350

The Institute of Chartered Accountants of Bangladesh ASSURANCE Professional Stage Knowledge Level www.icab.org.bd Study Manual

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | erfan-khan |

| View: | 95 times |

| Download: | 13 times |

The Institute of Chartered Accountants of Bangladesh

ASSURANCEProfessional Stage Knowledge Level

Study Manual

www.icab.org.bd

ii © The Institute of Chartered Accountants in England and Wales, March 2009

AssuranceThe Institute of Chartered Accountants of Bangladesh Professional Stage

These learning materials have been prepared by the Institute of Chartered Accountants in England and Wales

ISBN 978-1-84152-637-9First edition 2009

All rights reserved. No part of this publication may be reproduced ortransmitted in any form or by any means or stored in any retrieval system, ortransmitted in, any form or by any means, electronic, mechanical, photocopying,recording or otherwise without prior permission of the publisher.

© The Institute of Chartered Accountants in England and Wales, March 2009 iii

Welcome to the ICAB

iv © The Institute of Chartered Accountants in England and Wales, March 2009

© The Institute of Chartered Accountants in England and Wales, March 2009 v

Contents

Introduction vii

Specification grid for Assurance viii

The learning materials ix

Study guide x

Getting help xvii

Syllabus and learning outcomes xviii

1. Concept of and need for assurance 1

2. Process of assurance: obtaining an engagement 17

3. Process of assurance: planning the assignment 37

4. Process of assurance: evidence and reporting 67

5. Introduction to internal control 85

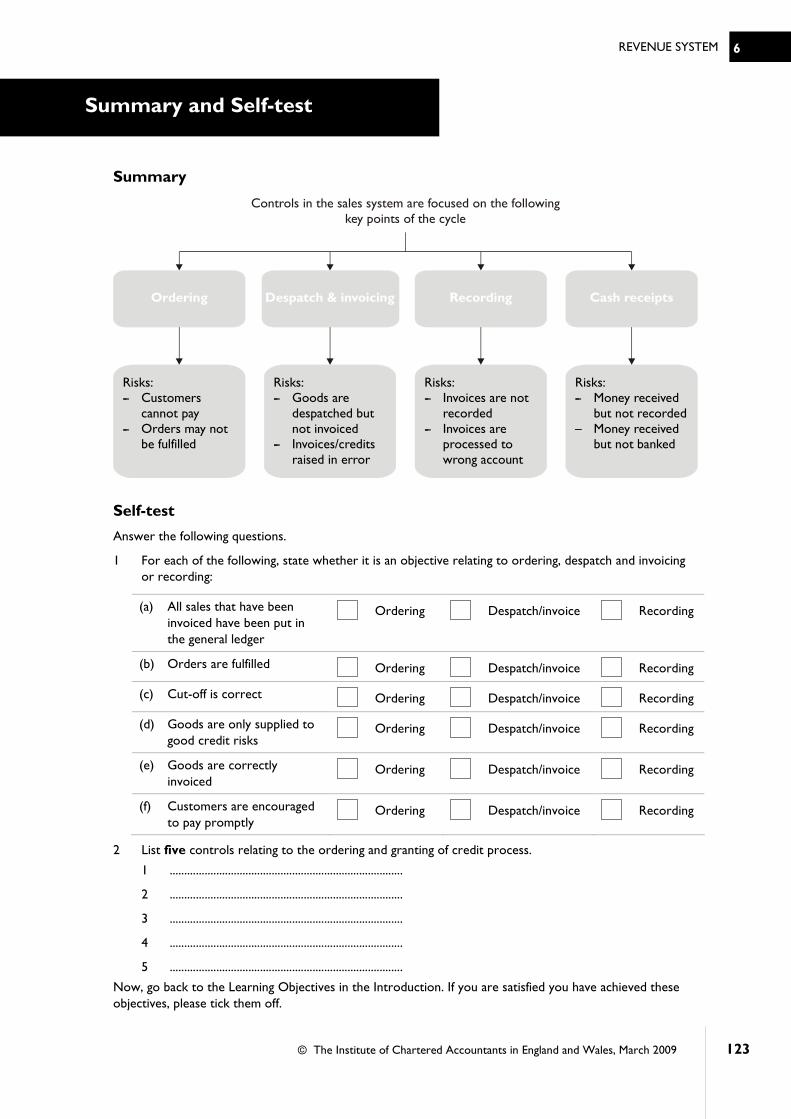

6. Revenue system 107

7. Purchases system 127

8. Employee costs 145

9. Internal audit 159

10. Documentation 169

11. Evidence and sampling 185

12. Management representations 209

13. Substantive procedures – key financial statement figures 221

14. Codes of professional ethics 251

15. Integrity, objectivity and independence 263

16. Confidentiality 287

Sample paper 299

vi © The Institute of Chartered Accountants in England and Wales, March 2009

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 vii

1 Introduction

1.1 What is Assurance and how does it fit within the ProfessionalStage?

Structure

The syllabus has been designed to develop core technical, commercial, and ethical skills and knowledge in astructured and rigorous manner.

The diagram below shows the fourteen modules at the Professional stage, where the focus is on theacquisition and application of technical skills and knowledge, and the Advanced stage, which comprises threetechnical modules and the Case Study.

The knowledge base

The aim of the Assurance module is ensure that students understand the assurance process andfundamental principles of ethics and are able to contribute to the assessment of internal controls andgathering of evidence on an assurance engagement.

Progression to application level

The knowledge base that is put in place here will be taken further in the Application level Audit andAssurance module where the aim will be to develop the students’ understanding of the critical aspects ofmanaging an assurance engagement (including audit engagements): acceptance, planning, managing,concluding and reporting. Students will be expected to have an understanding of the audit of not-for-profitentities as well as non-specialised profit oriented entities.

Progression to advanced stage

The Advanced level paper Advanced Audit & Assurance then takes things further again. Ethical and auditissues are likely to be important in the compliance issues faced by business, including controls andcorporate governance. At Advanced Stage this paper also looks at the modern audit process and servicesother than audit, as well as taking the principles learnt and applying these to services performed for a widerange of different clients.

Assurance

viii © The Institute of Chartered Accountants in England and Wales, March 2009

The above illustrates how the knowledge of assurance principles gives a platform from which a progressionof skills and assurance expertise is developed.

1.2 Services provided by professional accountants

Professional accountants should be able to:

Explain the concept of assurance, why assurance is required and the reasons for assuranceengagements being carried out by appropriately qualified professionals

Explain the nature of internal controls and why they are important, document an organisation’sinternal controls and identify weaknesses in internal control systems

Select sufficient and appropriate methods of obtaining assurance evidence and recognise whenconclusions can be drawn from evidence obtained or where issues need to be referred to a seniorcolleague

Understand the importance of ethical behaviour to a professional and explain issues relating tointegrity, objectivity, conflicts of interest, conflicts of loyalty, confidentiality and independence.

2 Specification grid for Assurance

2.1 Module aim

To ensure that students understand the assurance process and fundamental principles of ethics, and areable to contribute to the assessment of internal controls and gathering of evidence on an assuranceengagement.

2.2 Specification grid

This grid shows the relative weightings of subjects within this module and should guide the relative studytime spent on each. Over time the marks available in the assessment will equate to the weightings below,while slight variations may occur in individual assessments to enable suitable questions to be set.

Weighting (%)1 The concept, process and need for assurance 202 Internal controls 253 Gathering evidence on an assurance engagement 354 Professional ethics 20

100

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 ix

3 The learning materials

You will find the learning materials are structured as follows:

Title page Contents page Introduction. This includes

– A review of the subject to set the context

– A list of the top level learning outcomes for this subject area entitled 'Services provided byprofessional accountants' (set with reference to what a newly qualified accountant would beexpected to do as part of their job)

The specification grid for Assurance

A brief note about the learning materials

Study Guide. This includes

– Hints and tips on how to approach studying for your CA exams

– Guidance on how to approach studying with this study manual

– A detailed study guide suggesting how you should study each chapter of this study manual andidentifying the essential points in each chapter

Information on how to obtain help with your studies

The detailed syllabus and learning outcomes

Each chapter has the following components where relevant:

Introduction

– Learning objectives– Practical significance– Stop and think– Working context– Syllabus links

Examination context

– Exam requirements

Chapter topics

Summary and Self-test

Technical reference

Answers to Self-test

Answers to Interactive questions

The technical reference section is designed to assist you when you are working in the office. It should helpyou to know where to look for further information on the topics covered. You will not be examined onthe contents of this section in your examination.

Assurance

x © The Institute of Chartered Accountants in England and Wales, March 2009

4 Study guide

4.1 Help yourself study for your CA exams

Exams for professional bodies such as ICAB are very different from those you have taken at college oruniversity. You will be under greater time pressure before the exam – as you may be combining yourstudy with work. Here are some hints and tips.

The right approach

1 Develop the right attitude

Believe in yourself Yes, there is a lot to learn. But thousands have succeededbefore and you can too.

Remember why you're doing it You are studying for a good reason: to advance your career.

2 Focus on the exam

Read through the Syllabus andStudy Guide

These tell you what you are expected to know and aresupplemented by Examination context sections in thetext.

3 The right method

See the whole picture Keeping in mind how all the detail you need to know fits intothe whole picture will help you understand it better.

The Introduction of each chapter puts the material incontext.

The Learning objectives, Section overviews andExamination context sections show you what youneed to grasp.

Use your own words To absorb the information (and to practise your writtencommunication skills), you need to put it into your ownwords.

Take notes. Answer the questions in each chapter. Draw mindmaps. Try 'teaching' a subject to a colleague or friend.

Give yourself cues to jog yourmemory

The Study Manual uses bold to highlight key points.

Try colour coding with a highlighter pen. Write key points on cards.

4 The right recap

Review, review, review Regularly reviewing a topic in summary form can fix it in yourmemory. The Study Manual helps you review in many ways.

Chapter summary will help you to recall each studysession.

The Self-test actively tests your grasp of the essentials.

Go through the Examples in each chapter a second orthird time.

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 xi

4.2 Study cycle

The best way to approach this Study Manual is to tackle the chapters in order. We will look in detail at howto approach each chapter below but as a general guide, taking into account your individual learning style,you could follow this sequence for each chapter.

Key study steps Activity

Step 1Topic list

This topic list is shown in the contents for each chapter and helps you navigateeach part of the book; each numbered topic is a numbered section in the chapter.

Step 2Introduction

This sets your objectives for study by giving you the big picture in terms of thecontext of the chapter. The content is referenced to the Study guide, andExamination context guidance shows what the examiners are looking for. TheIntroduction tells you why the topics covered in the chapter need to be studied.

Step 3Section

overviews

Section overviews give you a quick summary of the content of each of the mainchapter sections. They can also be used at the end of each chapter to help youreview each chapter quickly.

Step 4Explanations

Proceed methodically through each chapter, particularly focussing on areashighlighted as significant in the chapter introduction or study guide.

Step 5Note taking

Take brief notes, if you wish. Don't copy out too much. Remember that beingable to record something yourself is a sign of being able to understand it. Yournotes can be in whatever format you find most helpful; lists, diagrams, mindmaps.

Step 6Examples

Work through the examples very carefully as they illustrate key knowledge andtechniques.

Step 7Answers

Check yours against the suggested solutions, and make sure you understand anydiscrepancies.

Step 8Chapter summary

Review it carefully, to make sure you have grasped the significance of all theimportant points in the chapter.

Step 9Self-test

Use the Self-test to check how much you have remembered of the topicscovered.

Step 10Question practice

Attempt the question(s) relating to this chapter in the Revision Question Bank.

Moving on...

When you are ready to start revising, you should still refer back to this Study Manual.

As a source of reference.

As a way to review (the Section overviews, Examination context, Chapter summaries and Self-testquestions help you here).

Remember to keep careful hold of this Study Manual – you will find it invaluable in your work. The technicalreference section has been designed to help you in the workplace by directing you to where you can findfurther information on the topics studied.

Assurance

xii © The Institute of Chartered Accountants in England and Wales, March 2009

4.3 Detailed study guide

Use this schedule and your exam timetable to plan the dates on which you will complete each study periodbelow:

Studyperiod

Approach Essential points Duedate

1 Read through Chapter 1 carefully. Makesure you understand what an assuranceengagement is and the different levels ofassurance which it can provide dependingon the specific nature of the engagement.You should also be familiar with theobjective of an audit and the meaning of‘true’ and ‘fair’.

Attempt the Interactive questions and theSelf-test questions to confirm yourunderstanding of the topics covered in thischapter.

Key elements of an assuranceengagement

Definitions of reasonableassurance and limited assurance

Purpose of an audit

Limitations of assurance andthe meaning of theexpectations gap

2 Read through sections 1 and 2 of Chapter2 paying particular attention to theappointment decision chart. You shouldalso attempt Interactive questions 1 and 2.

Read through section 3 and make sure youunderstand the purpose of the engagementletter.

Complete all remaining Interactive and Self-test questions.

Appointment considerations

Communication with previousauditors

Purpose and content of theengagement letter

3 Chapter 3 introduces a number ofimportant auditing concepts and principlesso work through it carefully.

Read through section 1. Make sure you candistinguish between the audit strategy andthe audit plan. You must also be familiarwith the ways in which the auditor willobtain an understanding of the entityincluding the various sources ofinformation.

Section 2 introduces analytical procedures.Work through the Worked example andmake sure you attempt the Interactivequestion on this topic.

Materiality is one of the key concepts inauditing. You must be familiar with thedefinition of materiality and understand itsimpact on the audit overall.

Section 4 deals with audit risk, another keyconcept. Look carefully at the componentsof audit risk and the way in which theyinteract.

Complete all the Interactive and Self-testquestions.

Planning procedures

The meaning of professionalscepticism

Applying analytical procedures

Concept of materiality

Audit risk model

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 xiii

Studyperiod

Approach Essential points Duedate

4 Section 1 of Chapter 4 is important as itintroduces some of the basic definitionsand principles of audit evidence which aredeveloped in later chapters. Read throughthis section carefully and attemptInteractive question 1.

Section 2 deals with reporting. You mustbe aware of the basic content of anunqualified audit report, and in particularthe opinion given. Also note section 2.4 onother reports.

Finally complete all the Self-test questionsto confirm your understanding of thetopics covered in this chapter.

Definitions of tests of controlsand substantive procedures

Evaluation of the quality ofdifferent types of evidence

Financial statement assertions

Explicit and implied opinions

Expectations gap

5 Chapter 5 is important as it provides anintroduction to internal control. Theprinciples introduced here are developedfor specific transaction cycles in Chapters6-8.

You need to be able to view this topicfrom both the business’s point of view andthat of the auditor. As you are reading thechapter notice that it is the responsibility ofthe business to implement and maintain asystem of internal controls. The auditorthen records and assesses the system aspart of the audit process.

Definition of internal control

Components of internalcontrol

Types of control activity

IT controls

Methods of recording internalcontrol

6 Chapter 6 looks at internal control withinthe revenue cycle taking each stage of thecycle in turn. This is an important chapteras questions in your assessment mayrequire application of knowledge to aspecific scenario. Read through sections1-4 carefully. Make sure you understandthe difference between the controlobjectives, controls and tests of controls.Attempt Interactive questions 1-4.

Section 5 looks at a particular way in whichthis topic could be examined. Make sureyou attempt Interactive question 5.

Complete all Self-test questions.

Control objectives

Tests of controls

Identifying weaknesses

7 The format of Chapter 7 is very similar tothat of Chapter 6. Again the key issues arethe control objectives at the various stagesof the cycle and the tests of controls whichthe auditor might perform to determinewhether the controls are operatingeffectively. Make sure you are familiar withboth of these aspects within the context ofthe purchases cycle.

Control objectives

Tests of controls

Identifying weaknesses

Assurance

xiv © The Institute of Chartered Accountants in England and Wales, March 2009

Studyperiod

Approach Essential points Duedate

Also note section 4 on the identification ofweaknesses and attempt Interactivequestion 5.

8 Chapter 8 continues the theme of internalcontrols but applied to the payroll cycle.Again, you must be familiar with the keycontrol objectives and tests of controls ateach stage of the cycle. Attempt Interactivequestions 1-3.

Work through section 4 and attemptInteractive question 4.

Complete all Self-test questions.

9 This is a brief chapter but includes someimportant information. Read throughsections 1 and 2 paying particular attentionto the distinction between the internal andthe external auditor and the role ofinternal audit.

You should also complete all of theInteractive and Self-test questions.

Definition of internal audit

Comparison of internal andexternal audit

Internal audit activities

Role within internal control

10 Chapter 10 deals with the straightforwardtopic of audit documentation. Readthrough sections 1 and 2 and review thesample working papers provided which willhelp you to put the topic in context.

Sections 3 and 4 are more technical innature so read through them carefully.Notice the minimum period for which auditdocuments must be retained and that theyare the property of the assurance provider.

Attempt Interactive question 1 and theSelf-test questions.

Purpose of auditdocumentation

Form and content

Permanent and current auditfiles

11 Section 1.1 of this chapter picks up onsome of the points on evidence introducedin Chapter 4. Review these points briefly asthey should be familiar. Then read throughsections 1.2-1.6. Notice in particular thedifferent procedures which can be used toobtain evidence and the way in whichCAATs may be used.

Section 1.4 considers analytical proceduresas a substantive procedure. You will havecome across analytical procedures inChapter 3 as a planning procedure.

Attempt Interactive question 1 beforemoving on.

Sections 2 and 3 look at the issue ofsampling. This is quite a technical topic so

Types of procedure

CAATs

Analytical procedures

Definition of audit sampling

Distinction between statisticaland non-statistical sampling

Factors affecting the samplesize

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 xv

Studyperiod

Approach Essential points Duedate

read through it slowly ensuring that youunderstand the various definitions as youwork through. Also note the different waysof selecting the sample in section 2.3 andreview the Worked example. You shouldattempt Interactive questions 2 and 3 toconfirm your understanding.

Finally attempt the Self-test questions.

12 Chapter 12 is a short chapter but looks atthe important issue of managementrepresentations. The key issues to note arethe general matters which are included inthe letter of representation and theinstances where other specific issues maybe addressed. It is important to note thatmanagement representations cannot be asubstitute for audit evidence which shouldbe available.

Read through sections 1 and 2. Thenreview the example of the managementrepresentation letter in section 3.

Finally attempt Interactive question 1 andthe Self-test questions.

Purpose of writtenmanagement representations

General matters which mustbe included

Instances where managementrepresentations are the onlyavailable audit evidence

13 This is a detailed chapter which looks atthe specific audit procedures which areapplied to key financial statement figures.

Read through section 1. Notice the way inwhich the procedures address the financialstatement assertions. Review the workedexamples and attempt Interactive question1.

In section 2 the key issue is the auditor’sattendance at the inventory count. Workthrough the Worked example takingparticular note of the proceduresperformed by the auditor before, duringand after the count. Then attemptInteractive question 2.

Section 3 deals with the audit ofreceivables. Read through section 3.1carefully and ensure you understand therole of the external confirmation as auditevidence. Make sure you understand thedifference between the positive method ofconfirmation and the negative method andthe circumstances in which these would beused.

In section 4 the key points to note are theprocedures for confirming informationabout a client with the bank and the

Audit tests on non-currentassets

The inventory count

Verification of tradereceivables by directconfirmation

Direct confirmation with thebank

Supplier statementreconciliations

Assurance

xvi © The Institute of Chartered Accountants in England and Wales, March 2009

Studyperiod

Approach Essential points Duedate

performance of the bank reconciliation.Read through section 4 carefully andreview the bank reconciliation in theWorked example. Complete Interactivequestion 4.

Then read through sections 5-7. For theaudit of payables notice the importance ofthe reconciliation of supplier statements.

Finally complete all remaining Interactivequestions and Self-test questions.

14 Chapter 14 introduces the concept ofethical behaviour and sets out the sourcesof guidance on this issue. Specific aspects ofethical behaviour are then developed inChapters 15 and 16.

Read through sections 1-4. Make sure youunderstand that ethical guidance can befound in the IFAC Code, and the ICABCode. Also note the nature of the guidancei.e. it is in the form of a framework ratherthan a set of rules.

Finally, complete Interactive question 1 andthe Self-test questions.

Nature of ethical guidance

Fundamental principles

Threats and safeguards

15 Sections 1 and 2 deal with the key ethicalissue of independence so read throughthese carefully. Questions are likely to testthis topic in detail so you need to have athorough understanding of this area.

You must be familiar with the basicprinciple behind the importance ofindependence and objectivity so do notunderestimate the importance of section 1.Then move on to section 2. There is a lotof detail here so work through itmethodically, taking note of the differentthreats and safeguards. Attempt Interactivequestions 1 and 2 to confirm yourunderstanding.

Sections 3 and 4 deal with the way in whichethical conflicts are resolved. Read thesesections and try Interactive questions 3 and4.

Finally, attempt the Self-test questions.

Self-interest threat andsafeguards

Self-review threat andsafeguards

Familiarity threat andsafeguards

Resolving ethical conflicts

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 xvii

Studyperiod

Approach Essential points Duedate

16 Read through Chapter 16. The key point tounderstand is that confidentiality is afundamental principle. Learn the safeguardsto confidentiality in section 2. There are alimited number of circumstances wheredisclosure is allowed. Read these carefullyin section 3 together with the points onmoney laundering.

You should also complete the Interactivequestion and the Self-test questions.

Safeguards to confidentiality

Circumstances in whichdisclosure is authorised

Revision phase

Your revision will be centred around using the questions and revision guidance in the ICAB RevisionQuestion Bank.

Assurance

xviii © The Institute of Chartered Accountants in England and Wales, March 2009

5 Syllabus and learning outcomes

The following learning outcomes should be read in conjunction with the Assurance and Audit and EthicsStandards tables in section 6.1.

1 The concept, process and need for assurance

Candidates will be able to explain the concept of assurance, why assurance is required and thereasons for assurance engagements being carried out by appropriately qualified professionals.

In the assessment, candidates may be required to:

a. Define the concept of assurance

b. State why users desire assurance reports and provide examples of the benefits gained from them

c. Compare the functions and responsibilities of the different parties involved in an assuranceengagement

d. Compare the purposes and characteristics of, and levels of assurance obtained from, differentassurance engagements

e. Identify the issues which can lead to gaps between the outcomes delivered by the assuranceengagement and the expectations of users of the assurance reports, and suggest how these canbe overcome

f. Define the assurance process, including:

Obtaining the engagement Continuous risk assessment Engagement acceptance The scope of the engagement Planning the engagement Performing the engagement Obtaining evidence Evaluation of results of assurance work Concluding and reporting on the engagement Reporting to the engaging party Keeping records of the work performed

g. Recognise the need to plan and perform assurance engagements with an attitude of professionalscepticism

h. Define the concept of reasonable assurance.

2 Internal controls

Candidates will be able to explain the nature of internal controls and why they are important,document an organisation’s internal controls and identify weaknesses in internal controlsystems.

In the assessment, candidates may be required to:

a. State the reasons for organisations having effective systems of control

b. Identify the fundamental principles of effective control systems

c. Identify the main areas of a business that need effective control systems

d. Identify the components of internal control in both manual and IT environments, including:

The overall control environment Preventative and detective controls Internal audit

e. Define and classify different types of internal control, with particular emphasis upon those whichimpact upon the quality of financial information

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 xix

f. Show how specified internal controls mitigate risk and state their limitations

g. Identify internal controls for an organisation in a given scenario

h. Identify internal control weaknesses in a given scenario

i. Identify, for a specified organisation, the sources of information which will enable a sufficientrecord to be made of accounting or other systems and internal controls.

3 Gathering evidence on an assurance engagement

Candidates will be able to select sufficient and appropriate methods of obtaining assuranceevidence and recognise when conclusions can be drawn from evidence obtained or whereissues need to be referred to a senior colleague.

In the assessment, candidates may be required to:

a. State the reasons for preparing and keeping documentation relating to an assurance engagement

b. Identify and compare the different methods of obtaining evidence from the use of tests of controland substantive procedures, including analytical procedures

c. Recognise the strengths and weaknesses of the different methods of obtaining evidence

d. Identify the situations within which the different methods of obtaining evidence should and shouldnot be used

e. Compare the reliability of different types of assurance evidence

f. Select appropriate methods of obtaining evidence from tests of control and from substantiveprocedures for a given business scenario

g. Recognise when the quantity and quality of evidence gathered from various tests and proceduresis of a sufficient and appropriate level to draw reasonable conclusions on which to base a report

h. Identify the circumstances in which written confirmation of representations from managementshould be sought and the reliability of such confirmation as a form of assurance evidence

i. Recognise issues arising whilst gathering assurance evidence that should be referred to a seniorcolleague.

4 Professional ethics

Candidates will be able to understand the importance of ethical behaviour to a professionaland identify issues relating to integrity, objectivity, professional competence and due care,confidentiality, professional behaviour and independence.

In the assessment, candidates may be required to:

a. State the role of ethical codes and their importance to the profession

b. Recognise the differences between a rules based ethical code and one based upon a set ofprinciples

c. Recognise how the principles of professional behaviour protect the public and fellowprofessionals

d. Identify the key features of the system of professional ethics adopted by IFAC and ICAB

e. Identify the fundamental principles underlying the IFAC and the ICAB code of ethics

f. Recognise the importance of integrity and objectivity to professional accountants, identifyingsituations that may impair or threaten integrity and objectivity

g. Suggest courses of action to resolve ethical conflicts relating to integrity and objectivity

h. Respond appropriately to the request of an employer to undertake work outside the confines ofan individual’s expertise or experience

i. Recognise the importance of confidentiality and identify the sources of risks of accidentaldisclosure of information

Assurance

xx © The Institute of Chartered Accountants in England and Wales, March 2009

j. Identify steps to prevent the accidental disclosure of information

k. Identify situations in which confidential information may be disclosed

l. Define independence and recognise why those undertaking an assurance engagement arerequired to be independent of their clients

m. Identify the following threats to the fundamental ethical principles and the independence ofassurance providers:

Self-interest threat Self-review threat Advocacy threat Familiarity threat Intimidation threat

n. Identify safeguards to eliminate or reduce threats to the fundamental ethical principles and theindependence of assurance providers

o. Suggest how a conflict of loyalty between the duty a professional accountant has to theiremployer and the duty to their profession could be resolved.

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 xxi

5.1 Technical knowledge

The tables contained in this section show the technical knowledge covered in the CA syllabus by module.

The level of knowledge required in the relevant Professional stage module and at the Advanced stage isshown.

The knowledge levels are defined as follows:

Level D

An awareness of the scope of the standard.

Level C

A general knowledge with a basic understanding of the subject matter and training in its applicationsufficient to identify significant issues and evaluate their potential implications or impact.

Level B

A working knowledge with a broad understanding of the subject matter and a level of experience in theapplication thereof sufficient to apply the subject matter in straightforward circumstances.

Level A

A thorough knowledge with a solid understanding of the subject matter and experience in the applicationthereof sufficient to exercise reasonable professional judgement in the application of the subject matter inthose circumstances generally encountered by Chartered Accountants.

Key to other symbols:

The knowledge level reached is assumed to be continued

Assurance

xxii © The Institute of Chartered Accountants in England and Wales, March 2009

ProfessionalStage

Title

Ass

ura

nce

Au

dit

an

d

Ass

ura

nce

Ad

van

ced

Sta

ge

The International Auditing and Assurance Standards Board C

The Authority Attaching to Standards Issued by the International Auditing andAssurance Standards Board

A

The Authority Attaching to Practice Statements Issued by the InternationalAuditing and Assurance Standards Board

A

Discussion Papers C

Working Procedures C

Bangladesh Standards on Auditing (BSAs)

200 Objective and General Principles Governing an Audit of FinancialStatements

B A

210 Terms of Audit Engagements B

220 Quality Control for Audit Work B

230 Documentation B A

240 The Auditor’s Responsibility to Consider Fraud and Error in an Audit ofFinancial Statements

B A

250 Consideration of Laws and Regulations in an Audit of Financial Statements B A

260 Communication of Audit Matters with Those Charged with Governance B A

300 Planning an Audit of Financial Statements B A

315 Understanding the Entity and its Environment and Assessing the Risk ofMaterial Misstatement

C A

320 Audit Materiality C A

330 The Auditor’s Procedures in Response to Assessed Risks B A

402 Audit Consideration Relating to Entities Using Service Organisations C C

500 Audit Evidence B A

501 Audit Evidence – Additional Considerations for Specific Items A

505 External Confirmations B B A

510 Initial Engagements Opening Balances B A

520 Analytical Procedures C C A

530 Audit Sampling and Other Means of Testing C C A

540 Audit of Accounting Estimates C C A

545 Auditing Fair Value Measurements and Disclosures A

550 Related Parties B A

560 Subsequent Events B A

INTRODUCTION

© The Institute of Chartered Accountants in England and Wales, March 2009 xxiii

ProfessionalStage

Title

Ass

ura

nce

Au

dit

an

d

Ass

ura

nce

Ad

van

ced

Sta

ge

570 Going Concern A

580 Management Representations C B A

600 Using the Work of Another Auditor C A

610 Considering the Work of Internal Auditing C A

620 Using the Work of an Expert C A

700 The Auditor’s Report on Financial Statements B A

701 Modifications to the Independent Auditor’s Report B

710 Comparatives B A

720 Other Information in Documents Containing Audited Financial Statements B A

800 The Auditor’s Report on Special Purpose Audit Engagements B

International Auditing Practice Statements (IAPS)

1000 Inter-bank Confirmation Procedures D

1004 The Relationship Between Banking Supervisors and Banks’ ExternalAuditors

D

1005 The Special Considerations in the Audit of Small Entities A

1006 Audits of the Financial Statements of Banks D

1010 The Consideration of Environmental Matters in the Audit of FinancialStatements

A

1012 Auditing Derivative Financial Instruments B

1013 Electronic Commerce: Effect on the Audit of Financial Statements A

1014 Reporting by Auditors on Compliance with International FinancialReporting Standards

A

International Standards on Review Engagements (ISREs)

2400 Engagements to Review Financial Statements B

International Standards on Assurance Engagements

3000R Assurance Engagements Other than Audits or Reviews of HistoricalFinancial Information

C B

3400 The Examination of Prospective Financial Information B

International Standards on Related Services (ISRSs)

4400 Engagements to Perform Agreed-upon Procedures Regarding FinancialInformation

B

4410 Engagements to Compile Financial Information B

Assurance

xxiv © The Institute of Chartered Accountants in England and Wales, March 2009

ProfessionalStage

Title

Ass

ura

nce

Au

dit

an

d

Ass

ura

nce

Ad

van

ced

Sta

ge

IFAC Statements

IPPS1 Assuring the Quality of Professional Services C B

BSQC1 Quality Control for Firms that Perform Audits and Reviews ofHistorical Financial Information, and Other Assurance and Related ServicesEngagements

C B

Candidates will also be required to apply the additional requirements set out inBSAs in respect of the standards above.

Ethics Codes and Standards

Ethics Codes and Standards Level Professional Stage modules

IFAC Code of Ethics for ProfessionalAccountants (parts A, B and C)

A AssuranceBusiness and FinanceLawTaxation

ICAB Code of Ethics(schedule C of members handbook)

A Audit and AssuranceBusiness StrategyFinancial ReportingTaxation

© The Institute of Chartered Accountants in England and Wales, March 2009 1

Contents

Introduction

Examination context

Topic List

1 What is assurance?

2 Why is assurance important?

3 Why can assurance never be absolute?

Summary and Self-test

Answers to Self-test

Answers to Interactive questions

chapter 1

Concept of and need forassurance

Assurance

2 © The Institute of Chartered Accountants in England and Wales, March 2009

Introduction

Learning objectives Tick off

Understand the concept of assurance

Recognise the criteria which constitute an assurance engagement

Recognise subject matter suitable to be the subject of an assurance engagement

Understand the different levels of assurance that can be provided in an assuranceengagement, including reasonable assurance

Understand the meaning of 'a true and fair view'

Understand the need for professional accountants to carry out assurance work in the publicinterest

Understand why users desire assurance reports and recognise examples of the benefitsgained from them

Compare the functions and responsibilities of the different parties involved in an assuranceengagement

Understand the issues which can lead to gaps between the outcomes delivered by theassurance engagement and the expectations of users of the assurance reports

Identify how these 'expectations gaps' can be overcome

Specific syllabus references for this chapter are: 1a, b, c, d, e, h.

Practical significance

Users of financial and non-financial information want to have confidence that the information they are usingis reliable and that they can draw valid conclusions as a result of it. They want assurance about the qualityof the information they are using to make decisions. Provision of assurance services is therefore a veryimportant area of business for accountants. Accountants are able to provide assurance on a range ofmatters because they are skilled business professionals. As accountants are subject to strict ethical codes,they are perceived to be trustworthy, and therefore users of information believe that the assurance theygive can be trusted.

Some forms of assurance are required by law in many countries. For example, in the EU, all but the smallestcompanies must have an annual audit of their financial statements. An audit is a high level of assuranceservice which we will introduce in this syllabus and look at in more detail in your later studies.

Stop and think

What other information (financial and non-financial) might users want assurance in relation to?

Working context

As an audit is a legal requirement for many companies, many of you are likely to carry out a lot of yourpractical training in audit. You will also focus on audit when you come to study for the Audit and Assurancepaper at the Application stage of the exams. The broad principles of assurance services can be applied tomany different engagements which may be carried out by your firm.

CONCEPT OF AND NEED FOR ASSURANCE

© The Institute of Chartered Accountants in England and Wales, March 2009 3

1

Syllabus links

You have studied the basic books, records and financial statements of a company in the Accounting paper. Itis in relation to these records that the auditor will seek evidence to be able to give assurance.

As already mentioned, audit is a key form of assurance and you will be able to apply the basic principleslearnt in this paper to that form of assurance service both here and in the Audit and Assurance Paper.

Assurance

4 © The Institute of Chartered Accountants in England and Wales, March 2009

Examination context

Exam requirements

It is crucial to the whole syllabus that you understand the concept of assurance, why it is required and thereason for assurance engagements being carried out by appropriately qualified professionals. You cantherefore expect to see questions in the exam testing your understanding of the definition of assurance andthe different levels of assurance.

In the sample paper, the first five questions relate to the subject matter you will cover in this chapter.

In the assessment, candidates may be required to:

Describe the concept of assurance

State the benefits of an assurance report

Compare the functions and responsibilities of the different parties involved in an assuranceengagement

Describe the levels of assurance obtained from different types of assurance engagement

Describe the concept of the ‘expectations gap’

CONCEPT OF AND NEED FOR ASSURANCE

© The Institute of Chartered Accountants in England and Wales, March 2009 5

1

1 What is assurance?

Section overview

An assurance engagement is one in which a practitioner expresses a conclusion, designed to enhancethe degree of confidence of the intended users, other than the responsible party, about the outcomeof the evaluation or measurement of a subject matter against criteria.

Key elements are: three party involvement, subject matter, suitable criteria, sufficient appropriateevidence, written report.

Assurance engagements can give either a reasonable level of assurance or a limited level of assurance.

There are various examples of assurance services, the key example in Bangladesh is the audit.

1.1 Definition (parties, subject matter, criteria)

Definition

An assurance engagement is one in which a practitioner expresses a conclusion designed to enhancethe degree of confidence of the intended users other than the responsible party about the outcome of theevaluation or measurement of a subject matter against criteria.

The key elements of an assurance engagement are as follows:

Three people or groups of people involved

– The practitioner (accountant)– The intended users– The responsible party (the person(s) who prepared the subject matter)

A subject matter

As we shall see below, the subject matter of an assurance engagement may vary considerably.However, it is likely to fall into one of three categories:

– Data (for example, financial statements or business projections)– Systems or processes (for example, internal control systems or computer systems)– Behaviour (for example, social and environmental performance or corporate governance)

Suitable criteria

The person providing the assurance must have something by which to judge whether the informationis reliable and can be trusted. So for example, in an assurance engagement relating to financialstatements, the criteria might be accounting standards. The practitioner will be able to test whetherthe financial statements have been put together in accordance with accounting standards, and if theyhave, then the practitioner can conclude that there is a degree of assurance that they are reliable.

In the context of company behaviour, suitable criteria to judge whether something is reliable and canbe trusted might be the Combined Code on Corporate Governance, or, if the company has one, itspublished Code of Practice.

Sufficient appropriate evidence to support the assurance opinion

The practitioner must substantiate the opinion that he draws in order that the user can haveconfidence that it is reliable. The practitioner must obtain evidence as to whether the criteria havebeen met. We will look at the collection of evidence in detail later in this Study Manual.

Assurance

6 © The Institute of Chartered Accountants in England and Wales, March 2009

A written report in appropriate form

Lastly, it is required that assurance reports are provided to the intended users in a written form andcontain certain specified information. This adds to the assurance that the user is being given, as itensures that key information is being given and that the assurance given is clear and unequivocal.

Worked example: Assurance engagement

In order to demonstrate these elements of an assurance engagement, the Worked example is that of ahouse purchase. Imagine you are buying a house. There are certain issues you would want assurance about,particularly whether the house is structurally sound. In this situation, you would be unlikely just to trust theword of the person who was selling the house but would seek the additional assurance of a qualifiedprofessional, such as a surveyor.

You should already be able to see the first key element of an assurance engagement, which is theinvolvement of three people:

You (the intended user) The house owner (the responsible party) The surveyor (the practitioner)

The subject matter of this assurance engagement is the house in question. The surveyor will visit the houseto test whether it is sound and will draw a conclusion.

The surveyor will judge whether the house is sound in the context of building regulations, planning rulesand best practice in the building industry. These are the criteria by which he will judge whether he can giveyou assurance that the house is structurally sound.

In order to make a conclusion, the surveyor will obtain evidence from the house (for example, by lookingfor damp patches and making inspections of key elements of the house).

Lastly, when he has drawn a conclusion, the surveyor will issue a report to you, outlining his opinion as towhether the house is sound or not. This report will contain any limitations to his work, for example, if hewas unable to access any of the property or he was unable to lift fitted carpets to inspect the floorunderneath them.

Ultimately, when you have read the surveyor’s report, you will have more assurance about the state of theproperty, and correspondingly, more confidence to pay the deposit, take out a mortgage and buy thathouse.

Interactive question 1: Assurance engagement [Difficulty level: Easy]

You are an accountant who has been approached by Jamal, who wants to invest in Company X. He hasasked you for assurance whether the most recent financial statements of Company X are a reliable basis forhim to make his investment decision.

Identify the key elements of an assurance engagement in this scenario, if you accepted the engagement.

See Answer at the end of this chapter.

1.2 Levels of assurance

The definition of an assurance engagement given above is taken from the International Framework forAssurance Engagements, which is issued by the International Federation of Accountants (IFAC), a globalorganisation for the accountancy profession, which works with its member organisations to protect thepublic interest by encouraging high quality practices around the world. ICAB is a member of IFAC.

CONCEPT OF AND NEED FOR ASSURANCE

© The Institute of Chartered Accountants in England and Wales, March 2009 7

1

The ICAB has adopted International Standards on Auditing (ISAs), some of which you will be introduced toin this Study Manual. However, Bangladesh has not currently adopted the general international standards onassurance provision, and the international framework although these represent good practice anywhere inthe world and some of the detail concerning assurance services you learn will be based on these standards.

The Framework identifies two types of assurance engagement:

Reasonable assurance engagement Limited assurance engagement

Definition

Reasonable assurance: A high, but not absolute, level of assurance.

The reason that there are two types of assurance engagement is that the level of assurance that can begiven depends on the evidence that can be obtained by the practitioner. Using the surveyor example above,a surveyor can only give assurance that a property is structurally sound if he is allowed to enter theproperty to inspect it. If he is only given access to part of the building, he can only give limited assurance.

The key differences between the two types of assurance engagement are therefore:

The evidence obtained The type of opinion given

We shall look in detail at obtaining evidence later in this Study Manual. The key point about evidence is thatin all assurance engagements, sufficient, appropriate evidence must be obtained. We will look at whatconstitutes sufficient, appropriate evidence as we go through the course. What determines whetherevidence is sufficient and appropriate is the level of assurance that the practitioner is trying to give, so it istied in with the type of opinion being given, which we shall look at here. In summary, a lower level ofevidence will be obtained for a limited assurance engagement.

The opinion given in an assurance engagement therefore depends on what type of engagement it is. Asnoted above, there are two levels of assurance expressed positively and negatively.

Say, for example, that a practitioner is seeking evidence to conclude whether the report issued by theChairman of a company in the financial statements is reasonable or not. He could seek evidence, concludethat the statement is reasonable and state in a report something like this:

‘In my opinion, the statement by the Chairman regarding X is reasonable’.

This is a positive statement of his conclusion that the statement is reasonable. Alternatively, he could statein a report something like this:

‘In the course of my seeking evidence about the statement by the Chairman, nothing has come to myattention indicating that the statement is not reasonable.’

This conclusion is less certain, as it implies that matters could exist which cause the statement to beunreasonable, but that the practitioner has not uncovered any such matters. This is therefore callednegative assurance. It is the conclusion that a practitioner gives when he carries out a limited assuranceengagement and seeks a lower level of evidence.

SUMMARY OF TYPES OF ENGAGEMENT

Type of engagement Evidence sought Conclusion given

Reasonable assurance Sufficient and appropriate Positive

Limited assurance Sufficient and appropriate (lower level) Negative

Assurance

8 © The Institute of Chartered Accountants in England and Wales, March 2009

1.3 Examples of assurance engagements

The key example of an assurance engagement in Bangladesh is a statutory audit. We shall look briefly at thenature of this engagement in the next section.

Other examples of assurance engagements include other audits, which may be specialised due to the natureof the business, for example:

Local authority audits

Insurance company audits

Bank audits

Pension scheme audits

Charity audits

Solicitors' audits

Environmental audits

Branch audit (where an overseas company trades in Bangladesh through a branch and requires an auditof that branch although an audit is not required by Bangladesh law)

There are also many issues users want assurance on, where the terms of the engagement will be agreedbetween the practitioner and the person commissioning the report, for example:

Value for money studies Circulation reports (for example, for magazines) Cost/benefit reports Due diligence (where a report is requested on an acquisition target) Reviews of specialist business activities Internal audit Reports on website security, such as WebTrust Fraud investigations Inventories and receivables reports Internal control reports Reports on business plans or projections

1.4 Audit

An audit is historically the most important type of assurance service in Bangladesh. This is because allLimited Liability companies registered with the Registrar of Joint Stock Companies have been required bylaw to have an audit.

Definition

The objective of an audit of financial statements is to enable the auditor to express an opinion whetherthe financial statements are prepared, in all material respects, in accordance with an applicable financialreporting framework.

CONCEPT OF AND NEED FOR ASSURANCE

© The Institute of Chartered Accountants in England and Wales, March 2009 9

1

Worked example: Audit

The key criteria of an assurance engagement can be seen in an audit as follows:

Three party involvement

– The shareholders (users)– The board of directors (the responsible party)– The audit firm (the practitioner)

Subject matter

– The financial statements

Relevant criteria

– Law and accounting standards

Evidence

– As has been said earlier, sufficient and appropriate evidence is required to support an assuranceopinion. The specific requirements in relation to evidence on assurance engagements will belooked at in Chapters 4 and 11.

Written report in a suitable form

– Again, as has been said, an assurance report is a written report issued in a prescribed form. Wewill look at the specific requirements for an audit report in Chapter 4.

In Bangladesh, the auditor will normally express his audit opinion by reference to the ‘true and fair view’,which is an expression of reasonable assurance. Whilst this term is at the heart of the audit, ‘true’ and ‘fair’are not defined in law or audit guidance. However, for practical purposes the following definitions aregenerally accepted.

Definitions

True: Information is factual and conforms with reality, not false. In addition the information conforms withrequired standards and law. The accounts have been correctly extracted from the books and records.

Fair: Information is free from discrimination and bias in compliance with expected standards and rules. Theaccounts should reflect the commercial substance of the company’s underlying transactions.

Auditors in Bangladesh are subject to both legal and professional requirements. The legal requirements arecurrently contained in the Companies Act 1994. Since the current wording of the Bangladesh audit report(see Chapter 4) refers to the Companies Act 1994 this text refers to the Companies Act 1994 throughout.The Companies Act 1994 requires that auditors must be a member of the Institute of CharteredAccountants of Bangladesh: The ICAB is a Recognised Supervisory Body under the Ministry of Commerceof the Government of Bangladesh. . Professional qualifications are a prerequisite of membership of ICAB.ICAB has also the responsibility to implement procedures for monitoring its licensed auditors. TheCompanies Act 1994 also sets out factors which make a person ineligible for being a company auditor, forexample, if he or she is:

i. an officer or employee of the company;ii. a partner or an employee of any officer, employee to the company;iii. a person who is indebted to the company exceeding Tk.1,000.iv. A person who is a director or member of a private company, or a partner of a firm, which is the

managing agent of the company.v. a person who is a director or holder of shares exceeding 5% of the subscribed capital.

As you will see later in this course, the professional ethics of the ICAB are usually similar to that of IFAC.

Assurance

10 © The Institute of Chartered Accountants in England and Wales, March 2009

In Bangladesh the responsibility for issuing auditing standards is with the ICAB, which has adopted theinternational standards.ICAB is also responsible for issuing Ethical Standards (ESs) in relation to the independence, objectivity andintegrity of auditors. ICAB is an autonomous body under the Ministry of Commerce, to whom theBangladesh Government has delegated the task of independent monitoring of the Bangladesh accountancyprofession. These standards set professional requirements for auditors.

For example, BSA 200 Objectives and General Principles Governing an Audit of Financial Statements states thatauditors should comply with relevant ethical requirements relating to audit engagements. These will beoutlined later in this Study Manual. An auditor should conduct an audit in accordance with ISAs. RelevantISAs will be referred to in this Study Manual. Auditors are required to carry out their work with a degreeof professional scepticism, meaning that they must make a critical assessment.

Auditors must assess the risks associated with the audit and seek to minimise those risks so that the risk ofgiving the wrong opinion on the financial statements is minimised. This risk is referred to as audit risk and itwill be outlined in detail later in this Study Manual.

2 Why is assurance important?

Section overview

Who the users are will depend on the nature of the subject matter. Users benefit from receiving an independent, professional opinion on the subject matter. Users may also benefit from additional confidence in the subject matter given to others. The existence of an assurance service may prevent errors or frauds occurring in the first place.

2.1 Users

In the key assurance service of audit, which we looked at above, the users were the shareholders of acompany, to whom the financial statements are addressed. In other cases, the users might be the board ofdirectors of a company or a subsection of them.

2.2 Benefits of assurance

The key benefit of assurance is the independent, professional verification being given to the users. Thiscan be seen in the example of the house purchase given above. The importance of independence andobjectivity in assurance provision will be looked at in Chapters 14 and 15.

In addition, assurance may have subsidiary benefits.

Although an assurance report may only be addressed to one set of people, it may give additional confidenceto other parties in a way that benefits the business. For example, audit reports are addressed toshareholders, but the existence of an unqualified audit report might give the bank more confidence to lendmoney to that business, in other words, it enhances the credibility of the information.

The existence of an independent check might help prevent errors or frauds being made and reduce the riskof management bias. In other words, the fact that an assurance service will be carried out might makepeople involved in preparing the subject matter more careful in its preparation and reduce the chance oferrors arising. Therefore it can be seen that an assurance service may act as a deterrent.

In addition, where problems exist within information, the existence of an assurance report draws attentionto the deficiencies in that information, so that users know what those deficiencies are.

Assurance is also important in more general terms. It helps to ensure that high quality, reliable informationexists, leading to effective markets that investors have faith in and trust. It adds to the reputation oforganisations and even countries, so that investors are happy to invest in country X because there is astrong culture of assurance provision there.

CONCEPT OF AND NEED FOR ASSURANCE

© The Institute of Chartered Accountants in England and Wales, March 2009 11

1

3 Why can assurance never be absolute?

Section overview

Assurance can never be absolute. Assurance provision has limitations which may not be understood by users. The expectations gap also adds to the lack of guarantee given by assurance.

Assurance can never be absolute. Assurance providers will never give a certification of absolute correctnessdue to the limitations set out below.

3.1 Limitations of assurance

A key issue for accountants is that there are limitations to assurance services, and therefore there is alwaysa risk involved that the wrong conclusion will be drawn. We shall look in more detail at this issue ofassurance engagement risk in Chapter 3.

The limitations of assurance services include:

The fact that testing is used – the auditors do not oversee the process of building the financialstatements from start to finish.

The fact that the accounting systems on which assurance providers may place a degree of reliance alsohave inherent limitations (we shall look at control systems and their limitations in Chapter 5).

The fact that most audit evidence is persuasive rather than conclusive.

The fact that assurance providers would not test every item in the subject matter (this would beprohibitively expensive for the responsible party, so a sampling approach is used – see Chapter 11).

The fact that the client's staff members may collude in fraud that can then be deliberately hidden fromthe auditor or misrepresent matters to them for the same purpose.

The fact that assurance provision can be subjective and professional judgements have to be made (forexample, about what aspects of the subject matter are the most important, how much evidence toobtain, etc).

The fact that assurance providers rely on the responsible party and its staff to provide correctinformation, which in some cases may be impossible to verify by other means.

The fact that some items in the subject matter may be estimates and are therefore uncertain. It isimpossible to conclude absolutely that judgemental estimates are correct.

The fact that the nature of the assurance report might itself be limiting, as every judgement andconclusion the assurance provider has drawn cannot be included in it.

3.2 The expectations gap

The problems users may experience in connection with assurance provision also arise from the limitationsand restrictions inherent in assurance provision. This is often because users are not aware of the nature ofthe limitations on assurance provision, or do not understand them and believe that the assurance provideris offering a service (such as a guarantee of correctness) which in fact he is not.

The distinction between reasonable and limited assurance may also be misunderstood by users.

We shall look at the concept of the expectations gap in more detail in Chapter 4, in the context ofreporting, but in essence it is this lack of understanding which constitutes the expectations gap – meaningthat there is a gap between what the assurance provider understands he is doing and what the user of theinformation believes he is doing.

Assurance providers need to close this gap as far as possible in order to maintain the value of the assuranceprovided for the user. This is done in a variety of ways, for example, by issuing an engagement letter spellingout the work that will be carried out and the limitations of that work (which we shall look at in the nextchapter) and by regularly reviewing the format and content of reports issued as a result of assurance work.

Assurance

12 © The Institute of Chartered Accountants in England and Wales, March 2009

Interactive question 2: Benefits of assurance [Difficulty level: Exam standard]

Which three of the following are benefits of assurance work?

An independent, professional opinion

Additional confidence given to other related parties

Testing as a result of sampling is cheaper for the responsible party

Judgements on estimates can be conclusive

Assurance may act as a deterrent to error or fraud

See Answer at the end of this chapter.

CONCEPT OF AND NEED FOR ASSURANCE

© The Institute of Chartered Accountants in England and Wales, March 2009 13

1

Summary and Self-test

Summary

An assurance engagement is one in

which a practitioner expresses a

conclusion designed to enhance

the degree of confidence of theintended users other than the

responsible party about the

outcome of the evaluation or

measurement of a subject matter

against criteria.

Levels of assurance:

– Limited

– Reasonable (high)

Key elements:

– Three party relationship

– Subject matter

– Suitable criteria

– Sufficient appropriate evidence

– Written report

Key example: audit

Directors, auditors, shareholders

Financial statements

Law and accounting standards

As prescribed by ISA 500

Audit report

Benefits:

– Independent, professional opinion

– Added confidence to other users

– Deterrent to error/fraud

Limitations:

Subjective, sampled, limitations of

systems, information from third

parties, limitations of reporting,

includes estimates

Self-test

Now answer the following questions.

1 Assurance services are required by law.

True

False

2 What five elements are required for an engagement to be an assurance engagement?

1........................................

2........................................

3........................................

4........................................

5........................................

Assurance

14 © The Institute of Chartered Accountants in England and Wales, March 2009

3 Name four limitations of an assurance service.

1........................................

2........................................

3........................................

4........................................

4 Reasonable assurance is a high level of assurance.

True

False

Now, go back to the Learning Objectives in the Introduction. If you are satisfied you have achieved theseobjectives, please tick them off.

CONCEPT OF AND NEED FOR ASSURANCE

© The Institute of Chartered Accountants in England and Wales, March 2009 15

1

Answers to Self-test

1 False (an audit is required by law for all registered limited liability companies, not the assuranceservices).

2 1 Three party relationship2 Subject matter3 Suitable criteria4 Sufficient appropriate evidence5 Written report

3 From:

1 Subjective exercise2 Sampling3 Limitations in systems4 Limitations in report5 Information from third parties6 Estimations

4 True

Assurance

16 © The Institute of Chartered Accountants in England and Wales, March 2009

Answers to Interactive questions

Answer to Interactive question 1

1 Three party involvement:

Jamal (the intended user) You (the practitioner) The directors of Company X as they produce the financial statements (the responsible party)

2 Subject matter

The most recent financial statements of Company X are the subject matter

3 Relevant criteria

It is most likely in this instance that the criteria would be accounting standards, so that Jamal wasassured that the financial statements were properly prepared and comparable with other companies'financial statements

4 Evidence

You would have to agree the extent of procedures in relation to this assignment with Jamal so that heknew the level of evidence you were intending to seek. This would depend on several factors,including the degree of secrecy in the proposed transaction and whether the directors of Company Xallowed you to inspect the books and documents

5 Report

Again, the nature of the report would be agreed between you and Jamal, however, it would be awritten report containing your opinion on the financial statements

Answer to Interactive question 2

An independent, professional opinion

Additional confidence given to other related parties

Assurance may act as a deterrent to error or fraud

C

I

E

T

S

T

A

A

c

Po

hapter 2

rocess of assurance:

© The Institute of Chartered Accountants in England and Wales, March 2009 17

ontents

ntroduction

xamination context

opic List

1 Obtaining an engagement

2 Accepting an engagement

3 Agreeing terms of an engagement

ummary and Self-test

echnical reference

nswers to Self-test

nswers to Interactive questions

btaining an engagement

Assurance

18 © The Institute of Chartered Accountants in England and Wales, March 2009

Introduction

Learning objectives Tick off

Be aware of how assurance firms obtain work

Understand the key issues practitioners must consider before accepting engagements

Know what a letter of engagement is and what it does

The specific syllabus reference for this chapter is: 1f.

Practical significance

In practice, the matters covered in this chapter are very important to assurance firms. It is important toknow how to obtain clients and therefore secure future revenue. It is important to only accept clientswhich the firm is able to serve and engagements which the firm has the resources to carry out. It isparticularly important that all parties understand the nature of the work that will be carried out, as this mayprevent disputes and problems later on.

Another important area for practitioners is the increased client awareness and identification proceduresrequired to guard against involvement in money laundering. The crime of money laundering includes chargeswhich accountants may fall foul of. It is vital to practitioners that 'know your client' procedures areunderstood by all staff and carried out properly.

Stop and think

Given the problems with assurance noted in the previous chapter, how can assurance firms ensure thattheir clients understand the services they are being offered?

Working context

During your training, you are unlikely to be involved in obtaining clients or determining whether anengagement is going to be accepted. However, if you continue in your career to higher levels, evenpartnership, then these will be important practical issues for you.

However, you are the face of the assurance firm when carrying out engagements, and you may be in aposition where it is necessary to clarify the scope of the work that you are carrying out to aid a client’sunderstanding. In such a case, it might be necessary to refer to the terms of engagement between the firmand the client, and it will be important that you understand what you are talking about, if asked.

Syllabus links

The issues of obtaining engagements will be looked at in much greater detail in the Audit and Assurancepaper at the Application level.

PROCESS OF ASSURANCE: OBTAINING AN ENGAGEMENT

© The Institute of Chartered Accountants in England and Wales, March 2009 19

2

Examination context

Exam requirements

This is a fairly minor area for the exam, but you could expect at least one question on the scope of theengagement (there is a question about engagement letters in the sample paper) and possibly another on theconsiderations of the assurance firm when deciding to accept engagements.

In the assessment, candidates may be required to:

Identify acceptance procedures

Identify sources of information about new clients

Select procedures required by money laundering legislation

Determine the purpose of a letter of engagement

Assurance

20 © The Institute of Chartered Accountants in England and Wales, March 2009

1 Obtaining an engagement

Section overview

Accountants may sometimes be invited to tender for an audit.

How assurance firms obtain clients is an important practical question, but it is largely outside the scope ofthis syllabus. In brief, you should be aware that:

Accountants are often invited to tender for particular engagements, which means that they offer aquote for services, outlining the personnel, usually in competition with other firms which are tendering atthe same time.

In this syllabus, if the topics in this chapter are examined, it will be in the context of an accountant beinginvited by a potential client to accept an engagement. We will go on now to look at the things which anaccountant must consider when he is so invited.

2 Accepting an engagement

Section overview

The present and proposed auditors should normally communicate about the client prior to theaudit being accepted.

The client must be asked to give permission for communication to occur. If the client refuses to givepermission, the proposed auditors must consider the reasons for such refusal.

The auditors must ensure they have sufficient resources (time and staff, for example) to carry out theappointment.

This section covers the procedures that the auditors must undertake to ensure that theirappointment is valid and that they are clear to act.

2.1 Appointment considerations

Schedule C of ICAB Code of Ethics as well as IFAC Code of Ethics sets out the rules under whichaccountants should accept new appointments. Before a new audit client is accepted, the auditors mustensure that there are no independence or other ethical issues likely to cause significant problems withthe ethical code (i.e. significant threats to complying with the fundamental principles of ethical behaviour –see later in this text). Furthermore, new auditors should ensure that they have been appointed in a properand legal manner.

The nominee auditors must carry out the following procedures.

Acceptance procedures

Ensure professionally qualified to act Consider whether disqualified on legal or ethical grounds,for example if there would be a conflict of interest withanother client. We will look in more detail at ethicalissues later in this Study Manual.

Ensure existing resources adequate Consider available time, staff and technical expertise.

PROCESS OF ASSURANCE: OBTAINING AN ENGAGEMENT

© The Institute of Chartered Accountants in England and Wales, March 2009 21

2

Acceptance procedures

Obtain references Make independent enquiries if directors not personallyknown.

Communicate with present auditors Enquire whether there are reasons/circumstances behindthe change which the new auditors ought to know, also asa matter of courtesy.

Some of the basic factors for consideration are given below.

The integrity of those managing a company will be of great importance, particularly if the company iscontrolled by one or a few dominant personalities.

The audit firm will also consider whether the client is likely to be high or low risk to the firm in termsof being able to draw an appropriate assurance conclusion in relation to that client. The following tablecontrasts low and high risk clients.

Low risk High risk

Good long-term prospects Poor recent or forecast performance

Well-financed Likely lack of finance

Strong internal controls Significant control weaknesses

Conservative, prudent accounting policies Evidence of questionable integrity, doubtful accountingpolicies

Competent, honest management Lack of finance director

Few unusual transactions Significant unexplained transactions or transactions withconnected companies

Where the risk level of a company's audit is determined as anything other than low, then the specific risksshould be identified and documented. It might be necessary to assign specialists in response to these risks,particularly industry specialists, as independent reviewers. Some audit firms have procedures for closelymonitoring audits which have been accepted, but which are considered high risk.

Generally, the expected fees from a new client should reflect the level of risk expected. They should alsooffer the same sort of return expected of clients of this nature and reflect the overall financial strategy ofthe audit firm. Occasionally, the audit firm will want the work to gain entry into the client's particularindustry, or to establish better contacts within that industry. These factors will all contribute to a totalexpected economic return.

The audit firm will generally want the relationship with a client to be long term. This is not only to enjoyreceiving fees year after year; it is also to allow the audit work to be enhanced by better knowledge of theclient and thereby offer a better service.

Conflict of interest problems can be significant; the firm should establish that no existing clients will causedifficulties as competitors of the new client. Other services to other clients may have an impact here, notjust audit.

The audit firm must have the resources to perform the work properly, as well as any specialistknowledge or skills. The impact on existing engagements must be estimated, in terms of staff time andthe timing of the audit.

Assurance

22 © The Institute of Chartered Accountants in England and Wales, March 2009

Sources of information about new clients

Enquiries of other sources Bankers, solicitors

Review of documents Most recent annual accounts, listing particulars, credit rating

Previous accountants/auditors Previous auditors should be invited to disclose fully allrelevant information

Review of rules and standards Consider specific laws/standards that relate to industry