• Taxpayers who are ineligible to use the SD– Married, filing separately when other spouse

itemizes deductions– Nonresident aliens– Individual filing return for tax year of less than

12 months

• Taxpayers who are ineligible to use the SD– Married, filing separately when other spouse

itemizes deductions– Nonresident aliens– Individual filing return for tax year of less than

12 months

C15 - 12

Standard Deductions (slide 5 of 7)

Standard Deductions (slide 5 of 7)

• Special limitations on BSD for dependents

– Individual claimed as dependent has a BSD limited to the greater of:

• $700 or

• $250 plus earned income (but not exceeding normal BSD)

– ASD amount(s) still available

• Special limitations on BSD for dependents

– Individual claimed as dependent has a BSD limited to the greater of:

• $700 or

• $250 plus earned income (but not exceeding normal BSD)

– ASD amount(s) still available

C15 - 13

Standard Deductions (slide 6 of 7)

Standard Deductions (slide 6 of 7)

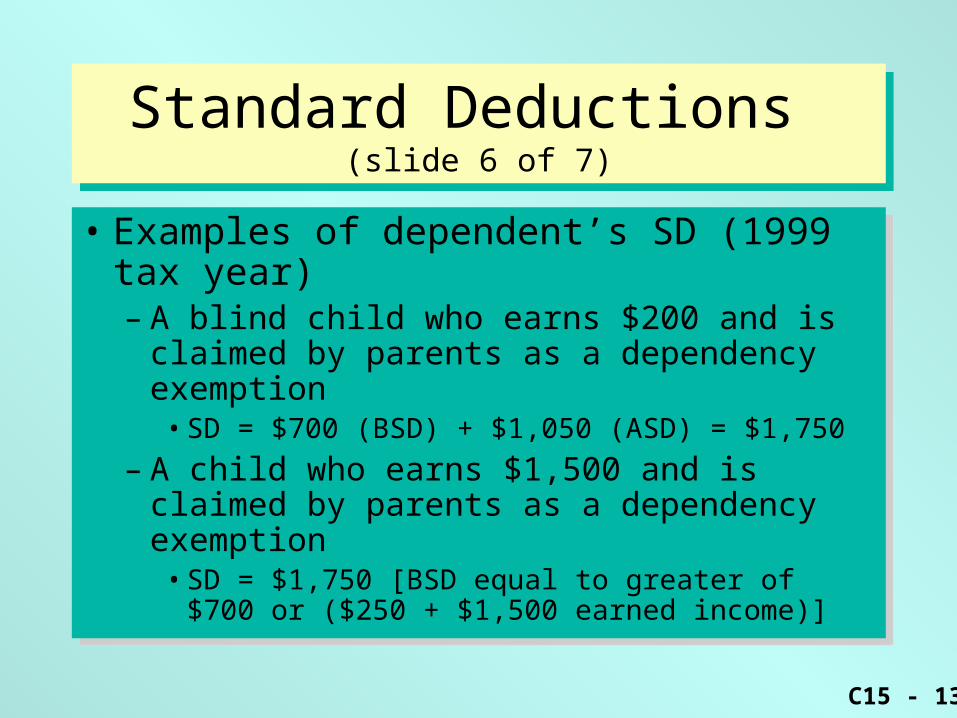

• Examples of dependent’s SD (1999 tax year)– A blind child who earns $200 and is claimed by

parents as a dependency exemption• SD = $700 (BSD) + $1,050 (ASD) = $1,750

– A child who earns $1,500 and is claimed by parents as a dependency exemption

• SD = $1,750 [BSD equal to greater of $700 or ($250 + $1,500 earned income)]

• Examples of dependent’s SD (1999 tax year)– A blind child who earns $200 and is claimed by

parents as a dependency exemption• SD = $700 (BSD) + $1,050 (ASD) = $1,750

– A child who earns $1,500 and is claimed by parents as a dependency exemption

• SD = $1,750 [BSD equal to greater of $700 or ($250 + $1,500 earned income)]

C15 - 14

Standard Deductions (slide 7 of 7)

Standard Deductions (slide 7 of 7)

• Examples of dependent’s SD (1998 tax year)– A child who earns $4,500 and is claimed by

parents as a dependency exemption• SD = $4,300 [BSD limited to normal

amount]

• Examples of dependent’s SD (1998 tax year)– A child who earns $4,500 and is claimed by

parents as a dependency exemption• SD = $4,300 [BSD limited to normal

amount]

C15 - 15

Learning Objective 2Learning Objective 2

Apply the rules for arriving at personal and dependency exemptions.

Apply the rules for arriving at personal and dependency exemptions.

C15 - 16

Personal and Dependency Exemptions (slide 1 of 14)

Personal and Dependency Exemptions (slide 1 of 14)

• Amounts– 1998: $2,700 per exemption– 1999: $2,750 per exemption

• Personal exemption– One per taxpayer (e.g., two personal

exemptions when married, filing jointly) • Exception: Individual claimed as dependent by

another taxpayer does not receive a personal exemption

• Amounts– 1998: $2,700 per exemption– 1999: $2,750 per exemption

• Personal exemption– One per taxpayer (e.g., two personal

exemptions when married, filing jointly) • Exception: Individual claimed as dependent by

another taxpayer does not receive a personal exemption

C15 - 17

Personal and Dependency Exemptions (slide 2 of 14)

Personal and Dependency Exemptions (slide 2 of 14)

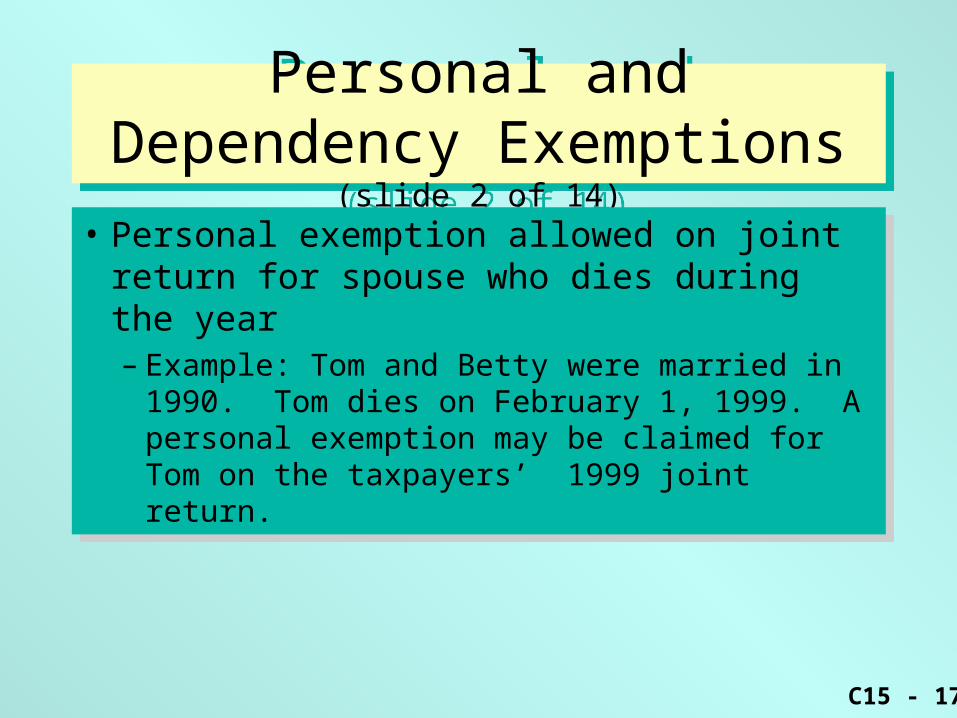

• Personal exemption allowed on joint return for spouse who dies during the year– Example: Tom and Betty were married in 1990.

Tom dies on February 1, 1999. A personal exemption may be claimed for Tom on the taxpayers’ 1999 joint return.

• Personal exemption allowed on joint return for spouse who dies during the year– Example: Tom and Betty were married in 1990.

Tom dies on February 1, 1999. A personal exemption may be claimed for Tom on the taxpayers’ 1999 joint return.

C15 - 18

Personal and Dependency Exemptions (slide 3 of 14)

Personal and Dependency Exemptions (slide 3 of 14)

• Taxpayer may claim a dependency exemption for each individual that meets all of the following tests:– Support– Relationship (or household member)– Gross income– Joint return– Citizen or residency

• Taxpayer may claim a dependency exemption for each individual that meets all of the following tests:– Support– Relationship (or household member)– Gross income– Joint return– Citizen or residency

C15 - 19

Personal and Dependency Exemptions (slide 4 of 14)

Personal and Dependency Exemptions (slide 4 of 14)

• Support– Taxpayer must provide more than 50% of the

dependent’s support• Only amounts expended are considered in the

support test• Scholarships of children not considered in the

support test

– Two exceptions to support test requirement• Multiple support agreements• Children of divorced parents

• Support– Taxpayer must provide more than 50% of the

dependent’s support• Only amounts expended are considered in the

support test• Scholarships of children not considered in the

support test

– Two exceptions to support test requirement• Multiple support agreements• Children of divorced parents

C15 - 20

Personal and Dependency Exemptions (slide 5 of 14)

Personal and Dependency Exemptions (slide 5 of 14)

• Multiple Support Agreements– Allows group providing > half support to claim

individual even though no one person provides > 50% support

• Eligible parties must provide > 10% of support

• Each eligible party must meet all other dependency requirements

– Example- Allows children of elderly parent to claim exemption for parent when none individually meets the 50% support test

• Multiple Support Agreements– Allows group providing > half support to claim

individual even though no one person provides > 50% support

• Eligible parties must provide > 10% of support

• Each eligible party must meet all other dependency requirements

– Example- Allows children of elderly parent to claim exemption for parent when none individually meets the 50% support test

C15 - 21

Personal and Dependency Exemptions (slide 6 of 14)

Personal and Dependency Exemptions (slide 6 of 14)

• Children of divorced parents– For post 1984 divorce decrees, custodial parent

gets exemption for children – Noncustodial parent may claim exemption for

children if custodial parent signs a Release of Claim to Exemption

• Children of divorced parents– For post 1984 divorce decrees, custodial parent

gets exemption for children – Noncustodial parent may claim exemption for

children if custodial parent signs a Release of Claim to Exemption

C15 - 22

Personal and Dependency Exemptions (slide 7 of 14)

Personal and Dependency Exemptions (slide 7 of 14)

• Relationship (or household member)– Dependent must be one of the specified

relatives of the taxpayer (either taxpayer, if joint return) or be a member of the taxpayer’s household for the entire year

– Once a relationship is established by marriage, it continues even if there is a change in marital status

• Relationship (or household member)– Dependent must be one of the specified

relatives of the taxpayer (either taxpayer, if joint return) or be a member of the taxpayer’s household for the entire year

– Once a relationship is established by marriage, it continues even if there is a change in marital status

C15 - 23

Personal and Dependency Exemptions (slide 8 of 14)

Personal and Dependency Exemptions (slide 8 of 14)

• Gross income– Dependent’s gross income cannot be greater

than amount allowed for an exemption (i.e., $2,750 for 1999)

• Exception: No gross income limitation if dependent is child of taxpayer AND either i) less than age 19 OR ii) less than age 24 and a full-time student

• Gross income– Dependent’s gross income cannot be greater

than amount allowed for an exemption (i.e., $2,750 for 1999)

• Exception: No gross income limitation if dependent is child of taxpayer AND either i) less than age 19 OR ii) less than age 24 and a full-time student

C15 - 24

Personal and Dependency Exemptions (slide 9 of 14)

Personal and Dependency Exemptions (slide 9 of 14)

• Example of gross income test (1999 tax year)– Grandparent (age 70) meets all dependency

tests for taxpayer except has gross income of $3,000

• Grandparent fails gross income test and cannot be claimed by taxpayer as dependency exemption

• Example of gross income test (1999 tax year)– Grandparent (age 70) meets all dependency

tests for taxpayer except has gross income of $3,000

• Grandparent fails gross income test and cannot be claimed by taxpayer as dependency exemption

C15 - 25

Personal and Dependency Exemptions (slide 10 of 14)

Personal and Dependency Exemptions (slide 10 of 14)

• Example of gross income test (1999 tax year)– Child (age 16) meets all dependency tests for

taxpayer except has gross income of $3,000• Gross income exception for child applies and

taxpayer can claim child as dependency exemption

• Example of gross income test (1999 tax year)– Child (age 16) meets all dependency tests for

taxpayer except has gross income of $3,000• Gross income exception for child applies and

taxpayer can claim child as dependency exemption

C15 - 26

Personal and Dependency Exemptions (slide 11 of 14)

Personal and Dependency Exemptions (slide 11 of 14)

• Joint return– Dependent cannot file a joint return with spouse

unless:• Filing solely for refund of all taxes withheld

• No tax liability exists for either spouse

• Neither spouse required to file return

• Joint return– Dependent cannot file a joint return with spouse

unless:• Filing solely for refund of all taxes withheld

• No tax liability exists for either spouse

• Neither spouse required to file return

C15 - 27

Personal and Dependency Exemptions (slide 12 of 14)

Personal and Dependency Exemptions (slide 12 of 14)

• Citizen or residency– Dependent must be a U.S. citizen or a resident

of U.S., Canada, or Mexico

• Citizen or residency– Dependent must be a U.S. citizen or a resident

of U.S., Canada, or Mexico

C15 - 28

Personal and Dependency Exemptions (slide 13 of 14)

Personal and Dependency Exemptions (slide 13 of 14)

Phase-out of exemption benefits applies when taxpayer’s AGI in 1999 exceeds:

$189,950 for married, filing jointly, or surviving spouse

$158,300 for head of household

$126,600 for single

$ 94,975 for married, filing separately

Phase-out of exemption benefits applies when taxpayer’s AGI in 1999 exceeds:

$189,950 for married, filing jointly, or surviving spouse

$158,300 for head of household

$126,600 for single

$ 94,975 for married, filing separately

C15 - 29

Personal and Dependency Exemptions (slide 14 of 14)

Personal and Dependency Exemptions (slide 14 of 14)

• Phase-out of exemption benefits (cont’d)– Exemptions deduction is reduced by 2% for

every $2,500 ($1,250 for MFS) or part thereof, that AGI exceeds threshold amounts

• Phase-out of exemption benefits (cont’d)– Exemptions deduction is reduced by 2% for

every $2,500 ($1,250 for MFS) or part thereof, that AGI exceeds threshold amounts

C15 - 30

Learning Objective 3Learning Objective 3

Use the proper method for

determining the tax liability.

Use the proper method for

determining the tax liability.

C15 - 31

Taxes RatesTaxes Rates

• Tax rates for 1999 are 15%, 28%, 31%, 36%, and 39.6%– Tax rate brackets are inflation adjusted yearly

• Maximum rate for long-term capital gains is 20%

• Tax rates for 1999 are 15%, 28%, 31%, 36%, and 39.6%– Tax rate brackets are inflation adjusted yearly

• Maximum rate for long-term capital gains is 20%

C15 - 32

Learning Objective 4Learning Objective 4

Identify and work with kiddie tax situations.Identify and work with kiddie tax situations.

C15 - 33

Kiddie Tax (slide 1 of 4)Kiddie Tax (slide 1 of 4)

• Net unearned income (NUI) of child is taxed at parents’ rate– Child must be under age 14 at end of year– NUI generally equals unearned income less

$1,400 (1999 tax year)

• Net unearned income (NUI) of child is taxed at parents’ rate– Child must be under age 14 at end of year– NUI generally equals unearned income less

$1,400 (1999 tax year)

C15 - 34

Kiddie Tax (slide 2 of 4)Kiddie Tax (slide 2 of 4)

• Unearned income includes taxable interest, dividends, capital gains, rents, royalties, pension and annuity income, and unearned income from trusts

• Unearned income includes taxable interest, dividends, capital gains, rents, royalties, pension and annuity income, and unearned income from trusts

C15 - 35

Kiddie Tax (slide 3 of 4)Kiddie Tax (slide 3 of 4)

• Computing NUI for Kiddie Tax:Unearned income

Less: $700

Less: the greater of i) $700 or ii) allowable itemized deductions for unearned income

Equals: net unearned income

• Computing NUI for Kiddie Tax:Unearned income

Less: $700

Less: the greater of i) $700 or ii) allowable itemized deductions for unearned income

Equals: net unearned income

C15 - 36

Kiddie Tax (slide 4 of 4)Kiddie Tax (slide 4 of 4)

• Net unearned income taxed at parents’ rate

• Remainder of taxable income taxed at child’s rate

• Use Form 8615 to compute tax

• Election available to report child’s income on parents’ return

• Net unearned income taxed at parents’ rate

• Remainder of taxable income taxed at child’s rate

• Use Form 8615 to compute tax

• Election available to report child’s income on parents’ return

C15 - 37

Learning Objective 5Learning Objective 5

Recognize filing requirements and

proper filing status.

Recognize filing requirements and

proper filing status.

C15 - 38

Filing Requirements (slide 1 of 2)

Filing Requirements (slide 1 of 2)

• Tax return– Must file if gross income equals of exceeds the

standard deduction and personal exemption amount

• ASD for blind does not apply for this determination

– Special rules for dependents and self-employed taxpayers

• See Table 15-4 for various filing levels

• Tax return– Must file if gross income equals of exceeds the

standard deduction and personal exemption amount

• ASD for blind does not apply for this determination

– Special rules for dependents and self-employed taxpayers

• See Table 15-4 for various filing levels

C15 - 39

Filing Requirements (slide 2 of 2)

Filing Requirements (slide 2 of 2)

• Tax return– Individual returns are due on or before the 15th

day of the 4th month after taxpayer’s year end• Most individuals are calendar year taxpayers, thus,

due date is April 15

• May obtain an extension of time to file

• Tax return– Individual returns are due on or before the 15th

day of the 4th month after taxpayer’s year end• Most individuals are calendar year taxpayers, thus,

due date is April 15

• May obtain an extension of time to file

C15 - 40

Filing Status (slide 1 of 7)Filing Status (slide 1 of 7)

• There are 5 filing statuses– Single

– Married, filing jointly

– Surviving spouse (qualifying widow or widower)

– Head of household

– Married, filing separately

• Filing status affects tax rate brackets, standard deduction, and other amounts

• There are 5 filing statuses– Single

– Married, filing jointly

– Surviving spouse (qualifying widow or widower)

– Head of household

– Married, filing separately

• Filing status affects tax rate brackets, standard deduction, and other amounts

C15 - 41

Filing Status (slide 2 of 7)Filing Status (slide 2 of 7)

• Single– Unmarried individual– Residual category (i.e., do not meet any of

other statuses)

• Single– Unmarried individual– Residual category (i.e., do not meet any of

other statuses)

C15 - 42

Filing Status (slide 3 of 7)Filing Status (slide 3 of 7)

• Married, filing jointly (MFJ)– Married as of last day of taxable year, or– Spouse dies during taxable year

• Married, filing jointly (MFJ)– Married as of last day of taxable year, or– Spouse dies during taxable year

C15 - 43

Filing Status (slide 4 of 7)Filing Status (slide 4 of 7)

• Surviving spouse– Same tax rate brackets as married, filing jointly– File as surviving spouse for 2 years after death

of spouse if taxpayer maintains a home in which a dependent child lives

• Surviving spouse– Same tax rate brackets as married, filing jointly– File as surviving spouse for 2 years after death

of spouse if taxpayer maintains a home in which a dependent child lives

C15 - 44

Filing Status (slide 5 of 7)Filing Status (slide 5 of 7)

• Married, filing separately– Married but not filing a return with spouse and

not abandoned spouse

• Married, filing separately– Married but not filing a return with spouse and

not abandoned spouse

C15 - 45

Filing Status (slide 6 of 7)Filing Status (slide 6 of 7)

• Head of household (HH)– Must be unmarried as of end of year or an

abandoned spouse– Must pay > half the cost of maintaining a

household which is the principal home of a dependent relative for more than half of tax year

• Head of household (HH)– Must be unmarried as of end of year or an

abandoned spouse– Must pay > half the cost of maintaining a

household which is the principal home of a dependent relative for more than half of tax year

C15 - 46

Filing Status (slide 7 of 7)Filing Status (slide 7 of 7)

• 2 Exceptions to the HH requirements– HH may be claimed if taxpayer maintains a

separate home for his or her parents if at least one parent qualifies as a dependent

– If the qualifying individual is an unmarried child or grandchild, the child or grandchild need not be taxpayer’s dependent

• 2 Exceptions to the HH requirements– HH may be claimed if taxpayer maintains a

separate home for his or her parents if at least one parent qualifies as a dependent

– If the qualifying individual is an unmarried child or grandchild, the child or grandchild need not be taxpayer’s dependent

C15 - 47

Learning Objective 6Learning Objective 6

Identify specific inclusions and exclusions applicable to individuals.

Identify specific inclusions and exclusions applicable to individuals.

C15 - 48

Alimony and Separate Maintenance Payments (slide 1 of 4)

Alimony and Separate Maintenance Payments (slide 1 of 4)

• Deductible by payor

• Includible in gross income of recipient

• Deductible by payor

• Includible in gross income of recipient

C15 - 49

Alimony and Separate Maintenance Payments (slide 2 of 4)

Alimony and Separate Maintenance Payments (slide 2 of 4)

• Alimony defined– Paid in cash – Pursuant to divorce or separation instrument– Payor and recipient are not members of same

household– Payments terminate no later than death of

recipient– Payments not called something other than

alimony in agreement or decree

• Alimony defined– Paid in cash – Pursuant to divorce or separation instrument– Payor and recipient are not members of same

household– Payments terminate no later than death of

recipient– Payments not called something other than

alimony in agreement or decree

C15 - 50

Alimony and Separate Maintenance Payments (slide 3 of 4)

Alimony and Separate Maintenance Payments (slide 3 of 4)

• Property settlements– Transfer of property to former spouse– No deduction or recognized gain or loss for

payor– No gross income and carryover of payor’s

basis for recipient– Front-loading of alimony payments

• Alimony recapture (gross income) for payor• Deduction (FOR AGI) for recipient

• Property settlements– Transfer of property to former spouse– No deduction or recognized gain or loss for

payor– No gross income and carryover of payor’s

basis for recipient– Front-loading of alimony payments

• Alimony recapture (gross income) for payor• Deduction (FOR AGI) for recipient

C15 - 51

Alimony and Separate Maintenance Payments (slide 4 of 4)

Alimony and Separate Maintenance Payments (slide 4 of 4)

• Child support payments– Payments made to satisfy legal obligation to

support child of taxpayer– Nondeductible by payor and not taxed to

recipient (or child)

• Child support payments– Payments made to satisfy legal obligation to

support child of taxpayer– Nondeductible by payor and not taxed to

recipient (or child)

C15 - 52

Prizes and AwardsPrizes and Awards

• General rule: FMV of item is included in income

• Exceptions:• Taxpayer designates qualified organization to

receive prize or award

• Employee awards of tangible personal property made in recognition of length of service or safety achievement

• General rule: FMV of item is included in income

• Exceptions:• Taxpayer designates qualified organization to

receive prize or award

• Employee awards of tangible personal property made in recognition of length of service or safety achievement

• Taxability based on taxpayer’s modified adjusted gross income (MAGI)– MAGI = AGI + foreign earned income

exclusion + tax exempt interest

• Two formulas for computing taxable benefits

• Up to 85% of benefits may be taxable

• Taxability based on taxpayer’s modified adjusted gross income (MAGI)– MAGI = AGI + foreign earned income

exclusion + tax exempt interest

• Two formulas for computing taxable benefits

C15 - 55

Gifts and Inheritances (slide 1 of 3)

Gifts and Inheritances (slide 1 of 3)

• Gifts are nontaxable to donee if:– Transfer is voluntary without adequate

consideration, and– Made because of affection, respect, admiration,

charity, or donative intent

• Gifts are nontaxable to donee if:– Transfer is voluntary without adequate

consideration, and– Made because of affection, respect, admiration,

charity, or donative intent

C15 - 56

Gifts and Inheritances (slide 2 of 3)

Gifts and Inheritances (slide 2 of 3)

• Inheritances are nontaxable to beneficiary

• Income earned on gifts or inheritances taxable under normal rules– Example: Father gifts corporate bond to

daughter. Gift is excluded from daughter’s gross income, but interest income earned after gift date is taxable to her.

• Inheritances are nontaxable to beneficiary

• Income earned on gifts or inheritances taxable under normal rules– Example: Father gifts corporate bond to

daughter. Gift is excluded from daughter’s gross income, but interest income earned after gift date is taxable to her.

C15 - 57

Gifts and Inheritances (slide 3 of 3)

Gifts and Inheritances (slide 3 of 3)

• Transfers by employers to employees do not qualify as excludible gifts– May be excludible under other provisions, e.g.,

employee achievement awards

• Transfers by employers to employees do not qualify as excludible gifts– May be excludible under other provisions, e.g.,

employee achievement awards

C15 - 58

Scholarships and FellowshipsScholarships and Fellowships

• An amount paid to or for the benefit of a student to aid in pursuing a degree at an educational institution

• Nontaxable to extent of tuition and related expenses (e.g., fees, books, and equipment required for courses)– Amounts received for room and board are

taxable

• An amount paid to or for the benefit of a student to aid in pursuing a degree at an educational institution

• Nontaxable to extent of tuition and related expenses (e.g., fees, books, and equipment required for courses)– Amounts received for room and board are

taxable

C15 - 59

Compensation for Injuries and Sickness (slide 1 of 3)

Compensation for Injuries and Sickness (slide 1 of 3)

• Personal injury damages– Compensatory damages received on account of

physical personal injury are excludible• All other personal injury damages taxable

– Compensatory damages for nonphysical injury

– All punitive damages

– Payments solely for loss of income are also taxable

• Personal injury damages– Compensatory damages received on account of

physical personal injury are excludible• All other personal injury damages taxable

– Compensatory damages for nonphysical injury

– All punitive damages

– Payments solely for loss of income are also taxable

C15 - 60

Compensation for Injuries and Sickness (slide 2 of 3)

Compensation for Injuries and Sickness (slide 2 of 3)

• Workers’ compensation– Although may be payment for loss of wages,

workers’ compensation is specifically excluded from gross income

• Workers’ compensation– Although may be payment for loss of wages,

workers’ compensation is specifically excluded from gross income

C15 - 61

Compensation for Injuries and Sickness (slide 3 of 3)

Compensation for Injuries and Sickness (slide 3 of 3)

• Accident and health insurance benefits– Benefits received under policy purchased by

taxpayer excludible• Even if benefits are substitute for income

• Accident and health insurance benefits– Benefits received under policy purchased by

taxpayer excludible• Even if benefits are substitute for income

• Interest on Series EE U.S. Savings Bonds may be excluded from income if:– Proceeds used to pay for qualified higher

educational expenses– Bonds issued after 12/31/89, and– Bonds issued to person at least 24 years old

• Exclusion is phased-out once modified AGI exceeds threshold amount

• Interest on Series EE U.S. Savings Bonds may be excluded from income if:– Proceeds used to pay for qualified higher

educational expenses– Bonds issued after 12/31/89, and– Bonds issued to person at least 24 years old

• Exclusion is phased-out once modified AGI exceeds threshold amount

C15 - 63

Learning Objective 7Learning Objective 7

Determine an individual’s allowable itemized deductions.

Determine an individual’s allowable itemized deductions.

C15 - 64

Itemized Deductions(slide 1 of 2)

Itemized Deductions(slide 1 of 2)

• Personal expenditures that are deductible FROM AGI as itemized deductions include: – Medical– Certain taxes– Certain interest expense– Charitable Contributions– Others

• Personal expenditures that are deductible FROM AGI as itemized deductions include: – Medical– Certain taxes– Certain interest expense– Charitable Contributions– Others

C15 - 65

Itemized Deductions(slide 2 of 2)

Itemized Deductions(slide 2 of 2)

• Itemized deductions provide a tax benefit only to extent that in total they exceed the standard deduction amount for the taxpayer.

• Itemized deductions provide a tax benefit only to extent that in total they exceed the standard deduction amount for the taxpayer.

C15 - 66

Medical Expenses (slide 1 of 12)

Medical Expenses (slide 1 of 12)

• Medical expense defined– Expenditure for the diagnosis, cure, treatment,

prevention, or for purpose of affecting any structure or function of the body of the taxpayer, spouse, or dependents

– Includes prescription drugs and insulin

• Medical expense defined– Expenditure for the diagnosis, cure, treatment,

prevention, or for purpose of affecting any structure or function of the body of the taxpayer, spouse, or dependents

– Includes prescription drugs and insulin

C15 - 67

Medical Expenses (slide 2 of 12)

Medical Expenses (slide 2 of 12)

• Medical expenses do not include the cost of items such as: – Elective cosmetic surgery– General health items– Hair transplant

• Medical expenses do not include the cost of items such as: – Elective cosmetic surgery– General health items– Hair transplant

C15 - 68

Medical Expenses (slide 3 of 12)

Medical Expenses (slide 3 of 12)

• Amount of medical deduction– Deductible to extent unreimbursed medical

expenses in total exceed 7.5% of AGI

• Amount of medical deduction– Deductible to extent unreimbursed medical

expenses in total exceed 7.5% of AGI

C15 - 69

Medical Expenses (slide 4 of 12)

Medical Expenses (slide 4 of 12)

• Example of medical deduction limitation:– Amy has AGI of $10,000 and medical expenses

of $1,000– Amy’s medical deduction = $250

[$1,000 - ($10,000 x 7.5%)]

• Example of medical deduction limitation:– Amy has AGI of $10,000 and medical expenses

of $1,000– Amy’s medical deduction = $250

[$1,000 - ($10,000 x 7.5%)]

C15 - 70

Medical Expenses (slide 5 of 12)

Medical Expenses (slide 5 of 12)

• Example of medical deduction limitation:– Bob has AGI of $4,000 and medical expenses

of $1,000– Bob’s medical deduction = $700

[$1,000 - ($4,000 x 7.5%)]

• Example of medical deduction limitation:– Bob has AGI of $4,000 and medical expenses

of $1,000– Bob’s medical deduction = $700

[$1,000 - ($4,000 x 7.5%)]

C15 - 71

Medical Expenses (slide 6 of 12)

Medical Expenses (slide 6 of 12)

• Nursing home expenditures– If primary purpose of placement in home is

medical, costs (including meals and lodging) qualify

– If primary purpose of placement in home is personal, only specific medical costs qualify (no meals or lodging)

• Nursing home expenditures– If primary purpose of placement in home is

medical, costs (including meals and lodging) qualify

– If primary purpose of placement in home is personal, only specific medical costs qualify (no meals or lodging)

C15 - 72

Medical Expenses (slide 7 of 12)

Medical Expenses (slide 7 of 12)

• Capital medical expenditures– Includes wheelchairs, medical beds, seeing eye dogs,

etc.

– Must be medical necessity, advised by a physician, used primarily by patient, and expense is reasonable

– Full amount of cost is medical expense in year paid

– Maintenance on capital expenditures also medical expenses

• Capital medical expenditures– Includes wheelchairs, medical beds, seeing eye dogs,

etc.

– Must be medical necessity, advised by a physician, used primarily by patient, and expense is reasonable

– Full amount of cost is medical expense in year paid

– Maintenance on capital expenditures also medical expenses

C15 - 73

Medical Expenses (slide 8 of 12)

Medical Expenses (slide 8 of 12)

• Capital improvement to home– Medical expense only to extent that cost of

improvement exceeds increase in value to home• Exception: removal of structural barriers to home of

handicapped are deemed to add no value to home. Thus, full amount is a medical expense.

• Capital improvement to home– Medical expense only to extent that cost of

improvement exceeds increase in value to home• Exception: removal of structural barriers to home of

handicapped are deemed to add no value to home. Thus, full amount is a medical expense.

C15 - 74

Medical Expenses (slide 9 of 12)

Medical Expenses (slide 9 of 12)

• Medical care of spouse and dependents– Taxpayer may deduct cost of medical care for

spouse and dependents• Dependents need not meet gross income or joint

return tests

• Children of divorced parents treated as dependents of both for purpose of medical deduction

• Medical care of spouse and dependents– Taxpayer may deduct cost of medical care for

spouse and dependents• Dependents need not meet gross income or joint

return tests

• Children of divorced parents treated as dependents of both for purpose of medical deduction

C15 - 75

Medical Expenses (slide 10 of 12)

Medical Expenses (slide 10 of 12)

• Medical transportation and lodging– Transportation to and from medical care is

deductible• Mileage allowance of 10 cents per mile

– Lodging while away from home for medical care

• Allowable amount is $50 per person per night

– If parent and/or aide needs to accompany patient, their expenses are also medical

• Medical transportation and lodging– Transportation to and from medical care is

deductible• Mileage allowance of 10 cents per mile

– Lodging while away from home for medical care

• Allowable amount is $50 per person per night

– If parent and/or aide needs to accompany patient, their expenses are also medical

C15 - 76

Medical Expenses (slide 11 of 12)

Medical Expenses (slide 11 of 12)

• Medical Savings Accounts (MSA)– Taxpayers with high deductible health

insurance can make deductible (for AGI) contributions to MSA

• Deduction limited to 65% (75% for family) of policy deductible

• Medical Savings Accounts (MSA)– Taxpayers with high deductible health

insurance can make deductible (for AGI) contributions to MSA

• Deduction limited to 65% (75% for family) of policy deductible

C15 - 77

Medical Expenses (slide 12 of 12)

Medical Expenses (slide 12 of 12)

• Medical Savings Accounts (MSA)– Earnings of MSA not currently taxed– MSA distributions used for noncovered medical

costs not taxed• Other distributions taxable and subject to 15%

penalty

• Medical Savings Accounts (MSA)– Earnings of MSA not currently taxed– MSA distributions used for noncovered medical

costs not taxed• Other distributions taxable and subject to 15%

penalty

C15 - 78

Taxes (slide 1 of 4)Taxes (slide 1 of 4)

• State, local, and foreign income and real property taxes are deductible in the year paid

• State and local personal property taxes based on value (ad valorem) are deductible in the year paid

• State, local, and foreign income and real property taxes are deductible in the year paid

• State and local personal property taxes based on value (ad valorem) are deductible in the year paid

C15 - 79

Taxes (slide 2 of 4)Taxes (slide 2 of 4)

• Other taxes such as sales, excise, etc., are not deductible– Deductible if incurred in business or production

of income activity

• Fees are not deductible as tax

• Other taxes such as sales, excise, etc., are not deductible– Deductible if incurred in business or production

of income activity

• Fees are not deductible as tax

C15 - 80

Taxes (slide 3 of 4)Taxes (slide 3 of 4)

• Real estate taxes for year property is sold must be apportioned between the buyer and the seller– Failure to correctly apportion requires

offsetting adjustments to seller’s amount realized and buyer’s adjusted basis

• Real estate taxes for year property is sold must be apportioned between the buyer and the seller– Failure to correctly apportion requires

offsetting adjustments to seller’s amount realized and buyer’s adjusted basis

C15 - 81

Taxes (slide 4 of 4)Taxes (slide 4 of 4)

• State and local income taxes– Deduct amounts paid during year

• Withheld amounts

• Estimated tax payments

• Amounts paid in year for prior year’s liability

• Foreign income taxes deductible or claimed as credit (FTC)

• State and local income taxes– Deduct amounts paid during year

• Withheld amounts

• Estimated tax payments

• Amounts paid in year for prior year’s liability

• Foreign income taxes deductible or claimed as credit (FTC)

C15 - 82

Student Loan Interest Student Loan Interest

• Interest on qualified education loans is deductible For AGI – Max deduction is $1,500 in 1999

• Phased out for AGI between $40,000 and $55,000 ($60,000 and $75,000 on joint returns)

– Deduction applies to interest paid during first 60 months of loan repayment

• Interest on qualified education loans is deductible For AGI – Max deduction is $1,500 in 1999

• Phased out for AGI between $40,000 and $55,000 ($60,000 and $75,000 on joint returns)

– Deduction applies to interest paid during first 60 months of loan repayment

C15 - 83

Investment Interest (slide 1 of 5)

Investment Interest (slide 1 of 5)

• Definition: interest on loans whose proceeds are used to purchase investment property, e.g., stock, bonds, land

• Deduction of investment interest is limited to net investment income

• Definition: interest on loans whose proceeds are used to purchase investment property, e.g., stock, bonds, land

• Deduction of investment interest is limited to net investment income

C15 - 84

Investment Interest (slide 2 of 5)

Investment Interest (slide 2 of 5)

• Net investment income:– Investment income less investment expenses

• Net investment income:– Investment income less investment expenses

C15 - 85

Investment Interest (slide 3 of 5)

Investment Interest (slide 3 of 5)

• Investment income:– Gross income from interest, dividends,

annuities, and royalties not derived from business

– Long-term capital gains treated as investment income only if elected

• Amount elected as investment income is not eligible for preferential reduced tax on LTCG

• Investment income:– Gross income from interest, dividends,

annuities, and royalties not derived from business

– Long-term capital gains treated as investment income only if elected

• Amount elected as investment income is not eligible for preferential reduced tax on LTCG

C15 - 86

Investment Interest (slide 4 of 5)

Investment Interest (slide 4 of 5)

• Investment expenses:– All expenses (other than interest) directly

related to portfolio income that are allowed as a deduction

– Application of 2% AGI floor for some investment expenses must be considered in computing amount of net investment income

• Investment expenses:– All expenses (other than interest) directly

related to portfolio income that are allowed as a deduction

– Application of 2% AGI floor for some investment expenses must be considered in computing amount of net investment income

C15 - 87

Investment Interest (slide 5 of 5)

Investment Interest (slide 5 of 5)

• Investment interest not deductible in current year due to limitation is carried forward to future years until ultimately used– Deductibility subject to net investment income

limitation in carryover years

• Investment interest not deductible in current year due to limitation is carried forward to future years until ultimately used– Deductibility subject to net investment income

limitation in carryover years

C15 - 88

Qualified Residence Interest (slide 1 of 4)

Qualified Residence Interest (slide 1 of 4)

• Interest on indebtedness secured by the principal residence and one other residence (qualified residences)

• Interest must be on acquisition or home equity indebtedness

• Interest on indebtedness secured by the principal residence and one other residence (qualified residences)

• Interest must be on acquisition or home equity indebtedness

C15 - 89

Qualified Residence Interest (slide 2 of 4)

Qualified Residence Interest (slide 2 of 4)

• Acquisition indebtedness: amounts incurred to acquire, construct, or substantially improve the qualified residences– Aggregate acquisition indebtedness for

qualified residences cannot be greater than $1 million

• Acquisition indebtedness: amounts incurred to acquire, construct, or substantially improve the qualified residences– Aggregate acquisition indebtedness for

qualified residences cannot be greater than $1 million

C15 - 90

Qualified Residence Interest (slide 3 of 4)

Qualified Residence Interest (slide 3 of 4)

• Home equity indebtedness: loans secured by qualified residences– Interest is deductible on the portion of a home

equity loan that does not exceed the lesser of:• $100,000

• FMV of home - acquisition indebtedness

• Home equity indebtedness: loans secured by qualified residences– Interest is deductible on the portion of a home

equity loan that does not exceed the lesser of:• $100,000

• FMV of home - acquisition indebtedness

C15 - 91

Qualified Residence Interest (slide 4 of 4)

Qualified Residence Interest (slide 4 of 4)

• Thus, maximum loans on qualified residences that will produce qualified residence interest is $1.1 million

• Interest on mortgage debt exceeding $1.1 million or on mortgage debt relating to nonqualified residence (e.g., second vacation home) is nondeductible personal interest

• Thus, maximum loans on qualified residences that will produce qualified residence interest is $1.1 million

• Interest on mortgage debt exceeding $1.1 million or on mortgage debt relating to nonqualified residence (e.g., second vacation home) is nondeductible personal interest

C15 - 92

Prepaid InterestPrepaid Interest

• Prepaid interest generally must be capitalized and amortized over the life of loan

• Exception: “Points” (prepaid interest on a mortgage) paid in the acquisition or improvement of principal residence– Entire amount of such points deductible in year

paid

• Prepaid interest generally must be capitalized and amortized over the life of loan

• Exception: “Points” (prepaid interest on a mortgage) paid in the acquisition or improvement of principal residence– Entire amount of such points deductible in year

paid

C15 - 93

Charitable Contributions(slide 1 of 12)

Charitable Contributions(slide 1 of 12)

• Charitable contribution defined– Contributor must have donative intent and

expect nothing in return– If contributor receives tangible benefit, the

FMV of such benefit must be deducted from the amount of the contribution

• Charitable contribution defined– Contributor must have donative intent and

expect nothing in return– If contributor receives tangible benefit, the

FMV of such benefit must be deducted from the amount of the contribution

C15 - 94

Charitable Contributions(slide 2 of 12)

Charitable Contributions(slide 2 of 12)

• Charitable contribution defined (cont’d)– Contribution must be to qualified domestic

charity or state or possession of U.S. or any subdivisions thereof

– Most domestic charities are listed in IRS Publication #78

• Charitable contribution defined (cont’d)– Contribution must be to qualified domestic

charity or state or possession of U.S. or any subdivisions thereof

– Most domestic charities are listed in IRS Publication #78

C15 - 95

Charitable Contributions(slide 3 of 12)

Charitable Contributions(slide 3 of 12)

• No deduction allowed for contribution of services– Unreimbursed expenses related to the services

are deductible– Out-of-pocket transportation costs or a standard

mileage rate of 14 cents per mile are also deductible

• No deduction allowed for contribution of services– Unreimbursed expenses related to the services

are deductible– Out-of-pocket transportation costs or a standard

mileage rate of 14 cents per mile are also deductible

C15 - 96

Charitable Contributions(slide 4 of 12)

Charitable Contributions(slide 4 of 12)

• Ordinary income property– Defined: assets that would produce ordinary

income or short-term capital gain if sold– Contribution amount

• FMV of asset less ordinary income (or STCG) potential; generally the lower of adjusted basis or FMV

• Ordinary income property– Defined: assets that would produce ordinary

income or short-term capital gain if sold– Contribution amount

• FMV of asset less ordinary income (or STCG) potential; generally the lower of adjusted basis or FMV

C15 - 97

Charitable Contributions(slide 5 of 12)

Charitable Contributions(slide 5 of 12)

• Capital gain property– Defined: assets that would produce long-term

capital gain or Section 1231 gain if sold– Contribution amount

• Generally FMV of asset

• Capital gain property– Defined: assets that would produce long-term

capital gain or Section 1231 gain if sold– Contribution amount

• Generally FMV of asset

C15 - 98

Charitable Contributions(slide 6 of 12)

Charitable Contributions(slide 6 of 12)

• Limitations on deductions: 50% limit– In no case can the charitable contribution

deduction for a year exceed 50% of the taxpayer’s AGI

– Contributions of cash, ordinary income property, and certain capital gain property (where the contribution amount is adjusted basis) are subject to the 50% limit (50% assets)

• Limitations on deductions: 50% limit– In no case can the charitable contribution

deduction for a year exceed 50% of the taxpayer’s AGI

– Contributions of cash, ordinary income property, and certain capital gain property (where the contribution amount is adjusted basis) are subject to the 50% limit (50% assets)

C15 - 99

Charitable Contributions(slide 7 of 12)

Charitable Contributions(slide 7 of 12)

• Limitations on deductions: 30% limit– Charitable contribution deduction for certain

assets cannot exceed 30% of the taxpayer’s AGI

• Applies to 30% assets which are:– Capital gain property for which the contribution amount is

FMV

– Certain contributions to private nonoperating foundations

• Limitations on deductions: 30% limit– Charitable contribution deduction for certain

assets cannot exceed 30% of the taxpayer’s AGI

• Applies to 30% assets which are:– Capital gain property for which the contribution amount is

FMV

– Certain contributions to private nonoperating foundations

C15 - 100

Charitable Contributions(slide 8 of 12)

Charitable Contributions(slide 8 of 12)

• Limitations on deductions: 30% limit– Taxpayer can elect to treat capital gain property

as 50% assets by limiting the amount of such contributions to their adjusted bases

• Limitations on deductions: 30% limit– Taxpayer can elect to treat capital gain property

as 50% assets by limiting the amount of such contributions to their adjusted bases

C15 - 101

Charitable Contributions(slide 9 of 12)

Charitable Contributions(slide 9 of 12)

• Limitations on deductions: 20% limit– Certain contributions of capital gain property to

private nonoperating foundations

• Limitations on deductions: 20% limit– Certain contributions of capital gain property to

private nonoperating foundations

C15 - 102

Charitable Contributions(slide 10 of 12)

Charitable Contributions(slide 10 of 12)

• Interaction of limitations– When applying the yearly overall 50%

limitation, allowable deductions come first from the 50% assets, then from the 30% assets

• Interaction of limitations– When applying the yearly overall 50%

limitation, allowable deductions come first from the 50% assets, then from the 30% assets

C15 - 103

Charitable Contributions(slide 11 of 12)

Charitable Contributions(slide 11 of 12)

• Contribution carryover– Contributions that cannot be taken in current

year due to limitations may be carried forward for 5 years

– When using carryovers, current contributions are used first, then carryovers used on a FIFO basis

• Contribution carryover– Contributions that cannot be taken in current

year due to limitations may be carried forward for 5 years

– When using carryovers, current contributions are used first, then carryovers used on a FIFO basis

C15 - 104

Charitable Contributions(slide 12 of 12)

Charitable Contributions(slide 12 of 12)

• Example of the 50% and 30% limits:– Taxpayer, AGI $100,000, contributed $40,000

cash and long-term stocks with a FMV of $35,000 and a basis of $8,000 to a University

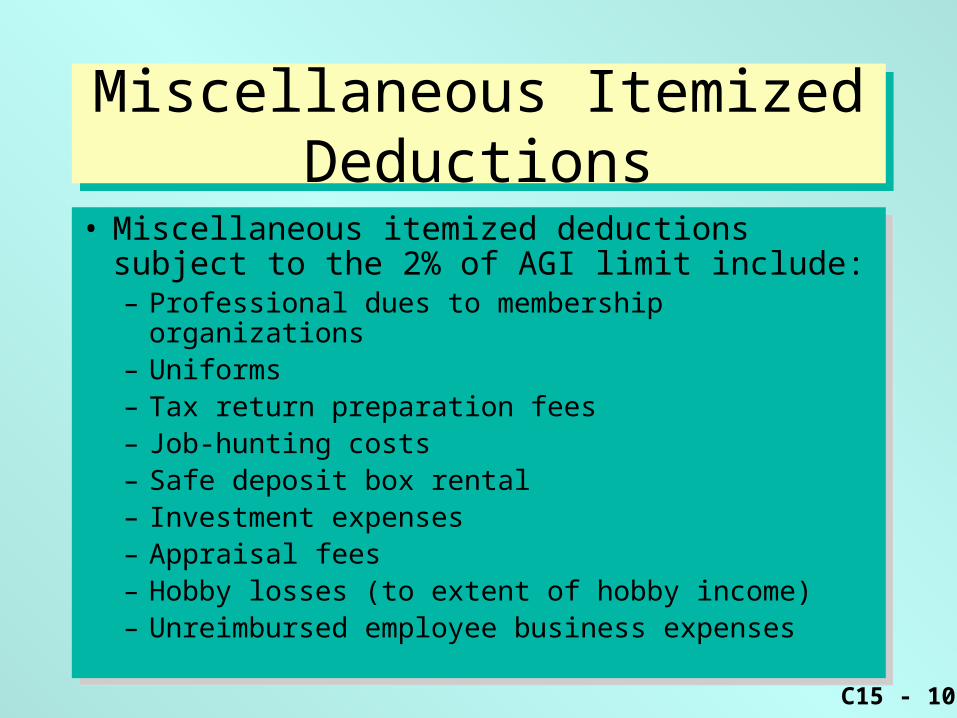

• Miscellaneous itemized deductions subject to the 2% of AGI limit include:– Professional dues to membership organizations– Uniforms– Tax return preparation fees– Job-hunting costs– Safe deposit box rental– Investment expenses– Appraisal fees– Hobby losses (to extent of hobby income)– Unreimbursed employee business expenses

• Miscellaneous itemized deductions subject to the 2% of AGI limit include:– Professional dues to membership organizations– Uniforms– Tax return preparation fees– Job-hunting costs– Safe deposit box rental– Investment expenses– Appraisal fees– Hobby losses (to extent of hobby income)– Unreimbursed employee business expenses

C15 - 106

Other Miscellaneous Itemized Deductions

Other Miscellaneous Itemized Deductions

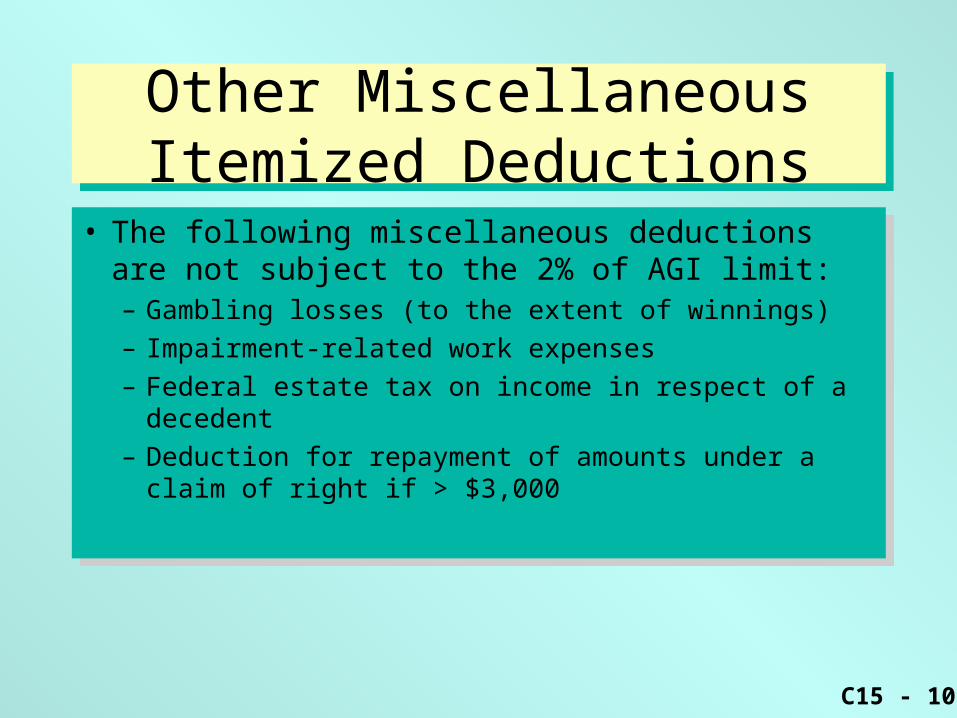

• The following miscellaneous deductions are not subject to the 2% of AGI limit:– Gambling losses (to the extent of winnings)

– Impairment-related work expenses

– Federal estate tax on income in respect of a decedent

– Deduction for repayment of amounts under a claim of right if > $3,000

• The following miscellaneous deductions are not subject to the 2% of AGI limit:– Gambling losses (to the extent of winnings)

– Impairment-related work expenses

– Federal estate tax on income in respect of a decedent

– Deduction for repayment of amounts under a claim of right if > $3,000

C15 - 107

Overall Limitation on Itemized Deductions (slide 1 of 3)

Overall Limitation on Itemized Deductions (slide 1 of 3)

• Taxpayers with AGI in excess of the specified threshold will lose part of their benefits from certain itemized deductions– Threshold amount in 1999 is $126,600

($63,300 if married, filing separately)

• Taxpayers with AGI in excess of the specified threshold will lose part of their benefits from certain itemized deductions– Threshold amount in 1999 is $126,600

($63,300 if married, filing separately)

C15 - 108

Overall Limitation on Itemized Deductions (slide 2 of 3)

Overall Limitation on Itemized Deductions (slide 2 of 3)

• Itemized deductions subject to possible reduction are:– Taxes, residential interest, charitable

deductions, and miscellaneous itemized deductions subject to the 2% floor

• Medical, investment interest, nonbusiness casualties & thefts, and gambling losses are not subject to reduction

• Itemized deductions subject to possible reduction are:– Taxes, residential interest, charitable

deductions, and miscellaneous itemized deductions subject to the 2% floor

• Medical, investment interest, nonbusiness casualties & thefts, and gambling losses are not subject to reduction

C15 - 109

Overall Limitation on Itemized Deductions (slide 3 of 3)

Overall Limitation on Itemized Deductions (slide 3 of 3)

• Amount of reduction– Reduction is lesser of:

• (AGI - threshold) x 3%, or

• 80% x total itemized deductions subject to reduction

• Amount of reduction– Reduction is lesser of:

• (AGI - threshold) x 3%, or

• 80% x total itemized deductions subject to reduction

C15 - 110

Learning Objective 8Learning Objective 8

Understand the adoption expenses credit, child tax credit, education tax credits, child and dependent care credit, credit for the elderly, and earned income credit.

Understand the adoption expenses credit, child tax credit, education tax credits, child and dependent care credit, credit for the elderly, and earned income credit.

C15 - 111

Adoption Expenses Credit (slide 1 of 2)

Adoption Expenses Credit (slide 1 of 2)

• Credit for qualified adoption expenses incurred in adoption of eligible child– Examples of expenses: adoption fees, court

costs, attorney fees– Maximum credit is $5,000 – Credit is phased-out ratably for modified AGI

between $75,000 and $115,000

• Credit for qualified adoption expenses incurred in adoption of eligible child– Examples of expenses: adoption fees, court

costs, attorney fees– Maximum credit is $5,000 – Credit is phased-out ratably for modified AGI

between $75,000 and $115,000

C15 - 112

Adoption Expenses Credit (slide 2 of 2)

Adoption Expenses Credit (slide 2 of 2)

• Eligible child is one that is: – Less than 18 years of age, or– Physically or mentally incapable of caring for

himself

• Nonrefundable credit– Excess may be carried forward for five years

• Married taxpayers must file jointly to claim

• Eligible child is one that is: – Less than 18 years of age, or– Physically or mentally incapable of caring for

himself

• Nonrefundable credit– Excess may be carried forward for five years

• Married taxpayers must file jointly to claim

C15 - 113

Child Tax Credit(slide 1 of 2)

Child Tax Credit(slide 1 of 2)

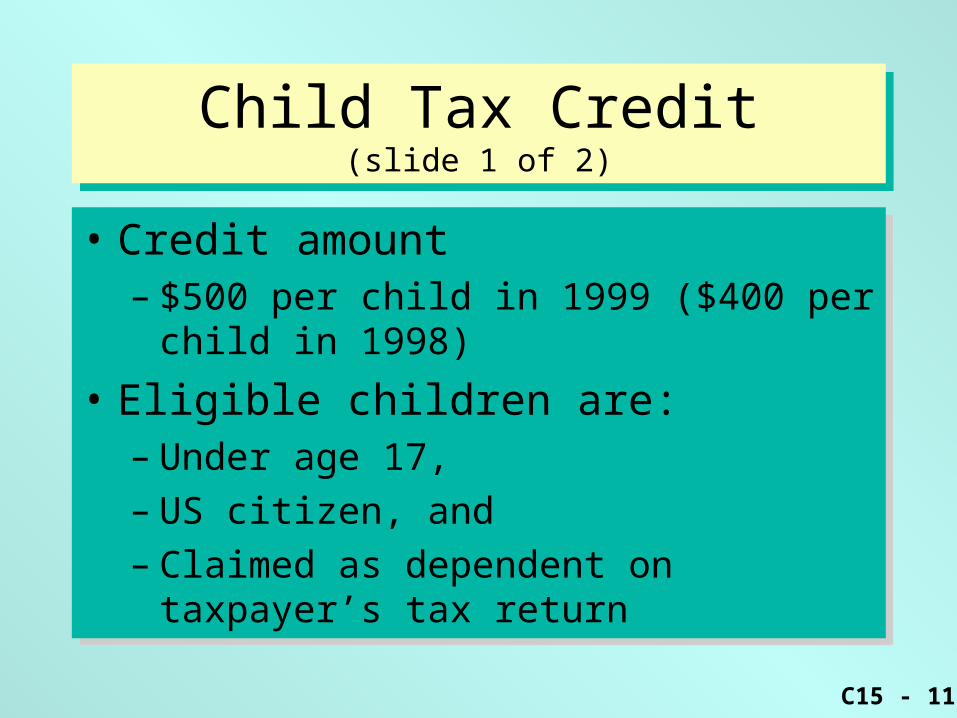

• Credit amount– $500 per child in 1999 ($400 per child in 1998)

• Eligible children are:– Under age 17,– US citizen, and– Claimed as dependent on taxpayer’s tax return

• Credit amount– $500 per child in 1999 ($400 per child in 1998)

• Eligible children are:– Under age 17,– US citizen, and– Claimed as dependent on taxpayer’s tax return

C15 - 114

Child Tax Credit(slide 2 of 2)

Child Tax Credit(slide 2 of 2)

• Credit is phased out by $50 for each $1,000 of AGI above specified levels– $110,000 for joint filers– $55,000 for married filing separately– $75,000 for single

• Credit is phased out by $50 for each $1,000 of AGI above specified levels– $110,000 for joint filers– $55,000 for married filing separately– $75,000 for single

C15 - 115

Child and Dependent Care Credit (slide 1 of 4)

Child and Dependent Care Credit (slide 1 of 4)

• General qualifications for credit– Must have employment related care costs for a

• Dependent under age 13, or

• Handicapped dependent or spouse

• General qualifications for credit– Must have employment related care costs for a

• Dependent under age 13, or

• Handicapped dependent or spouse

C15 - 116

Child and Dependent Care Credit (slide 2 of 4)

Child and Dependent Care Credit (slide 2 of 4)

• Credit amount– Eligible care costs x applicable percentage– Applicable percentage ranges from 20% to 30%

• Married taxpayers must file a joint return to obtain credit

• Credit amount– Eligible care costs x applicable percentage– Applicable percentage ranges from 20% to 30%

• Married taxpayers must file a joint return to obtain credit

C15 - 117

Child and Dependent Care Credit (slide 3 of 4)

Child and Dependent Care Credit (slide 3 of 4)

• Eligible care costs defined– Costs for care of qualified individual within taxpayer’s

home or outside home

– If outside home, handicapped dependent or spouse must spend at least 8 hours a day within taxpayer’s home

– Amount of costs that qualify is the lesser of actual costs or $2,400 for one qualified individual, and $4,800 for two or more qualified individuals

• Eligible care costs defined– Costs for care of qualified individual within taxpayer’s

home or outside home

– If outside home, handicapped dependent or spouse must spend at least 8 hours a day within taxpayer’s home

– Amount of costs that qualify is the lesser of actual costs or $2,400 for one qualified individual, and $4,800 for two or more qualified individuals

C15 - 118

Child and Dependent Care Credit (slide 4 of 4)

Child and Dependent Care Credit (slide 4 of 4)

• Earned income limitation– Amount of eligible care costs cannot exceed

taxpayer’s or spouse’s earned income– Full-time student or disabled taxpayer or

spouse are assumed to have earned income up to maximum per month limits

• Earned income limitation– Amount of eligible care costs cannot exceed

taxpayer’s or spouse’s earned income– Full-time student or disabled taxpayer or

spouse are assumed to have earned income up to maximum per month limits

C15 - 119

Education Tax Credits(slide 1 of 4)

Education Tax Credits(slide 1 of 4)

• Beginning in 1998, 2 new credits– Hope scholarship credit– Lifetime learning credit

• Both nonrefundable credits are available for qualifying tuition and related expenses– Room, board, and book costs are ineligible for

the credits

• Beginning in 1998, 2 new credits– Hope scholarship credit– Lifetime learning credit

• Both nonrefundable credits are available for qualifying tuition and related expenses– Room, board, and book costs are ineligible for

the credits

C15 - 120

Education Tax Credits(slide 2 of 4)

Education Tax Credits(slide 2 of 4)

• Maximum credits– Hope scholarship credit maximum per eligible student

is $1,500 per year for first 2 years of postsecondary education

• 100% of first $1,000 of tuition expenses plus 50% of next $1,000 of tuition expenses

– Lifetime learning credit maximum per taxpayer is 20% of qualifying expenses (up to $5,000 per year) incurred after 6/30/98

• Cannot be claimed in same year the Hope credit is claimed

• Maximum credits– Hope scholarship credit maximum per eligible student

is $1,500 per year for first 2 years of postsecondary education

• 100% of first $1,000 of tuition expenses plus 50% of next $1,000 of tuition expenses

– Lifetime learning credit maximum per taxpayer is 20% of qualifying expenses (up to $5,000 per year) incurred after 6/30/98

• Cannot be claimed in same year the Hope credit is claimed

C15 - 121

Education Tax Credits(slide 3 of 4)

Education Tax Credits(slide 3 of 4)

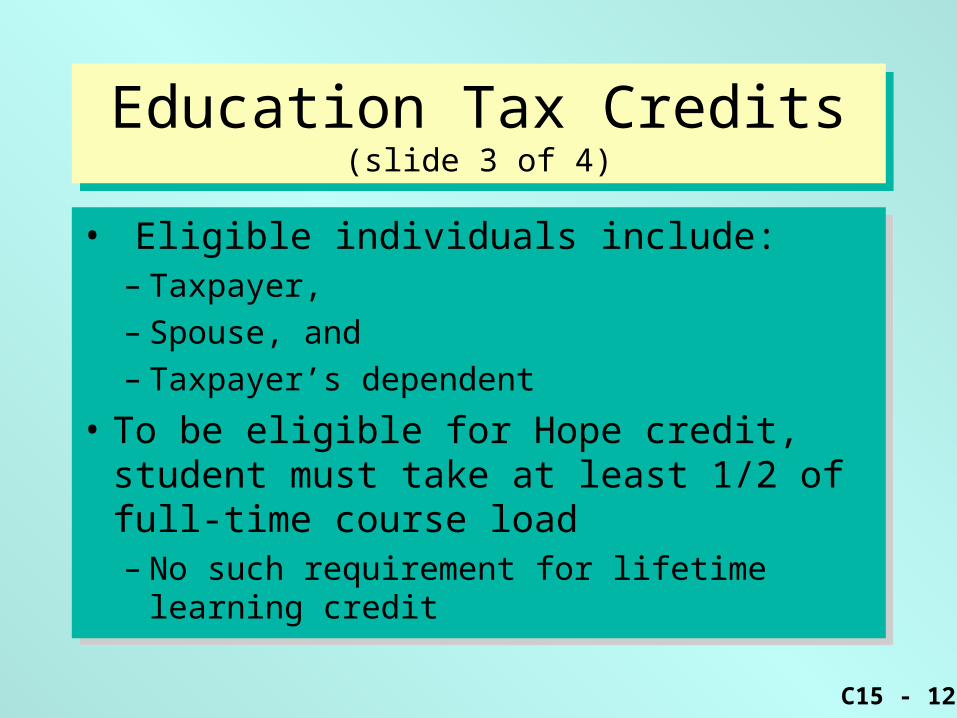

• Eligible individuals include:– Taxpayer,– Spouse, and – Taxpayer’s dependent

• To be eligible for Hope credit, student must take at least 1/2 of full-time course load– No such requirement for lifetime learning credit

• Eligible individuals include:– Taxpayer,– Spouse, and – Taxpayer’s dependent

• To be eligible for Hope credit, student must take at least 1/2 of full-time course load– No such requirement for lifetime learning credit

C15 - 122

Education Tax Credits(slide 4 of 4)

Education Tax Credits(slide 4 of 4)

• Education Tax Credits(cont’d)– Income Limitations

• Both education credits are combined and phased out for AGI of $80,000 to $100,000 for married filing jointly and $40,000 to $50,000 for others

• Taxpayers can’t receive a double tax benefit for education expenses

• Can’t claim a credit for amounts otherwise excluded from income (e.g., scholarships and employer-paid education assistance)

• Education Tax Credits(cont’d)– Income Limitations

• Both education credits are combined and phased out for AGI of $80,000 to $100,000 for married filing jointly and $40,000 to $50,000 for others

• Taxpayers can’t receive a double tax benefit for education expenses

• Can’t claim a credit for amounts otherwise excluded from income (e.g., scholarships and employer-paid education assistance)

C15 - 123

Credit for Elderly or Disabled Taxpayers(slide 1 of 2)

Credit for Elderly or Disabled Taxpayers(slide 1 of 2)

• General qualifications– Age 65 or older, or– Under age 65 and permanently and totally

disabled

• General qualifications– Age 65 or older, or– Under age 65 and permanently and totally

disabled

C15 - 124

Credit for Elderly or Disabled Taxpayers(slide 2 of 2)

Credit for Elderly or Disabled Taxpayers(slide 2 of 2)

• Credit amount– Maximum credit = $1,125

• Amount reduced for taxpayers with Social Security benefits or AGI in excess of specified amounts

– IRS will figure for taxpayer if necessary

• Credit amount– Maximum credit = $1,125

• Amount reduced for taxpayers with Social Security benefits or AGI in excess of specified amounts

– IRS will figure for taxpayer if necessary

C15 - 125

Earned Income Credit(slide 1 of 2)

Earned Income Credit(slide 1 of 2)

• General qualifications for credit– Must have earned income from being an

employee or self-employed, and– Must have a qualifying child

• Exception: credit is available for some taxpayers having no children

• Qualifying child must meet relationship, residency, and age tests

• General qualifications for credit– Must have earned income from being an

employee or self-employed, and– Must have a qualifying child

• Exception: credit is available for some taxpayers having no children

• Qualifying child must meet relationship, residency, and age tests

C15 - 126

Earned Income Credit(slide 2 of 2)

Earned Income Credit(slide 2 of 2)

• Credit amount (1999 tax year)– Applicable percentage rate x earned income

• Rate and maximum amount of earned income determined by number of qualifying children

• Phase-out of credit begins when earned income (or AGI) exceeds $12,460

• Use IRS tables to calculate exact credit amount

• Credit amount (1999 tax year)– Applicable percentage rate x earned income

• Rate and maximum amount of earned income determined by number of qualifying children

• Phase-out of credit begins when earned income (or AGI) exceeds $12,460

• Use IRS tables to calculate exact credit amount

C15 - 127

West’s Federal Taxation:An Introduction to Business Entities

West’s Federal Taxation:An Introduction to Business Entities

Chapter 15 Introduction To The

Taxation Of Individuals

Chapter 15 Introduction To The

Taxation Of Individuals

The End

C15 - 128

If you have any comments or suggestions concerning this PowerPoint Presentation for West's Federal Taxation, please contact:

Donald R. Trippeer, PhD, CPA

East Carolina University

He is eager to hear from you.

If you have any comments or suggestions concerning this PowerPoint Presentation for West's Federal Taxation, please contact:

Donald R. Trippeer, PhD, CPA

East Carolina University

He is eager to hear from you.

West’s Federal Taxation:An Introduction to Business Entities

West’s Federal Taxation:An Introduction to Business Entities