CAPITAL INVESTMENT APPRAISAL: APPRAISAL PROCESS AND METHODS Objectives: Describe the nature of capital investment appraisal Apply the main investment appraisal techniques Recognise the limitations of investment appraisal technique 1

Transcript

1

CAPITAL INVESTMENT APPRAISAL: APPRAISAL PROCESS AND METHODS

Objectives:Describe the nature of capital investment appraisalApply the main investment appraisal techniquesRecognise the limitations of investmentappraisal technique

2

DEFINITION OF INVESTMENT

Any act which involves the sacrifice of an immediate and certain level of consumption in exchange for the expectation of an increase in future consumption.forgo the present consumption in order to increase resources in future

3

TYPES OF CAPITAL INVESTMENT

Replacement of obsolete assetsCost reduction e.g. IT systemExpansion e.g new building & equipmentStrategic proposal: improve delivery service, staff training.Diversification for risk reduction

4

NEED FOR INVESTMENT APPRAISAL

Large amount of resources are involved and wrong decisions could be costlyDifficult and expensive to reverseInvestment decisions can have a direct impact on the ability of the organisation to meet its objectives

5

INVESTMENT APPRAISAL PROCESS

Stages: identify objectives. What is it? Within the corporate objectives?Identify alternatives. Use CAD, CAM or use external service.Collect and analyse data. Examine the technical and economic feasibility of the project, cash flows etc.

6

INVESTMENT APPRAISAL PROCESS

Stages:decide which one to undertakeauthorisation and implementationreview and monitor: learn from its experience and try to improve future decision - making.

7

APPRAISAL METHODS

Payback method - length of time it takes to repay the cost of initial investment

1. Discounted Cash Flow (DCF) Criteria Net Present Value (NPV) Internal Rate of Return (IRR) Profitability Index (PI)

2. Non-discounted Cash Flow Criteria Payback Period (PB) Discounted Payback Period (DPB) Accounting Rate of Return (ARR)

PAYBACK METHOD

Payback could occur during a year

Can take account of this by reducing the cash inflows from the investment to days, weeks or years.

PAYBACK METHOD e.g.

Cost of machine = £600,000

Annual income streams from investment = £255,000 per year

Payback is some where between …Year 2 & year 3 it will pay back – but when?

Income

Year 1 255,000

Year 2 255,000

Year 3 255,000

Payback formula

= 600,000255,000

= 2.35 years

What’s just over a 1/3 of a year?= 4 months

= 2 years and 5 months…

Payback formula

2 years = 255,000 + 255,000 = 510,000

= 2 years & some months….

600,000 - 510,000 = 90,000 still owing

255,000 = 21,25012 months

= 90,000 = 4.235 month 21,250

= 2 years and 5 months…

10

PAYBACK PERIOD

Lecture Example 1LBS Ltd uses the payback period as its sole investment appraisal method. LBS invests £30,000 to replace its computers and this investment returns £9,000 annually for the five years. From the information above evaluate the investment using the payback. Assume that £9,000 accrues evenly throughout the year.

11

PAYBACK PERIODSolution 2.1Year Yearly cash flow cumulative net cash flow

£ £0 (30,000) (30,000)

1 9,000 (21,000

2 9,000 (12,000)

3 9,000 (3,000)

4 9,000 6,000 5 9,000 15,000

Therefore 3years = 27,000 then 3000/9000 x 12 = 4Payback period = 3 years 4months

12

EXAMPLE 2. You are faced with two investment opportunities which each cost £30,000 and which

have the net cash inflows shown in the table below.

Year Project A cash flows (£) Project B cash flows (£)

1 7500 5,000

2 7500 5,000

3 7500 6,000

4 7500 6,000

5 5000 8,000

6 0 15,000

7 0 15,000

Required:

a) Use the payback method to choose between the two projects.

b) Using a discount rate of 12%, which project has the faster payback?

13

EXAMPLE 2. SOLUTION

a) Undiscounted pay backFor A = 4 yearsFor B = 5 years

DISCOUNTED PAY BACK METHOD Takes into account the fact that money

values change with time

How much would you need to invest today to earn x amount in x years time?

Value of money is affected by interest rates

Shows you what your investment would have earned in an alternative investment regime

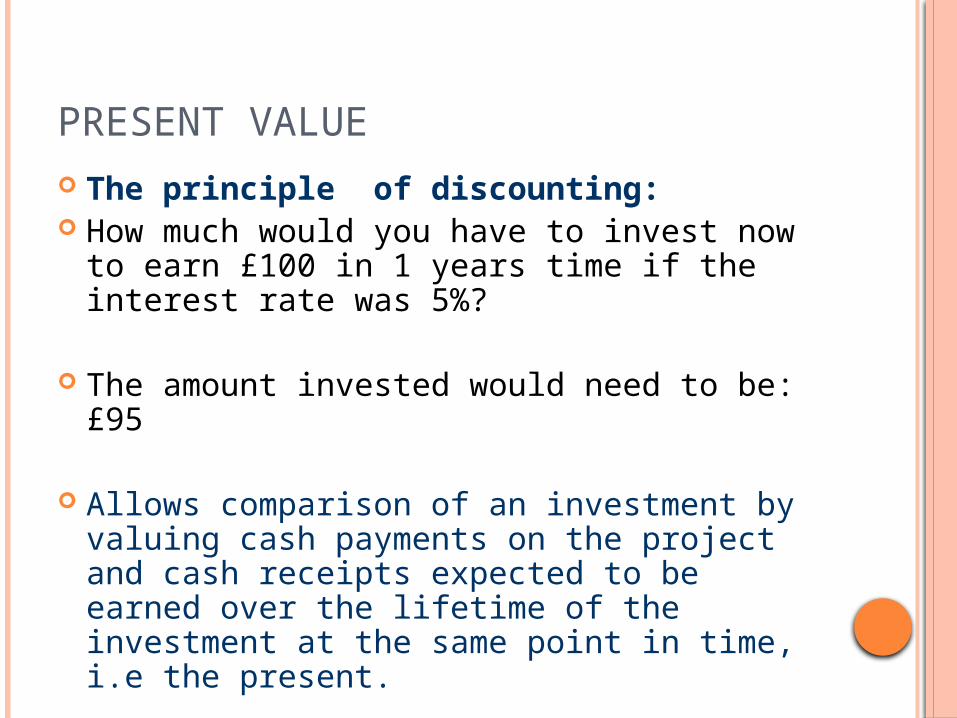

PRESENT VALUE The principle of discounting: How much would you have to invest now to

earn £100 in 1 years time if the interest rate was 5%?

The amount invested would need to be: £95

Allows comparison of an investment by valuing cash payments on the project and cash receipts expected to be earned over the lifetime of the investment at the same point in time, i.e the present.

PRESENT VALUE

Future ValuePV = ----------------- (1 + i)n

Where i = interest rate n = number of years

The Present Value of £1 @ 10% in 1 years time is 0.9090.

If you invested 0.9090p today and the interest rate was 10% you would have £1 in a years time

Process referred to as: ‘Discounting Cash Flow’

PRESENT VALUE

Cash flow x discount factor = present value

e.g. PV of £500 in 10 years time at a rate of interest of 4.25% = 500 x .6595373 = £329.77

£329.77 is what you would have to invest today at a rate of interest of 4.25% to earn £500 in 10 years time

PVs can be found through valuation tables (Always given to you in exams!)

Payback = 2 years & ??? Months Y3 400/12mths = £33.33 so need to repay

100 in 3rd year so in 2 years and 4 months

ARR = 1080 – 600 = 480 / 4 years = 120 /300 = 0.4 x 100 = 40%

23

ACCOUNTING RATE OF RETURN (ARR)

Accounting Rate of Return method relates average annual profit to either the amount

initially invested or the average investment, as a percentage.

Formulae:

ARR = Average annual accounting profit x 100

Average investment

Where:

Average annual profit = Total profit/Number of years

Average investment = (initial capital investment + scrap value) / 2

Average incomeARR =

Average investment

ACCEPTANCE RULE

This method will accept all those projects whose ARR is higher than the minimum rate established by the management and reject those projects which have ARR less than the minimum rate.

This method would rank a project as number one if it has highest ARR and lowest rank would be assigned to the project with lowest ARR.

25

LECTURE EXAMPLE

Using the data below, calculate the ARR. Project C Year 0 1 2 3 4 Cash flows (£45,000) 11,000 12,250 12,250 32,000 Depreciation (11,250) 11,250) (11,250) (11,250) Accounting profit

The ARR method may claim some meritsSimplicity Accounting data Accounting profitability

Serious shortcomingCash flows ignored Time value ignored Arbitrary cut-off

28

NET PRESENT VALUE

Net Present Value (NPV) - the difference between the present values of cash inflows and outflows of an investmentOpportunity cost of undertaking the investment is the alternative of earning interest rate in the financial market.

29

NPV

Net Present Value of an Investment is the present value of all its present and future

cash flows, discounted at the opportunity cost of those cash flows. NPV is

mathematically represented as:

nn

r

CF

r

CF

r

CF

r

CFCFNPV

)1(.....

)1()1()1( 33

22

11

0

Where: CF0 = Cash flow at time zero (t0)

CF1 = Cash flow at time one (t1), one year after time zero

30

DEFINITIONS

Present value:- the amount of money you must invest or lend at the present time so as to end up with a particular amount of money in the future.

Discounting: -finding the present value of a future cash flow

CALCULATING NET PRESENT VALUE Assume that Project X costs Rs 2,500 now and

is expected to generate year-end cash inflows of Rs 900, Rs 800, Rs 700, Rs 600 and Rs 500 in years 1 through 5. The opportunity cost of the capital may be assumed to be 10 per cent.

The NPV method can be used to select between mutually exclusive projects; the one with the higher NPV should be selected.

33

EXAMPLE 2.4

A company can purchase a machine at the price of £2200. The machine has a productive life of three years and the net additions to cash inflows at the end of each of the three years are £770, £968 and £1331. The company can buy the machine without having to borrow and the best alternative is investment elsewhere at an interest rate of 10%.Evaluate the project using the

a) Net present value method.b) Internal rate of return

The project is worthwhile and the machine should be bought (can you suggest why?)

35

NET PRESENT VALUE

Lecture Example 2.5A firm invest £180,000 in a project that will give a net cash inflow of 50,000 in real terms in each of the next six years. Its real pre-tax cost of capital is 13%.Required:Calculate NPV

Positive NPV indicates viability of the project. Negative NPV indicates non-viability of the project.

37

ALTERNATIVE SOLUTION TO 2.5

Use the annuity tableYear Cash flow DF @13% PV

0 (180,000) 1(180,000)1-6 50,000 3.998 199,900

NPV 19,900

EVALUATION OF THE NPV METHOD NPV is most acceptable investment rule for the

following reasons:Time value Measure of true profitability Value-additivity Shareholder value

Limitations: Involved cash flow estimation Discount rate difficult to determineMutually exclusive projects Ranking of projects

INTERNAL RATE OF RETURN METHOD

The internal rate of return (IRR) is the rate that equates the investment outlay with the present value of cash inflow received after one period. This also implies that the rate of return is the discount rate which makes NPV = 0.

31 20 2 3

01

01

(1 ) (1 ) (1 ) (1 )

(1 )

0(1 )

nn

ntt

t

ntt

t

C CC CC

r r r r

CC

r

CC

r

CALCULATION OF IRR

Uneven Cash Flows: Calculating IRR by Trial and ErrorThe approach is to select any discount rate to

compute the present value of cash inflows. If the calculated present value of the expected cash inflow is lower than the present value of cash outflows, a lower rate should be tried. On the other hand, a higher value should be tried if the present value of inflows is higher than the present value of outflows. This process will be repeated unless the net present value becomes zero.

CALCULATION OF IRR

Level Cash Flows Let us assume that an investment

would cost Rs 20,000 and provide annual cash inflow of Rs 5,430 for 6 years.

The IRR of the investment can be found out as follows:

6,

6,

6,

NPV Rs 20,000 + Rs 5,430(PVAF ) = 0

Rs 20,000 Rs 5,430(PVAF )

Rs 20,000PVAF 3.683

Rs 5,430

r

r

r

42

IRR

Use interpolation method to calculate the IRR. The formula is as follows:

)( LHNN

NLIRR

HL

L

Where: L = Lower rate of interest H = Higher rate of interest NL = NPV at lower rate of interest NH = NPV at higher rate of interest

43

EXAMPLE 2.6

Using Lecture example 2.4 (above), calculate the internal rate of return for the project.

44

INTERNAL RATE OF RETURN

Solution to 2.6IRR Try 15%Year Cash flow Discount Factor

Accept the project when r > k. Reject the project when r < k. May accept the project when r = k. In case of independent projects, IRR and NPV

rules will give the same results if the firm has no shortage of funds.

49

EVALUATION OF IRR METHOD

IRR method has following merits:Time value Profitability measure Acceptance rule Shareholder value

IRR method may suffer from:Multiple rates Mutually exclusive projects Value additivity

50

PROFITABILITY INDEX

Profitability index is the ratio of the present value of cash inflows, at the required rate of return, to the initial cash outflow of the investment.

PROFITABILITY INDEX The initial cash outlay of a project is Rs 100,000

and it can generate cash inflow of Rs 40,000, Rs 30,000, Rs 50,000 and Rs 20,000 in year 1 through 4. Assume a 10 per cent rate of discount. The PV of cash inflows at 10 per cent discount rate is:

The following are the PI acceptance rules:Accept the project when PI is greater than

one. PI > 1Reject the project when PI is less than one.

PI < 1May accept the project when PI is equal to

one. PI = 1 The project with positive NPV will have PI

greater than one. PI less than means that the project’s NPV is negative.

53

EVALUATION OF PI METHOD It recognises the time value of money. It is consistent with the shareholder value

maximisation principle. A project with PI greater than one will have positive NPV and if accepted, it will increase shareholders’ wealth.

In the PI method, since the present value of cash inflows is divided by the initial cash outflow, it is a relative measure of a project’s profitability.

Like NPV method, PI criterion also requires calculation of cash flows and estimate of the discount rate. In practice, estimation of cash flows and discount rate pose problems.

54

APPRAISAL METHODS

Please read more on the advantages and disadvantages of these techniques

Why is the NPV considered superior over the other methods, even the IRR?