16

Can Coastal Europe Insure Against Climate Change: A Review of Experiences on Floods and Soil Erosion Phoebe Koundouri, Bénédicte Rulleau, and Mavra Stithou 1

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | jocelyn-peters |

| View: | 212 times |

| Download: | 0 times |

Can Coastal Europe Insure Against Climate Change: A Review of

Experiences on Floods and Soil Erosion

Phoebe Koundouri, Bénédicte Rulleau, and Mavra Stithou

1

Characteristics of Natural Disaster Risks• Climate change is expected to increase the frequency and severity of

flooding in certain regions (IPCC, 2007). The damage from natural disasters in Europe has rapidly increased over the past decades, mainly because of the growth of capital accumulated in flood-prone areas

Socio-economic change and climate change “Risk”

• Low probability • Not completely unpredictable• Highly publicized, impact on individuals, firms and governments• Involve unpredictable risk components but also individual control

2

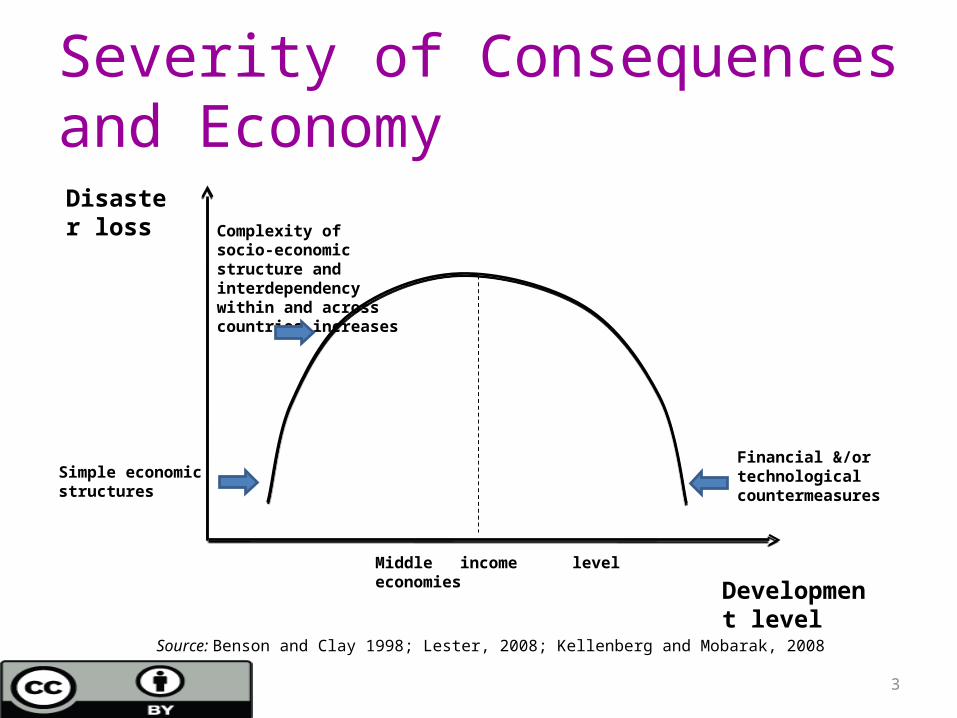

Severity of Consequences and Economy

Financial &/or technological countermeasures

Disaster loss

Development level

Middle income level economies

Simple economic structures

Complexity of socio-economic structure and interdependency within and across countries increases

Source: Benson and Clay 1998; Lester, 2008; Kellenberg and Mobarak, 2008

3

Hazard Risk Management

4

Determinants of Perception• How well people understand the process ,

the degree of catastrophe • How equitably the danger is distributed

over time and space• How well individuals can control their

exposure• Whether exposure is familiar

“The feelings, emotions and values that people gain through experience through living in their social networks, have a major effect on their reactions towards risk ” (Morrow 2009)

• Another determinant of risk attitude is the general disposition towards risk

• Subjective risk perceptions very much depend on how the risky situation is framed or presented to an individual decision-maker (Kahneman and Tversky, 1979)

• Individual underestimate the probability of a future disaster if they have not personally experienced the event

• Difficulties interpreting correctly low probability

• Even if there is knowledge about the probability of disaster that does not imply awareness about consequences or action

5

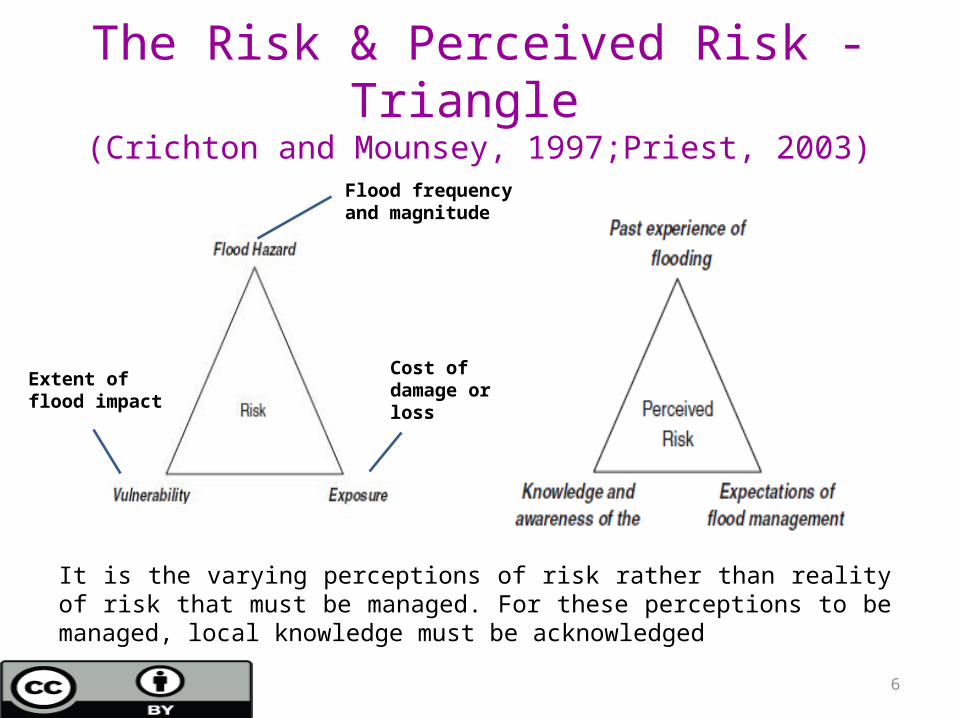

The Risk & Perceived Risk - Triangle (Crichton and Mounsey, 1997;Priest, 2003)

Flood frequency and magnitude

Extent of flood impact

Cost of damage or loss

It is the varying perceptions of risk rather than reality of risk that must be managed. For these perceptions to be managed, local knowledge must be acknowledged

6

Response of Individuals

• Move out from areas that are at high risk and reallocate in a safer area• Self – protect by building structures less vulnerable to damage• Insure by paying a premium in an insurance company

• Institutions can influence the decision to undertake mitigation (Botzen et al. 2009):

Existing arrangements for compensating flood damage (the role of government), risk awareness and perceptions, and geographical characteristics were more important determinants than the socioeconomic characteristics. The main incentive for homeowners to choose for investing in water barriers was likely to be the premium discount on the flood insurance policy provided to them

8

Response of Government• Ex ante public program e.g well-enforced regulations, mandatory private

disaster insurance, building codes in disaster prone areas, incentives through grants, loans and taxes

• Ex post public program eg. rehabilitation and recovery, reconstruction

• Reinsurance, public-private or national-international partnerships, catastrophe bonds

• When it is not possible to find international reinsurance, governments tend to self-insure through budgetary allocation

• An interrelationship exists between individual behaviour and structure of government policies

9

Response of Insurance Schemes• Increasing premiums or pulling out of risky markets common strategy

• Link premium to mitigation measures

• Public-private partnerships

• Reinsurance markets

• Alternative Risk Transfers (ARTs) in global markets, for example catastrophe bonds

• Invest in Research and Development to explore significant changes of known risks in their structure or occurrence probability and to identify new risks at an early stage

10

Flood Risk Management Measures (Adapted from Parker 2007)

Probability of flooding

11

Types of Flood Insurance

Different countries have different home insurance markets where insurance can come bundled with all cover (including flooding), or unbundled (where each component is sold separately) whilst the market may be entirely private, or a state monopoly (Dawson et al. 2011).

Netherlands?

12

The Role of Insurance• Although insurance schemes

cannot impact on hazard (frequency and magnitude of flood), they impact on vulnerability (extent of impact on property) and exposure (cost of damage).

• Vulnerability: By using pricing or restrictions on available cover (i.e. keeping valuable items above flood level, don't enter an area)

• Exposure: modifying the insurance excesses/deductable and create incentives to relocate away from flood hazard zones

13

Conclusions• A catastrophe recovery, cost limitation and management tool (Clark 1998)

by risk sharing, influencing decisions to locate in the floodplain and by encouraging the use of measures to minimise damage (Doornkamp, 1995; Arnell, 2000).

• A wider portfolio of measures to adapt to climate change is needed

• A combination of measures that both limit damage (economic use of a flood zone by creating incentives) and reduce the probability of flooding (engineered coastal defense measures) is likely to be the most effective way of preventing the occurrence of extremely large flood damages (Aerts et al. 2008)

• Increase individual coastal flood risk awareness by risk communication, financial mechanisms and technical engineering solutions (Filatova et al. 2011)

16

THESEUS: “Innovative Technologies for Safer European Coasts in a Changing Climate”• Qualitative questionnaire survey: explore initial

behavioural patterns and investigate the degree of awareness and knowledge on strategies of hedging natural hazards

• Respondents: residents, business owners, environmental NGOs, insurance companies and local authorities

• Case studies: Spain, UK, Italy, France, Poland and Bulgaria

17

THESEUS: “Innovative Technologies for Safer European Coasts in a Changing Climate”• Santander Choice Experiment (WTP survey)

• Elicit public preferences for climate change mitigation measures

Reduction of beach size/erosion BiodiversityHealth risk

18

Thank you...

19