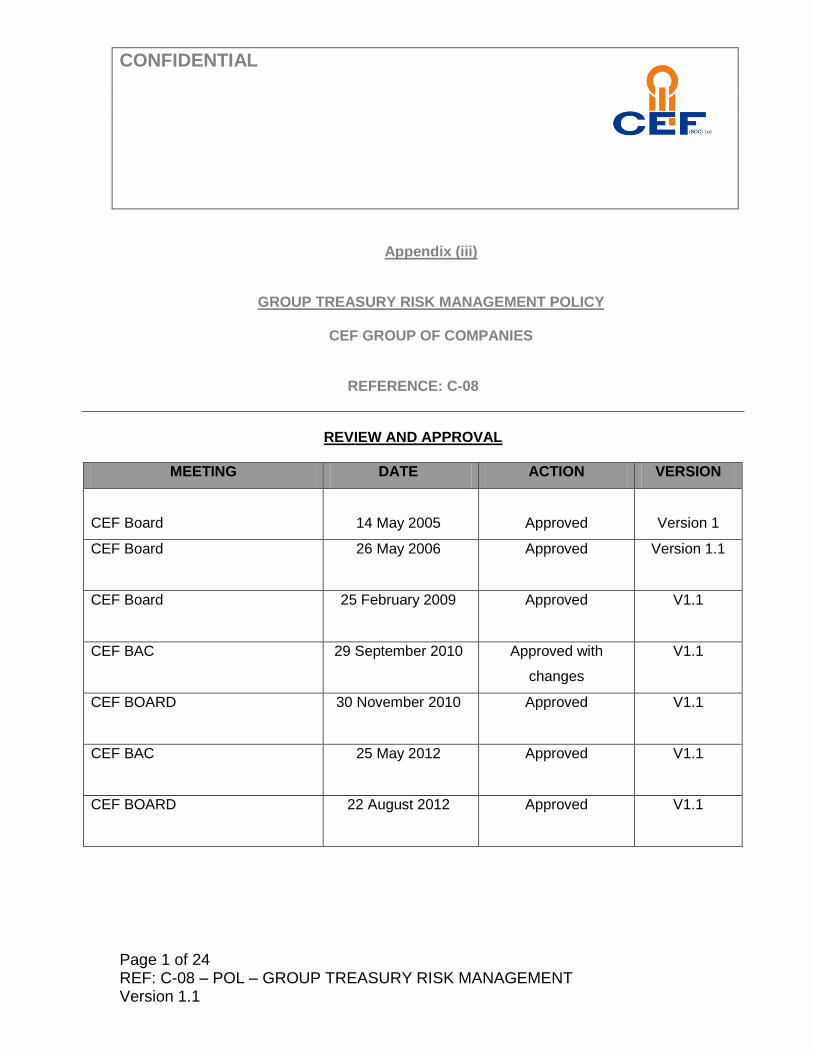

CONFIDENTIAL Page 1 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1 Appendix (iii) GROUP TREASURY RISK MANAGEMENT POLICY CEF GROUP OF COMPANIES REFERENCE: C-08 REVIEW AND APPROVAL MEETING DATE ACTION VERSION CEF Board 14 May 2005 Approved Version 1 CEF Board 26 May 2006 Approved Version 1.1 CEF Board 25 February 2009 Approved V1.1 CEF BAC 29 September 2010 Approved with changes V1.1 CEF BOARD 30 November 2010 Approved V1.1 CEF BAC 25 May 2012 Approved V1.1 CEF BOARD 22 August 2012 Approved V1.1

Transcript

CONFIDENTIAL

Page 1 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

Appendix (iii)

GROUP TREASURY RISK MANAGEMENT POLICY

CEF GROUP OF COMPANIES

REFERENCE: C-08

REVIEW AND APPROVAL

MEETING DATE ACTION VERSION

CEF Board

14 May 2005

Approved

Version 1

CEF Board 26 May 2006 Approved Version 1.1

CEF Board 25 February 2009 Approved V1.1

CEF BAC 29 September 2010

Approved with

changes

V1.1

CEF BOARD 30 November 2010

Approved V1.1

CEF BAC

25 May 2012 Approved V1.1

CEF BOARD 22 August 2012 Approved V1.1

CONFIDENTIAL

Page 2 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

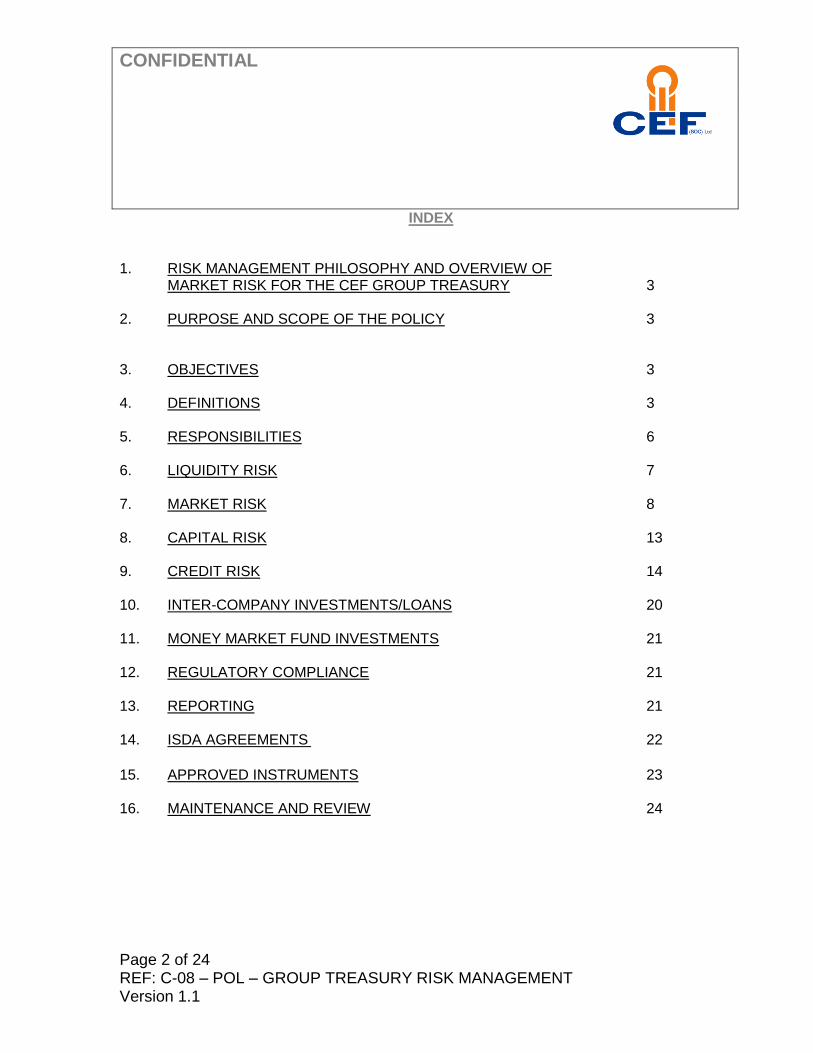

INDEX

1. RISK MANAGEMENT PHILOSOPHY AND OVERVIEW OF MARKET RISK FOR THE CEF GROUP TREASURY 3 2. PURPOSE AND SCOPE OF THE POLICY 3 3. OBJECTIVES 3 4. DEFINITIONS 3 5. RESPONSIBILITIES 6 6. LIQUIDITY RISK 7 7. MARKET RISK 8 8. CAPITAL RISK 13 9. CREDIT RISK 14 10. INTER-COMPANY INVESTMENTS/LOANS 20 11. MONEY MARKET FUND INVESTMENTS 21 12. REGULATORY COMPLIANCE 21 13. REPORTING 21 14. ISDA AGREEMENTS 22

15. APPROVED INSTRUMENTS 23 16. MAINTENANCE AND REVIEW 24

CONFIDENTIAL

Page 3 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

1. RISK MANAGEMENT PHILOSOPHY AND OVERVIEW OF MARKET RISK

FOR CEF GROUP TREASURY

Companies in the CEF Group operate in the financial markets where there is uncertainty and volatility in the market with regard to commodities, interest rates and currency.

2. PURPOSE AND SCOPE OF THE POLICY

The purpose of this policy is to ensure that the CEF Group minimises its risks with regard to: - Liquidity Risk - Market Risk - (i) Currency risk - (ii) Interest rate risk - Credit (Counterparty) risk - Capital risk

The scope of this Policy extends to all companies, legal entities and joint ventures in the CEF Group where the financials are consolidated into the results of the Group or where CEF exercises management and control. Furthermore, this Policy also applies to all other companies and legal entities in which CEF may have a significant interest or influence and any other entity that may form part of the CEF Group by way of a Ministerial Directive.

3. OBJECTIVES

Capital preservation Ensuring sufficient liquidity available to meet cash flow needs Maximise the yield subject to various constraints placed on the portfolio Manage risk appropriately

4. DEFINITIONS

4.1 Bonds: Fixed or variable rate interest bearing instruments (normally issued for periods of longer than one year) with known cash flows coupons and capital redemption. These instruments are quoted and valued using a yield and standard pricing formula. Government, parastatals, corporates and banks, may issue bonds from time to time.

4.2 Corporate paper: bonds, money market or other financial instruments issued by corporate or other non-banking entities.

CONFIDENTIAL

Page 4 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

4.3 Concentration Risk is the risk of an uneven distribution in the placing of investments with any one type of asset or counterparty. It is important to diversify any cash portfolio thus ensuring that the concentration risk is not too high.

4.4 Money Market instruments are shorter term financial instruments (generally less than one year in tenor, but can include instruments with final maturities of 3 years in the case of floating rate instruments) and are issued in a variety of forms including Negotiable certificates of deposits (NCD’s), Promissory Notes etc. These instruments can be issued by government, parastatals, banks, corporates or other entities.

4.5 Credit ratings are issued by a variety of independent and internationally recognised rating agencies, which attempt to capture an indication of the level of credit risk one bears in holding any particular instrument issued by a third party and are categorised into short and long term ratings.

These ratings, provided by the different rating agencies, can be divided into

Global Scale Ratings, also known as International or offshore ratings, as well as National Scale Ratings, also known as the Domestic rating or local ratings. It is important to note that all agencies have their own methodologies for classifying bonds, money market instruments as well as companies.

The CEF Group subscribes to one of the rating agencies to get an independent

and up to date view of the credit risk of the instrument and the counter party. The rating agency to which we subscribe will be the rating that will be used. CEF Group currently subscribes to Moody’s Rating Agency. Ratings of other agencies

must be noted and managed when known.

4.6 Repurchase Agreement (Repo): is a transaction whereby two parties agree to do two deals as a package. The first deal is a purchase or sale of a security, normally a government bond, for delivery against payment. The second deal is the reversal of the first deal for settlement on another date in the future, at a price that takes into account the cost of borrowing in the market. Reverse Repurchase Agreement (Reverse Repo); the same as a Repo as above, but from the perspective of the buyer rather than the seller.

4.7 Subordinated Debt: debt where the holder has a claim which is junior to the claim of debt specified as senior. Subordinated debt issues generally make up large portions of Tier 2 capital of South African registered banks.

CONFIDENTIAL

Page 5 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

4.8 Call Bonds: are a specific category of money market instruments with a tenor of between 2 and 31 days.

4.9 Cross Currency Swap: A cross currency swap is an agreement between two

parties to exchange obligations on different currencies. 4.10 Forward Rate Agreement (FRA): A FRA is a contract with a bank on a forward

interest rate which calls for an exchange of payment based on an interest rate (be it Jibar or libor etc.) at a future date in return for payment based on a fixed rate of interest agreed on the contracting date.

4.11 Interest Rate Swap: An interest rate swap is an agreement between two parties

to exchange streams of interest payments over a predetermined period. Interest rate swaps are used to hedge interest rate exposure, Implement short-term asset/liability management strategies, reduce funding cost and restructure debt mix.

4.12 Interest Rate Cap – An Interest Rate Cap is a contract whereby the purchaser

limits its floating rate to a specified rate of interest for a period of time. An Interest Rate Cap is a Call Option with a sequence of Caplets on Jibar or Libor (etc.) organized to correspond to a multi-period floating rate loan based on Jibar or Libor etc.

4.13 Interest Rate Floor – An Interest Rate Floor is a contract whereby the purchaser

locks in a minimum rate of interest for a specified period of time. An Interest Rate Floor is a Put Option with a sequence of Caplets on Jibar or Libor organised to correspond to a multi-period floating rate loan based on Jibar or Libor etc.

4.14 Interest Rate Collar – An Interest Rate Collar is an agreement whereby a

company simultaneously buys a Cap (Liability hedge: Cap exposure) and sells a Floor to the bank or the Company sells a Cap to the bank and buys a Floor from the bank (guarantee minimum return). Intuitively, a Collar would result from a combination of a Call and a Put Option on Jibar or Libor etc.

4.15 Weighted Average Maturity is a measure of the average, weighted, term to

maturity of a set of cash flows or financial assets held in a portfolio. 4.16 Uncommitted Cash – is the cash buffer or free cash to meet emergencies i.e.

not needed to meet working capital payments or known capital purchases.

4.17 Liquid Assets – Assets in the form of cash or any type of negotiable assets that can be converted quickly and easily into cash with little or no impact on price.

CONFIDENTIAL

Page 6 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

4.18 JIBAR RATE– Johannesburg Interbank Agreed Rate. The Jibar Rate is a rate

that is independently derived from quotes obtained from a number of different banks for deposits in ZAR for relevant periods, which appear daily on SAFEX Screen page at 11h00a.m. It is therefore an independent market benchmark rate. This is the money market rate used in South Africa.

4.19 NACM RATE – Nominal Annual, Compounded Monthly. Banks calculate the interest daily and compound, or add the interest monthly. Calculated over a year, the nominal annual compounded monthly rate (nacm rate) becomes what the banks talk about, an effective rate

4.20 An Issuer - is a legal entity that develops registers and sells securities for the

purpose of financing its operations. Issuers may be governments, corporations etc. Issuers are legally responsible for the obligations of the issue and for reporting financial conditions, material developments etc. Types of securities issued are bonds, stocks, debentures, notes, bills etc. Securities are also referred to as the product. The credit rating of securities (bonds as an example) asses the credit worthiness of a corporation’s debt issued. The credit rating is a financial indicator to potential investors of debt securities such as bonds. The credit rating assigned to a security (bond) represents the quality of a security (bond).

4.21 MONEY MARKET FUND (MMF) – An investment vehicle which pools funds

(cash) from investors. These funds are invested as per the MMF’s investment mandate in the financial instruments with a maturity date of no longer than one year. The return on the investment portfolio is calculated daily in arrears (converted to NACM). The interest is paid monthly in arrears less a management fee. Management fees are agreed upfront.

5. RESPONSIBILITIES 5.1 Senior Manager Treasury

The responsibilities of the Senior Manager Treasury are to ensure that the policy is reviewed annually in conjunction with the whole group to ensure execution and adherence of policy.

5.2 Treasury Dealer

The responsibility of the Money Market and Forex Dealer is to ensure execution of policy.

CONFIDENTIAL

Page 7 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

6. LIQUIDITY RISK

6.1 Definition:

Liquidity risk is the risk that the Group will not be able to meet its financial obligations as they fall due. The Group’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Group’s reputation.

6.2 Adequate cash resources or access to adequate cash is required to meet

immediate financial demands. Factors that must be considered in liquidity risk management of a cash portfolio

are: - The difficulty to liquidate the assets (Money market instruments)

- The ability to trade the assets/instruments (The negotiability of the assets) - The length of time to maturity. - The economic impact of selling a security into the secondary market should be Economically acceptable to meet the liquidity needs.

6.3 Liquid assets include: a) Cash b) Call and Term investments c) Negotiable certificates of deposits (NCD) d) Debentures (Primary & Secondary) e) Treasury Bills f) Corporate and Government Bonds g) Repo’s and Reversed Repo’s h) Corporate and Government Paper i) Promissory notes (PN)

6.4 Liquidity management The most optimal way of managing liquidity risk is to structure the cash assets of the Group into a short duration fund (for meeting the immediate liquidity needs of the business) and longer dated fund (the Core Fund – which will take advantage of the liquidity premiums and wider investment universe that is available for assets with a longer maturity). The short term fund is to be termed the Liquid Portfolio and the longer dated fund to be called the Core Portfolio. The Liquid and Core portfolio have different parameters for such key factors as performance benchmarks, average weighted duration, liquidity levels, negotiability of instruments (for liquidity purposes), maximum maturities etc. These are covered specifically in each Portfolio category in the document below.

CONFIDENTIAL

Page 8 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

Refer to Section 8.3.3 for Liquidity Parameters for Liquid and Core Portfolio.

6.5 Liquidity Requirements:

a) Uncommitted cash buffer to meet emergencies (cash, liquid assets and/or

overdraft facilities) as defined by each company in the Group. b) Minimum interest and capital cover of one year, based on interest and capital

payable on interest bearing borrowings provided that all required debt covenants are met.

c) Adequate liquid assets to cover all committed cash requirements e.g. guarantees, abandonment, business interruption, and loan interest and capital repayments.

d) Monitoring of the cash requirements will be monthly by management and quarterly by the board.

6.6 Risk Mitigation Techniques

In mitigating liquidity risks the group strives to ensure that loan and overdraft facilities of appropriate terms are available and that revenue match loan redemption commitments.

7. MARKET RISK Market risk is the risk that the value of an investment will decrease due to changes in market risk factors. The market risk factors are: - Equity risk, the risk that stock prices will change. - Commodity risk, the risk that commodity prices will change

(e.g. Crude oil, metals, grain etc.) - Currency risk, the risk that foreign exchange rates will change. - Interest rate risk, the risk that interest rates will change.

These factors will affect the Group’s income or the value of its holdings of financial instruments. The objective of market risk management is to manage and control market risk exposure within acceptable parameters, while optimizing the return.

Treasury manages currency risk and interest rate risk.

CONFIDENTIAL

Page 9 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

7.1 CURRENCY RISK 7.1.1 Definition Currency risk is the effect that exchange rate movements have on the value of

assets, liabilities and the income statement. 7.1.2 Management of Currency Risk

Exchange rate movements may cause business exposures that are complex, and often not obvious. Exposure periods may range from relatively short periods for current assets and liabilities, to several years in the case of long term borrowings/receivables.

7.1.3 The foreign exchange risk management covers the following transactions in foreign currencies for local operations as well as offshore operations:

a) Selling oil, petroleum and chemical products in foreign currency; b) Purchasing raw material such as condensate and consumables offshore, in

foreign currency; c) Purchasing capital equipment offshore in foreign currency; d) Incurring foreign currency borrowing commitments to fund capital expenditure

and working capital requirements. These are interest, foreign finance charges or fees on foreign borrowings;

e) Investing in offshore operations; or f) Making joint venture cash call payments in foreign currencies; g) Incurring foreign currency commitments to purchase services.

7.1.4 Natural Hedge Principle

The net currency position in relation to foreign currency export proceeds and import commitments will be managed in accordance with the natural hedge principle.

Where local sales of finished products are sold on a foreign currency denominated basis it also leads to a situation where foreign currency denominated inflows can be matched with foreign currency outflows, thus creating a natural hedge to manage foreign currency exposures.

CONFIDENTIAL

Page 10 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

It is however important to note that this does not represent a perfect hedge due to the timing differences associated with the receipt of the ZAR denominated revenues and payment of the foreign currency commitments. The company will be allowed to enter into foreign exchange transactions to hedge this timing mismatch. Hedging techniques under the natural hedge principle consist of the matching of payables and receivables e.g.

a) Receivables: Sales directly in a foreign currency or Sales in ZAR but determined by the reference prices (Basic Fuel Price - BFP)

converted to the ruling ZAR/Forex exchange rates b) Payables: Purchasing of finished products; Purchasing raw material such as condensate and consumables offshore, in

foreign currency; Purchasing capital equipment offshore in foreign currency; Incurring foreign currency borrowing commitments to fund capital expenditure

and working capital requirements; Incurring foreign currency commitments to pay interest and other foreign

finance charges or fees on foreign borrowings; investing in offshore operations; or

Making joint venture cash call payments in foreign currencies Incurring foreign currency commitments to purchase services

A Customer Foreign Currency (CFC) overdraft facility can be utilised if the cost of hedging is found to be more expensive than the interest charge associated to the overdraft facility. A Customer Foreign Currency (CFC) account will only be allowed to go into overdraft with prior approval from the relevant bank, considering the credit lines afforded to the group

7.1.5 No Natural Hedge Principle

In the event that a natural hedge is not apparent, the group should actively manage the “unhedged/open” exposures as soon as a firm and ascertainable commitment and/or accrual have been established. Cognisance should be taken of the latest Exchange Control Regulations, as updated from time to time.

7.1.6 Hedging Techniques

The CEF Group is allowed to enter into currency derivatives in order to hedge exchange rate risks.

CONFIDENTIAL

Page 11 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

Derivatives may only be used for the purposes of “hedging or protecting the portfolio from risk. Derivatives must be used in accordance with the following principles: a) Derivatives are not permitted to be used for speculative and/or gearing

purposes. b) The Group must hold the underlying asset in the Portfolio to cover the full

exposure (i.e. no “naked” positions may be taken). c) The Group is not allowed to write options other than in combination with

purchased options where there is a perfect match in both nominal and term i.e. collar positions.

The use of the CFC account is considered a synthetic hedge as the principles for calculating the forward points are emulated through the use of a CFC overdraft.

7.1.7 Daily exchange rates for the CEF Group of Companies

The Reuters/Bloomberg 11h00 exchange rates (for each different currency) will be used to set the daily exchange rates. All foreign transactions in the group will be converted in the group using the 11h00 daily exchange rates. At each month end, the rate will be agreed between all treasuries in the group. The Basic Fuel Price (BFP) is calculated at the 11h00 rate and by using this

exchange rate the assets and liabilities are converted at the same rate. 7.2 INTEREST RATE RISK 7.2.1 Definition

Interest rate risk is defined as the potential for increased costs to the borrower due to higher interest rates, or the potential for reduced income to a lender/investor due to lower interest rates. Interest rate risk is, therefore, the risk of a negative impact from interest rate changes on a company’s earnings, profitability or the viability of a project. Interest rate exposure and trends must be reported monthly to company investment committees and management and quarterly to the board. The Group is exposed to market risk relating to interest rate fluctuations in local and foreign markets. Assets as well as liabilities are impacted by these fluctuations. Interest rate movements have an impact on cashflow in the case of loans as well as book values of assets and liabilities measured at fair value.

CONFIDENTIAL

Page 12 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

7.2.2 Management of Interest Rate Risk pertaining to Group Liabilities

This interest rate risk relates to the interest payable on long term loan capital (longer 3 years), which if driven high for reasons, which do not equally drive project revenues higher, may adversely affect project economics.

For any one project (longer than three years) 30 – 50% of the financing must be at fixed interest rates based on the interest rate trend over the term of the loan. Any deviations from this must be specifically approved by the relevant board.

If strong volatility risk threatens, the interest rate risk can then be further mitigated by the use of hedging instruments (refer to 6.2.4)

7.2.3 Management of Interest Rate Risk pertaining to Group Assets

The interest rate risk on assets relates to the exposure that the companies in the Group have on interest rate movements on its surplus Rand and foreign currency funds. It is therefore practice to invest funds for as long as possible in a market of falling interest rates and as short as possible in a market of rising interest rates.

7.2.4 Hedging of Interest Rate Risk

Treasury must determine the financial instrument that will mitigate the risk in the most favourable way. It’s important to operate within the context of the shareholder-defined limits and choose the optimal hedging structure for a particular exposure and economic environment. Treasury should also be able to tailor the hedging strategy so that it mitigates the risk in a way that is acceptable to the view of the senior management and the board of directors.

Interest rate risk can be hedged by utilising the following approved derivative instruments:

Note that all over-the counter (OTC) derivatives and should be limited to approved counterparties and must be included in the counterparty limits for credit risk management purposes.

The Group may not enter into any speculative positions.

CONFIDENTIAL

Page 13 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

The Group is prohibited from writing options other than in combination with purchased options where there is a perfect match in both nominal and term i.e. collar positions.

7.2.5 Interest Rate Return Benchmarks

The Benchmarks must be quantifiable, easy to measure and not open to manipulation. The group benchmarks should be revisited and recalibrated on an annual basis, if there is a significant change in market conditions. The responsibility for obtaining and recommending benchmarks vests with the Treasury Managers. Benchmarks must be approved by the CEF board at a group level. JIBAR: Johannesburg Interbank Agreed Rate. The Jibar Rate is the mid-market rate of deposits in ZAR for relevant periods, which appear daily on Safex Screen page at or about 11h00a.m. It is therefore an independent market benchmark rate. JIBAR plus or minus a margin will be used to set the benchmark on money market investments Core Portfolio and the JIBAR SARB Interbank call rate on Liquid Portfolio.

8. CAPITAL RISK 8.1 Definition

Capital Risk is the risk the Group will lose all or part of the principal amount invested. The Group should strive to manage its capital to ensure that entities in the Group will be able to continue as a going concern while maximizing the return to stakeholders through optimization of the debt and equity balance.

8.2 Gearing ratio

The Group has a target gearing ratio gearing ratio of 20 – 30% debt determined as the proportion of net debt to equity for each project. The maximum group balance sheet gearing must not exceed the Debt Covenants requirements of existing loans. Currently this is 60 percent.

CONFIDENTIAL

Page 14 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

Projects should be funded to the greatest extent possible with borrowed funds thus preserving free cash flow for development activities and/or distribution to shareholders. This is subject to the maintenance of appropriate gearing and to the cost of finance in relation to the project being financed. As borrowing facilities are not available for exploration, all exploration will be funded internally.

In all instances, the project needs to generate a return in excess of the entity’s weighted average cost of capital after taking into account the funding requirements. The group strives to raise finance over a long enough term, lowest cost and best terms so that revenue streams flowing from projects are sufficient to service the interest and the capital redemption commitments in respect of the loans raised to finance the projects. Failure to do so creates risks that a funding shortfall arises if the group’s financiers call up short-term loans. The Debt to Equity ratio must be reviewed on an annual basis by taking into account the Debt Covenants of existing loans.

9. CREDIT (COUNTERPARTY) RISK 9.1 Definition Credit risk is the risk of financial loss to the Group if a customer or a counterparty

to a financial instrument fails to meet its contractual obligations, and arises principally from the Group’s receivables and investment securities. The degree of risk involved is (theoretically) reflected in the borrower’s credit rating. It is key to ensure that the credit risk taken in the cash portfolios is diversified and does not exceed the risk appetite of CEF Group, either on an individual counterparty or industry sector basis.

9.2 Management of Credit (Counterparty) Risk

The PFMA requires that a public entity must have an investment policy that is approved by the accounting authority.

Funds may only be invested according to this Board approved policy. Any deviation from this policy requires CEF Board approval.

Primary and Secondary securities maybe bought or sold from or to Brokers, provided settlement risk is eliminated. All settlements and delivery must be done through the authorised Trade Reporting Agent.

CONFIDENTIAL

Page 15 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

9.3 Counterparty Ratings

It is critical to obtain independent information of counterparty ratings. As such, the Group will subscribe to at least one rating agency, whose Long Term Issuer ratings (National Scale Ratings) for South African issuers and Global Scale Ratings for International issuers will apply. The Group subscribes to International Rating Agencies.

To take cognisance of foreign currency moratorium risk inherent in South Africa, there is a distinction between Long Term Foreign currency deposit ratings and LT Domestic deposit ratings for local (South African) banks. As such the National Scale Ratings exclude the moratorium risks. There is no such differentiation for foreign banks. Although Moody’s have attempted to map the NSR to the GSR, the inherent moratorium risk results in the mapping spanning over more than one rating, and the resultant rating bands. As a result, CEF Group has separated the rating bands for local and foreign banks. For comparative purposes, and in the event that the issuer does not possess a Moody’s rating, the comparable ratings of the two additional ratings agencies are included in this table. The short term ratings are opinions as to the ability of the obligors to honour financial obligations with an original maturity of twelve months or less. As such, the CEF Group has determined that the long term rating will apply, regardless of the duration of the investment.

In order to assess the risk associated with local investors, the Long Term National Scale ratings (also known as Long Term Bank Deposit Rating) will apply. Money Market Fund investment mandates must comply with this policy.

CONFIDENTIAL

Page 16 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

9.4 Investment Mandate:

LIQUID PORTFOLIO

CORE PORTFOLIO

a) Description

A short dated maturity fund, aimed at meeting the immediate liquidity needs of the business.

A longer dated fund, which takes advantage of the liquidity premiums, that is available for assets with a longer maturity.

b) Benchmark Return

JIBAR SARB Interbank call rate. JIBAR plus or minus a margin

c) Liquidity Parameters

i. A minimum of 0.5% of the Liquid Portfolio is to be available within 24 hours notice

ii. The portfolio must have a maximum weighted average maturity of 120 days.

iii. The term to maturity of any one instrument may not exceed one year

i. A minimum of (1)% of the Core Portfolio is to be available within one month notice

ii. The maximum maturity of any one instrument is limited to three years.

iii. The portfolio must have a maximum weighted average maturity of 365 days.

9.4.1 Counterparty Parameters

a) Concentration Limits

National Rating Band as Per Table

in 8.4.9 International Rating Band

as Per Table i 8.4.10

Total Investment Exposure

Limit Per band

Issuer Limit as a % of Market Value of Asset Comprising

the Portfolio

1

100%

25% of pool

2

50%

20% of pool

3

10%

10%

CONFIDENTIAL

Page 17 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

b) Long term and short term Ratings

The Long term rating is the most prudent approach, regardless of the

term of the investment.

c) Breach of Limits)

If any limit prescribed in this policy is breached, through no default of Treasury (i.e. rating downgrade; sudden reduction in total cash holding) Treasury must reduce the exposure to within limits within the earliest time possible. Failing which, a detailed plan setting out remedial measures to be submitted to the General Manager Finance CEF/PetroSA CFO and reported to CEF Investment Committee and PetroSA Group Assurance Committee. Limits are review weekly or same day with a downgrade.

d) Instruments issued by the Government of South Africa

Treasury may invest up to 100 per cent of the market value of the underlying money market instruments comprising a portfolio in all instruments issued by the Government of the Republic, South African Reserve Bank, or any public entity as defined in the Public Finance and Management Act, 1999 (Act No.1 of 1999), and listed in terms of that Act as a Major Public Entity and National Public Entity, and not rated but carrying an explicit guarantee by the Government of the Republic. This includes investments at the Corporation for Public Deposits (CPD).

e) Investments in local subsidiaries of a foreign entity

Treasury may invest up to the percentage indicated in the Table in 8.4.10 of the market value of the underlying securities comprising a portfolio in all instruments issued by a local subsidiary of a foreign entity or concern and that foreign entity or concern guarantees that instrument, and where that foreign entity or concern is assigned a long-term rating on the international rating scale

f) Mapping of National Scale Ratings and Global Scale Ratings

In the absence of a national scale rating of the instruments, issuers or guarantors of such instruments, the relevant instruments, issuers or guarantors, whether such issuer or guarantor is a local entity, has been assigned a Global Scale or International Rating the latest mapping table of the Rating Agency can be used to determine the National Scale Rating.

g) Exclusions

Money market instruments in the Portfolio – (i) having no fixed maturity; or (ii) in respect of which the interest rate is not known at the date of inclusion may not be included in the portfolio.

This excludes Money Market Funds, whose rates are only known the day after investment date.

CONFIDENTIAL

Page 18 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

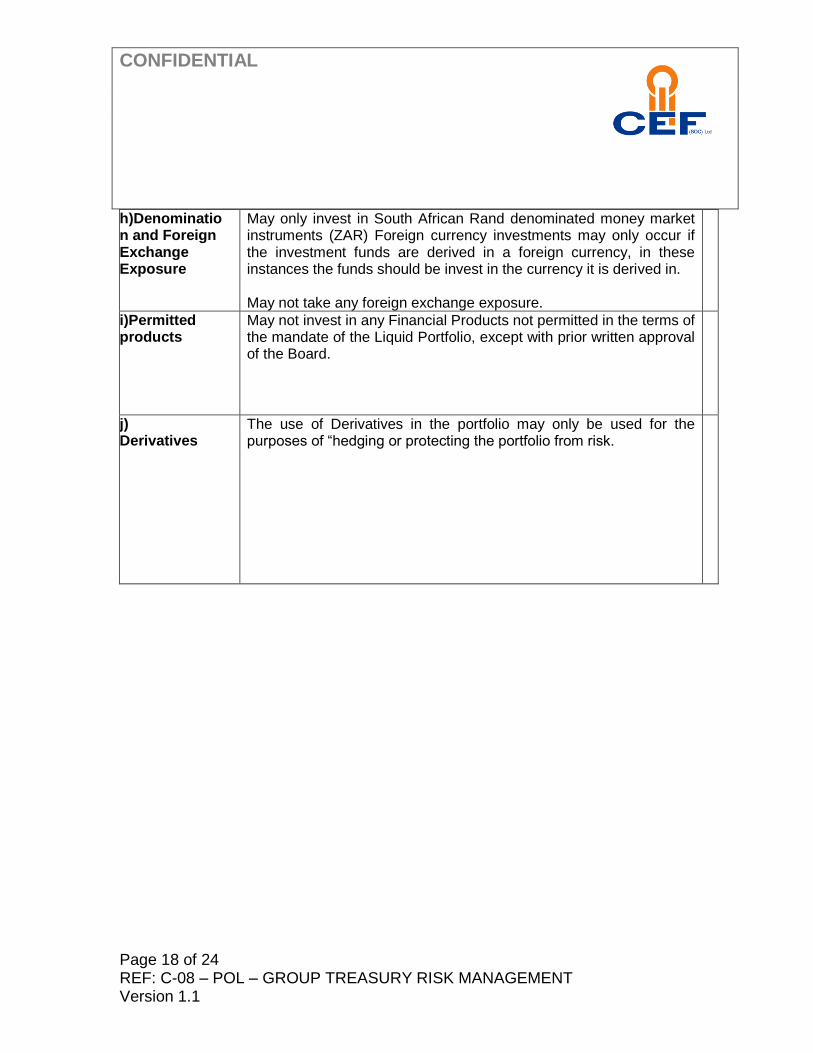

h)Denomination and Foreign Exchange Exposure

May only invest in South African Rand denominated money market instruments (ZAR) Foreign currency investments may only occur if the investment funds are derived in a foreign currency, in these instances the funds should be invest in the currency it is derived in. May not take any foreign exchange exposure.

i)Permitted products

May not invest in any Financial Products not permitted in the terms of the mandate of the Liquid Portfolio, except with prior written approval of the Board.

j) Derivatives

The use of Derivatives in the portfolio may only be used for the purposes of “hedging or protecting the portfolio from risk.

CONFIDENTIAL

Page 19 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

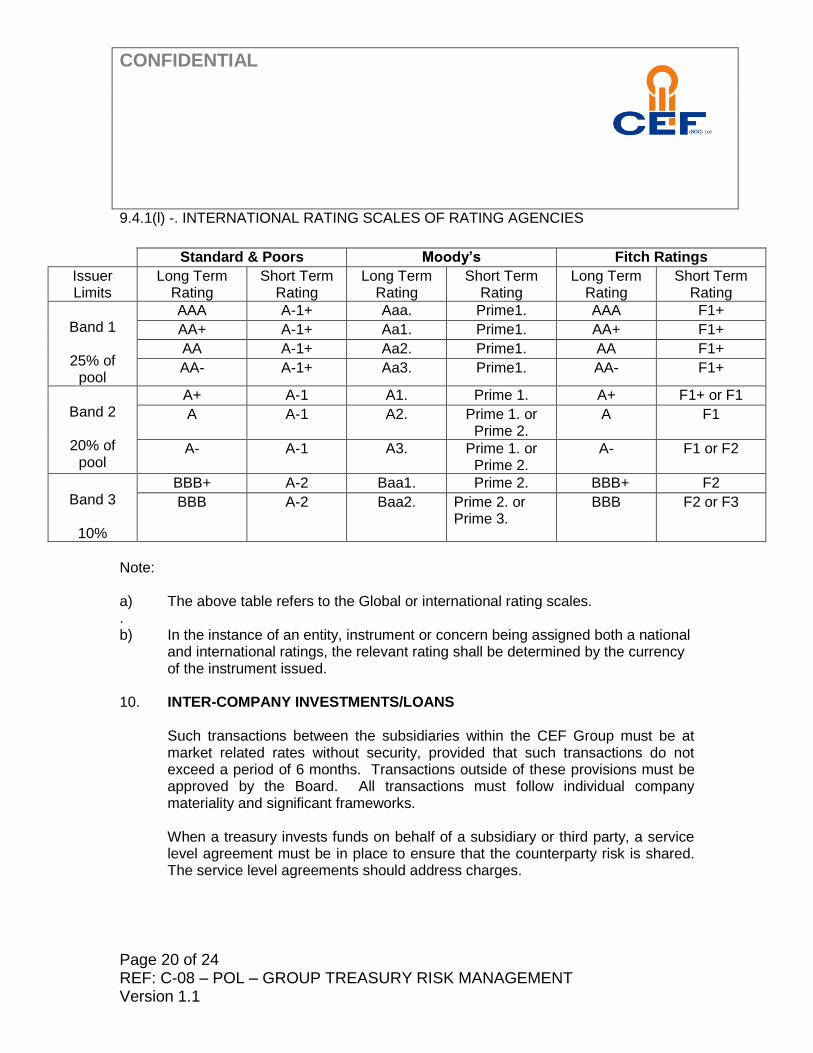

9.4.1(k) - NATIONAL RATING SCALES OF RATING AGENCIES

Note: a) The above table refers to the domestic or national rating scales.

S&P Moody’s Fitch Ratings

Issuer Limits

Long Term

Rating

Short Term

Rating

Long Term

Rating

Short Term

Rating

Long Term

Rating

Short Term

Rating

Band: 1 Limit: 25%

e.g. ABSA, Nedbank, Standard & FNB

AAA A-1+ Aaa.za Prime 1.za

AAAzaf F1+zaf

AA+

A-1+

Aa1.za

Prime 1.za

AA+zaf

F1+zaf

AA

A1+

Aa2.za

Prime 1.za

AAzaf

FI+zaf

Band: 2 Limit: 20% e.g.

Investec

AA-

A-1+

Aa3.za

Prime 1.za

AA-zaf

F1+zaf

A+ A-1 A1.za Prime 1.za

A+zaf F1+zaf Or F1zaf

Band: 3

Limit: 10%

A A-1 A2.za Prime 1.zaor Prime 2.za

Azaf F1zaf

A- A-2 A3.za Prime 1.zaor Prime 2.za

A-zaf F1zaf or F2zaf

N.A.

BBB+ A-2 Baa1.za Prime 2.za

BBB+zaf F2zaf

BBB A-2 Baa2.za Prime 2.zaor Prime 3.za

BBBzaf F2zaforF3zaf

CONFIDENTIAL

Page 20 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

9.4.1(l) -. INTERNATIONAL RATING SCALES OF RATING AGENCIES

Note: a) The above table refers to the Global or international rating scales. . b) In the instance of an entity, instrument or concern being assigned both a national

and international ratings, the relevant rating shall be determined by the currency of the instrument issued.

10. INTER-COMPANY INVESTMENTS/LOANS

Such transactions between the subsidiaries within the CEF Group must be at market related rates without security, provided that such transactions do not exceed a period of 6 months. Transactions outside of these provisions must be approved by the Board. All transactions must follow individual company materiality and significant frameworks.

When a treasury invests funds on behalf of a subsidiary or third party, a service level agreement must be in place to ensure that the counterparty risk is shared. The service level agreements should address charges.

Standard & Poors Moody’s Fitch Ratings

Issuer Limits

Long Term Rating

Short Term Rating

Long Term Rating

Short Term Rating

Long Term Rating

Short Term Rating

Band 1

25% of

pool

AAA A-1+ Aaa. Prime1. AAA F1+

AA+ A-1+ Aa1. Prime1. AA+ F1+

AA A-1+ Aa2. Prime1. AA F1+

AA- A-1+ Aa3. Prime1. AA- F1+

Band 2

20% of

pool

A+ A-1 A1. Prime 1. A+ F1+ or F1

A A-1 A2. Prime 1. or Prime 2.

A F1

A- A-1 A3. Prime 1. or Prime 2.

A- F1 or F2

Band 3

10%

BBB+ A-2 Baa1. Prime 2. BBB+ F2

BBB A-2 Baa2. Prime 2. or Prime 3.

BBB F2 or F3

CONFIDENTIAL

Page 21 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

11. MONEY MARKET FUND INVESTMENTS The selection criteria for money market funds must be in line with this

policy, in terms of rating of the underlying asset, concentration limits, and liquidity and yield.

Additional selection criteria:

The fund must be rated by at least one of the major ratings agencies, the ratings of which must meet the criteria set out in section 8.4(k) and 8.4(l) above.

CEF group may not hold more than 10% of the specific money market fund

As funds pass through the fund manager, settlement risk must be suitably mitigated by contractual documentation.

12. REGULATORY COMPLIANCE

The implementation of this policy shall comply with the regulations of all relevant legislative and governing bodies inter alia:

a) PFMA Act b) Ministerial Directives c) Board of Directors resolutions d) The CEF & PetroSA Group’ related Policies e) Security Services Act 36 (2004) f) Financial Institutions (Protection of Funds) Act g) Marketable Securities Tax Act h) South African Reserve Bank

13. REPORTING 13.1 Performance evaluation will be conducted in terms of the portfolio performance

relative to the benchmark, performance target and risk guidelines.

13.2 The Treasurers shall furnish the relevant CEF investment committee/ PetroSA Group Assurance Committee with the written reports:

a) Monthly reports

CONFIDENTIAL

Page 22 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

13.3 On a quarterly basis, the Treasurers shall present the performance,

benchmarking, returns, risk management and compliance pertaining to this policy to the relevant Boards.

13.3 The Treasurer will then also provide the CEF Investment Committee/PetroSA Group Assurance Committee with a treasury risk management strategy review for the prior period and will discuss the likely risk management strategy for the ensuing period.

13.5 Should the guidelines in this mandate be transgressed, the Treasurer must notify

the General Manager Finance CEF/CEF Investment Committee/PetroSA Group Assurance Committee, in writing within 3 working days. This notification must be followed up with a detailed action plan to rectify this breach, in writing, within 10 working days, together with the quantification of any losses suffered.

13.6 Respective risk management committees should be notified of any related issues, which may impact the portfolio performance

14. ISDA AGREEMENTS WITH BANKS

14.1 Introduction

This agreement is used to document transactions between parties located in the same jurisdiction and transactions involving one currency. This agreement is designed, among other things, to facilitate cross-product netting and may be used to document a wide variety of derivatives transactions.

14.2 ISDA Master Agreement 14.2.1 The agreement is accepted as the definitive agreement for governing privately

negotiated Over the Counter derivative transactions in every significant legal jurisdiction.

14.2.2 The principal benefit provided by this agreement is that it creates an “agreement”

as envisaged by Section 35(B) of the South African Insolvency Act. This section was introduced in 1995 and brought to an end many years of speculation as to the right of a liquidator to “cherry pick” between exposures created by exchange traded and OTC derivative transactions. An ISDA Agreement therefore ensures that in an insolvency situation full rights of set-off (i.e. netting) exist for both parties.

14.2.3 The agreement contains sophisticated payment and close-out netting provisions

which, given the recognition of the enforceability of a set-off agreement, enable parties to account for exposures on a net rather than a gross basis. This also

CONFIDENTIAL

Page 23 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

means that Settlement Risk and Credit Risk are kept at the lowest possible levels.

14.2.4 Best practice recommendations by the Global Derivatives Study Group, which

formed part of their so-called “G30 Recommendations”, include: “Credit exposures on derivatives, and all other credit exposures to a counterparty,

should be aggregated taking into account enforceable netting arrangements.”, and

“Dealers and end users are encouraged to use one master agreement as widely

as possible with each counterparty to document existing and future derivatives transactions including foreign exchange forwards and options.”

These recommendations support the “single agreement approach” in a legal

relationship where the parties intend to transact OTC derivatives on an ongoing basis. It is best practise to negotiate general terms, which will apply to every transaction to be entered into (regardless of product types) and then proceed on the basis that those terms apply to a transaction unless otherwise agreed for the purposes of a specific transaction. This is indicative of the flexibility provided by the ISDA Master Agreement.

14.3 A general benefit provided by the agreement is that all rights and obligations created are mutual, creating no more rights or obligations for either party. The agreement therefore ensures that both parties receive equal protection in their derivative dealings.

14.4 The Legal Risk created by executing an agreement each time a transaction is

concluded or alternatively, recording the salient terms of a transaction on a short confirming document in the absence of an executed master agreement, is substantially avoided. This also provides contracting parties with the opportunity to negotiate one agreement for all OTC transactions.

14.5 The cost reduction which flows from the aforementioned cannot be quantified as

it is rather a matter of avoiding unwanted and therefore, unnecessary costs. It is recommended to enter into an ISDA Agreement for long term relationships with derivative counterparties.

15. APPROVED INSTRUMENTS Any instrument, whose issuance meets the criteria as set out in this policy, is an

approved instrument. Some examples follow, but are not limited to: Bonds

CONFIDENTIAL

Page 24 of 24 REF: C-08 – POL – GROUP TREASURY RISK MANAGEMENT Version 1.1

Corporate paper Negotiable certificates of deposit Promissory notes Capital project bills Repos Call bonds Cross currency swaps Interest rate swaps Interest rate caps/floors Forward rate agreements Fixed/floating rate notes Options Futures Money market funds 16. MAINTENANCE AND REVIEW

This policy must be reviewed annually to ensure that it is up to date and appropriate and all changes must be communicated by the CEF Treasury Manager to all relevant parties in the CEF Group as appropriate.

All changes must be approved by the CEF BAC and CEF BOARD.