Consolidated statements present financial performance and status of consolidated companies as a single economic entity Intercompany transactions must be removed

Two types of intercompany sales/transfers Downstream sale/transfer

Occurs when the parent sells to a subsidiary

Upstream sale/transfer Occurs when a subsidiary sells to a parent

Providing services such as design, maintenance, accounting, payroll, etc. Eliminate revenue on the provider’s books Eliminate expense on the recipient’s books

Loans between parent and subsidiary Eliminate loan receivable on lender’s books Eliminate loan payable on borrower’s books Eliminate interest revenue on lender’s books Eliminate interest expense on borrower’s

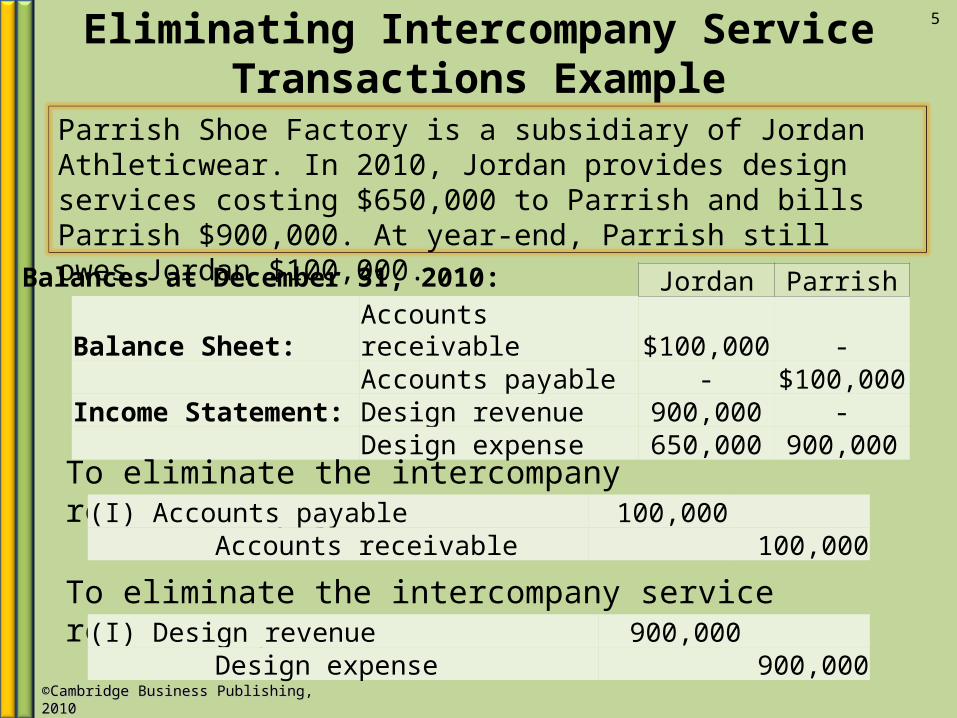

Eliminating Intercompany Service Transactions Example

Parrish Shoe Factory is a subsidiary of Jordan Athleticwear. In 2010, Jordan provides design services costing $650,000 to Parrish and bills Parrish $900,000. At year-end, Parrish still owes Jordan $100,000.

5

Balances at December 31, 2010: Jordan ParrishBalance Sheet: Accounts receivable $100,000 - Accounts payable - $100,000Income Statement: Design revenue 900,000 - Design expense 650,000 900,000

To eliminate the intercompany receivable/payable:(I) Accounts payable 100,000

Accounts receivable 100,000

To eliminate the intercompany service revenue/expense:(I) Design revenue 900,000

Eliminating Intercompany Loan Transactions Example

Parrish Shoe Factory is a subsidiary of Jordan Athleticwear. In 2010, Jordan loans $1,000,000 to Parrish. Interest on the loan totals $50,000, and is accrued and paid.

6

Balances at December 31, 2010:

To eliminate the intercompany loan principal:

To eliminate the intercompany interest revenue/expense:

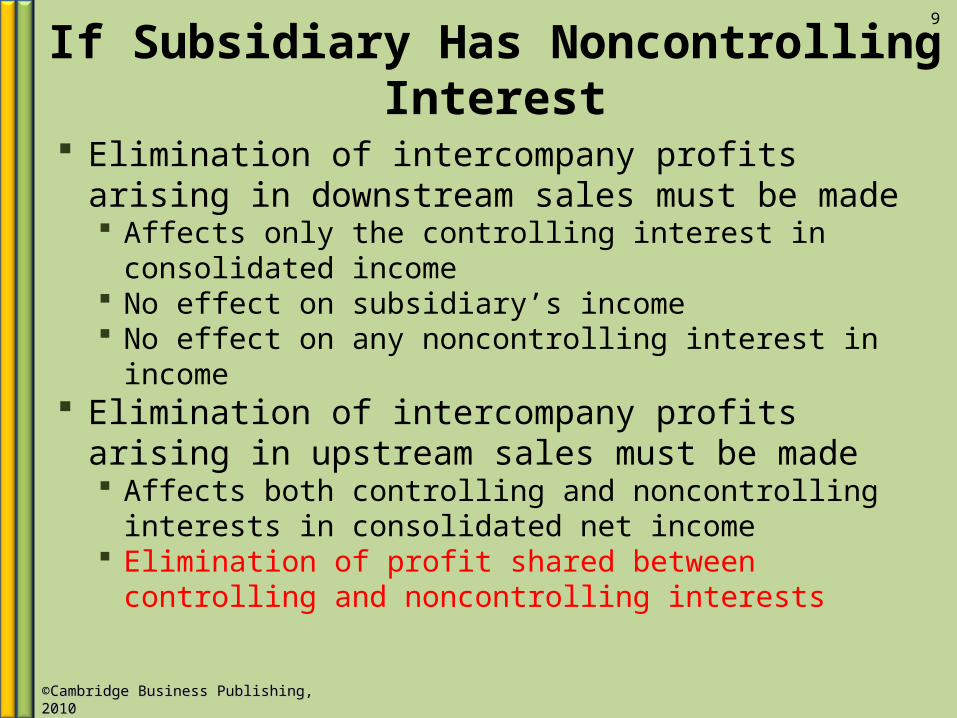

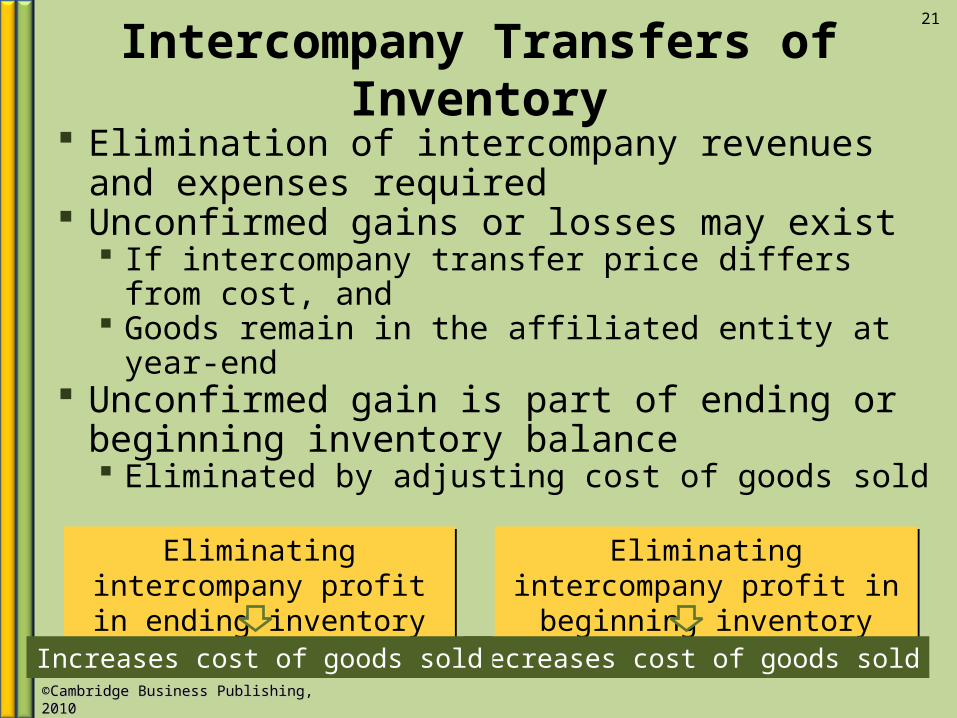

Result from transferred assets from one affiliate to the other

Per ARB 51, profits not yet confirmed by further sale to outside parties must be eliminated Both upstream and downstream transactions i.e., not considered to be arm’s-length transactions

Parrish Shoe Factory is a subsidiary of Jordan Athleticwear. In 2010, Jordan sells land to Parrish for $1,400,000 that had an original cost of $1,000,000. Prior to consolidation, Jordan shows a gain of $400,000 on its books while Parrish carries the land at $1,400,000.

8

To eliminate the unconfirmed intercompany profit and reduce the land to original acquisition cost:

(I) Gain on sale of land 400,000 Land 400,000

• Land in consolidated balance sheet will be $1,000,000• Gain of $400,000 remains in Jordan’s retained earnings• Land remains at $1,400,000 on Parrish’s books

Equity Method ExampleJordan Athleticwear acquires 80% of Parrish Shoe Factory on January 1, 2010. During 2010, Jordan sells merchandise costing $380,000 to Parrish for $400,000, which Parrish still holds at year-end.

12

$20,000 profit unconfirmed until Parrish

sells to an outside customer

Equity in Income of Parrish

Deduct $20,000 to remove downstream intercompany profit

Suppose Parrish sells the merchandise to Jordan, and Jordan holds the merchandise at year-end.

$20,000 profit unconfirmed until Jordan sells to an

Intercompany Transfers of Land –Year of Transfer Example

14

In 2010, one affiliate sells land costing $2,000,000 to the other affiliate for $2,300,000. The buying affiliate holds the land at year-end.

Consolidation eliminating entry, year of transferTo eliminate the unconfirmed intercompany profit and reduce the land to original acquisition cost (same entry, downstream or upstream):

(I) Gain on sale of land 300,000 Land 300,000

Effects of $300,000 Unconfirmed Intercompany Profit in Year of Transfer

Equity in Net

Income20% Noncontrolling

Interest in Net IncomeDownstream transfer Subtract $300,000 No effectUpstream transfer Subtract $240,000 Subtract $60,000

Intercompany Transfers of Land –Subsequent Year Upstream Example

Parrish Shoe is a subsidiary of Jordan Athleticwear. In 2010, Parrish sells land costing $2,000,000 to Jordan for $2,300,000. Jordan still holds the land at the end of 2011.

16

To eliminate the unconfirmed upstream intercompany profit from a previous year and reduce the land to the original acquisition cost:

December 31, 2011 Consolidation eliminating entry:

(I) Retained earnings, beginning-Parrish 300,000 Land 300,000

The gain was originally included in Parrish’s 2010 net income.

Intercompany Transfers of Land –Subsequent Year Downstream Example

Parrish Shoe is a subsidiary of Jordan Athleticwear. In 2010, Jordan sells land costing $2,000,000 to Parrish for $2,300,000. Parrish still holds the land at the end of 2011.

17

To eliminate the unconfirmed downstream intercompany profit from a previous year and reduce the land to the original acquisition cost:

December 31, 2011 Consolidation eliminating entry:

(I) Investment in Parrish 300,000 Land 300,000

The gain was originally subtracted from the investment account.

Intercompany Transfers of Land –Year of Sale to Outside Party Example

Assume the land was sold in 2012 for $3 million. The original cost to the consolidated entity was $2 million, requiring a consolidated gain of $1 million to be reported. The selling entity carries the land at $2,300,000, and reports a gain of $700,000.

19

Upstream - To include in current consolidated net income the previously recorded upstream gain now confirmed through external sale:

(I) Retained earnings, beginning-Parrish 300,000 Gain on sale of land 300,000

Downstream - To include in current consolidated net income the previously recorded downstream gain now confirmed through external sale:

(I) Investment in Parrish 300,000 Gain on sale of land 300,000

Intercompany Transfers of Land –Year of Sale to Outside Party Example

Assume the land was sold in 2012 for $3 million. The original cost to the consolidated entity was $2 million, requiring a consolidated gain of $1 million to be reported. The selling entity carries the land at $2,300,000, and reports a gain of $700,000.

20

Effects of $300,000 Unconfirmed Intercompany Profit in Year of Sale to Outside Party

During 2010, Jordan sells merchandise costing $1 million to Parrish for $1.5 million. Parrish holds all the inventory in its year-end inventory at December 31, 2010.

Assume merchandise priced at $5 million is sold to an affiliate during 2010. The buyer’s ending inventory includes $840,000 purchased from the seller. The seller’s markup is 20% of cost.

25

To eliminate intercompany merchandise sales and purchases.

To eliminate unconfirmed profit from the buyer’s ending inventory: $840,000 – ($840,000 ÷ 1.2) = $140,000

(I-1) Sales 5,000,000 Cost of goods sold 5,000,000

(I-2) Cost of goods sold 140,000 Inventory 140,000

Eliminations are the same whether upstream or downstream.

Assume merchandise priced at $5 million is sold to an affiliate during 2010. The buyer’s ending inventory includes $840,000 purchased from the seller. The seller’s markup is 20% of cost.

26

Effect of $140,000 unconfirmed profit in ending inventory:

Equity in Net

Income20% Noncontrolling

Interest in Net IncomeDownstream transfer Subtract $140,000 No effectUpstream transfer Subtract $112,000 Subtract $28,000

Assume merchandise priced at $5 million is sold to an affiliate during 2010. The buyer’s ending inventory includes $840,000 purchased from the seller. The seller’s markup is 20% of cost.

28

Downstream: Parrish’s beginning inventory includes $840,000 purchased from Jordan. To eliminate intercompany merchandise sales and purchases:

Upstream: Jordan’s beginning inventory includes $840,000 purchased from Parrish. To eliminate unconfirmed profit from beginning inventory:

(I) Investment in Parrish 140,000 Cost of goods sold 140,000

(I) Retained earnings, beginning - Parrish 140,000 Cost of goods sold 140,000

Assume merchandise priced at $5 million is sold to an affiliate during 2010. The buyer’s ending inventory includes $840,000 purchased from the seller. The seller’s markup is 20% of cost.

29

Effect of $140,000 unconfirmed profit in ending inventory:

Equity in Net

Income20% Noncontrolling

Interest in Net IncomeDownstream transfer Add $140,000 No effectUpstream transfer Add $112,000 Add $28,000

Eliminations in Year of Transfer for Depreciable Assets Example

On January 2, 2010, Jordan sells equipment with a 10-year remaining life and an original cost of $5 million to Parrish for $4,500,000. Accumulated depreciation on the transfer date was $2 million.

Balances on 2010 statements: Jordan ParrishBalance Sheet, December 31, 2010 Equipment (remaining on Parrish's books) $ - $4,500,000 Accumulated depreciation - 450,0002010 Income Statement Depreciation expense 450,000 Gain on sale of equipment 1,500,000 -

To eliminate the excess annual depreciation expense recorded by the purchasing affiliate: $1,500,000 ÷ 10 = $150,000

To restate the assets and accumulated depreciation accounts to their original acquisition cost basis. The amount of adjustment is equal to the accumulated depreciation at the date of transfer:

Comprehensive IllustrationAdonis Corp. acquired 90% of the voting stock of Reelok Company, on January 2, 2007 at a cost of $27,830,000. Other data:

38

Reelock’s book value at date of acquisition $2,000,000Estimated fair value of noncontrolling interest 2,170,000Plant and equipment with 10-year remaining life undervalued by 7,000,000Long-term debt with a 4-year remaining term overvalued by 400,000Previously unreported identifiable intangibles: Order backlog with a 2-year life 1,000,000 Favorable leaseholds with a 5-year life 3,000,000

Adonis Corp. acquired 90% of the voting stock of Reelok Company, on January 2, 2007 at a cost of $27,830,000. Total calculated goodwill is $16,600,000. The total fair value of Reelok’s identifiable net assets is $13,400,000.

Adonis Corp.’s intercompany transactions during 2010:

Sale of land in 2008 costing $5 million by Reelock to Adonis for $5.5 million; Sale in 2010 by Adonis to outside firm for $6.5 millionReelock sells merchandise to Adonis at a 20% markup on sales. Adonis’ January 1, 2010 inventory balance includes $400,000 of merchandise purchased from Reelock, and its December 31, 2010 inventory includes $450,000 purchased from Reelock.

Adonis Corp.’s intercompany transactions during 2010:

Adonis sells merchandise to Reelock at a 20% markup on cost. Reelock’s January 1, 2010 inventory balance includes $300,000 of merchandise purchased from Adonis, and its December 31, 2010 inventory includes $240,000 purchased from Adonis. On January 2, 2007, Adonis sold equipment costing $5 million with $3 million of accumulated depreciation and a 10-year remaining life to Reelock for $3.5 million. Reelock holds the equipment at year-end.

Adonis Corp. acquired 90% of the voting stock of Reelok Company, on January 2, 2007 at a cost of $27,830,000. Total calculated goodwill is $16,600,000. Reelock’s reported income for 2010 is $2,000,000.

42

2010 Equity in net income and noncontrolling interest in income:

To recognize the confirmed gain on the upstream land sales.

(I-1) Retained earnings, January 1 500,000 Gain on sale of land 500,000

In 2008, Reelock sold land costing $5 million to Adonis for $5.5 million. In 2010, Adonis sold the land to a real estate investment firm for $6.5 million.

Total 2010 retail sales by Reelock to Adonis were $3 million. Adonis’ January 1, 2010 inventory balance includes $400,000 in merchandise purchased from Reelock. Total 2010 retail sales by Adonis to Reelock were $2 million. Reelock sells to Adonis at a 20% markup on sales.

45

To eliminate intercompany sales and purchases: $3,000,000 + $2,000,000 = $5,000,000

(I-2) Sales revenue 5,000,000 Cost of goods sold 5,000,000

To recognize the confirmed upstream profit in beginning inventory: $400,000 × 20% = $80,000(I-3) Retained Earnings, January 1 80,000

Adjustments for Intercompany TransactionsAdonis sells to Reelock at a 20% markup on cost. Reelock’s January 1, 2010 inventory includes $300,000 in merchandise purchased from Adonis.

46

To recognize the confirmed downstream profit in beginning inventory: $300,000 – ($300,000 ÷ 1.2) = $50,000

(I-4) Investment in Reelock 50,000

Cost of goods sold 50,000

(I-5) Cost of goods sold 130,000 Current assets 130,000

To eliminate the unconfirmed upstream and downstream profit in ending inventory: ($450,000 × 20%) + ($240,000 – ($240,000/1.2)) = $130,000

Reelock’s December 31, 2010 inventory includes $240,000 purchasedfrom Adonis (20% markup on cost). Adonis’ December 31, 2010 inventory includes $450,000 purchased from Reelock (20% markup on sales).

On January 2, 2007, Adonis sold equipment costing $5 million with $3 million accumulated depreciation, and a 10-year remaining life, straight-line, to Reelock for $3.5 million. Reelock still holds the equipment at year-end.

47

(I-6) Investment in Reelock 1,050,000 Accumulated depreciation 450,000

Plant and equipment 1,500,000

To remove the unconfirmed beginning-of-year profit on downstream sale of equipment: Total gain = $3,500,000 – ($5,000,000 - $3,000,000) = $1,500,000 Unconfirmed gain = $1,500,000 – [($1,500,000 ÷ 10) × 3 years] = $1,050,000

On January 2, 2007, Adonis sold equipment costing $5 million with $3 million accumulated depreciation, and a 10-year remaining life, straight-line, to Reelock for $3.5 million. Reelock still holds the equipment at year-end.

In 2010, Adonis charged Reelock $500,000 for marketing services costing $400,000. At year-end, Reelock owes Adonis $25,000 related to marketing services. At year-end, Adonis owes Reelock $100,000 related to merchandise sales, and Reelock owes Adonis $85,000 related to merchandise sales.

49

To eliminate the intercompany sale of marketing services:

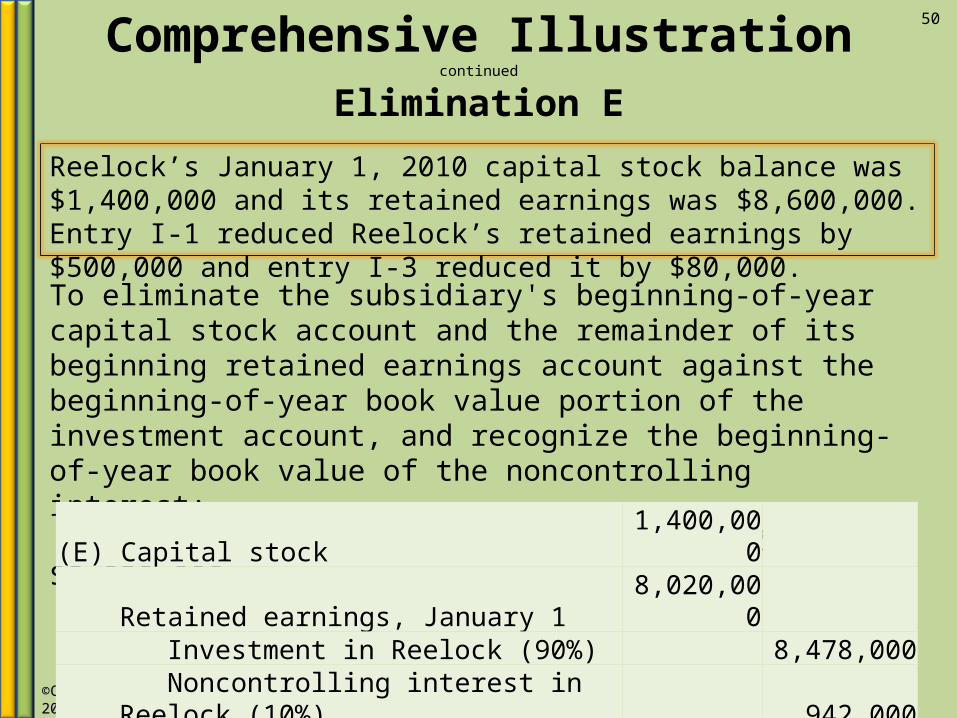

Reelock’s January 1, 2010 capital stock balance was $1,400,000 and its retained earnings was $8,600,000. Entry I-1 reduced Reelock’s retained earnings by $500,000 and entry I-3 reduced it by $80,000.

50

To eliminate the subsidiary's beginning-of-year capital stock account and the remainder of its beginning retained earnings account against the beginning-of-year book value portion of the investment account, and recognize the beginning-of-year book value of the noncontrolling interest: $8,600,000 – $500,000 – $80,000 = $8,020,000

(E) Capital stock 1,400,000 Retained earnings, January 1 8,020,000

Investment in Reelock (90%) 8,478,000 Noncontrolling interest in Reelock (10%) 942,000

Reelock’s assets and liabilities were fairly reported except for plant and equipment undervalued by $7 million; long-term debt overvalued by $400,000; and previously unreported identifiable intangibles: order backlog for $1 million and favorable leaseholds for $3 million. Accumulated goodwill impairment for 2007-2009 was $1 million.

51

To revalue Reelock's net assets as of the beginning of the year and allocate the revaluations to the controlling interest: ($7,000,000 + $1,200,000 + $100,000 – $2,100,000) = $6,200,000 (90% × $6,200,000) + (95% × $15,600,000) = $20,400,000 (10% × $6,200,000) + (5% × $15,600,000) = $1,400,000

Reelock’s assets and liabilities were fairly reported except for plant and equipment undervalued by $7 million; long-term debt overvalued by $400,000; and previously unreported identifiable intangibles: order backlog for $1 million and favorable leaseholds for $3 million. Goodwill impairment is $200,000 for 2010.

52

To write off the revaluations for the current year: $7,000,000 ÷ 10 = $700,000 $3,000,000 ÷ 5 = $600,000 $400,000 ÷ 4 = $100,000