21

By : Gowtham Kumar C. K Asst Professor Dept of Commerce and Management Dr. NSAM FGC

By : Gowtham Kumar C. K

Asst Professor

Dept of Commerce and Management

Dr. NSAM FGC

Cost Accounting

CA is a formal system of accounting for costs in the books of accounts by means of which costs of products and services are ascertained and controlled.

Cost means “the price paid for something”

Cost ascertainment is computation of actual costs incurred

Cost estimation is a process of predetermining costs of goods and service.

Objectives of CostAccounting

Ascertainment of cost

Control of cost

Guide to business policy such as make or buy, introduction of new product etc

Determination of selling price

CA and FA - Comparison Purpose

Statutory requirements

Analysis of cost and profit

Periodicity of reporting

Control aspect

Historical and predetermined costs

Format of presenting information

Types of transactions recorded

Cost CentreCost center is a location, person, or item of

equipment (or group of these) for which costs may be ascertained and used for the purpose of control

It refers to a section of the business to which costs can be charged.

Types:Personal and Impersonal cost centre

Production and Service cost centre

Cost Unit Cost units are the things, that the business is set

up to provide, of which cost is ascertained.

Unit of product, service or time in relation to which cost may be ascertained or expressed

Types: Units of production such as a ream of paper, a tonne of

steel, a meter of cable etc.

Units of services such as passenger miles, consulting hours, room per day, bed per day

Methods of costing

It refers to the techniques and processes employed in the ascertainment of costs

Choice of the method depends upon the type and nature of manufacturing activity

Types: Broadly,

Job costing or job order costing

Process Costing

Other methods are variations of one of these methods.

Methods of costing - Types

Job Order Costing – Applies where work is undertaken to customers special requirements.

Contract Costing or Terminal Costing: It is same as Job order costing; however, job is small and contract is big contract. Contract is of long duration and may continue for more than a financial year.

Batch costing: Cost of a batch or group of identical products is ascertained; each batch of products is a cost unit for which costs are ascertained.

Methods of costing –Types….. Process Costing – Applies to a context where there is a continuous process. Costs are accumulated for each process. And then total cost of a process is divided by the number of units produced to arrive at cost per unit.

Operations Costing: Involves cost ascertainment for each operation.

Operating or services costing: It is applied to services; cost units are passenger –kilometer, room per day, bed per day.

Methods of costing –Types…..

Multiple or composite costing – Application of more than one method of costing in respect of the same product. Used in industries where a number of components are separately manufactured and then assembled into a final product.

Single, output or unit costing: Applied to a context where output produced are identical, the cost per unit is found by dividing the total cost by the number of units produced. E.g. Steel output is identical but differentiated by grades.

Techniques of costing –Types….. Standard costing – Standard cost is

predetermined as target of performance and actual performance is measured against the standard.

Budgetary control: By comparing actual with planned / budgeted performance

Marginal costing: Only variable cost is allocated to individual cost centers or cost units

Techniques of costing –Types….. Total Absorption costing – Both fixed and variable

costs are charged to products.

Uniform Costing: It is not a technique but a situation wherein several undertakings use the same costing principle and practices.

Elements of costs - Materials Material cost : cost of commodities supplied to an

undertaking

Direct materials cost: those costs which are incurred for and conveniently identified with a particular cost unit, process or department.Ex: cost of raw material

Indirect materials cost: those costs which cannot be conveniently identified with a particular cost unit, process or department.Ex: cost of material that are inexpensive but may or may not

physically become part of the finished goods

Elements of costs – Labourcost

Labour cost : cost of remuneration (wages, salaries, commissions, bonuses, etc etc) of the employees of an undertaking

Direct labour cost: wages paid to workers directlyengaged in the production process.

Eg: Wages of machine operator

Indirect labour cost: those wages which cannot be

conveniently identified with a particular cost unit,process or department

Elements of costs – Expenses

Eg: Royalty paid, depreciation of a plant used Indirect Expenses: All indirect costs other than indirect

materials and labor. They cannot be directly identified with a particular job, process or work order and are common to cost units or cost centers

Ex: Rent and rates, lighting and power

Expenses: The cost of services provided to an undertaking

Direct Expenses: those expenses which can be identified with and allocated to cost centers or units.

Elements of Cost- Price Cost

Direct Material +

Direct labour +

Direct Expenses

Elements of costs

Indirect Material +

Indirect labour +

Indirect expenses

Overheads are divided into

f. Production overheads

g. Office and administration overheads

h. Selling and distribution overheads

Elements of costs – Production

overheads Indirect Material such as coal, oil grease,

stationary in factory office+

Indirect labour such as work manager’s salary,salary of factory office staff, salary of inspectorand supervisors, watchman, sweeper

Indirect Expenses such as factory rent, depreciation of plant, repairs and maintenance of plant, insurance of factory building, factory lighting and power, internal transport expenses

Elements of costs –Office and administration

overheads

Indirect Material such as stationary used in administration office, postage, etc

Indirect labour such as salary of office staff, salary of of MD, Directors, watchman, sweeper

Indirect Expenses such as office rent, insurance of office building, office lighting and power, telephone, depreciation of office furniture, office a/c, sundry office expenses

Elements of costs Selling cost: cost of seeking to create and stimulate demand

and of securing orders such as ads, samples and free gifts, salaries of salesmen

Distribution cost: cost of making packed product available for dispatch and returning of empty packages for reuse

Indirect Material such as stationary used in sales office, packing mat, cost of samples, price list, oil for delivery vans

Indirect labour such as salary of sales staff, salary of of MD, Directors, watchman, sweeper

Indirect Expenses such as advertising, traveling expenses, showroom expenses, carriage outwards, rent of warehouse, bad debts, insurance of goods in transit etc.

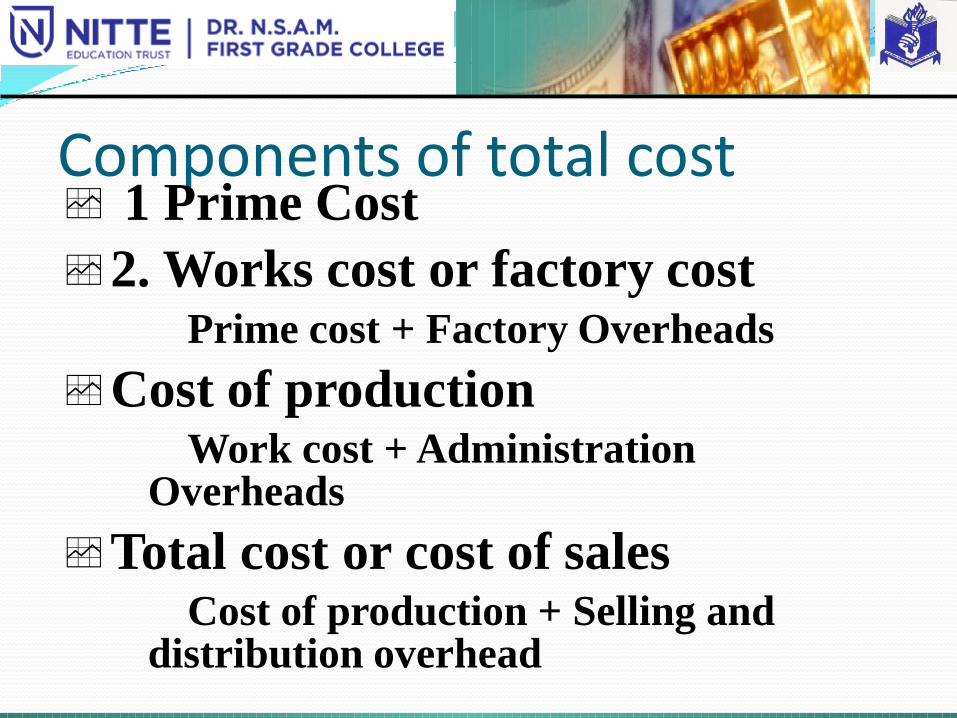

Components of total cost 1 Prime Cost

2. Works cost or factory costPrime cost + Factory Overheads

Cost of productionWork cost + Administration

Overheads

Total cost or cost of salesCost of production + Selling and

distribution overhead