31

1 Buyers Research: Key Findings from acquirers of Consulting firms

1 Buyers Research: Key Findings from acquirers of Consulting firms

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S2

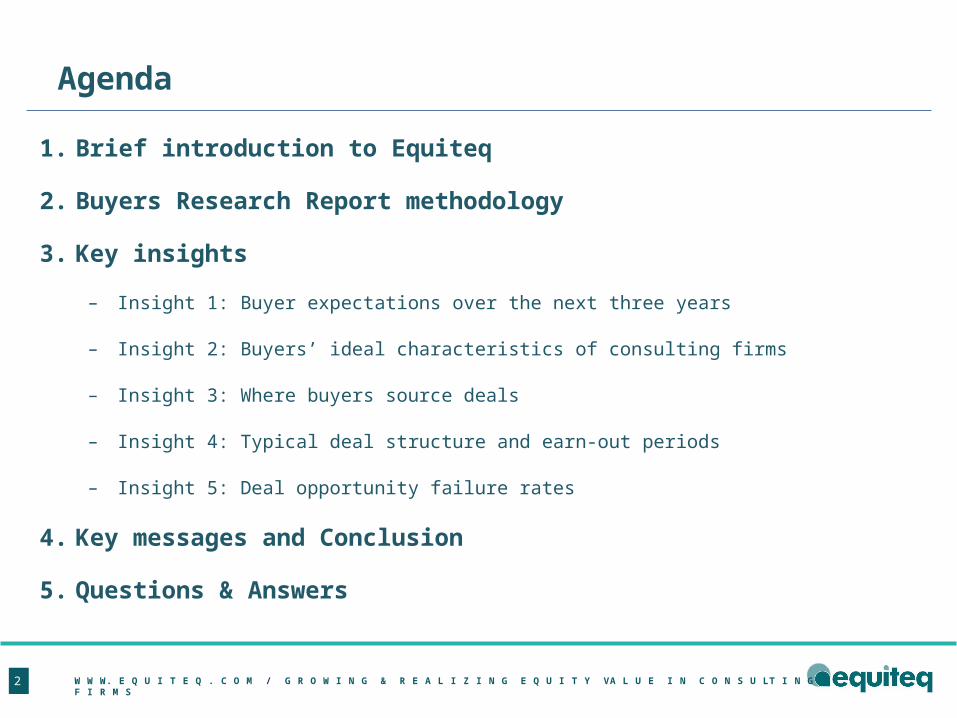

1. Brief introduction to Equiteq

2. Buyers Research Report methodology

3. Key insights

– Insight 1: Buyer expectations over the next three years

– Insight 2: Buyers’ ideal characteristics of consulting firms

– Insight 3: Where buyers source deals

– Insight 4: Typical deal structure and earn-out periods

– Insight 5: Deal opportunity failure rates

4. Key messages and Conclusion

5. Questions & Answers

Agenda

Equiteq

Introduction

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S4

Equiteq is a boutique M&A and strategic advisory firm wholly focused on the consulting sector

Our experts provide added value to our clients

Equiteq is based in London, with hubs in New York and Singapore. We are run by world class investment bankers, corporate finance experts and growth consultants in all three locations

• Community insights• Deal documentation• Buyer insight• M&A research• Unique IP

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S5

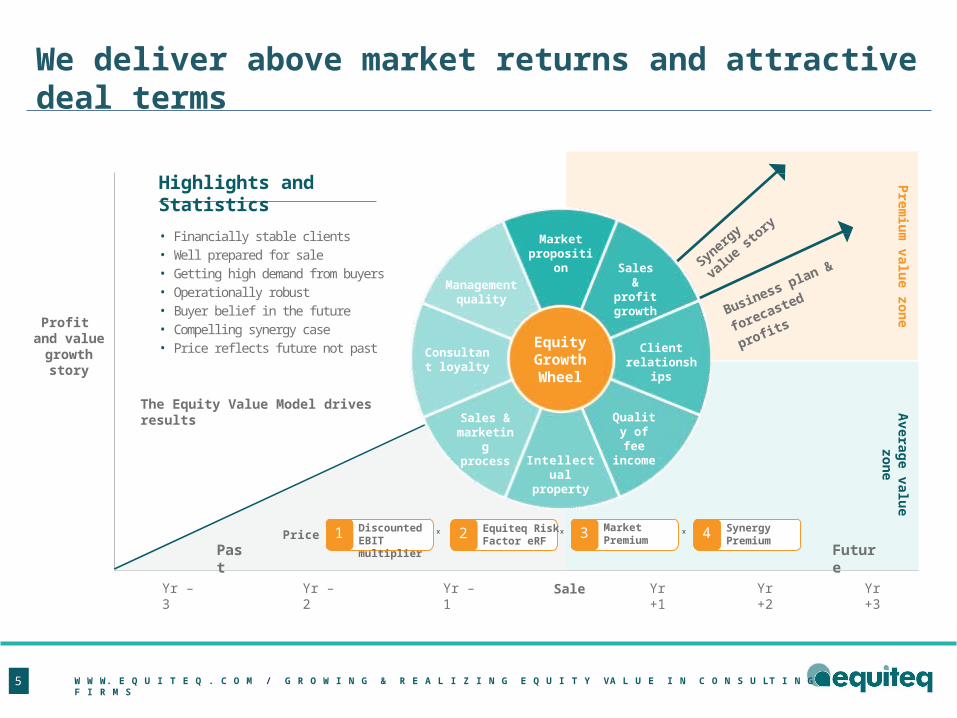

We deliver above market returns and attractive deal terms

Highlights and Statistics

• Financially stable clients• Well prepared for sale• Getting high demand from buyers• Operationally robust• Buyer belief in the future• Compelling synergy case• Price reflects future not past

The Equity Value Model drives results

Sale

Profit and value

growthstory

Yr –1 Yr +3Yr –2 Yr +2Yr –3 Yr +1

Syner

gy valu

e

story

Business plan &

forecasted profits

Past Future

Prem

ium

value zo

ne

Averag

e value zo

ne

Price = x x xDiscounted EBIT multiplier

1 MarketPremium3Equiteq Risk

Factor eRF2 Synergy

Premium4

EquityGrowthWheel

Market proposition

Intellectual property

Sales& profit growth

Management quality

Client relationships

Consultant loyalty

Quality of fee

income

Sales & marketing process

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S6

(Brand/Media Consulting)Acquired

SonaaEquiteq acted as lead advisor to 1HQ

on the transaction2013

(FS Consulting)Sold to

CordiumEquiteq and Corbett Keeling

advised on sale prep and sale2014

Equiteq is a global leader in consulting services M&A

8

(Management Consulting)Sold to

Chime Communications plcEquiteq and Corbett Keeling advised on

sale preparation and sale2012

(Management Consulting)Sold to

Baird CapitalEquiteq and Corbett Keeling advised on

sale preparation and sale2013

(Management Consulting)Initial Public Offering

Equiteq advised on equity growth and IPO preparation

2012

(Oil and Gas Consulting)Sold to

SLREquiteq advised on sale

preparation and sale 2014

(Technology Consulting)Sold to

Sagentia GroupEquiteq advised on business strategy

and equity growth2013

(Real Estate Advisory) Sold to

NavigantEquiteq advised on growth, sale prep and partnered with 7 Mile on the sale

2012

(HR Consulting)Sold to Capita

Equiteq advised on growth, sale preparation and sale

2013

(Technology Consulting)Acquired Hexarus

Equiteq advised Absoft on target acquisitions

2012

(Management Consulting)Sold to

FTI ConsultingEquiteq advised on sale preparation

and sale2013

(Management Consulting)Acquired

Polestar Group (USA)Equiteq acted as lead advisor on the

transaction2013

(Disputes Advisory)Sold to

Parentebeard, USAEquiteq and Paramax advised on sale

preparation and sale2013

(Market Research Consulting)Sold to

M-BrainEquiteq advised on sale preparation

and sale2014

(Int’n Development Consulting)Sold to AECOM

Equiteq advised on sale preparation and sale

2014

(Property Consulting)Sold to

EC HarrisEquiteq advised on sale preparation

and sale2014

(Engineering Consulting)Acquired

E3 ConsultEquiteq advised CDM on target

acquisitions2011

(Management Consulting)Sold to

Take SolutionsEquiteq advised on sale preparation

2011

(Management Consulting)Sold to

Sovereign CapitalEquiteq and Corbett Keeling advised

IMS on sale2010

(Management Consulting)Sold toBT plc

Equiteq advised on growth sale preparation and sale

2008

Methodology

Research

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S8

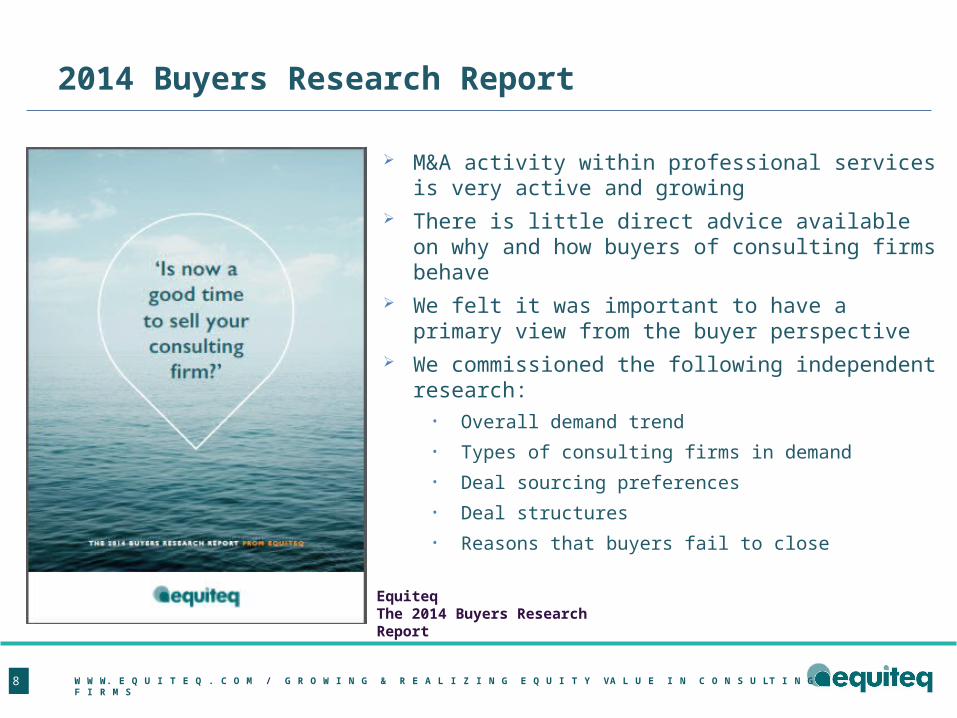

M&A activity within professional services is very active and growing

There is little direct advice available on why and how buyers of consulting firms behave

We felt it was important to have a primary view from the buyer perspective

We commissioned the following independent research:• Overall demand trend

• Types of consulting firms in demand

• Deal sourcing preferences

• Deal structures

• Reasons that buyers fail to close

EquiteqThe 2014 Buyers Research Report

2014 Buyers Research Report

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S9

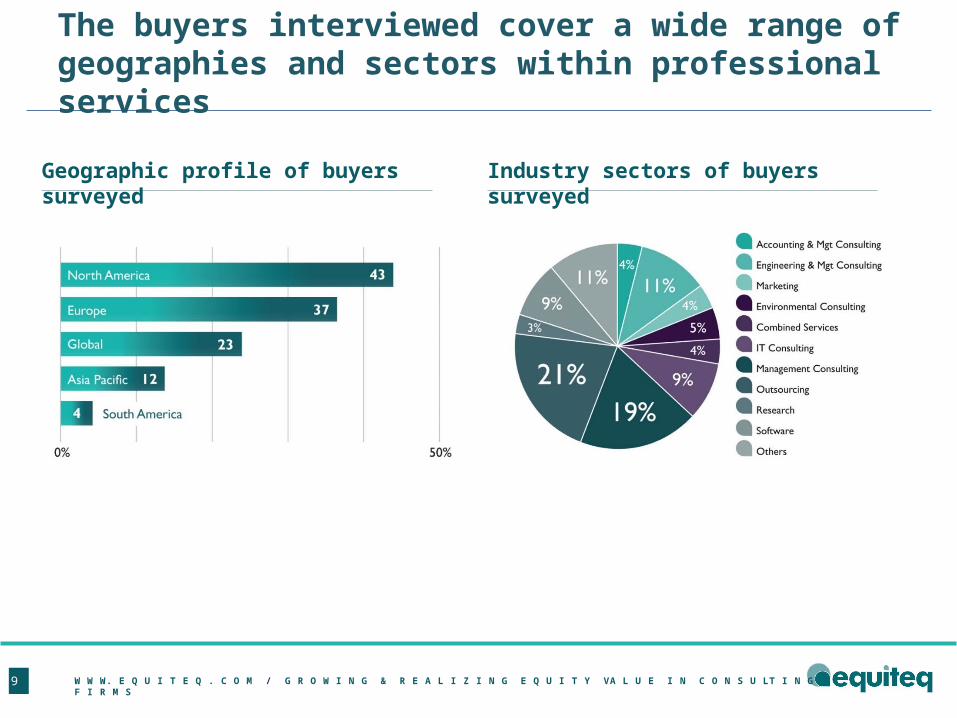

Geographic profile of buyers surveyed Industry sectors of buyers surveyed

The buyers interviewed cover a wide range of geographies and sectors within professional services

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S10

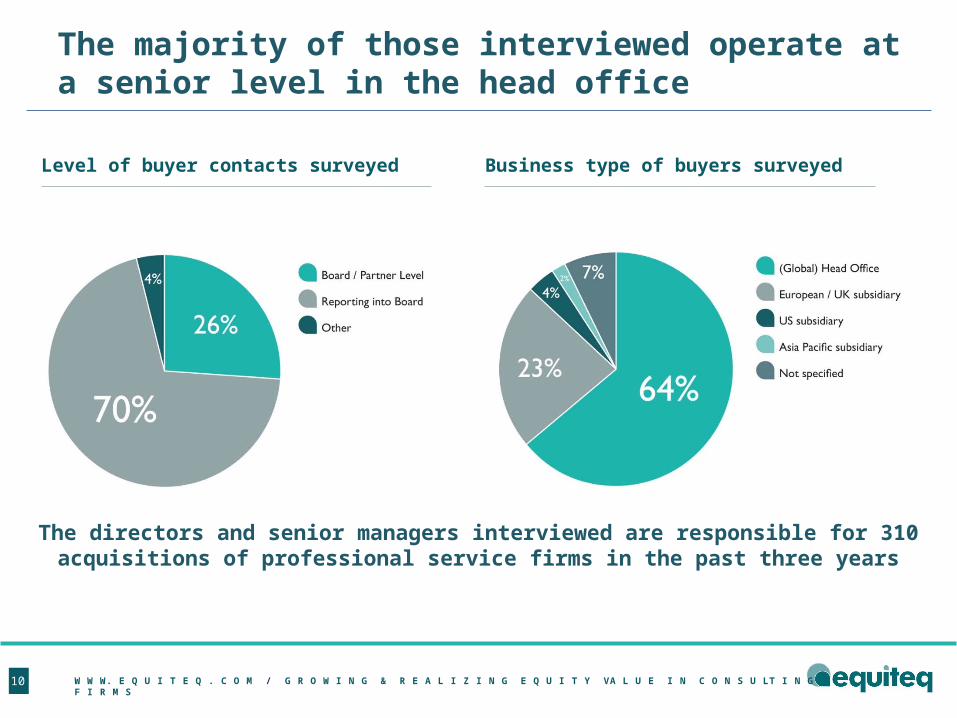

Level of buyer contacts surveyed Business type of buyers surveyed

The majority of those interviewed operate at a senior level in the head office

The directors and senior managers interviewed are responsible for 310 acquisitions of professional service firms in the past three years

Buyers’ expectations over the next three years

Insight 1

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S12

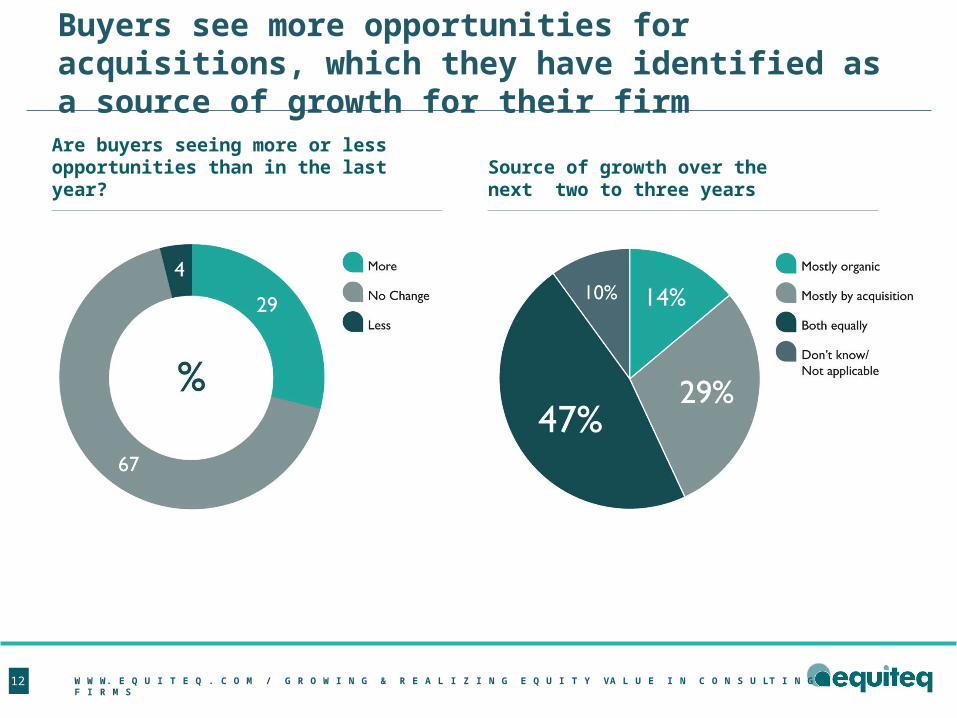

Source of growth over the next two to three years

Are buyers seeing more or less opportunities than in the last year?

Buyers see more opportunities for acquisitions, which they have identified as a source of growth for their firm

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S13

• Buyers of professional service firms expect a 6%+ increase in deals over the next 3 years

• Buyers anticipate acquiring an average of 3.3 professional service firms over the next 2-3 years

• The average buyer acquisition budget is $65M

• $90M for prolific buyers (5% of prolific buyers cited a budget of $200M or more)

• $35M for regular buyers

• Buyers are looking to do more deals

• We are currently in a strong market for sellers – a good time to be thinking about an exit

• Sellers must be able to demonstrate standalone value and synergy

Key Findings

What this means for sellers

The acquisition appetite reflects favourably on sellers

“We absolutely want to accelerate our acquisitions both in terms of size and numbers because we

are quite cash rich”

“Since the financial crisis, it’s become more obvious who the good players are and they tend

to be a lot more expensive!”

Buyers’ ideal characteristics for consulting firms

Insight 2

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S15

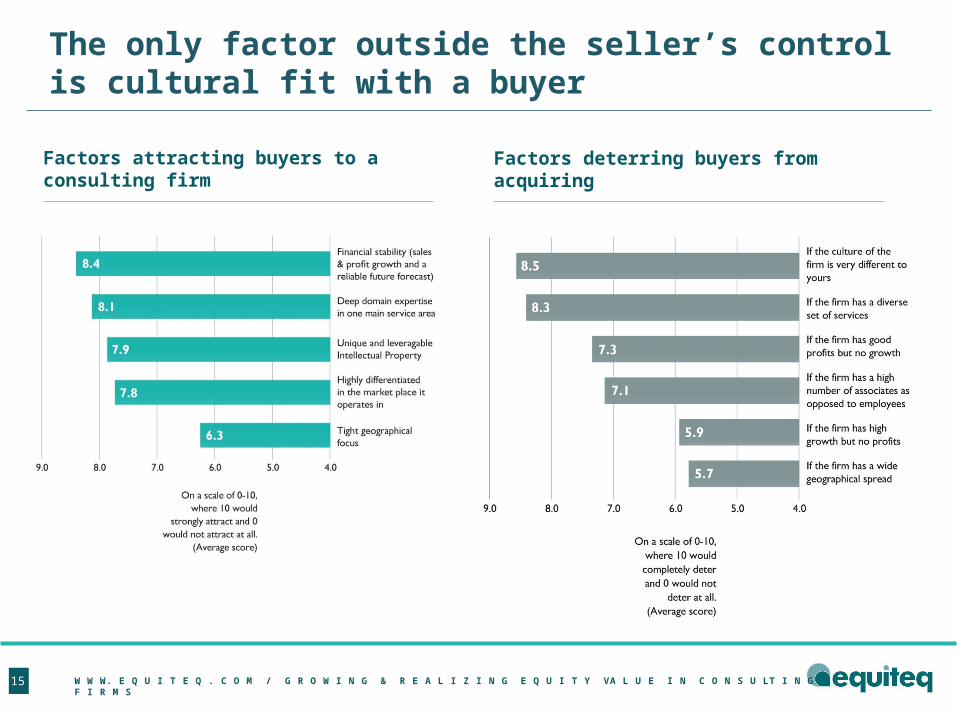

Factors attracting buyers to a consulting firm Factors deterring buyers from acquiring

The only factor outside the seller’s control is cultural fit with a buyer

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S16

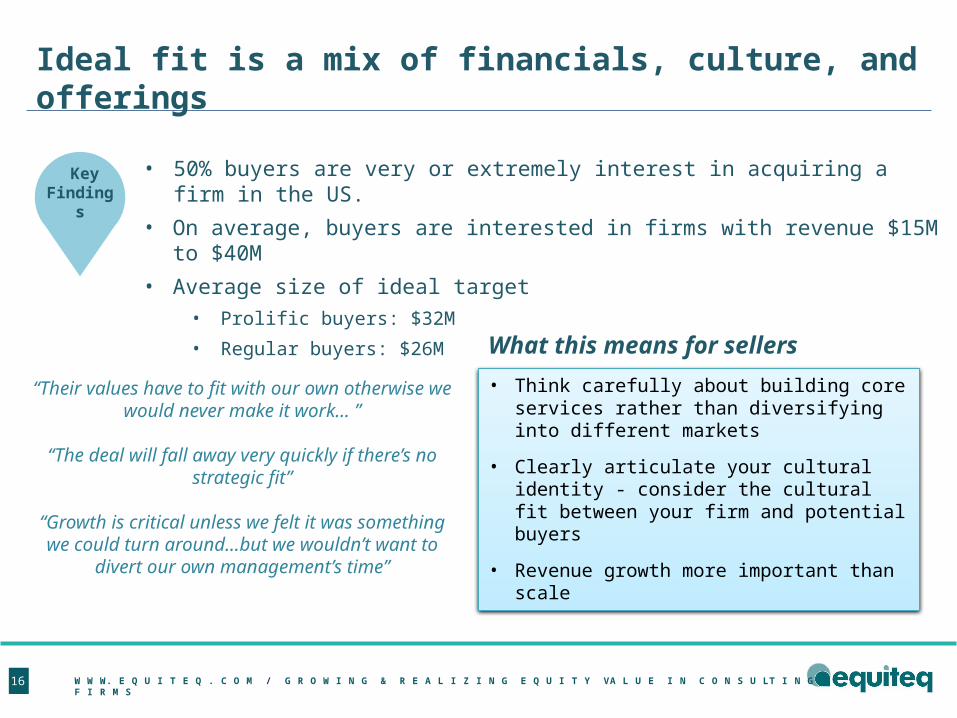

• 50% buyers are very or extremely interest in acquiring a firm in the US.

• On average, buyers are interested in firms with revenue $15M to $40M

• Average size of ideal target

• Prolific buyers: $32M

• Regular buyers: $26M

• Think carefully about building core services rather than diversifying into different markets

• Clearly articulate your cultural identity - consider the cultural fit between your firm and potential buyers

• Revenue growth more important than scale

Key Findings

What this means for sellers

Ideal fit is a mix of financials, culture, and offerings

“Their values have to fit with our own otherwise we would never make it work… ”

“The deal will fall away very quickly if there’s no strategic fit”

“Growth is critical unless we felt it was something we could turn around…but we wouldn’t want to divert our

own management’s time”

Where buyers source deals

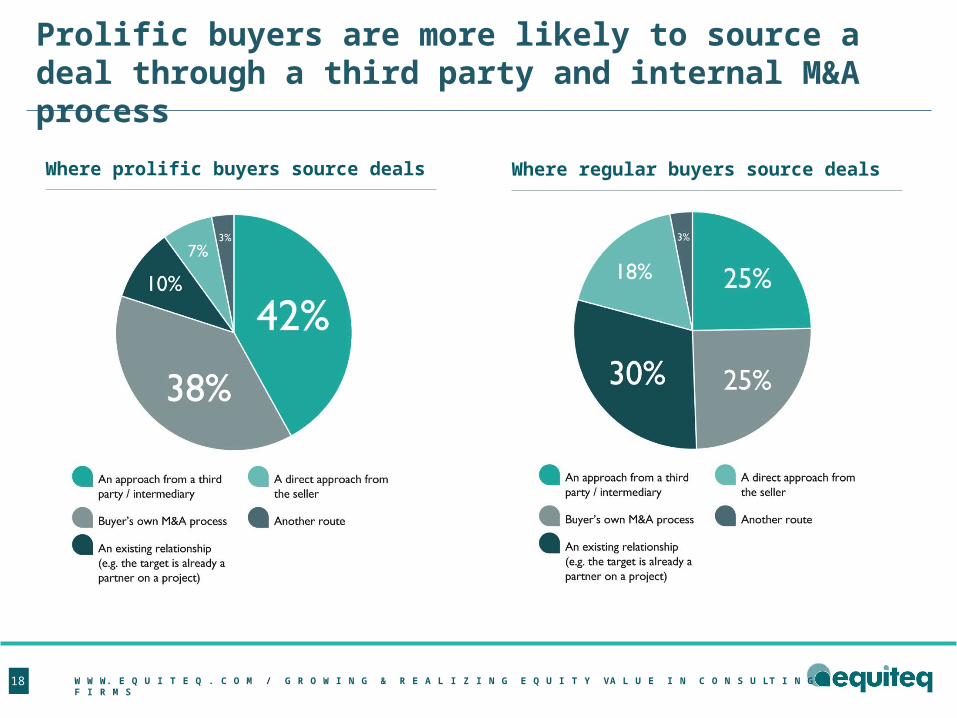

Insight 3

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S18

Where prolific buyers source deals Where regular buyers source deals

Prolific buyers are more likely to source a deal through a third party and internal M&A process

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S19

• It is not easy to get through the early filtering rounds

• Even more difficult to initiate a secondary approach to the same buyer

• It is important to understand each buyer’s process

Key Findings

Buyers have different approaches to sourcing deals.It is important to tailor your strategy

What this means for sellers

• Prolific buyers source 42% of their acquisition opportunities via third parties and 38% via their internal M&A team.

• Even buyers with M&A operations put the intermediary route as the most effective source of deals

• Regular buyers tend to rely on their existing relationships with acquisition targets as their best deal source

“Direct approaches are very, very rare. It almost all comes from our own activity or from third

parties.”

“Intermediaries definitely help…they are a sort of filtering process.”

Typical deal structures and earn-out periods

Insight 4

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S21

On what targets do buyers base earn-outs?

Gross Margin / Profit is the most common earn out metric

Proportion of earn-outs that hit target

Most buyers focus on revenue or gross margin to drive growth

Earn-outs are typically structured to be mostly achievable

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S22

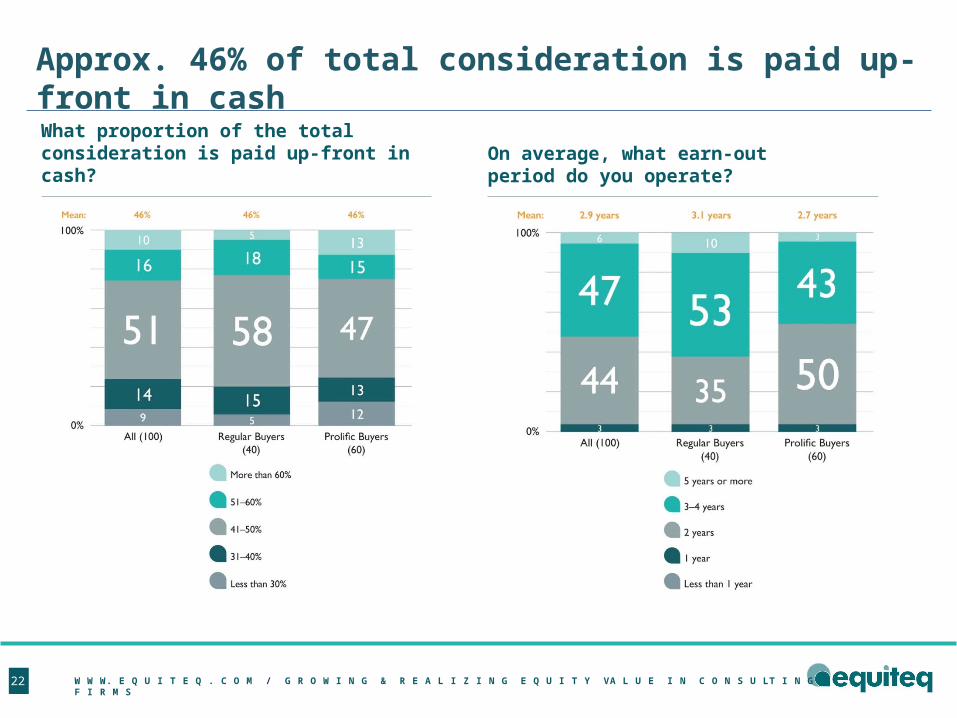

What proportion of the total consideration is paid up-front in cash?

On average, what earn-out period do you operate?

Approx. 46% of total consideration is paid up-front in cash

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S23

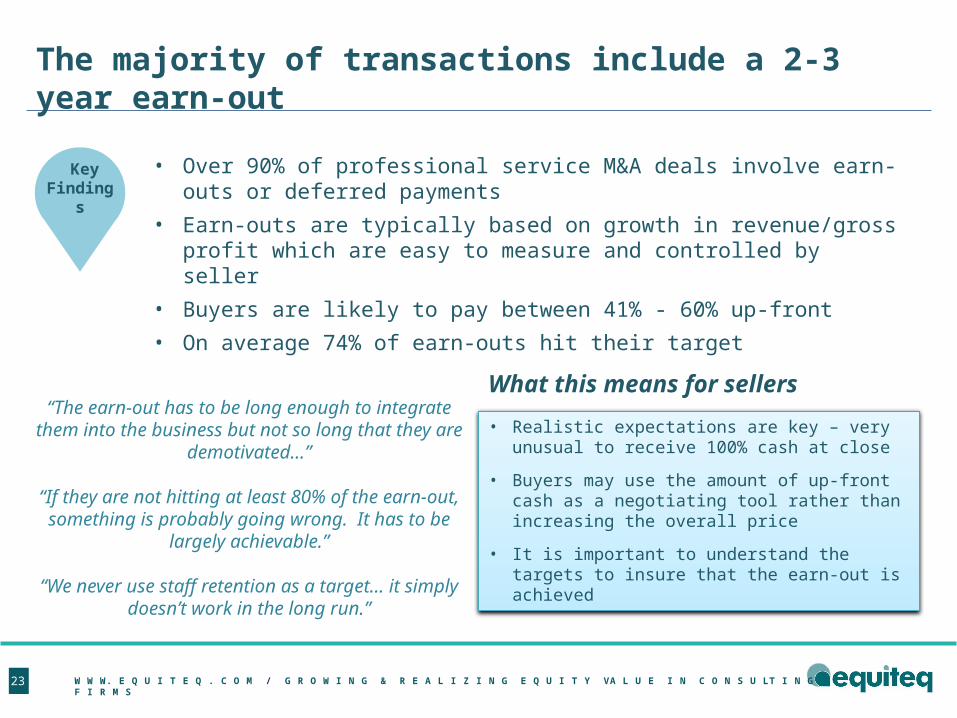

• Over 90% of professional service M&A deals involve earn-outs or deferred payments

• Earn-outs are typically based on growth in revenue/gross profit which are easy to measure and controlled by seller

• Buyers are likely to pay between 41% - 60% up-front

• On average 74% of earn-outs hit their target

• Realistic expectations are key – very unusual to receive 100% cash at close

• Buyers may use the amount of up-front cash as a negotiating tool rather than increasing the overall price

• It is important to understand the targets to insure that the earn-out is achieved

Key Findings

The majority of transactions include a 2-3 year earn-out

What this means for sellers“The earn-out has to be long enough to integrate

them into the business but not so long that they are demotivated…”

“If they are not hitting at least 80% of the earn-out, something is probably going wrong. It has to be

largely achievable.”

“We never use staff retention as a target… it simply doesn’t work in the long run.”

Deal opportunity failure rates

Insight 5

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S25

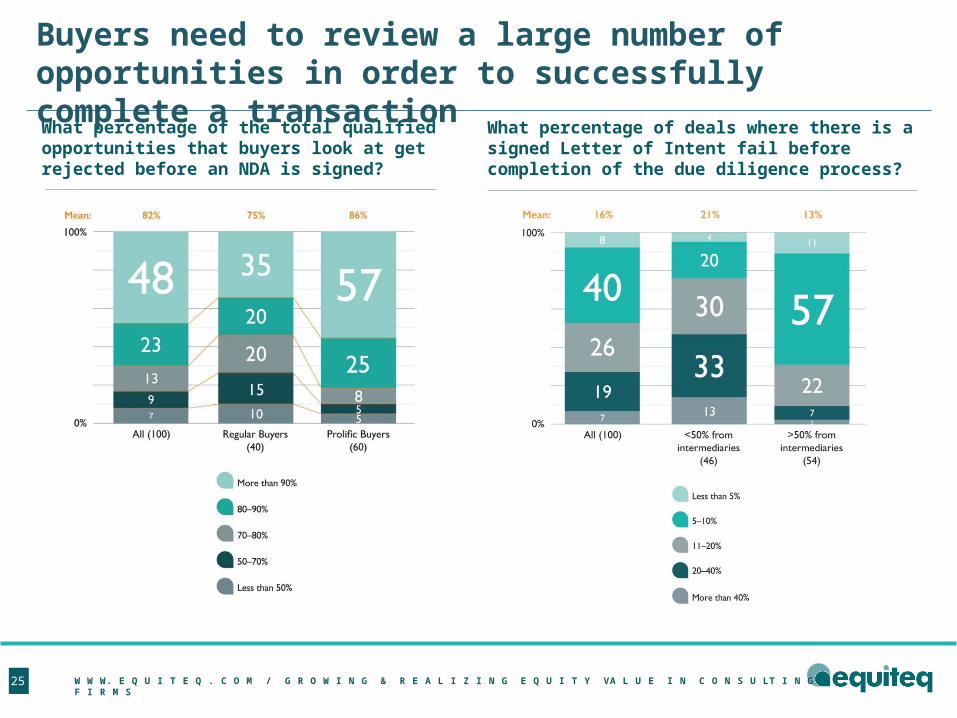

What percentage of the total qualified opportunities that buyers look at get rejected before an NDA is signed?

What percentage of deals where there is a signed Letter of Intent fail before completion of the due diligence process?

Buyers need to review a large number of opportunities in order to successfully complete a transaction

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S26

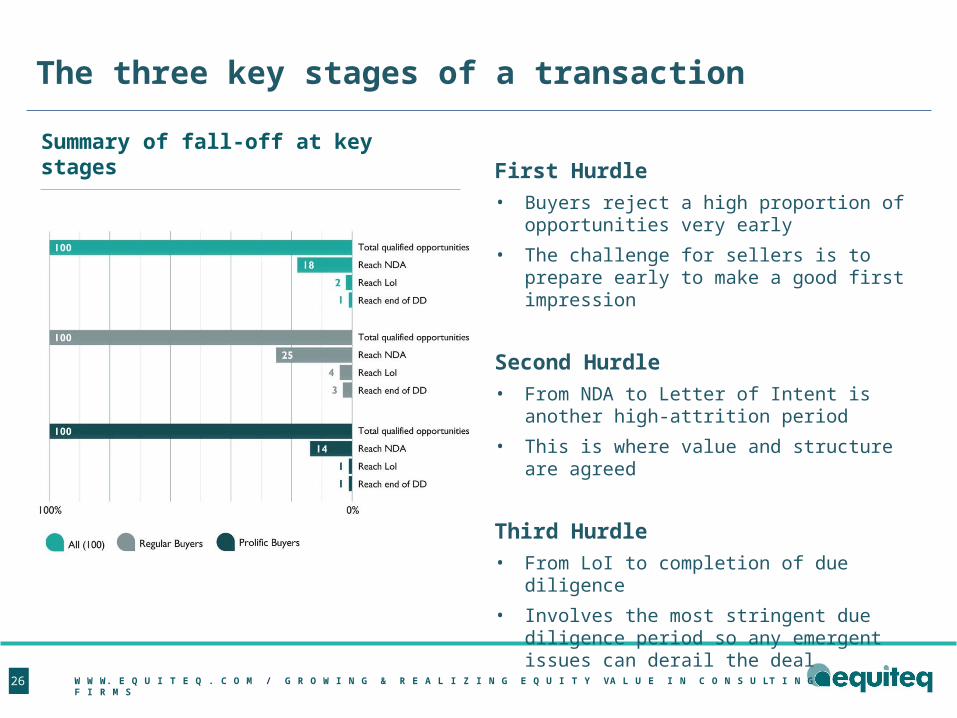

First Hurdle

• Buyers reject a high proportion of opportunities very early

• The challenge for sellers is to prepare early to make a good first impression

Second Hurdle

• From NDA to Letter of Intent is another high-attrition period

• This is where value and structure are agreed

Third Hurdle

• From LoI to completion of due diligence

• Involves the most stringent due diligence period so any emergent issues can derail the deal

The three key stages of a transaction

Summary of fall-off at key stages

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S27

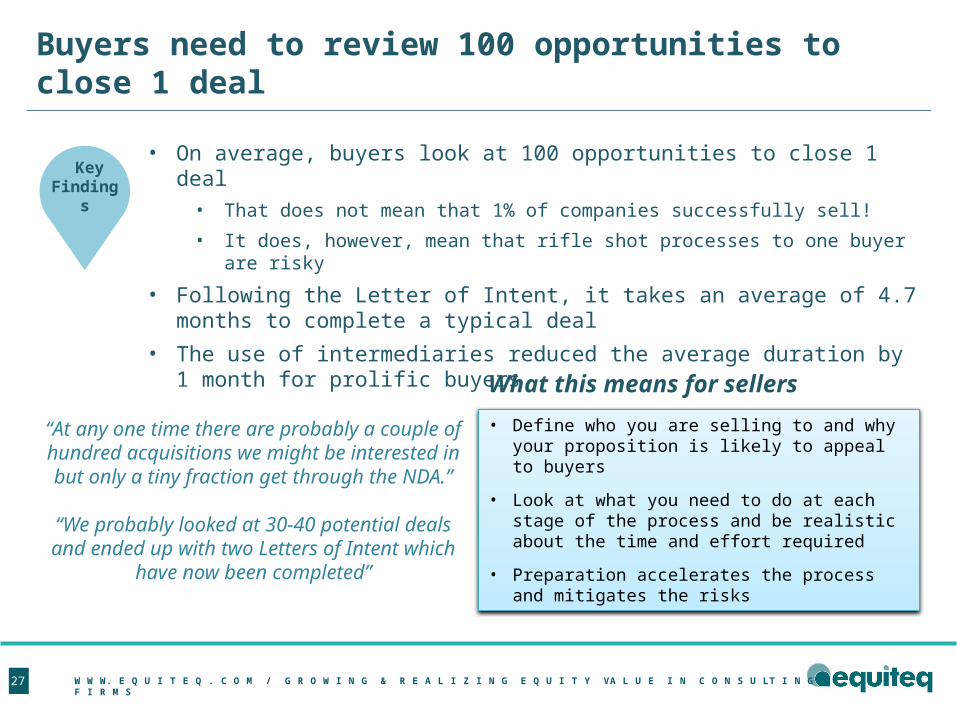

• On average, buyers look at 100 opportunities to close 1 deal• That does not mean that 1% of companies successfully sell!

• It does, however, mean that rifle shot processes to one buyer are risky

• Following the Letter of Intent, it takes an average of 4.7 months to complete a typical deal

• The use of intermediaries reduced the average duration by 1 month for prolific buyers

• Define who you are selling to and why your proposition is likely to appeal to buyers

• Look at what you need to do at each stage of the process and be realistic about the time and effort required

• Preparation accelerates the process and mitigates the risks

Key Findings

Buyers need to review 100 opportunities to close 1 deal

“At any one time there are probably a couple of hundred acquisitions we might be interested in but

only a tiny fraction get through the NDA.”

“We probably looked at 30-40 potential deals and ended up with two Letters of Intent which have now

been completed”

What this means for sellers

Ways to increase odds of a successful transaction

Conclusion

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S29

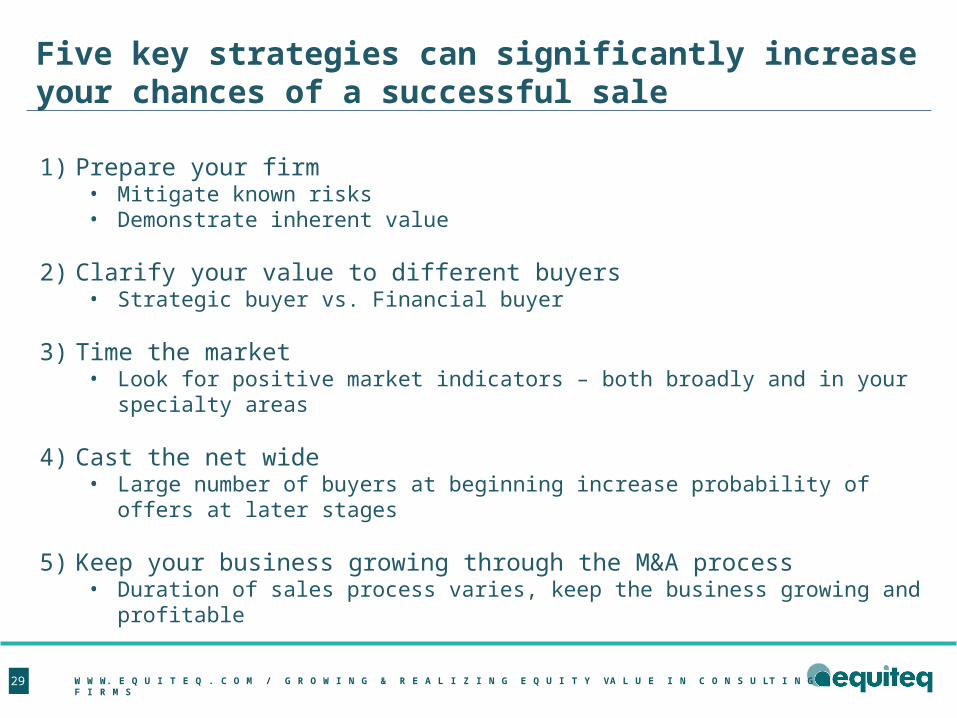

1) Prepare your firm• Mitigate known risks• Demonstrate inherent value

2) Clarify your value to different buyers• Strategic buyer vs. Financial buyer

3) Time the market• Look for positive market indicators – both broadly and in your specialty areas

4) Cast the net wide• Large number of buyers at beginning increase probability of offers at later stages

5) Keep your business growing through the M&A process• Duration of sales process varies, keep the business growing and profitable

Five key strategies can significantly increase your chances of a successful sale

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S30

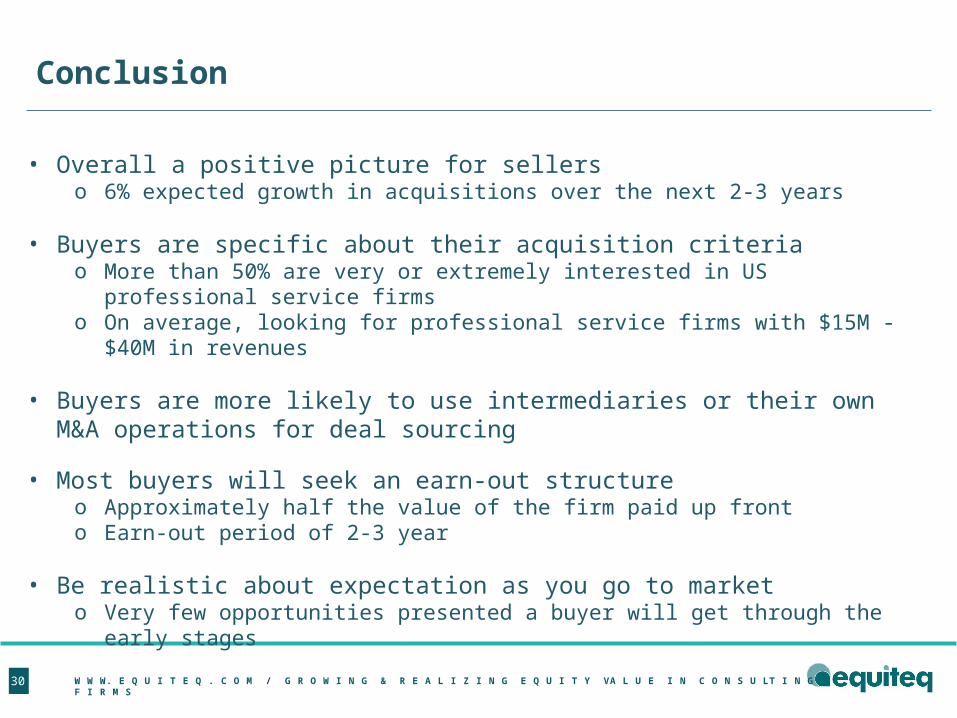

• Overall a positive picture for sellerso 6% expected growth in acquisitions over the next 2-3 years

• Buyers are specific about their acquisition criteriao More than 50% are very or extremely interested in US professional service firmso On average, looking for professional service firms with $15M - $40M in revenues

• Buyers are more likely to use intermediaries or their own M&A operations for deal sourcing

• Most buyers will seek an earn-out structureo Approximately half the value of the firm paid up fronto Earn-out period of 2-3 year

• Be realistic about expectation as you go to marketo Very few opportunities presented a buyer will get through the early stages

Conclusion

W W W. E Q U I T E Q . C O M / G R O W I N G & R E A L I Z I N G E Q U I T Y VA L U E I N C O N S U LT I N G F I R M S31

More resources available at www.equiteq.com