, they can be a little noisy.”

“Companies need to be transparent about buybacks and other capital return. Maybe the annual investor day is a better opportunity to make the point [than a written disclosure].”

Director views about buyback disclosures

Buybacks and the board | 32IRRC Institute and Tapestry Networks

ConclusionsObservers and experts can use share buyback data to advance many theories about broader corporate phenomena. What appears as a criticism of share buybacks may actually be a criticism of short-termism, activism, shareholder value maximization theory, executive compensation, wage stagnation, or the competitiveness of the US economy. Buybacks have become a new battlefield for old corporate governance and finance wars.

This research provides no simple answers about why this is happening or whether the

growth in buyback activity is a good thing. It does provide information and nuance about how corporate directors think and act. Lurking beneath the surface of many complaints about buybacks is a belief that board members are not engaged in meaningful oversight

when authorizing repurchase programs. The board members interviewed for this report, without exception, demonstrated an earnest commitment to getting buyback decisions right. Indeed, interviewed directors offered four independent but related reasons why their companies might repurchase shares. A corollary to that finding is that board members and senior managers may support buybacks for diverse reasons and may

evaluate their success using different metrics.

Some opportunities for improvement did emerge from the research:

• When multiple committees and individuals have responsibilities for aspects of

buyback programs, those responsibilities should be stated directly and the outcomes

communicated clearly, internally and externally.

• Companies face criticism for rewarding senior executives for buyback programs. Explaining the relationship between buyback programs and executive pay – particularly the relationship between buybacks and metrics like EPS in short- and long-term plans – improves disclosure and demonstrates effective oversight.

• Disclosing the purpose of a buyback program, along with a short discussion of the

factors relevant to a given buyback program, would enable investors and others

to better evaluate the company’s philosophy relating to share repurchases and, over time, help them judge how successful buybacks have been relative to the goal(s) established.

Buybacks and the board | 33IRRC Institute and Tapestry Networks

Areas for future research

During the development of this report, we identified three areas for additional research:

• What do investors think? This research focuses on public company director attitudes

about share buybacks. More work is needed to understand exactly how investment professionals evaluate buyback programs.

• How much dilution is being offset? Should it be offset? Are buybacks masking a substantial transfer of corporate equity from outside investors to managers? What are the consequences of offsetting this dilution through share repurchase programs? We were struck by how universal was the assumption that dilution caused by equity-related compensation should be offset. Should it be in all cases?

• When comparing alternative investment options, what time horizons are most important to decision-makers? Not many directors were explicit about the period over which they evaluate the expected returns from buybacks or other uses of capital. More research on this subject is warranted.

Buybacks and the board | 34IRRC Institute and Tapestry Networks

About the authorRichard R.W. Fields is a principal at Tapestry Networks. Rich leads a number of corporate governance networks

and initiatives at Tapestry, including the Lead Director Network, the Compensation Committee Leadership Network, and a number of national and regional audit committee leadership networks. He is also co-chair of the Shareholder-Director Exchange and a principal architect of the SDX Protocol. Rich was one of four global winners of the Millstein Center for Global Markets and Corporate Ownership’s Rising Star of Corporate Governance Award in 2015.

AcknowledgmentsThis report began with a request from the IRRC Institute to discover how board members view share buyback activity.

Nearly everyone at Tapestry Networks provided support during the lengthy interview

and drafting process for this report. Extra special thanks are due to my chief research assistant, Amy Sampson; without Amy’s substantial support, this report would not have been possible. I would also like to thank Kate Cady for invaluable administrative support and Eric Shor for serving as a thought partner and interview leader.

Notwithstanding this extensive support, this report and its errors and omissions are mine and mine alone.

Buybacks and the board | 35IRRC Institute and Tapestry Networks

Appendix 1: Interviewed directors and affiliated public company boards61

• Barbara T. Alexander, Allied World Assurance Company Holdings, AG, Choice Hotels International Inc., QUALCOMM Incorporated

• H. Raymond Bingham, Cypress Semiconductor Corporation, Flextronics International Ltd., Oracle Corporation, TriNet Group, Inc.

• Frank J. Biondi Jr., Amgen Inc., Cablevision Systems Corporation, Seagate Technology plc, ViaSat Inc.

• Ralph F. Boyd Jr., Sandy Spring Bancorp Inc.

• Joseph R. Bronson, Jacobs Engineering Group Inc., Maxim Integrated Products, Inc., PDF Solutions Inc.

• Peter C. Browning, Acuity Brands, Inc., GMS, Inc., ScanSource, Inc.

• Mark Buthman, IDEX Corporation, West Pharmaceutical Services, Inc.

• Daniel A. Carp, Delta Air Lines, Inc., Norfolk Southern Corporation, Texas Instruments Inc.

• Vanessa C. L. Chang, Edison International, Sykes Enterprises, Incorporated, Transocean Ltd.

• Rodney F. Chase, Hess Corporation, Tesoro Corporation

• Jeffrey E. Curtiss, KBR, Inc.

• Erroll B. Davis, Union Pacific Corporation

• Henry T. DeNero, Western Digital Corporation

• Raymond V. Dittamore, QUALCOMM Incorporated

• David Wyatt Dorman, CVS Health Corporation, PayPal Holdings, Inc., Yum! Brands, Inc.

• William H. Easter, Baker Hughes Incorporated, Concho Resources, Inc., Delta Air Lines, Inc.

• David S. Engelman, Private Bancorp of America, Inc.

• Donald E. Felsinger, Archer Daniels Midland Company, Gannett Co., Inc., Northrop Grumman Corporation

• Robert L. Guido, Commercial Metals Company

• Ann Fritz Hackett, Capital One Financial Corporation, Fortune Brands Home & Security, Inc.

61 Board affiliations confirmed by http://capitaliq.com/, as of July 8, 2016, unless subsequently corrected by an interviewed director.

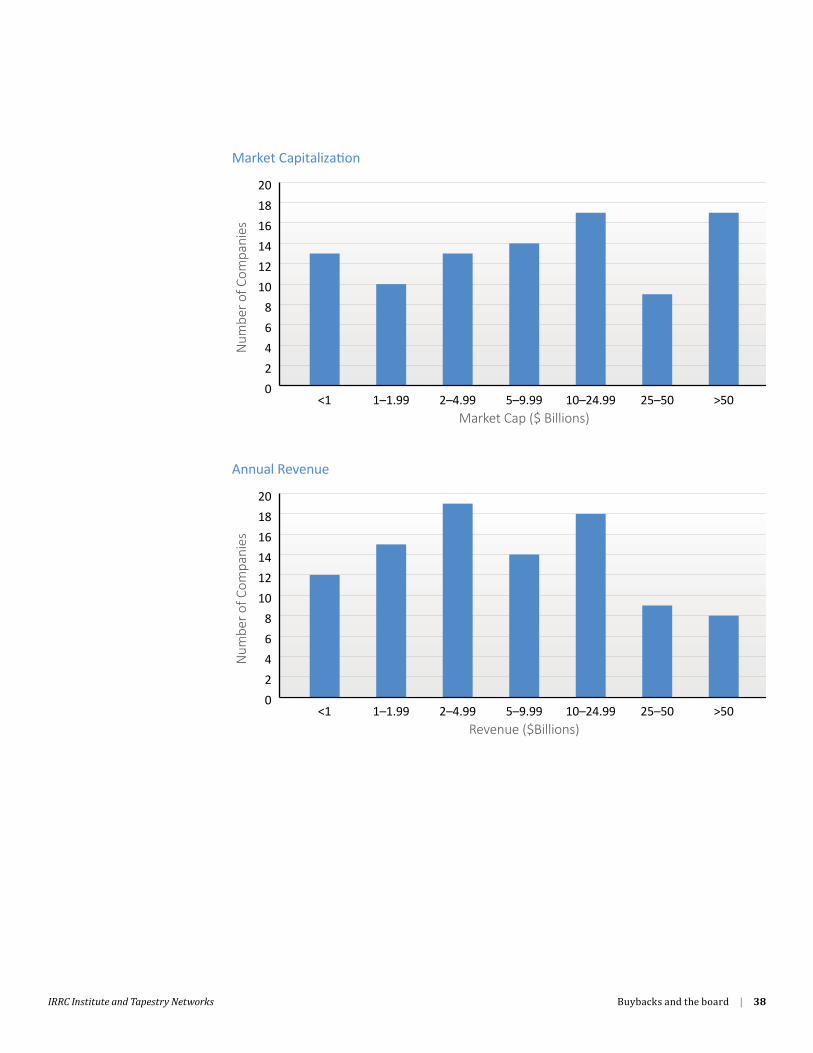

Appendix 2: Analysis of public companies affiliated with interviewed directors

Buybacks and the board | 38IRRC Institute and Tapestry Networks

0

2

4

6

8

10

12

14

16

18

20

25–5010–24.995–9.992–4.991–1.99<1 >50

Nu

mb

er o

f C

om

pa

nie

s

Revenue ($Billions)

Annual Revenue

Market Capitalization

0

2

4

6

8

10

12

14

16

18

20

25–5010–24.995–9.992–4.991–1.99<1 >50

Nu

mb

er o

f C

om

pa

nie

s

Market Cap ($ Billions)

Buybacks and the board | 39IRRC Institute and Tapestry Networks

Appendix 3: Buyback disclosure examplesFedEx62

“Stock Repurchase Program-Related Adjustments to EPS for LTI Plan Purposes. During