21

Can Brazil Qualify for the Investment Grade League? Shelly Shetty Senior Director

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | lillian-porter |

| View: | 213 times |

| Download: | 0 times |

Can Brazil Qualify for the Investment Grade League?

Shelly Shetty Senior Director

Agenda

Brazil’s Macro Picture

Brazil’s Credit Dynamics

Brazil versus India: Comparing Two of the BRICs

Agenda

Brazil’s Macro Picture

Brazil’s Credit Dynamics

Brazil versus India: Comparing Two of the BRICs

Brazil in a Snapshot

2003 2004 2005 2006 2007 2008 2009

Real GDP growth (%) 1.1 5.7 2.9 3.7 5.4 4.3 4.1

Consumer prices (ann. avg. % change)

14.3 6.1 5.7 2.7 3.7 4.0 4.0

CXR (% change) 18.7 28.7 22.3 18.8 19.4 8.4 8.5

CAB (% of GDP) 0.7 1.7 1.6 1.2 0.3 -0.7 -1.2

Govt. balance (% of GDP) -5.8 -3.4 -3.6 -3.5 -2.4 -2.3 -2.2

Source: Fitch Ratings.

Brazil’s likely to be more resilient to external turmoil

> Ample international liquidity

> Lower external financing needs

> Liability management has reduced FX exposure of public debt

> Central bank has the choice to let FX act as a shock absorber

-20

-10

0

10

20

30

40

50

60

70

80

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

f

2008

f

2009

f

Current Account Debt repayments Financing need

External Financing Needs (USD Bn)

Source: Fitch Ratings.

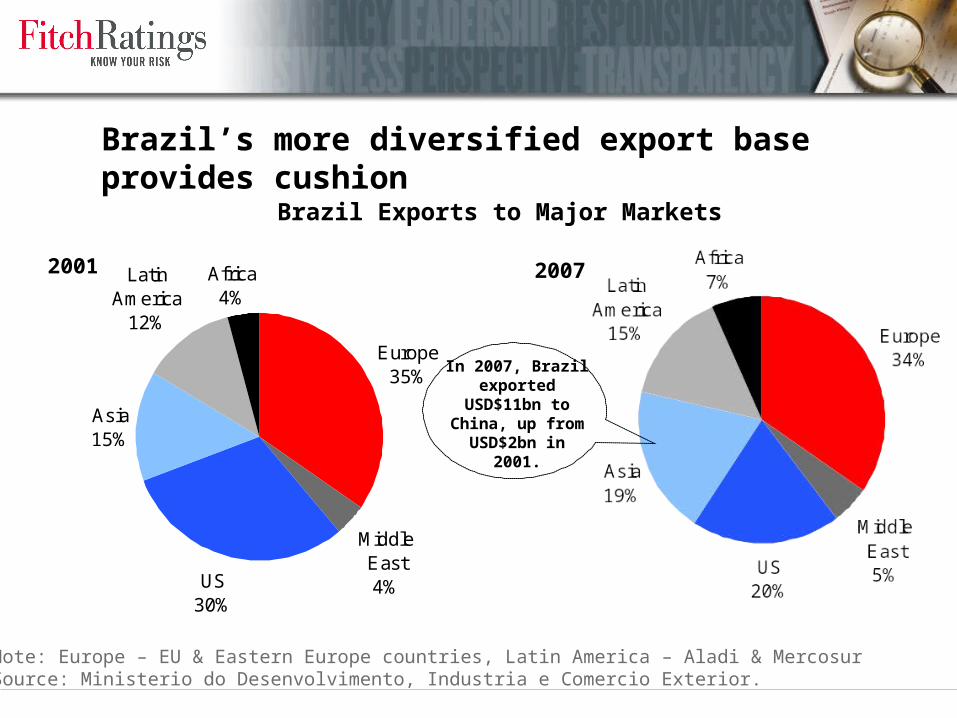

Brazil Exports to Major Markets

Note: Europe – EU & Eastern Europe countries, Latin America – Aladi & MercosurSource: Ministerio do Desenvolvimento, Industria e Comercio Exterior.

20072001

In 2007, Brazil exported

USD$11bn to China, up from

USD$2bn in 2001.

Europe35%

Middle East4%US

30%

Asia15%

Latin America

12%

Africa4%

Brazil’s more diversified export base provides cushion

Agenda

Brazil’s Macro Picture

Brazil’s Credit Dynamics

Brazil versus India: Comparing Two of the BRICs

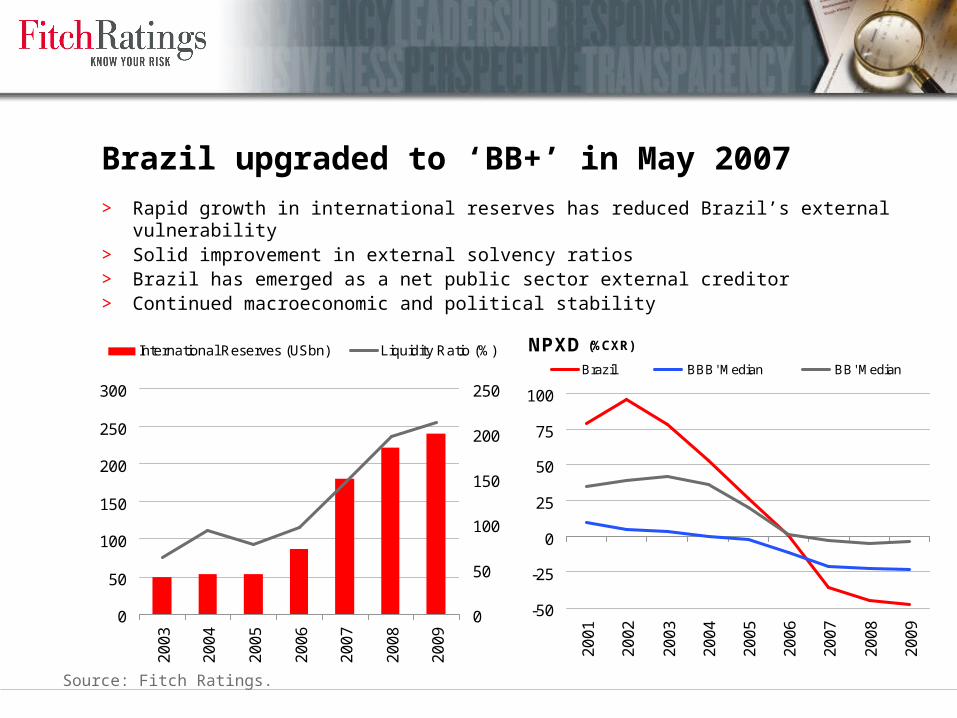

Brazil upgraded to ‘BB+’ in May 2007

0

50

100

150

200

250

300

20

03

20

04

20

05

20

06

20

07

20

08

20

09

0

50

100

150

200

250

International Reserves (USbn) Liquidity Ratio (%)

(US bn) (%)

NPXD (%CXR)

-50

-25

0

25

50

75

100

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

Brazil 'BBB' Median 'BB' Median

> Rapid growth in international reserves has reduced Brazil’s external vulnerability> Solid improvement in external solvency ratios> Brazil has emerged as a net public sector external creditor> Continued macroeconomic and political stability

Source: Fitch Ratings.

What is slowing Brazil’s ascent to Investment Grade?

> A heavy public debt burden

> Unfavorable domestic debt profile

> Weaker growth prospects compared with IG Sovereigns

> Public debt dynamics not improving fast enough

Brazil Key Indicators 2008BBB

Median

Real GDP growth (%, 5 yr avg) 4.4 5.3

GDP per capita (USD) 8,031 7,286

Consumer prices (% change) 4.0 5.7

CAB (% of GDP) -0.7 -1.5

Govt. balance (% of GDP) -2.7 -1.7

Govt. debt (% of GDP) 65.2 24.9

Govt. debt (% of revenue) 171.5 102.5

Net external debt (% of CXR) -13.7 9.6

Net public external debt (% of CXR) -45.4 -25.6

External debt service (% of CXR) 18.2 10.1

Liquidity ratio (%) 196.2 161.2

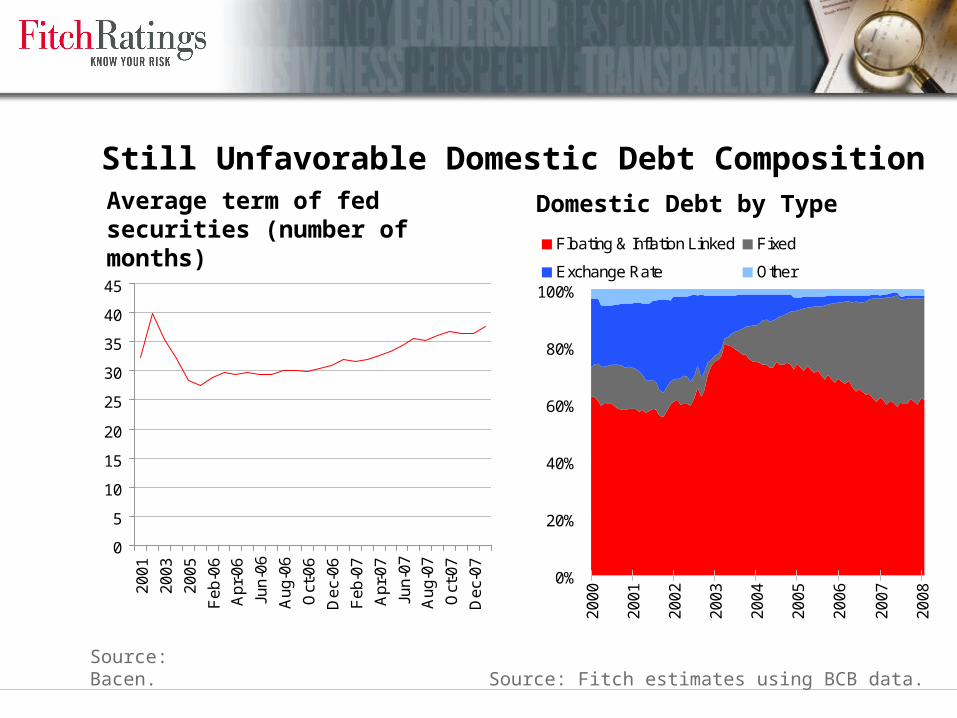

Still Unfavorable Domestic Debt Composition

0

5

10

15

20

25

30

35

40

45

20

01

20

03

20

05

Fe

b-0

6

Ap

r-0

6

Jun

-06

Au

g-0

6

Oct

-06

De

c-0

6

Fe

b-0

7

Ap

r-0

7

Jun

-07

Au

g-0

7

Oct

-07

De

c-0

7

Average term of fed securities (number of months)

Source: Bacen.

0%

20%

40%

60%

80%

100%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Floating & Inflation Linked Fixed

Exchange Rate Other

Domestic Debt by Type

Source: Fitch estimates using BCB data.

> Brazil’s resilience in the unfavorable external environment

> Central bank’s monetary and currency management

> Signs of sustained investment and GDP growth

> Improvements in external solvency and liquidity ratios

> Fiscal performance

> Reform progress

Real Interest Rate – Selic*2003-2007

0

2

4

6

8

10

12

14

16

Jan

-03

Ap

r-0

3Ju

l-0

3O

ct-0

3Ja

n-0

4A

pr-

04

Jul-

04

Oct

-04

Jan

-05

Ap

r-0

5Ju

l-0

5O

ct-0

5Ja

n-0

6A

pr-

06

Jul-

06

Oct

-06

Jan

-07

Ap

r-0

7Ju

l-0

7O

ct-0

7Ja

n-0

8

*Note: Uses average nominal Selic and prospective inflation (IPCA index) for the next 12 months. Source: Bacen.

What will Fitch Ratings monitor in the coming months?

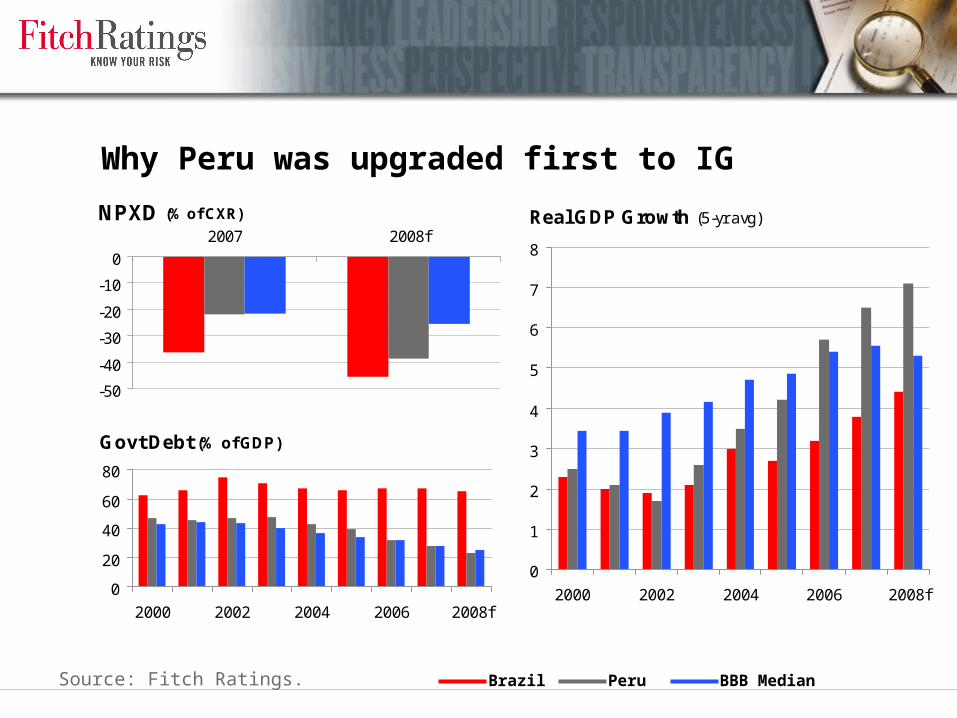

Why Peru was upgraded first to IG

NPXD (% of CXR)

-50

-40

-30

-20

-10

0

2007 2008f

Govt Debt (% of GDP)

0

20

40

60

80

2000 2002 2004 2006 2008f

Real GDP Growth (5-yr avg)

0

1

2

3

4

5

6

7

8

2000 2002 2004 2006 2008f

Brazil Peru BBB MedianSource: Fitch Ratings.

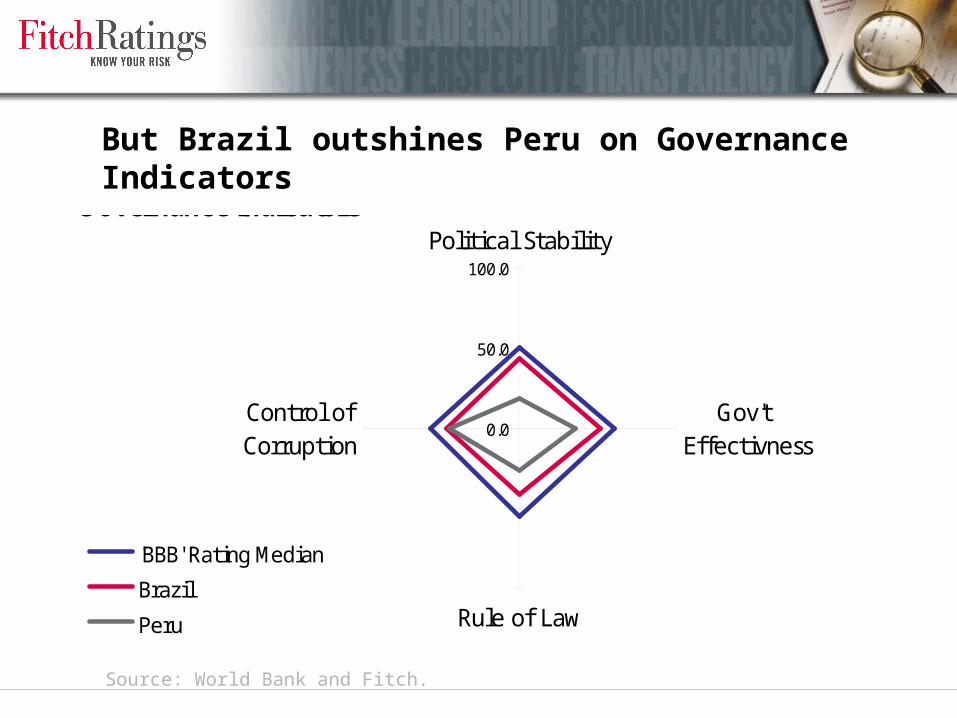

But Brazil outshines Peru on Governance Indicators

Source: World Bank and Fitch.

Governance Indicators

0.0

50.0

100.0

Political Stability

Gov't Effectivness

Rule of Law

Control ofCorruption

'BBB' Rating Median

Brazil

Peru

Agenda

Brazil’s Macro Picture

Brazil’s Credit Dynamics

Brazil versus India: Comparing Two of the BRICs

Brazil and India: Similar in many respects

> Large and closed economies

– Brazil GDP (2007e): USD1.2 trn

– India GDP: (2007e): USD 1.1 trn

> Weak Public Finances

> Deep and sophisticated domestic bond markets

> Robust external liquidity and solvency ratios

> Suffer from cumbersome coalition politics

IndiaPrimary

18%

Industry28%

Services54%

but India was assigned IG in August 2006.

BrazilPrimary

6%

Industry30%

Services64%

GDP Growth by sectors

Source: National Authorities

India’s growth story more sustainable

0

5

10

15

20

25

30

35

40

2000

2001

2002

2003

2004

2005

2006

2007

2008

f

2009

f

India Saving Brazil SavingIndia Investment Brazil Investment

> Higher saving and investment levels

> India’s manufacturing sector restructured since mid-90s

> India has shifted towards knowledge economy

> India is less commodity dependent

but Brazil’s Per Capita Income is nearly 7 times that of India.

Saving and Investment rates

Source: Fitch Ratings.

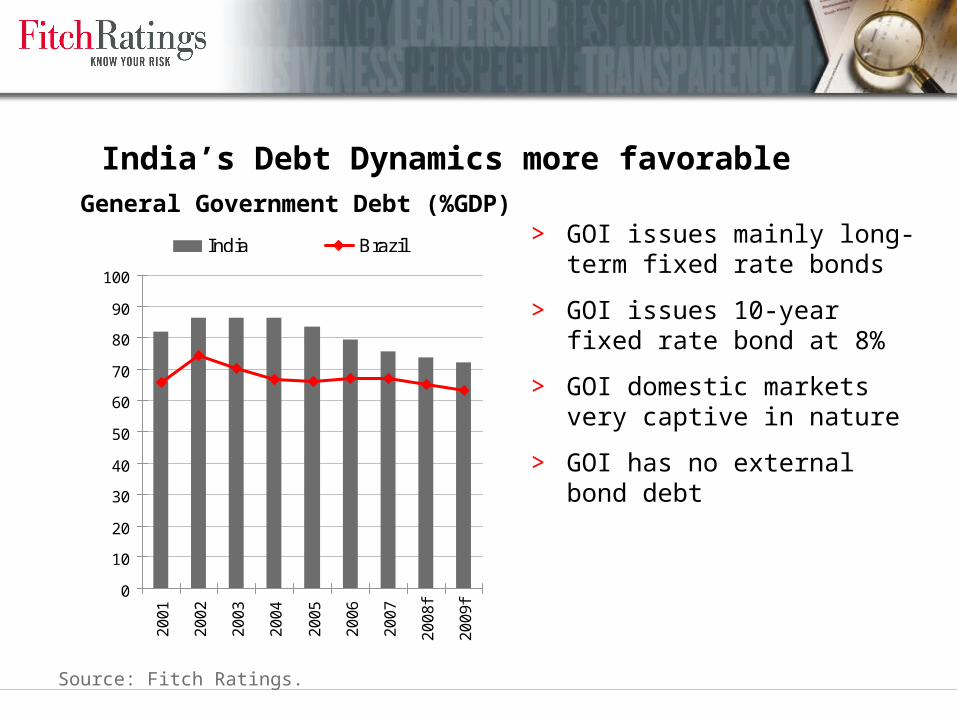

India’s Debt Dynamics more favorable

> GOI issues mainly long-term fixed rate bonds

> GOI issues 10-year fixed rate bond at 8%

> GOI domestic markets very captive in nature

> GOI has no external bond debt

0

10

20

30

40

50

60

70

80

90

100

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

f

20

09

f

India Brazil

General Government Debt (%GDP)

Source: Fitch Ratings.

India’s fiscal problems may have easier solutions

0

5

10

15

20

25

30

35

40

2000 2001 2002 2003 2004 2005 2006 2007 2008f 2009f

Brazil India

Source: Fitch Ratings.

Revenues (% GDP)

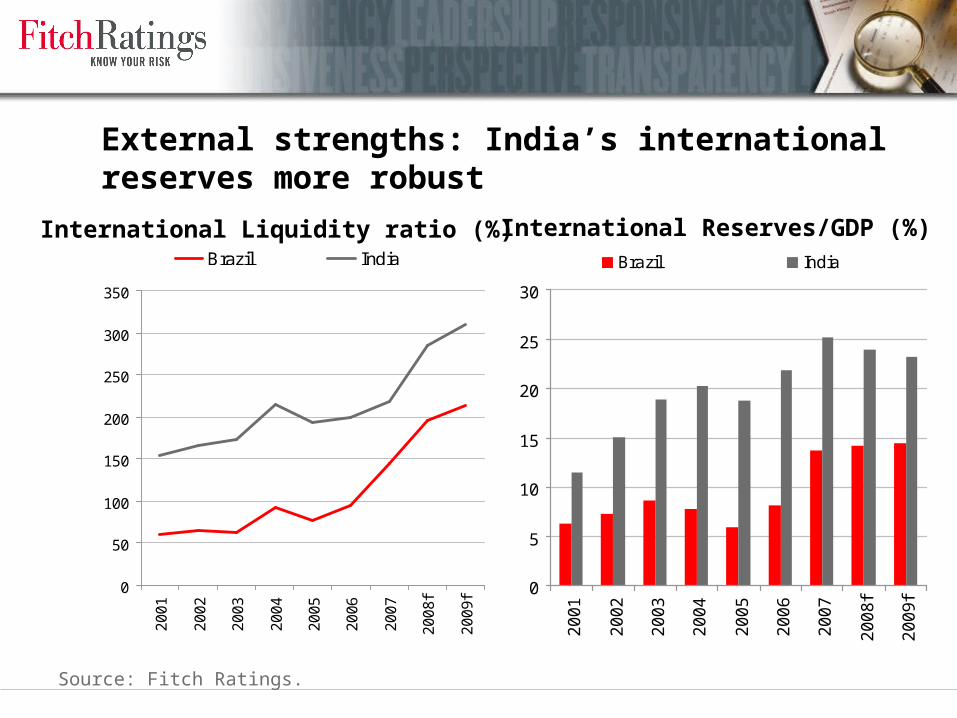

External strengths: India’s international reserves more robust

0

5

10

15

20

25

30

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

f

20

09

f

Brazil India

0

50

100

150

200

250

300

350

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

f

20

09

f

Brazil India

International Liquidity ratio (%) International Reserves/GDP (%)

Source: Fitch Ratings.

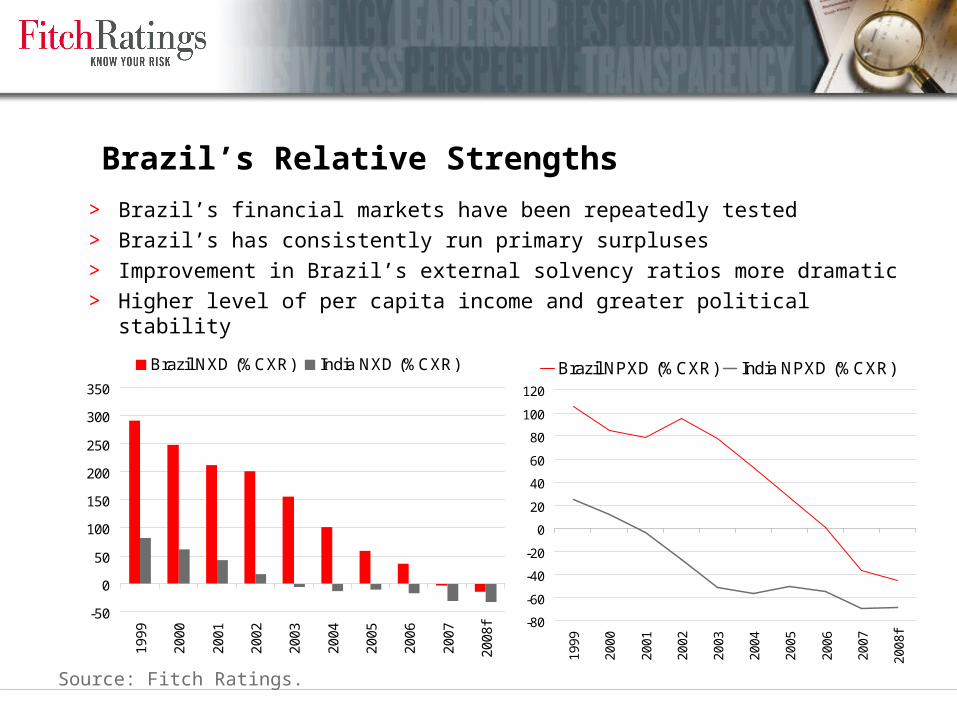

Brazil’s Relative Strengths

> Brazil’s financial markets have been repeatedly tested> Brazil’s has consistently run primary surpluses> Improvement in Brazil’s external solvency ratios more dramatic> Higher level of per capita income and greater political stability

-50

0

50

100

150

200

250

300

350

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

f

Brazil NXD (%CXR) India NXD (%CXR)

-80

-60

-40

-20

0

20

40

60

80

100

120

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

f

Brazil NPXD (%CXR) India NPXD (%CXR)

Source: Fitch Ratings.

Fitch Ratingswww.fitchratings.com

New YorkOne State Street PlazaNew York, NY 10004+1 212 908 0500+1 800 75 FITCH

Fitch Group Fitch Ratings Fitch Solutions Algorithmics

London101 Finsbury PavementLondonEC2A 1RS44 20 7417 4222

Singapore6 Temasek Blvd.#35-03/04/05Suntec Tower FourSingapore 038986+65 6336 6801