17

Canada’s Advantages Mitigate Household Debt Risks Derek Holt Vice-President, Scotia Capital Economics Presented to the Durham Economic Prosperity Conference, November 5 th , 2010

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | kenzie-veil |

| View: | 216 times |

| Download: | 2 times |

Canada’s Advantages Mitigate Household Debt Risks

Derek HoltVice-President,

Scotia Capital Economics

Presented to the Durham Economic Prosperity Conference, November 5th, 2010

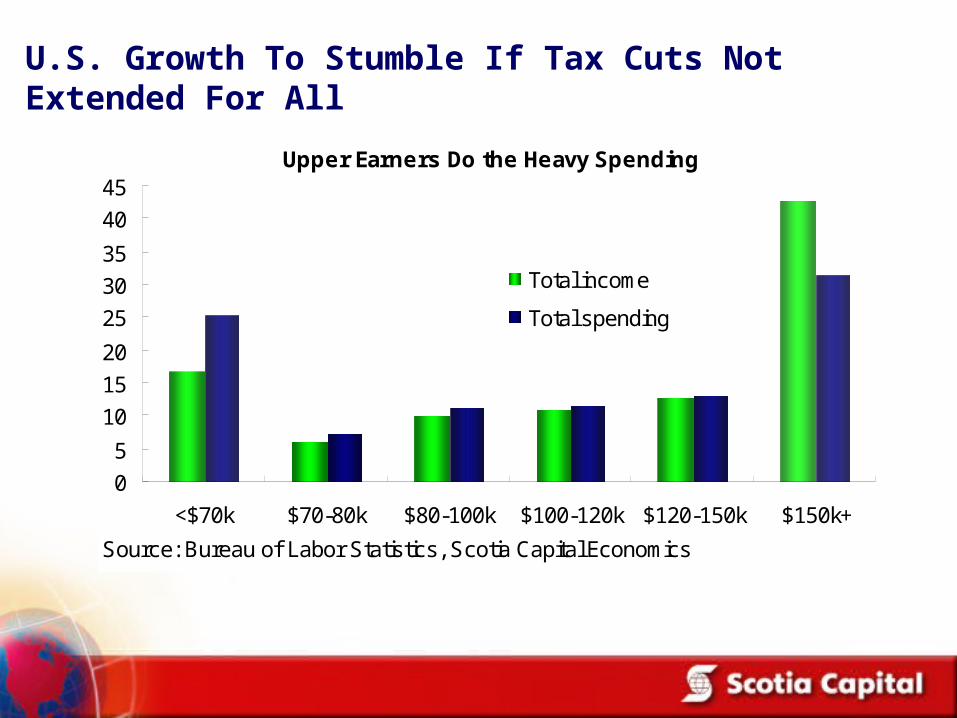

U.S. Growth To Stumble If Tax Cuts Not Extended For All

Upper Earners Do the Heavy Spending

0

5

10

15

20

25

30

35

40

45

<$70k $70-80k $80-100k $100-120k $120-150k $150k+

Source: Bureau of Labor Statistics, Scotia Capital Economics

Total income

Total spending

% share of grow th in income and consumption, 2003-08

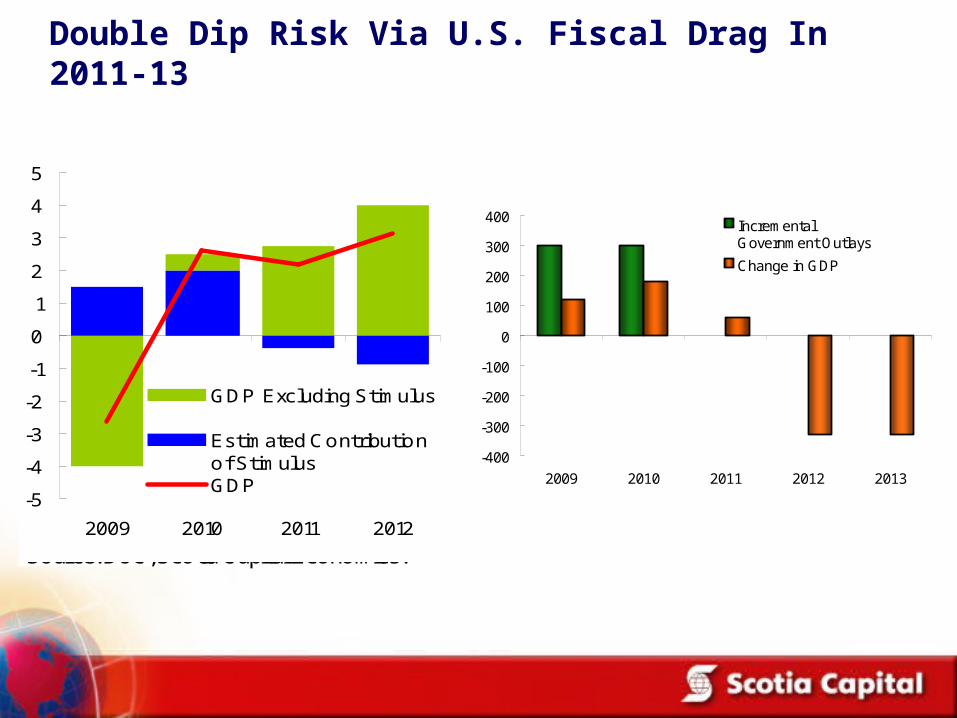

Double Dip Risk Via U.S. Fiscal Drag In 2011-13

-400

-300

-200

-100

0

100

200

300

400

2009 2010 2011 2012 2013

IncrementalGovernment Outlays

Change in GDP

US$ bns

Barro's "five-year plan" Estimates from 2009-2013

Source: Wall Street Journal; Scotia Capital Economics-5

-4

-3

-2

-1

0

1

2

3

4

5

2009 2010 2011 2012

GDP Excluding Stimulus

Estimated Contributionof StimulusGDP

The BoC 's Assumptions on U.S. Growth

Source: BoC, Scotia Capital Economics.

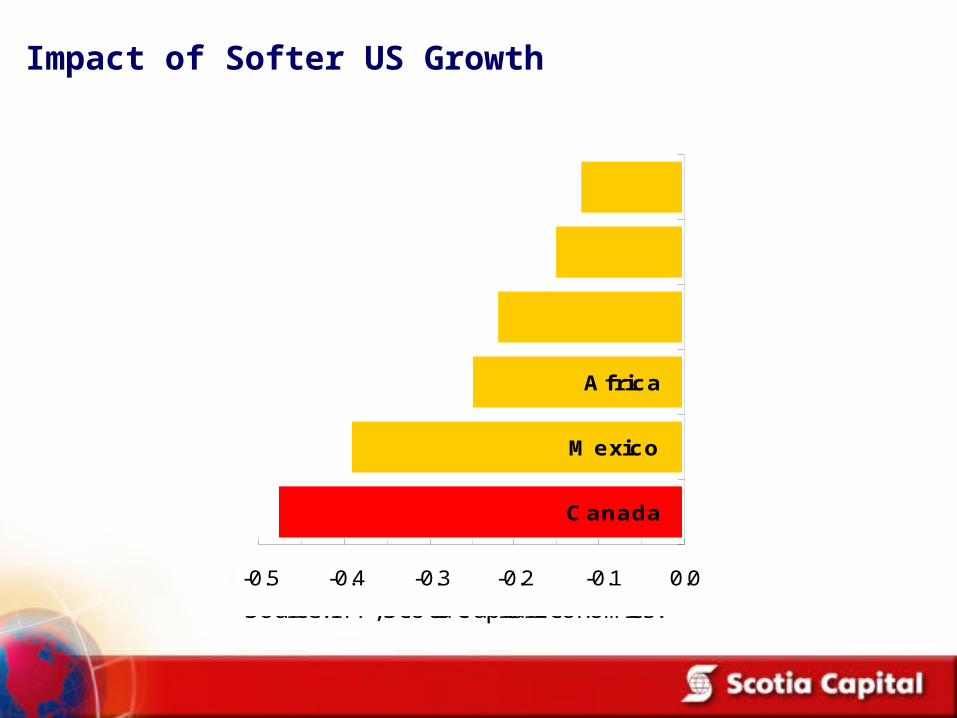

Impact of Softer US Growth

-0.5 -0.4 -0.3 -0.2 -0.1 0.0

Canada

Mexico

Africa

Growth Decline Implications

Source: IMF, Scotia Capital Economics.

impact of a 1% decline in growth rate of the United States

Other Advanced Economies

Latin America

Emerging Asia

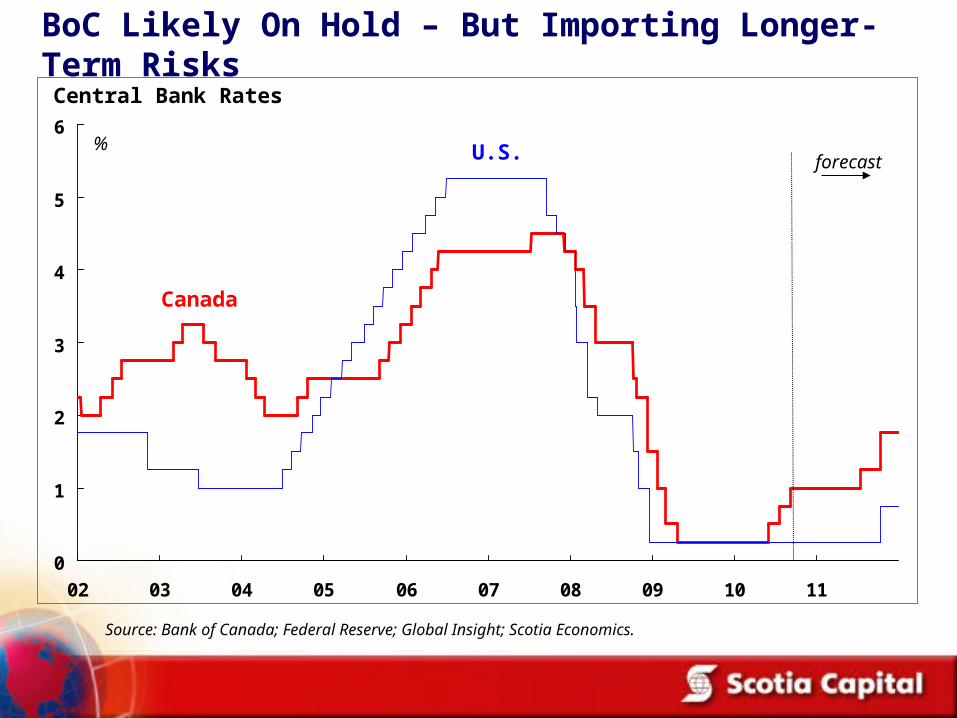

BoC Likely On Hold – But Importing Longer-Term Risks

0

1

2

3

4

5

6

02 03 04 05 06 07 08 09 10 11

Canada

U.S.%forecast

Source: Bank of Canada; Federal Reserve; Global Insight; Scotia Economics.

Central Bank Rates

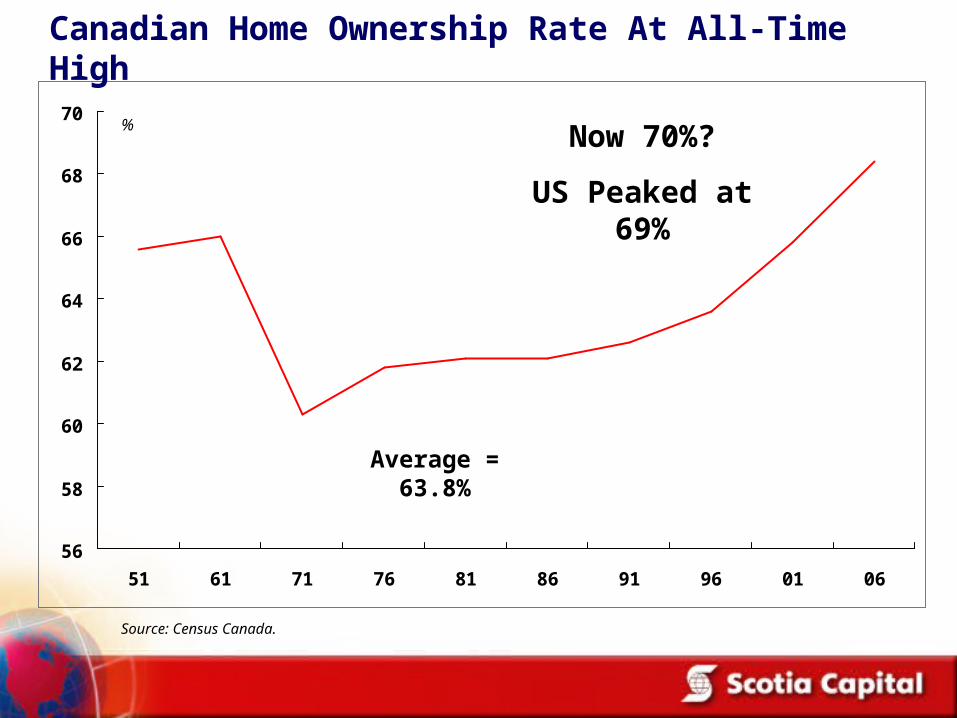

56

58

60

62

64

66

68

70

51 61 71 76 81 86 91 96 01 06

%

Canadian Home Ownership Rate At All-Time High

Source: Census Canada.

Average = 63.8%

Now 70%?

US Peaked at 69%

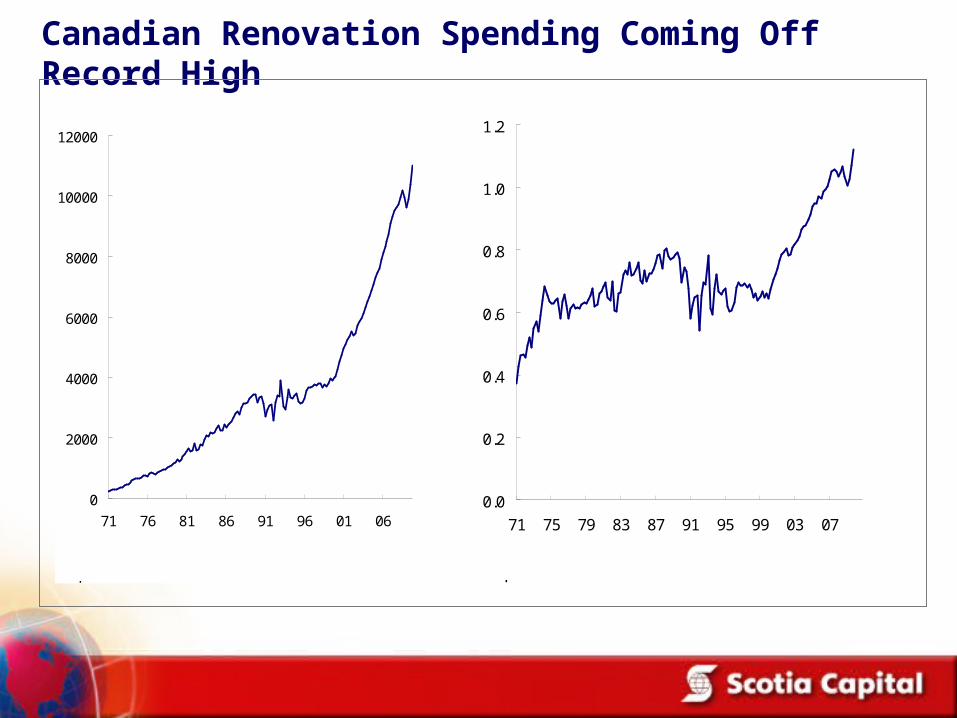

Canadian Renovation Spending Coming Off Record High

0

2000

4000

6000

8000

10000

12000

71 76 81 86 91 96 01 06

Canadian Renovation Spending

millions, saar

Source: Statistics Canada, Global Insight, Scotia Capital Economics

0.0

0.2

0.4

0.6

0.8

1.0

1.2

71 75 79 83 87 91 95 99 03 07

Renovation Spending

% PDI, sa

Source: Statistics Canada, Global Insight, Scotia Capital Economics

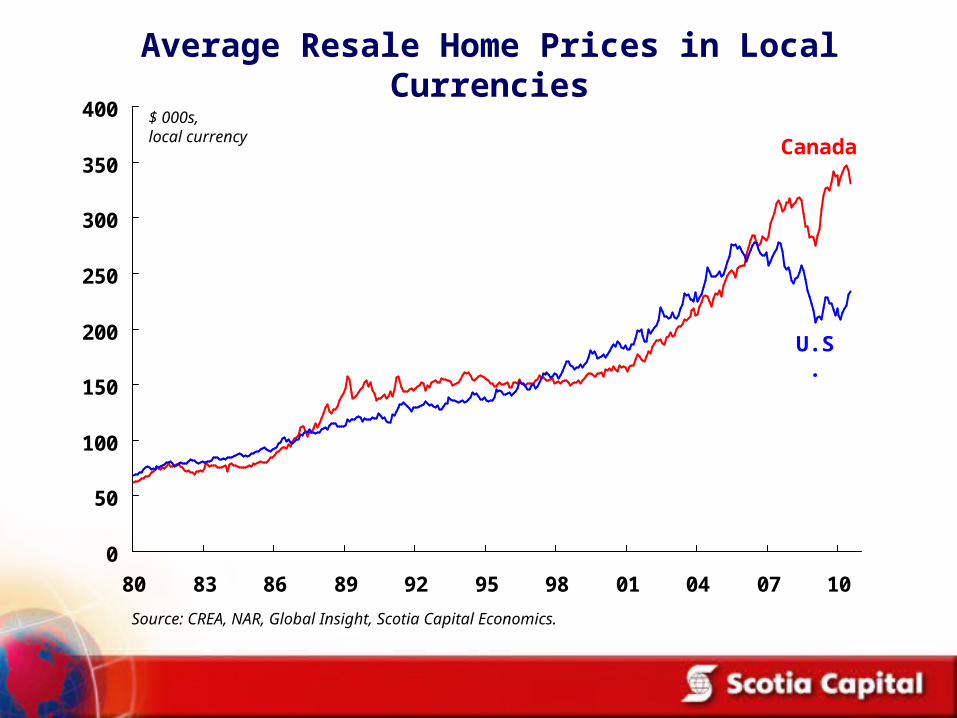

0

50

100

150

200

250

300

350

400

80 83 86 89 92 95 98 01 04 07 10

Canada

U.S.

Source: CREA, NAR, Global Insight, Scotia Capital Economics.

$ 000s,local currency

Average Resale Home Prices in Local Currencies

Not Just One or Two Cities Driving House Price Gains

020406080

100120140160180

MB SK Nfld AB BC QC NS ON NB PEI

Source: CREA, MLS, Scotia Capital Economics

Provincial Resale Prices% chg from Dec. 1999 - January 2010

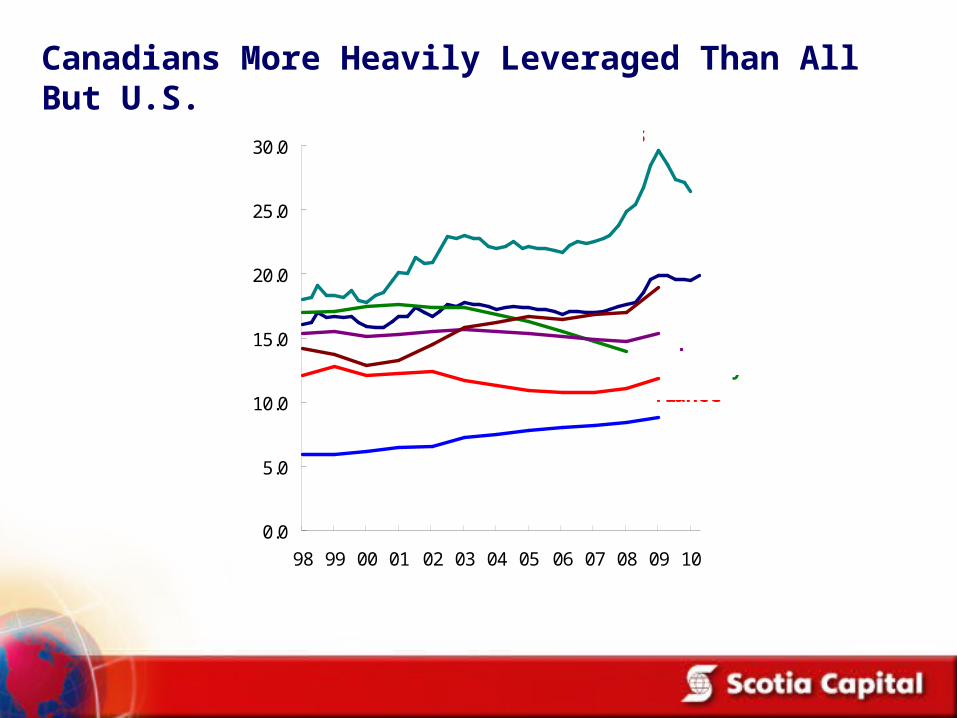

Canadians More Heavily Leveraged Than All But U.S.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

98 99 00 01 02 03 04 05 06 07 08 09 10

Canada

US

UK

Japan

FranceGermany

Italy

%

Household Liabilities as Share of Assets

Source: OECD, Federal Reserve, Statistics Canada, Scotia Capital Economics

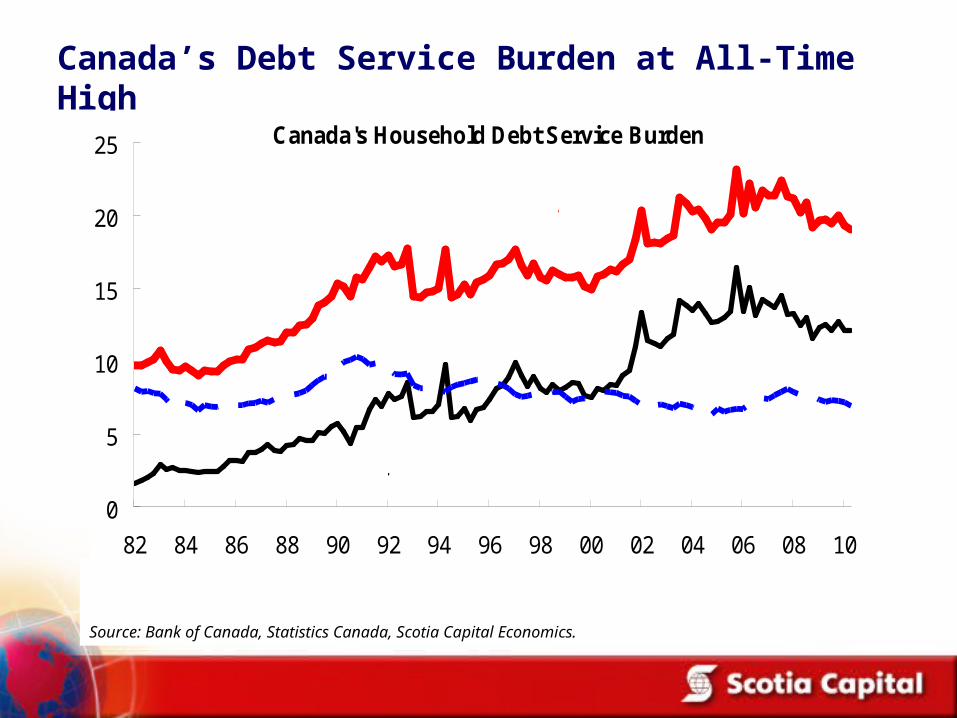

Canada’s Debt Service Burden at All-Time High

Canada's Household Debt Service Burden

0

5

10

15

20

25

82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

interest payments on all debt + mortgage principal payments (% share of after-tax PDI )

Source: Bank of Canada, Statistics Canada, Scotia Capital Economics

Principal

Interest

Total

Source: Bank of Canada, Statistics Canada, Scotia Capital Economics.

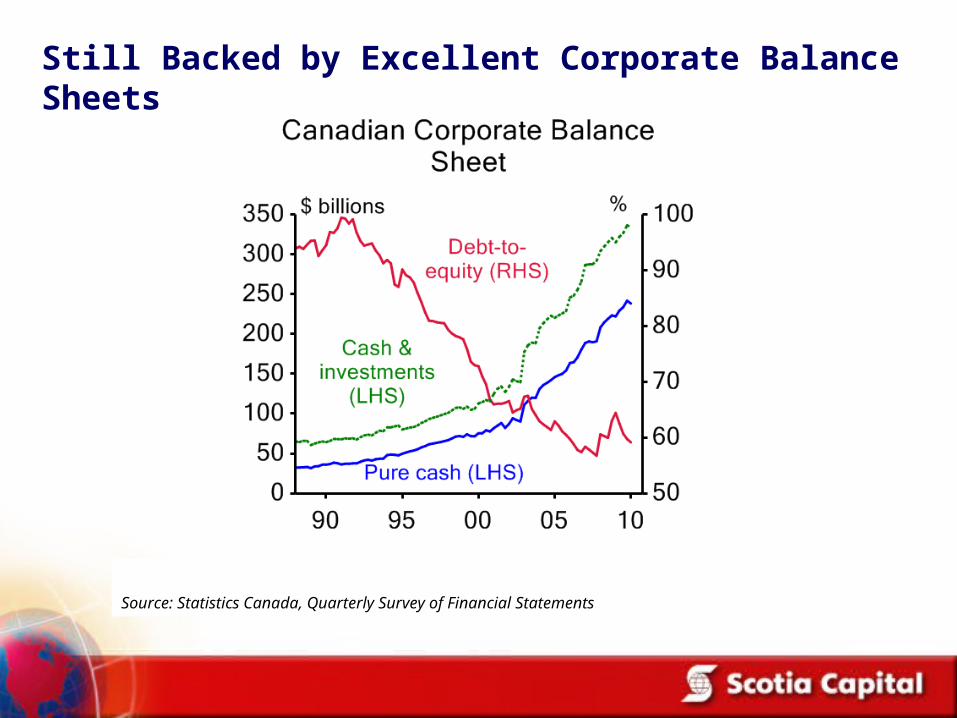

Still Backed by Excellent Corporate Balance Sheets

Source: Statistics Canada, Quarterly Survey of Financial Statements

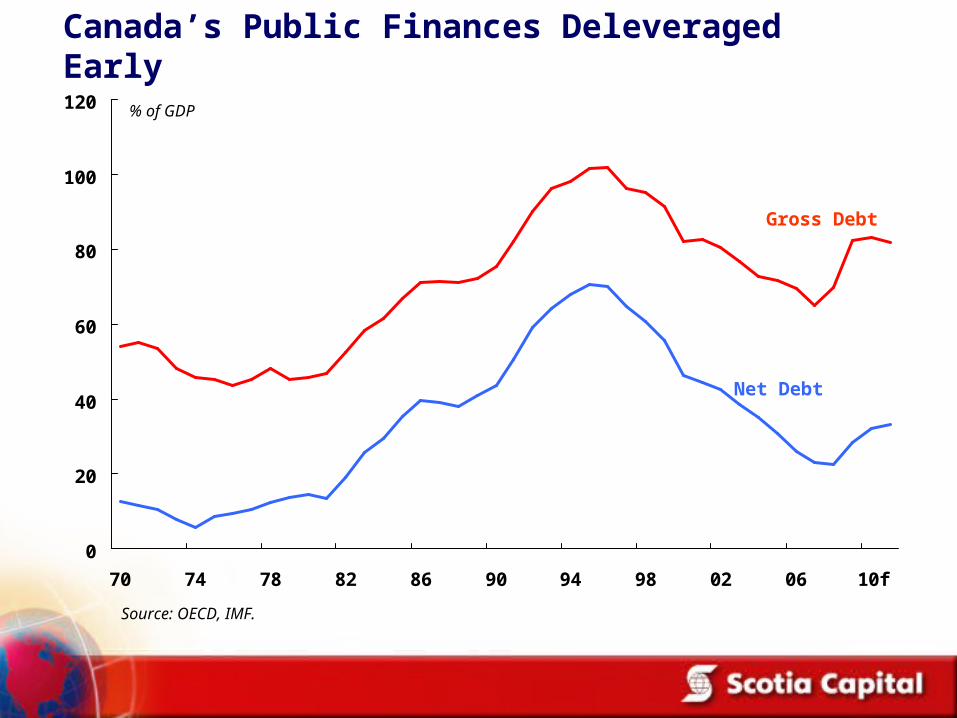

Canada’s Public Finances Deleveraged Early

0

20

40

60

80

100

120

70 74 78 82 86 90 94 98 02 06 10f

% of GDP

Gross Debt

Net Debt

Source: OECD, IMF.

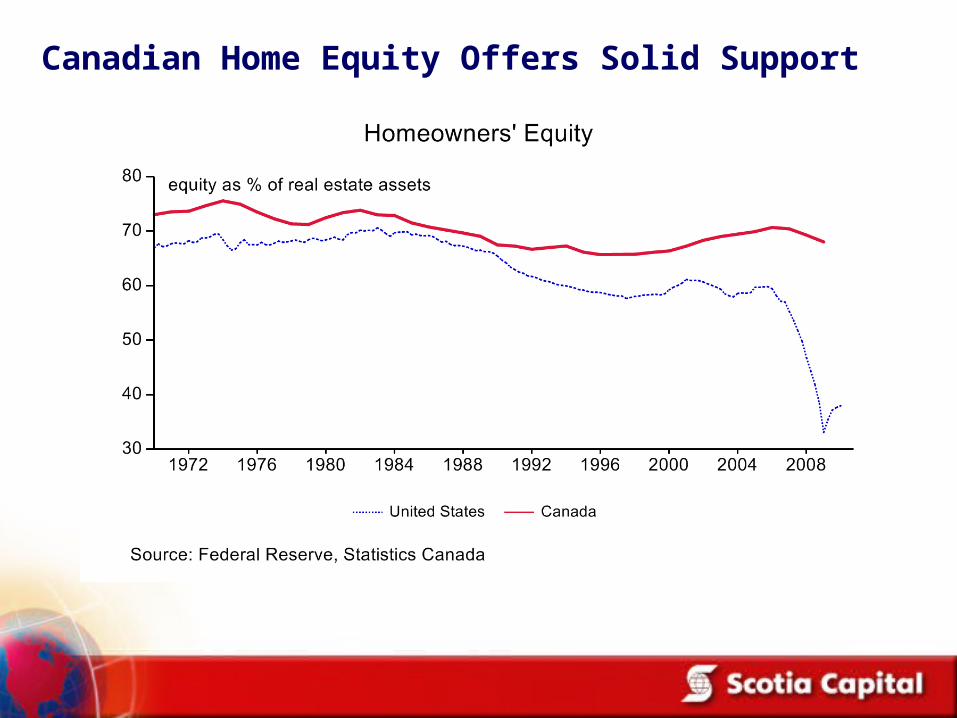

Canadian Home Equity Offers Solid Support

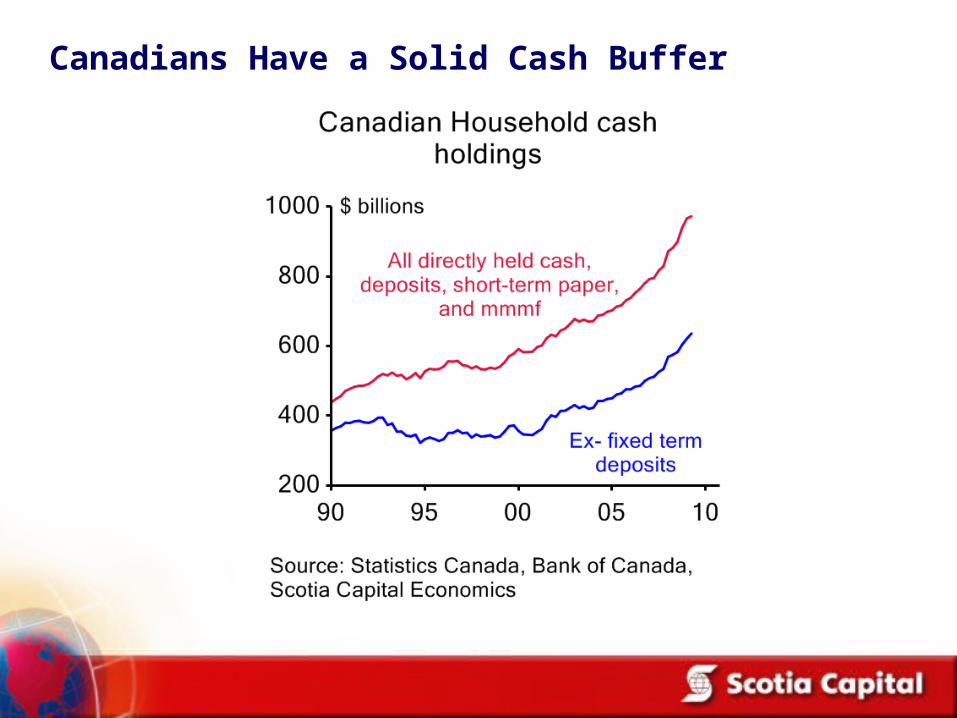

Canadians Have a Solid Cash Buffer

Firmer Micro Foundations to Cdn Mortgage Markets, Despite Macro Parallels

• Explicit GSE guarantees

• Strongly capitalized banks & captive dealers, no shadow banking leverage

• Totally different funding model: deposit funding & large held-on-book

component, versus reliance upon revolving door financing

• Financial institutions less reliant upon short-term lines

• No strategic defaults, outside of Alberta & Saskatchewan

• Less outsourcing of sales force in Canada

• Generally more conservative products, but not entirely

• No option ARMs in Canada, but entire book resets within 5 years

• No mortgage interest deductibility (with exceptions)

• Stricter underwriting criteria including independent appraisals & hair-cuts

Contacts

Economics

Derek Holt, Vice-President [email protected]

Gorica Djeric, Financial Markets [email protected]

Disclaimer This report has been prepared by SCOTIA CAPITAL INC. (SCI), a subsidiary of the Bank of

Nova Scotia. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither SCI nor its affiliates accepts any liability whatsoever for any loss arising from any use of this report or its contents.