42

Housing’s Lost Decade: Where we go from here By Kent Colton, PhD, Gopal Ahluwalia and Jay Shackford January 11, 2013 Copyright 2013 The Colton Housing Group

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | buck-tyrone-george |

| View: | 213 times |

| Download: | 0 times |

Housing’s Lost Decade: Where we go from here

By Kent Colton, PhD, Gopal Ahluwalia and Jay Shackford

January 11, 2013

Copyright 2013 The Colton Housing Group

2

19901991

19921993

19941995

19961997

19981999

20002001

20022003

20042005

20062007

20082009

20102011

2012*0

500

1,000

1,500

2,000

2,500

Annual Housing Starts/1990-2012

Single-family Multifamily

Starts in thousands of units

Housing peaks in 2005 before collapsingRecovery slow but in sight

Source: U.S. Census Bureau *Forecast by Colton, Ahluwalia and Shackford

Chart 1

Copyright 2013 The Colton Housing Group

3

Worst housing crash in post-World War II period

Source: U.S. Census Bureau*Forecast by Colton, Ahluwalia and Shackford

Chart 2

Copyright 2013 The Colton Housing Group

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

0

500

1,000

1,500

2,000

2,500

Annual Housing Starts/1960-2012

Total Single Family Multifamily

4

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

*200

400

600

800

1,000

1,200

1,400

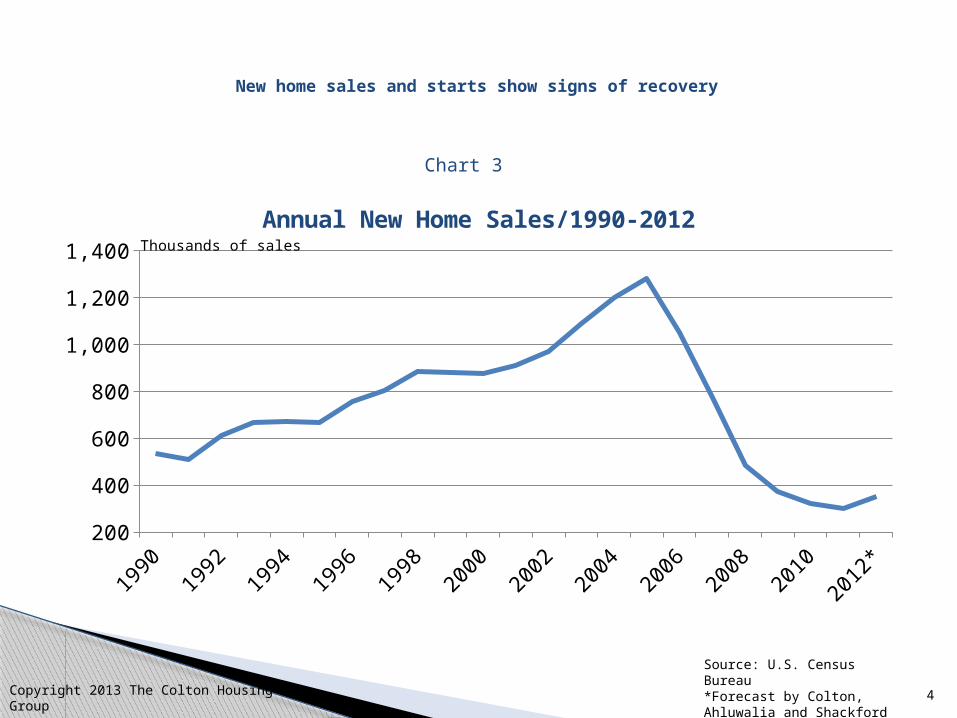

Annual New Home Sales/1990-2012Thousands of sales

New home sales and starts show signs of recovery

Source: U.S. Census Bureau *Forecast by Colton, Ahluwalia and Shackford

Chart 3

Copyright 2013 The Colton Housing Group

5

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

*2,000

3,000

4,000

5,000

6,000

7,000

8,000

Annual Sales of Existing Homes/1990-2012Thousands of sales

Existing home sales fall but not as dramatically as new homes

Source: National Association of Realtors*Forecast by Colton, Ahluwalia and Shackford

Chart 4

Copyright 2013 The Colton Housing Group

6

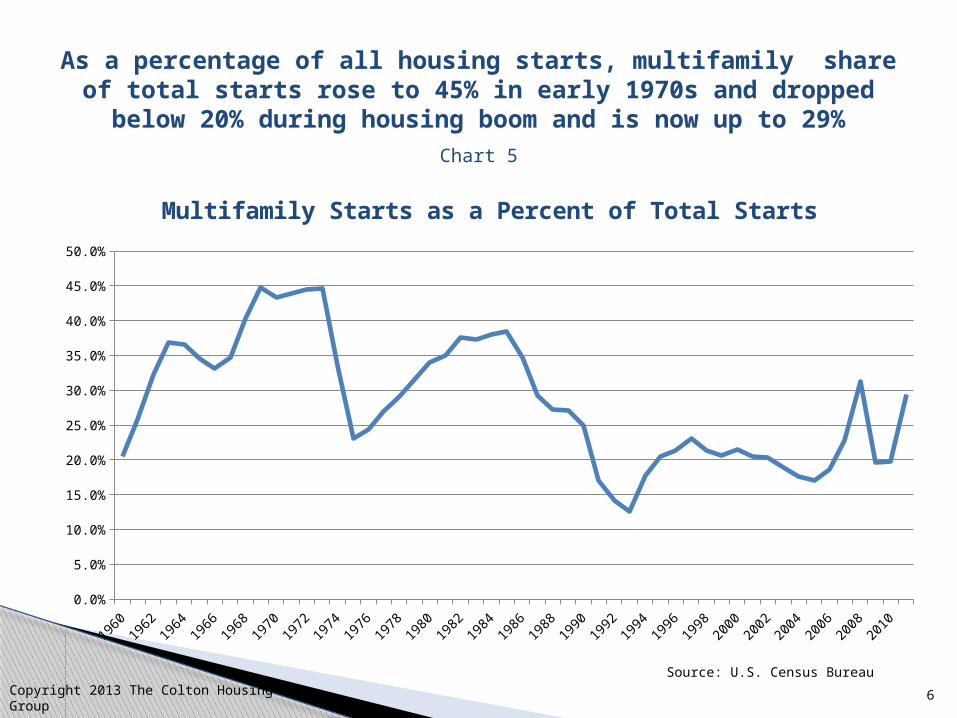

As a percentage of all housing starts, multifamily share of total starts rose to 45% in early 1970s and dropped below

20% during housing boom and is now up to 29%

Source: U.S. Census Bureau

Chart 5

Copyright 2013 The Colton Housing Group

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Multifamily Starts as a Percent of Total Starts

7

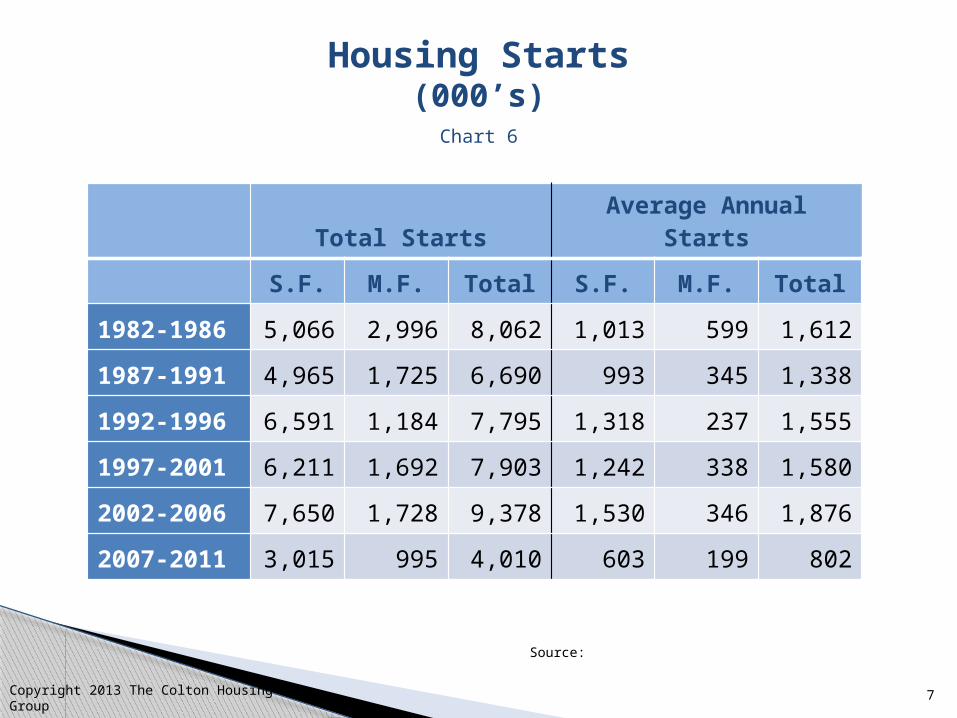

Housing Starts(000’s)

Source:

Chart 6

Copyright 2013 The Colton Housing Group

Total StartsAverage Annual

Starts

S.F. M.F. Total S.F. M.F. Total

1982-1986 5,066 2,996 8,062 1,013 599 1,612

1987-1991 4,965 1,725 6,690 993 345 1,338

1992-1996 6,591 1,184 7,795 1,318 237 1,555

1997-2001 6,211 1,692 7,903 1,242 338 1,580

2002-2006 7,650 1,728 9,378 1,530 346 1,876

2007-2011 3,015 995 4,010 603 199 802

8

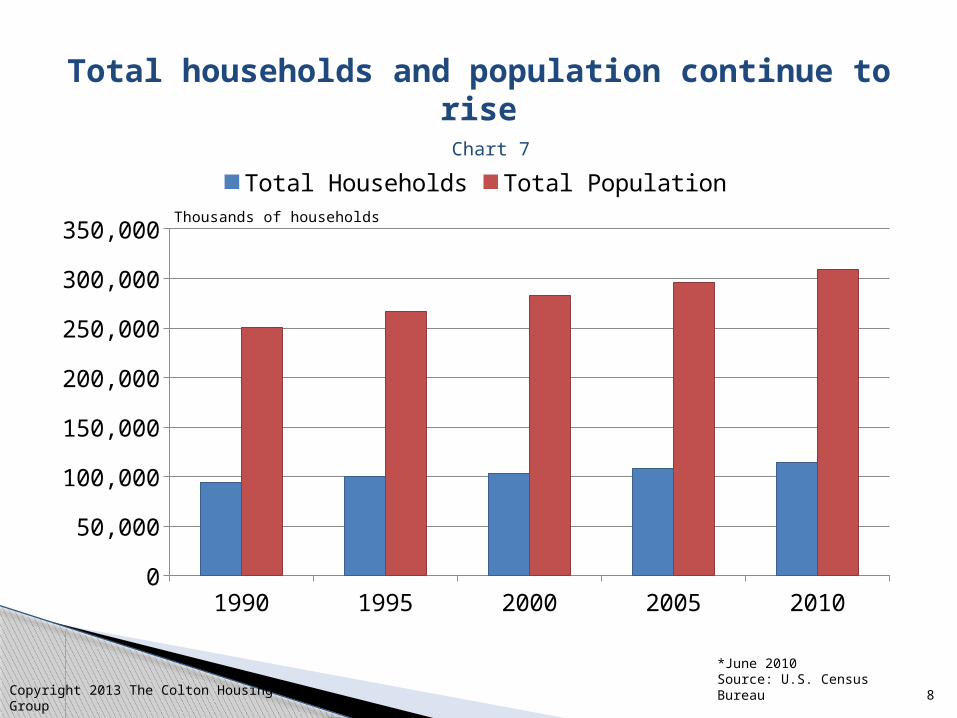

1990 1995 2000 2005 20100

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Total Households Total PopulationThousands of households

Total households and population continue to rise

*June 2010Source: U.S. Census Bureau

Chart 7

Copyright 2013 The Colton Housing Group

9

Net increase in households decline (major factors are Immigration and

Households Doubling Up)

* June 2010Source: U.S. Census Bureau

Chart 8

Copyright 2013 The Colton Housing Group

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Average1992-1996

1,063

Average 1997-2001 1,288

Average 2002-20061,349

Average 2007-2011568

Change in total number of householdsAverage

thousands

10

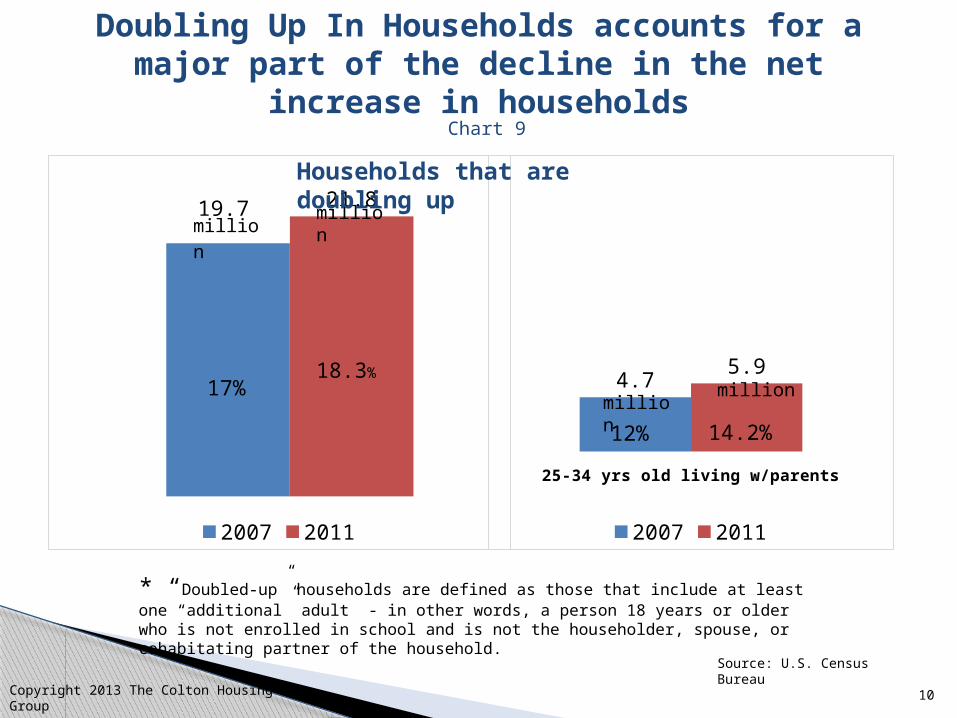

Doubling Up In Households accounts for a major part of the decline in the net increase

in householdsChart 9

Copyright 2013 The Colton Housing Group

19.7 21.8

2007 2011

million

17% 4.75.9

2007 2011

25-34 yrs old living w/parents

million

18.3%

12% 14.2%million

million

* “Doubled-up” households are defined as those that include at least one “additional” adult - in other words, a person 18 years or older who is not enrolled in school and is not the householder, spouse, or cohabitating partner of the household.

Source: U.S. Census Bureau

Households that are doubling up

11

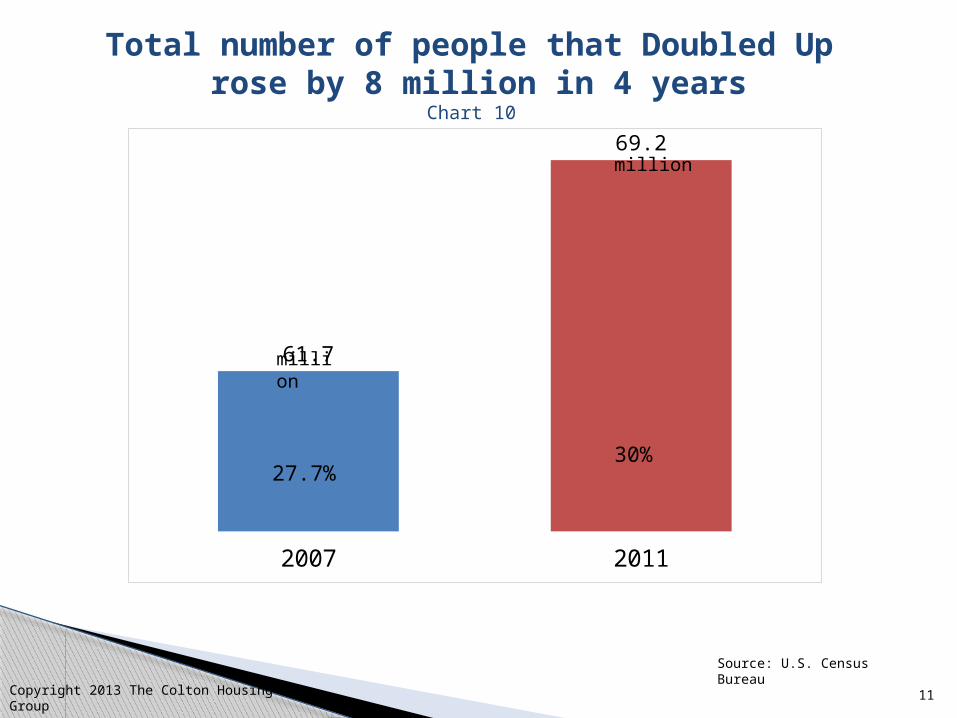

Total number of people that Doubled Up rose by 8 million in 4 years

Copyright 2013 The Colton Housing Group

2007 2011

61.7

69.2

million

million

27.7%30%

Chart 10

Source: U.S. Census Bureau

12

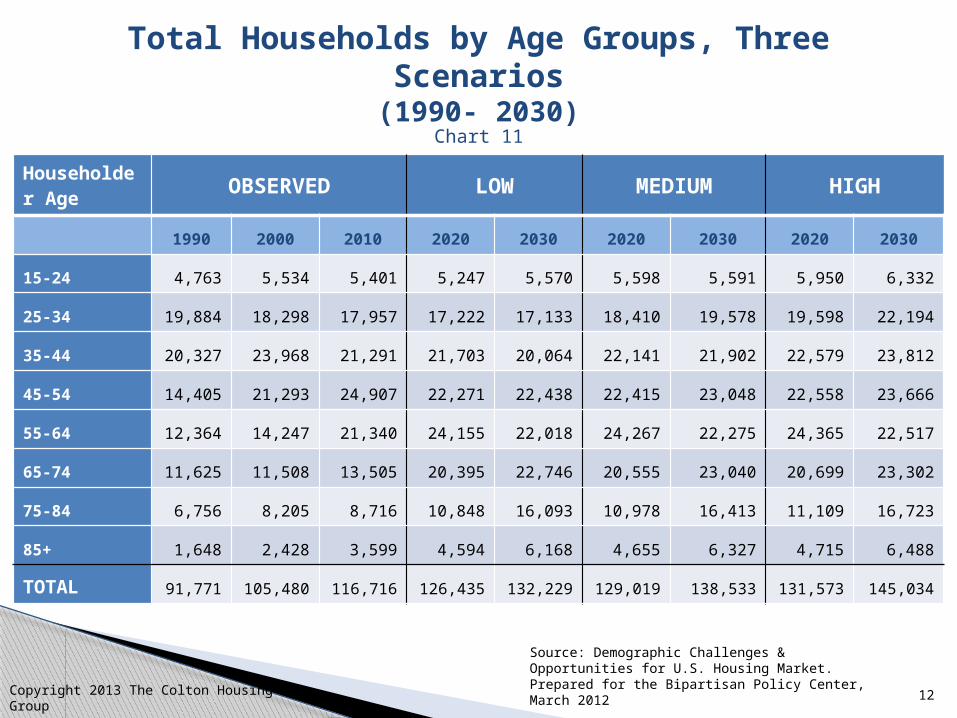

Total Households by Age Groups, Three Scenarios

(1990- 2030)

Source: Demographic Challenges & Opportunities for U.S. Housing Market. Prepared for the Bipartisan Policy Center, March 2012

Chart 11

Copyright 2013 The Colton Housing Group

Householder Age OBSERVED LOW MEDIUM HIGH

1990 2000 2010 2020 2030 2020 2030 2020 2030

15-24 4,763 5,534 5,401 5,247 5,570 5,598 5,591 5,950 6,332

25-34 19,884 18,298 17,957 17,222 17,133 18,410 19,578 19,598 22,194

35-44 20,327 23,968 21,291 21,703 20,064 22,141 21,902 22,579 23,812

45-54 14,405 21,293 24,907 22,271 22,438 22,415 23,048 22,558 23,666

55-64 12,364 14,247 21,340 24,155 22,018 24,267 22,275 24,365 22,517

65-74 11,625 11,508 13,505 20,395 22,746 20,555 23,040 20,699 23,302

75-84 6,756 8,205 8,716 10,848 16,093 10,978 16,413 11,109 16,723

85+ 1,648 2,428 3,599 4,594 6,168 4,655 6,327 4,715 6,488

TOTAL 91,771 105,480 116,716 126,435 132,229 129,019 138,533 131,573 145,034

13

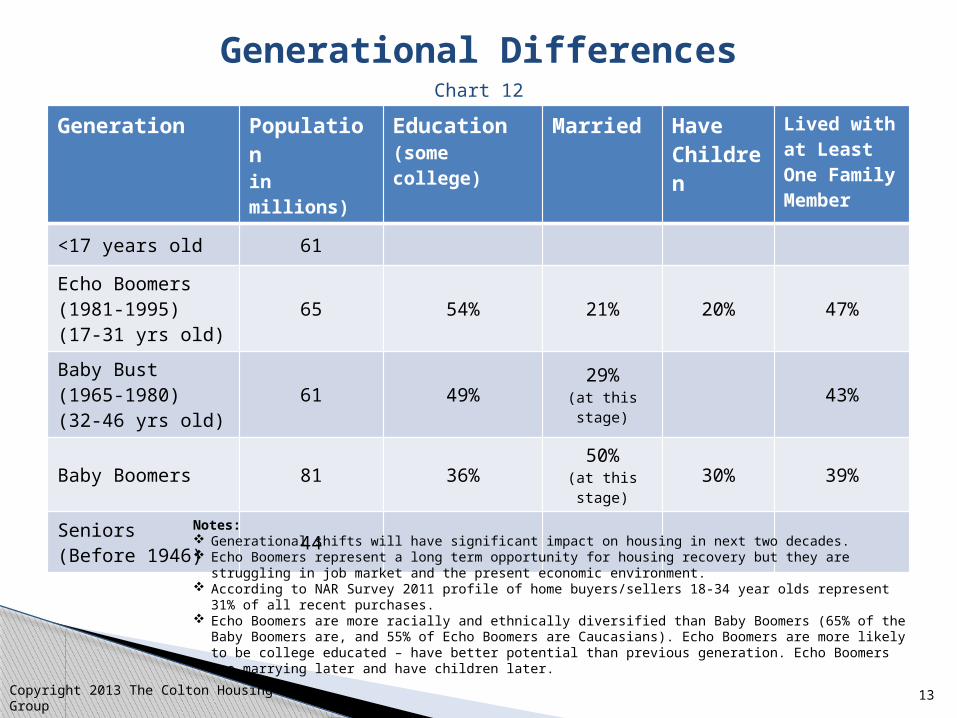

Generation Population in millions)

Education(some college)

Married Have Children

Lived with at Least One Family Member

<17 years old 61

Echo Boomers(1981-1995)(17-31 yrs old)

65 54% 21% 20% 47%

Baby Bust(1965-1980)(32-46 yrs old)

61 49%29%

(at this stage)

43%

Baby Boomers 81 36%50%

(at this stage)

30% 39%

Seniors (Before 1946)

44

Generational DifferencesChart 12

Notes: Generational shifts will have significant impact on housing in next two decades. Echo Boomers represent a long term opportunity for housing recovery but they are struggling in job

market and the present economic environment. According to NAR Survey 2011 profile of home buyers/sellers 18-34 year olds represent 31% of all recent

purchases. Echo Boomers are more racially and ethnically diversified than Baby Boomers (65% of the Baby Boomers

are, and 55% of Echo Boomers are Caucasians). Echo Boomers are more likely to be college educated – have better potential than previous generation. Echo Boomers are marrying later and have children later.

Copyright 2013 The Colton Housing Group

14

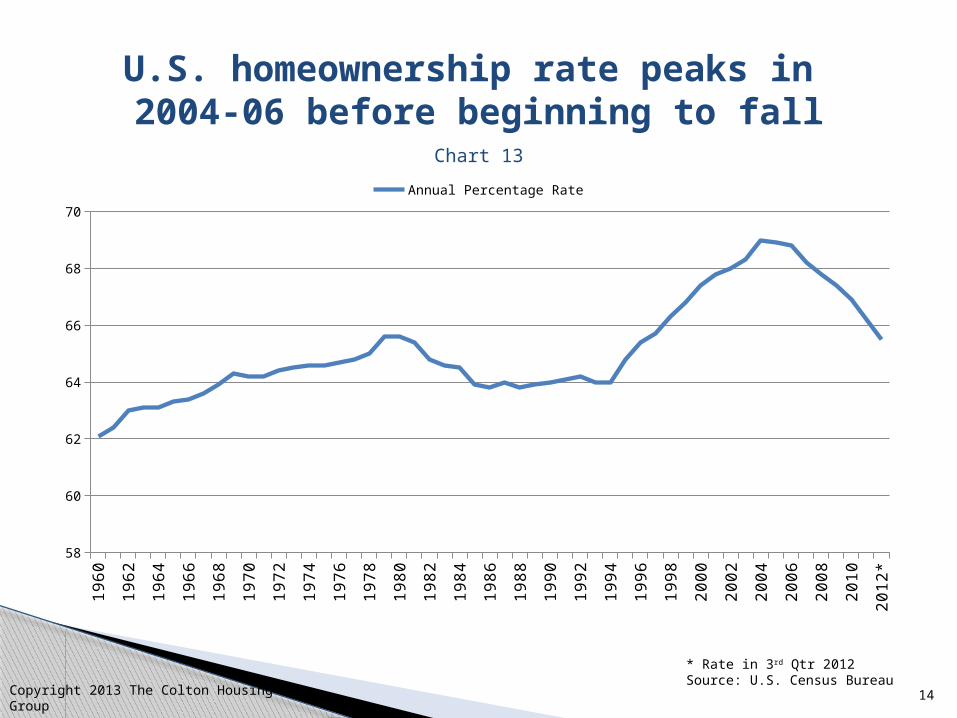

U.S. homeownership rate peaks in 2004-06 before beginning to fall

* Rate in 3rd Qtr 2012Source: U.S. Census Bureau

Chart 13

Copyright 2013 The Colton Housing Group

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012*

58

60

62

64

66

68

70

Annual Percentage Rate

15

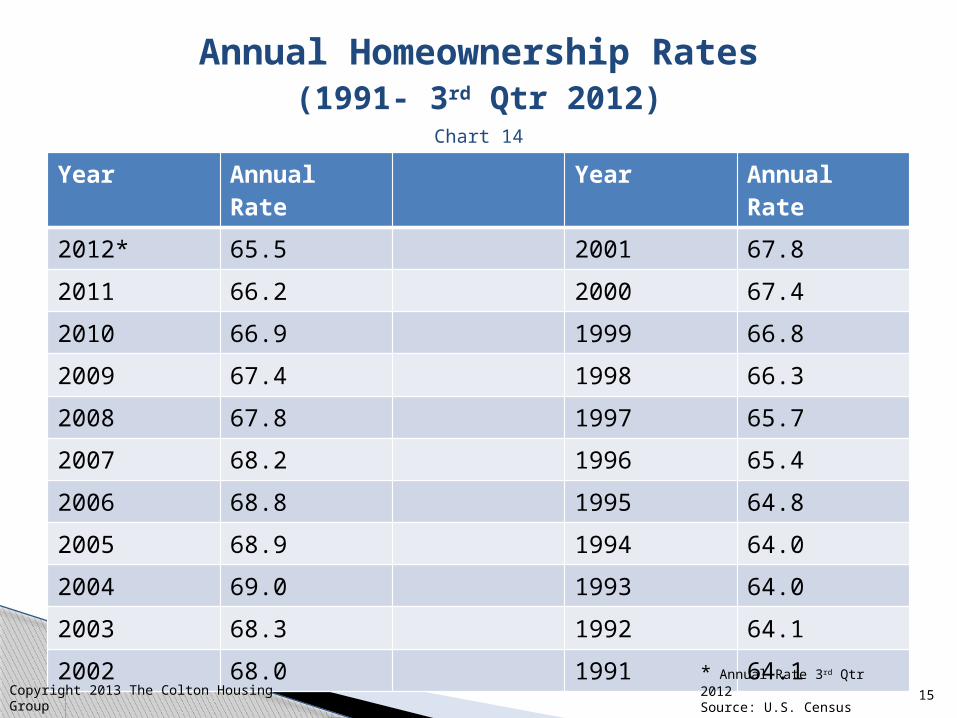

Year Annual Rate

Year Annual Rate

2012* 65.5 2001 67.8

2011 66.2 2000 67.4

2010 66.9 1999 66.8

2009 67.4 1998 66.3

2008 67.8 1997 65.7

2007 68.2 1996 65.4

2006 68.8 1995 64.8

2005 68.9 1994 64.0

2004 69.0 1993 64.0

2003 68.3 1992 64.1

2002 68.0 1991 64.1

Annual Homeownership Rates(1991- 3rd Qtr 2012)

* Annual Rate 3rd Qtr 2012Source: U.S. Census Bureau

Chart 14

Copyright 2013 The Colton Housing Group

16

Homeownership Rates Vary by Age group

Source: U.S. Housing Market Conditions/HUD

Chart 15

Copyright 2013 The Colton Housing Group

1985 1990 1995 2000 2005 2010 2011 2012*

Change in homeownership

2005-3rd Qtr 2012

Less than 35 yrs 39.9% 38.5% 38.6% 40.8% 43.0% 39.1% 37.8% 36.3% -6.7%

35-44 yrs 68.1% 66.3% 65.2% 67.9% 69.3% 65.0% 63.5% 61.8% -7.5%

45-54 yrs 75.9% 75.2% 75.2% 76.5% 76.6% 73.5% 72.7% 72.0% -4.6%

55-64 yrs 79.5% 79.3% 79.5% 80.3% 81.2% 79.0% 78.5% 76.9% -4.3%

65 yrs and over 74.8% 76.3% 78.1% 80.4% 80.6% 80.5% 80.9% 81.4% +0.8%

U.S. 63.9% 63.9% 64.7% 67.4% 68.9% 66.9% 66.4% 65.5% -3.4%

Note: Homeownership rate declined from peak of 68.9% in 2005 to 65.5% (decline of 3.4%) in 3rd Qtr 2012. The decline in homeownership varies significantly among different population segments. Among less than 35 years old, homeownership declined from43.0% in 2005 to 36.3% in 3rd Qtr 2012 (decline of 6.7%) and among 35-44 years old, homeownership declined from 69.3% in 2005 to 61.8% in 3rd Qtr 2012 (decline of 7.5%).

17

What is a $200,000 home purchased in 2000 worth today?

Significant drop in equity since 2005 but equity in 2012 is still up compared to 2000 in almost all markets. And some markets have experienced price increases or more

modest declines since 2006.

Source: Federal Housing Finance Agency

Chart 16

Copyright 2013 The Colton Housing Group

Los Angeles Sacramento Las VegasRiverside/San

Bernardino Phoenix MiamiFt.

Lauderdale Wash DC

2000 200,000 200,000 200,000 200,000 200,000 200,000 200,000 200,000

2005 465,487 444,958 394,375 471,000 355,000 444,000 436,000 443,000

2012 332,000 258,000 178,000 262,000 218,000 302,000 294,000 396,000

Los

Angeles Sacramento Las VegasRiverside/San

Bernardino Phoenix MiamiFt.

Lauderdale Wash DC

2000-2005 132.7% 122.5% 97.2% 135.5% 77.5% 122.0% 118.0% 121.5%

2005-2012 -28.7% -42.0% -54.9% -44.4% -38.6% -32.0% -32.6% -10.6%

2000-2012 66.0% 29.0% -11.0% 31.0% 9.0% 51.0% 47.0% 98.0%

Percentage Change

18

Source: Federal Housing Finance Agency

Chart 17

Copyright 2013 The Colton Housing Group

Atlanta Seattle Chicago Boston Raleigh Denver Dallas Houston

2000 200,000 200,000 200,000 200,000 200,000 200,000 200,000 200,000

2005 247,000 297,000 301,000 347,000 234,000 254,000 238,000 247,000

2012 180,000 269,000 225,000 311,000 254,000 257,000 256,000 298,000

Atlanta Seattle Chicago Boston Raleigh Denver Dallas Houston

2000-2005 23.5% 48.5% 50.5% 73.5% 17.0% 27.0% 19.0% 23.5%

2005-2012 -27.1% -9.4% -25.2% -10.4% 8.5% 1.2% 7.6% 20.6%

2000-2012 -10.0% 34.5% 12.5% 55.5% 27.0% 28.5% 28.0% 49.0%

Percentage Change

What is a $200,000 home purchased in 2000 worth today?

Significant drop in equity since 2005 but equity in 2012 is still up compared to 2000. And some markets have experienced price increases or more modest declines since

2005.

19

Jan-00Jul-00Jan-01Jul-01Jan-02Jul-02Jan-03Jul-03Jan-04Jul-04Jan-05Jul-05Jan-06Jul-06Jan-07Jul-07Jan-08Jul-08Jan-09Jul-09Jan-10Jul-10Jan-11Jul-11Jan-12Jul-12

100.0

120.0

140.0

160.0

180.0

200.0

220.0

240.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

240.0

10-city composite 20-city composite National Aggregate index

Top 1

0 a

nd 2

0 H

om

e P

rice

Indexes

Month

ly

Natio

nal A

ggre

gate

Index Q

uarte

rly

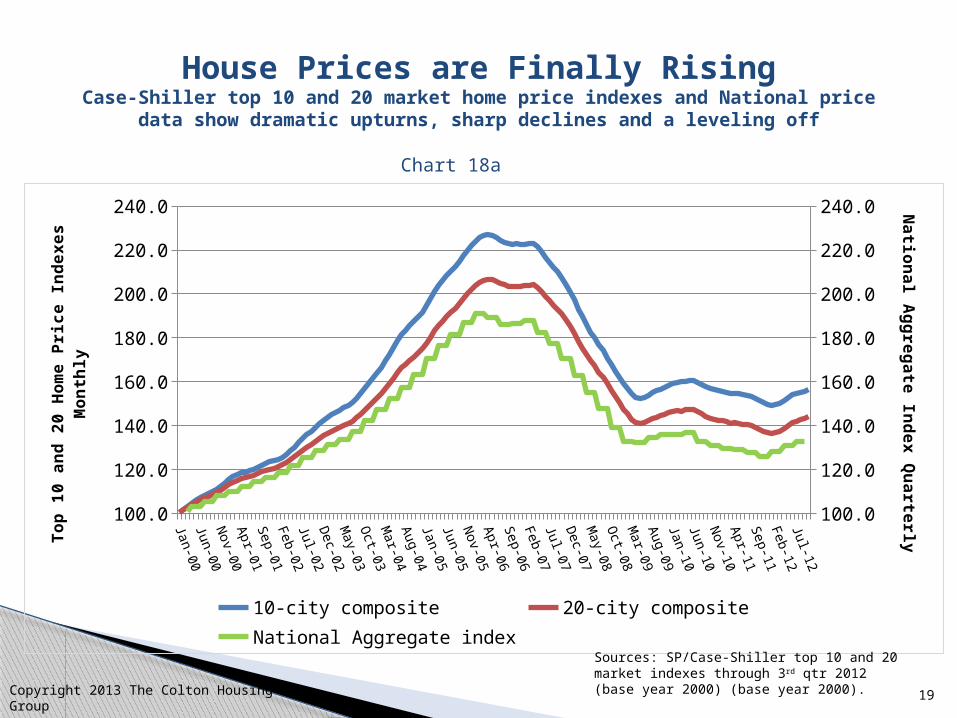

House Prices are Finally RisingCase-Shiller top 10 and 20 market home price indexes and National price data

show dramatic upturns, sharp declines and a leveling off

Chart 18a

Sources: SP/Case-Shiller top 10 and 20 market indexes through 3rd qtr 2012 (base year 2000) (base year 2000).

Copyright 2013 The Colton Housing Group

20

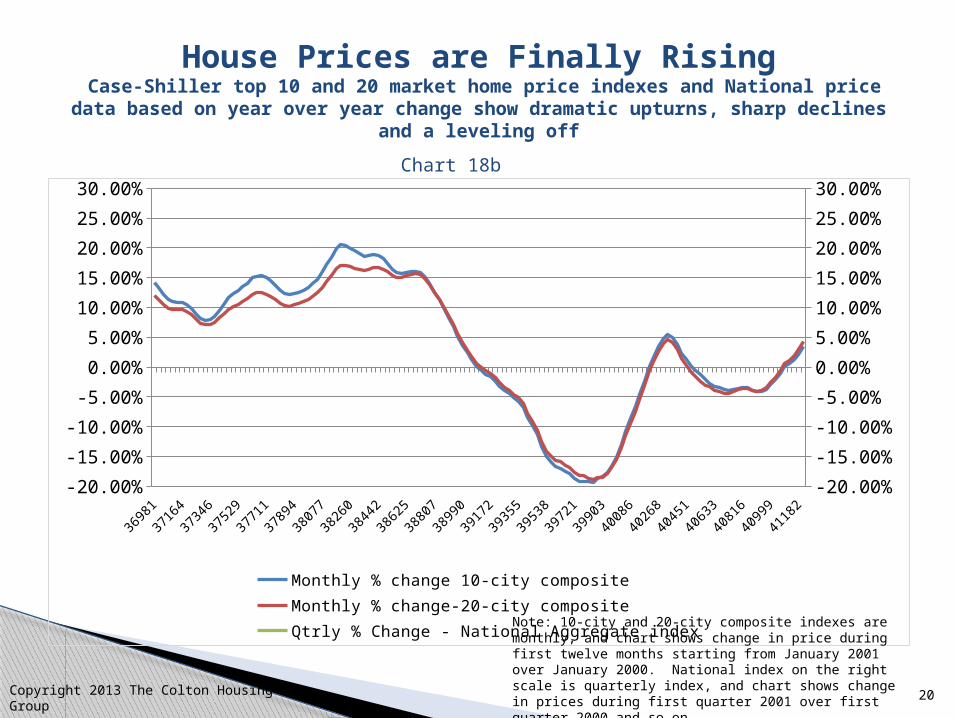

House Prices are Finally Rising Case-Shiller top 10 and 20 market home price indexes and National price data based on year over year change show dramatic upturns, sharp declines and a

leveling off

3698

1

3716

4

3734

6

3752

9

3771

1

3789

4

3807

7

3826

0

3844

2

3862

5

3880

7

3899

0

3917

2

3935

5

3953

8

3972

1

3990

3

4008

6

4026

8

4045

1

4063

3

4081

6

4099

9

4118

2-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Monthly % change 10-city composite Monthly % change-20-city compositeQtrly % Change - National Aggregate index

Chart 18b

Note: 10-city and 20-city composite indexes are monthly, and chart shows change in price during first twelve months starting from January 2001 over January 2000. National index on the right scale is quarterly index, and chart shows change in prices during first quarter 2001 over first quarter 2000 and so on.Copyright 2013 The Colton Housing Group

21

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

*40

45

50

55

60

65

70

75

80

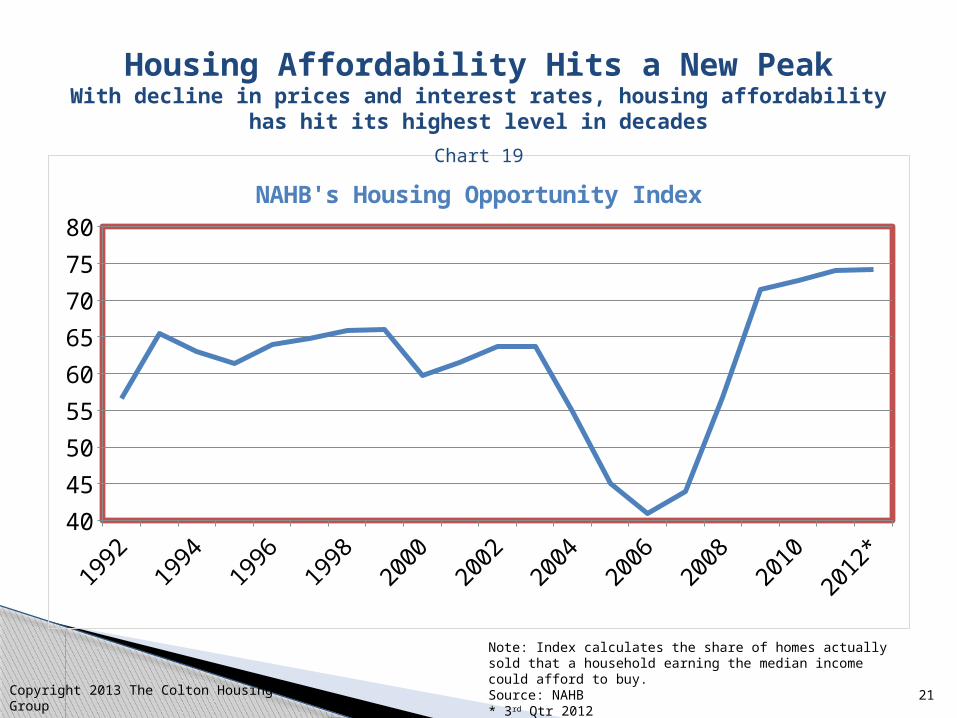

NAHB's Housing Opportunity Index

Housing Affordability Hits a New PeakWith decline in prices and interest rates, housing affordability has hit

its highest level in decades

Note: Index calculates the share of homes actually sold that a household earning the median income could afford to buy.Source: NAHB * 3rd Qtr 2012

Chart 19

Copyright 2013 The Colton Housing Group

22

Jan-

85

Jan-

87

Jan-

89

Jan-

91

Jan-

93

Jan-

95

Jan-

97

Jan-

99

Jan-

01

Jan-

03

Jan-

05

Jan-

07

Jan-

09

Jan-

110

10

20

30

40

50

60

70

80

90

100

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

NAHB/Wells Fargo Housing Market Index (HMI) and New Single-Family Starts

Housing Market Index Single-Family Starts

Ho

usin

g M

ark

et

Ind

ex

New

Sin

gle

-Fam

ily S

tarts

(in th

ousands o

f units

)

Chart 20

Builder Confidence Rises

Copyright 2013 The Colton Housing Group

23

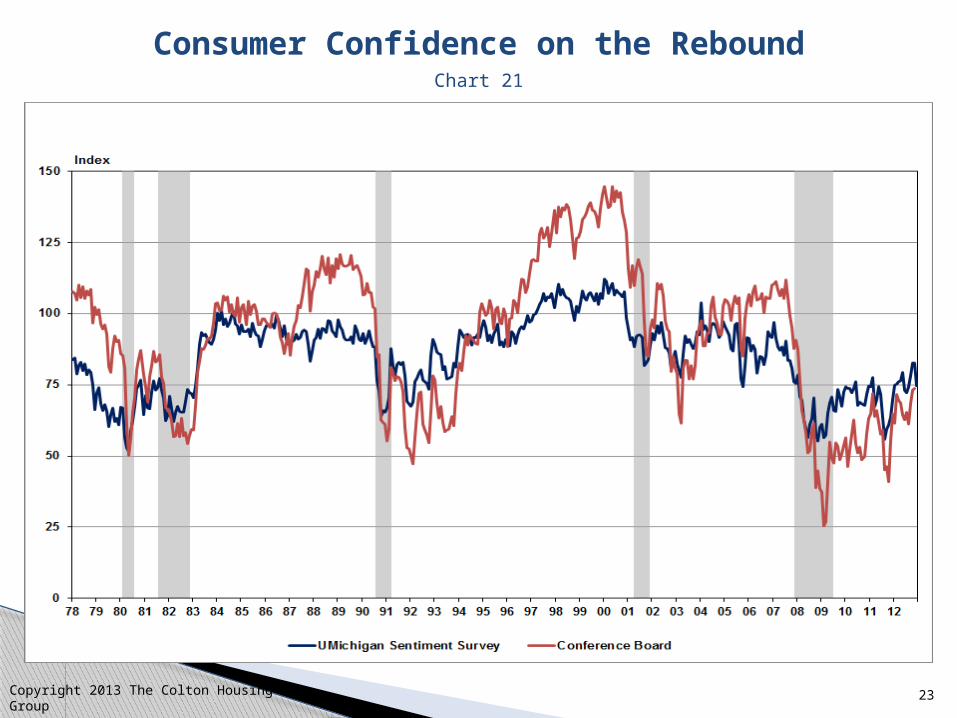

Chart 21

Consumer Confidence on the Rebound

Copyright 2013 The Colton Housing Group

24

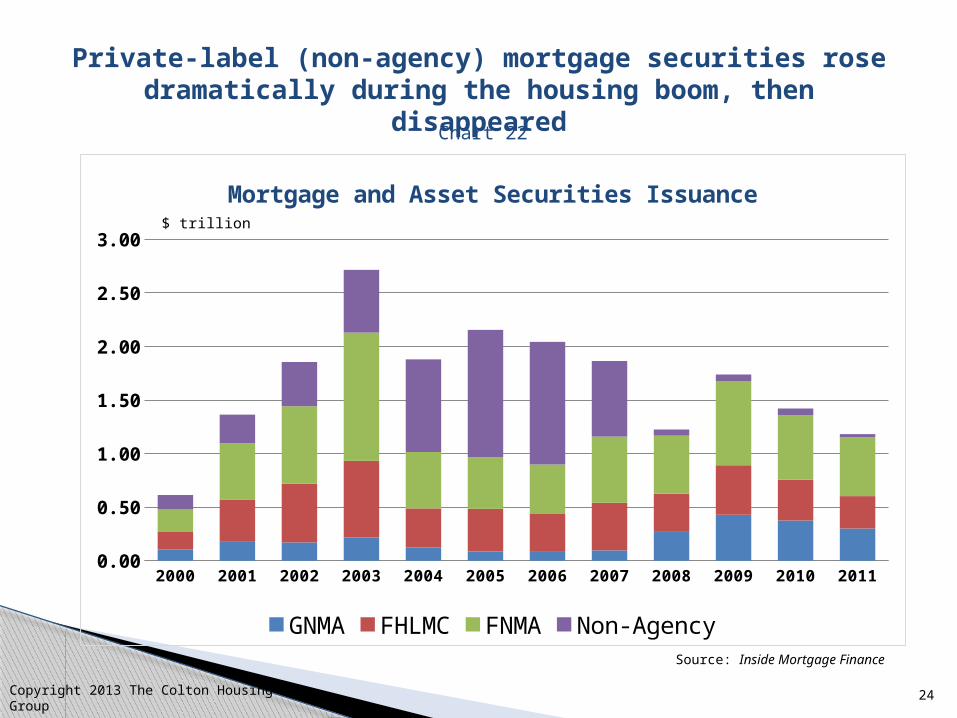

Private-label (non-agency) mortgage securities rose dramatically during the housing boom, then

disappeared

Source: Inside Mortgage Finance

Chart 22

Copyright 2013 The Colton Housing Group

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110.00

0.50

1.00

1.50

2.00

2.50

3.00

Mortgage and Asset Securities Issuance

GNMA FHLMC FNMA Non-Agency

$ trillion

25

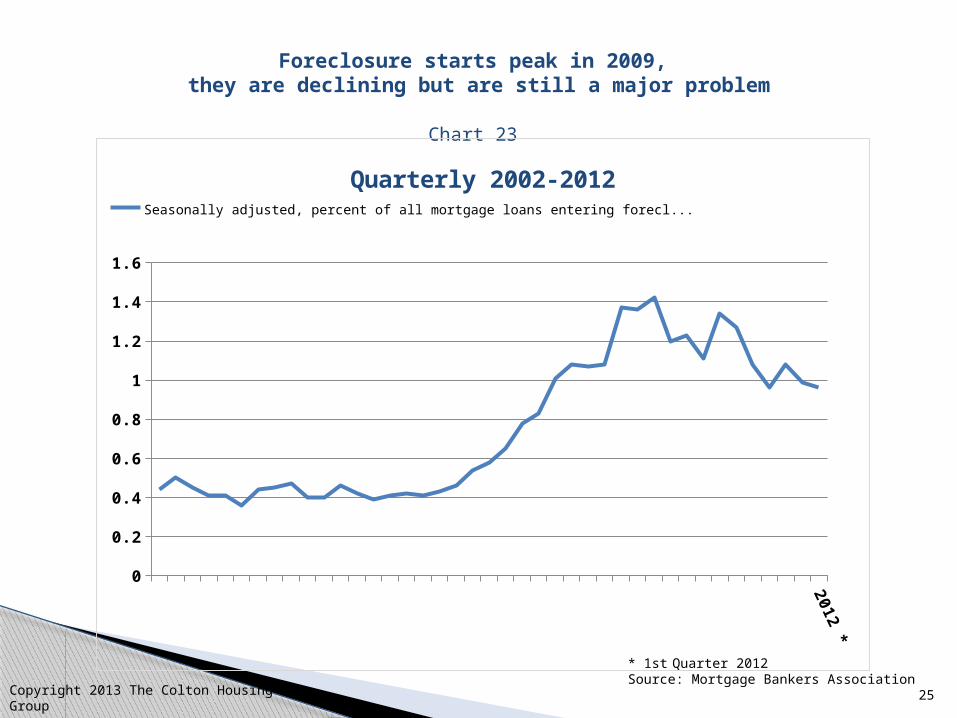

Foreclosure starts peak in 2009, they are declining but are still a major problem

* 1st Quarter 2012Source: Mortgage Bankers Association

Chart 23

Copyright 2013 The Colton Housing Group

2012 *

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Quarterly 2002-2012Seasonally adjusted, percent of all mortgage loans entering foreclosure

26

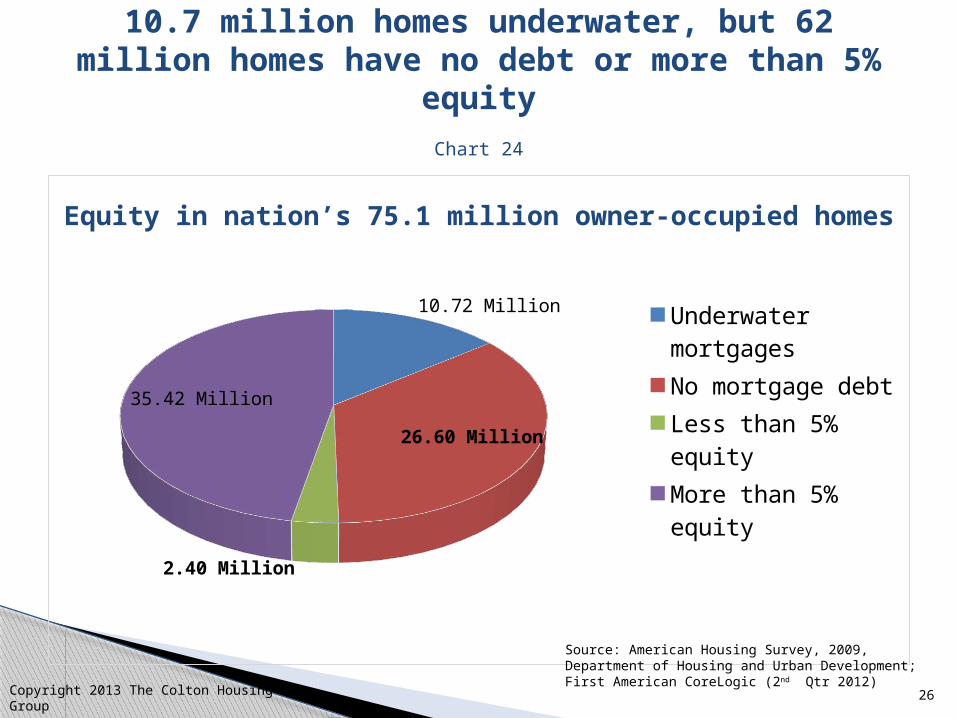

10.72 Million

26.60 Million

2.40 Million

35.42 Million

Underwater mortgagesNo mortgage debtLess than 5% equityMore than 5% equity

10.7 million homes underwater, but 62 million homes have no debt or more than 5% equity

Equity in nation’s 75.1 million owner-occupied homes

Source: American Housing Survey, 2009,Department of Housing and Urban Development;First American CoreLogic (2nd Qtr 2012)

Chart 24

Copyright 2013 The Colton Housing Group

27

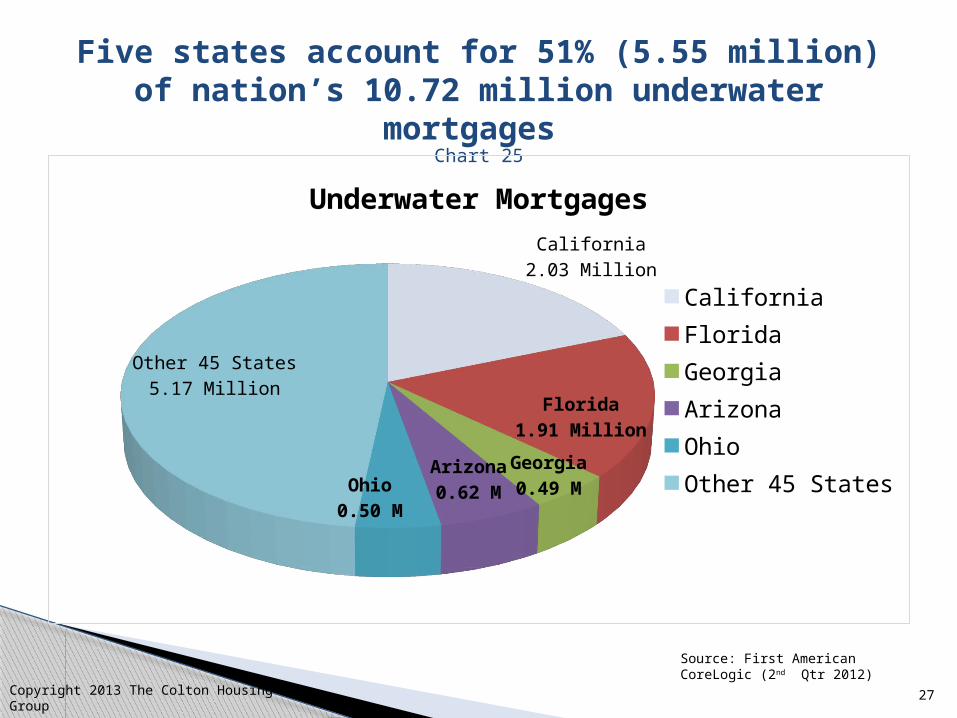

Five states account for 51% (5.55 million) of nation’s 10.72 million underwater mortgages

Chart 25

Source: First American CoreLogic (2nd Qtr 2012)

Copyright 2013 The Colton Housing Group

California2.03 Million

Florida1.91 Million

Georgia0.49 M

Arizona0.62 MOhio

0.50 M

Other 45 States5.17 Million

Underwater Mortgages

CaliforniaFloridaGeorgiaArizonaOhioOther 45 States

28

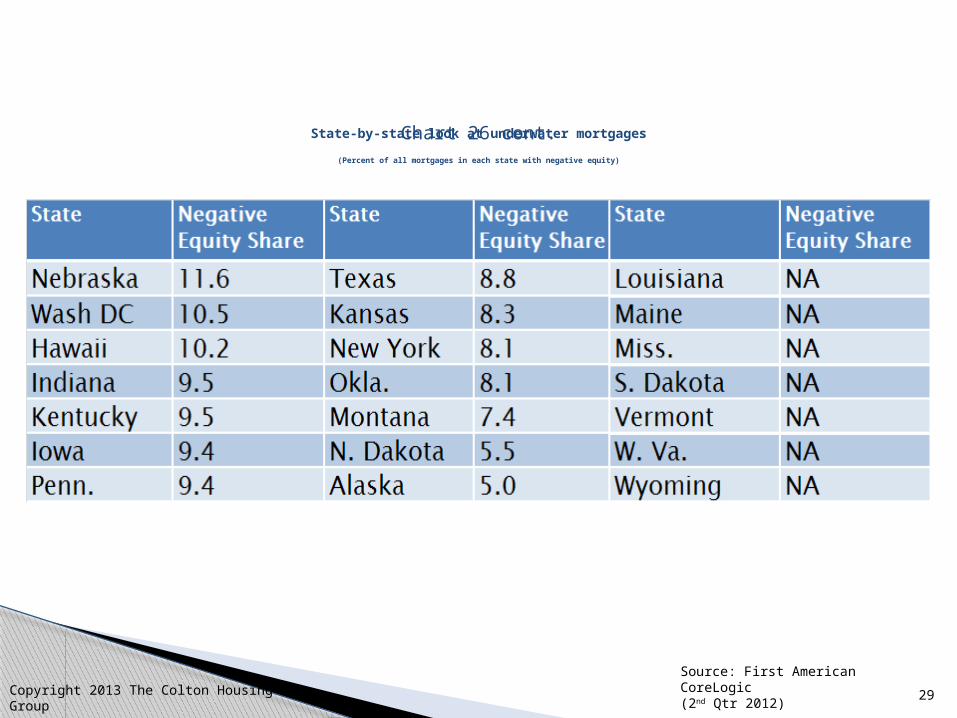

State-by-state look at underwater mortgages(as of 2nd Qtr 2012)

(Percent of all mortgages in each state with negative equity) Chart 26

Source: First American CoreLogic(2nd Qtr 2012)Copyright 2013 The Colton Housing Group

29

State-by-state look at underwater mortgages

(Percent of all mortgages in each state with negative equity)

Chart 26 cont.

Source: First American CoreLogic(2nd Qtr 2012)Copyright 2013 The Colton Housing Group

30

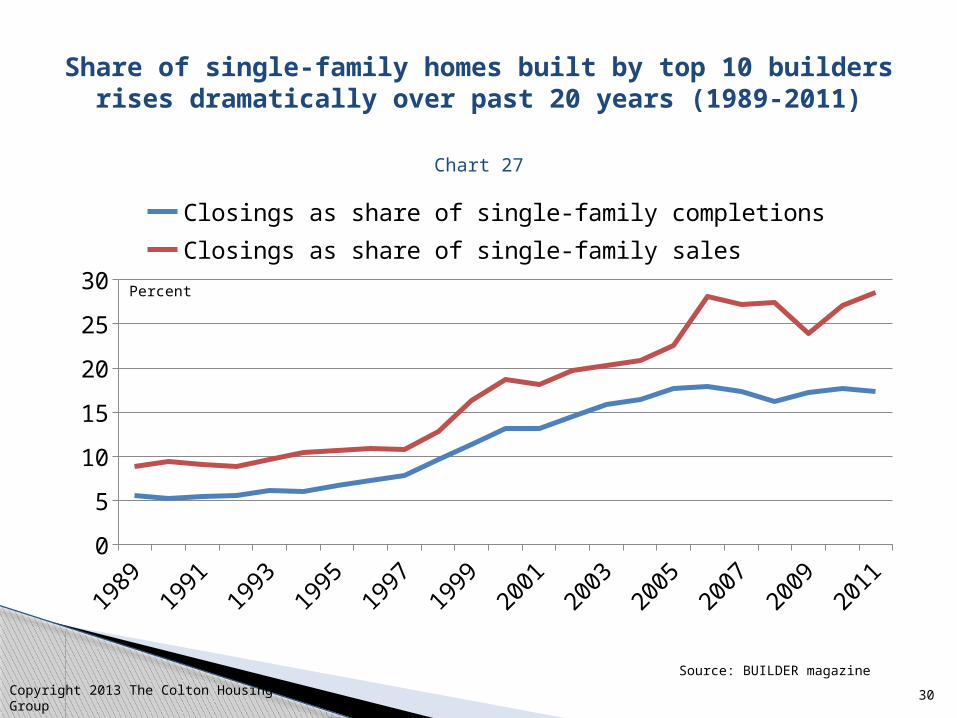

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

0

5

10

15

20

25

30

Closings as share of single-family completionsClosings as share of single-family sales

Percent

Share of single-family homes built by top 10 builders rises dramatically over past 20 years (1989-2011)

Source: BUILDER magazine

Chart 27

Copyright 2013 The Colton Housing Group

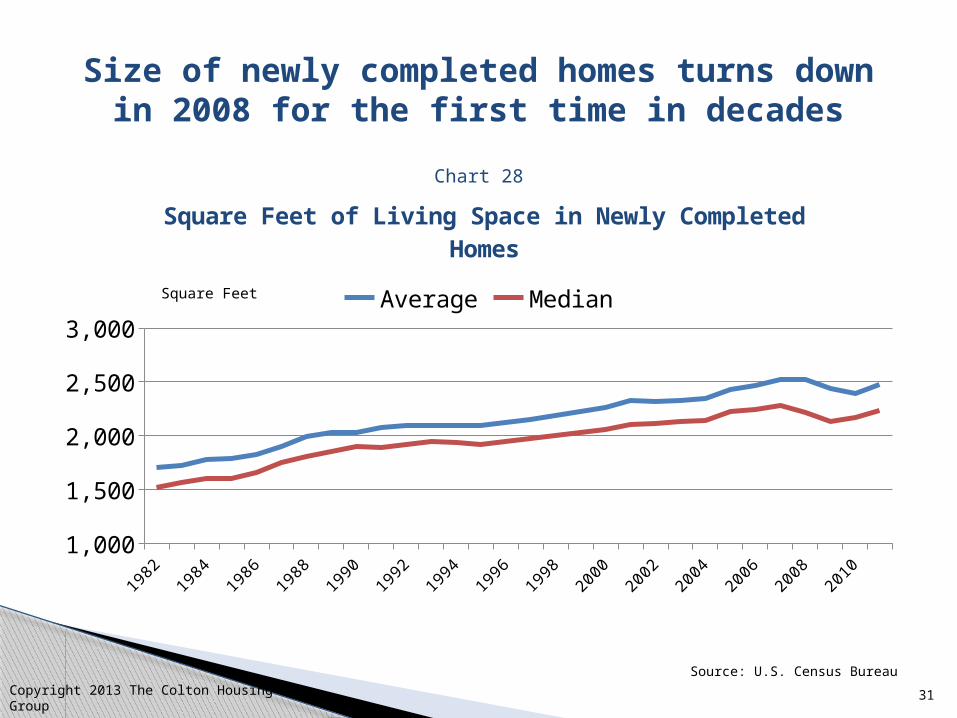

31

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

1,000

1,500

2,000

2,500

3,000

Square Feet of Living Space in Newly Completed Homes

Average Median

Size of newly completed homes turns down in 2008 for the first time in decades

Source: U.S. Census Bureau

Chart 28

Square Feet

Copyright 2013 The Colton Housing Group

32

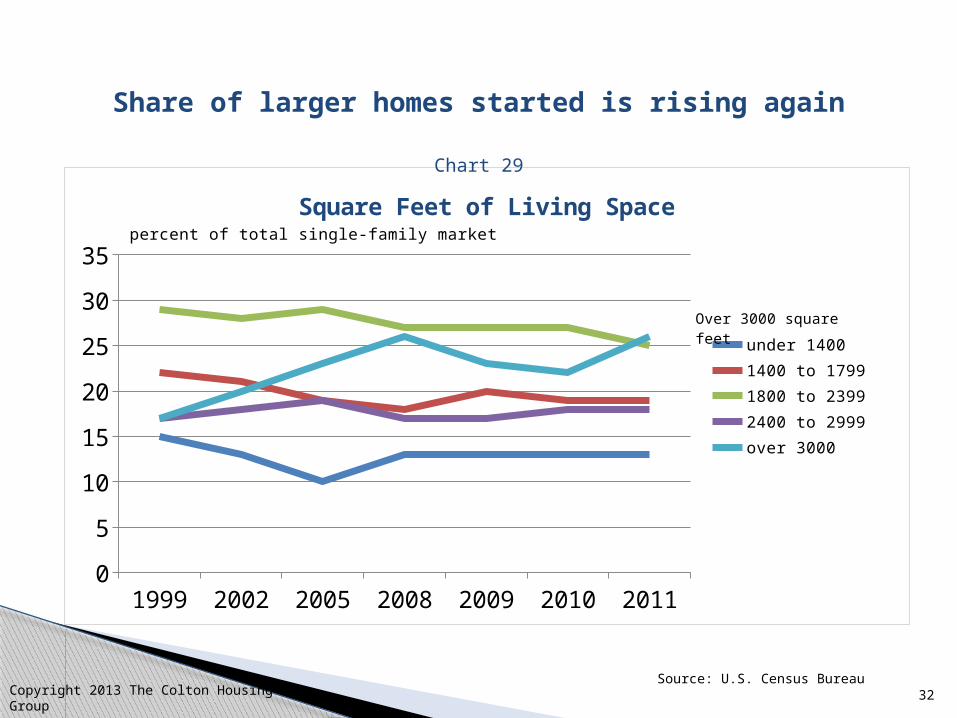

1999 2002 2005 2008 2009 2010 20110

5

10

15

20

25

30

35

Square Feet of Living Space

under 14001400 to 1799 1800 to 23992400 to 2999over 3000

percent of total single-family market

Over 3000 square feet

Share of larger homes started is rising again

Source: U.S. Census Bureau

Chart 29

Copyright 2013 The Colton Housing Group

33

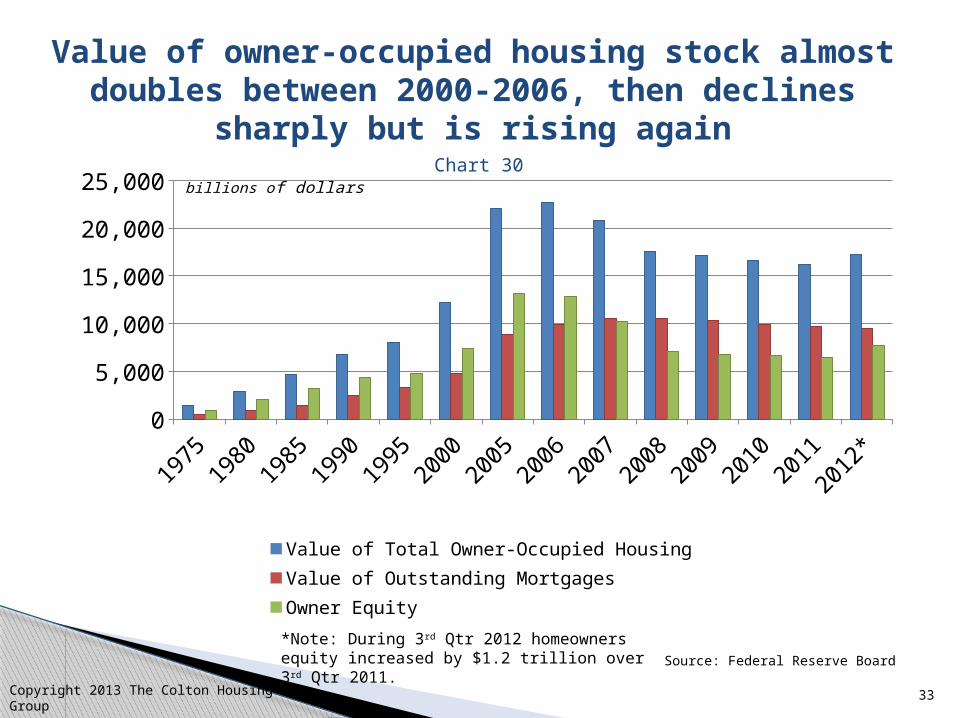

1975

1980

1985

1990

1995

2000

2005

2006

2007

2008

2009

2010

2011

2012

*0

5,000

10,000

15,000

20,000

25,000

Value of Total Owner-Occupied Housing Value of Outstanding Mortgages Owner Equity

billions of dollars

Value of owner-occupied housing stock almost doubles between 2000-2006, then declines

sharply but is rising again

Source: Federal Reserve Board

Chart 30

Copyright 2013 The Colton Housing Group

*Note: During 3rd Qtr 2012 homeowners equity increased by $1.2 trillion over 3rd Qtr 2011.

34

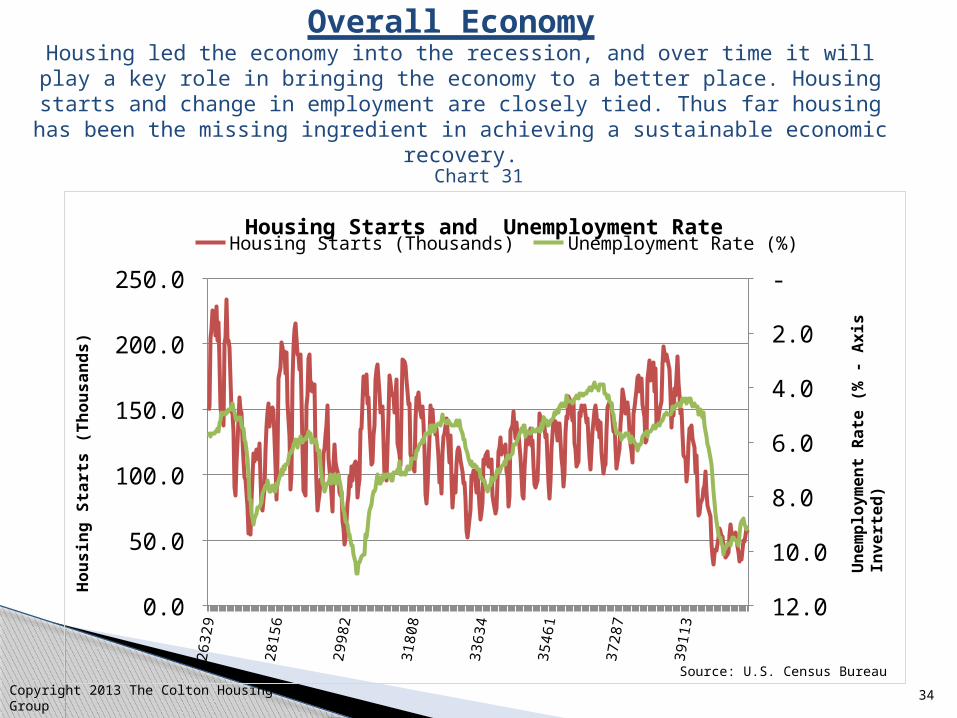

Overall Economy Housing led the economy into the recession, and over time it will play a key role

in bringing the economy to a better place. Housing starts and change in employment are closely tied. Thus far housing has been the missing ingredient in

achieving a sustainable economic recovery.

Source: U.S. Census Bureau

Chart 31

Copyright 2013 The Colton Housing Group

26

32

9

28

15

6

29

98

2

31

80

8

33

63

4

35

46

1

37

28

7

39

11

3

0.0

50.0

100.0

150.0

200.0

250.0 -

2.0

4.0

6.0

8.0

10.0

12.0

Housing Starts and Unemployment RateHousing Starts (Thousands) Unemployment Rate (%)

Housin

g S

tart

s (

Thousands)

Un

em

plo

ym

en

t R

ate

(%

- A

xis

In

vert

ed

)

35

2000

2002

2004

2006

2008

2010

2012*

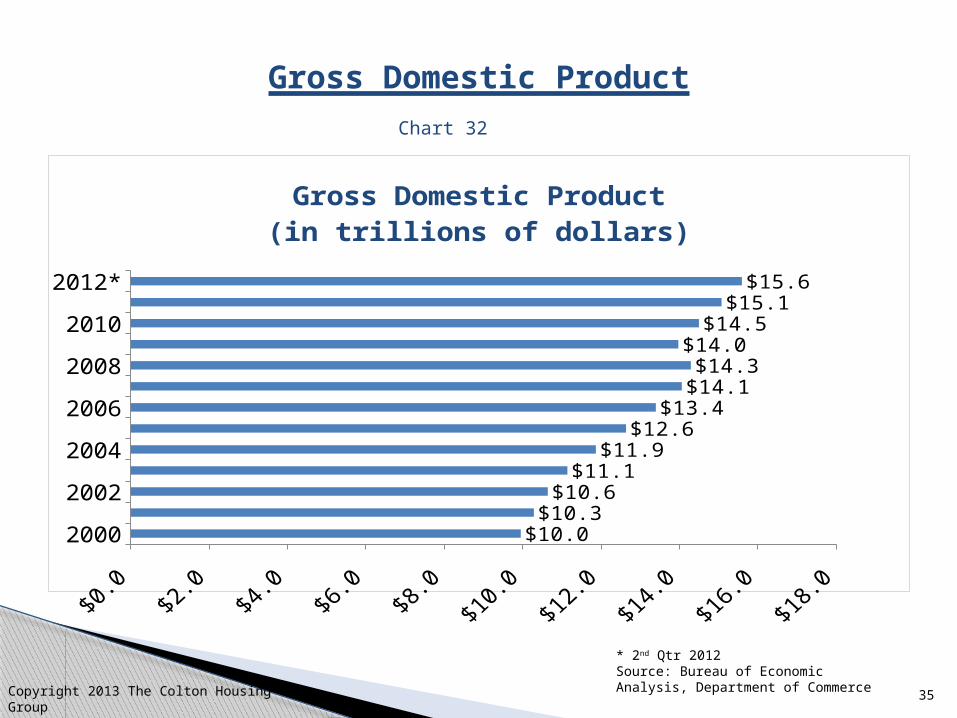

$0.0 $2.0 $4.0 $6.0 $8.0 $10.0 $12.0 $14.0 $16.0 $18.0

$10.0 $10.3

$10.6 $11.1

$11.9 $12.6

$13.4 $14.1 $14.3

$14.0 $14.5

$15.1 $15.6

Gross Domestic Product(in trillions of dollars)

Copyright 2013 The Colton Housing Group

Gross Domestic Product

* 2nd Qtr 2012Source: Bureau of Economic Analysis, Department of Commerce

Chart 32

36

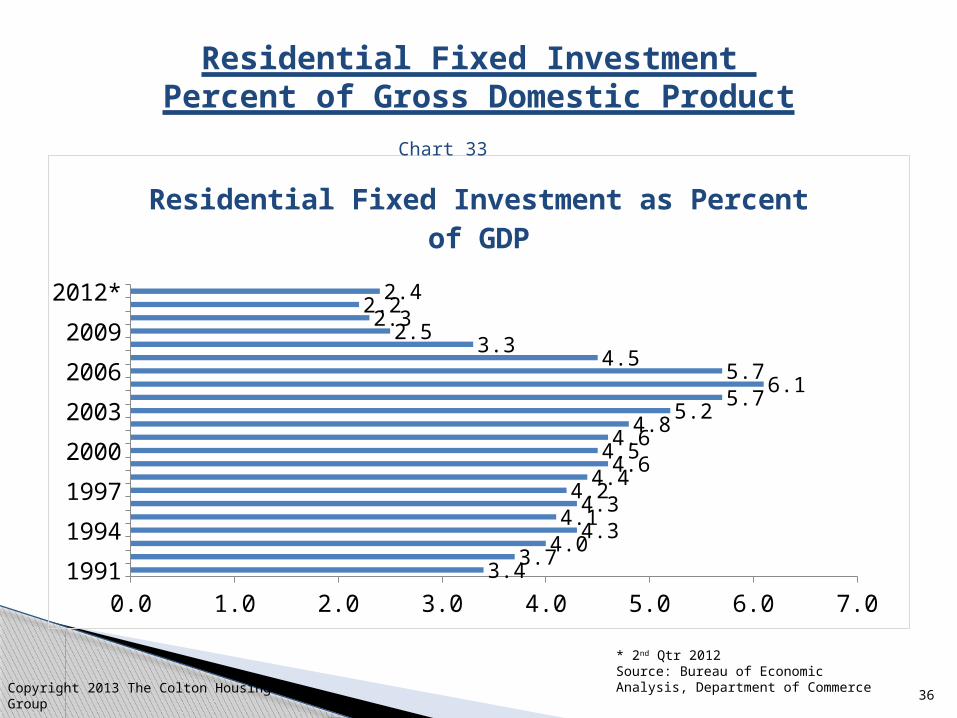

1991

1994

1997

2000

2003

2006

2009

2012*

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.03.4

3.74.0

4.34.1

4.34.2

4.44.6

4.54.6

4.85.2

5.76.1

5.74.5

3.32.5

2.32.2

2.4

Residential Fixed Investment as Percent of GDP

Copyright 2013 The Colton Housing Group

Residential Fixed Investment Percent of Gross Domestic Product

* 2nd Qtr 2012Source: Bureau of Economic Analysis, Department of Commerce

Chart 33

37

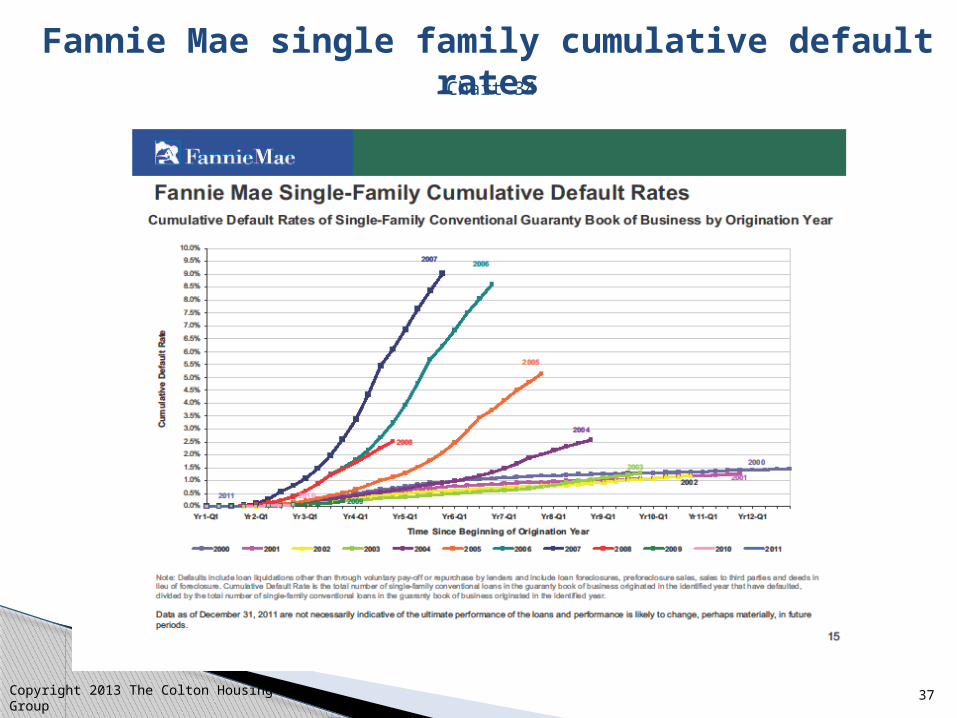

Fannie Mae single family cumulative default ratesChart 34

Copyright 2013 The Colton Housing Group

38

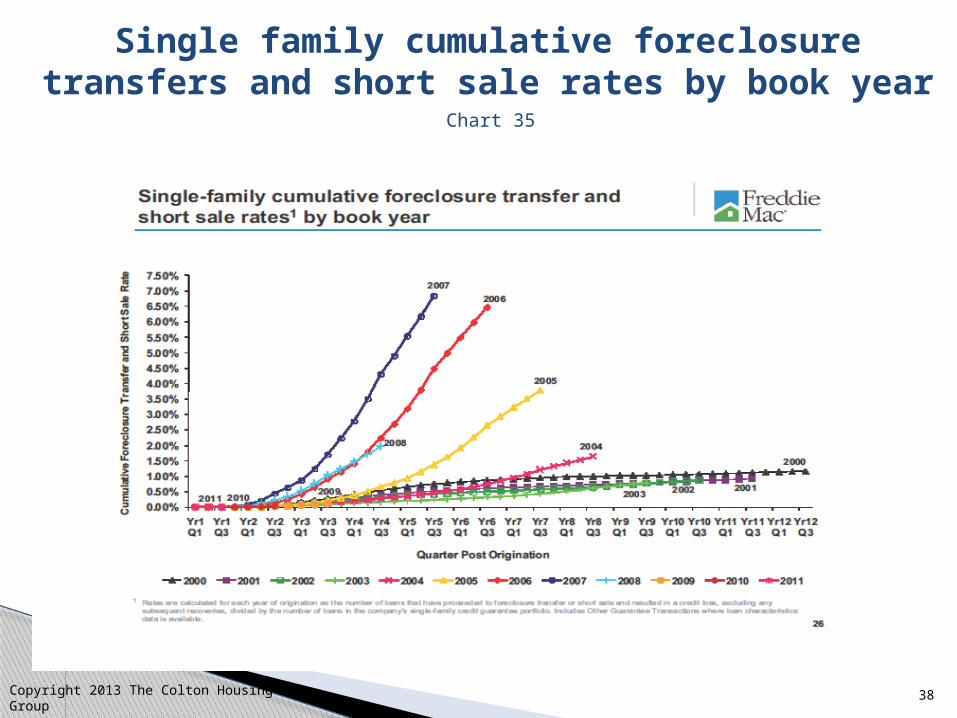

Single family cumulative foreclosure transfers and short sale rates by book year

Chart 35

Copyright 2013 The Colton Housing Group

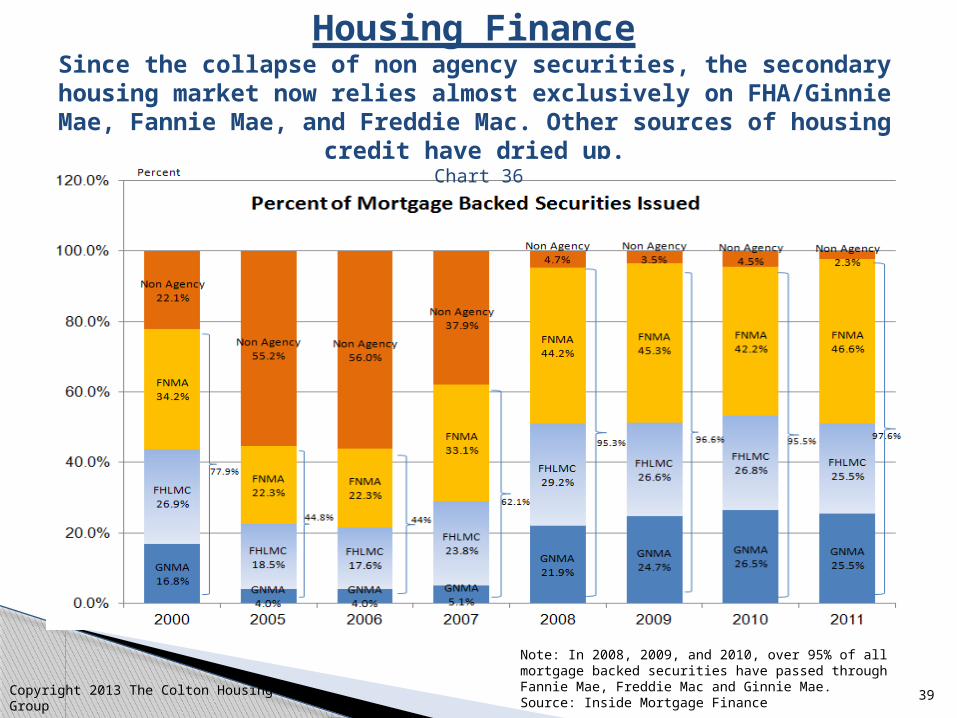

39

Since the collapse of non agency securities, the secondary housing market now relies almost exclusively on FHA/Ginnie Mae, Fannie Mae, and Freddie Mac. Other sources of housing

credit have dried up.

Note: In 2008, 2009, and 2010, over 95% of all mortgage backed securities have passed through Fannie Mae, Freddie Mac and Ginnie Mae.Source: Inside Mortgage Finance

Housing Finance

Copyright 2013 The Colton Housing Group

Chart 36

40

Foreclosure problem is generally concentrated in a select number of states.

Source: The State of the Nation’s Housing, 2010. Joint Center for Housing Studies of Harvard University, Table A-6, Page 39.

Chart 37

Foreclosure

Rate

Share of US Loans in

Foreclosure

Share of US Households with

Mortgages Foreclosure

Rate

Share of US Loans in

Foreclosure

Share of US Households

with MortgagesUnited States 4.6 100.0 100.0 Missouri 2.1 0.9 2.1Florida 14.0 23.6 6.2 Louisiana 3.4 0.8 1.2California 5.2 14.8 10.2 Utah 3.4 0.7 0.9Illinois 5.8 5.0 4.5 Kentucky 3.3 0.7 1.4New York 4.3 4.3 5.0 Oklahoma 3.0 0.6 1.1New Jersey 6.2 3.9 2.9 Alabama 2.2 0.6 1.5Ohio 4.9 3.5 4.2 Idaho 3.7 0.5 0.5Arizona 5.9 3.4 2.1 Iowa 2.8 0.5 1.1Georgia 3.9 3.2 3.3 Hawaii 4.8 0.4 0.3Texas 2.1 3.2 6.8 Mississippi 3.1 0.4 0.8Michigan 4.4 3.0 3.7 New Mexico 3.1 0.4 0.6Nevada 10.4 2.8 0.9 Kansas 2.3 0.4 1.0Pennsylvania 2.9 2.3 4.3 Maine 4.6 0.3 0.5Maryland 4.0 2.1 2.2 Delaware 3.7 0.3 0.3Indiana 4.5 1.9 2.4 Arkansas 2.1 0.3 0.9North Carolina 2.3 1.6 3.2 Rhode Island 3.6 0.2 0.3Minnesota 3.3 1.5 2.2 New Hampshire 2.6 0.2 0.5Virginia 2.1 1.5 2.9 Nebraska 1.9 0.2 0.6Massachusetts 3.4 1.4 2.2 District of Columbia 3.0 0.1 0.2Colorado 2.8 1.4 1.9 Vermont 2.7 0.1 0.2Washington 2.3 1.3 2.4 West Virginia 2.2 0.1 0.6Wisconsin 3.5 1.2 2.1 Montana 1.9 0.1 0.3South Carolina 3.4 1.1 1.5 South Dakota 1.8 0.1 0.3Connecticut 3.9 1.0 1.3 Wyoming 1.7 0.1 0.2Oregon 3.3 1.0 1.3 Alaska 1.3 0.1 0.2Tennessee 2.4 1.0 2.1 North Dakota 1.2 0.0 0.2

Copyright 2013 The Colton Housing Group

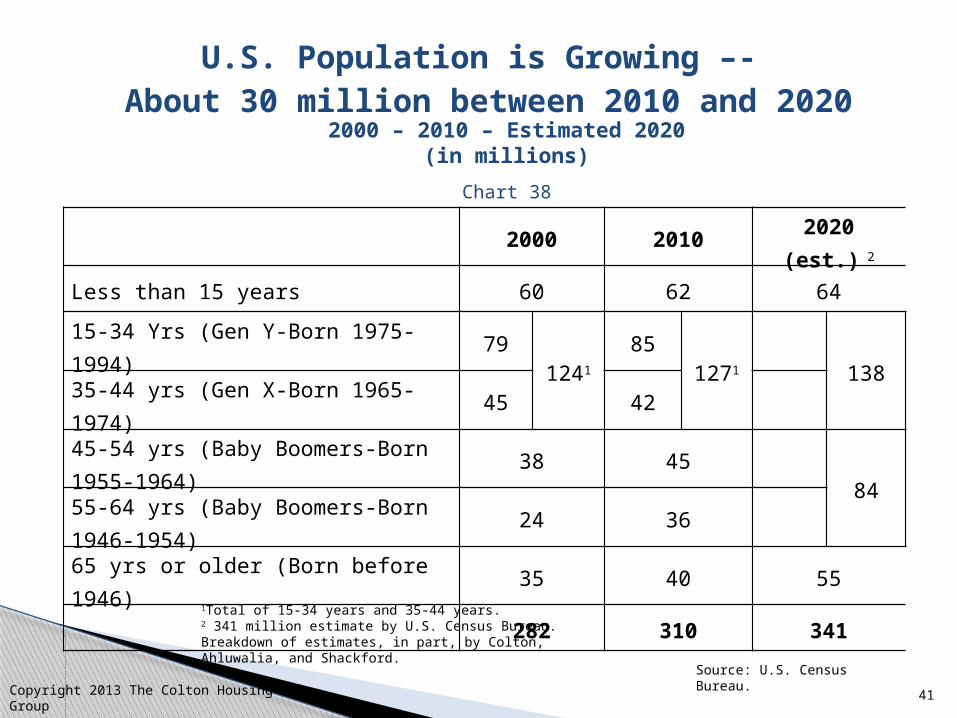

41

U.S. Population is Growing –- About 30 million between 2010 and 2020

Source: U.S. Census Bureau.

Chart 38

2000 2010 2020 (est.) 2

Less than 15 years 60 62 64

15-34 Yrs (Gen Y-Born 1975-1994) 791241

851271 138

35-44 yrs (Gen X-Born 1965-1974) 45 42

45-54 yrs (Baby Boomers-Born 1955-1964) 38 4584

55-64 yrs (Baby Boomers-Born 1946-1954) 24 36

65 yrs or older (Born before 1946) 35 40 55

282 310 341

1Total of 15-34 years and 35-44 years.2 341 million estimate by U.S. Census Bureau. Breakdown of estimates, in part, by Colton, Ahluwalia, and Shackford.

2000 – 2010 – Estimated 2020(in millions)

Copyright 2013 The Colton Housing Group

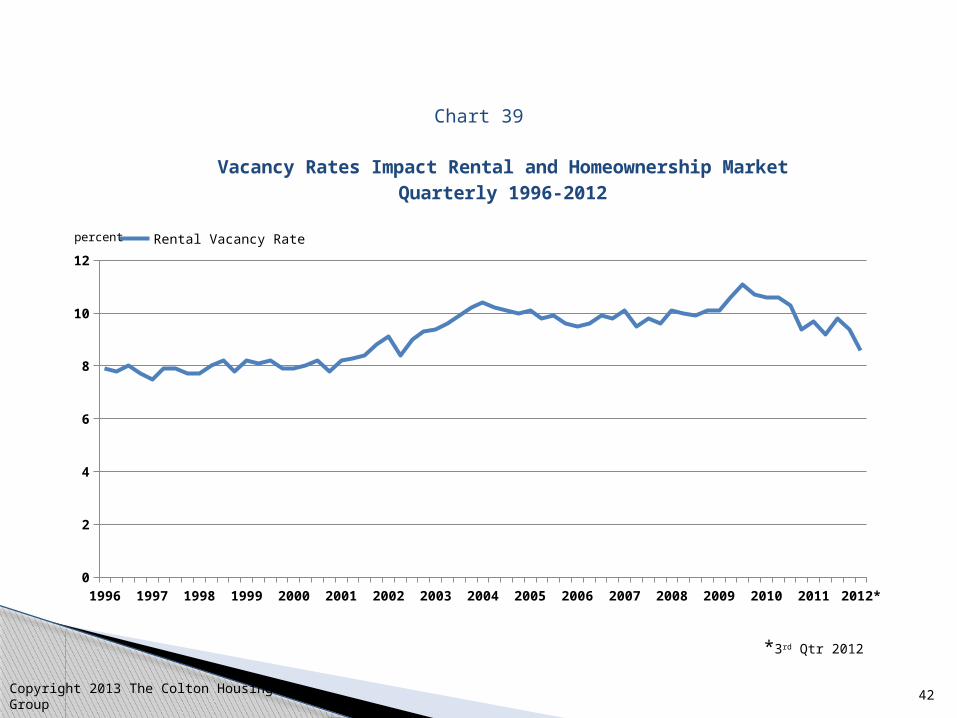

42

Chart 39

Copyright 2013 The Colton Housing Group

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012*0

2

4

6

8

10

12

Vacancy Rates Impact Rental and Homeownership MarketQuarterly 1996-2012

Rental Vacancy Ratepercent

*3rd Qtr 2012